U.S. Department of Health and Human Services

U.S. Department of Health and Human Services

National Long-Term Care Insurance Claims Decision Study: An Empirical Analysis of the Appropriateness of Claims Adjudication Decisions and Payments

LifePlans, Inc.

April 2010

PDF Version: http://aspe.hhs.gov/daltcp/reports/2010/claims.pdf (20 PDF pages)

This report was prepared under contract #HHS-100-02-0014 between the U.S. Department of Health and Human Services (HHS), Office of Disability, Aging and Long-Term Care Policy (DALTCP) and LifePlans, Inc. For additional information, you can visit the DALTCP home page at http://aspe.hhs.gov/_/office_specific/daltcp.cfm or contact the ASPE Project Officers, Pamela Doty and Hunter McKay, at HHS/ASPE/DALTCP, Room 424E, H.H. Humphrey Building, 200 Independence Avenue, S.W., Washington, D.C. 20201. Their e-mail addresses are: Pamela.Doty@hhs.gov and Hunter.McKay@hhs.gov

The opinions and views expressed in this report are those of the authors. They do not necessarily reflect the views of the Department of Health and Human Services, the contractor or any other funding organization.

TABLE OF CONTENTS

- SAMPLING AND METHODOLOGY

- Weights and Sample Size

- ANALYSIS AND FINDINGS

- Policy Information

- Initial Decision Information

- Reviewer Determination

- Liability Estimations

- Payment Information

- LIST OF FIGURES

- FIGURE 1: Proportion of Case with Documentation Supporting the Initial Insurer Determination by Decision Status

- FIGURE 2: Distribution of Clinical Auditor and Insurance Company Adjudicator Benefit Eligibility Decisions

- FIGURE 3: Agreement between Insurance Company and Clinical Auditor Decisions

- FIGURE 4: Agreement between Insurance Company and Clinical Auditor Decisions by Insurer

- FIGURE 5: Potential Maximum Liability

- LIST OF TABLES

- TABLE 1: Policy Design Information

INTRODUCTION

Private long-term care insurance (LTCI) has been selling in the market for over two decades and a small but growing number of individuals -- roughly seven million -- have this coverage. An estimated 200,000 policyholders are currently claiming benefits (Mulvey, 2009). In the last ten years, both state government and Federal Government have been signaling their support for the development of a robust private LTCI industry through various means such as the partnership programs, the implementation of a federal LTCI program for federal employees and most recently, the Community Living Assistance Services and Support Act. The merits of private LTCI continue to be debated as critics warn that policies may be of little value because they will not cover enough of the costs of care when it is needed (Feder, 2009). Publicity in the New York Times and other newspapers and magazines has raised the issue of whether the LTCI industry is engaging in inappropriate denials of long-term care claims (New York Times, 2007a; New York Times, 2007b). While the focus of these articles was on a small number of individuals who had had extreme difficulties trying to obtain benefits from two major companies, the publicity increased focus on the practices of the entire industry. In fact, Congress held investigative hearings in 2008 on the issue of claims payment practices in the industry (U.S. Senate Special Committee on Aging, 2009). In addition, state insurance departments began conducting more company-specific audits, and there has been additional negative press related to the industry.

In the past, critics pointed to the complexity of the product and how it was marketed. As a result, the product evolved and changed over the years with a greater emphasis on both consumer value and protections. Moreover, the industry has engaged in much greater education of agents to assure that consumer-friendly marketing guidelines were adhered to. The focus of industry efforts was on the point of purchase. The New York Times article called in to question the legitimacy of private LTCI as a product in which consumers and the Federal Government can have confidence.

Clearly, the insurance is not only defined by the insurance contract and how it is structured, but also by how it is administered and serviced once someone files a claim under their policy. Recent criticism has shifted the focus from sales and marketing to the relationship between the insurer and the insured at the time of contract enforcement -- when the insured needs benefits. It was precisely this aspect that was being called into question.

PURPOSE

Much of the information behind the charges of critics is anecdotal and based on a relatively small number of individuals concentrated in two companies who may indeed have had legitimate grievances based on their personal experience. Yet, this information alone should not allow one to draw broad conclusions about private industry performance in general. Clearly, empirical data on an industry-wide basis is needed to definitively validate or dispense with these charges. The purpose of the current project is to conduct a thorough scientific review of an industry-wide sample of private LTCI claims decision made in 2007 and 2008 in order to determine and quantify the extent to which those decisions were appropriate. More specifically, we focused on answering two broad questions:

Is the denial of benefits to policyholders making claims on their policy appropriate? and;

Is the approval of benefits to policyholders making claims on their policy appropriate?

SAMPLING AND METHODOLOGY

We reviewed a sample of claims from seven of the largest LTCI carriers in the United States in order to determine if the decisions made for those claims are appropriate. The following carriers provided a sample of their claims decisions:

- Bankers Life and Casualty

- Genworth Financial

- John Hancock

- Long Term Care Partners

- Medamerica

- Metropolitan Life

- Prudential

These companies represent major carriers that are currently selling policies in the individual and group markets, with significant claims numbers for analysis. Together these companies comprise more than 70% of the in-force claims. We were not successful in our attempts to include those companies that are no longer selling LTCI, but have significant claims activity. These include the two who were cited in the New York Times article.1

The focus of the review is on the initial claim decision -- approval or denial -- of both individual and group claims filed in 2007 and 2008 on tax-qualified policies.2 All reviews were completed in 2008 and 2009. Initial discussions with the insurance carriers revealed the need for clear and uniform definitions regarding what is meant by an approved or denied claim. An approved claim is one in which the insurance company determines that the policyholder meets the functional and/or cognitive impairment triggers under their policy definitions, regardless of whether or not they received a payment for that claim. A denied claim is one in which the insurance company determines that the policyholder does not meet the functional and/or cognitive impairment triggers under the policy definitions. It is important to note that whenever the words approved and denied appear in this report they are defined as stated above.

Each company was given instructions for drawing the sample and the information needed in order to perform an audit of decisions chosen. A complete list of policy numbers that met our criteria was requested from each company and then LifePlans drew a random sample of approvals and a random sample of denials from that list, thereby ensuring a review of cases that were representative of a companys adjudication. In some cases, the entire population of denials was chosen.

In general, companies were asked to provide the entire claim file for a chosen case, including, but not limited to, claims forms, medical records, assessments, case notes, clinical notes, images and any other documents or information that was used to render a decision. A copy of the policy was also requested. Companies who could not provide copies of this information to the research (audit) team were given the option to have files reviewed onsite. In addition to this information, each company was asked to complete an administrative questionnaire, which details specific rules, definitions and criteria that adjudicators used when making decisions (for instance, the cut-off score used to determine cognitive impairment on a standardized test).3 Reviews were completed onsite for four of the participating companies and the other three sent copies of the requested materials to LifePlans.

Over the period of February 2008 to November 2009, companies provided the policy numbers for the following groups:

All those who submitted a claim in either 2007 or 2008 that was approved on or before August 1st of the corresponding year, and had received at least one claims payment in the six months following their approval.

All those who submitted a claim in either 2007 or 2008 that was approved on or before August 1st of the corresponding year, but did not receive a claims payment in the six months following their approval.

All those who submitted a claim in either 2007 or 2008 that was denied.

Once all of the requested documentation and information was provided, the files were reviewed by LifePlans clinical audit team. This team consisted of registered nurses who have over ten years of experience reviewing and adjudicating long-term care claims. The clinical audit team conducted reviews to determine whether the decision was supported by the facts in the file. A form was filled out detailing the reason for the insurance companys decision regarding denial or acceptance of the claim, and then it was re-adjudicated based on the information available in the file at the time of the review.

There were three possible outcomes of the in-depth review:

If the information in the file and contract language supported the decision, the denial or acceptance was be deemed as appropriate.

If there was a lack of relevant health care information in the file to make a determination, LifePlans noted this and the denial or acceptance was deemed unclear/unable to make determination.

If a decision was incorrect based on the application of the health care and provider information to the contract language of the policy, the denial or acceptance was deemed inappropriate.

Weights and Sample Size

While each company was evaluated separately, most of the results in this report are aggregated. To assure that the results can be generalized to the population of claims decisions across the industry, we weighted the data based on the market share of open claims for each of the participating companies. These market share numbers were obtained from the insurance companies by asking for the total number of open claims at the end of the calendar year.4 In this manner, we assure that we are not giving too much weight to companies with smaller market shares that contributed larger samples to the survey and alternatively, too little weight to companies with larger market shares, but smaller samples. All of the tables and charts that follow are based on analyses done with the weighted sample unless otherwise noted.

The total weighted sample is comprised of 863 initial approvals (70%) and 374 (30%) initial denials for a total of 1237 cases reviewed. It is important to note that the proportion of approved and denied cases drawn from each company does not represent rate at which these companies or the industry as a whole approves or denies claims. The sample was stratified so that we could ensure that enough initial denial decisions for review.

HIPAA AND CONFIDENTIALITY

Protecting policyholder privacy and confidentiality is part and parcel of the research teams approach. In order to participate in the study, each insurance company must have had a Business Associates Agreement in place with LifePlans. In addition, all physical and electronic data kept on site at LifePlans is secured appropriately. All reviewed cases were assigned a random identification number, which is the only identifying information used on the evaluation forms by the clinicians. The original list containing the linkage of policy number and random ID number was either destroyed or returned to the insurance company. Therefore, no permanent record exists at LifePlans of which cases were reviewed and which forms are associated with policy numbers.

ANALYSIS AND FINDINGS

Policy Information

Table 1 outlines the policy design information of the files we reviewed and shows results for all cases in the Total column, cases designated as approved by an insurance company in the Approved column and cases designated as denied in the Denied column. The table also indicates where differences were significant at the p=0.05 level.

The majority of claims were on individual policies, most of which were comprehensive with some level of inflation protection. From the table, we note that significantly more of the approved decisions had inflation protection, four year benefit periods and 100 day elimination periods.

Initial Decision Information

Clinical staff recorded pertinent information related to the initial insurance company decision, indicating whether the file was approved or denied and details about the functional and cognitive findings, as well as chronic illness/90 day expected loss certification. It is important to note that insureds filing a claim for benefits under a tax-qualified policy must meet the following criteria in order to be deemed eligible to receive benefits under their policy:

- They must require substantial assistance in at least two or three activities of daily living as defined by their policy; AND

- Dependency must be certified to exist for at least 90 days or more; OR

- They must require substantial assistance due to cognitive impairment as defined by their policy.

One of the reasons only tax-qualified policies were reviewed was because these standards are uniformly present across all HIPAA (tax-qualified) policies regardless of the insurance company. Grandfathered policies were not included in the sample unless this definition was used by the company when adjudicating claims on grandfathered policies.

| Policy Information | Total Claims | Approved Claims (A) | Denied Claims (B) |

|---|---|---|---|

| Contract Type | |||

| Group | 15% | 15% | 13% |

| Individual | 85% | 85% | 87% |

| Coverage Type | |||

| Comprehensive | 89% | 89% | 87% |

| Community-Based Care only | 4% | 4% | 6% |

| Facility-Based Care only | 7% | 7% | 7% |

| Benefit Period | |||

| 1 Year | 2% | 2% | 4%A |

| 2 Years | 14% | 14% | 13% |

| 3 Years | 23% | 21% | 28%A |

| 4 Years | 22% | 24%B | 18% |

| 5 Years | 8% | 8% | 8% |

| 6 Years | 7% | 8% | 6% |

| Lifetime | 17% | 17% | 16% |

| Other | 7% | 6% | 7% |

| EP/Deductible Period | |||

| 0 day | 2% | 2% | 4%A |

| 30 day | 10% | 10% | 12% |

| 60 day | 5% | 4% | 6% |

| 90 day | 20% | 19% | 21% |

| 100 day | 51% | 54%B | 44% |

| Other | 12% | 11% | 13% |

| Lifetime Maximum Benefit | |||

| Average | $194,247 | $201,648 | $177,120 |

| Minimum | $13,520 | $14,600 | $13,520 |

| Maximum | $1,296,000 | $1,138,800 | $1,296,000 |

| Sum | $228,722,475 | $165,798,982 | $62,923,493 |

| Inflation Protection | |||

| Yes | 61% | 65%B | 51% |

| No | 39% | 35% | 49%A |

The first step in the analysis was to review the documentation in the claims file to indicate which activities of daily living were noted as dependencies, record the cognitive screening score (if present), and to record evidence of an expected loss duration of 90 days or greater. This information was then compared to the contract language of the policy to determine if the insured met the functional or cognitive and 90 day chronic illness requirements as outlined by that policy. Also reviewed was documentation that summarized the insurance companys decision, which was often communicated in a letter to the insured. This was done in order to determine whether or not there was documentation present in the file that matched the insurance company adjudicators decision.

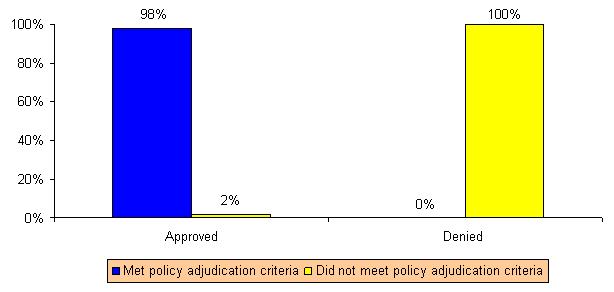

Figure 1 below shows that among those cases classified as approvals by the insurance company, almost all (98%) had documentation that supported the standard Tax-Qualified adjudication criteria; that is, we found documented evidence of functional and/or cognitive dependencies consistent with definitions in the policy contract language as well as the information on the expected loss duration. However, in 2% of approved cases, there was no documentation that indicated that the insured met the trigger as indicated by the insurance company adjudicator.

FIGURE 1: Proportion of Case with Document Supporting the Initial Insurer Determination by Decision Status

Regarding denial decisions, we found that in all cases, there was no evidence to suggest that the individual met the tax-qualified criteria for benefit eligibility in their policy. This would suggest that companies are consistently applying their clinical contract language to their claims decisions. There were very few cases where a claim was approved where the documentation was contrary to the clinical contract language. This can occur if a company makes a business decision to pay a claim, even in the absence of definitive clinical documentation.

Reviewer Determination

Study reviewers (clinical auditors) conducted a blind review of the insurance companys initial decision on a case. They applied their clinical skills to adjudicate the claim, independent of a companys decision. Based upon the documents and the policy definitions the clinical auditor determined whether or not the case should be approved or denied. There were three possible outcomes of the review:

- Claimant met policy definitions (approved)

- Claimant did not meet policy definitions (denied)

- Unclear

If the clinical reviewer was unable to render a decision based on the information in the file, (s)he was required to document the reasons why. The possible reasons included:

Not enough information in the file to make a decision: This response was used when the reviewer felt it necessary to obtain additional information, records, statements or documents before being in a position to make an accurate benefit eligibility decision. In such cases, there was no indication in the file that this information had been requested or received by the insurance company. Even so, the insurance company adjudicator made a decision based upon partial supporting documentation.

Conflicting information on file, further documentation needed to make a decision: This category was used when the reviewer found conflicting information in the file (such as two attending physician statements stating conflicting information) and they would have requested further clarification before making a decision.

Information was not obtained from the proper source: Companies are required to obtain chronic illness information from a licensed health care practitioner. If the information in the file was documented as having come from a source other than this, the reviewers would choose this category.

Reviewer could not find documents in hard copy or on file that were reviewed by the insurance company adjudicator: There were times when notes in the file or on a system would indicate that a document was requested and obtained and used in the decision making process by the insurance company adjudicator, but the reviewer was unable to find the document in the file.

Any unclear responses that could not be categorized into one of the four categories above were marked as other and described in detail by the reviewer in a notes section of the form.

As previously stated, the sample we obtained from the insurance companies was comprised of 70% initial approvals and 30% initial denials. If there was complete agreement between the clinical auditors and the insurance company adjudicators, we would expect to see the same distribution result from the clinical audit review. Figure 2 summarizes the distribution of auditor benefit eligibility decisions and shows the proportion of cases for which there was disagreement with the initial finding of the insurance company adjudicator. As shown, upon a blind review of cases, clinical auditors would have approved 65% of the cases for benefits, denied 30% and would have required additional or clarifying information in 5% of the cases. Put another way, the clinical auditors would have approved 5% fewer cases than the insurance company adjudicators, denied the same proportion of claims, and in 5% of the cases, were unable to render a benefit eligibility decisions.

FIGURE 2: Distribution of Clinical Auditor and Insurance Company Adjudicator Benefit Eligibility Decisions

NOTE: These proportions are not representative of the approval and denial rates of the insurance companies.

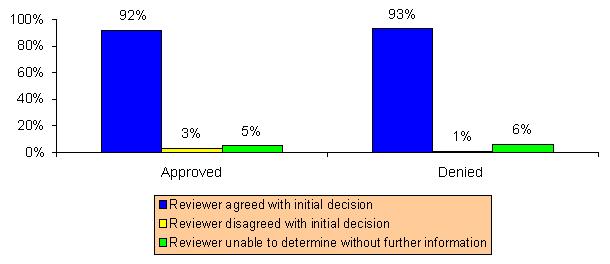

Figure 3 highlights the fact that the LifePlans clinical auditors agreed with the decision in the majority (92%) of cases that were approved for claims payment. There was disagreement in 3% of the cases that were approved, meaning that clinical auditors disagreed with the insurance company determination that the individual was at a level of disability consistent with the clinical eligibility trigger spelled out in the policy.

FIGURE 3: Agreement between Insurance Company and Clinical Auditor Decisions

The clinical audit team was unable to make a determination for 5% of the cases that were initially approved by the insurance company. In a little more than half of these cases, the reviewers felt that there was not enough information obtained by the insurance company to make a definitive claims decision. Other reasons why a decision could not be made included: (a) there was conflicting documentation in the file; (b) the information was not obtained from a licensed health care practitioner or valid source in another, and; (c) the auditors were unable to find the documentation that was referenced by the insurance company adjudicator to make the decision.

The results for denial decisions were similar. There was disagreement with the initial denial decision in only 1% of the cases. In other words, only 1% of the cases initially denied by the insurance company would have been approved by the clinical auditors. The clinical auditors were unable to make a decision in 6% of the initially denied cases. Again, the primary reason for the inability to make a determination resulted from inadequate information in the file. Other reasons included conflicting information and the auditors were unable to find the documentation that was referenced by the insurance company adjudicator to make the decision.

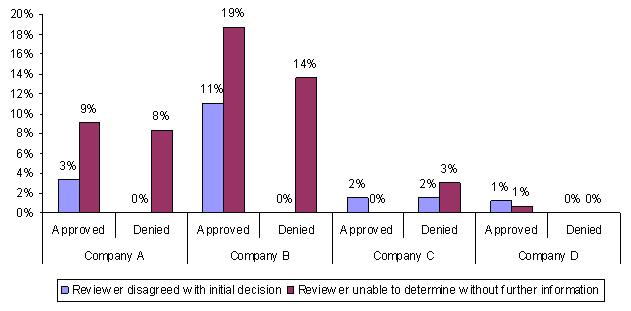

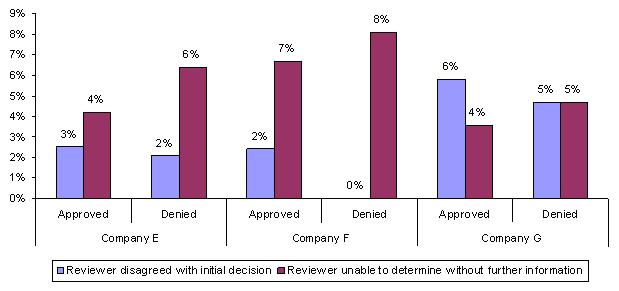

The following figure highlights the degree of variation found across the industry.

Being unable to make a determination does not necessarily mean that the decision was incorrect. It is quite possible that the initial decision of the insurance company was appropriate, but the clinical auditors judged that given the nature of the information present in the file, they were unable to make a decision.

These findings presented here suggest that there is a low incidence of disagreement between the clinical audit team and the insurance company adjudicators, particularly when it comes to denied claims. These results do suggest that in some cases companies are making decisions in the absence of information that the clinical auditors felt was necessary to make that decision. There is a greater probability of approving rather than denying a questionable claim.

Liability Estimations

Because we collected information regarding policy design parameters, we were able to estimate the maximum potential claim liability associated with a companys claims decisions. Using the lifetime maximum dollar value of a policy (as provided by the companys system or calculated using the policy benefit amount and benefit period), we estimated the total potential liability (for the lifetime of the policy) associated with all claims. In this way, we are able to associate a specific dollar liability with each claim decision and measure the impact of differences in decision making on total liabilities.

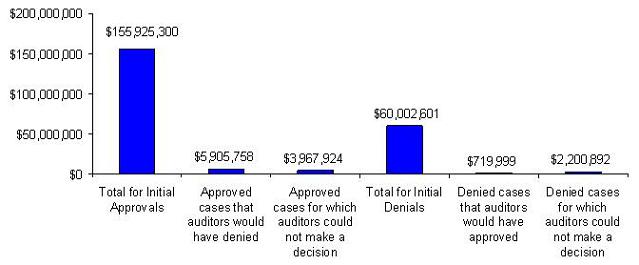

Figure 5 below shows the total potential claim liability for the sample of cases reviewed by the clinical audit team.5

FIGURE 5: Potential Maximum Liability

Figure 5 shows that the total potential maximum liability for all initially approved decisions by the insurance company (1237 cases) is about $156 million. Of that total, roughly 4% ($6 million) of the potential maximum liability associated with the approvals would have been denied based upon the clinical audit team reviews. The cases for which the clinical audit team was unable to make a definitive determination, represents about 2% or roughly $4 million of the potential maximum liability associated with the initial approval decision.

Figure 5 also shows that the total potential maximum liability of the claims that were initially denied by the insurance company, but deemed approvals by the clinical audit team totaled roughly $700,000 or about 1% of the total potential liability of all denied claims. The maximum potential liability associated with initial insurance company denials for which the audit team was unable to make a decision, totaled about $2 million or about 3%.

Payment Information

We also gathered payment information to determine if there were any inappropriate payment denials or delays. Our research indicates that there were no inappropriate payment denials or delays for approved claims and no payments made to denied claims. Said another way, the review indicated that everyone who was eligible to receive a payment for benefits under their policy, in fact received it, and those who the insurance company determined did not meet their policy triggers did not receive payments.

We also collected information related to reasons there may have been a lag between notification of benefit eligibility to the insured and the date that the first payment was made. There are many reasons that a payment might be denied or delayed after an insured is approved for benefits based upon the clinical criteria of their policy. These reasons include provider ineligibility, elimination period not met, coordination of benefits (other payment source), and lack of documentation about service costs or bills. The clinical audit team found that 19% of the sample had not met their elimination period within six months of notification of clinical benefit eligibility, while another 14% had not submitted bills within that same timeframe. Although Table 1 indicates that the most common elimination periods for this sample were 90 and 100 days, some elimination periods are measured on a per visit basis (as opposed to a calendar day basis). This means that if an insured uses home care and receives 1 or 2 visits a week; it may take longer to reach the elimination period.

CONCLUSION

The detailed review of more than 1200 claims decisions suggests that when a third party independent audit is conducted, clinical benefit eligibility decisions are in line with the supporting documentation in the files and the contract provisions of the policy. The data suggests that when disagreements were present between the audit team and the insurance company adjudicators, they were more likely to be about approval decisions rather than denial decisions. Put another way, insurance companies tend to err slightly on the side of approving claims that may not meet policy contract benefit eligibility criteria. Moreover, there was no evidence of inappropriate payments being made to individuals approved for claim and those denied.

REFERENCES

Duhigg, C. (2007a). Aged Frail and Denied Care by Their Insurers. New York Times. Retrieved December 4, 2009 from http://www.nytimes.com/2007/03/26/business/26care.html.

Duhigg, C. (2007b). Scrutiny for insurers of the aged. New York Times. Retrieved December 4, 2009 from http://www.nytimes.com/2007/10/03/business/03care.html?scp=3&sq=long-ter....

Feder, Judith (Georgetown University Professor and former Clinton Administration official). Quote: The benefits tend to be limited and fixed in dollar amount. So even if you buy ahead of time, it still leaves you exposed to substantial costs. In Andrews, M. (2009, March 11). Four ways to cover the cost of long-term care. U.S. News and World Report. Retrieved on December 4, 2009 from http://health.usnews.com/articles/health/best-nursing-homes/2009/03/11/4....

Mulvey, L. (2009). Factors affecting the demand for long-term care insurance: Issues for Congress. Washington, DC: Congressional Research Service. Retrieved December 4, 2009 from http://assets.opencrs.com/rpts/R40601_20090527.pdf.

U.S. Senate Special Committee on Aging. (2009). Hearing: Boon or Bane? Examining the Value of Private Long-Term Care Insurance. Testimony retrieved December 4, 2009 from http://aging.senate.gov/hearing_detail.cfm?id=313934&.

NOTES

A number of additional companies were approached to participate in the study for which we were not able to obtain their participation due to various reasons. It is worth noting that the two companies identified in the New York Times article were willing to participate, but because of sampling errors that were unable to be corrected and state regulatory decisions that participation would detract from the day-to-day operation of the company, we were unable to use them in the final analysis.

The sample was limited to a review of tax-qualified policies due to the standard language and criteria used when adjudicating these types of policies -- criteria are more uniform and verifiable. Medical necessity policies require a doctors (or similar) verification.

Companies were instructed to be sure to provide answers detailing the administrative procedures that were in-force during the time of the decisions being reviewed. For instance, although the data was requested in 2008, if claims decisions under review were made in 2007, then the company was instructed to detail their adjudication procedure from that time period.

Open claims data was gathered for each company as of December 31 of 2007, 2008 and 2009. The ratio of companies to each other did not change in any year; therefore the decision was made to calculate the weights based upon 2009 data.

It is important to note the following: for policies with lifetime benefits, a period of ten years was used when calculating total policy value and liability estimations are based upon the lifetime value of the policy at the time of purchase. The values and estimations do not take in to account inflation. Also, the estimates represent the maximum value of the policy, even though it is unlikely that every one of these claimants will max out their benefit dollars.

LONG-TERM CARE INSURANCE CLAIMANTS "ADMISSIONS COHORT" STUDY: DATA COLLECTION AND ANALYSIS PHASE REPORTS AVAILABLE

- Following an Admissions Cohort: Care Management, Claim Experience and Transitions among an Admissions Cohort of Privately Insured Disabled Elders over a 16 Month Period

- Executive Summary: http://aspe.hhs.gov/daltcp/reports/2007/16moclmes.htm

- Full HTML Version: http://aspe.hhs.gov/daltcp/reports/2007/16moclm.htm

- Full PDF Version: http://aspe.hhs.gov/daltcp/reports/2007/16moclm.pdf

- National Long-Term Care Insurance Claims Decision Study: An Empirical Analysis of the Appropriateness of Claims Adjudication Decisions and Payments

- Full HTML Version: http://aspe.hhs.gov/daltcp/reports/2010/claims.htm

- Full PDF Version: http://aspe.hhs.gov/daltcp/reports/2010/claims.pdf

- Private Long-Term Care Insurance: Following an Admission Cohort over 28 Months to Track Claim Experience, Service Use and Transitions

- Executive Summary: http://aspe.hhs.gov/daltcp/reports/2008/coht28moes.htm

- Full HTML Version: http://aspe.hhs.gov/daltcp/reports/2008/coht28mo.htm

- Full PDF Version: http://aspe.hhs.gov/daltcp/reports/2008/coht28mo.pdf

- Service Use and Transitions: Decisions, Choices and Care Management among an Admissions Cohort of Privately Insured Disabled Elders

- Executive Summary: http://aspe.hhs.gov/daltcp/reports/2006/admcohortes.htm

- Full HTML Version: http://aspe.hhs.gov/daltcp/reports/2006/admcohort.htm

- Full PDF Version: http://aspe.hhs.gov/daltcp/reports/2006/admcohort.pdf

To obtain a printed copy of this report, send the full report title and your mailing information to:

U.S. Department of Health and Human ServicesOffice of Disability, Aging and Long-Term Care PolicyRoom 424E, H.H. Humphrey Building200 Independence Avenue, S.W.Washington, D.C. 20201FAX: 202-401-7733Email: webmaster.DALTCP@hhs.gov

RETURN TO:

Office of Disability, Aging and Long-Term Care Policy (DALTCP) Home [http://aspe.hhs.gov/_/office_specific/daltcp.cfm]Assistant Secretary for Planning and Evaluation (ASPE) Home [http://aspe.hhs.gov]U.S. Department of Health and Human Services Home [http://www.hhs.gov]