The Risk and Costs of Severe Cognitive Impairment at Older Ages: Key Findings from our Literature Review and Projection Analyses

ASPE RESEARCH BRIEF

Melissa Favreault and Richard W. Johnson

Urban Institute

January 2021

Link to Printer Friendly Version in PDF Format (18 PDF pages)

ABSTRACT: Projections of future care needs and costs are difficult because the older population is changing in ways that will likely shape the course of cognitive impairment. This study uses the Dynamic Simulation of Income Model (DYNASIM) to project the risk and costs of severe cognitive impairment at older ages over the coming decades. We project large differences in the chances of ever experiencing severe cognitive impairment for different groups, for example, African Americans, Hispanics, and women. Our estimates of the prevalence and duration of severe cognitive impairment fall within the bounds of prior literature. Lastly, those lower in the income distribution can expect to use most or all of their wealth on care should they become impaired.

The authors gratefully to the Office of the Assistant Secretary for Planning and Evaluation (ASPE) and to all our funders, who make it possible for Urban to advance its mission. Brenda Spillman of Urban's Health Policy Center and Judith Dey, Helen Lamont, and William Marton of ASPE provided helpful comments on earlier drafts.

This brief was prepared under contract #HHSP233201600024I between HHS's ASPE/BHDAP and the Urban Institute. For additional information about this subject, you can visit the BHDAP home page at https://aspe.hhs.gov/bhdap or contact the ASPE Project Officers, at HHS/ASPE/BHDAP, Room 424E, H.H. Humphrey Building, 200 Independence Avenue, S.W., Washington, D.C., 20201; Judith.Dey@hhs.gov, Lauren.Anderson@hhs.gov, Helen.Lamont@hhs.gov.

DISCLAIMER: The opinions and views expressed in this report are those of the authors. They do not reflect the views of the Department of Health and Human Services, the contractor or any other funding organization. This report was completed and submitted on July 2020.

| The possibility of becoming severely cognitively impaired is among the most consequential risks facing older adults and their families. In addition to the emotional and physical toll associated with dementia, the financial consequences can be overwhelming, as many patients require expensive paid care. Projections of future care needs and costs are difficult because the older population is changing in ways that will likely shape the course of cognitive impairment. This brief summarizes key findings from our recent report (Favreault and Johnson 2020) on the risks and costs of severe cognitive impairment (SCI). We project that 31% of older adults born from 1955-1959 in the United States and who survive to 65 will become cognitively impaired. We project large differences in the chances of ever experiencing SCI for different groups. Those with less than a high school education, for example, are about three-fifths to three-quarters more likely to ever become severely cognitively impaired in late life than their counterparts with even a high school diploma, despite not living as long. African Americans and Hispanics are also more likely to become impaired than non-Hispanic Whites. Women are more likely to become impaired than men, in large part due to their longer life expectancy. We project that a typical spell of SCI lasts about 3-5 years. The cost and care burdens can be quite significant for families of those who become impaired. Average paid cost burdens for those ever impaired are over $280,000 (nearly $164,000 in present value terms), including nearly $158,000 in out-of-pocket costs ($89,000 in present value terms); the value of unpaid care that families and friends provide is similar. |

Introduction

The possibility of developing cognitive impairment is among the most consequential risks older adults and their families face. In addition to the emotional and physical toll associated with dementia, the financial consequences can be overwhelming. As cognitive functioning declines, help with personal care and everyday activities often becomes necessary. Assistance is usually provided by unpaid family members and friends (Kasper et al. 2015; Rainville, Skufca and Mehegan 2016; Reckrey et al. 2020; Wolff et al. 2016), which can have financial, health and emotional consequences. Paid help, often provided in nursing homes and other residential settings or in the home as a supplement to family care, frequently becomes necessary when patients' limitations become more extensive or they need round-the-clock care. Most care costs are initially paid out-of-pocket, which can create substantial financial burdens. Private insurance for long-term services and supports (LTSS), which might help alleviate this burden, is not affordable for many mid-life and older adults, as many carriers exit the market and those remaining increase premiums (Cohen 2016; Schmitz and Giese 2019; Ujvari 2018). Patients with severe cognitive impairment (SCI) may exhaust their financial resources and qualify for Medicaid. As the population ages in coming decades, Medicaid spending on older adults with SCI could surge, posing significant financial risks to federal and state governments (Congressional Budget Office 2013).

A growing literature examines the incidence, costs, and correlates of SCI at older ages. However, relatively little is known about how SCI risks and costs will likely evolve over the coming decades. Projections of future care needs and costs are difficult because the older population is changing in ways that could alter the course of cognitive impairment. For example, the older population is becoming better educated and more racially and ethnically diverse. At the same time, some health risks--like obesity and diabetes--have grown among older adults and could affect the future trajectory of cognitive impairment. Care delivery options are changing, as residential care and care at home are slowly replacing nursing home care. While long-term productivity growth is raising incomes, these gains have not been shared evenly across the population, and long-term income growth limits the share of the population that can qualify for Medicaid.

This study uses the Dynamic Simulation of Income Model (DYNASIM), the Urban Institute's dynamic microsimulation model, to project the risk and costs of moderate and SCI among older adults over the coming decades. Using multiple data sources, DYNASIM simulates the future population and its characteristics, projecting financial resources, disability status, medical conditions, cognitive status, and use of LTSS (Favreault and Johnson 2020). Unlike some past research, this study shows how SCI and associated costs vary across the population, with a focus on differences by socioeconomic status. We show how projected experiences with cognitive impairment vary across birth cohorts and compare outcomes by gender, education, race/ethnicity, and income within each cohort.

Key Definitions

Box 1 presents concise definitions of key terms surrounding cognitive impairment. We draw the definitions from various sources (Alzheimer's Association 2016, table 1; Centers for Disease Control and Prevention 2011; Hugo and Ganguli 2014; National Academies of Sciences 2017). Throughout this brief, we focus on severe cases of cognitive impairment; we do not differentiate between different types of dementia (such as Alzheimer's disease, vascular dementia, Lewy body dementia, or mixed dementia).

| BOX 1: Selected Terms Related to Cognitive Impairment |

|---|

|

| SOURCE: Definitions derived and adapted from Alzheimer's Association (2016), Centers for Disease Control and Prevention (2011), Hugo and Ganguli (2014), and National Academy of Sciences (2017). Other terms for specific types of dementia--like vascular dementia, frontotemporal dementia, or dementia with Lewy Bodies--are described in some of these sources. |

Findings

Prevalence of Dementia Increases Steadily with Age

The prevalence of SCI climbs rapidly with age, from around 2% at ages 65-69 to between one-third to one-half of people at ages 90 and older.

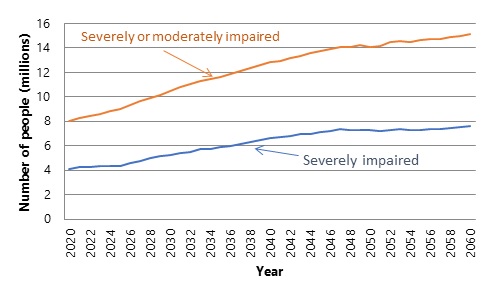

As Baby Boomers Age and Life Expectancy Increases, the Number of People with Dementia or CIND will Grow if Rates Hold Steady or Even if Rates Decline

Figure 1 shows the DYNASIM projections over a long time horizon--2020-2060. The numbers of people with cognitive impairment increase steadily as the population ages, especially as the large post-war baby boom cohorts reach ages at which age-specific SCI rates are highest. Moreover, the number impaired increases as exposure to the risk of cognitive impairment rises with increased life expectancy.

Importantly, Figure 1 underscores that the number of people living with moderate cognitive impairment will also grow markedly in coming decades--from about 3.5 million people living with moderate cognitive impairment in recent years to over 7.5 million in 2060.

Risk of Dementia Differs by Gender, Education, and Race/Ethnicity

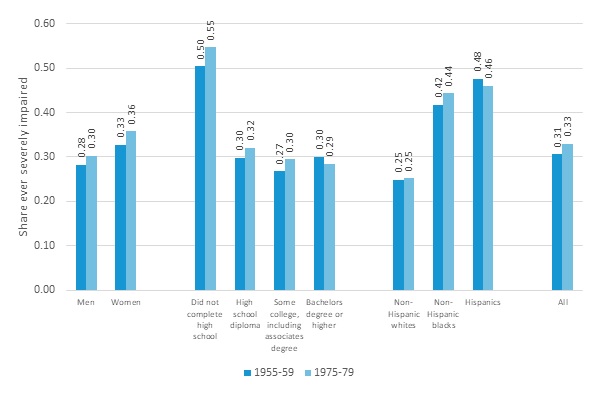

DYNASIM projects that about 31% of people born from 1955 to 1959 who survive to age 65 will eventually become severely cognitively impaired.[1] The model projects this will increase modestly, to roughly a third for those born from 1975 to 1979. This modest increase is driven by the expected increase in life expectancy across the birth cohorts, not by an increase in expected age-specific disease levels.

| FIGURE 1. DYNASIM Projections of Number of CI Adults in the United States Using Different Measures of Severity of CI at Older Ages, 2010-2060 |

|---|

|

| SOURCES: Authors' calculations from DYNASIM (run 974). |

Women are more likely than men to ever become severely impaired, and for both men and women there is a modest increase in the share ever impaired from the earlier cohorts to the later ones. Those without a high school diploma are significantly more likely to be impaired than those who graduated from high school. There is less difference in the prevalence of ever experiencing SCI for those who have at least a high school diploma. (Figure 2). DYNASIM projects that non-Hispanic Blacks and Hispanics are much more likely to ever become severely cognitively impaired than non-Hispanic Whites; in the 1975-1979 birth cohort, about two-fifths of non-Hispanic Blacks and Hispanics are projected to become impaired, compared with less than a quarter of non-Hispanic Whites.[2]

| FIGURE 2. DYNASIM Projections of the Share of Older Adults in the United States Who Survive to Age 65 Who Become CI by Birth Cohort and Gender, Education, and Race-Ethnicity |

|---|

|

| SOURCE: Authors' calculations from DYNASIM (run 974). |

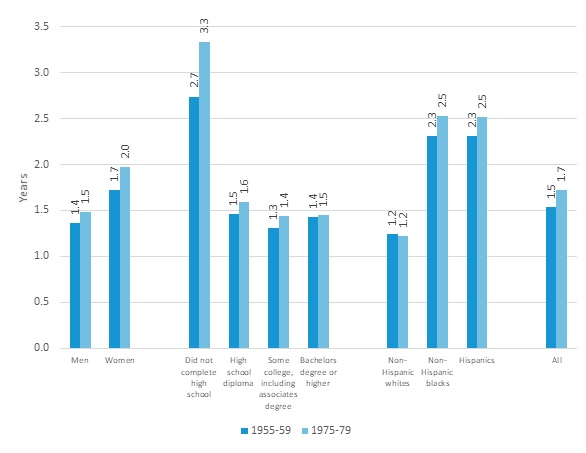

| FIGURE 3. DYNASIM Projections of the Expected Time CI for Older Adults who Survive to Age 65 by Birth Cohort and Gender, Education, and Race-Ethnicity |

|---|

|

| SOURCE: Authors' calculations from DYNASIM (run 974). |

These projected differences in the chances of ever becoming severely impaired are reflected in the projections of unconditional remaining life expectancy with SCI at age 65 (Figure 3). Within the entire older population, people can expect to live about 1.5 years with SCI in the oldest cohorts and about 1.7 years in the youngest.[3] Women in the oldest cohorts reaching age 65 over the next few years can expect to live 1.7 years with SCI, compared with 1.4 years for men. In the youngest cohorts, the corresponding projections are 2.0 and 1.5 years, respectively. Differences by education are again stark, with those in the oldest cohort who lack a high school diploma expected to live about 2.7 years with SCI, compared with 1.5 years for those with only a high school diploma who never attended college. Racial and ethnic differences in expected life with SCI from age 65 onward are also very large, about 2.5 years of remaining life expectancy impaired for non-Hispanic Blacks and Hispanics in the later cohorts, compared to closer to 1.2 years among non-Hispanic Whites.

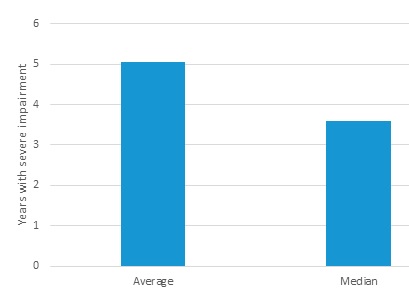

Figure 4 reports the mean and median conditional remaining life expectancy impaired, which is the amount of time that those who are impaired can expect to live with cognitive impairment. The mean duration is about seven years, but the median is closer to four and a half years. The difference between the mean and median values reflects the skewness of the distribution, with a relatively small number of older adults experiencing very long dementia spells.[4]

| FIGURE 4. Average and Median Projected Years with SCI from Age 65, for Those Who Become Severely Impaired, People Born 1955-1959 (%) |

|---|

|

| SOURCE: Authors' tabulations from DYNASIM (runid 974). |

Costs for Paid Services Can be Devastating for Families

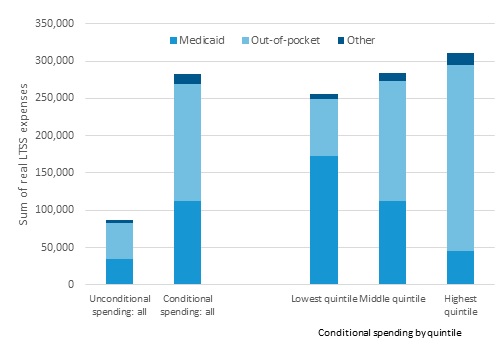

Figure 5 presents our projections of the paid LTSS costs that those with dementia incur and describes who pays these costs, focusing on those now entering retirement. It expresses costs as a sum of inflation-adjusted costs incurred from age 65 through death. (We additionally report present values, which reflect the amount a person would need to set aside at age 65 to pay for those expenses after accounting for the interest they accrue, assuming a real interest rate of 2.5%). It presents both the unconditional costs for all those who survive until age 65 and the conditional costs for those who survive until age 65 and become severely cognitively impaired at some subsequent age. Average paid LTSS costs are about $86,000 (or $50,000 in present value terms). Conditional on having dementia, the paid costs more than triple--to over a quarter million dollars, about $282,000 (or 163,500 in present value terms). Families' additional out-of-pocket expenses average $157,500 ($89,400 in present value terms)--less for those in lower-income quintiles, where people with SCI are more likely to qualify for Medicaid, and more in higher-income quintiles.

| FIGURE 5. Average Projected Cost of SCI from Age 65 Onward for Paid LTSS: DYNASIM 1955-1959 Birth Cohorts, by Lifetime Earnings Quintile |

|---|

|

| SOURCE: Author's tabulations from DYNASIM4 (runid 974, dated: October 2019). NOTES: Projected costs are reported in 2020 inflation-adjusted dollars. Estimates in the bar to the left include people who never experienced SCI; all other bars include only those who experienced severe SCI. We include assisted living and attempt to include care costs that families incur in private transactions (see Newquist, DeLiema and Wilber [2015] or Seavey and Marquand [2011] for discussion). |

People with Dementia Rely Heavily on their Families and Friends

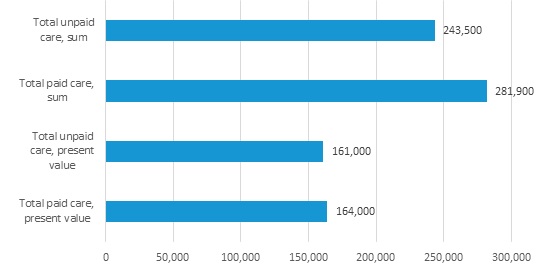

Consistent with prior literature, we find that informal care from families and friends plays a critical role for people with dementia--comparable in scope to formal care. Conditional on having dementia, the value of informal care that care partners provide--close to $243,5000 ($161,000 in present value terms)--just exceeds the formal costs--$281,000 ($164,000 in present value terms).

| FIGURE 6. Average Projected Value of Care for People with SCI from Age 65 Onward Compared to Cost of Paid LTSS: DYNASIM 1955-1959 Birth Cohorts, by Lifetime Earnings Quintile |

|---|

|

| SOURCE: Author's tabulations from DYNASIM4 (runid 974). NOTES: Projected present value costs are discounted to age 65 using a 2.5% real interest rate. Both sums and present values are reported in 2020 inflation-adjusted dollars. Estimates include only people who experienced SCI. The amount of unpaid family care is computed based on the residual between LTSS need and paid care received and historical data on average hours of unpaid care received by people with dementia residing in the community. Unpaid care is valued at the median home care wage in the recipient's state of residence, based on 2019 estimates from Genworth (2019), wage-indexed to the year in which care is provided. |

Placing our estimates in the context of the prior literature, those who compare formal care and informal care often find a roughly equal split (Hurd et al. 2013)--consistent with our findings.[5] Our unpaid family care estimate is comparable to Jutkowitz et al. (2017)'s base case estimate, which values lifetime family care at about $155,000 when expressed in current dollars and present value terms.

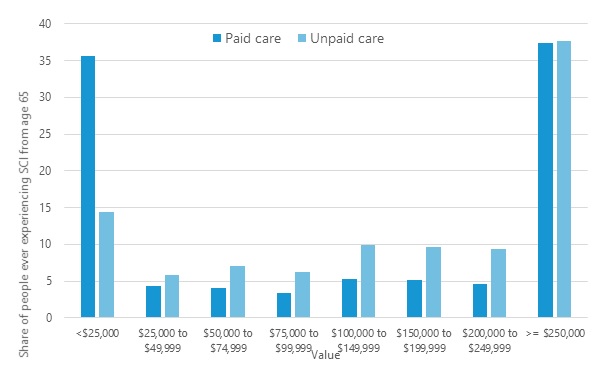

Because extreme values can distort averages, it is helpful to examine full distributions. Figure 7 shows the cost distribution for paid services and the distribution of the value of unpaid family care, expressed as simple sums of real costs, for those with SCI in the 1955-1959 birth cohorts. We see that there is a significant right tail for both formal costs and the value of unpaid care. Over one in three (37.5%) of those ever experiencing SCI will incur paid costs of more than $250,000 in real terms. When we consider the value of family care, nearly the same share--roughly 37.6%--will need the equivalent of at least $250,000 in care when valued at replacement cost.

| FIGURE 7. Distribution of Projected Costs of Paid LTSS and Value of Unpaid Care for Those Who Ever Experience SCI: DYNASIM 1955-1959 Birth Cohorts |

|---|

|

| SOURCE: Author's tabulations from DYNASIM4 (runid 974). NOTES: Projected costs are discounted to age 65 using a 2.5% real interest rate and reported in 2020 inflation-adjusted dollars. Estimates are restricted to those who experienced SCI at ages 65 and older. The amount of unpaid family care is computed based on the residual between LTSS need and paid care received and historical data on average hours of unpaid care received by people with dementia residing in the community. Unpaid care is valued at the median home care wage in the recipient's state of residence, based on 2019 estimates from Genworth (2019), wage-indexed to the year in which care is provided. |

A Spell with Dementia Could Exhaust Many Families' Wealth

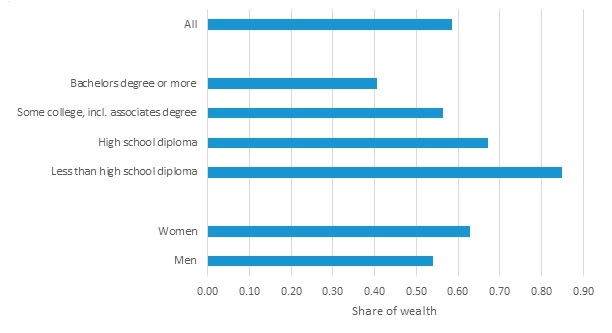

Following Kelley et al. (2015), we provide context about the affordability of the out-of-pocket costs for LTSS in Figure 8. It compares the lifetime out-of-pocket burdens for LTSS with late-life wealth, using wealth five years prior to death, which is typically around the beginning of the dementia spell. We define wealth to include both financial assets and retirement accounts.

For those reaching 65 from 2020 through 2024, the unconditional costs of out-of-pocket costs due to cognitive impairment represent about half of total wealth. Conditional on experiencing cognitive impairment, costs represent nearly three-fifths of total wealth 5 years prior to death in the earlier cohorts and close to half later.

| FIGURE 8. Projected Out-of-Pocket LTSS Spending from Age 65 while SCI as a Percentage of Financial Wealth 5 Years Before Death: DYNASIM 1955-1959 Birth Cohorts, by Gender and Education |

|---|

|

| SOURCE: Author's tabulations from DYNASIM4 (runid 974). NOTES: Projected costs are discounted to age 65 using a 2.5% real interest rate and reported in 2019 inflation-adjusted dollars. Costs as share of wealth are capped at 100% and set at that level for people who report no wealth. Conditional estimates are restricted to those who experienced SCI at ages 65 and older, and unconditional estimates include the entire population, including those who never experience SCI. |

Different groups face very different burdens: those with less education and lower incomes, for example, can expect to spend nearly all their wealth on out-of-pocket costs associated with dementia. They are also more likely to face a financial risk that exceeds their total wealth. Those with less education who need LTSS are thus most likely to rely on a public safety net program, Medicaid. This projection underscores the point that those most likely to experience dementia are those with the lowest ability to finance it.

Conclusion and Policy Implications

As our population ages, families and governments can expect to face increased demands for services from older adults with SCI. Although recent trends suggest that the age-specific prevalence of SCI may be declining modestly (Freedman et al. 2018; Hudomiet, Hurd and Rohwedder 2018; Langa et al. 2008; Langa et al. 2016; Li et al. 2017; Rocca et al. 2011; Stallard and Yashin 2016; Wu et al. 2017), increases in the number of older adults at the oldest ages, when cognitive impairment risks are especially high, are likely to raise the number of people with SCI who need care. Simply because the population is aging, with the large baby boom cohorts now in their late 50s through early 70s moving into their 80s and 90s over the next three decades, policymakers should prepare for a surge in the number of people with significant, often hard-to-serve LTSS needs. Our best projection is that between 2020 and 2060 the population ages 65 and older with SCI will roughly double, from about 3.5 million adults to 7.5 million. Including people with MCI, DYNASIM projects an increase from over 8 million to 15 million older adults with at least moderate impairments from 2020 to 2060.

On an individual level, the risk of becoming severely cognitively impaired at older ages is significant. Estimates from the literature vary. Our best estimate is that about three in ten of today's working-age adults who survive to age 65 will become severely cognitively impaired before they die, and half of those who do become impaired will need care for more than four years. In future cohorts, this could reach one-third ever impaired. Those with extended spells will face heavy care burdens. People who develop dementia at early ages are especially vulnerable.

Importantly for public policy, those who are most likely to become impaired and who experience the longest impairment spells tend to have limited education and thus low lifetime earnings. African Americans and Hispanics are also at especially high risk, and they also have relatively low lifetime earnings (Favreault 2018). The higher risk among those with the lowest lifetime earnings is likely to limit the ability of prefunding and private market solutions to address the country's LTSS financing challenges. Public solutions, whether through changes to Medicaid or broader social insurance will continue to be examined by policymakers. At the same time, states are beginning to move forward with new programs and reforms. Innovative state initiatives, including the enactment of legislation in Washington State to create a new public insurance program for a long-term care benefit and new public caregiver support in Hawaii, are two examples.

References

Alzheimer's Association. 2016. 2016 Alzheimer's Disease Facts and Figures. Chicago, IL: Author.

Centers for Disease Control and Prevention. 2011. Cognitive Impairment: A Call for Action Now! https://www.cdc.gov/aging/pdf/cognitive_impairment/cogimp_poilicy_final.pdf.

Chêne, G., A. Beiser, R. Au, S.R. Preis, P.A. Wolf, C. Dufouil, and S. Seshadri. 2015. "Gender and Incidence of Dementia in the Framingham Heart Study from Mid-Adult Life." Alzheimers & Dementia, 11(3): 310-320, doi:10.1016/j.jalz.2013.10.005.

Cohen, Marc A. 2016. "The State of the Long-Term Care Insurance Market." In E.C. Nordman, ed., The State of Long-Term Care Insurance: The Market, Challenges, and Future Innovations. Washington, DC: National Association of Insurance Commissioners and the Center for Insurance Policy and Research.

Congressional Budget Office. 2013. Rising Demand for Long-Term Services and Supports for Elderly People. Washington, DC: U.S. Congress. http://www.cbo.gov/sites/default/files/44363-LTC.pdf.

Favreault, Melissa M. 2018. How Might Earnings Patterns and Interactions among Certain Provisions in OASDI Solvency Packages Affect Financing and Distributional Goals? Working Paper 2018-2. Chestnut Hill, MA: Center for Retirement Research at Boston College. http://crr.bc.edu/wp-content/uploads/2018/03/wp_2018-2-1.pdf.

Favreault, Melissa, and Richard Johnson. 2020. The Risk and Costs of Severe Cognitive Impairment at Older Ages: Literature Review and Projection Analyses. Washington, DC: U.S. Department of Health and Human Services, Office of the Assistant Secretary for Planning and Evaluation. https://aspe.hhs.gov/basic-report/risk-and-costs-severe-cognitive-impairment-older-ages-literature-review-and-projection-analyses

Freedman, Vicki A., Judith D. Kasper, Brenda C. Spillman, and Brenda L. Plassman. 2018. "Short-Term Changes in the Prevalence of Probable Dementia: An Analysis of the 2011-2015 National Health and Aging Trends Study." Journals of Gerontology: Series B, 73(S1): S48-S56, doi:10.1093/geronb/gbx144.

Genworth. 2019. Cost of Care Survey, 2019: Median Cost Data Tables.

Helzner, E.P., D.N. Scarmeas, S. Cosentino, M.X. Tang, N. Schupf, and Y. Stern. 2008. "Survival in Alzheimer Disease: A Multiethnic, Population-based Study of Incident Cases." Neurology, 71: 1489-1495.

Hudomiet, Péter, Michael D. Hurd, and Susann Rohwedder. 2018. "Dementia Prevalence in the United States in 2000 and 2012: Estimates Based on a Nationally Representative Study." Journals of Gerontology: Social Sciences, 73(S1): S10-S19, doi:10.1093/geronb/gbx169.

Hugo, Julie, and Mary Ganguli. 2014. "Dementia and Cognitive Impairment: Epidemiology, Diagnosis, and Treatment." Clinics in Geriatric Medicine, 30(3): 421-442. doi:10.1016/j.cger.2014.04.001.

Hurd, M.D., P. Martorell, A. Delavande, K.J. Mullen, and K.M. Langa. 2013. "Monetary Costs of Dementia in the United States." New England Journal of Medicine, 368: 1326-34.

Jutkowitz, Eric, Robert L. Kane, Joseph E. Gaugler, Richard F. MacLehose, Bryan Dowd, and Karen M. Kuntz. 2017. "Societal and Family Lifetime Cost of Dementia: Implications for Policy." Journal of the American Geriatric Society, 65(10): 2169-2175, doi:10.1111/jgs.15043.

Kasper, Judith D., Vicki A. Freedman, Brenda C. Spillman, and Jennifer L. Wolff. 2015. "The Disproportionate Impact of Dementia on Family and Unpaid Caregiving to Older Adults." Health Affairs, 34(10): 1642-1649.

Kelley, Amy S., Kathleen McGarry, Rebecca Gorges, and Jonathan S. Skinner. 2015. "The Burden of Health Care Costs for Patients with Dementia in the Last 5 Years of Life." Annals of Internal Medicine, 163(10): 729-736, doi:10.7326/M15-0381.

Langa, K.M., M.E. Chernew, M.U. Kabeto, A.R. Herzog, M.B. Ofstedal, R.J. Willis, R.M. Wallace, L.M. Mucha, W.L. Straus, and A.M. Fendrick. 2001. "National Estimates of the Quantity and Cost of Informal Caregiving for the Elderly with Dementia." Journal of General Internal Medicine, 16: 770-778.

Langa, K.M., E.B. Larson, E.M. Crimmins, J.D. Faul, D.A. Levine, M.U. Kabeto, and D.R. Weir. 2016. "A Comparison of the Prevalence of Dementia in the United States in 2000 and 2012." JAMA Internal Medicine, 177(1): 51-58, doi:10.1001/jamainternmed.2016.6807.

Langa, K.M., E.B. Larson, J.H. Karlawish, D.M. Cutler, M.U. Kabeto, S.Y. Kim, and A.B. Rosen. 2008. "Trends in the Prevalence and Mortality of Cognitive Impairment in the United States: Is there Evidence of a Compression of Cognitive Morbidity?" Alzheimer's & Dementia, 4: 134-144, doi:10.1016/j. jalz.2008.01.001.

Larson, Eric B., Marie-Florence Shadlen, Li Wang, Wayne C. McCormick, James D. Bowen, Linda Teri, and Walter A. Kukull. 2004. "Survival after Initial Diagnosis of Alzheimer Disease." Annals of Internal Medicine, 140(7): 501-511.

LeadingAge. 2016. LeadingAge Pathways Report: Perspectives on the Challenges of Financing Long-Term Services and Supports. Washington, DC: Author. http://www.leadingage.org/sites/default/files/Pathways_Report_February_2016.pdf.

Li, Q., D. Ramirez, W. Chi, N. Chong, J. Williams, and S.L. Karon. 2017. Trend in Disability and Dementia Prevalence from 2011 to 2015: Exploratory Analysis of National Health and Aging Trends Study Data. Washington, DC: U.S. Department of Health and Human Services, Office of the Assistant Secretary for Planning and Evaluation.

Lichtenstein, Maya L., Nader Fallah, Benita Mudge, Ging-Yuek R. Hsiung, Dean Foti, B. Lynn Beattie, Howard H. Feldman. 2018. "16-Year Survival of the Canadian Collaborative Cohort of Related Dementias." Canadian Journal of Neurological Sciences, 45: 367-374.

Long-Term Care Financing Collaborative. 2016. A Consensus Framework for Long-Term Care Financing Reform. Washington, DC: Convergence Center for Policy Resolution. http://morningconsult.com/wp-content/uploads/2016/02/LTCFC-Final-Report-EMBARGOED-2-22-16.pdf.

Mayeda, E.R., M.M. Glymour, C.P. Quesenberry, and R.A Whitmer. 2016. "Inequalities in Dementia Incidence between Six Racial and Ethnic Groups over 14 Years." Alzheimer's & Dementia, 12(3): 216-224, doi:10.1016/j.jalz.2015.12.007.

Murtaugh, C.M., B.C. Spillman, and X. Wang. 2011. "Lifetime Risk and Duration of Chronic Disease and Disability." Journal of Aging and Health, 23(3): 554-77.

National Academies of Sciences, Engineering, and Medicine. 2017. Preventing Cognitive Decline and Dementia: A Way Forward. Washington, DC: National Academies Press. doi:10.17226/24782.

Newquist, Deborah D., Marguerite DeLiema, and Kathleen H. Wilber. 2015. "Beware of Data Gaps in Home Care Research: The Streetlight Effect and Its Implications for Policy Making on Long-Term Services and Supports." Medical Care Research and Review, 72(5): 622-640, doi:10.1177/1077558715588437.

Rainville, Chuck, Laura Skufca, and Laura Mehegan. 2016. Family Caregiving and Out-of-Pocket Costs: 2016 Report. Washington, DC: AARP. http://www.aarp.org/content/dam/aarp/research/surveys_statistics/ltc/2016/family-caregiving-cost-survey-res-ltc.pdf.

Reckrey, Jennifer M., R. Sean Morrison, Kathrin Boerner, Sarah L. Szanton, Evan Bollens-Lund, Bruce Leff, and Katherine A. Ornstein. 2020. "Living in the Community With Dementia: Who Receives Paid Care?" Journal of the American Geriatric Society, 68: 186-191.

Rocca, W.A., R.C. Petersen, D.S. Knopman, L.E. Hebert, D.A. Evans, K.S. Hall, S. Gao, F.W. Unverzagt, K.M. Langa, E.B. Larson, and L.R. White. 2011. "Trends in the Incidence and Prevalence of Alzheimer's Disease, Dementia, and Cognitive Impairment in the United States." Alzheimer's & Dementia, 7(1): 80-93. https://www.ncbi.nlm.nih.gov/pmc/articles/PMC3026476/pdf/nihms253378.pdf.

Schmitz, Al, and Chris Giese. 2019. "Is Insurance the Answer to the Long-Term-Care Financing Challenge?" Generations, 43(1): 86-88.

Seavey, Dorie, with Abby Marquand. 2011. Caring in America: A Comprehensive Analysis of the Nation's Fastest Growing Jobs: Home Health and Personal Care Aides. https://phinational.org/.

Stallard, E. 2011. "Estimates of the Incidence, Prevalence, Duration, Intensity and Cost of Chronic Disability among the U.S. Elderly." North American Actuarial Journal, 15(1): 32-58.

Stallard, P.J.E., and Anatoliy I. Yashin. 2016. Long Term Care Morbidity Improvement Study: Estimates for the Non-Insured U.S. Elderly Population Based on the National Long Term Care Survey 1984-2004. Schaumberg, IL: Society of Actuaries.

Ujvari, Kathleen. 2018. Disrupting the Marketplace: The State of Private Long -Term Care Insurance, 2018 Update. Washington, DC: AARP Public Policy Institute. https://www.aarp.org/content/dam/aarp/ppi/2018/08/disrupting-the-marketplace-the-state-of-private-long-term-care-insurance.pdf.

Wolff, Jennifer L., Brenda C. Spillman, Vicki A. Freedman, and Judith D. Kasper. 2016. "A National Profile of Family and Unpaid Caregivers Who Assist Older Adults with Health Care Activities." JAMA Internal Medicine, 176(3): 372-79, doi:10.1001/jamainternmed.2015.7664.

Wu, Yu-Tzu, Alexa S. Beiser, Monique M.B. Breteler, Laura Fratiglioni, Catherine Helmer, Hugh C .Hendrie, Hiroyuki Honda, M. Arfan Ikram, Kenneth M. Langa, Antonio Lobo, Fiona E. Matthews, Tomoyuki Ohara, Karine Pérès, Chengxuan Qiu, Sudha Seshadri, Britt-Marie Sjölund, Ingmar Skoog, and Carol Brayne. 2017. "The Changing Prevalence and Incidence of Dementia over Time: Current Evidence." Nature Reviews Neurology, 13(6): 327-339.

Yang, Zhou, and Allan Levey. 2015. "Gender Differences: A Lifetime Analysis of the Economic Burden of Alzheimer's Disease." Women's Health Issues, 25(5): 436-40. http://www.whijournal.com/article/S1049-3867(15)00076-6/pdf.

Yang, Zhou, Kun Zhang, Pei-Jung Lin, Carolyn Clevenger, and Adam Atherly. 2012. "A Longitudinal Analysis of the Lifetime Cost of Dementia." Health Services Research, 47(4): 1660-1678.

Zissimopoulos, Julie M., Bryan C. Tysinger, Patricia A. St. Clair, and Eileen M. Crimmins. 2018. "The Impact of Changes in Population Health and Mortality on Future Prevalence of Alzheimer's Disease and Other Dementias in the United States." Journals of Gerontology: Social Sciences, 73(S1): S38-S47.

End Notes

-

Compared with earlier studies, DYNASIM's overall estimate of shares severely impaired at some point from age 65 exceeds the projected shares in Chêne et al. (2015), Murtaugh, Spillman, and Wang (2011) and Yang and Levey (2015) and falls just below the projected shares in Zissimopoulos et al. (2018).

-

We do not present projections for other race-ethnicity categories, including Asian Americans, Pacific Islanders, Native Americans, Alaska Natives, and others, because our underlying source data do not permit reliable estimation of dementia dynamics for these groups. The Health and Retirement Study oversamples African Americans and Latinos, allowing us to have more confidence in the parameter estimates and thus the projections for these groups. Mayeda et al. (2016) present projections of rates of dementia for more groups, including American Indians and Alaska Natives, Asian Americans, and Pacific Islanders though based on plan data from a Northern California health care organization rather than nationally representative data.

-

Placing these estimates in the context of prior literature, DYNASIM's projected unconditional duration with SCI from age 65 from DYNASIM exceeds those reported in Stallard (2011) and Stallard and Yashin (2016) and falls short of the duration reported in Zissimopoulos et al. (2018).

-

Validating these estimates against other data is challenging, as studies of time to death for those with SCI often use very different samples and concepts (e.g., time from diagnosis compared to time of onset of impairment compared to time of enrollment in a study); also, estimates are highly sensitive to age of onset of impairment. Helzner et al. (2008) report median times with SCI of 3.7-7.1 years depending on race/ethnicity, Larson et al. (2004) report medians of 4.2 for men to 5.7 for women, and Lichtenstein et al. (2018) report medians of 7.0 years. Murtaugh, Spillman, and Wang (2011) estimate mean durations of 4.4 years and Yang and Levey (2015) estimate means around 5 years. So the DYNASIM estimates appear broadly consistent, but further monitoring of the literature and validation is warranted.

-

Reckrey et al. (2020) estimate a higher share of unpaid care, but their estimates focus solely on those in the community.

Improving Health and Long-Term Care Modeling Capacity

This report was prepared under contract #HHSP233201600024I between HHS's ASPE/BHDAP and the Urban Institute. For additional information about this subject, you can visit the BHDAP home page at https://aspe.hhs.gov/bhdap or contact the ASPE Project Officers, at HHS/ASPE/BHDAP, Room 424E, H.H. Humphrey Building, 200 Independence Avenue, S.W., Washington, D.C., 20201; Judith.Dey@hhs.gov, Lauren.Anderson@hhs.gov, Helen.Lamont@hhs.gov.

Reports Available

Economic Hardship and Medicaid Enrollment in Later Life: Assessing the Impact of Disability, Health, and Marital Status Shocks

- HTML version: https://aspe.hhs.gov/basic-report/economic-hardship-and-medicaid-enrollment-later-life-assessing-impact-disability-health-and-marital-status-shocks

- PDF version: https://aspe.hhs.gov/pdf-report/economic-hardship-and-medicaid-enrollment-later-life-assessing-impact-disability-health-and-marital-status-shocks

Extended LTSS Utilization Makes Older Adults More Reliant on Medicaid Issue Brief

- HTML version: https://aspe.hhs.gov/basic-report/extended-ltss-utilization-makes-older-adults-more-reliant-medicaid-issue-brief

- PDF version: https://aspe.hhs.gov/pdf-report/extended-ltss-utilization-makes-older-adults-more-reliant-medicaid-issue-brief

Most Older Adults Are Likely to Need and Use Long-Term Services and Supports Issue Brief

- HTML version: https://aspe.hhs.gov/basic-report/most-older-adults-are-likely-need-and-use-long-term-services-and-supports-issue-brief

- PDF version: https://aspe.hhs.gov/pdf-report/most-older-adults-are-likely-need-and-use-long-term-services-and-supports-issue-brief

Risk of Economic Hardship Among Older Adults Issue Brief

- HTML version: https://aspe.hhs.gov/basic-report/risk-economic-hardship-among-older-adults-issue-brief

- PDF version: https://aspe.hhs.gov/pdf-report/risk-economic-hardship-among-older-adults-issue-brief

The Risk and Costs of Severe Cognitive Impairment at Older Ages: Literature Review and Projection Analyses

- HTML version: https://aspe.hhs.gov/basic-report/risk-and-costs-severe-cognitive-impairment-older-ages-literature-review-and-projection-analyses

- PDF version: goto

Long-Term Services and Supports for Older Americans: Risks and Financing, 2020 Research Brief

- HTML version: https://aspe.hhs.gov/basic-report/long-term-services-and-supports-older-americans-risks-and-financing-2020-research-brief

- PDF version: https://aspe.hhs.gov/pdf-report/long-term-services-and-supports-older-americans-risks-and-financing-2020-research-brief

Projections of Risk of Needing Long-Term Services and Supports at Ages 65 and Older

- HTML version: https://aspe.hhs.gov/basic-report/projections-risk-needing-long-term-services-and-supports-ages-65-and-older

- PDF version: https://aspe.hhs.gov/pdf-report/projections-risk-needing-long-term-services-and-supports-ages-65-and-older

The Risk and Costs of Severe Cognitive Impairment at Older Ages: Key Findings from our Literature Review and Projection Analyses Research Brief

- HTML version: https://aspe.hhs.gov/basic-report/risk-and-costs-severe-cognitive-impairment-older-ages-key-findings-our-literature-review-and-projection-analyses-research-brief

- PDF version: https://aspe.hhs.gov/pdf-report/risk-and-costs-severe-cognitive-impairment-older-ages-key-findings-our-literature-review-and-projection-analyses-research-brief