Galina Khatutsky, Joshua M. Wiener, Nga Thach and Angela M. Greene

RTI International

Printer Friendly Version in PDF Format (18 PDF pages)

ABSTRACT

Previous research demonstrates that lack of planning for the potential need for long-term services and supports (LTSS) is associated with lack of knowledge about these services. People who do not have a firm understanding of their longevity risks, probability of needing and using LTSS, and the associated costs for services may be less likely to plan for their future LTSS needs. With the rapid aging of the American population, the demand for LTSS is expected to increase. Americans are not well informed about how the LTSS system works and their risks within it. Without adequate preparation on the part of individuals, many Americans will receive LTSS that do not align with their preferences.

This Issue Brief exams LTSS knowledge using the data from the 2014 Survey of Long-Term Care Planning and Awareness. It was authored by Galina Khatutsky, Joshua M. Wiener, Nga Thach and Angela M. Greene from RTI International. The authors gratefully acknowledge contributions of William Marton and Samuel Shipley of ASPE/HHS. They also wish to thank Genworth Financial for conducting special data analyses of its cost of LTC survey and making the results available. The views expressed in this brief are those of the authors and do not express the views of HHS or RTI International.

Executive Summary

Previous research demonstrates that lack of planning for the potential need for long-term services and supports (LTSS) is associated with lack of knowledge about these services. People who do not have a firm understanding of their longevity risks, probability of needing and using LTSS, and the associated costs for services may be less likely to plan for their future LTSS needs. With the rapid aging of the American population, the demand for LTSS is expected to increase. Without adequate preparation on the part of individuals, many Americans will receive LTSS that do not align with their preferences.

The purpose of this issue brief is to examine LTSS knowledge using the data from the 2014 Survey of Long-Term Care Awareness and Planning sponsored by the Office of the Assistant Secretary for Planning and Evaluation (ASPE)/U.S. Department of Health and Human Services (HHS). The survey was conducted in the summer of 2014 with a nationally representative sample of 15,298 non-institutionalized persons aged 40-70 from the web-based KnowledgePanel® (KP).

Key Findings:

-

Survey respondents had reasonable expectations of their possible longevity and chances of needing long-term care (LTC) in nursing homes, although many thought they would live to a very old age but not use nursing home care. Most people were not well informed about how the LTSS system works. Significant proportions of respondents were unaware that the average length of nursing home stay is less than 5 years or that Medicaid is the primary government payer of LTSS in the United States.

-

Respondents were better informed about private LTC insurance policies. Two-thirds of respondents were aware that private LTC insurance policies are more expensive when purchased at an older age, and two-fifths of respondents understood that good health is often a requirement for purchase.

-

Respondents were also uninformed about the costs of LTSS. Only one-fifth of all respondents correctly estimated the average costs of nursing home care and just 15 percent knew the costs of home health care aides in their state.

-

Over half of survey respondents had some exposure to LTSS through personal use or having a close family member or friend who needed LTSS because of a disability or illness.

-

Those with exposure to LTSS were more likely to correctly answer questions about LTSS utilization risks, costs, and financing and more likely to correctly answer questions about LTC insurance. As far as planning for future LTSS need, participants with LTSS experience were also slightly more likely to own a LTC insurance policy.

-

Although there is some variation in LTSS knowledge by sociodemographic characteristics, the differences are not large and rarely exceed 10 percentage points, suggesting a broad lack of knowledge about LTSS.

Americans are not well informed about how the LTSS system works and their risks within it. These findings highlight the need for increased education of the American public on their LTSS choices and financing options.

Introduction

The need for LTSS is certain to increase over time and to become a more common experience, especially among older Americans. The lack of understanding among the general public of the likelihood of needing LTSS, the associated costs, and how public and private programs work have been linked to inadequate preparedness for LTSS (MetLife Mature Market Institute, 2009; Stringfellow, 2012; Tompson et al., 2013; U.S. Senate Commission on Long-Term Care, 2013). Previous studies also have connected the extent of LTSS awareness with having personal experiences with LTSS or exposure to caregiving (Courbage & Roudaut, 2008; Finkelstein, Reid, Kleppinger, Pillemer, & Robison, 2012; Tennyson & Yang, 2014). Unless people have basic information about LTSS--what it is, their risks for needing it, what it costs, and how the current financing system works--they are unlikely to be motivated to plan for their potential LTSS needs. Planning may include discussing care preferences with family, purchasing a private LTC insurance policy or an annuity, or saving to pay for services. Experience with LTSS may increase the level of knowledge that individuals have about LTSS.

The purpose of this issue brief is to examine LTSS experience and knowledge using the data from the 2014 Survey of Long-Term Care Awareness and Planning sponsored by ASPE/ HHS and to compare beliefs about LTSS costs, utilization risk, and financing among people aged 40-70 with factual information.

Research Questions

This brief provides answers to the following important policy questions:

-

How do people assess their expected longevity and chances of needing nursing home care?

-

How common is personal experience with LTSS, either personally or through family and close friends, and how does it vary by key demographic characteristics?

-

What do people know about the costs of LTSS and how does this knowledge vary by key demographic characteristics and by previous experience with LTSS?

-

What do people know about LTSS financing and some key features of private LTC insurance policies, and how does this knowledge vary by key demographic characteristics?

-

How does perceived longevity, perceived need for nursing home care, and knowledge about LTSS and LTC insurance differ between people who had personal experience with LTSS and those who had not?

Background

Previous research has established that the general public's LTSS literacy is low. Many people have little understanding of how the current LTSS system works and have few opinions about how the system should be reformed. Data from the MetLife Long-Term Care IQ Survey (MetLife Mature Market Institute, 2009), found that only 21 percent of respondents could score 70 percent or higher on the 10-item LTSS knowledge quiz. In a nationally representative study conducted by the Associated Press-NORC Center in 2013, almost one-third of respondents reported not wanting to think about aging at all (Tompson et al., 2013).

People are often poor judges of their own survivorship, with most under age 65 underestimating how long they will live (Abraham & Harris, 2014; Elder, 2013). Estimating longevity is important because advanced age is strongly related to disability and the need for and use of LTSS (He & Larsen, 2014). Knowing their realistic life expectancies may prompt people to plan ahead and ensure adequate savings and appropriate strategies for obtaining needed services. Actuaries define the risk of living beyond expectations as "longevity risk." Failure to understand and plan for a long life in retirement and for years of frailty and chronic illness often undermine whatever saving and LTSS preparedness efforts individuals may take. According to the American Academy of Actuaries, as of 2012, the life expectancy based on Social Security tables at age 65 is 18.9 years for males and 20.9 years for females. The probability of living a very long life is significant, especially for "survivors" who have good health, have lived healthy lifestyles, and have worked in jobs that did not take a physical toll (Abkemeier et al., 2013).

Lack of knowledge about the average life expectancy may explain why people tend to underestimate their risks of having to use LTSS. For example, in the 2012 National Health and Interview survey, only 40 percent of respondents aged 40-65 reported expectations of developing LTSS needs in the future (Henning-Smith & Shippee, 2015). In contrast, a study using a sophisticated microsimulation model estimated that approximately 70 percent of Americans aged 65 and older are expected to need LTSS at some point in their lives (Kemper, Komisar, & Alecxih, 2005; Tompson et al., 2013). The Kemper, Komisar, and Alecxih (2005) study also estimated that approximately 35 percent of people aged 65 and older would experience a non-Medicare nursing home stay before death. Although individuals' expectations of whether they will use nursing home care certainly influence the actual likelihood of staying in a nursing home (Akamigbo & Wolinsky, 2006; Taylor, Osterman, Will Acuff, & Østbye, 2005), more recent findings suggest there are high risks of nursing home placement despite low preference. A 2013 study using data from the Health and Retirement Study (HRS) suggests that a 50 year old has a 53-59 percent chance of having a stay in a nursing home, with an average length of stay of 370 days (Hurd, Michaud, & Rohwedder, 2013). Another study suggests that length of stay is under 1 year (321 days) for men, and close to a year and a half for women (526 days) (Friedberg, Sun, Webb, Hou, & Li, 2014).

A major component of LTSS literacy is understanding how much LTSS costs in various settings and who pays for it. Because they do not know how expensive LTSS can be, individuals may be less accurate in their planning and unlikely to sufficiently prepare financially. An AARP multistate survey of Americans aged 45 and older found that although 60 percent of respondents reported that they are at least "somewhat familiar" with LTSS currently available and 21 percent said they are "very familiar," their estimates of LTSS costs were not accurate (AARP, 2006). The 2013 Associated Press-NORC (AP-NORC) study offered similar findings, with 58 percent of interviewees underestimating the national average monthly cost of staying in a nursing home and 52 percent of interviewees overestimating the national average monthly cost of a part-time home health care aide (Tompson et al., 2013).

Several studies also find that many people think that they already have coverage for LTSS, either through Medicare or through their private health insurance policies, even though they do not. The Kaiser Family Foundation's (2007) report on the public's views about LTSS noted that 23 percent of respondents said that a major reason they do not have LTC insurance is that they believe Medicare will cover the cost of care, even though it will not; other reasons given for not having LTC insurance include the belief that Medicaid will cover the cost (21 percent) and the expectation that family members will provide care (23 percent). The AP-NORC study (Tompson et al., 2013) found that 54 percent of Americans do not expect assistance from the Medicaid system as they age. Additionally, it appears that many people believe they have private LTC insurance coverage when they probably do not. Twenty-nine percent of respondents in the AARP (2006) survey reported having LTC insurance either through work, a private policy, or some other means. This percentage is approximately twice as much as estimates of the number of people covered by LTC insurance based on recent surveys. According to data from the 2010 HRS, 13 percent of single people aged 65 and over have LTC insurance coverage (Friedberg, Hou, Sun, & Webb, 2014). Findings from a study conducted by America's Health and Insurance Plans and LifePlans, Inc. suggest that approximately 15 percent of adults over the age of 65 with incomes of at least $20,000 have an LTC insurance policy (LifePlans, 2012).

Although many people, especially those of working-age, do not know much about LTSS, people in the Baby Boom cohort are learning about LTSS and are acquiring first-hand experience because their aging parents and other relatives require assistance. Others have second-hand experience through discussions with family members and friends who have had experiences with LTSS. Experience with LTSS can be obtained in any of the following ways: (1) as a recipient of services; (2) as an arranger and supervisor of LTSS for others; (3) as a caregiver; or (4) as a payer of LTSS bills. As the Baby Boom cohort ages, their experience with LTSS will likely increase.One common hypothesis is that people with experience with LTSS will be more likely to engage in LTSS planning activities and purchase plans. In a 2012 study examining LTSS planning among Baby Boomers in Connecticut, researchers found that, compared to non-caregivers, adult caregivers have more realistic expectations of their own future LTSS needs, but are not any more likely to have taken LTSS planning actions (Finkelstein et al., 2012).

Data and Methods

Data from this issue brief are from the 2014 Survey of Long-Term Care Awareness and Planning, which was sponsored by ASPE/HHS. The survey instrument was developed by RTI International in close cooperation with ASPE and with guidance from a Technical Expert Panel of experts on survey methodology, LTSS, and LTC insurance.

The survey has two components. The first component asks questions on: (1) self-perceived longevity and the risk of needing LTC; (2) basic financial literacy and psychological characteristics such as risk tolerance; (3) LTC knowledge and LTC experience; (4) beliefs and concerns about LTC; (5) retirement and LTC planning; (6) LTC information gathering and decision making; (7) attitudes toward LTC financing options; and (8) core demographic and socioeconomic information. The second component of the survey is a discrete choice experiment, where respondents are asked to choose among LTC insurance products with different features. The survey underwent two rounds of cognitive testing and was revised based on results of the testing.

The survey was fielded by using KP, GfK's standing Internet panel.1 The survey sample consisted of non-institutionalized adults aged 40-70 residing in the United States. The survey was administered online from August 8, 2014, to September 21, 2014. Survey respondents received e-mail notifications and reminders to fill out the survey, and were rewarded for their participation with 10,000 KP "points" (equivalent to about $10) that can be exchanged for merchandise and other prizes. Of the 24,878 people sampled, 15,298 completed the main survey, yielding a response rate of 61.5 percent. Thirty cases were excluded because of respondent omission of more than one-third of the substantive survey questions. GfK used data from the 2013 March supplement of the Current Population Survey to weight the respondents to represent the non-institutionalized population. Qualified respondents were weighted to match the 40-70 year old United States population on the dimensions of gender, age, race/ethnicity, census region by metropolitan status, education, and household income.

To assess the accuracy of respondents' estimates of LTSS costs, we used unpublished data from the 2014 Genworth Cost of Care Survey on average hourly rates for home health aide services and monthly costs of a semiprivate room in a nursing home (Genworth Financial, 2014a). Respondents' estimates of costs for these services were matched to average costs in their states of residence, then coded as correct or incorrect. Respondents were also categorized by LTSS experience. Those categorized as having LTSS experience have had at least two of the following five experiences: (1) provided LTSS for a family member or friend in the past; (2) currently providing LTSS for a family member or friend; (3) had or know someone who has had a severe illness or disability requiring LTSS; (4) received or know someone who has received paid in-home care; and (5) has been a resident or know someone who has been a resident in a nursing home or in an assisted living residence.

Findings

Self-Reported Chances of Living to 85 Years Old or Older. In our survey of people between the ages of 40 and 70, 82.1 percent of respondents estimated their chances of living to be 85 years old or older as 50 percent or higher. Table 1 presents data on LTSS/LTC insurance knowledge for the entire sample, and then stratified by age and gender. Although there was not much difference by age, women were more likely to think that they would live to age 85 or older. Although not directly comparable, the life tables developed by the American Academy of Actuaries (Abkemeier et al., 2013) show that, as of 2012, at age 65, males have a 40 percent chance of living to age 85 and females have a 53 percent chance of living to age 85. For individuals of good health with healthy lifestyles, the probability of living to age 85 is 51 percent for males and 62 percent for females. Although our survey estimates were calculated differently, respondents had a reasonably good understanding of their chances of living long lives. Actuaries point out "that an important issue underlying many causes of inadequate lifetime income is the unpredictability of an individual's lifespan and an understanding that life expectancy is not how long an individual will live" (Abkemeier et al., 2013, p. 6).

Self-Reported Chances of Moving to Nursing Home >50 Percent. Perhaps because of their expectation to live to old ages, a significant proportion of respondents thought that there was a substantial risk of their using nursing home care. Slightly over 40 percent of all respondents (41.5 percent) rated their chances of needing to move to a nursing home sometime in the future as 50 percent or higher, which is lower than the estimated risk reported in recent studies (Hurd et al., 2013) but about equal to the level estimated in the earlier study (Kemper et al., 2005). The proportion of respondents assessing their chances of needing nursing facility care as high did not vary much with age.

Table 2 presents LTSS/LTC insurance knowledge stratified by race/ethnicity, education, and marital status. Table 3 displays the same data stratified by income categories. There are no differences in respondents' assessments of their chances of needing nursing facility care by gender and marital status and there is a mixed pattern by race. However, people make higher estimates of longevity and nursing home use with increased educational attainment, income, and asset level. Significantly more respondents with personal LTSS experience assess their chances of needing nursing home care being more than 50 percent compared with respondents with no such experience (46.4 percent vs. 36.3 percent).

Prior Long-Term Care Experience. Over half of all respondents (52.8 percent) reported using LTSS personally or knowing a close family member or friend who needed LTSS because of a disability or illness. About one-third (31.1 percent) of respondents reported receiving or knowing somebody receiving paid in-home care for help with activities of daily living (ADLs), and 44.2 percent reported knowing a nursing home or assisted living resident or having been one themselves. As shown in Table 1, the likelihood of having a personal experience with LTC and knowing somebody who required LTSS significantly increases with age. Women also reported significantly more experiences with LTSS than men. In Table 2, a larger proportion of non-minority respondents reported having a personal experience with LTSS and knowing somebody who required LTSS compared to respondents of other races. Compared to lower-educated respondents, respondents with higher education levels also were more likely to report prior LTSS experience, both personally and through people they know. People of higher income categories also report more prior experience with LTSS than people of lower financial means (Table 3). Significantly more respondents with past and present personal LTSS experience assess their chances of needing nursing home care being more than 50 percent compared with respondents with no such experience (46.4 percent vs. 36.3 percent).

Knowledge of Long-Term Care Costs and Use of Services. LTSS are very expensive and Medicare and most private health insurance plans do not cover these expenses. As a result, many Americans who use LTSS incur catastrophic out-of-pocket expenses and spend down to Medicaid (Wiener, Anderson, Khatutsky, Kaganova, & O'Keeffe, 2013). In 2014, nationally, the median cost of a semiprivate room in a nursing home was $77,380 per year and the median cost of home health aide care was $20 per hour (Genworth Financial, 2014b). Rates varied greatly between states and geographic regions, with the average monthly price of nursing home care costing as little as $4,253 in Texas, to as high as $18,806 in Alaska. Similarly, the range for average cost of home health aide care ranged from $15.08 in Louisiana to $25.40 in Hawaii, per hour (Genworth Financial, 2014a). Data from Genworth's annual surveys indicate that these costs are steadily increasing. Nursing home care costs for a semiprivate room had an annual growth rate of 3.91 percent between 2009 and 2014, while home health aide care costs increased by 1.32 percent over the same time period.

The Survey of Long-Term Care Awareness and Planning measured how well the general public understands the costs associated with LTSS in the community and institutional settings. Despite the magnitude of LTSS costs and their continuing inflation, Americans do not have a good grasp of the costs. Only about one-fifth of all respondents (20.2 percent) correctly estimated the average cost of a semiprivate room for a month of nursing home care in their states of residence and 15.3 percent correctly estimated the average cost of 1 hour of home health aide care in their states (Table 1). Aside from those who estimated nursing home and home health costs incorrectly, more than one-third of our sample (36 percent) reported not knowing the costs of either of these services.

Besides knowing the cost of services, how long people use them is another critical factor in planning for financial protection against potentially catastrophic out-of-pocket costs. Another survey item gauged respondents' knowledge of the average time an individual spends in a nursing facility. About one-third of all respondents selected the correct answer (the average length of stay in a nursing home is less than 5 years); compared to younger respondents, significantly more respondents in the older age group selected the correct response (43.5 percent vs. 33.4 percent). There were almost no differences in selecting the correct response to this question between genders. White, married, and better-educated respondents were more likely to know the average length of nursing home stay compared to minority, unmarried, and lower-educated respondents (Table 2). Knowledge of the average nursing home stay duration also increased with higher household income (Table 3). Thus, most people did not know what level of financial protection they needed.

Knowledge of Medicaid and Long-Term Care Insurance. Previous studies consistently have found a lack of clear understanding among the general public in terms of what is and is not covered under the Medicare program and the role of Medicaid--a means-tested program--in financing LTSS. In 2007, Medicare covered one-quarter of the $190.4 billion spent on nursing home and home health care in the United States. In comparison, Medicaid and other public funds paid 42 percent of that total, making it the most common payer of LTSS (Ng, Harrington, & Kitchener, 2010). The Congressional Budget Office projects that Medicaid LTSS expenditures will increase by an average of 5.5 percent each year between 2013 and 2023 (Congressional Budget Office, 2013). The results from the Survey of Long-Term Care Awareness and Planning indicated that only one-quarter of all respondents correctly identified Medicaid as the government program that pays the most for LTSS in the United States. As presented in Table 1, significantly more respondents aged 65 and older (32.4 percent) selected the correct answer to this question compared to respondents under the age of 65 (24.1 percent).

Although statistically significant, the differences between males and females in selecting the correct answer were not large. White and higher educated respondents were somewhat more familiar with the role of Medicaid in covering LTSS, with the differences being statistically significant but moderate in effect. Although still only approaching 30 percent, respondents with prior LTSS experience was the category of respondents that selected the correct answer to the Medicaid question most often. The 2014 Survey of Long-Term Care Awareness and Planning also measured basic knowledge among respondents on key LTC insurance features. Our data showed that respondents were fairly knowledgeable of some of the features of standard LTC insurance policies. For example, about two-thirds (66.7 percent) knew that the monthly cost of a private LTC insurance increases with buyer's age, and 41.0 percent knew that medical underwriting was usually required for purchase of a policy. Table 1 shows that significantly more respondents in the 65 years and older age category selected the correct answer on the age-related price increases question than respondents under the age of 65 (75.2 percent vs. 65.2 percent). There was no difference between the age groups in the likelihood of selecting a correct response on medical underwriting questions, even though older people are more likely to have health problems that preclude them from purchasing policies. Males selected the correct answers more often than females, but the differences in proportions were not large. White, married, and better-educated respondents were more knowledgeable about the two features of private LTC insurance compared to minority, unmarried, and lower-educated respondents, respectively (Table 2). The probability of selecting a correct response on both LTC insurance features questions progressively increased with rise in household income (Table 3).

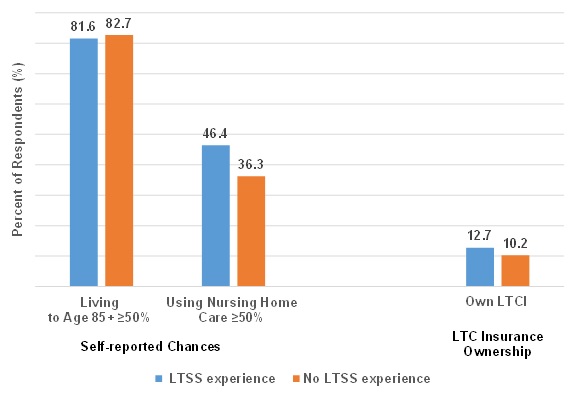

Role of Long-Term Services and Supports Experience in Long-Term Services and Supports Knowledge. Direct or indirect personal exposure to LTSS by either personally using LTSS or providing caregiving generally affects knowledge of LTSS. Figure 1 and Figure 2 present data on LTSS knowledge by personal experience with LTSS. Personal experience with LTSS does not affect self-reported longevity expectations: approximately the same proportion of people with and without LTSS experience rate their chances of living to age 85 or older at 50 percent or higher. On the other hand, significantly more people in the experienced group rate their chances of needing nursing home care as 50 percent or higher compared to those who had no personal experience with LTSS (46.4 percent and 36.3 percent, respectively).

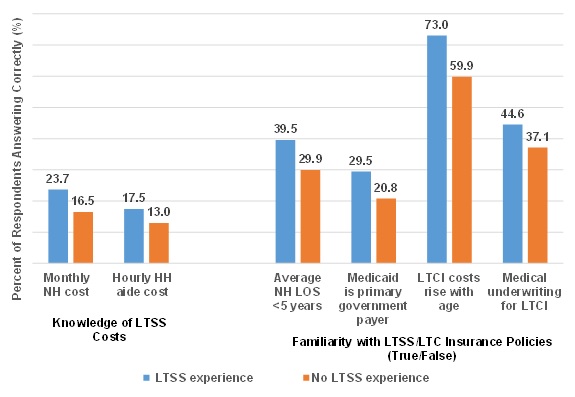

On LTSS knowledge items (Figure 2), there were consistent and significant differences between those with and without LTSS experience. For example, although the general knowledge of LTC costs is low, 23.7 percent of respondents with LTSS experience provided correct estimates of nursing home costs and 17.5 percent provided correct estimates of home health care in their states, compared to 16.5 percent and 13.0 percent, respectively, among respondents without any personal LTSS experience. Similarly, 39.5 percent of respondents exposed to LTSS selected the correct response about the duration of nursing home care, compared to 29.9 percent among non-exposed respondents. More respondents among the group exposed to LTC (29.5 percent) knew about Medicaid being the primary government program paying for most LTSS in the United States than among the non-exposed group (20.8 percent). More survey respondents who had personal experience with LTSS also knew important details of private LTC insurance policies such as cost increases with buyer's age (73.0 percent) and medical underwriting (44.6 percent): about 60 percent among the group without experience knew about age-related increases in policy costs and only about 37 percent knew about medical underwriting of LTC insurance policies.

Conclusions

Knowledge of the risk of needing LTSS and of the costs, use, and ways to finance those services is critical for motivating people to plan for LTSS. Data presented in this issue brief suggest that although many people have an understanding of their risks of needing care, relatively few people have a good understanding of how the LTSS system works. For example, knowing the average length of stay in a nursing home may help people select the proper LTC insurance product or estimate the amount of savings needed to pay the nursing home care costs.

Survey respondents have a moderately clear understanding of their possible longevity and their chances of needing LTC in nursing homes. Conversations about retirement and LTSS preparedness require some information about the risk of becoming disabled and needing LTSS. If people believe that they do not face a significant risk of needing LTSS, there is little motivation to plan for it.

Despite the fact that LTSS exposure and personal experience are relatively common, respondents display low knowledge of the current LTSS system. Only about one-fifth of all respondents correctly identified the average costs of nursing home care in their states and only about one-third were able to identify an incorrect statement about length of stay in nursing homes. Importantly for reform efforts, only one-quarter of respondents knew that Medicaid was the government payer for LTSS. Surprisingly, overall, there is far better familiarity with the basic requirements of purchasing private LTC insurance than with the role of Medicaid in LTSS. Two-thirds of respondents knew that premiums increase with the buyer's age and two-fifths knew that medical underwriting is usually required for private LTC insurance. Although there is some variation in knowledge by sociodemographic characteristics, the differences are not large and rarely exceed 10 percentage points, suggesting a broad lack of knowledge about LTSS. Highly educated people and those with higher incomes are more knowledgeable than lower-educated people and those with lower incomes.

Between one-third and one-half of the survey respondents reported some kind of exposure and personal experience with LTSS. This study indicates that personal experience with LTSS increases knowledge of LTSS. As Baby Boomers age and provide more caregiving to their parents and other relatives and experience more health problems themselves with the subsequent need for LTSS, their personal exposure to LTSS will only grow. Baby Boomers will also observe their parents struggling with LTSS costs and spending down to Medicaid and will face a need to contribute to their parents' LTSS expenses. As a result, more people will learn about the lack of adequate coverage and the substantial out-of-pocket costs of providing LTSS, hopefully prompting them to plan for LTSS care.

The data presented in this brief provide policymakers some guidance on the knowledge gaps of the general population about LTSS and how to target these efforts to particular segments of the general population that are most in need of education.

References

AARP. (2006). The Costs of Long-Term Care: Public Perceptions versus Reality in 2006. Washington, DC: AARP.

Abkemeier, N., Bennett, N., Bevacqua, J., Esch, J., Ferris, A., Fickett-Wilbar, D., et al. (2013). Risky Business: Living Longer Without Income for Life. Report prepared for American Academy of Actuaries. Washington, DC.

Abraham, K.G., & Harris, B.H. (2014). Better Financial Security in Retirement? Realizing the Promise of Longevity Annuities. Report prepared for The Brookings Institution.

Akamigbo, A.B., & Wolinsky, F.D. (2006). Reported expectations for nursing home placement among older adults and their role as risk factors for nursing home admissions. The Gerontologist, 46(4), 464-473.

Congressional Budget Office. (2013). Rising Demand for Long-Term Services and Supports for Elderly People. Report prepared for Congress of the United States, Congressional Budget Office. Washington, DC.

Courbage, C., & Roudaut, N. (2008). Empirical evidence on long-term care insurance purchase in France. Geneva Papers on Risk and Insurance, 33, 645-658.

Elder, T.E. (2013). The predictive validity of subjective mortality expectations: Evidence from the Health and Retirement Study. Demography, 50(2), 569-589.

Finkelstein, E.S., Reid, M.C., Kleppinger, A., Pillemer, K., & Robison, J. (2012). Are baby boomers who care for their older parents planning for their own future long-term care needs? Journal of Aging & Social Policy, 24(1), 29-45.

Friedberg, L., Hou, W., Sun, W., & Webb, A. (2014). Long-Term Care: How Big a Risk? Report prepared for Center for Retirement Research at Boston College. Chestnut Hill, MA.

Friedberg, L., Sun, W., Webb, A., Hou, W., & Li, Z. (2014). New Evidence on the Risk of Requiring Long-Term Care. Report prepared for Center for Retirement Research at Boston College. Chestnut Hill, MA.

Genworth Financial. (2014a). 2014 Cost of Care Survey.

Genworth Financial. (2014b). Genworth 2014 Cost of Care Survey Home Care Providers, Adult Day Health Care Facilities, Assisted Living Facilities and Nursing Homes. Report prepared for Genworth Financial. Richmond, VA.

He, W., & Larsen, L.J. (2014). Older Americans with a Disability: 2008-2012. Report prepared for U.S. Census Bureau. Washington, DC.

Henning-Smith, C.E., & Shippee, T.P. (2015). Expectations about future use of long-term services and supports vary by current living arrangement. Health Affairs, 34(1), 39-47.

Hurd, M., Michaud, P.-C., & Rohwedder, S. (2013). The Lifetime Risk of Nursing Home Use. Discoveries in the Economics of Aging: University of Chicago Press.

Kemper, P., Komisar, H.L., & Alecxih, L. (2005). Long-term care over an uncertain future: What can current retirees expect? Inquiry, 42(4), 335-350.

LifePlans. (2012). Who Buys Long-Term Care Insurance in 2010-2011?: A Twenty Year Study of Buyers and Non-Buyers (in the Individual Market). Report prepared for America's Health Insurance Plans. Washington, DC.

MetLife Mature Market Institute. (2009). Removing Myths, Reinforcing Realities. Report prepared for MetLife Mature Market Institute. New York, NY: M.L.I. Company.

Ng, T., Harrington, C., & Kitchener, M. (2010). Medicare and Medicaid in long-term care. Health Affairs, 29(1), 22-28.

Stringfellow, A. (2012). Northwestern Mutual's Long-Term Care Awareness Study: Key Findings. Retrieved February 13, 2015, from http://www.seniorhomes.com/w/northwestern-mutuals-long-term-care-awareness-study-key-findings/.

Taylor, D.H., Osterman, J., Will Acuff, S., & Østbye, T. (2005).Do seniors understand their risk of moving to a nursing home? Health Services Research, 40(3), 811-828.

Tennyson, S., & Yang, H.K. (2014). The role of life experience in long-term care insurance decisions. Journal of Economic Psychology, 42, 175-188.

Tompson, T., Benz, J., Agiesta, J., Junius, D., Nguyen, K., & Lowell, K. (2013). Long-Term Care: Perceptions, Experiences, and Attitudes among Americans 40 or Older. Report prepared for Associated Press-NORC Center for Public Affairs Research. Chicago, IL.

U.S. Senate Commission on Long-Term Care. (2013). Report to the Congress. Retrieved from http://www.gpo.gov/fdsys/pkg/GPO-LTCCOMMISSION/pdf/GPO-LTCCOMMISSION.pdf.

Wiener, J.M., Anderson, W.L., Khatutsky, G., Kaganova, Y.M., & O'Keeffe, J. (2013). Medicaid Spend Down: New Estimates and Implications for Long-Term Services and Supports Financing Reform. Long Beach, CA: SCAN Foundation. Retrieved February 25, 2015, from http://www.thescanfoundation.org/sites/thescanfoundation.org/files/rti_medicaid-spend-down_3-20-13_1.pdf.

| FIGURE 1. Longevity/Nursing Home Use Risk and LTC Insurance Ownership by LTSS Experience |

|---|

|

| SOURCE: RTI analysis of the 2014 ASPE Survey of Long-Term Care Awareness and Planning. NOTES: All proportions are presented weighted. All differences are significant at p = 0.001, except for "Living to Age 85," which is not significant. |

| FIGURE 2. LTSS/LTC Insurance Knowledge by LTSS Experience |

|---|

|

| SOURCE: RTI analysis of the 2014 ASPE Survey of Long-Term Care Awareness and Planning. NOTES: All proportions are presented weighted. All differences are significant at p = 0.001. |

| TABLE 1. LTC Knowledge by Age and Gender | |||||

|---|---|---|---|---|---|

| Survey Questions | All Respondents N=15,298 % | Age Under 65 N=11,824 % | Age 65+ N=3,474 % | Gender: Male N=5,950 % | Gender: Female N=9,348 % |

| Self-reported chances of living to age 85+ >50% | 82.1 | 81.8 | 84.1** | 78.6 | 85.3*** |

| Self-reported chances of moving to nursing home >50% | 41.5 | 41.9 | 39.0** | 41.5 | 41.5 |

| Experience With LTSS (Have you or has someone you know ever...) | |||||

| Required LTC because of a disability or illness? | 52.8 | 51.7 | 59.7*** | 49.6 | 55.7*** |

| Received paid in-home care for ADLs? | 31.3 | 30.7 | 34.7*** | 28.9 | 33.5*** |

| Been a resident in a nursing home/assisted living facility? | 44.2 | 42.5 | 54.1*** | 42.6 | 45.7*** |

| Knowledge of LTSS Costs | |||||

| Average cost of 1 month of nursing home care | 20.2 | 19.7 | 23.4*** | 19.9 | 20.5 |

| Average cost of 1 hour of home health aide care | 15.3 | 14.9 | 17.7*** | 13.7 | 16.7*** |

| Knowledge of LTSS/LTC Insurance (True/False) | |||||

| Average length of nursing home stay is less than 5 years | 34.9 | 33.4 | 43.5*** | 34.3 | 35.4* |

| Medicaid is the government program that pays the most for LTSS in the United States | 25.3 | 24.1 | 32.4*** | 24.9 | 25.6*** |

| Monthly cost of a private LTC insurance policy first purchased at age 45 will be the same as the monthly cost of a policy first purchased at age 65 | 66.7 | 65.2 | 75.2*** | 69.4 | 64.2*** |

| In order to buy most private LTC insurance policies, you usually need to be in good health (medical underwriting) | 41.0 | 41.0 | 41.0 | 41.8 | 40.2*** |

| SOURCE: RTI analysis of the 2014 ASPE Survey of Long-Term Care Awareness and Planning. NOTE: All proportions and means are weighted. Statistical Significance: ns = p > 0.05; * = p 0.05; ** = p 0.01; *** = p 0.001. | |||||

| TABLE 2. LTC Knowledge by Race, Education, and Marital Status | |||||||

|---|---|---|---|---|---|---|---|

| Survey Questions | All Respondents N=15,298 % | Race/Ethnicity | Education | Marital Status | |||

| White, Non-Hispanic N=12,169 % | Other N=3,129 % | High School or Less N=2,802 % | Some College, Bachelor's Degree or Higher N=12,496 % | Married N=9,204 % | Not Married N=6094 % | ||

| Self-reported chances of living to age 85+ >50% | 82.1 | 80.9 | 85.1*** | 77.1 | 85.4*** | 84.1 | 78.7*** |

| Self-reported chances of moving to nursing home >50% | 41.5 | 43.7 | 36.4*** | 38.2 | 43.7*** | 41.5 | 41.5 |

| Experience With LTSS (Have you or has someone you know ever...) | |||||||

| Required LTC because of a disability or illness? | 52.8 | 55.5 | 46.4*** | 47.1 | 56.5*** | 53.2 | 52.2 |

| Received paid in-home care for ADLs? | 31.3 | 32.5 | 28.3*** | 25.3 | 35.2*** | 31.2 | 31.5 |

| Been a resident in a nursing home/assisted living facility? | 44.2 | 50.3 | 29.5*** | 37.4 | 48.7*** | 46.6 | 40.1*** |

| Knowledge of LTSS Costs (% Correct) | |||||||

| Average cost of 1 month of nursing home care | 20.2 | 22.3 | 15.1*** | 16.6 | 22.6*** | 21.4 | 18.1*** |

| Average cost of 1 hour of home health aide care | 15.3 | 16.2 | 13.2*** | 12.9 | 16.9*** | 15.6 | 14.8 |

| Knowledge of LTSS/LTC Insurance (True/False) | |||||||

| Average length of nursing home stay is less than 5 years. | 34.9 | 38.9 | 25.2*** | 29.6 | 38.4*** | 36.9 | 31.5*** |

| Medicaid is the government program that pays the most for LTC services in the United States. | 25.3 | 26.4 | 22.6*** | 23.8 | 26.3*** | 25.9 | 24.2* |

| Monthly cost of a private LTC insurance policy first purchased at age 45 will be the same as the monthly cost of a policy first purchased at age 65. | 66.7 | 70.5 | 57.4*** | 56.9 | 73.1*** | 69.4 | 61.9*** |

| In order to buy most private LTC insurance policies, you usually need to be in good health (medical underwriting). | 41.0 | 42.2 | 38.1*** | 38.2 | 42.8*** | 42.8 | 37.9*** |

| SOURCE: RTI analysis of the 2014 ASPE Survey of Long-Term Care Awareness and Planning. NOTE: All proportions and means are weighted. Statistical Significance: ns = p > 0.05; * = p 0.05; ** = p 0.01; *** = p 0.001. | |||||||

| TABLE 3. LTC Knowledge by Household Income | |||||

|---|---|---|---|---|---|

| Survey Questions | All Respondents N=15,298 % | Less Than $15,000 N=1,336 % | $15,000-$40,000 N=3,275 % | $40,000-$100,000 N=7,174 % | More than $100,000 N=3,513 % |

| Self-reported chances of living to age 85+ >50% | 82.1 | 71.1 | 76.7 | 83.3 | 88.4*** |

| Self-reported chances of moving to nursing home >50% | 41.5 | 38.4 | 36.6 | 41.9 | 45.8*** |

| Experience With LTSS (Have you or has someone you know ever...) | |||||

| Required LTC because of a disability or illness? | 52.8 | 51.7 | 52.8 | 52.8 | 53.4 |

| Received paid in-home care for ADLs? | 31.3 | 29.1 | 29.6 | 31.2 | 33.6*** |

| Been a resident in a nursing home/assisted living facility? | 44.2 | 32.5 | 40.0 | 46.1 | 48.6*** |

| Knowledge of LTSS Costs | |||||

| Average cost of 1 month of nursing home care | 20.2 | 11.6 | 16.1 | 21.3 | 24.7*** |

| Average cost of 1 hour of home health aide care | 15.3 | 12.6 | 12.5 | 15.8 | 17.7*** |

| Knowledge of LTSS/LTC Insurance (True/False) | |||||

| Average length of nursing home stay is less than 5 years. | 34.9 | 26.6 | 29.9 | 35.9 | 40.0*** |

| Medicaid is the government program that pays the most for LTSS in the United States. | 25.3 | 21.8 | 22.6 | 26.4 | 26.6*** |

| Monthly cost of a private LTC insurance policy first purchased at age 45 will be the same as the monthly cost of a policy first purchased at age 65. | 66.7 | 49.0 | 59.2 | 68.3 | 76.3*** |

| In order to buy most private LTC insurance policies, you usually need to be in good health (medical underwriting). | 41.0 | 33.9 | 38.0 | 42.2 | 43.8*** |

| SOURCE: RTI analysis of the 2014 ASPE Survey of Long-Term Care Awareness and Planning. NOTE: All proportions and means are weighted. Statistical Significance: ns = p > 0.05; * = p 0.05; ** = p 0.01; *** = p 0.001. | |||||

NOTES

-

Documentation regarding KP sampling, data collection procedures, weighting, and Institutional Review Board-bearing issues are available at the following online resources: http://www.knowledgenetworks.com/ganp/reviewer-info.html; http://www.knowledgenetworks.com/knpanel/index.html; and http://www.knowledgenetworks.com/ganp/irbsupport/.

Survey on Long-Term Care Awareness and Planning

This report was prepared for U.S. Department of Health and Human Services (HHS), Office of Disability, Aging and Long-Term Care Policy (DALTCP) under contract #HHSP233201000693G with Knowledge Networks and contract #HHSP23320100021WI with the Research Triangle Institute. For additional information about this subject, you can visit the DALTCP home page at http://aspe.hhs.gov/office-disability-aging-and-long-term-care-policy-daltcp or contact the ASPE Project Officers, Samuel Shipley and William Marton, at HHS/ASPE/DALTCP, Room 424E, H.H. Humphrey Building, 200 Independence Avenue, S.W., Washington, D.C. 20201; William.Marton@hhs.gov.

Reports Available

Choosing Long-Term Care Insurance Policies: What Do People Want? Issue Brief

- HTML: https://aspe.hhs.gov/basic-report/choosing-long-term-care-insurance-policies-what-do-people-want

- PDF: https://aspe.hhs.gov/pdf-report/choosing-long-term-care-insurance-policies-what-do-people-want

Long-Term Services and Supports: What are the Concerns and What are People Willing to Do? Issue Brief

- HTML: https://aspe.hhs.gov/basic-report/long-term-services-and-supports-what-are-concerns-and-what-are-people-willing-do

- PDF: https://aspe.hhs.gov/pdf-report/long-term-services-and-supports-what-are-concerns-and-what-are-people-willing-do

What Do People Know About Long-Term Services and Supports? Issue Brief

- HTML: https://aspe.hhs.gov/basic-report/what-do-people-know-about-long-term-services-and-supports

- PDF: https://aspe.hhs.gov/pdf-report/what-do-people-know-about-long-term-services-and-supports

Which Way for Long-Term Services and Supports Financing Reform? Issue Brief