Amy Burke, Arpit Misra, and Steven Sheingold

Department of Health and Human Services

Office of the Assistant Secretary for Planning and Evaluation

This brief provides an overview of health insurance plan premiums available in the 2014 Marketplace and the important role of the advanced premium tax credit (“tax credit”) in helping families afford coverage. It contains information on the change in the premium cost associated with the tax credit for individuals who made Marketplace plan selections through the Federally-facilitated Marketplace (FFM) during the initial open enrollment period. Also, it analyzes over 19,000 Marketplace plans for 2014, within four metal levels (bronze, silver, gold, and platinum) for each of the 501 rating areas across 50 states and the District of Columbia. Tax credits reduced premiums by approximately 76 percent, on average, for individuals who selected plans in the FFM with tax credits. Competition, as measured by the number of issuers in a rating area, was associated with more affordable benchmark plans (the second-lowest cost silver plan).

A central feature of the Affordable Care Act1 is the establishment of the Health Insurance Marketplace (“Marketplace”) where consumers can purchase health insurance plans in a competitive market. Consumers may be eligible for financial assistance to offset the cost of premiums, if their income meets certain requirements.2 Since October 1, 2013, over eight million Americans have selected a private health insurance plan through the Marketplace, the vast majority of whom are receiving financial assistance—making coverage even more affordable.3

As an initial step to understanding how the Marketplace is working in its first year of operation, and in looking forward to future years, we provide an overview of health insurance plan premiums available in the Marketplace and the important role of the advanced premium tax credit (“tax credit”) in helping families afford coverage. We analyze data on the change in the premium cost associated with the tax credit for Marketplace plan selections that were made through the Federally-facilitated Marketplace (FFM) during the initial open enrollment period.

Also, we examine over 19,000 Marketplace plans4 for 2014, within the four metal levels (bronze, silver, gold, and platinum)5 for each of the 501 rating areas across 50 states and the District of Columbia.6 Our analysis shows how differences in plan and market characteristics are associated with differences in premiums across the nation.

Research Brief Highlights

Marketplace Plan Choices and the Impact of Advanced Premium Tax Credits on

Premiums:

- Individuals who selected plans in the FFM with tax credits7 have a post-tax credit premium that is 76 percent less than the full premium, on average, as a result of the tax credit—reducing their premium from $346 to $82 per month.

- 69 percent of individuals selecting plans with tax credits in the FFM have premiums of $100 or less after tax credits—nearly half (46 percent) have premiums of $50 or less after tax credits.

- Individuals choosing silver plans in the FFM tended to select lower premium plans—65 percent chose the lowest or second-lowest cost silver plan.

Overview of the 2014 Health Insurance Marketplace and the Association Between Competition, Other Market Factors, and Variation in Premiums:

- Most individuals had a wide range of health plan choices. Eighty-two percent of people eligible to purchase a qualified health plan live in rating areas with 3 to 11 issuers in the Marketplace; 96 percent live in rating areas with 2 to 11 issuers in the Marketplace.

- Competition, as measured by the number of issuers in a rating area, is associated with more affordable benchmark plans (the second-lowest cost silver plan) for individuals and reduced costs for the federal government. An additional issuer in a rating area is associated with a 4 percent lower benchmark premium.

- Areas with a greater number of issuers also tend to offer a wider range of choices among plan types (e.g. PPOs, HMOs, CO-OP) to better meet consumers’ preferences and financial needs.

1 The Patient Protection and Affordable Care Act, Pub. L. 111-148, was enacted on March 23, 2010; the Health Care and Education Reconciliation Act of 2010, Pub. L. 111-152, was enacted on March 30, 2010. In this research brief, we refer to the two Acts collectively as the Affordable Care Act.

2 The type of financial assistance offered is known as “The Premium Tax Credit (PTC)” and is calculated as the difference between the cost of the adjusted monthly premium for the second-lowest cost silver with respect to the applicable taxpayer and the applicable percentage determined by household income that a person is statutorily required to pay. An individual may choose to have all or a portion of the PTC paid in advance to an issuer of a qualified health plan to reduce their monthly premiums. This is referred to as the “Advance Premium Tax Credit” (APTC). APTCs are provided to people with projected household income between 100 percent (133 percent in states that have chosen to expand their Medicaid programs) and 400 percent of the Federal Poverty Level (FPL). A reconciliation of the APTC paid on behalf of an individual or family and the PTC they are eligible for will occur during their annual tax return. If an individual receives a greater APTC than the PTC they are determined eligible for, the individual may be required to repay the difference. The applicable percentage that a qualified individual or family will pay toward a health insurance premium will range from 2.0 percent of income at 100 percent FPL to 9.5 percent of income at 400 percent FPL.

3 For more information, see the Marketplace Summary Enrollment Report, which can be accessed at http://aspe.hhs.gov/health/reports/2014/MarketPlaceEnrollment/Apr2014/i….

4 A Marketplace plan is a qualified health plan (QHP) that has been certified to be offered in a Marketplace. A health insurance issuer may offer multiple Marketplace plans. For example, a silver plan and a bronze plan from one health insurance issuer would be counted as two Marketplace plans. Catastrophic plans were not counted toward this total. This analysis also excludes Virginia plans that required coverage of bariatric surgery as these were extreme price outliers.

5 The Affordable Care Act requires that Marketplace plans must be one of four tiers, or “metal levels,” based on actuarial value (AV) (Catastrophic plans are exempt from this requirement). Section 1302(d)(2)(A) of the Affordable Care Act stipulates that AV be calculated based on the provision of essential health benefits (EHB) to a standard population. The statute groups the plans into four tiers: bronze, with an AV of 60 percent; silver, with an AV of 70 percent; gold, with an AV of 80 percent; and platinum, with an AV of 90 percent. The final rule implementing the calculation of AV establishes that a de minimis variation of +/- 2 percentage points of AV is allowed for each tier.

6 Plan and premium data were taken from the following publicly available sources: Healthcare.gov, state rate filings (where available), and State-based Marketplace websites.

7 Represents individuals who have selected a Marketplace plan with a non-zero tax credit.

I. The Impact of Advanced Premium Tax Credits on Consumer Share of Premiums

Section I Highlights

Marketplace Plan Selection Choices and Premiums:

- Individuals who selected Marketplace plans with tax credits through the FFM have a post-tax credit premium that is 76 percent less than the full premium amount, on average, as a result of premium tax credits.

- 69 percent of individuals who selected Marketplace plans with tax credits in the FFM had premiums of $100 or less after tax credits—46 percent had premiums of $50 or less after tax credits.

- Individuals choosing silver plans in the Federally-facilitated Marketplace (FFM) tended to select lower premium plans—65 percent chose the lowest or second-lowest cost silver plan.

During the initial open enrollment period more than 5.4 million people selected a Marketplace plan through the Federally-facilitated Marketplace (FFM). This section utilizes data on these individuals and their plan selections in the 36 FFM states to assess the impact of tax credits on consumers’ premiums. Comparable data for SBM states are not available. In the FFM, 87 percent of the individuals who selected a Marketplace plan during the initial open enrollment period selected a plan with tax credits.8

8 This estimate is based on FFM plan selections through 5/12/2014. Data presented in the Marketplace Summary Enrollment Report is based on plan selections through 4/19/2014. For more information, the Marketplace Summary Enrollment Report can be accessed at: http://aspe.hhs.gov/health/reports/2014/MarketPlaceEnrollment/Apr2014/ib...

Advance Premium Tax Credit Basics

The Affordable Care Act caps the amount that individuals who are eligible for advance premium tax credits must pay toward obtaining “benchmark” coverage through the Marketplace; benchmark coverage is defined as the second-lowest cost silver plan available in the Marketplace to that individual. Individuals with family incomes between 100 percent (133 percent in states that have chosen to expand their Medicaid programs) and 400 percent of the FPL must pay only a specified percentage of their income for benchmark coverage. This maximum percentage increases with income, so lower-income individuals receive a larger tax credit toward their purchase of Marketplace coverage.

While the second-lowest cost silver plan is designated as the benchmark for determining the amount of the tax credit, an individual may apply her tax credit toward a Marketplace plan from any metal level (excluding catastrophic). In some cases, the tax credit amount may even exceed a plan’s price, resulting in a plan that costs the enrollee $0 after tax credits.

To calculate the premium tax credit amount, the Affordable Care Act specifies that an individual or family with a particular income will pay a fixed percentage of their income for the second-lowest cost silver plan available in the Marketplace in their local area (see Table 1). This is a fixed percentage, expressed as a percentage of the federal poverty level (FPL), without regard to age or the actual premiums in the Marketplace. For example, the law specifies that a single individual earning 150 percent of the FPL, or $17, 235 per year, will pay no more than 4 percent of her income ($57 per month) for the second-lowest cost silver plan. Her tax credit will cover the difference between $57 and the monthly cost of the second-lowest cost silver plan available to her. Table 1 shows the percent of income and maximum payment associated with various incomes for single individuals.

For example, the amount that a 27-year-old woman with an income of $25,000 (218 percent of the FPL) would pay for the second-lowest cost silver plan is capped at $145 per month. If she lived in Jackson, Mississippi, the premiums for the second-lowest cost silver plan available would cost her $336 per month before tax credits. Therefore, the amount of the premium tax credit would be $191 per month—the difference between specified contribution to the benchmark plan and the actual cost of the benchmark plan. Her use of the tax credit would not be restricted to the second-lowest cost silver plan. She could apply the $191 per month tax credit toward any plan of her choosing in any metal level. By applying her tax credit to the lowest-cost bronze plan in Jackson, which is priced at $199 per month, she could obtain Marketplace coverage for just $8 per month after tax credits.

TABLE 1 Examples of Maximum Monthly Health Insurance Premiums for the Second-Lowest Cost Silver Plan for a Single Adult, by Income9

| Single Adult Income10 | Percent of the Federal Poverty Level | Maximum Percent ofIncome Paid toward Second-Lowest Cost Silver Plan | Maximum Monthly Premium Payment for Second-Lowest Cost Silver Plan |

|---|---|---|---|

| $11,49011 | 100% | 2.0% | $19 |

| $17,235 | 150% | 4.0% | $57 |

| $22,980 | 200% | 6.3% | $121 |

| $28,725 | 250% | 8.05% | $193 |

| $34,470 | 300% | 9.5% | $273 |

| $40,215 | 350% | 9.5% | $318 |

| $46,075 | 401% | None | No Limit |

9 For more information, see the Internal Revenue Service final rule on “Health Insurance Premium Tax Credit” (Federal Register, May 23, 2012, vol, 77, no. 100, p. 30392; available at: http://www.gpo.gov/fdsys/pkg/FR-2012-05-23/pdf/2012-12421.pdf) and the 2013 federal poverty guidelines (available at:

http://aspe.hhs.gov/poverty/13poverty.cfm).

10 Income examples are based on the federal poverty guidelines for the continental United States. The FPL percentages in Column 2 correspond to higher income amounts in Alaska and Hawaii.

11 In Medicaid expansion states, an individual at 133 percent of the FPL may be Medicaid eligible, rather than eligible for tax credits in the Marketplace.

The Health Insurance Marketplace: Choice and Competition

One aim of the Affordable Care Act is to promote competition in the individual health insurance market to improve the coverage, quality, choices, and affordability of premiums available for purchase. The Affordable Care Act eliminated the ability of issuers to use medical underwriting to establish premiums for most new plans in the individual and small group market, and required issuers to accept all applicants for non-grandfathered coverage, regardless of health status. The new Marketplace facilitates comparison shopping, and those who qualify can also receive financial assistance to help pay for coverage. As a result, consumers now have greater opportunities to find affordable health plans that fit their preferences regarding premiums and type of coverage.

The Marketplace represents a new market environment that will evolve over time and there are different theories on how competition will work in this setting. The simplest view of competition suggests that as the number of issuers increase in a market, premium rates should decline. A more nuanced view of competition suggests a more varied set of outcomes. In that view health plans are not identical and their different features are valued differently by different consumers. This creates customer loyalty to plans that, in turn, means issuers of those plans can exert some limited control over the premiums they charge. A potential outcome of this type of competition is that rating areas with a larger number of issuers13 may exhibit a greater variety of plan types being offered and a corresponding wider variety of premiums relative to markets with fewer issuers. In this brief, we examine these potential effects by using a number of premium measures by rating area to assess the effects of larger numbers of issuers.

13 A health insurance issuer is a company that may offer multiple Marketplace plans. For example, a hypothetical Blue Cross and Blue Shield licensed company would be a health insurance issuer, while its $2000 deductible silver plan would be a Marketplace plan. An enrollee may have fewer issuers participating in his or her rating area than the total number participating in that state, because issuers are not required to offer a Marketplace plan in every rating area.

Advance Premium Tax Credit Reduces Monthly Consumer Premiums

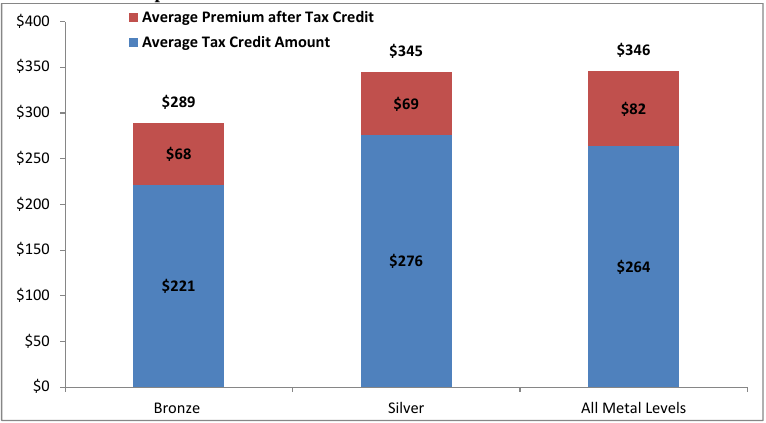

Table 2 and Figure 1 show the impact of the tax credit on the monthly premiums for consumers who selected Marketplace plans with tax credits in the FFM (see Appendix for state-level estimates).12 Approximately 87 percent of individuals in the FFM selected plans with tax credits and these individuals have post-tax credit premiums that are 76 percent less than the full premium, on average. The average premium before tax credits for persons selecting Marketplace plans of any metal level with tax credits through the FFM was $346. The average tax credit amount was $264 and the after-tax credit premium was $82. The tax credit for people who selected silver plans resulted in the highest percent reduction in premiums after tax credits (80 percent) relative to the persons selecting plans from the other three metal levels. Persons who selected bronze plans had the next highest percent reduction in premiums after tax credits (76 percent), followed by persons who selected gold and platinum plans—51 percent for both. However, it is important to note that people selecting bronze plans are not eligible for cost-sharing reductions, so consumers selecting bronze plans may be trading off a lower premium at the time of purchase for higher cost sharing at a later date.

The tax credit also helped many individuals select Marketplace plans for less than $100 per month. Table 3 and Figure 2 show the percent of individuals whose premiums fell into one of several categories after tax credits (see Appendix for state-level estimates). Of all individuals who selected a Marketplace plan with tax credits through the FFM, 82 percent selected plans with a monthly premium of $150 or less after tax credits, 69 percent with a premium of $100 per month or less after tax credits, and 46 percent with a premium of $50 or less after tax credits. While the average premium before tax credits across all metal levels was $346 for selected Marketplace plans with tax credits, only 18 percent of plan selections with tax credits have premiums that cost more than $150 on average after tax credits.

TABLE 2 Average Monthly Premiums before and after Tax Credits, Tax Credit Amount, and Percent Reduction in Premium after Tax Credits for Individuals Who Selected Plans with Tax Credits through the 2014 Federally-facilitated Marketplace

| Metal Level | Percent of Individuals WhoSelected Plans With Tax Credits | Average Premium before TaxCredits | Average Tax Credit Amount | Average Premium after Tax Credits | Average Percent Reduction in Premium after Tax Credits |

|---|---|---|---|---|---|

| Bronze | 73% | $289 | $221 | $68 | 76% |

| Silver | 94% | $345 | $276 | $69 | 80% |

| Gold | 65% | $428 | $220 | $208 | 51% |

| Platinum | 64% | $452 | $232 | $220 | 51% |

| All Metal Levels | 87% | $346 | $264 | $82 | 76% |

Source: ASPE computations of CMS Federally-facilitated Marketplace data as of 5/12/2014.

*Calculated as the number of individuals who selected Marketplace plans with tax credits as a percentage of all individuals who selected a Marketplace plan.

FIGURE 1: Average Monthly Tax Credit Amount and Premiums after Tax Credits by Metal Level for Individuals Who Selected Plans with Tax Credits, 2014 Federally-facilitated Marketplace

Source: ASPE computations of CMS Federally-facilitated Marketplace data as of 5/12/2014.

TABLE 3 Percent of Marketplace Plan Selections by Selected Monthly Premium Amounts After Tax Credits for Individuals Who Selected Plans with Tax Credits, 2014 Federally-facilitated Marketplace

| Monthly Premiums After Tax Credits | Percent of Marketwith Tax Creditsplace Plan Selections Through the FFM | |

|---|---|---|

| % | Cumulative % | |

| $50 or Less | 46% | 46% |

| $51 to $100 | 23% | 69% |

| $101 to $150 | 13% | 82% |

| Greater than $150 | 18% | 100% |

Source: ASPE computations of CMS Federally-facilitated Marketplace data as of 5/12/2014.

Note: Represents distribution of monthly Marketplace plan selections across bronze, silver, gold, and platinum metal levels.

FIGURE 2: Distribution of Marketplace Plan Selections by Monthly Premiums after Tax Credits at Selected Amounts for Individuals Who Selected Plans with Tax Credits, 2014 Federally-facilitated Marketplace

Source: ASPE computations of CMS Federally-facilitated Marketplace data as of 5/12/2014.

Note: Represents distribution of monthly Marketplace plan selections across bronze, silver, gold, and platinum metal levels.

12 The analyses presented in Tables 2 and 3 and Figures 1 and 2 are based on plan selections of people with non-zero tax credits, who self-identified as non-tobacco users, and those who selected a bronze, silver, gold, or platinum metal level plan. Catastrophic plans were not included as these plans are not eligible for tax credits. Table 4 and Figure 3 include all individuals who selected a plan through the FFM.

Consumer Selections Based on Price

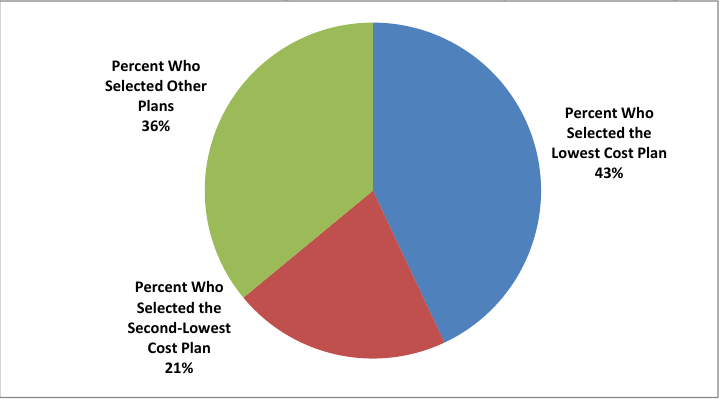

Analysis of data on FFM plan selections reveals that within each metal level, individuals tended to select the plans with the lowest premiums (see Table 4 and Figure 3). Within the FFM, the lowest or second-lowest plan accounted for 60 percent or more of plan selections in the bronze, silver and platinum metal levels, 54 percent in the gold metal level, and 93 percent in the catastrophic level. For the silver level, 22 percent of Marketplace plan selections were for the benchmark plan (the second-lowest cost silver plan), while 43 percent were for the lowest cost silver plan and 35 percent were for silver plans at other premium price levels. On average, consumers had 16 silver plans per rating area to choose from, ranging from a low of two silver plans to a maximum of 67 silver plans.

TABLE 4 Distribution of Marketplace Plan Selections within Metal Level and Plan Cost Rank for All Individuals Who Selected Marketplace Plans, 2014 Federally-facilitated Marketplace

| Metal Level | Percent Who Selected the Lowest or Second-Lowest Cost Plan | Percent Who Selected the Lowest Cost Plan | Percent Who Selected the Second- Lowest Cost Plan | Percent Who Selected Other Plans |

|---|---|---|---|---|

| Bronze | 60% | 39% | 21% | 40% |

| Silver | 65% | 43% | 22% | 35% |

| Gold | 54% | 37% | 16% | 46% |

| Platinum | 69% | 50% | 19% | 31% |

| Catastrophic | 93% | 76% | 17% | 7% |

| Total Where Metal Level Is Known | 64% | 43% | 21% | 36% |

Source: ASPE computations of CMS Federally-facilitated Marketplace data as of 5/12/2014.

Note: The lowest and second-lowest plans are defined as the lowest cost Marketplace plan available in the rating area, even if that plan may not have a service area that covers the entire rating area. If multiple plans are tied for lowest (or second-lowest) in a metal level and rating area, then selections of those plans are all counted toward selection of the lowest (or second-lowest) plan.

FIGURE 3: Distribution of Marketplace Plan Selections by Plan Cost Ranking for All Individuals Who Selected Marketplace Plans, 2014 Federally-facilitated Marketplace

Source: ASPE computations of CMS Federally-facilitated Marketplace data as of 5/12/2014.

Note: The lowest and second-lowest plans are defined as the lowest cost Marketplace plan available in the metal level in the rating area, even if that plan may not have a service area that covers the entire rating area.

II. Overview of Premiums in the 2014 Individual Health Insurance Marketplace

Section II Highlights

Overview of Premiums for the Second-Lowest Cost Silver Plans:

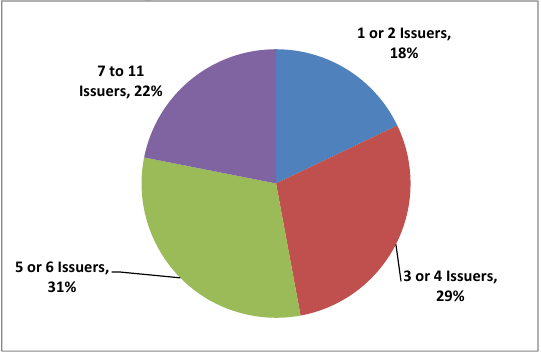

- 82 percent of people eligible to purchase a Marketplace plan live in rating areas with 3 to 11 issuers; 96 percent live in rating areas with 2 to 11 issuers.

- On average, consumers eligible to purchase a Marketplace plan can choose from 5 health plan issuers and 47 Marketplace plans across all metal levels—of which, approximately 16 are silver plans.

- The national average for the second-lowest cost silver plan premium rate is $226 per month for a 27-year-old, ranging between a low of $127 to a high of $406.

- Second-lowest cost silver plan premium rates were comparable for rating areas located in both Federally-facilitated Marketplace (FFM) and State-based Marketplace (SBM) states and those located in states that chose to expand their Medicaid programs under the Affordable Care Act and those states that did not choose to expand.

Rating areas are geographic markets where insurers compete on premiums and other factors for customers in the Marketplace. The number of rating areas14 varies by state from a low of one rating area in smaller states like Rhode Island or Vermont to a high of 67 rating areas in Florida—corresponding to each of Florida’s 67 counties. However, rating areas are often an aggregation of counties. On average, there are approximately 10 rating areas per state for the 50 states and the District of Columbia.

There were a total of 266 issuers by state15 offering Marketplace plans, ranging from a low of one issuer in New Hampshire and West Virginia to a high of 16 issuers in New York. New issuers16 represent almost 26 percent of all state issuers. Among the new entrants, the majority had a history as Medicaid issuers and now offer commercial coverage through the Marketplace. New entrants also include consumer-operated and oriented plans (CO-OPs) authorized by section1322 of the Affordable Care Act.17

On average, there are approximately five health plan issuers per rating area, ranging from one to 11 issuers. The rating areas with the most choice as measured by the number of issuers are located in New York and Oregon; the rating areas with the most choice as measured by the number of Marketplace plans available are located in Wisconsin and Florida. On average, consumers shopping in the Marketplace can choose from approximately 47 Marketplace plans.

TABLE 5 Summary of Rating Areas, Health Plans, and Health Plan Issuers by Rating Area or State, 2014 Health Insurance Marketplace

| Average | Minimum | Maximum | |

|---|---|---|---|

| Rating Areas per State | 10 | 1 | 67 |

| Marketplace Plans (excluding Catastrophic Plans) | 47 | 6 | 165 |

| Bronze Plans | 14 | 1 | 42 |

| Silver Plans | 16 | 2 | 67 |

| Gold Plans | 13 | 2 | 45 |

| Platinum Plans | 5 | 1 | 23 |

| Issuers | 5 | 1 | 11 |

Source: ASPE computations of plan and premium data from the following publicly available sources: Healthcare.gov, state rate filings (where available), and State-based Marketplace websites. Averages are weighted by the QHP-eligible18 population in each rating area estimated using the 2011 American Community Survey Public Use Microdata Sample.

As displayed on Figure 4, 82 percent of the people eligible to purchase a Marketplace plans live in rating areas with at least three issuers of Marketplace plans and 96 percent live in areas with at least two issuers. Fifty six percent can choose from plans offered by five or more issuers. This compares favorably with those covered by employer-sponsored insurance. One study found that approximately 46 percent of employees could choose from more than two issuers, while 25 percent had two issuer options, and the remaining 24 percent had only one issuer of plans from which to choose.19 In addition, prior to the implementation of the Marketplace, the individual market was dominated by one or two different issuers in most states. In 2012, 11 states had 85 percent of the individual market covered by the largest two issuers in the state. In 29 states, more than half of all enrollees in the individual market were covered by only one issuer and in 46 states (including DC)—two issuers covered more than half of the individual market.20

FIGURE 4: Percent of QHP-Eligible Population by Number of Issuers in a Rating Area, 2014 Health Insurance Marketplace

Source: Source: ASPE computations of plan and premium data from the following publicly available sources: Healthcare.gov, state rate filings (where available), and State-based Marketplace websites.

14 Rating areas are state-defined pricing regions for issuers. They overlap with the issuer service areas in many, but not all, cases. In general, the number of issuers or plans available in a rating area will be the number of choices available to all individuals and families living in that rating area. Issuers are not required to offer a Marketplace plan in every rating area within a state, however, so the number of available issuers and Marketplace plans varies by rating area. These totals exclude catastrophic plans, which are not available to all enrollees.

15 This is the number of unique issuer-state combinations nationally. For example, Aetna offers coverage in both Arizona and Florida, which is considered as two issuer-state combinations. Therefore, although Aetna is one company, it would be counted twice in the summation of issuer-state combinations for the total of 266 nationally.

16 New issuers are defined as issuers participating in the individual market for the first time in a given state.

17 The Consumer-Operated and Oriented Plan (CO-OP) program was created by the Affordable Care Act to provide support for the creation of nonprofit, member-controlled health insurance plans that offer ACA-compliant policies in the individual and small business markets.

18 For the purposes of this analysis, we define “QHP eligible” as U.S. citizens and others lawfully present who have only individual market coverage or are uninsured and have incomes that are: above 133 percent of the FPL for adults in Medicaid expansion states; above 100 percent of the FPL for adults in non-expansion states; and above 250 percent of the FPL for children (age 0-18) in all states. These estimates do not take into account the eligibility requirements relating to other minimum essential coverage.

19 Meredith B. Rosenthal, Bruce E. Landon, Sharon-Lise T. Normand, Richard G. Frank, Thaniyyah S. Ahmad, Arnold M. Epstein. 2007. “Employer’s Use of Value-Based Purchasing Strategies.” JAMA. 2007 Nov 21. 298(19):2281-8.

20 The White House, "Early Results: Competition, Choice, and Affordable Coverage in the Health Insurance Marketplace in 2014,” Available at: http://www.whitehouse.gov/sites/default/files/private/docs/competition_memo_5-30... .

Variation in Premiums—Second-Lowest Cost Silver Plan Premium by Rating Area

We are interested in understanding the pattern of premium levels across rating areas. There are several premium measures that might be used in order to analyze variation in premiums across rating areas. In this brief we study differences with respect to a benchmark premium (the second-lowest cost silver plan premium in a rating area), all premiums and a measure of premium dispersion (coefficient of variation). 21 One rationale for choosing to focus on the second-lowest cost silver plan premium is that it is the benchmark used to determine premium tax credits. If premiums for second-lowest cost silver plans are lower, the cost of tax credits will also be lower, saving taxpayers money.22 In addition, evidence from other insurance markets suggests that lower-cost plans may be of particular importance to consumers.23,24 Notably, the majority (65 percent) of people who selected a Marketplace plan during the initial open enrollment period selected a silver plan.25

In most states, premium rates differ according to a person’s age (at the time of the policy’s effective date). In contrast, New York and Vermont do not permit age rating, meaning that an individual’s premium is not dependent upon the individual’s age. In other words, a 21-year-old in New York or Vermont would pay the same rate as someone who is 64-years-old, despite the difference in age.

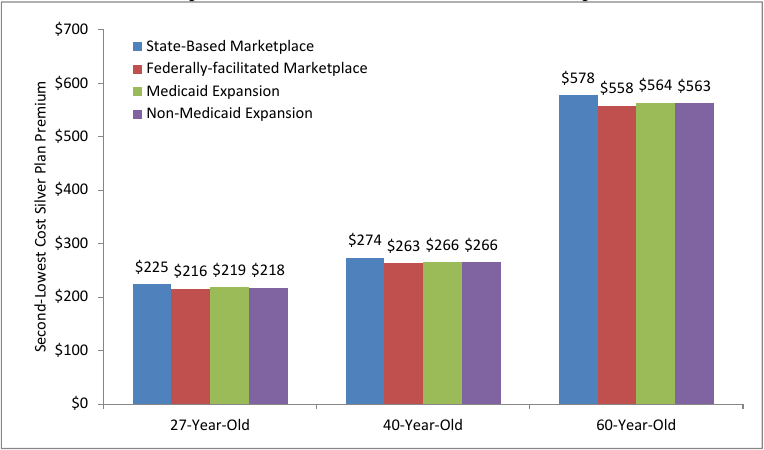

Table 6 presents the average second-lowest cost silver plan premium by selected ages across rating areas. The average second-lowest silver plan premium for a 27-year-old individual is approximately $226 per month before tax credits and drops to $219 per month (3 percent) when New York and Vermont, which do not age rate, are excluded from the calculation. A 27-year-old iving in rating area 8 in Minnesota (which includes 11 counties in the greater Minneapolis area) can purchase the second-lowest cost silver plan for $127 a month—almost half the national average. As a point of comparison, in 2013, statewide premiums averaged across covered employees of all ages in the small group market were approximately $446 per month in Minnesota.26

Figure 5 shows the average second-lowest cost silver plan premium by selected ages and rating areas grouped by Marketplace type (FFM or SBM) and state decisions to expand their Medicaid programs or not. By the end of the initial open enrollment period (March 31, 2014), 25 states and the District of Columbia had chosen to expand their Medicaid programs under the ACA, including all 15 SBM states and 11 of the 36 FFM states.28 The premiums are comparable between the rating areas based on market type and the decision by a state to expand or not to expand its Medicaid program under the Affordable Care Act.

TABLE 6 Second-Lowest Cost Silver Plan Monthly Premiums (before Tax Credits)* by Selected Ages and Rating Area, 2014 Health Insurance Marketplace

| Average (NY & VT Included) | Average (NY & VT Excluded) | Minimum (NY & VT Excluded) | Maximum (NY & VT Excluded) | |

|---|---|---|---|---|

| 27-Year-Old | $226 | $219 | $127 | $406 |

| 35-Year-Old | $260 | $254 | $148 | $474 |

| 40-Year-Old | $271 | $266 | $154 | $496 |

| 50-Year-Old | $371 | $371 | $215 | $693 |

| 60-Year-Old | $572 | $584 | $335 | $1,136 |

Source: ASPE computations of plan and premium data from the following publicly available sources: Healthcare.gov, state rate filings (where available), and State-based Marketplace websites. Averages are weighted by the QHP-eligible population in each rating area estimated using the 2011 American Community Survey Public Use Microdata Sample.

*These premiums represent the premiums before the application of tax credits. Of those consumers who purchased plans through the Marketplace, 85 percent selected plans with financial assistance.27

FIGURE 5: Second-Lowest Cost Silver Plan Premium by Age Group, Marketplace Type, and State Medicaid Expansion Status, 2014 Health Insurance Marketplace

Source: ASPE computations of plan and premium data were taken from the following publicly available sources: Healthcare.gov, state rate filings (where available), and State-based Marketplace websites. The national average is weighted by the QHP-eligible population in each rating area estimated using the 2011 American Community Survey Public Use Microdata Sample. Second-lowest cost silver plan premiums for rating areas in New York (nine rating areas) and Vermont (one rating area), which do not establish premium rates based on age, were excluded from the analysis.

21 The coefficient of variation is a normalized measure of dispersion defined as the ratio of the standard deviation to the mean. Here it is used to measure the dispersion in premiums within a rating area.

22 As premiums decline, the amount of public funds needed to subsidize consumers also declines.

23 Leemore Dafny, Jonathan Gruber, and Christopher Ody. “More Insurers Lower Premiums: Evidence from Initial Pricing on the Health Exchanges.” NBER Working Paper No. 20140. May 2014.

24 Keith M. Ericson and Amanda Starc. “Heuristics and Heterogeneity in Health Insurance Exchanges: Evidence from the Massachusetts Connector.” American Economic Review, 2012. 102(3) 493-97.

25 The Department of Health and Human Services, Office of the Assistant Secretary for Planning and Evaluation, May 1, 2014, “Health Insurance Marketplace: Summary Enrollment Report for the Initial Annual Open Enrollment Period,” http://aspe.hhs.gov/health/reports/2014/MarketPlaceEnrollment/Apr2014/ib...

26 John Holahan. “Will Premiums Skyrockets in 2015?” In-Brief: Timely Analysis of Immediate Health Policy Issues. The Robert Wood Johnson Foundation/Urban Institute. May 2014

27 Represents individuals who have selected a Marketplace plan, and qualify for an advance premium tax credit (APTC), with or without a cost-sharing reduction (CSR) from: The Department of Health and Human Services, Office of the Assistant Secretary for Planning and Evaluation, May 1, 2014, “Health Insurance Marketplace: Summary Enrollment Report for the Initial Annual Open Enrollment Period,” http://aspe.hhs.gov/health/reports/2014/MarketPlaceEnrollment/Apr2014/ib....

28 These numbers represent the status of states regarding FFM, SBM, and Medicaid expansion decisions for the time of the initial open enrollment period. A FFM state is one in which the Marketplace is administrated by the Federal government, and a SBM is one in which the state opted to create and operate its own Marketplace. Here we include states that are a hybrid of the FFM and SBM, a State Partnership Marketplace (SPM) in the FFM group of states. For

current information on the sates regarding Medicaid expansion decisions see http://www.medicaid.gov/AffordableCareAct/Medicaid-Moving-Forward-2014/D... .

III. Competition, Other Market Factors, and Second-Lowest Cost Silver Plan Premiums

Section III Highlights

The Association Between Competition, Other Market Factors, and Second-Lowest Cost Silver Plan Premiums:

- The number of issuers in a rating area was associated with lower premiums among the second-lowest cost silver plans.

- On average, an increase of one issuer in a rating area is associated with a 4 percent decline in the second-lowest cost silver plan premium.

In order to more carefully examine the sources of variation in second-lowest cost silver plan premiums among rating areas, we applied statistical models to obtain estimates of the association between second-lowest cost silver plan premiums for selected ages and a number of Marketplace characteristics. Our primary indicator of competition is the number of issuers in a rating area. We also examine the percent of all issuers that were defined as “established,” meaning that they issued a policy in the private individual market within the state during 2012 and 2013. Such issuers may have greater knowledge of the area or have established provider markets that allow them to charge a lower premium; or, on the other hand, they may have a loyal customer base that

is willing to accept higher premiums. We also included a variable to reflect a specific type of issuer—the consumer operated and oriented plan issuers (CO-OP). The consumer operated and oriented plan program was established to foster the creation of qualified nonprofit health insurance issuers to offer competitive health plans in the individual and small group markets. We expect the presence of a CO-OP in a rating area to have a negative association with the second-lowest cost silver plan premium.

In addition, we use a measure of hospital market concentration, the Herfindahl-Hirschmann Index (HHI),29 in our statistical models. Since more concentrated hospital markets could result in higher prices for hospital services, insurance premiums may be higher in these rating areas relative to those with less concentrated hospital markets. Since we focus on premiums within age bands, a variable was included to denote market areas in New York and Vermont, which are the only two states that do not permit setting premium rates based on age. Other market characteristics included an indicator of a Federally-facilitated Marketplace, an indicator of a Medicaid expansion state, the percent of the rating area population that is uninsured, the log of state health care expenditures, and the log of the rating area population density. We used three different model specifications in order to investigate the association between premiums and both an alternative measure of health expenditures and the exclusion of health expenditure measures from the model.30

Results indicate that the premiums are negatively correlated with the number of issuers (see Table 7). Specifically, an increase of one issuer in a rating area is associated with a decrease of approximately 4 percent in the second-lowest cost silver plan premium for a 27-year-old individual.31 These results are consistent with recent findings using a somewhat different approach that also found that greater competition reduced second-lowest cost silver plan

premiums in 2014.32 In addition, a greater percent of established issuers in a state is associated with lower premiums—approximately a 2 percent reduction in second-lowest cost silver premiums for each 10 percentage point increase in the percent of all issuers that were established issuers. However, this finding was not statistically significant for all model specifications shown in Table 7. The hospital market concentration did not have a statistically significant association with the second-lowest cost silver plan premium.

TABLE 7 Linear Regression Model Results of the Association Between Second-Lowest Cost Silver Plan Premiums, the Number of Issuers, and Other Marketplace Characteristics, by Rating Area, 2014 Health Insurance Marketplace

| Log of the SeconFord-Lowest Cost Silve a 27-Year-Old (N=r Plan Premiums 494) | |||

|---|---|---|---|

| Model 1 | Model 2 | Model 3 | |

| Market Characteristics by Rating Area | Coefficient (P-Value) | Coefficient (P-Value) | Coefficient (P-Value) |

| Number of Issuers | -0.04 (<0.001) | -0.04 (<0.001) | -0.04 (<0.001) |

| Percent of Established Issuers | -0.19 (0.03) | -0.22 (0.11) | -0.14 (0.19) |

| CO-OP (1,0) | -0.03 (0.48) | -0.05 (0.30) | -0.02 (0.63) |

| FFM State (1,0) | -0.09 (0.23) | -0.05 (0.51) | -0.08 (0.27) |

| Medicaid Expansion State (1,0) | 0.00 (0.83) | 0.01 (0.81) | -0.01 (0.85) |

| Full Community Rating State (1,0) | 0.55 (<0.001) | 0.50 (<0.001) | 0.56 (<0.001) |

| Log of Hospital Market Concentration (HHI) | -0.01 (0.78) | 0.01 (0.73) | -0.00 (0.98) |

| Percent Uninsured Population | 0.18 (0.57) | 0.13 (0.72) | 0.09 (0.79) |

| Log of State-Level Health Care Expenditures | 0.54 (0.001) | NA | NA |

| Log of State-Level Small Group Premiums | NA | 0.56 (0.01) | NA |

| Log of Population Density | -0.01 (0.41) | -0.01 (0.63) | -0.00 (0.80) |

| Constant | 1.32 (0.28) | 0.94 (0.59) | 5.73 (<0.001) |

| F-Statistic | 60.57 (<0.001) | 114.93 (<0.001) | 105.66 (<0.001) 0.26 |

| R2 | 0.32 | 0.31 | 0.26 |

Source: ASPE computations of plan and premium data from the following publicly available sources: Healthcare.gov, state rate filings (where available), and State-based Marketplace websites.

NOTE: Other model specifications included using the second-lowest cost silver plan premiums for 35, 40, 50, and 60-year-olds as the dependent variable, respectively. Results were consistent across different specifications.

29 The HHI refers to the Herfindahl-Hirschmann Index which is the standard measure used in economic analysis of market competition and is computed as the sum of squared market shares in the market. The HHI ranges from 0 indicating perfect competition to 10,000 indicating monopoly. The Department of Justice and the Federal Trade Commission guidelines define a market as “highly concentrated” if the HHI exceeds 2500.

30 Variations of the final model use as the dependent variable the logged values of the second-lowest cost silver premiums for ages 27, 35, 40, 50, and 60 with consistent results across these different model specifications. The model is a multivariate linear regression model utilizing the cluster option in Stata to produce robust standard errors that take into account the potential that premiums in rating areas within a state may not be independent of each other. State-level health care expenditures were estimated using Truven MarketScan Commercial Claims and Encounters Database for 2012 and the average state-level small group premiums were taken from the Agency for Healthcare Research and Quality, Center for Financing, Access and Cost Trends, 2012 Medical Expenditure Panel Survey-Insurance Component, Table II.C.1, “Less than 50 Employees.”

31 The observed association may also reflect other factors which we could not currently measure, such as the extensiveness of provider networks. Our cross-sectional analysis implies association and not causality.

32 Leemore Dafny, Jonathan Gruber, and Christopher Ody. “More Insurers Lower Premiums: Evidence from Initial Pricing on the Health Exchanges.” NBER Working Paper No. 20140. May 2014.

IV. Competition, Other Market Factors, and Different Measures of Marketplace Premiums

Section IV Highlights

The Association Between Competition, Other Market Factors, and All Marketplace Premiums

- The absolute number of issuers within a rating area did not, on average, have a significant association with the average premium for 27-year-olds for all plans by metal level (bronze, silver, gold, and platinum). In part, this difference may be due to markets with ore issuers exhibiting greater variability in premiums—that is, these markets had both higher and lower premiums within each metal level.

- Consumers had a wider choice of plan types in areas with more issuers. The variability in premiums associated with a greater number of issuers was in part related to these rating areas being more likely to have the full range of plan types including; CO-OPs, HMOs and plans issued by insurers offering Medicaid plans in the market prior to Marketplace implementation.

- CO-OPs and HMOs exhibited significantly lower premiums than other plan types.

- Areas that had more concentrated hospital markets (higher HHI) exhibited higher average premiums.

- A higher percentage of established issuers in a state was associated with lower premiums at each metal level.

In the preceding analyses, we examined factors that were associated with variation in one measure of market premiums (the second-lowest cost silver plan) across rating areas. In order to conduct a more complete analysis, we examined factors that affected the full range of Marketplace premiums in all four metal levels. In our initial models of the second-lowest cost silver plan premium, we also examined similar statistical models, replacing the second-lowest cost silver plan premium with both the average and median silver plan premiums for the rating area (not displayed in this Brief). In contrast to the results for the second-lowest cost silver plan premium, the number of issuers did not have an effect on either the mean or median silver plan premium. 33

To further examine these findings, we conducted several other analyses. Specifically, we examine the extent to which a greater number of issuers results in greater variation in plan types being offered in the rating area. A greater dispersion of premiums could mean that the lower premiums offered are offset, on average, by higher premium plans offered for particular plan types.

First, we examined models at the individual plan level rather than for the rating area. Hierarchal linear modeling techniques were utilized to examine the effect of market factors and competition on all premiums across all four metal levels (bronze, silver, gold and platinum).34 We present in the discussion and Table 8 the results related to premiums for 27-year-old individuals.

In addition to the results for the number of issuers, there are several other results of interest. These models included indicators for whether the plan was a PPO, HMO, CO-OP or other type of plan.35 As displayed in Table 8, the results suggest that premiums for HMO plans were lower on average than PPO, point of service (POS) and exclusive provider organizations (EPOs). In addition, CO-OP plans tended to have lower premiums than non-CO-OP plans within areas, which is consistent with the intent of their creation— to offer competitive health plans. Established issuers were also associated with lower bronze, silver, and gold premiums, but higher platinum plan premiums. As discussed previously, such issuers may have greater knowledge of the area or have established provider markets that allow them to charge a lower premium; or, on the other hand, they may have a loyal customer base that is willing to accept higher premiums. These results indicate that both of these dynamics may be in play for plans at varying metal levels.

Another important factor was the measure of hospital market concentration (HHI). While this variable was not associated with premium levels for the second-lowest cost silver plan premium, it does demonstrate a positive and statistically significant effect on the full range of premiums across all metal levels. This result supports the view that insurers likely have less price negotiating leverage in more concentrated hospital markets, resulting in higher premiums.

In the plan-level models, the number of issuers does not have a significant effect on premiums in any metal level. Thus, it appears that a greater number of issuers is associated with lower benchmark (second-lowest cost silver) plan premiums being offered, but is not related to the average of all premiums offered. Further statistical analyses offer a plausible explanation for this finding. We find that the variability in premiums increases with the number of issuers in a rating area. As displayed in Table 9, a common measure of variability—the coefficient of variation—increases with the number of issuers. This indicates that as the number of issuers increases, the number of plans offered also increases which leads to a greater dispersion of premiums. As the regression results in Table 10 demonstrate, the association between number of issuers and the coefficient of variation is statistically significant after removing the variation that might be attributable to other market factors. So, even while controlling for other factors that may contribute to the dispersion in premiums, the association between the number of issuers and premium dispersion remains.

The premium variation is in turn at least partly attributable to the plan types offered. The rating areas with more issuers are more likely to offer HMOs and CO-OP plans than those with only one issuer, while only areas that have four or more issuers offer the full range of plan types—corresponding to the dispersion of a full-range of premium rates (see Table 11). Consumers can expect more choice in plan types in markets with robust competition as measured by number of issuers participating.

TABLE 8 Hierarchical Linear Regression Model Results, Premiums for 27-Year-Olds by Plan and Metal Level, 2014 Health Insurance Marketplace

| Log of the Average Premiums for 27-Year-Olds By Metal Level | ||||

|---|---|---|---|---|

| Bronze (n=5,721) | Silver (n=6,896) | Gold (n=5,221) | Platinum (n=1,523) | |

| Market Characteristics by Plan | Coefficient(P-Value) | Coefficient (P-Value) | Coefficient (P-Value) | Coefficient (P-Value) |

| Number of Health Insurance Issuers | 0.00 (0.97) | -0.00 (0.36) | -0.00 (0.27) | 0.00 (0.46) |

| PPO Plan (1,0) | 0.11 (<0.001) | 0.09 (<0.001) | 0.10 (<0.001) | 0.05 (0.003) |

| HMO Plan (1,0) | -0.04 (<0.001) | -0.05 (<0.001) | -0.06 (<0.001) | -0.04 (0.001) |

| FFM State (1,0) | 0.02 (0.76) | 0.01 (0.93) | -0.02 (0.70) | 0.01 (0.95) |

| Medicaid Expansion State (1,0) | -0.00 (0.96) | -0.00 (0.93) | -0.02 (0.73) | -0.00 (0.96) |

| Full Community Rating State (1,0) | 0.52 (<0.001) | 0.50 (<0.001) | 0.49 (<0.001) | 0.58 (<0.001) |

| Established Issuers (1,0) | -0.08 (<0.001) | -0.08 (<0.001) | -0.07 (<0.001) | 0.06 (0.001) |

| Issuers Offering Medicaid Plans (1,0) | 0.06 (0.001) | 0.02 (0.17) | 0.02 (0.27) | -0.00 (0.95) |

| Issuers that are CO-OPs (1,0) | -0.09 (<0.001) | -0.05 (0.001) | -0.07 (<0.001) | -0.08 (0.02) |

| Log of Hospital Market Concentration (HHI) | 0.02 (0.04) | 0.02 (0.05) | 0.02 (0.01) | 0.05 (<0.001) |

| Constant | -0.19 (0.90) | 0.75 (0.59) | 0.43 (0.76) | -1.38 (0.58) |

| Wald (Х2) | 776.77 (<0.001) | 901.93 (<0.001) | 991.61 (<0.001) | 118.94 (<0.001) |

| Log Likelihood | 5,082.93 | 6,674.71 | 4,714.07 | 1,247.09 |

Source: ASPE computations of plan and premium data from the following publicly available sources: Healthcare.gov, state rate filings (where available), and State-based Marketplace websites.

*Other market characteristics for a rating area include the percent of the population that is uninsured, log of state health care expenditures, and the log of the population density.

NOTE: Other model specifications included: 1) excluding the log of state health care expenditures and 2) excluding the log of state health care expenditures and replacing it with the log of the average state small group premium. Results were consistent across specifications.

TABLE 9 Coefficient of Variation of Silver Plan Premiums for 27-Year-Olds, by Rating Area and Number of Issuers, 2014 Health Insurance Marketplace

| Number of Issuers | Coefficient of Variation |

|---|---|

| Only 1 Issuer | 0.06 |

| 2 or 3 Issuers | 0.09 |

| 4 to 6 Issuers | 0.12 |

| 7 to 11 Issuers | 0.15 |

Source: ASPE computations of plan and premium data from the following publicly available sources: Healthcare.gov, state rate filings (where available), and State-based Marketplace websites.

TABLE 10 Coefficient of Variation (CV) Regression Analysis Including the Number of Issuers and Other Market Characteristics,* Premiums for 27-Year-Olds by Rating Area and Metal Level, 2014 Health Insurance Marketplace

| CV Based on Premiums for 27-Year-Olds by Metal Level | ||||

|---|---|---|---|---|

| Bronze | Silver | Gold | Platinum | |

| Market Characteristics by Rating Area | Coefficient (P-Value) | Coefficient (P-Value) | Coefficient (P-Value) | Coefficient (P-Value) |

| Number of Health Insurance Issuers | 0.01 (<0.001) | 0.01 (<0.001) | 0.01 (<0.001) | 0.01 (<0.001) |

| Number of Observations (Rating Areas) | 483 | 494 | 494 | 205 |

| F-Statistic | 12.83 (<0.001) | 9.42 (<0.001) | 9.22 (<0.001) | 26.11 (<0.001) |

| R2 | 0.32 | 0.31 | 0.32 | 0.49 |

Source: ASPE computations of plan and premium data from the following publicly available sources: Healthcare.gov, state rate filings (where available), and State-based Marketplace websites.

*Other market characteristics for a rating area include established issuers as a proportion of all issuers, issuers offering Medicaid plans in the rating area prior to the implementation of the Marketplace as a proportion of all issuers, indicator that a CO-OP has plans available in the rating area, indicator of a Federally-facilitated Marketplace state, indicator of a Medicaid expansion state, indicator of a full-community rating state, log of the hospital HHI, the percent of the population that is uninsured, log of state health care expenditures, and the log of the population density.

TABLE 11 The Percent of Rating Areas with at Least One Silver Plan of Selected Types, by Number of Issuers, 2014 Health Insurance Marketplace

| The percent of rating areas with at least one silver plan that is one of the following types: | ||||

|---|---|---|---|---|

| HMO | CO-OP | Medicaid* | HMO, CO-OP, Medicaid | |

| Any Number of Issuers | 55% | 32% | 22% | 5% |

| Only 1 Issuer | 21% | 0% | 2% | 0% |

| 2 or 3 Issuers | 46% | 31% | 13% | 0% |

| 4 to 6 Issuers | 75% | 40% | 26% | 8% |

| 7 to 11 Issuers | 62% | 45% | 77% | 21% |

Source: ASPE computations of plan and premium data from the following publicly available sources: Healthcare.gov, state rate filings (where available), and State-based Marketplace websites.

*These are plans provided by issuers that were offering only Medicaid plans in the market prior to the implementation of the Marketplace.

33 Our results are comparable to those from Dafny, Gruber and Ody (2014) who found a relatively consistent relationship between their measure of competition and the second-lowest cost, mean, and median silver plan premiums in a rating area. While Dafny et. al. use the change in issuer HHI if United Healthcare had entered the 2014 Marketplace to test the effect of competition based on pre-Affordable Care Act shares of the individual market, in our analysis, we incorporate both the number of issuers and the proportion of issuers that had been established in the individual market prior to the implementation of the Marketplace. While we did not find a statistically significant association between the number of issuers and the mean and median silver plan premiums, it is notable that we find that established issuers generally offered lower premiums.

34 Hierarchical linear modeling (HLM) regression techniques are designed to deal with clustered or grouped data in which analytic units are naturally nested or grouped within other units of interest. For example, the number of Marketplace plans nested within issuer nested within rating area nested within state. Hierarchal linear models recognize the existence of such data hierarchies by allowing for residual components at each level in the hierarchy. In analyzing premiums of Marketplace plans being offered by issuers within a rating area, interest centers on the effects of plans, issuers, rating area, and state characteristics.

35 The reference group for the PPO and HMO variables consists of plans that are POS or EPO. For the CO-OP variable, the reference group is established issuers, including all commercial and Medicare plans.

V. Conclusion

The Affordable Care Act aims to improve consumer access to and choice of affordable coverage by promoting competition in the individual health insurance market and by providing financial assistance to consumers based on their income.

Premium affordability is enhanced by the advance premium tax credit—69 percent of the individuals who selected a plan with tax credits through the Marketplace have coverage that costs $100 or less a month in premiums after tax credits. Overall, individuals selecting plans with tax credits have premiums that are 76 percent less, on average, than the full premium before tax credits. Individuals selecting silver plans with tax credits experienced an 80 percent reduction in premiums due to the tax credits and have a monthly premium of $69, on average.

We find that consumers have, on average, five issuers and 47 Marketplace plans from which to choose when considering their options for coverage. Our analysis of second-lowest cost silver plan premiums indicates that in markets with more sellers there are lower premiums for the second-lowest cost silver plan. This analysis finds that each additional issuer is associated with a 4 percent decline in the second-lowest cost silver plan premium.

Areas with a greater number of issuers also tend to offer a wider range of choices for consumers among plan types (e.g. PPOs, HMOs, CO-OPs) that appear to result in greater variation in premiums across the rating areas, suggesting complex competitive interactions. If more issuers come into the Marketplace in future years, it seems likely not only that consumers will have a greater choice of plans, but also that the benchmark plan (second-lowest cost silver plan) will become even more affordable.

The findings in this brief represent early analyses for the first year of the Marketplace, and we expect this new, competitive health insurance market will continue to evolve.

Appendix

TABLE A1 Average Monthly Premiums Before and After Tax Credits, Tax Credit Amount, and Percent Reduction in Premium after Tax Credits for Individuals Who Selected Plans with Tax Credits through the 2014 Federally-facilitated Marketplace

| State | Average Premium after Tax Credits | Average Percent Reduction in Premium after Tax Credits | Average Premium before Tax Credits | Average Tax Credit Amount | Percent of Individuals Who Selected Plans with Tax Credits* |

|---|---|---|---|---|---|

| Alabama | $76 | 77% | $334 | $258 | 85% |

| Alaska | $94 | 81% | $507 | $413 | 88% |

| Arizona | $113 | 58% | $272 | $159 | 76% |

| Arkansas | $94 | 76% | $387 | $293 | 89% |

| Delaware | $130 | 67% | $392 | $263 | 81% |

| Florida | $68 | 80% | $347 | $278 | 91% |

| Georgia | $54 | 84% | $341 | $287 | 87% |

| Idaho | $68 | 75% | $276 | $207 | 91% |

| Illinois | $114 | 64% | $316 | $202 | 76% |

| Indiana | $88 | 79% | $424 | $336 | 89% |

| Iowa | $108 | 69% | $350 | $242 | 83% |

| Kansas | $67 | 77% | $290 | $223 | 78% |

| Louisiana | $83 | 79% | $397 | $314 | 88% |

| Maine | $99 | 78% | $443 | $344 | 89% |

| Michigan | $97 | 72% | $342 | $246 | 87% |

| Mississippi | $23 | 95% | $438 | $415 | 94% |

| Missouri | $59 | 83% | $344 | $286 | 85% |

| Montana | $99 | 71% | $345 | $246 | 85% |

| Nebraska | $94 | 69% | $308 | $214 | 87% |

| New Hampshire | $100 | 74% | $390 | $290 | 76% |

| New Jersey | $148 | 68% | $465 | $317 | 84% |

| New Mexico | $120 | 64% | $334 | $214 | 78% |

| North Carolina | $81 | 79% | $381 | $300 | 91% |

| North Dakota | $132 | 62% | $350 | $218 | 84% |

| Ohio | $121 | 67% | $372 | $250 | 84% |

| Oklahoma | $75 | 73% | $277 | $202 | 79% |

| Pennsylvania | $84 | 74% | $330 | $246 | 81% |

| South Carolina | $84 | 77% | $367 | $283 | 87% |

| South Dakota | $101 | 73% | $372 | $271 | 89% |

| Tennessee | $86 | 69% | $281 | $195 | 78% |

| Texas | $72 | 76% | $305 | $233 | 84% |

| Utah | $84 | 66% | $243 | $159 | 86% |

| Virginia | $77 | 77% | $331 | $254 | 82% |

| West Virginia | $113 | 73% | $415 | $302 | 85% |

| Wisconsin | $112 | 74% | $427 | $316 | 90% |

| Wyoming | $113 | 79% | $536 | $422 | 93% |

| All FFM States | $82 | 76% | $346 | $264 | 87% |

Source: ASPE computations of CMS Federally-facilitated Marketplace (FFM) data as of 5/12/2014.

*Calculated as the number of individuals who selected Marketplace plans with tax credits as a percentage of all individuals who selected a Marketplace plan.

TABLE A2 Average Monthly Silver Plan Premiums before and after Tax Credits, Tax Credit Amount, and Percent Reduction in Premium after Tax Credits for Individuals Who Selected Silver Plans with Tax Credits through the 2014 Federally-facilitated Marketplace

| State | Average Premium After Tax Credits | Average Percent Reduction in Premium after Tax Credits | Average Premium Before Tax Credits | Average Tax Credit Amount | Percent of Individuals Who Selected Plans with Tax Credits* |

|---|---|---|---|---|---|

| Alabama | $58 | 82% | $323 | $264 | 94% |

| Alaska | $82 | 85% | $531 | $449 | 95% |

| Arizona | $94 | 63% | $257 | $163 | 89% |

| Arkansas | $83 | 79% | $393 | $309 | 96% |

| Delaware | $103 | 73% | $378 | $275 | 91% |

| Florida | $50 | 85% | $340 | $290 | 98% |

| Georgia | $39 | 88% | $332 | $293 | 96% |

| Idaho | $54 | 80% | $274 | $220 | 97% |

| Illinois | $105 | 67% | $320 | $214 | 89% |

| Indiana | $86 | 81% | $441 | $355 | 94% |

| Iowa | $95 | 73% | $350 | $255 | 94% |

| Kansas | $50 | 83% | $289 | $239 | 93% |

| Louisiana | $68 | 83% | $401 | $332 | 97% |

| Maine | $87 | 81% | $452 | $365 | 95% |

| Michigan | $87 | 75% | $342 | $255 | 94% |

| Mississippi | $15 | 96% | $434 | $419 | 98% |

| Missouri | $45 | 87% | $347 | $302 | 96% |

| Montana | $78 | 78% | $347 | $269 | 95% |

| Nebraska | $79 | 74% | $309 | $230 | 94% |

| New Hampshire | $87 | 78% | $396 | $309 | 88% |

| New Jersey | $127 | 72% | $457 | $330 | 91% |

| New Mexico | $115 | 66% | $338 | $224 | 88% |

| North Carolina | $70 | 82% | $382 | $312 | 97% |

| North Dakota | $106 | 69% | $344 | $238 | 94% |

| Ohio | $111 | 70% | $372 | $261 | 92% |

| Oklahoma | $72 | 75% | $286 | $214 | 90% |

| Pennsylvania | $60 | 81% | $312 | $252 | 90% |

| South Carolina | $75 | 80% | $371 | $296 | 95% |

| South Dakota | $90 | 76% | $370 | $280 | 94% |

| Tennessee | $78 | 72% | $281 | $204 | 90% |

| Texas | $68 | 78% | $314 | $246 | 94% |

| Utah | $68 | 72% | $242 | $174 | 95% |

| Virginia | $66 | 80% | $338 | $272 | 94% |

| West Virginia | $89 | 78% | $407 | $317 | 93% |

| Wisconsin | $103 | 76% | $429 | $326 | 95% |

| Wyoming | $99 | 82% | $543 | $444 | 96% |

| All FFM States | $69 | 80% | $345 | $276 | 94% |

Source: ASPE computations of CMS Federally-facilitated Marketplace (FFM) data as of 5/12/2014.

*Calculated as the number of individuals who selected Marketplace plans with tax credits as a percentage of all individuals who selected a Marketplace plan.

TABLE A3 Distribution of Marketplace Plan Selections by Monthly Premiums after Tax Credits for Individuals Who Selected Plans with Tax Credits, 2014 Federally-facilitated Marketplace

| State | $50 or Less | $51 to $100 | $101 to $150 | Greater than $150 |

|---|---|---|---|---|

| Alabama | 53% | 20% | 11% | 16% |

| Alaska | 42% | 21% | 14% | 23% |

| Arizona | 26% | 32% | 17% | 25% |

| Arkansas | 35% | 30% | 15% | 19% |

| Delaware | 20% | 30% | 19% | 31% |

| Florida | 56% | 19% | 10% | 15% |

| Georgia | 60% | 19% | 10% | 11% |

| Idaho | 50% | 27% | 11% | 12% |

| Illinois | 25% | 31% | 18% | 26% |

| Indiana | 41% | 26% | 14% | 18% |

| Iowa | 29% | 28% | 19% | 25% |

| Kansas | 52% | 22% | 12% | 14% |

| Louisiana | 45% | 25% | 13% | 17% |

| Maine | 38% | 25% | 14% | 23% |

| Michigan | 39% | 24% | 15% | 23% |

| Mississippi | 68% | 17% | 7% | 7% |

| Missouri | 57% | 20% | 11% | 13% |

| Montana | 37% | 26% | 16% | 22% |

| Nebraska | 38% | 26% | 15% | 21% |

| New Hampshire | 38% | 24% | 15% | 23% |

| New Jersey | 20% | 25% | 17% | 38% |

| New Mexico | 20% | 30% | 21% | 29% |

| North Carolina | 48% | 23% | 12% | 16% |

| North Dakota | 15% | 31% | 21% | 33% |

| Ohio | 24% | 28% | 19% | 29% |

| Oklahoma | 47% | 27% | 13% | 13% |

| Pennsylvania | 47% | 21% | 12% | 20% |

| South Carolina | 45% | 25% | 13% | 17% |

| South Dakota | 34% | 27% | 16% | 23% |

| Tennessee | 42% | 28% | 14% | 16% |

| Texas | 50% | 24% | 12% | 14% |

| Utah | 36% | 33% | 17% | 15% |

| Virginia | 48% | 25% | 12% | 15% |

| West Virginia | 31% | 27% | 15% | 27% |

| Wisconsin | 32% | 25% | 16% | 27% |

| Wyoming | 33% | 21% | 15% | 30% |

| All FFM States | 46% | 23% | 13% | 18% |

Source: ASPE computations of CMS Federally-facilitated Marketplace (FFM) data as of 5/12/2014.

Note: Represents distribution of monthly Marketplace plan selections across bronze, silver, gold, and platinum metal levels.

TABLE A4 Cumulative Distribution of Marketplace Plan Selections by Monthly Premiums after Tax Credits for Individuals Who Selected Plans with Tax Credits, 2014 Federally-facilitated Marketplace

| State | $50 or Less | $100 or less | $150 or Less | All Plans |

|---|---|---|---|---|

| Alabama | 53% | 73% | 84% | 100% |

| Alaska | 42% | 62% | 77% | 100% |

| Arizona | 26% | 58% | 75% | 100% |

| Arkansas | 35% | 65% | 81% | 100% |

| Delaware | 20% | 50% | 69% | 100% |

| Florida | 56% | 75% | 85% | 100% |

| Georgia | 60% | 79% | 89% | 100% |

| Idaho | 50% | 77% | 88% | 100% |

| Illinois | 25% | 56% | 74% | 100% |

| Indiana | 41% | 67% | 82% | 100% |

| Iowa | 29% | 57% | 75% | 100% |

| Kansas | 52% | 75% | 86% | 100% |

| Louisiana | 45% | 70% | 83% | 100% |

| Maine | 38% | 63% | 77% | 100% |

| Michigan | 39% | 62% | 77% | 100% |

| Mississippi | 68% | 86% | 93% | 100% |

| Missouri | 57% | 77% | 87% | 100% |

| Montana | 37% | 62% | 78% | 100% |

| Nebraska | 38% | 64% | 79% | 100% |

| New Hampshire | 38% | 62% | 77% | 100% |

| New Jersey | 20% | 45% | 62% | 100% |

| New Mexico | 20% | 50% | 71% | 100% |

| North Carolina | 48% | 71% | 84% | 100% |

| North Dakota | 15% | 46% | 67% | 100% |

| Ohio | 24% | 52% | 71% | 100% |

| Oklahoma | 47% | 74% | 87% | 100% |

| Pennsylvania | 47% | 68% | 80% | 100% |

| South Carolina | 45% | 70% | 83% | 100% |

| South Dakota | 34% | 61% | 77% | 100% |

| Tennessee | 42% | 69% | 84% | 100% |

| Texas | 50% | 74% | 86% | 100% |

| Utah | 36% | 69% | 85% | 100% |

| Virginia | 48% | 73% | 85% | 100% |

| West Virginia | 31% | 58% | 73% | 100% |

| Wisconsin | 32% | 57% | 73% | 100% |

| Wyoming | 33% | 55% | 70% | 100% |

| All FFM States | 46% | 69% | 82% | 100% |

Source: ASPE computations of CMS Federally-facilitated Marketplace (FFM) data as of 5/12/2014.

Note: Represents distribution of monthly Marketplace plan selections across bronze, silver, gold, and platinum metal levels.