This issue brief provides an overview of pre-Affordable Care Act and post-Affordable Care Act trends in Medicare spending, plan premiums, beneficiary choice of plans, and quality in the Medicare Advantage program

Executive Summary

Private insurance plans were introduced into the Medicare program in the 1980s based on the theory that private plans could provide coordinated, high-quality care, and enhanced benefits for beneficiaries at a cost below that of the traditional fee-for-service (FFS) program. Under this scenario, beneficiaries would have a choice of plans from which they could obtain extra benefits for an extra premium.

Goal with Affordable Care Act:

The Affordable Care Act includes changes that are designed to make good on this original rationale:

- Providing a choice of plans,

- Maintaining and improving quality ,

- Providing better value,

- Keeping costs comparable to those of fee-for-service Medicare.

Baseline Before 2010:

Prior to the enactment of the Affordable Care Act, Medicare Advantage (MA) plans were being paid 114 percent of FFS costs on average – translating into an extra $1,280 per MA enrollee or $14 billion in higher aggregate payments, and a $3.35 per month increase in the Part B premiums paid by all Medicare beneficiaries during 2009.

Experience Under the Affordable Care Act:

In 2010, the Affordable Care Act made significant changes to the MA program that were designed to reduce higher MA payments while providing incentives for quality improvements. Concerns were raised that the Affordable Care Act would lead to a drop in beneficiary enrollment and a drop in plan participation. To the contrary, experience indicates that the MA program is moving in the right direction – beneficiaries have a choice of plans and are enrolling in record numbers, costs are coming down relative to FFS, while benefits remain stable and quality is improving.

- Beneficiary Choice of MA Plans Remains High – Nearly all beneficiaries (99 percent) continue to have access to an MA plan in their area in 2014. Additionally, the number of plan choices has generally remained stable since the transition to FFS-based rates began in 2012. In 2014, the average beneficiary can choose from among 10 plans, including plans from a wide number of MA organizations.

- Costs Are Coming Down – The transition to FFS-based rates under the Affordable Care Act, which began in 2012 and is scheduled to end in 2017, has already begun to reduce payments to MA plans relative to FFS Medicare (from 114 percent of FFS on average in 2009 to 106 percent of FFS in 2014). Additionally, average MA beneficiary premiums have decreased by 10 percent since the passage of the Affordable Care Act.

- Quality Is Improving – In 2014, over half of all MA enrollees are enrolled in plans with four or more stars, which represents a significant increase from the 24 percent of enrollees who were in such plans in 2011 and the 37 percent of enrollees who were in such plans in 2013. Additionally, over one-third of MA contracts have four or more stars in 2014, compared to 14 percent in 2011.

- Enrollment is at a Historic High and Increasing – MA enrollment has increased by over 30 percent since the enactment of the Affordable Care Act – enrollment is now at levels not ever seen before (private plan contracting began in the Medicare program in the early 1980s). Nationwide, approximately 15 million Medicare beneficiaries are now enrolled in an MA plan, which represents nearly 30 percent of all beneficiaries in the Medicare program, a historic high.

- Plan Profitability Remains Strong – Insurers’ total revenues have increased by 29 percent, their combined operating profits have increased by 13 percent, and their profit margins have remained stable since the enactment of the Affordable Care Act, ranging from 5 to 6 percent on average. Health insurance companies have looked to Medicare Advantage as an area to increase enrollment as employer-sponsored insurance coverage has eroded.

Full Report: the Medicare Advantage Program in 2014

I. Overview

There has been considerable interest in the impact of the Affordable Care Act1 on the Medicare Advantage (MA) program. This paper provides an overview of pre-Affordable Care Act and post-Affordable Care Act trends in Medicare spending, plan premiums, beneficiary choice of plans, and quality in the MA program. The paper starts with a review of private plan contracting in Medicare to provide a broader context for understanding these trends.

A Brief History of Private Plans in the Medicare Program

- Private health plans were expanded in the Medicare program in the early 1980s, a time of rapidly growing health spending, because of their potential to provide higher-quality care and enhanced benefits at a lower cost to taxpayers and beneficiaries.

- At that time, Medicare private plans were paid 95 percent of the estimated cost of treating an average beneficiary in the traditional fee-for-service (FFS) program.

- However, beginning in the late 1990s, the linkage between private plan payments and FFS costs was weakened, and by 2009, Medicare Advantage (MA) plans were being paid 114 percent of FFS costs on average – translating into an extra $1,280 per MA enrollee or $14 billion in higher payments, and a $3.35 per month increase in the Part B premiums paid by all Medicare beneficiaries during that year.

- Despite the extra costs to the Medicare program, National Center for Quality Assurance surveys found that quality in MA plans was not better than that of the traditional program.

- The Affordable Care Act implemented changes designed to reduce higher MA payments while providing incentives for quality improvements.

- The health insurance industry has been profitable since the enactment of the Affordable Care Act, with total operating margins ranging between 5 and 6 percent on average between 2010 and 2013 for ten publicly-traded insurers participating in the MA program.

- Health insurance companies have looked to Medicare Advantage as an area to increase enrollment as employer-sponsored insurance coverage has eroded.

- The transition to fee-for-service-based rates is reducing previous higher payments to MA plans, which is encouraging MA plans to become more efficient without reductions in quality or access.

- Beneficiaries continue to have a large number of MA plans to choose from. Beneficiary enrollment is increasing and is at historically high levels in early 2014. Additionally, beneficiaries are increasingly enrolling in MA plans with high-quality ratings; in 2014, over half (53 percent) of all MA enrollees are in plans with four or more stars, compared with 24 percent in 2011.

1 In this paper, The Patient Protection and Affordable Care Act of 2010 and the Health Care and Education Reconciliation Act of 2010 are collectively known as the Affordable Care Act.

II. History of Private Plans in the Medicare Program

The private plan option has been available in Medicare for over 30 years; it has grown considerably over that period from representing a small part of the program to accounting for nearly 30 percent of all enrollment today.2 Medicare Advantage (MA) is the name of the current program that allows beneficiaries to enroll in private health plans, rather than having their care covered through Medicare’s traditional fee-for-service (FFS) program. The rationale for allowing private plan participation in Medicare was to encourage private plans to: 1) use their provider networks to coordinate high-quality care for beneficiaries, 2) provide enhanced benefits, and 3) do so at a cost below that of the traditional FFS program.3 For example, the Tax Equity and Fiscal Responsibility Act (TEFRA) of 1982 provided assured savings for taxpayers by paying private plans 95 percent of the estimated cost of treating an average beneficiary in the traditional FFS program (known as the adjusted average per capita cost (AAPCC)). Based on data from the Centers for Medicare & Medicaid Services (CMS), Medicare private plan enrollment grew to about 6 million beneficiaries by 1997, primarily concentrated in urban counties, but various studies raised concerns about excess spending due to inadequate risk adjustment of payments to reflect the healthier-than-average population that was enrolled in the private plans.4

- Medicare Private Plan Trends Prior to the Affordable Care Act

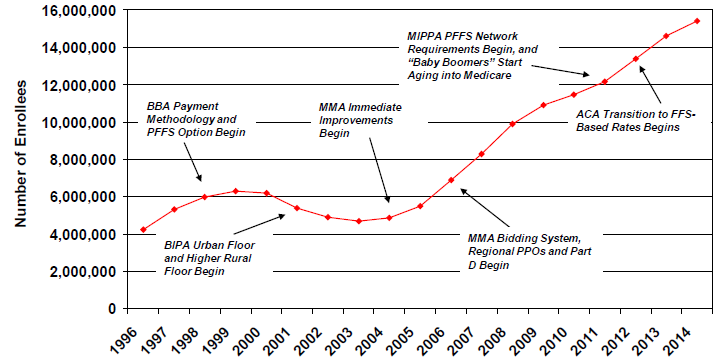

Beginning in the late 1990s, Medicare’s private plan program underwent several significant changes that weakened the linkage between private plan payment rates and FFS costs, and for the first time resulted in plan payments in some areas being higher than the costs of treating similar patients in the traditional FFS program. In particular, several provisions in the Balanced Budget Act of 1997 (BBA) and the Benefits Improvement and Protection Act of 2000 (BIPA) sought to expand Medicare private plans beyond urban areas by increasing the minimum payment rates in rural areas so that they exceeded comparable FFS costs;5 however, the increased payment rates for rural areas were not sufficient to attract increased plan participation. Meanwhile, overall private plan participation and enrollment decreased during this period because the BBA’s reductions in FFS payments and limits on annual increases in the capitation rates that Medicare paid private plans 6 7 occurred at a time when underlying health care costs began to rise much more rapidly.8 9 As a result, private plan enrollment decreased from 6.3 million in 1999 to 4.7 million by 2003 (see Figure 1).

Subsequently, the Medicare Prescription Drug, Improvement, and Modernization Act of 2003 (MMA) authorized the MA program, which included a new competitive bidding process in which MA plans were required to submit bids against a fixed benchmark to provide services to Medicare beneficiaries at the local or regional level, beginning with the 2006 contract year.10 The MMA also provided immediate enhancements to MA plan payment rates (such as a 6.3 percent minimum update for 2004) and other program improvements that were designed to encourage plan participation and reverse the downward trend in Medicare private health plan enrollment. As a result of the increased payment rates under the MMA, and facilitated by an increase in the number of private fee-for-service plans (PFFS) being offered,11 MA enrollment more than doubled between 2005 and 2010 (increasing from 5.5 million to 11.4 million).

Figure 1

Trends in Medicare Advantage Enrollment, 1996-2014

Notes: Excludes Cost plans, PACE, Demos, and Pilots. The MMA required a transition from Medicare+Choice to the Medicare Advantage program, which began in 2006. Enrollment for 1996-1997 reflects risk plan enrollment. Enrollment for 1998-2005 reflects Medicare+Choiceenrollment.

Source: ASPE analysis of CMS Enrollment Data

The Medicare Improvements for Patients and Providers Act of 2008 (MIPPA) provided for a small reduction in MA payments by phasing out of the inclusion of indirect medical education (IME) costs in the calculation of MA payment rates. MIPPA also included a provision that was designed to slow the growth in PFFS enrollment: a requirement that most PFFS plans develop written provider contracts beginning in 2011.12

However, there continued to be considerable concern that payment rates for MA plans were too high relative to the costs of caring for comparable beneficiaries under the traditional FFS program. Indeed, MA payment rates were estimated to exceed FFS payments by a considerable amount; for example the average ratio of MA payments to FFS rates was 114 percent in 2009 nationally. Additionally, the Medicare Payment Advisory Commission (MedPAC) noted that “In 2009, Medicare spent roughly $14 billion dollars more for the beneficiaries enrolled in MA plans than it would have spent if they had stayed in FFS Medicare.”13

Higher payments: The concerns about the higher payments were greater than just their impact on Medicare program spending. The higher payments undermined the competitive rationale for private plan participation in Medicare. Because plans were submitting their bids (based on their expected costs for providing care to a beneficiary) relative to a known and generous benchmark, and rebates equal to 75 percent of the difference between their bid and the benchmark, there was no need to compete with each other or with the traditional program by becoming more efficient or by providing higher quality care.14

Quality Did Not Improve: Indeed, in spite of years of increased costs, prior to the enactment of the Affordable Care Act, there was no evidence of better quality in MA plans relative to the traditional Medicare program.15 Although MA enrollees generally expressed high levels of satisfaction with the care they received, and with their providers and health plans, the National Center for Quality Assurance (NCQA) found that MA plans’ performance on various quality measures for clinical processes and intermediate outcomes was “flat” between 2005 and 2008.16 Additionally, MedPAC found that there was considerable variation in quality performance across plans, with newer plans performing worse than established plans on many measures.17

- Changes to Private Plans Under the Affordable Care Act

In 2010, the Affordable Care Act made significant changes to the MA program that were designed to reduce higher MA payments while providing incentives for quality improvements. Most notably, the Affordable Care Act required a transition from MA payments that were significantly higher than FFS (114 percent of FFS in 2009) to comparable FFS-based MA payment rates,18 beginning in 2012.19 Additionally, the law reduced MA plans’ rebate levels and based rebates on plans’ five-star quality ratings. The Affordable Care Act also provided for additional quality bonus payments (QBPs) for MA contracts that meet quality standards measured under the five-star quality rating system.

2 Medicare’s ability to offer private health plans as options for beneficiaries began with the Social Security Amendments of 1972, which authorized risk contracting with managed care plans. However, it was not until changes made in the risk sharing arrangements under the Tax Equity and Fiscal Responsibility Act (TEFRA) of 1982 that plan participation and enrollment began to increase.

3 For example, the Medicare Payment Advisory Commission has noted that “Private plans, because they are paid a capitated rate rather than on an FFS basis, have greater incentives to innovate and use care management techniques.” Medicare Payment Advisory Commission, “The Medicare Advantage Program: Status Report,” Chapter 13, Report to the Congress: Medicare Payment Policy, March 2014.

4 General Accounting Office (GAO), “Medicare HMOs: HCFA Can Promptly Eliminate Hundreds of Millions in Excess Payments,” GAO/HEHS-97-16, Apr. 25, 1997, accessed at http://www.gao.gov/assets/230/224084.pdf.

5 For example, the Balanced Budget Act of 1997 (BBA), which established the Medicare+Choice program, set national payment floors for lower cost counties, and guaranteed a minimum 2 percent annual increase to all plans; and the Benefits Improvement and Protection Act of 2000 (BIPA) increased the national payment floor; created a second, higher urban floor; and increased the minimum payment update from March 2001 through the end of the calendar year.

6 Under the Medicare + Choice (M+C) program, the county-level payment rates were set based on the greater of: 1) a minimum increase from the previous year’s rate (2 percent), 2) the applicable floor rate, or 3) a blend of the local rate and a national rate. The 2 percent minimum increase was designed to provide protection for private plans due to the dramatic reductions in FFS spending under the BBA (Berenson and Dowd, 2008). Additionally, plans were required to submit Adjusted Community Rate Proposals to CMS for review, summarizing their estimated per-person costs for providing benefits to a Medicare beneficiary.

7 The BBA reduced the national payment update for private plans in 1998 and 1999. Medicare Payment Advisory Commission, “Medicare+Choice: Trends Since the Balanced Budget Act,” Report to the Congress: Medicare Payment Policy, March 2000, accessed at http://www.medpac.gov/document_TOC.cfm?id=150.

8 Marsha Gold, “Medicare+Choice: An Interim Report Card,” Health Affairs, 20, no.4 (2001):120-138, accessed at http://content.healthaffairs.org/content/20/4/120.long.

9 Researchers from Mathematica Policy Research found that the “Managed care organizations (MCOs) that withdrew from the Medicare+Choice program in 2001 had lower enrollments, higher premiums, and less-generous benefit packages than those that remained in the program.” Lori Achman and Marsha Gold, Mathematica Policy Research, Inc., “Medicare+Choice 1999-2001: An Analysis of Managed Care Plan Withdrawals and Trends in Benefits and Premiums,” Commonwealth Fund, February 2, 2002, accessed at http://www.commonwealthfund.org/~/media/Files/Publications/Fund%20Report....

10 Specifically, plans whose bids are below the county benchmark receive their per capita bid risk adjusted for each enrollee, plus a rebate equal to 75 percent of the difference between the bid and the benchmark. Plans bidding above the benchmark amount receive a risk adjusted per capita payment equal to the benchmark and must charge a supplemental premium to beneficiaries.

11 Overall, MA enrollment increased by 68 percent between 2005 and 2008 (3.7 million new enrollees), with PFFS plans accounting for more than half of the total increase in MA enrollees during that period (2.0 million). PFFS plans, which were established under the Balanced Budget Act of 1997, were initially not required to have contracted provider networks in order to meet Medicare’s access standards; instead, they were allowed to deem that a provider had a contract with the plan if they agreed to accept Medicare FFS rates as payment and met other requirements. Studies have shown that the absence of network requirements made PFFS plans particularly attractive to MA organizations and enrollees during the first few years of the MA program. (For more information, see M. Gold & S. Peterson, “Analysis of the Characteristics of Medicare Advantage Plan Participation,” prepared for ASPE/HHS by Mathematica Policy Research, 2006.)

12 As discussed earlier, prior to 2011, PFFS plans were not required to have a contracted provider network as long as they paid willing providers based on Medicare FFS rates.

13 MedPAC also noted that “To support the extra spending, Part B premiums were higher for all Medicare beneficiaries (including those in FFS). CMS estimated that the Part B premium was $3.35 per month higher in 2009 than it would have been if spending for MA enrollees had been the same as in FFS.” Medicare Payment Advisory Commission, “The Medicare Advantage Program,” Chapter 4, Report to the Congress: Medicare Payment Policy, March 2010.

14 A. McDowell and S. Sheingold, “Payment for Medicare Advantage Plans: Policy Issues and Options,” Office of Health Policy, Office of the Assistant Secretary for Planning & Evaluation, U.S. Department of Health & Human Services, accessed at http://aspe.hhs.gov/health/reports/09/medicareadvantage/index.shtml.

15 For example, the National Committee for Quality Assurance (NCQA) found that “While payment policy in the MA program has led to growth in the number of plans available, growth in access to plans across the country, and increased enrollment, the higher funding has not necessarily resulted in cost containment or better quality of care for enrollees.” Cited in Medicare Payment Advisory Commission, “The Medicare Advantage Program,” Chapter 3, Report to the Congress: Medicare Payment Policy, March 2009, p. 263.

16 Medicare Payment Advisory Commission, “The Medicare Advantage Program,” Chapter 4, Report to the Congress: Medicare Payment Policy, March 2010, page 270.

17 Medicare Payment Advisory Commission, “Update on the Medicare Advantage Program,” Chapter 3, Report to the Congress, March 2008; Medicare Payment Advisory Commission, “The Medicare Advantage Program,” Chapter 3, Report to the Congress:Medicare Payment Policy, March 2009.

18 Under the Affordable Care Act section 3201, the county rates transition on a two-, four- or six-year schedule to a methodology based on a percentage of estimated FFS per capita costs in each county. Counties are grouped into quartiles by their relative FFS spending; rates for counties in the highest cost quartile are set at 95% of FFS costs and counties in the lower cost quartiles are set at 100%, 107.5% and 115% of FFS costs respectively.

19 The Affordable Care Act provides for a transition from the pre-Affordable Care Act rates to the FFS-based Affordable Care Act rates. During the transition period, county-level MA payment rates are calculated based on a blend of these two rates, with various counties transitioning to the FFS-based rates in two, four or six years, beginning in 2012.

III. The Impact of the Affordable Care Act on the Medicare Advantage Program

Prior to the enactment of the Affordable Care Act, concerns were raised about how the transition of MA plan payments to the FFS-based rates provided for in the Affordable Care Act would affect plan participation, enrollment, premiums and benefits. With the enactment, some predicted that the reduction in higher MA payments would cause a significant number of MA plans to withdraw from the market, leading to reductions in plan availability, enrollment and benefits, and increased costs to beneficiaries.20 Other experts predicted that the changes under the Affordable Care Act would strengthen the MA program by encouraging MA plans to compete based on price and quality, and achieve greater efficiencies for taxpayers and beneficiaries.21 The recent data displayed below support the latter arguments, as early trends suggest that since the Affordable Care Act, costs have decreased and quality has improved, while enrollment continues to grow. The scheduled quality bonus payments (QBPs) were increased by a demonstration project effective from 2012-2014 that offset some of the payment reductions during this period.22

20 James C. Capretta, “Obamacare and Medicare Advantage Cuts: Undermining Seniors’ Coverage Options,” The Heritage Foundation, January 20, 2011, accessed at http://www.heritage.org/research/reports/2011/01/obamacare-and-medicare-....

21 For example, the Commonwealth Fund anticipated that the Affordable Care Act’s “new incentives should make participation in Medicare attractive for plans that provide well-coordinated, responsive care for beneficiaries.” Brian Biles, Giselle Casillas, Grace Arnold, and Stuart Guterman, “The Impact of Health Reform on the Medicare Advantage Program: Realigning Payment with Performance,” Commonwealth Fund, October 2012, accessed at http://www.commonwealthfund.org/~/media/Files/Publications/Issue%20Brief....

22 Beginning in 2012, the Centers for Medicare & Medicaid Services’ Medicare Advantage Quality Bonus Payment Demonstration extends quality bonus payments to 3 and 3.5 star plans, and eliminates the cap on blended county benchmarks that would otherwise limit quality bonus payments. The demonstration ends in 2014.

Since the Affordable Care Act: Medicare Advantage Higher Payments Have Decreased

Table 1 shows that the transition to FFS-based rates under the Affordable Care Act, which began in 2012 and is scheduled to end in 2017, has already begun to reduce payments to MA plans relative to fee-for-service Medicare. Moreover, MA plan bids have declined from slightly higher (101 to 102 percent) to slightly less (96 to 98 percent) than fee-for-service costs in the last few years. This decline suggests that plans are adjusting to the new payment incentives by becoming more efficient.23

Since the Affordable Care Act: Medicare Advantage Enrollment Has Increased By Over 30 Percent

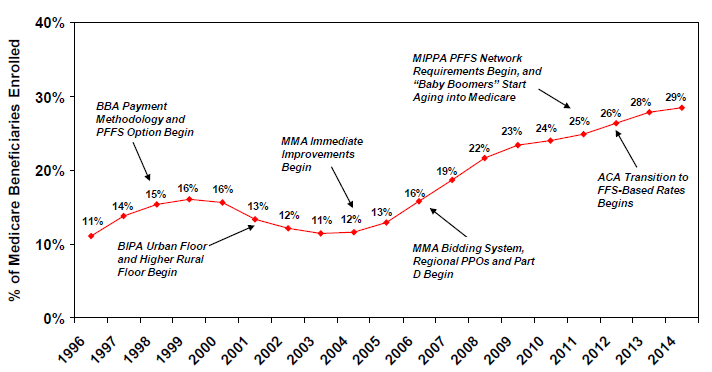

As discussed earlier, since the Affordable Care Act was enacted, actual MA enrollment has exceeded previous projections.24 Figure 1 and Figure 2 show that Medicare Advantage enrollment and penetration are at an all-time high. Nationwide, approximately 15 million Medicare beneficiaries25 are now enrolled in an MA plan, which represents nearly 30 percent of all beneficiaries in the program. MA enrollment has increased by nearly 38 percent since 2010 (when the Affordable Care Act was enacted), and by more than 25 percent since the transition to FFS-based payment rates began, and enrollment is projected to continue increasing.26

Figure 2

Trends in Medicare Advantage Penetration Rates, 1996-2014

Notes: Penetration rate represents private plan enrollment as a percentage of total Medicare beneficiaries with beneficiaries with HI and/or SMI coverage. Excludes Cost plans, PACE, Demos, and Pilots. The MMA required a transition from Medicare+Choice to the Medicare Advantage program, which began in 2006. Enrollment for 1996-1997 reflects risk plan enrollment. Enrollment for 1998-2005 reflects Medicare+Choiceenrollment.Source: ASPE analysis of CMS Enrollment Data; Medicare Trustees Report, 2011 and 2013

24 Gretchen Jacobson, Tricia Neuman and Jennifer Huang, “Projecting Medicare Advantage Enrollment: Expect the Unexpected?,” Kaiser Family Foundation, June 2013, accessed at http://kff.org/medicare/perspective/projecting-medicare-advantage-enroll....

25 Medicare Advantage/Part D Contract and Enrollment Data, Contract Summary, February 2014, accessed at http://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trend....

26 FY 2015 President’s Budget, Technical Budget Analyses, “Table 25–3 Baseline Beneficiary Projections For Major Benefit Programs,” accessed at http://www.whitehouse.gov/sites/default/files/private/omb/budget/fy2015/assets/t....

Since the Affordable Care Act: Medicare Advantage Plan Availability Remains High

Table 2 shows that MA plan availability has been stable since the enactment of the Affordable Care Act, with most Medicare beneficiaries having access to at least one MA plan. Plan participation continues to be robust, with nearly all (99.1 percent)27 of beneficiaries having access to an MA plan in their area in 2014. Additionally, the number of plan choices has remained stable since the transition to FFS-based rates began in 2012. The average beneficiary can choose from among 10 plans (based on unweighted data, or 17 plans if the data are weighted by the number of Medicare eligible in a given county), including plans from a wide number of MA organizations – a number which has generally held steady for the past 4 years, during the transition to FFS payment levels. Additionally, over 80 percent of Medicare beneficiaries have access to a $0 premium MA plan.

Table 2

Percent of Beneficiaries with Access to Medicare Advantage Plans By Type, 2011-2014 (1)

| Type of Plan | 2011 | 2012 | 2013 | 2014 |

|---|---|---|---|---|

| All Plan Types | 99.7% | 99.7% | 99.6% | 99.1% |

| Local Coordinated Care Plan (CCP) | 92.3% | 92.9% | 95.0% | 95.0% |

| Regional Preferred Provider Organization (PPO) | 86.0% | 75.8% | 70.5% |

70.5% |

| Private Fee-For-Service (PFFS) | 63.3% | 61.2% | 59.1% | 51.5% |

| Zero-Premium Plans With Drugs | 89.8% | 87.6% | 85.9% | 84.2% |

| Average Number of Plan Choices (unweighted) (2) | 12 | 12 | 12 | 10 |

| Average Number of Plan Choices (weighted) (3) | 20 | 19 | 19 | 17 |

(1) These figures exclude special needs plans and employer-only plans. A zero premium plan with drugs includes Part D coverage and has no premium beyond the Part B premium. Regional PPOs were created in 2006. Part D began in 2006.

(2) The unweighted averages are consistent with the MedPAC 2014 Report to the Congress.

(3) For the weighted averages, the data on the number of plan choices have been weighted based on the number of Medicare eligibles in a given county.

Sources: Centers for Medicare & Medicaid Services; Medicare Payment Advisory Commission (MedPAC), March 2014 Report to the Congress; Centers for Medicare & Medicaid Services

27 Centers for Medicare & Medicaid Services, “More, higher quality options for seniors in Medicare Advantage,” Press Release, September 19, 2013, accessed at http://www.hhs.gov/news/press/2013pres/09/20130919b.html.

28 Mathematica Policy Research and Kaiser Family Foundation, “Medicare Advantage 2014 Spotlight: Benefits and Premiums,” December 2014.

Since the Affordable Care Act: There Have Been Substantial Improvements in Medicare Advantage Quality

The Affordable Care Act requires CMS to make Quality Bonus Payments (QBPs) to MA organizations that achieve at least four stars in a five-star quality rating system. The QBP demonstration finalized in the CMS 2012 Call Letter is testing whether providing scaled bonuses to MA organizations with three or more stars will lead to more rapid and larger year-to-year quality improvements in their quality scores, compared to the current law bonus structure. For contracts at or above three stars, QBPs were computed along a scale; the higher a contract’s star rating, the greater the QBP percentage. Although there was little change in MA plans’ performance on quality measures between 2008 and 2010, beginning in 2011, a larger number of measures have shown improvement in comparison with previous years.29 Table 3 shows that in 2014, over half of all MA enrollees were enrolled in plans with four or more stars, which represents a significant increase from the 24 percent of enrollees who were in such plans in 2011 and the 37 percent of enrollees who were in such plans in 2013. Additionally, over one-third of MA contracts have four or more stars in 2014, compared to 14 percent in 2011.30 31

Table 3

Trends in Medicare Advantage (MA) 5-Star Quality Ratings, 2011-2014

| Description | 2011 | 2012 | 2013 | 2014 |

|---|---|---|---|---|

| Percentage of MA Contracts With 4 or More Stars | 14% | 24% | 28% | 38% |

| Percentage of MA Enrollees in Plans With 4 or More Stars | 24% | 29% | 37% | 53% |

Notes: Percentages are based on the total number of contracts with a quality rating.

Source: Centers for Medicare & Medicaid Services.

29 Medicare Payment Advisory Commission, “The Medicare Advantage Program: Status Report,” Chapter 12, Report to the Congress: Medicare Payment Policy, March 2012..

30 Centers for Medicare & Medicaid Services, “More, higher quality options for seniors in Medicare Advantage,” Press Release, September 19, 2013, accessed at http://www.hhs.gov/news/press/2013pres/09/20130919b.html.

31 CMS calculates star ratings from 1 to 5 (with 5 being the best) based on quality and performance for MA and Medicare prescription drug plans to help beneficiaries, their families, and caregivers compare plans.

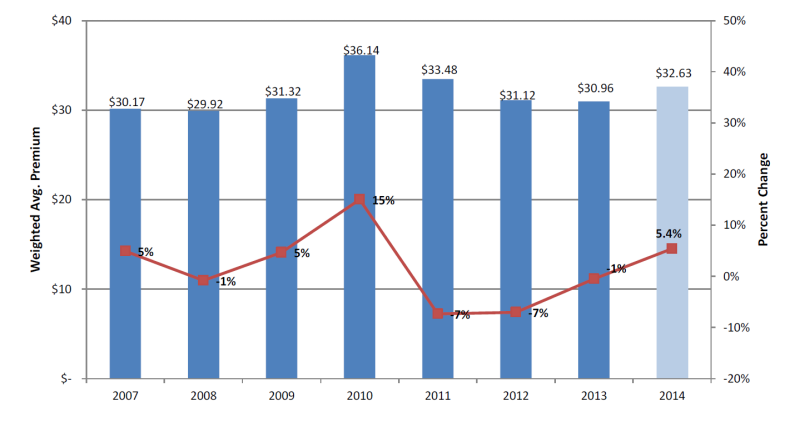

Since the Affordable Care Act: Medicare Advantage Premiums Have Fallen and Benefits Have Remained Stable

Medicare Advantage plans have responded to the Affordable Care Act incentives by becoming more competitive for enrollment by reducing or holding steady their beneficiary premiums; MA plans have not responded with an increase in beneficiary premiums. Figure 3 shows that since the passage of the Affordable Care Act, average MA premiums are down by 10 percent.32 The average MA premium in 2014 is projected to increase by only $1.64 from last year, coming to $32.60.33

Over 80 percent of Medicare beneficiaries have access to a MA-PD plan (MA plan with Part D drug coverage) with a yearly maximum out-of-pocket limit of $3,400 or less. All MA enrollees are in plans that will have a maximum out-of-pocket limit for all Medicare covered services of $6,700 or lower. Additionally, access to MA supplemental benefits, such as dental and vision benefits, has generally remained stable.34

Figure 3

Trend in Average Medicare Advantage Premiums, 2007-2014

Note: 2007-2013 data is weighted by July enrollment of the plan year, 2014 data is weighted by plan projected enrollment.

Source: Centers for Medicare & Medicaid Services

32 Centers for Medicare & Medicaid Services, “More, higher quality options for seniors in Medicare Advantage,” Press Release, September 19, 2013, accessed at http://www.hhs.gov/news/press/2013pres/09/20130919b.html.

33 Centers for Medicare & Medicaid Services, “More, higher quality options for seniors in Medicare Advantage,” Press Release, September 19, 2013, accessed at http://www.hhs.gov/news/press/2013pres/09/20130919b.html.

34 Centers for Medicare & Medicaid Services, “More, higher quality options for seniors in Medicare Advantage,” Press Release, September 19, 2013, accessed at http://www.hhs.gov/news/press/2013pres/09/20130919b.html.

Since the Affordable Care Act: Health Insurance Company Revenues Have Increased

Analysis of data for several large publicly-traded insurance companies that participate in the MA program reveals that these insurers’ total revenues have increased by 29 percent since the enactment of the Affordable Care Act in 2010 (from $275 billion to $355 billion), and their combined operating profits have increased by 13 percent (from $20 billion to $23 billion). Meanwhile, these insurers’ profit margins have remained stable since the enactment of the Affordable Care Act, ranging from 5 to 6 percent on average between 2010 and 2013.35 Additionally, health insurance companies have looked to Medicare Advantage as an area to increase enrollment as employer-sponsored insurance coverage has eroded.36

Financial analysts continue to maintain a positive long-term view of the MA program, and have suggested that “the industry can absorb the proposed 2015 payment adjustments through increased efficiency and benefit reductions while retaining members and economics.” 37

35 Represents the unweighted average of the company-specific operating margins (total revenues divided by margins before income tax, interest, and non-net operating losses or gains) for 10 publicly-traded insurance companies participating in the Medicare Advantage (MA) program (e.g., with MA covered lives) that are included in the Bloomberg Industries dashboard, which includes information from these companies’ filings with the U.S. Securities and Exchange Commission (SEC). Together, these 10 companies account for 60 percent of total MA enrollment, including the 5 publicly-traded companies with the most MA enrollees, which collectively account for 50 percent of MA enrollment. The average operating margins (unweighted) for these 10 companies were: 5.2% in 2010, 5.9% in 2011, 4.9% in 2012, and 4.5% in 2013. The total combined revenue for these 10 companies was $275 billion in 2010, $285 billion in 2011, $312 billion in 2012, and $355 billion; and the total combined operating profits for these 10 companies was $20.2 billion in 2010, $21.6 billion in 2011, $21.9 billion in 2012, and $22.9 billion in 2013. These data include all company activities (such as non-health insurance business, overseas operations, etc.)

36 For example, analysts have stated that in 2013, the five largest publicly-traded U.S. health insurers’ “growth in revenue was driven primarily by insurers' targeted expansions of their Medicaid and Medicare Advantage enrollments, as most companies continued to experience attrition in their fully insured employer accounts.” Matt Dunning, “Medicaid, Medicare Advantage enrollment drive rise in health insurer revenue,” Business Insurance, March 30, 2014, accessed at http://www.businessinsurance.com/article/20140330/NEWS03/303309984?tags=....

37 Wall Street Journal, “Health Insurers Rally as Fears Over Medicare Cuts Ease,” February 24, 2014, accessed at http://online.wsj.com/news/articles/SB1000142405270230461040457940308151...

IV. Looking Forward to 2015

Our goal is to continue improving the MA program while keeping costs down, reducing fraud and abuse, and fostering competition. As discussed earlier, the changes that are underway under the Affordable Care Act reduce higher payments to MA plans, by transitioning to FFS-based payment rates; and provide incentives for quality improvements by basing part of the MA payment on plan quality performance. In 2015, we will continue implementing the provisions of the Affordable Care Act, and pursuing policies that seek to improve MA payment accuracy and quality, while providing greater protections for beneficiaries and value for taxpayers.

Two important factors are expected to affect MA payments in 2015:

- Slower Growth In FFS Spending – The Medicare program has been experiencing historically low growth in underlying Medicare per-capita spending, which is tied, in part, to successful initiatives undertaken to promote value over volume and help curb fraud, waste, and abuse in the Medicare fee-for-service program in recent years. As the rate of growth in underlying FFS Medicare spending decreases, MA plans are likely to be experiencing similar trends, which should be helpful as more and more counties transition to FFS-based MA payment rates.38

- Increases in Coding Intensity and Policy Responses – Since 2004, when CMS began adjusting payments to MA plans based on the relative health of their enrollees, the average MA risk score (which measures beneficiaries’ estimated relative costs based on demographics and health characteristics) has increased faster than the average FFS risk score. However, most of this growth appears to result from MA plans identifying more diagnoses to code in a population that is no sicker, and therefore no more costly to treat, than before the coding change.39 The change in “coding intensity” has resulted in MA payments increasing to a greater degree than would be consistent with actual changes in the health risk of enrollees. The policy responses have included both across-the-board adjustments and changes to CMS’s risk adjustment model.40

38 For 2015, most counties will be fully transitioned to the new rate methodology, while others will continue to be based on a blended rate.

39 For example, the Government Accountability Office has found that “differences in diagnostic coding caused risk scores for MA beneficiaries to be higher than those for comparable beneficiaries in Medicare FFS in 2010, 2011, and 2012.” Government Accountability Office, “Medicare Advantage: Substantial Excess Payments Underscore Need for CMS to Improve Accuracy of Risk Score Adjustments,” GAO-13-206, January 2013, accessed at http://www.gao.gov/assets/660/651712.pdf.

40 The CMS-HCC risk adjustment model was modified for 2013 and again for 2014 in ways that disproportionately affect plans with large increases in average risk scores. However, even if the 2014 model (which was 75 percent phased in for 2014) had been used starting in 2004, MA risk scores would still have increased every year since then. The FY 2015 President’s Budget proposes increasing the MA coding pattern adjustment to account for ongoing growth in coding intensity.

V. Conclusion

In order to make good on the original rationale for including private plans in Medicare, the Medicare Advantage program needs to continue improving quality, while lowering costs. The early experience following the enactment of the Affordable Care Act indicates that the MA program is moving in the right direction – beneficiaries have a robust choice of plans, costs are coming down (relative to fee-for-service), while benefits remain stable, and quality is improving.