A. Executive Summary

The purposes of this environmental scan are to develop a conceptual framework, review and discuss the major research questions and hypotheses, and identify the “ideal” set of metrics for understanding the effects of the Affordable Care Act (ACA) on safety net hospitals. This report is part of a larger effort by the Office of the Assistant Secretary for Planning and Evaluation (ASPE) to develop a strategy for monitoring safety net hospitals during and after implementation of the ACA. ASPE has contracted with The Center for Studying Health System Change to conduct this environmental scan (the focus of this report) and to prepare separate reports that assess the availability of data sources and metrics for a safety net monitoring effort, as well as a plan for conducting case studies of safety net hospitals.

It is important to monitor the effects of the ACA on safety net hospitals because even after full implementation of the ACA expansions in coverage, there will still be an estimated 31 million uninsured people who will rely on these hospitals for medical care (CBO 2013). The ACA creates both opportunities and challenges for safety net hospitals as they try to adapt to a changing health care marketplace. Health insurance coverage expansions through Medicaid and the state-based marketplaces will increase patient revenues and reduce uncompensated care for hospitals. However, many safety net hospitals are concerned that these gains may not be sufficient to offset reduced revenues through Medicaid and Medicare Disproportionate Share Hospital (DSH) payments, which may affect their ability to care for patients who remain uninsured. Safety net hospitals could also see competition increase as more of their patients become insured and thus have more options to seek health care at other hospitals. Payment and delivery system reforms that emphasize primary care and the clinical and organizational integration of medical care will provide further opportunities and challenges for safety net hospitals.

Drawing on previous safety net monitoring efforts, our own understanding of the ACA and other delivery system reforms, and comments from a technical expert panel (TEP) convened for this project, we present a conceptual framework that describes how health care policy—including the ACA and other state and local policies—affects demand for care, revenue, and the costs of care at safety net hospitals. We also show how contextual factors related to the characteristics of the population in the community, local delivery systems, and unique organizational attributes of hospitals will affect safety net hospitals’ experiences with and responses to health reform. In the second part of this report, we expand on the conceptual framework by discussing the key issues and hypotheses about how the ACA will affect safety net hospitals. This discussion is based on a review of recent research, policy analyses, and commentaries published in peer review journals and by government and private organizations.

The report concludes with a summary of the major research questions and the “ideal” set of metrics that should guide an effort to monitor the effects of the ACA on safety net hospitals.

B. Introduction and Objectives

Safety net hospitals are critical providers of medical care to low-income uninsured and other vulnerable populations. In addition to being the major providers of inpatient, emergency, outpatient, and many types of specialty care for uninsured people, they often are the sole providers of certain critical services in the community, such as trauma and burn care, as well as inpatient behavioral health. Safety net hospitals often operate with low or negative margins, in large part because a high proportion of patients are either uninsured or Medicaid beneficiaries, for whom patient revenues often do not cover the costs of providing care. To cover the costs of uncompensated care, most safety net hospitals receive subsidies from federal, state, and/or local governments.

The Affordable Care Act (ACA) creates both opportunities and challenges for safety net hospitals. Health insurance coverage expansions through Medicaid and the state-based marketplaces are expected to increase patient revenues and reduce uncompensated care (typically defined as the combination of charity care and bad debt) for hospitals. However, many safety net hospitals are concerned that these gains may not be sufficient to offset planned reductions in Medicaid and Medicare Disproportionate Share Hospital (DSH) payments, which may affect their ability to care for patients who remain uninsured. In addition, safety net hospitals are concerned about their capacity to meet the increased demand for care that they expect will occur with the insurance coverage expansions.

Other provisions of the ACA could also directly or indirectly affect safety net hospitals, such as whether health plans that operate in the new marketplaces include safety net hospitals as “essential community providers” in plan networks. In addition, competition with other hospitals may also increase as providers seek greater alignment and integration with one another; such integration is encouraged by federal incentives and demonstration programs for the purpose of increasing the efficiency, coordination, and quality of care. Although many safety net hospitals are attempting to align themselves with these new delivery systems, including Accountable Care Organizations (ACOs) for various payers (Medicare, Medicaid, or commercial), they face a number of potential barriers to ACO participation that may not be experienced by other hospitals.

Although safety net hospitals receive federal subsidies and grant support for various activities, there are no federal requirements that these facilities provide data on hospital utilization, capacity, and finances in a manner that would facilitate the government’s ability to quantify the impact of health reform on safety net hospitals. This is in contrast to federally funded health centers, which are the major safety net providers of primary care and other outpatient services to uninsured and other medically underserved populations. Health centers receive federal grants from the Health Resources and Services Administration (HRSA) within the Department of Health and Human Services (HHS) and are required to provide detailed data to HRSA annually on health center patients, utilization, services, staffing, and financial performance.

Because safety net hospitals will continue to be essential providers of inpatient, emergency, ambulatory care, and specialty services to an estimated 31 million Americans who will remain uninsured after the implementation of health insurance coverage expansions, the Office of the Assistant Secretary for Planning and Evaluation (ASPE) has a compelling interest in understanding how safety net hospitals will be affected by health care reform. This includes the effects of insurance coverage expansions on hospital utilization, capacity, and finances, as well as on their ability to adapt to changes in payment and delivery system reforms. To this end, ASPE has asked The Center for Studying Health System Change (HSC) to develop the key hypotheses and planning documents for assessing and monitoring the impact of the ACA on safety net hospitals. The ultimate purpose of this task was to identify the major research questions and develop a strategy for conducting case studies on how safety net hospitals are being affected by and responding to health reform.

This report provides an environmental scan of the issues that safety net hospitals are likely to encounter with the implementation of health care reform. Specifically, the objectives of the environmental scan are to (1) develop a conceptual framework for understanding the effects of the ACA on safety net hospitals, (2) identify the major research questions and hypotheses concerning both the direct and indirect effects of the ACA on safety net hospitals, and (3) identify the “ideal” list of key indicators needed for monitoring safety net hospitals during implementation of health care reform. The environmental scan will be used to inform the development of a strategy for conducting case studies of the effects of the ACA on safety net hospitals. Additional reports for this task will include an assessment of data sources and metrics that will be available for tracking changes in safety net hospitals during and after implementation of the ACA, as well as a report on a plan and methodology for conducting case studies.

C. Definition of Safety Net Hospitals

For the purposes of this environmental scan, we use the Institute of Medicine’s definition of safety net providers: “providers that organize and deliver a significant level of both health care and other health-related services to the uninsured, Medicaid, and other vulnerable populations,” as well as providers “who by mandate or mission offer access to care regardless of a patient’s ability to pay and whose patient population includes a substantial share of uninsured, Medicaid, and other vulnerable patients” (IOM 2000).

This definition includes most—if not all—public hospitals that are often the providers of last resort in their community by virtue of their mission, governance, services provided, and dependence on revenue from local taxes and other government subsidies. Academic medical centers also serve a major safety net function in many communities, combining their teaching function with a mission to serve vulnerable populations. In communities without public hospitals or academic medical centers, private hospitals often are the major safety net providers, either by mission (for example, religiously affiliated hospitals) or default, especially for those located in low-income urban areas. Safety net hospitals often provide services that other hospitals in the community do not offer, such as trauma, burn care, neonatal intensive care, and inpatient behavioral health. In addition, many safety net hospitals are major providers of ambulatory care services in their community. For example, the average member hospital of the National Association of Public Hospitals and Health Systems (NAPH) had a network of 20 or more ambulatory care sites, which could include on-campus clinics as well as freestanding clinics that may serve as medical homes for community residents (Zaman et al. 2012).

Most safety net hospitals—both public and private—receive subsidies from Medicaid and Medicare DSH payments because of the large amount of care they provide to uninsured people; however, because of the way that some states allocate DSH funds, the amount of DSH subsidies that hospitals receive is not always a good indicator of their commitment to uninsured and vulnerable populations (GAO 2008). Many researchers have identified safety net hospitals based on the volume of care provided to uninsured and/or Medicaid patients, although there is no specific threshold of the amount of care provided to uninsured people that clearly identifies an institution as being a safety net hospital (Gaskin and Hadley 1999). Thus, although all agree that safety net hospitals comprise a broader group than just public hospitals, there is no standard or widely agreed-upon definition that is used to identify all safety net hospitals from available data.

D. Conceptual Framework

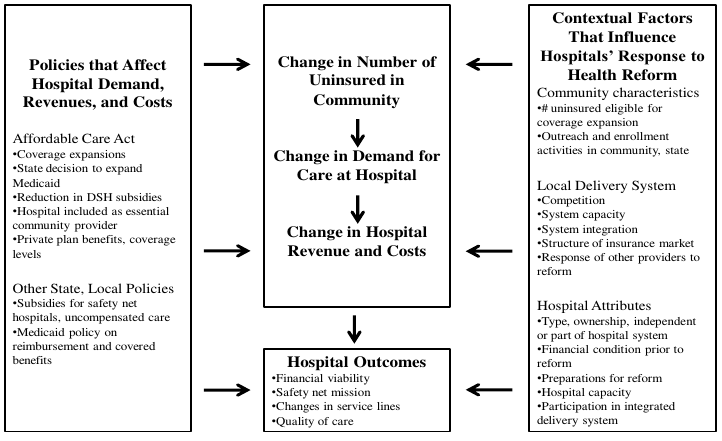

A conceptual framework for understanding the effects of health reform on safety net hospitals is shown in Figure 1. The framework draws on other efforts to develop a monitoring strategy for safety net hospitals, such as the Agency for Healthcare Research and Quality’s Safety Net Monitoring Initiative, as well as an initiative by HRSA to monitor the impact of state health insurance expansions on safety net organizations (AHRQ 2003; Harrington and Byrd 2009). We adapt the conceptual frameworks used in these prior efforts to account for both specific provisions of the ACA and recent changes in the health care delivery system, along with issues that are specific to safety net hospitals. We also incorporate comments made by a technical expert panel (TEP) that was convened by ASPE as part of this project (HHS/ASPE 2013).

Policies That Affect Demand for Care, Revenues, and Costs. The most direct effect of the ACA on safety net hospitals is that about 25 million people will gain coverage by 2023 through Medicaid expansions or subsidized private coverage through the new state-based health insurance marketplaces (CBO 2013). This is likely to increase the demand for care at safety net hospitals as well as patient revenue from insured persons.

The extent of increased demand will depend on a number of state implementation decisions relevant to the ACA, especially whether the state decides to expand Medicaid eligibility to all adults with family incomes below 138 percent of the federal poverty line and whether safety net hospitals are included as “essential community providers” in qualified health plans. ACA provisions that dramatically decrease federal subsidies to safety net hospitals through DSH have the potential to offset any gains in patient revenue from insurance coverage expansions. Changes in other state and local subsidies to safety net hospitals will also affect their ability to respond to increased demand for care from the ACA coverage expansions as well as to payment and delivery system reforms.

Characteristics of Communities and Local Delivery Systems. Health reform’s impact on demand for care at safety net hospitals will depend in part on the size of the uninsured population in the community prior to reform and on the number of uninsured who will be eligible for coverage expansions.

Demand for care, patient revenues, and costs will also be affected by the organization and dynamics of the local delivery system, including the degree of competition for newly insured patients between hospitals and other health care providers; the overall capacity of the system—especially for primary care; the extent of system integration; and, the size and breadth of health plan provider networks. The ACA includes provisions to both increase system capacity and promote care coordination through payment and delivery system reforms, such as Patient-Centered Medical Home (PCMH) initiatives and Accountable Care Organizations (ACOs). If successful, such reforms will increase the demand for outpatient and primary care (as well as compensation for these services) and decrease the demand for inpatient and emergency department care.

Figure 1. Conceptual Framework

Hospital Attributes. Characteristics of safety net hospitals will also affect their response to health reform. Type of ownership, capacity (both inpatient and outpatient), whether they are the dominant safety net hospital in the community, if they are part of a larger hospital system, their financial condition before reform, and preparations they made in anticipation of reform could all affect safety net hospitals’ ability to retain existing patients, attract new patients, and form or participate in integrated delivery systems.

Safety Net Hospital Outcomes. Key hospital outcomes to monitor include the financial performance and viability of safety net hospitals, continued commitment to their safety net mission of serving patients regardless of their ability to pay (that is, the remaining uninsured population), changes in service lines offered, and changes in the quality of care. Quality of care includes not only indicators required by the Centers for Medicare & Medicaid Services (CMS) (for example, 30-day readmission rates for specific conditions), but also quality-of-care measures that reflect better access to primary care for patients and greater care coordination between hospital and community providers.

Below is a more detailed discussion of the major issues and research questions concerning the potential effects of the ACA on safety net hospitals.

E. Potential Effects of the ACA on Safety Net Hospitals

1. Effect on Demand for Care

The expansion of Medicaid and the availability of subsidized coverage through health insurance marketplaces will generally increase the demand for medical care at safety net hospitals and reduce the amount or proportion of care provided by these institutions to uninsured persons. The most recent estimates from the Congressional Budget Office (CBO) predict that there will be 25 million fewer uninsured persons by 2023 compared to what would have happened without health reform, and that Medicaid will account for about half of the newly insured (CBO 2013). Increased demand could potentially come from both newly insured patients who used safety net hospitals when they were uninsured, as well as newly insured patients who previously had little or no health care utilization.

The extent of the increase in demand for care at safety net hospitals will vary considerably depending on a number of factors, but especially on the size of the increase in the insured population in the community. States and communities vary considerably in the size and proportion of their population uninsured prior to the ACA, due to differences in local socioeconomic characteristics, variations in the local economy that affect enrollment in private insurance coverage, and differences in state Medicaid eligibility policies (Buettgens and Hall 2011).

Even within states, communities will vary in terms of how many uninsured people gain coverage. Many safety net hospitals will continue to serve large numbers of uninsured people. CBO estimates that about 31 million people will remain uninsured by 2023; the size of the uninsured population will vary across communities for a number of reasons (CBO 2013). An especially important consideration will be the size of the uninsured immigrant population in the community: undocumented immigrants are barred from enrolling in Medicaid or receiving subsidized coverage in the health insurance marketplaces, whereas legal immigrants are permitted to purchase subsidized coverage and are eligible to enroll in Medicaid if they have been in the country for at least five years. Communities that have relatively large undocumented immigrant populations will therefore continue to have large uninsured populations (Hoefer et al.

2011).

Safety net hospitals may be able to increase demand from newly insured patients to the extent that they are able to assist and encourage uninsured patients to enroll in Medicaid or private insurance coverage, which they become eligible for on January 1, 2014. Many safety net hospitals have considerable experience in providing application assistance and enrolling eligible individuals in Medicaid and CHIP, but it is unclear whether additional support will be needed to facilitate private insurance enrollment through the health plan marketplaces (Snyder et al. 2012). The rate of “churning”—the extent to which people switch back and forth from public and private coverage because of changes in their eligibility status—could also pose a challenge to safety net hospitals in their ability to track patients and bill insurers for services.

2. Other ACA Provisions That Will Mitigate Increased Demand

The extent of the increase in demand for care will also depend in part on decisions that states make in implementing the reforms. Of particular importance is whether state governments decide to expand Medicaid coverage to adults— which is no longer mandatory, based on the Supreme Court’s 2012 decision on the constitutionality of the ACA. As of this writing, 30 states including the District of Columbia have decided to proceed with the expansion, 15 states currently oppose expansion, and 6 are undecided (Kaiser Family Foundation, State Health Facts). Moreover, a number of states that have decided not to expand Medicaid have large numbers of uninsured people who might otherwise have gained insurance coverage through the Medicaid expansions. Thus, the decision not to expand Medicaid in a state is likely to substantially limit the increase in demand for care at safety net hospitals.

Another potentially mitigating factor that may affect the size of the increase in demand at any specific hospital is whether the hospital is included in qualified health plans as an “essential community provider.” The ACA requires that qualified health plans sold in the marketplaces have a “sufficient number and geographic distribution of essential community providers (which includes public and nonprofit hospitals), where available, to ensure reasonable and timely access to a broad range of such providers for low-income, medically underserved individuals.” Although this generally includes safety net providers, not all safety net providers need to be included in plan networks, and states will still have considerable discretion in identifying the specific providers that must be included in a qualified health plan. For example, under the “safe harbor” standard, CMS requires that plans include a minimum of 20 percent of available essential community providers in their network, whereas only 10 percent of available essential community providers are required under the “minimum expectation” requirement (CMS-CCIIO 2013). Movement by some health plans toward narrower network insurance products could further serve to exclude some safety net hospitals, especially those that are perceived to be high cost (Christianson et al. 2011b). Exclusion from plan networks would seriously affect safety net hospitals’ ability to retain and attract patients who are newly insured through the health insurance marketplaces.

3. Changes in Patient Revenue

Increases in patient revenue from Medicaid and private insurance may not be entirely commensurate with increased demand for care. Revenue from Medicaid patients might be limited to the extent that states have or will cut back on reimbursement and benefits (Bachrach et al. 2012). Medicaid reimbursement levels to hospitals and physicians have historically been low compared to Medicare and private payers. According to the American Hospital Association (AHA), hospital payment-to-cost ratios (payments for services as a percentage of the cost of providing services) average 88.7 percent for Medicaid, compared to 128.3 percent for private payers (AHA 2010). The recession of 2007–2009 and state budget problems have led to further reductions in Medicaid reimbursement rates to hospitals, including 33 states that cut rates in 2010 (Smith et al. 2010). Increased revenue from privately insured patients also depends on the payment rates that plans sold in the new state-based marketplaces negotiate with hospitals.

The amount of patient revenue from Medicaid and private payers can also be affected by whether reimbursement favors certain types of services over others. Historically, hospital payment in Medicaid has generally favored (that is, covered more of the cost of) inpatient over outpatient care (Ginsburg and Grossman 2005). This could be a problem if initiatives to increase use of primary care and outpatient care services—and to decrease use of inpatient care—are not accompanied by a realignment of financial incentives for outpatient versus inpatient care. Some states, including New York, have increased outpatient rates relative to inpatient rates in their Medicaid programs (Quinn and Courts 2010).

Some policy analysts also have raised concerns that revenue from new, privately insured patients might be limited to the extent that some services are not covered or will require high cost-sharing on the part of patients (Witgert and Hess 2012). Although qualified health plans in the marketplaces are required to offer “essential health benefits” agreed upon by the state and federal government, states and health plans still have flexibility in defining benefit packages based on benchmark plans in the state. The level of coverage of certain services, such as inpatient mental and behavioral health, may be of particular importance to safety net hospitals that often provide such services. Most private plans include deductibles and co-pays that could limit direct revenue from private insurers. However, cost-sharing subsidies are available for lower-income enrollees in marketplace plans. In addition, with more advanced information and billing systems, many safety net hospitals have become adept at collecting cost-sharing amounts and bad debt from privately insured patients (Felland and Stark 2012).

4. Reductions in Medicare and Medicaid DSH Revenue

Most safety net hospitals receive substantial amounts of revenue from DSH payments in order to at least partially offset the costs of uncompensated care to uninsured people. On average, Medicaid DSH payments accounted for 24 percent of unreimbursed care for members of the National Association of Public Hospitals (Zaman et al. 2012). Revenue from DSH has become critical to most safety net hospitals’ financial viability, as most of these hospitals also serve a high proportion of Medicaid patients, where direct reimbursement for these services is insufficient to cross-subsidize care for the uninsured.

Beginning in 2014, the ACA will reduce both Medicare and Medicaid DSH payments to hospitals. Medicare DSH payments will be cut 75 percent in 2014, although these funds will be redistributed in order to provide additional payment to hospitals that continue to experience high levels of uncompensated care. Medicaid DSH cuts will be reduced somewhat more gradually, to 50 percent by 2019. The rationale for the reductions in Medicare and Medicaid DSH payments is that increases in patient revenue through insurance coverage expansions will dramatically reduce the amount of uncompensated care that hospitals provide and, therefore, the need for supplemental payments.

The 2006 Massachusetts health reform law was similar to the ACA in that insurance coverage expansions were accompanied by reductions in subsidies from the state’s uncompensated care pool. Despite 98 percent of the state’s population being insured, increases in patient revenue were insufficient to offset the loss of state subsidies, and many safety net hospitals—including the two major safety net hospitals in Boston—sustained operating losses as a result (Kane et al. 2012; Tu et al. 2010)

Whether other safety net hospitals experience similar losses as a result of cuts in DSH will depend on a number of factors. Chief among these will be whether the state expands Medicaid coverage to adults up to 138 percent of the federal poverty level. Without additional Medicaid enrollees among those who already make up a large percentage of safety net hospital patients, it could be extremely difficult for these hospitals to offset the loss of DSH revenue through increases in privately insured patients alone. The National Association of Public Hospitals estimates that without Medicaid DSH subsidies, average margins of their member hospitals would decrease from 2.3 percent to –6.1 percent (Zaman et al. 2012). This estimate (which is based on 2010 data) does not account for the potential increases in revenue that safety net hospitals may see in states which opt to expand eligibility for the Medicaid program. On the other hand, the methodologies that states have used to distribute DSH funds in the past have varied, and some have been much less effective in targeting payments to the safety net hospitals most in need (that is, those with the greatest uncompensated care costs) (GAO 2008). In addition, the Medicaid DSH cuts will not be evenly distributed across states. The ACA requires a DSH Health Reform Methodology (DHRM) to target higher reductions in states with the lowest uninsured rates and the lowest levels of care provided to Medicaid and uninsured patients and in states that have not previously targeted DSH payments to hospitals with a high volume of Medicaid patients. Realizing that the DSH reductions could have serious consequences for safety net hospitals in states that are not expanding Medicaid coverage, CMS recently proposed a DHRM methodology only for 2014 and 2015—when the DSH reductions are relatively small—and is postponing decisions about the larger reductions scheduled for subsequent years (CMS 2013).

5. Other Federal, State, and Local Subsidies

Safety net hospitals often receive other subsidies from state and local governments to help cover operating costs and care to the uninsured. For NAPH member hospitals, these subsidies account for almost one-third of care provided to uninsured persons (Zaman et al. 2012). Public hospitals operated by county or city governments often receive local property and/or sales tax revenues—in some cases, raised specifically for the hospital through special tax districts or voter initiatives. Some states also assess fees on health care providers, payers, or others to establish pools from which funds are allocated to safety net providers to help cover their uncompensated care costs. Often, these state and local funds are eligible for matching supplemental payments from the federal government. Hospital revenues from these sources tend to fluctuate, however, due in part to how the funding mechanisms are structured, and provider taxes are under growing federal scrutiny (Felland and Stark 2012). In California, revenues from state sales tax and vehicle licensing fees are distributed to counties to help cover the expense of caring for uninsured people; most of these funds go to the core safety net hospitals.

Strained state and local budgets are resulting in reductions of these subsidies in some areas, and there is concern that there will be further reductions based on the assumption that they are less necessary due to the insurance coverage expansions (Felland et al. 2010).

6. Impact on Hospital Costs

Potentially, the largest and most direct effect of the ACA on safety net hospital costs and expenses will be to reduce the amount of uncompensated care, although, as described above, the extent to which a hospital’s total amount of “unfunded” care is reduced (including the costs of providing services to Medicaid patients that are not fully reimbursed) will depend on the amount of reduction in public subsidies and other factors that affect patient revenues.

Other costs and expenses may increase, at least in the short term, to the extent that hospitals need to expand capacity to accommodate the expected increase in demand, especially for outpatient services. For safety net hospitals positioning themselves to participate in integrated delivery systems, health information technology may need to be upgraded in order to perform the functions needed to coordinate care of patients with other providers, collect and analyze indicators of quality of care, and implement decision-support systems for chronic disease management (Andrulis and Siddiqui 2011). To compete with other hospitals for the newly insured patients, especially privately insured patients, investments and upgrades in both facilities and staffing may be needed (Lewis et al. 2012). Making the necessary short-term investments to position themselves for delivery system reforms and to compete for newly insured patients may be difficult for many safety net hospitals, which often have neither sufficiently high margins nor cash reserves to fund such investments without some public support (Ku et al. 2011). However, such investments—especially in health information technology and care coordination processes—could lead to lower costs in the longer term.

The ACA also may increase some regulatory requirements on safety net providers (AcademyHealth 2011). For example, the law requires that nonprofit hospitals perform community health needs assessments at least every three years and develop strategies to meet these needs. In addition, new requirements for tracking and reporting on quality indicators, such as inpatient readmission rates, could increase costs for data collection. To avoid financial penalties from Medicare that are associated with high readmission rates, safety net hospitals will also have to make investments in care processes, such as discharge planning and care coordination with ambulatory care providers. Because of the nature of the patient population—which often includes many homeless and mentally ill persons and patients with low compliance with medical regimens—many safety net providers are concerned that the risk-adjustment methodologies for the quality measures do not adequately account for the risk profile of their patients (Berenson and Shih 2012).

7. Organization and Dynamics of the Local Health Care System

How safety net hospitals are affected by and respond to health reform will depend in part on a number of factors related to the local delivery system. The most important of these local delivery system factors include system capacity, competition between providers, and payment and delivery system reforms.

a. Capacity of the Local Health System

It is likely that increased demand for care from insurance coverage expansions will strain the capacity of many local health systems, especially the capacity for primary care. As is currently the case, newly insured patients who are unable to find physicians willing and/or able to accept new patients, or who encounter long waiting times to see primary care physicians or specialists, are likely to end up in already crowded hospital emergency departments for treatment of relatively minor or non-urgent health care problems. Shortages of primary care physicians could make it especially hard for newly enrolled Medicaid beneficiaries to find a physician, because historically physicians have been less willing to accept new Medicaid patients than privately insured patients (MACPAC 2013; Decker 2012; Cunningham 2011). Such problems were anticipated with the implementation of Massachusetts health reform, although both physicians and hospitals in Boston reported mild to moderate increases in demand that did not overwhelm their capacity (Tu et al. 2010).

However, Boston benefitted from both low rates of uninsured persons before reform (and therefore modest increases in demand from newly insured persons) as well as a relatively large supply of health care providers, including safety net providers. Other communities will see a potentially much larger increase in the number of insured people due to the coverage expansions, and many areas with high numbers of uninsured have a lower supply of health care providers, especially states with large rural areas (Cunningham 2011). The ACA includes a number of provisions to expand health care capacity, including funding for expansion of Federally Qualified Health Centers (FQHCs), “teaching” health centers (hospital residency programs located at FQHCs), nurse-managed health centers, and the National Health Service Corps, which provides scholarships and loans to health care providers to locate in medically underserved areas. Although these reform-related capacity expansions will not directly affect safety net hospitals, increased primary care capacity in the community could increase demand for inpatient and specialty care at hospitals because of more referrals and the overall increase in the number of

people seeking medical care.

b. Competition for Newly Insured Patients

Prior research has shown that greater competition between hospitals in a community generally reduces financial margins as well as the amount of uncompensated care provided, including by safety net hospitals (Vogt and Town 2006). However, more recent research shows that the effects of competition on safety net hospitals specifically are more complex and not always consistent with expectations. Kane et al. (2012) found that some public hospitals (for example, those governed directly by elected officials) in highly competitive markets were more profitable than other public hospitals in less competitive markets.

Competition for patients newly insured through the ACA-related coverage expansions may add a new dynamic to hospital competition. Even if safety net hospitals are included in health plan networks as essential community providers, they could still face greater competition from other hospitals in the community for previously uninsured patients who gain coverage through the ACA. Similar concerns were expressed by safety net hospitals in Massachusetts prior to the state’s reform, although research indicates that previously uninsured patients at safety net providers continued to seek care at the same providers when they gained coverage (Ku et al. 2011). Convenience, proximity of the provider to where they live, the availability of culturally appropriate services for racial/ethnic minorities, and satisfaction with the quality of care were cited as reasons why newly insured persons continued to seek care at the same providers.

Increased competition for insured patients in the community could result in some non-safety net hospitals decreasing or even eliminating care provided to uninsured patients, resulting in care for the remaining uninsured becoming more concentrated in safety net providers. For the past decade, researchers have documented increasing concentration of care for the uninsured and Medicaid beneficiaries at safety net providers, as private health care providers are becoming less willing and able to accept the low reimbursement rates in Medicaid and to cross-subsidize free care to the uninsured by charging higher rates to privately insured patients (Cunningham et al. 2008; Cunningham and May 2006). With health reform, this trend may accelerate, as public and private purchasers will continue to exert pressure on health care providers to lower costs and some providers will perceive that it is no longer necessary to provide charity care because of the ACA-related expansions in coverage.

c. Collaboration and Experience with Medicaid Managed Care

The ACA also includes a number of provisions intended to accelerate the movement toward more integrated delivery systems and other reforms intended to improve efficiency, bend the cost curve, and improve quality of care for patients. These provisions are likely to have a profound impact, because historically the safety net has been fragmented in most communities, similar to the health care system in general. The safety net has often been referred to as a “patchwork of providers, funding, and programs” that varies substantially across states and communities—and one where safety net providers compete with each other at least as often as they cooperate (IOM 2000). Over the past decade, various forms of collaboration and coordination between safety net providers in many communities have increased as a way to respond to increasing demand for care by the uninsured, address gaps in access and quality of care, and stretch decreasing resources and funding. These collaboration efforts include fairly modest efforts to establish centralized referral networks for specialty care and also more comprehensive, community-wide coordination involving safety net hospitals, community health centers, and local government health departments (Cunningham et al. 2012; Hall et al. 2011).

At the same time—and largely separate from efforts by safety net providers to integrate—Medicaid has long experimented with managed care through either risk-based managed care or Primary Care Case Management programs. The proportion of Medicaid beneficiaries enrolled in some type of managed care continues to increase nationally—to 74 percent as of 2011 (Kaiser State Health Facts). Along with the expansions of Medicaid coverage in the ACA, enrollment in Medicaid managed care is likely to expand greatly. And although most of the managed care enrollees continue to be relatively low-cost children and families, many states are seeking to expand managed care to the sickest and highest-cost beneficiaries—the aged, blind, and disabled—who previously have been excluded from Medicaid managed care (MACPAC 2013). States realize that controlling the costs of their sickest beneficiaries is essential to controlling program costs, although questions remain as to whether managed care will be able to control the costs of these populations without harming medical care access and quality (Sparer 2012).

For safety net hospitals, it will be crucial to participate in Medicaid managed care networks in order to retain existing patients and attract newly insured patients covered by Medicaid. Although safety net hospitals feared that the movement to Medicaid managed care in the 1990s would create more competition for Medicaid patients, safety net hospitals have generally maintained or increased their volume of Medicaid patients; many safety net hospitals operate Medicaid managed care plans themselves, such as Denver Health and Wishard Health Services in Indianapolis (Rawlings-Sekunda and Kaye 2001). Although it was intended that Medicaid managed care would lead to decreases in hospital emergency department and inpatient care use, because beneficiaries are required to have a primary care provider who manages and coordinates their care needs, research on the effects of Medicaid managed care on hospital utilization is mixed (Sparer 2012). Some state Medicaid managed care plans have been able to reduce costs and hospital use by improving access to primary care, but in other cases health plans lack the clout to fundamentally change delivery systems used by poor people, which are often fragmented and lack coordination between primary and specialty care as well as between outpatient and inpatient care.

d. Movement Toward More Integrated Delivery and Payment Systems Intensifies

Many federal and state policymakers are realizing that effective change and cost control may require going beyond current managed care models. The more advanced collaboration and integration efforts attempt to change compensation and payment so that (in contrast to fee-for-service payment) providers are incentivized to assume more responsibility for the health and health outcomes of patients, obtain greater value in the health care they provide, monitor quality indicators, emphasize primary and preventive care, and engage in greater coordination of care with specialists. Consequently, many recent innovations have emphasized patient-centered medical homes (PCMH) that focus on team-based care centered on primary care physicians who provide both care management and care coordination with specialists (Takach 2011; KFF 2011). PCMH initiatives for the Medicaid program exist in 38 states, although they vary considerably in terms of the regions covered, types of beneficiaries (for example, dual eligible) and whether they are part of multipayer efforts that include private insurance. Eight states participate in the CMS Multi-Payer Advanced Primary Care Practice demonstration, whereas others participate in the Comprehensive Primary Care Initiative (CPCI), another CMS multipayer program based on a comprehensive program care model. The ACA also authorized the establishment of “health homes,” which are similar to PCMH but are geared specifically to beneficiaries with chronic conditions.

The newest and most far-reaching of the delivery system and payment reforms include ACOs, shared savings, and bundled payment arrangements. Although the details of these models differ, they are similar in that a group of providers (including both hospitals and community providers) are responsible for the care of a pool of patients and share in the financial risk and potential cost savings generated by improved quality and efficiency of care (indicated by defined quality metrics). Provisions in the ACA authorized ACOs for Medicare and also established a new Center for Medicare & Medicaid Innovation within CMS to test new payment and delivery models.

Although focused initially on Medicare, ACOs and similar types of payment and delivery reforms have attracted considerable interest in the private sector and among state Medicaid programs. Among states pursuing Medicaid ACOs, significant variation exists across these models in terms of implementation status, organization, geographic coverage, target population, scope of services, provider composition, and payment methods. Perhaps the most comprehensive is the Oregon Integrated and Coordinated Health Care Delivery System, which establishes coordinated care organizations statewide that will serve virtually all Oregon Health Plan enrollees—including dual eligibles—and coordinate the provision of a broad range of services, including dental, behavioral, and mental health care. Other programs are statewide in scope (Minnesota, Colorado, and North Carolina) but do not necessarily require beneficiaries to enroll in a participating ACO organization, or exclude groups of beneficiaries, such as dual eligibles. Other programs are limited geographically to cities, counties, or other local areas. Most are restricted to Medicaid beneficiaries, although several are part of multipayer initiatives (for example, Arkansas; Grand Junction, Colorado; and Vermont).

The relationships of new payment arrangements with existing managed care organizations and PCMH initiatives also vary (Gold et al. 2012). Managed care organizations act as ACOs in some states (for example, Utah); other states bypass managed care organizations and contract directly with provider-led ACOs. Some state ACO programs “evolved” from PCMH programs (for example, in North Carolina), building on the provider networks, IT infrastructure, and use of quality metrics that had already been established. Some members of the TEP convened for this project assert that ACOs will be most relevant for safety net hospitals in states that still have significant fee-for-service payment, but less so in states that already have a long-standing infrastructure of Medicaid managed care (HHS/ASPE 2013). The reason is that with risk-based payment already in place in states with extensive managed care, there is less potential to extract savings and therefore little to be gained by an ACO-like shared-savings model.

e. Safety Net Hospitals and Integrated Delivery Systems

Although it is too early to assess the effect of ACOs and other integrated delivery systems on safety net hospitals, such initiatives—if widely adopted—could have a profound impact on safety net hospitals by restructuring the delivery system to emphasize and incentivize primary care, care management, and care coordination with specialists. By design, such restructuring is intended to reduce the need for hospital inpatient and emergency department care. Already, hospitals and health systems are seeking greater alignments and partnerships with primary care providers, both to form ACOs and to provide a buffer against the expected changes in the way care is delivered and paid for in the community (Witgert and Hess 2012). Competition for patients will increase as more private and public purchasers of care require or incentivize patients to use some form of integrated delivery system.

In many communities, it will be crucial for safety net hospitals to participate in and even lead integrated systems in order to compete for patients and be included in health plan networks. A number of safety net hospitals have already developed or are a part of integrated care systems. For example, Cambridge Health Alliance (a major safety net hospital in the Boston area) provides primary care, pharmacy, and behavioral health care for Medicaid and uninsured patients (Witgert and Hess 2012). Denver Health is another fully integrated system that includes community health centers, other primary care providers, a Medicaid plan, and even public health functions. Some integration efforts are community wide, such as the Camden Coalition of Healthcare Providers in New Jersey and the Medical Home Network in Chicago.

Another way of integrating care is through local programs that seek to provide and manage a comprehensive set of services for low-income, uninsured people as if they have insurance coverage. With safety net hospitals as core components of the provider networks, the Health Advantage Program in Indianapolis, Boston Medical Center’s HealthNet, and the Healthy San Francisco program create broad delivery systems with community health centers and others in an effort to help direct patients to the most appropriate services; such systems may give these communities a leg-up on identifying and helping transition uninsured people into coverage.

Some safety net hospitals will be well positioned to form or participate in ACOs and other integrated systems, especially for their Medicaid patients. Safety net hospitals that have operated managed care plans have experience in taking on the financial risk of providing care to Medicaid patients. In addition, many safety net hospitals have already developed partnerships and collaborations with other providers in the community as part of previous efforts to coordinate and integrate care for the uninsured and Medicaid populations (Cunningham et al. 2012; Hall et al. 2011). For example, Los Angeles County operates an extensive safety net system consisting of three acute care hospitals, a rehabilitation hospital, and multiple primary care and specialty care sites as well as a Medicaid managed care organization, LA Care. It is partnering with other safety net hospitals, community health centers, and private practice physicians to form a regional ACO for Medicaid patients, with a goal of incorporating patients with other types of insurance in the future (Felland et al. 2013).

There are a number of barriers to being part of integrated systems that some safety net hospitals will encounter, however. For example, some safety net hospitals may believe that forming integrated care systems is inconsistent with their mission. Or doing so might require a legal change to their mission that could be politically difficult with their key constituencies (Witgert and Hess 2012). Similarly, questions about governance—who owns the system and who is represented on the board—could be an issue for some safety net hospitals, when the hospital and ACO organization have conflicting requirements for the composition of board membership (Shortell and Weinberger 2012).

Funding for infrastructure, staffing, and training to support integrated care may also be a barrier for some safety net hospitals (Ku et al. 2011). Infrastructure includes not only the physical facilities to expand capacity and purchase new equipment, but also upgrades to health information technology necessary to coordinate care with other providers and monitor utilization of services by patients as well as key quality indicators. Many safety net hospitals lack the access to capital, margins, or cash reserves needed for such infrastructure improvements and will need assistance from both public and private sources. As part of the American Recovery and Reinvestment Act (ARRA) of 2009, the Health Information Technology for Economic and Clinical Health (HITECH) Act includes provisions to support and incentivize providers to adopt and use health information technology to improve health care quality and care coordination; this includes extra support for some types of safety net providers such as Critical Access Hospitalsand other small rural hospitals (Gold et al. 2012; Heisey-Grove et al. 2012). Establishment of Regional Extension Centers through HITECH prioritizes engagement with safety net providers in order to reduce disparities in health care that may arise from the “digital divide” (Heisey-Grove 2012). Some states have used Section 1115 Medicaid Waivers to support development of the infrastructure needed for integrated care. For example, California’s “Bridge to Reform” Medicaid waiver included Delivery System Reform Incentive Payments (DSRIP) to safety net hospitals for such purposes (Harbage and Ledford 2012).

In addition, the risk profile of many patients who use safety net hospitals may make inclusion of the hospital or many of its patients less attractive to an ACO, which may wish, for example, to include only private and Medicare patients, who have a better risk profile as well as higher reimbursement than Medicaid patients. Risk-adjustment methodologies used to define spending targets may or may not adequately account for the high clinical risk of Medicaid patients; it will be more difficult to account for other aspects of being socially disadvantaged, such as language barriers, social isolation, and the lack of other critical social services that could make it harder to realize cost savings and improvements in quality of care (Lewis et al. 2012). For the most vulnerable patients, coordination of care with other social services will be necessary to realize the cost and quality benefits of integrated care systems. Some safety net hospitals, such as Wishard Health Services in Indianapolis, have invested in housing units for their homeless patients as a way of meeting patients’ primary care and social services needs while saving the hospital money by reducing their use of the emergency department (Katz et al. 2011).

Failure to participate in or adapt to the new, integrated delivery systems could have significant consequences for safety net hospitals and their patients. Their ability to retain existing patients and compete for newly insured patients could be undermined if health plans (both private and Medicaid) require or strongly incentivize enrollees to use providers who are part of ACOs or other integrated delivery systems. In addition, to the extent that integrated delivery systems improve the quality of care to patients—such as through better access to primary and specialty care, fewer emergency department visits, and fewer inpatient stays for ambulatory-care-sensitive conditions—these improvements will not accrue to patients of safety net hospitals that do not participate in integrated delivery systems.

8. Differences in Responses to Health Reform by Type of Safety Net Hospital

As mentioned above, safety net hospitals include not only public hospitals, but also many academic medical centers and private hospitals. These distinctions may be less meaningful and important than in the past, as many safety net hospitals—regardless of ownership—have pursued similar strategies in recent years of reducing costs, expanding into more affluent areas and services to compete for more privately insured patients, and often minimizing their safety net “image” (Cunningham et al. 2008).

Nevertheless, differences in ownership and type of safety net hospitals may still have some relevance for how they adapt to health reform. Public hospitals—many of which are controlled by state and/or local governments and are more dependent on federal, state, and local subsidies—are likely to be more constrained by their governance requirements and mission in how they respond to payment and delivery system reforms. Politically influential labor unions for hospital staff can also prevent streamlining of operations and staff in order to reduce costs (Christianson et al. 2011a). Although such constraints would seem to make them less competitive with other hospitals, Kane et al. (2012) found that public hospitals governed directly by elected officials were more profitable than safety net hospitals with other governance structures (for example, governed by a politically appointed board). Nevertheless, many local governments have seemingly helped their public hospitals by turning direct management over to an independent governing body to separate strategic and operational decision making from local politics (Felland and Stark 2012). Public hospitals may also be well positioned for changes related to health care reform, as they are usually one of the largest Medicaid providers in the community and often the only place for critical services such as trauma, burn, mental health, and neonatal intensive care units. In addition, many public hospitals have strong connections with FQHCs that can serve as the basis for increased collaboration and formation of integrated delivery systems.

The role of private hospitals in the safety net varies. In some communities—especially those with large public hospitals—private hospitals play a secondary, though still important, role in providing services to uninsured and other low-income populations. In communities without public hospitals, they often serve as the primary safety net hospital. Private hospitals receive Medicare and Medicaid DSH payments if they serve a certain volume of low-income patients, but are not directly supported by local tax revenue or controlled by local or state governments. This gives them more flexibility in altering their governance and mission—and to limit “low-revenue” patients and services—although they must still demonstrate that they are providing “community benefit” in order to maintain their tax-exempt status. Private safety net hospitals that are part of a larger hospital system in the community are often cross-subsidized by other hospitals in the system that serve a much higher number of privately insured patients. Hospitals that are part of larger systems can also have lower costs for supplies and higher payment from privately insured persons because of the greater negotiating leverage of the hospital system (Bachrach et al. 2012).

Academic medical centers are similar to private hospitals in terms of their safety net orientation. They are often the major safety net hospital in a community, including the main provider of tertiary, quaternary, and other highly specialized services to Medicaid and uninsured persons, as well as trauma treatment, burn care, and organ transplants for all people in the community. As prestigious institutions, they are better able to negotiate higher payment rates from health plans than public hospitals.

Academic centers have multiple missions of teaching, research, and providing care to vulnerable patients in the community; balancing them has become increasingly difficult in recent years. Academic activities such as research and teaching are often at odds with the improved efficiency, productivity, and lower costs needed to prepare for reform (Coughlin et al. 2012). Although many academic medical centers have traditionally been located in inner-city areas close to low-income populations, some are more aggressively expanding in ways intended to attract more lucrative services and patients. For example, although community and political pressures prevented the University of California at San Diego—the city’s largest safety net hospital—from closing their main campus in a low-income neighborhood, the university is relocating some services to more affluent areas and substantially expanding tertiary and quaternary services in more affluent suburban areas as well as areas outside the state (Tu et al. 2013).

9. Preparations for Health Reform by Safety Net Hospitals

How successfully safety net hospitals can adapt to the reforms will depend on the financial performance of the hospitals before reform, as well as the preparations they have made in anticipation of reform. In particular, the TEP identified the scope of future pension obligations of safety net hospitals that offer defined benefit plans—especially the large county- or city-run public hospital systems—as an important factor that could affect their ability to adapt and respond to health care reform because of the impact on both cash reserves and credit ratings (HHS/ASPE 2013).

Hospitals in a stronger financial position prior to reform will have more resources to make the necessary expansions in capacity to meet the increase in demand for care and compete for newly insured patients. For example, Alameda County Medical Center in northern California has made a financial turnaround and, assisted by funding from a local bond measure, is rebuilding its facilities and expanding primary and specialty care both on its campus and throughout the community (Tu et al. 2012). Safety net hospitals have also been preparing for reform by streamlining operations to control costs, upgrading infrastructure (especially electronic medical records and other health information technology), and developing partnerships with other hospitals and providers in the community in anticipation of delivery system reforms (Coughlin et al. 2012; Felland and Stark 2012). Some hospitals are using performance improvement strategies, such as the LEAN method, to identify waste, improve efficiency, and improve employee and patient satisfaction, patient safety, and quality of care (Eslan 2011).

Improvements in health information technology are especially important for improved efficiency, the ability to track and report on key quality indicators as required by many payment and delivery system reform models, decision support for chronic disease management, and improved billing processes in order to maximize reimbursement. Expanding capacity for primary care, increasing patient flows and referrals from primary care providers, and improving the “patient experience” have also been identified by some hospitals as key to competing and thriving during health reform.

Under the state’s Bridge to Reform Medicaid waiver, California safety net hospitals have been particularly immersed in health care reform preparations. In addition to the DSRIP payments to help hospitals expand their capacity and improve care processes and health outcomes, the hospitals are involved in implementing low-income health programs (Harbage and Ledford 2012). These county-based programs provide Medicaid-like benefits to low-income, uninsured people as a way to help identify who will become eligible under an expanded Medicaid program in 2014, provide care early to reduce pent-up demand and strains on provider capacity, and build patient loyalty to safety net providers. As part of this effort, safety net hospitals are focused on expanding their own primary care capacity and coordinating with community health centers, as a key focus of the program is to establish PCMH and increase the availability of primary care (Felland and Cross 2013).

10. Safety Net Hospital Outcomes

Based on the above discussion, it will be important to monitor the effects of health care reform and other changes in the delivery system on (1) hospitals’ financial performance and viability, (2) whether they maintain their mission to serve uninsured and other vulnerable populations, and (3) the quality of health care they provide.

a. Hospital Financial Performance

Because of their reliance on Medicaid revenue, the relatively large amount of care provided to uninsured patients, and decreasing revenue streams from federal, state, and local governments, most safety net hospitals operate with very low or negative margins. NAPH margins averaged 2.3 percent in 2010 compared to the 7.2 percent average margin nationwide, and many safety net hospitals operate with chronically negative margins (Zaman et al. 2012).

Whether safety net hospitals can maintain their financial viability will depend primarily on (1) their ability to offset the loss of Medicare and Medicaid DSH funds—as well as other potential decreases in state and local subsidies—with increased patient revenues from newly insured patients, including both existing patients who gain coverage and new patients they are able to attract from other health care providers, and (2) finding ways to streamline costs while at the same time making the necessary investments to position themselves for delivery system reforms and greater competition with other hospitals.

b. Maintaining Safety Net “Mission”

In the past decade, increased competition with other hospitals, rising demand from uninsured patients, and decreased revenue from payers resulted in a number of safety net hospitals adopting strategies that often mimicked non-safety net hospitals, including limiting their exposure to uncompensated care, managing payer mix, and expanding into more profitable service lines and communities to attract private payers (Cunningham et al. 2008). Some hospitals have limited their exposure to uncompensated care by reducing or eliminating certain service lines—such as mental and behavioral health—that are often heavily utilized by vulnerable populations but tend to produce less revenue than other service lines, such as oncology and cardiac care. Although such activities did not result in an explicit change of mission, some hospitals were consciously trying to change their safety net image in order to appeal to a broader spectrum of patients. In Massachusetts, such activities by some safety net hospitals were spurred in part by the state’s health reform, which—along with the decrease in state subsidies—compelled safety net hospitals to more vigorously compete for the newly insured patients, who now had a wider range of choices.

Such competitive pressures could intensify nationally. Yet, given the estimated 31 million who will remain uninsured, many policymakers agree that there will still be considerable need for safety net hospitals. As in the past, safety net hospitals will need to walk a fine line between engaging in activities designed to maintain or increase their margins and still being an essential provider of inpatient and outpatient services to low-income, uninsured people.

c. Quality of Care at Safety Net Hospitals

In addition to changes in utilization, revenue, and financial performance, health reform also has implications for measuring the quality of care provided, although there is uncertainty about the adequacy and appropriateness of some of these measures for safety net hospitals. Hospitals will now be required to monitor and track quality-of-care indicators both to comply with provisions of the ACA and to adhere to standards set by ACOs and other integrated systems. For example, the Hospital Readmissions Reduction Program established by the ACA penalizes hospitals up to 2 percent of Medicare revenue (FY 2014) for excessive 30-day readmission rates for conditions such as heart failure and pneumonia (penalties for FY 2015 and beyond increase to as much as 3 percent). Also, CMS has implemented the Medicare Hospital Value Based Purchasing Program that provides incentive payments to hospitals based on measures of clinical processes of care and patient experiences with care (Gage 2012). The TEP also raised concerns about the potential impact of CMS’s Hospital Acquired Conditions program—established under the ACA—which now penalizes hospitals 1 percent of their payments for having high rates of hospital- acquired conditions. States and localities also have initiatives designed to reward and incentivize hospitals for quality improvements. For example, DSRIP—part of California’s Bridge to Reform Medicaid waiver—was designed to incentivize primarily public hospitals for improvement projects such as infrastructure, care coordination, patient experiences, and clinical processes (Harbage and Ledford 2012).

Safety net hospitals are vulnerable to showing poor performance on a number of the standard quality measures being used in these initiatives. One study found that safety net hospitals had readmission rates that were 30 percent above the national average compared with non-safety net hospitals (Berenson and Shih 2012). There is concern that risk-adjustment methodologies may not adequately take into account the complex health and social problems of patients at many safety net hospitals, and that many of these hospitals do not have adequate financial resources needed to invest in the care processes, staff, and technologies necessary to reduce readmission rates (Lewis et al. 2012). Reductions in revenue due to poor performance on quality indicators, along with the added costs of having to invest and maintain quality-of-care monitoring, could adversely affect the financial performance of safety net hospitals.

Some researchers have suggested that quality indicators such as high hospital readmission rates do not reflect poor quality of care at the hospital, but rather the lack of follow-up care in the community and low patient compliance with care regimens—areas over which hospitals often have little control (Joynt and Jha 2012). Due to the high proportion of low-income and other vulnerable patients they serve, such limitations of quality-of-care measures would apply even more to safety net hospitals.

Quality measures that reflect improved access to primary care and care coordination between hospitals and community providers may be more meaningful for many safety net hospitals. Because of low-income people’s lack of access to timely primary and other ambulatory care in their communities, safety net hospitals often experience high levels of emergency department utilization—including for non-urgent conditions—as well as high rates of inpatient admissions for ambulatory care-sensitive conditions. Prior research has shown that when safety net hospitals are involved in integrated systems with primary care providers, there is a reduction in emergency department utilization and an increased use of primary care providers by uninsured and Medicaid patients (Roby et al. 2010; Katz and Brigham 2011). Indicators that reflect improved access to primary care and greater care coordination may be especially important to monitor at safety net hospitals.

F. Summary of Research Questions and Metrics

Consistent with the above discussion, Table 1 summarizes the main research questions for monitoring the effects of the ACA on safety net hospitals, as well as the “ideal” set of measures that would be needed to answer these questions. For the environmental scan, we do not consider the feasibility of obtaining each of the measures or the potential sources of data for a project that would monitor safety net hospitals—only what is ideally needed to monitor the effects of reform on safety net hospitals. A follow-up report to this environmental scan assesses the feasibility and potential sources of data for obtaining these measures.

To understand the impact of the ACA on safety net hospitals, it will be essential to understand how the ACA has affected the community that the hospital serves, especially in terms of changes in the number of people who are insured, the number of people who remain uninsured, and the characteristics of the remaining uninsured population. Changes in the number of people with insurance coverage in the community will directly affect changes in hospital utilization, uncompensated care, patient revenue, and hospital capacity.

It will also be important to determine how other provisions in the ACA—such as reductions in Medicare and Medicaid DSH subsidies, whether safety net hospitals are included as essential community providers in health plan networks, and benefit structures and cost-sharing levels in the Qualified Health Plans—affect both utilization and revenue. Even if safety net hospitals see a net increase in revenues, it will be important to assess the costs of certain ACA provisions, such as increased regulation of community benefit, as well as the costs of upgrades to infrastructure, staffing, quality monitoring, and capacity in preparation of reform.

It will also be important to assess key aspects of the local delivery system, especially whether strained primary care capacity has spillover effects on safety net hospitals, such as increased use of hospital emergency departments. The extent and nature of competition between health care providers in the community could have implications for safety net hospitals’ ability to retain existing patients who gain insurance coverage, as well as their ability to attract new patients. It will also be important to assess the extent of payment and delivery system reforms in the community, which will have implications for changes in demand for specific types of services (for example, primary care versus specialty care or outpatient care versus inpatient care), quality of care, and the ability of safety net hospitals to compete for patients.

Finally, it will be important to understand how unique organizational attributes of safety net hospitals, such as their ownership, financial position before reform, and specific preparations made in anticipation of reform, affect their experiences with and responses to reform. Of particular importance are efforts by safety net hospitals to form or participate in integrated delivery systems such as ACOs. As these are viewed as key to improving quality of care and controlling costs, it will be important to assess the barriers to participation and the potential consequences to safety net hospitals of not participating in integrated delivery systems.

Table 1. Research Questionsand Potential Measures for Assessingand Monitoring the Effect of Health Reform on Safety Net Hospitals.

| Topic | Research Questions | Potential Measures |

|---|---|---|

| ACA Coverage Expansions—Effect on Insurance Coverage in the Community | How will the ACA coverage expansions affect the number and proportion of people in the community with Medicaid, privately insured, and uninsured? How many uninsured in the community will remain after ACA implementation, and what are their characteristics How will coverage be affected by the state’s decision to expand or not expand Medicaid? |

|

| ACA Coverage Expansions—Effect on Demand For Care at Safety Net Hospitals | What steps have safety net hospitals taken to improve enrollment How will insurance coverage expansions affect utilization of safety From existing patients who gain coverage? From existing patients who remain uninsured? From new patients with coverage From new patients who are uninsured? Mix of inpatient, emergency department, other outpatient services? How are safety net hospitals affected by “churning” (e.g., when patients switch back and forth from Medicaid to private insurance), and what steps have the hospitals taken to minimize the effects of churning? |

|

| Effect of ACA coverage expansions on patient revenue | How will changes in the demand for care affect patient revenue?

|

|

| ACA provisions that reduce Medicaid and Medicare DSH subsidies | Will the decrease in subsidies from Medicaid and Medicare DSH and other sources be offset by increases in patient revenue from insured patients? Do safety net hospitals in states that do not expand Medicaid or continue to see high numbers of uninsured patients experience smaller DSH reductions? |

|

| ACA provision on including safety net providers as essential community providers in marketplace health plans | Is the safety net hospital included in provider networks of marketplace How does exclusion of safety net hospitals in plan networks affect utilization, revenues, and financial performance? |

|

| Benefit structure and cost-sharing in Qualified Health Plans sold in the marketplaces | How will cost-sharing (copayments, deductibles) in the marketplace health plans affect revenues from privately insured patients? |

|

| Other state and local subsidies to safety net hospitals | Will safety net hospitals see changesin other subsidies received from states, local governments, or private sources? |

|

| State Medicaid policy | Have there been changes in the state’s level of reimbursement for

Have there been changes in Medicaid benefits for services that are important for safety net hospitals? |

|

| Effects of ACA on hospital costs? | How will the ACA affect hospital costs?

|

|

| Impact of managed care | How will differences in managed care across states affect safety net hospitals?

|

|

| Local delivery system—competition | What is the extent of competition among hospitals for insured patients? Will increases in the insured population increase competition for patients between health care providers? Will increased competition affect demand for care (and patient revenue) at safety net hospitals? Will increased competition for insured patients result in increased concentration of the remaining uninsured at safety net hospitals? |

|

| Local delivery system—capacity | Is the capacity of the local delivery system sufficient to handle increased demand for care? What have been the major capacity expansions in the community, How have expansions in primary care in the community affected demand for care at safety net hospitals? How have shortages of primary care physicians and other providers affect demand for care at safety net hospitals, (e.g., use of hospital |

|

| Local health system— delivery system integration | Are there care delivery and payment reform initiatives in the community sponsored by the federal, state, local govts., or the private sector?

How does the extent of care integration/ fragmentation in a local health system affect safety net hospitals?

|

|

| Safety net hospital attributes—financial condition | How does the financial condition of the hospital pre-ACA affect experiences with health reform? |

|

| Safety net hospital attributes—capacity | Will safety net hospitals have sufficient capacity to handle increased demand?

|

|

| Safety net hospital attributes—preparations for reform | What other preparations did hospitals make to prepare for reform, Has the hospital received funding from the HITECH Act or is it part of a Regional Extension Network? What has been the effect of these initiatives on the hospital’s readiness for health reform? |

|

| Safety net hospital attributes—collaborations with other providers | Is the hospital part of a community collaboration of safety net How will the ACA change these collaborative arrangements? (e.g., are they still viable, will they expand to include Medicaid patients, will they evolve into an ACO or other integrated delivery system?) Have safety net hospitals formed or are participating in any relevant ACOs or other integrated delivery systems? |

|

| What are the advantages/ disadvantages of ACOs for safety net hospitals and their patients? |

| |

| What are the barriers that safety net hospitals face in forming or participating in ACOs? |

| |

| What are the consequences for safety net hospitals of not participating in ACOs? |

| |

| Hospital financial outcomes—viability | How will the combined effects of changes in patient revenue, direct subsidies (including Medicare and Medicaid DSH), and hospital costs affect the financial performance of safety net hospitals? |

|

| Hospital outcomes—safety net mission | To what extent will payment and delivery reforms—and the potential for increased competition for patients—affect the “mission” of safety net hospitals to care for uninsured and other vulnerable populations? |

|

| Hospitalof care outcomes—quality | What steps are safety net hospitals taking to measure, monitor, and improve quality of care? How have safety net hospitals performed on CMS quality-of-care Are CMS requirements for quality reporting (e.g., 30-day readmission rates) appropriate measures for safety net hospitals? |

|

| Is there evidence of improved access to primary care and care coordination between PCPs and hospitals? |

|

References