U.S. Department of Health and Human Services

The Nursing Home Liability Insurance Market: A Case Study of Florida

Michael Schaefer and Brian Burwell

Thomson Medstat

June 1, 2006

This report was prepared under contract between the U.S. Department of Health and Human Services (HHS), Office of Disability, Aging and Long-Term Care Policy (DALTCP) and Medstat. For additional information about the study, you may visit the DALTCP home page at http://aspe.hhs.gov/_/office_specific/daltcp.cfm or contact the ASPE Project Officer, Susan Polniaszek, at HHS/ASPE/DALTCP, Room 424E, H.H. Humphrey Building, 200 Independence Avenue, SW, Washington, DC 20201. Her e-mail address is: Susan.Polniaszek@hhs.gov.

The opinions and views expressed in this report are those of the authors. They do not necessarily reflect the views of the Department of Health and Human Services.

TABLE OF CONTENTS

- STATE ENVIRONMENT

- Florida Nursing Home Industry

- Nursing Home Quality and Oversight in Florida

- Nursing Home Litigation and Liability Insurance Trends in Florida

- Nursing Home Liability Insurance Market in Florida

- Legal and Legislative Environment in Florida

INTRODUCTION

The market for professional liability insurance for nursing facility operators is in a state of flux, and the cost of professional liability insurance has increased substantially in all areas of the country, though more so in some states than in others. At the same time, the number of insurance carriers offering liability coverage to nursing homes has decreased dramatically, as many regulated insurance carriers incurred huge losses in this product line in the late 1990s, and consequently decided to get out of the market altogether. Those carriers that have decided to stay in the market have changed the terms and conditions of liability coverage dramatically, taking on far less risk at much higher prices.a Consequently, in some areas of the country, many nursing facility owners have decided to operate without any professional liability insurance coverage whatsoever.

A major contributing factor to increased cost and reduced availability of professional liability insurance for nursing homes has been increased litigation. However, the nature of the link between nursing home litigation and the cost and availability of professional liability insurance is a matter of considerable debate in the policy arena.

This report presents an update of the nursing home liability insurance market in Florida. The report is one of five case studies that were prepared as part of a larger study sponsored by the Office of the Assistant Secretary for Planning and Evaluation within the Department of Health and Human Services (HHS) on trends and issues in the nursing home liability insurance market. Additional case studies have been conducted of the nursing home liability insurance market in the states of California, Ohio, Texas, and Georgia. The case studies are designed to provide greater insight into the dynamics of the liability insurance market by examining the experience of states with differing long-term care, economic, political, legal, and insurance landscapes. This report presents the case study on nursing home facility litigation and insurance issues in Florida.

The methodology employed in the Florida case study was somewhat different than the methodologies employed in the other four case studies. Initially, Florida was not selected as a case study state because, due to the extremely severe liability insurance crisis in that state, a number of other research projects focusing on Florida had been recently completed or were currently underway. However, it was later decided to conduct an abbreviated case study analysis of Florida, focusing on the impacts of Senate Bill 1202, a comprehensive tort reform initiative enacted by the Florida legislature in 2001. The Florida case study was conducted primarily through an analysis of secondary materials and phone interviews with key informants, including nursing home providers, state officials, plaintiff and defense attorneys, insurance carriers, and researchers.

STATE ENVIRONMENT

For the past decade, Florida has been a focal point of the national nursing home liability insurance crisis. In the mid 1990s, Florida was one of the first states to experience a significant increase in liability claims against nursing homes.1 By the late 1990s, most commercial insurers had stopped selling professional liability coverage to Florida nursing homes altogether, and had decided to exit the market. As a result, a large number of nursing home operators in the state (some stakeholders estimated 50%) were operating without liability insurance coverage at all. In 2001, the Florida state legislature enacted major tort reform legislation (Senate Bill 1202 or S.B. 1202) which had the dual policy objectives of: (1) improving the quality of care provided in Floridas nursing homes; and (2) limiting both the frequency and severity of nursing home claims. This case study provides an update on Floridas nursing home liability insurance crisis since the enactment of S.B. 1202 in 2001.

Florida Nursing Home Industry

One impact of the nursing home liability insurance situation in Florida, and to a lesser extent elsewhere, has been the divestiture of nursing home facilities by large national chains. Many of the larger, multi-state nursing facility operators adopted a strategy of identifying facilities accounting for a disproportionate share of patient liability costs and reducing their liability exposure by divesting those facilities entirely. In some cases, national chains have elected to exit specific states entirely. In a 2003 Health Care Industry Market Update conducted by the Centers for Medicare and Medicaid Services (CMS) it was noted that the top ten largest nursing facility companies accounted for a decreasing percentage of all nursing home beds.2 Moreover, the report noted that the nations largest chains were divesting at a faster rate than the overall nursing home sector. While the overall nursing home bed count dropped by 2.1%, the combined bed count of the largest ten chains declined 17.9%. The report speculated that this development may be attributable to the recent departures of some of the larger chains from states with high liability exposure such as Florida.3 As described further below, four of the top ten largest nursing home chains have completely divested their Florida operations in recent years.

In January 2002, Beverly Enterprises, the nations largest nursing facility operator, with over 40,000 beds in 355 facilities across 25 states, sold the entirety of its Florida operations. Beverlys 49 nursing facilities and four assisted living centers were purchased for $165 million by FC Properties. FC Properties arranged a leasing agreement with Florida Health Care Properties, which continues to operate the facilities. Beverly stated that the sale was part of a strategy to divest facilities that accounted for a disproportionately high share of its patient care liability costs.4

Kindred Healthcare, Inc., the nations third largest nursing facility operator with 250 facilities in 29 states, exited Florida completely in July 2003. To execute the Florida divestiture, Kindred initially purchased its 15 leased properties and then sold the properties to a third company. The lease buyout cost Kindred $64 million, approximately the same price the company negotiated for the subsequent sale of the properties. In connection with the Florida divestiture and a simultaneous divestiture of its Texas facilities, Kindred reported a pre-tax loss of $43 million for the second quarter of 2003.5

In December 2003, Mariner Health Care, Inc., completed the divestiture of its remaining facilities in Florida by terminating the leases associated with seven properties throughout the state. Mariner, the fourth largest nursing facility operator in the U.S., with 260 facilities in 20 states, once operated 27 facilities in Florida. Following the divestiture of 20 Florida facilities in August 2003, Mariners chief executive officer (CEO) cited liability cost concerns as a primary reason for the sale: [T]his transaction affords us the opportunity to substantially reduce our exposure to liability insurance costs and litigation risks in the State of Florida and at the same time de-leverage the company.6

Another top ten nursing facility operator, Extendicare Health Services, Inc., ceased all of its nursing home operations in Florida in January 2001. Extendicare, an operator of 266 long-term care facilities in 12 states, launched a plan to divest all Florida operations much earlier, in December 1999. The 2001 announcement marked the sale of its remaining 16 facilities in the state for a combined sum of $62.4 million.

In late 2000, National HealthCare Corporation (NHC), operator of 76 long-term health centers in 11 states, divested completely its nursing facility business in Florida through the sale of its 12 nursing facilities to 12 newly formed companies. At the time of the divestiture, the President of NHC stated that their decision to leave Florida was motivated by their inability to secure affordable liability insurance coverage. The NHC divestiture was especially newsworthy due to the controversial nature of its sale. The change-of-ownership papers filed by the company identified a former NHC official as the leader of the group of investors taking over the facilities.7

Nursing Home Quality and Oversight in Florida

One of the policy objectives of S.B. 1202 was to enact reforms that would improve the quality of nursing home care in Florida. Since its enactment, there have been some signs of improved quality throughout Floridas nursing facilities. Most notably, the Joint Select Committee on Nursing Homes reported in 2004 that the stakeholders who testified before the Committee unanimously agreed that the quality of care in Florida nursing homes was improving. Many experts and industry insiders attributed the improvement to the implementation of S.B. 1202, primarily its mandate for (and funding of) increased staffing levels. Nursing facilities in Florida had achieved a reduction in quality of care deficiencies, in both frequency and severity. The Florida Health Care Association testified that since S.B. 1202 the state had enacted the highest nursing home staffing standards in the nation, and Floridas facilities performed better than the national average on multiple standardized quality indicators. In testimony, these sentiments were also supported by consumers and advocates including the American Association of Retired Persons (AARP) and the National Citizens Coalition for Nursing Home Reform.8

CMS recently released data that concur with the findings of the Joint Select Committee on Nursing Homes. As part of the national Nursing Home Quality Initiative, Floridas facilities have been working with the state Quality Improvement Organization, Florida Medical Quality Assurance, Inc. (FMQAI). The CEO of FMQAI applauded the efforts of Floridas facilities, citing the 2004 CMS finding that the states nursing homes had improved significantly across several important quality indicators, including measures of chronic pain and post acute pain.9

Finally, in January 2005, Floridas Agency for Health Care Administration announced that it would begin providing small grants to fund innovative nursing home quality improvement projects. The agency is utilizing the states Quality of Long Term Care Improvement Trust Fund to provide $500,000 for the first year of grants. Nursing facilities can submit proposals with ideas to improve care and enhance the quality of life for their residents.10

Nursing Home Litigation and Liability Insurance Trends in Florida

A 2003 study conducted by researchers at Harvard Universitys School of Public Health estimated that compensation payments to plaintiffs in cases of nursing facility litigation in Florida amounted to $1.1 billion in 2001.11 Data from the Insurance Services Office (ISO) reported in 2002 indicated that claim severity in Florida was an estimated 2.1 times the national average.12 The ISO report also stated that while the national average loss ratio was 357%, Floridas average was 1072%. While only 17% of claims nationally generated losses in excess of $50,000, that number soared to 56% in Florida. A 2003 study conducted by Aon Risk Consultants estimated average loss costs per occupied bed of $10,480, over four times the national average.13 This estimate was derived from liability claims data representing 54% of all nursing home beds in the state.

The second policy objective of S.B. 1202 was to limit both the frequency and severity of nursing home claims. An initial effect of the legislation was an immediate increase in the number of lawsuits filed, as litigators rushed to file their suits before the effective date of the legislation, October 5, 2001. A survey of 675 Florida nursing facilities found that 62% were sued in the first nine months of 2001. Researchers at the University of South Floridas (USF) Florida Policy Exchange Center on Aging theorized that if S.B. 1202 was unable to improve the situation for the states nursing facilities, legislators would likely face new demands for further tort reform, including lower limits on punitive damages and new limits on compensatory damages.14 Many insurance industry insiders agreed with this point of view and believed that S.B. 1202 would fall short of curbing litigation to an extent sufficient to lure insurers back into the Florida market. Insurers praised the patient care quality measures enacted in the law but expressed the view that the legislation would have minimal impact on curbing frivolous litigation.15

Evidence of the effect of S.B. 1202 on reducing the frequency and/or severity of nursing home lawsuits is mixed. The Tampa-based plaintiff firm of Wilkes & McHugh, one of the most aggressive nursing home litigators in the entire country, reported that the number of suits brought against nursing homes in Florida in 2003 was down 17% from the year 2000. Separate research conducted by the Orlando Sentinel found that the number of lawsuits brought against nursing homes declined sharply after the enactment of S.B. 1202, and was at a four-year low in five Central Florida counties.16 Attorneys representing the nursing home industry offered an explanation for the decline in suits during testimony before the Joint Select Committee on Nursing Homes. They claimed that liability insurance policies with minimal coverage limits (e.g., $25,000) had discouraged plaintiffs from filing lawsuits. The nursing home attorneys testified that when plaintiffs lawyers learn through pre-suit inquiries that a facility has a very low coverage limit, they often choose to settle the claim within policy limits. They noted that the opposite is true as well; large insurance caps act as an incentive to bring suits.17

Other data suggest that S.B. 1202 has had a minimal effect on reducing nursing home liability costs in the state. In December 2003, the Florida Health Care Association estimated the pace of lawsuits for Florida nursing facilities continued at 2-3 per day.18 In its most recent analysis of general and professional liability insurance costs in the nursing home industry, published in March 2005, Aon Risk Consultants significantly lowered its estimates of average loss costs per occupied bed in Florida during the 2002-2004 time period from estimates made in previous studies.19 However, average loss costs in Florida still exceeded average loss costs in the country as a whole by a factor of three ($7,500 in Florida in 2004 versus $2,310 nationwide). Regarding the impact of S.B. 1202 and other tort reform bills enacted in Florida, Aon concluded based on our current study, it is inconclusive whether or not the bills have had an effect on reducing claim frequency in Florida.20 Furthermore, Aon concluded the impact of Senate Bills 1200 and 1202 on claim severity is similarly inconclusive at this time.21

One intention of S.B. 1202 was to reduce the number of frivolous lawsuits filed against nursing homes. However, some evidence has come forward suggesting that the majority of lawsuits in Florida are not frivolous. When Floridas 2001 Task Force on Availability and Affordability of Long-Term Care released its report, it concluded that all of the 225 cases it examined had merit.22 Also, two large Florida newspapers, the South Florida Sun Sentinel and the Orlando Sentinel, conducted their own review of nearly 1,000 lawsuits filed from 1997-2001, and concluded that virtually all of the lawsuits reviewed had merit.23

The reforms passed in S.B. 1202 may have had an effect on reducing lawsuits brought against facilities that carry finite policies. As discussed earlier, the provisions of S.B. 1202 did not include a mandatory minimum coverage amount or scope; it only required that facilities maintain an active liability policy. In the face of increasing costs, many facilities chose to buy finite policies with extremely low coverage limits (e.g., $25,000 per claim). Anecdotal accounts surfacing since the passage of S.B. 1202 indicate that facilities carrying policies with low limits are far less likely to be sued. Note that large self-insured chains are not similarly protected by low coverage limits, simply due to the fact that they are self-insured. This may partly explain why the large nursing home chains were leaving the Florida market altogether.

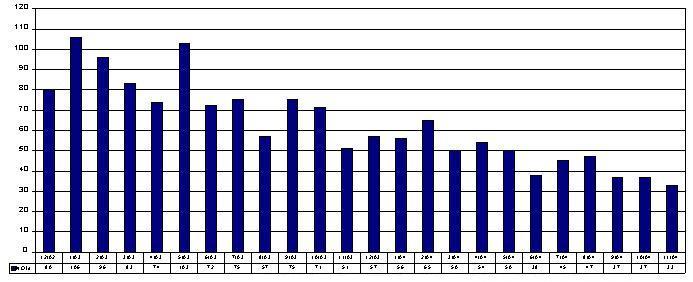

Figure 1 below, provided by the Florida Agency for Health Care Administration, shows that the frequency of attorney notices of intent has trended down in recent years. If, in fact, future research finds that lawsuit frequency is decreasing, it will remain unclear whether the decline was primarily attributable to the frivolous lawsuit deterrents set forth in S.B. 1202, or to the increasing use of finite liability insurance policies.

Nursing Home Liability Insurance Market in Florida

In the mid to late 1990s, many commercial insurers experienced significant losses in their nursing home professional liability product lines, particularly in the Gulf and southern states, as loss costs greatly exceeded insurance reserves. Consequently, many commercial insurers decided to exit the nursing home liability insurance market altogether. When researchers from the AARP Public Policy Institute commissioned Weiss Ratings, Inc., to survey nursing home liability insurers, they found that insurers mentioned Florida, Alabama, and Texas most frequently as the states where they had stopped offering coverage.24 A University of South Florida study found that from February through October of 2001, there were no admitted insurance carriers (which adhered to state insurance regulations) offering nursing home liability coverage in Florida.25 The USF study found that at the time of the survey, nearly 20% of nursing facilities in the state were without liability coverage entirely, while an additional 36% were self-insured.26 In March 2004, Floridas Joint Select Committee on Nursing Homes asked Floridas Office of Insurance Regulation (OIR) to survey the 21 admitted insurers that at one time offered liability coverage for nursing homes. OIR found that only six were still offering coverage at the time, although all on a non-admitted basis.27 The Committees final report concluded that [g]eneral and professional liability insurance, with actual transfer-of-risk, is virtually unavailable in Florida.28

Compounding the insurance availability problem, Floridas 2001 landmark passage of S.B. 1202 set forth a requirement that all facilities had to have professional liability insurance by January 1, 2002, but set forth no minimum requirement for the amount of coverage. Without any state-licensed liability insurance carriers to provide coverage, nursing facilities were left with few, generally inadequate, options for purchasing liability coverage. According to the Florida Health Care Association, most nursing home facilities faced only two legitimate options for coverage: limited coverage from commercial surplus lines carriers, or costly coverage through the Long Term Care Risk Retention Group (LTCRRG).29

Commercial insurers remaining in Florida were providing professional liability coverage on a non-admitted basis only. The USF study found that in 2001, insured Florida facilities paid a liability insurance premium minimum average cost of $6,434 per bed.30 That compared to a national per bed minimum average of $2,340. An in-depth examination of the issue confirmed the extent of the insurance availability and affordability problem when Floridas Joint Select Committee on Nursing Homes was re-appointed by the Florida Legislature in late 2003. The Committee, charged with examining the liability insurance crisis and assessing the impact of S.B. 1202, detailed in their report that excess and surplus line carriers were exclusively offering finite policies to nursing facilities with very low limits in the range of $25,000-$50,000 per single occurrence. Typically, a $25,000 finite liability policy cost a Florida nursing home operator $32,500. In the event of a liability claim, insurers paid out only up to the limit amount offered under the policy. These finite policies accomplished little more than allowing facilities to meet the coverage requirement established in S.B. 1202, without insurance carriers assuming any real risk for professional liability. Due to their size and financial stability, some of the publicly-traded, multi-state nursing facility chains were able to purchase catastrophic coverage with higher coverage amounts, albeit with very high deductibles. For example, a Florida representative for Manor Care/HCR told the Committee that they were able to purchase coverage from a European carrier with a $5 million per case deductible.31

The other option for liability insurance coverage available to Floridas nursing facilities is the LTCRRG. Announced in February 2003, the LTCRRG is a stock certificate company providing general and professional liability insurance to nursing facilities, assisted living centers, and independent living centers. The LTCRRG is licensed by the Florida OIR and was initially capitalized with an interest-free surplus note of $6 million from the Florida Agency for Health Care Administration. By law, all facilities insured through the LTCRRG must be stockholders in the Group as well. Nursing facilities were required to invest $780 per insured bed, with this capitalization charge used to repay the $6 million surplus note. Over and above the initial capitalization charge, the average premium for nursing facilities was set at $1,049 per bed. The LTCRRG limits coverage to $250,000 per claim with an aggregate limit of $500,000.32 As of January 15, 2004, the Group had 182 policy holders accounting for over $2 million in premiums. However, of the 182 policy holders, only two were nursing facilities. The vast majority (176) were assisted living facilities.33 The Joint Select Committee on Nursing Homes found that the capitalization charge was the main factor deterring nursing facilities from joining the LTCRRG.34 Given the choice, most facilities were choosing the less expensive option of purchasing the minimal amount of liability coverage available, from surplus line carriers, as previously discussed.

At the time of this writing, it is unclear when professional liability insurance carriers will return to the Florida market on an admitted basis. In a February 2004 interview, the President of Uni-Ter, a major underwriting management corporation, captured the gravity of the liability insurance availability situation for nursing facilities in Florida. [Nursing facilities] are up against it in terms of what is worse. Losing your assets by going broke because youre buying insurance or going broke because you cant afford to buy insurance and get sued.35

Legal and Legislative Environment in Florida

In response to the nursing home liability insurance crisis, the Florida legislature enacted S.B. 1202 in 2001 with the policy objective in restoring stability to the liability insurance market. The legislation included a relatively long list of reforms that were intensely negotiated between constituencies who believed that the fundamental cause of the crisis in Florida was substandard quality of care, and constituencies who believed that unrestrained litigation and frivolous lawsuits were the root cause of the situation. Some of the more significant tort reform measures in the bill included caps on punitive damages, a shortening of the statute of limitations, the application of a higher negligence standard for filing residents rights lawsuits, and the removal of automatic attorneys fees. Importantly, however, the legislation included no absolute caps on claims for non-economic damages.

Since the passage of S.B. 1202, other noteworthy legislative measures have been debated. In April 2004, a proposed constitutional amendment that may have reduced the number of lawsuits in Florida died on the floor in Committee on Health, Aging, and Long-Term Care. The proposed amendment, S.B. 3020, would have required that a claimant receive at least 70% of the first $250,000 of recovery in a medical liability claim involving a contingent fee. The amendment would have also required that claimants receive at least 90% of all damages in excess of $250,000.36

A recent court decision may also have a positive impact on reducing loss costs in Florida, thereby bringing down insurance costs. In December 2004, the Florida Supreme Court in Knowles v. Beverly Enterprises held that the survivors of deceased nursing home patients had a right to recover damages under the nursing home residents bill of rights only in cases when alleged abuse and neglect directly resulted in the patients death. The four-to-two decision applied only to lawsuits filed before May 15, 2001, the date when Governor Bush signed S.B. 1202 into law. The ruling applied to an estimated 600-1,500 outstanding cases, and according to one source, eliminated approximately 20%-50% of all active nursing home abuse and neglect cases.37

SUMMARY

Some five years after enactment, the impact of S.B. 1202 on stabilizing the nursing home liability insurance market remains inconclusive. The available data, on the whole, suggest that the frequency of nursing home lawsuits in Florida is declining. However, some attribute this decline in claim frequency to the lack of insurance coverage among many nursing home facilities, thereby reducing the incentive for plaintiffs to litigate. The divestiture of large national chains of their Florida facilities has had the same effect of limiting opportunities for plaintiffs to target nursing home operators with deep pockets. Thus, in addition to the legislative impacts of S.B. 1202 itself, it is reasonable to conclude that the dramatic increase in nursing home litigation during the late 1990s planted the seeds of its own demise by decimating the insurance market which fed it. Should the liability insurance market again stabilize, it will be interesting to observe whether increased insurance coverage for Floridas nursing home facilities might spark another increase in litigation activity in the future.

REFERENCES

-

Tanner, R. Nursing Home Liability Insurance. Washington, DC: National Conference of State Legislatures Health Policy Tracking Service. Issue Brief 1, July 2004.

-

van der Walde, L, and Choi, K. Health Care Industry Market Update--Nursing Facilities. Baltimore, MD: Centers for Medicare & Medicaid Services. Pp. 5-6, May 2003.

-

van der Walde, L, and Choi, K. op. cit.

-

Beverly Enterprises. Beverly Completes Sale of Florida Operations. Press release available at http://www.beverlycorp.com/BeverlyCorp/News/Jan_08_02+Beverly+completes+.... January 2002. Beverly Enterprises. Beverly Finalizes Lease of Florida Operations. Press release available at http://www.beverlycorp.com/BeverlyCorp/News/Dec_16_01+Beverly+finalized+.... December 2001.

-

Kindred Healthcare. Kindred Healthcare Completes Divestiture of its Florida and Texas Nursing Center Operations. Press release available at http://www.kindredhealthcare.com/Press/2003-07-01.asp. July 2003. Howington, P. Florida, Texas Exit is Costly for Kindred. Louisville Courier-Journal. July 2, 2003.

-

"Mariner Health Care Announces Divestiture of Seven Florida and Three Louisiana Facilities. PR Newswire. December 2, 2003. Mariner Health Care Announces Agreement to Divest Florida Facilities. PR Newswire. August 20, 2003.

-

Bender JP. Florida Approves NHC Divestiture. South Florida Business Journal. December 22, 2000.

-

Report of the Joint Select Committee on Nursing Homes. March 4, 2004. Available at http://www.myfloridahouse.gov/committees_detail.aspx?id=2196&sessionID=36.

-

"Florida Medical Quality Assurance, Inc.: Floridas Nursing Home Residents Receive Higher Quality of Care Today Than in 2002. PR Newswire. August 20, 2003.

-

Business to Encourage Programs to Improve Nursing Homes. Business Journal of Jacksonville. January 3, 2005.

-

Stevenson, DG, and Studdert, DM. The Rise of Nursing Home Litigation: Findings from a National Survey of Attorneys. Health Affairs. 22(2):224, 2003.

-

Insurance Services Office, Inc. Nursing Home Liability Insurance: A Discussion of the Current Insurance Crisis. Jersey City, NJ: ISO Properties. Pages 9-12.

-

Bourdon, T, and Dubin, S. Long-Term Care: General Liability and Professional Liability Actuarial Analysis. New York, NY: Aon Risk Consultants, Inc. March 3, 2003.

-

Polivka, L, Salmon, J, Hedgecock, D, and Hyer, K. Nursing Home Litigation and Liability: Implications for Long-Term Care Policy in Florida. Aging Research and Policy Report. 10:57-61, 2004.

-

Report of the Joint Select Committee on Nursing Homes, op. cit.

-

Salinero, M. Reforms appear to Have Curtailed Nursing Home Suits, Study Shows. Tampa Tribune. January 19, 2004.

-

Report of the Joint Select Committee on Nursing Homes, op. cit.

-

Florida Health Care Association. Bad News: Liability Insurance Situation Worse: Nursing Homes Continue to Close. FHCA Pulse. December 2003.

-

Aon Risk Consultants. Long Term Care: 2005 General Liability and Professional Liability Benchmark Analysis. March 21, 2005.

-

Wright, B. Nursing Home Liability Insurance: An Overview. Washington, DC: AARP. July 2003.

-

Wright, op. cit.

-

Hedgecock, D, and Salmon, JR. Lawsuits and Liability Insurance Experience of Florida Nursing Facilities, January-October 5, 2001. Tampa, FL: Florida Policy Exchange Center on Aging, University of South Florida. December 2001. Admitted insurers are companies which operate under state insurance regulations. Non-admitted insurers, which are called surplus line carriers, are companies which operate largely outside the regulated market.

-

Report of the Joint Select Committee on Nursing Homes, op. cit.

-

Hedgecock and Salmon, op. cit.

-

Report of the Joint Select Committee on Nursing Homes, op. cit.

-

U.S. RE Corporation. Florida Risk Retention Group Formed to Provide Liability Insurance to Long-Term Care Facilities. Press release available at http://www.usre.com/index.cfm?a=444. February 2003. OReilly, KB. Florida RRG Hopes to Address LTC Liability Crisis. Insurance Journal (Texas/South Central Edition). 2003.

-

Risk Retention Group. All Submission Report, January 15, 2004. 2004. Provided as a report to Floridas Joint Select Committee on Nursing Homes, op. cit.

-

Report of the Joint Select Committee on Nursing Homes, op. cit.

-

Thomas, D. Nursing All the Right Answers in the Sunshine State. Insurance Journal (Southeast Edition). 2004.

-

Hopkins, G. 2004 State Tort Reform and Litigation Update. Washington, DC: American Health Care Association. April 2004. Bill text and status available at http://www.flsenate.gov/session/index.cfm?Mode=Bills&SubMenu=1&BI_Mode=V....

-

Lynch, D. Fla. Supreme Court Curbs Survivors Right to Sue Over Nursing Home Deaths. Miami Daily Business Review. December 29, 2004.

NOTES

-

For a more extensive discussion of recent trends in the nursing home liability insurance market, see Burwell, B., Stevenson, D., Tell, E., and Schaefer, M. Recent Trends in the Nursing Home Liability Insurance Market. Report prepared for the Office of the Assistant Secretary for Planning and Evaluation HHS, June 2006. [http://aspe.hhs.gov/daltcp/reports/2006/NHliab.htm]

GLOSSARY

Admitted Carriers are commercial insurers whose nursing home liability insurance products are regulated by state departments of insurance. These carriers enjoy some advantages over non-admitted carriers. They can participate in state guaranty funds, which help protect policyholders in the case of insurer insolvency. Also, they have a marketing advantage over non-admitted carriers because some brokers, facility providers and lenders value state oversight and participation in the guaranty fund.

The Alternative Market to nursing home liability insurance is composed of various forms of self-insurance, meaning the risk is borne by the participants and not an insurance company. The different forms of self-insurance include risk retention and risk purchasing groups (RPGs), captives, rent-a-captives, and sponsored captives (Joint Underwriting Associations).

Arbitration Agreements are contracts, the terms of which are determined by an arbitrator, entered into by opposing parties. An arbitrator is a person or panel of people who are not judges and may be: (1) agreed to by the parties; (2) required by a provision in a contract for settling disputes; or (3) provided for under statute. Arbitration is designed to be a fair and equitable means of dispute resolution agreed to by both parties to avoid a court trial and the associated expenses and time investment.

Capitalization means funding the reserves of an insurance or self-insurance program to pay claims.

A Cell Captive is a captive in which member providers share administrative expenses but not risk.

A Captive is a self-formed pool of providers who share risk among themselves, thus acting as their own insurance company. Members do their own underwriting, meaning they decide among themselves which providers to admit to the captive. Members will share liability risk with the providers they admit.

Claims Made Policies provide coverage for insured events that both occur and for which a claim is made during the term of the policy. Thus, if an incident occurs, but the policy is terminated before a claim is made, liability for the incident is not insured.

Claims Occurrence Policies provide coverage for all incidents and events that occur during the term of the policy, regardless of when a liability claim is made, or when a lawsuit is settled.

Collateral Damages are damages incurred by the plaintiff that are already covered by other sources of payment. Collateral source offset rules reduce awards by denying plaintiffs compensation for losses that are recouped from other sources, such as health insurance. These rules aim to prevent plaintiffs from double dipping by recovering for losses for which the plaintiff has already been remunerated through other sources of payment.

Deductibles are initial amounts of claims incurred by the policyholder not covered by the insurance policy. Insurance coverage begins only for losses incurred above the deductible amount.

Economic Damages in civil litigation is compensation due the plaintiff for financial losses caused by the wrongful actions of another party (e.g., awards for the medical bills of a nursing home resident caused by an abusive employee).

Estimated Liability Costs are approximate calculations of expenses for damages to which a nursing home is exposed. Because estimates are derived from information provided by nursing homes and the cost of settlements of lawsuits is confidential information known only to the insurance carrier, plaintiffs attorney and defense attorney, these calculations are only estimates and are subject to change.

General Liability Claims/Losses are amounts a nursing home liability insurer is legally obligated to pay as damages to a plaintiff due to bodily injury or property damage.

A Joint Underwriting Association is a state-sponsored organization that creates insurance pools and functions as an insurer in markets without a significant number of licensed insurers. It has the power to sell insurance policies, collect premiums, and purchase reinsurance and it can usually guarantee a certain level of premium rates to its members. It can also levy surcharges on policyholders and, in some cases, on licensed insurers selling liability insurance, to create reserves to pay claims.

Joint and Several Liability in civil litigation is a situation in which the concurrent acts of two or more defendants bring harm to the plaintiff. Such acts need not occur simultaneously, but must contribute to the same event. In such a case, the damages may be collected from one or more of the defendants. If the court does not apportion blame in specific shares, the damages may be collected from any and all defendants. If a defendant does not have the financial wherewithal to pay, the others must make up the difference.

Non-admitted Carriers, also called Surplus Line Carriers, are commercial insurers whose nursing home liability insurance products are not regulated by state departments of insurance. These insurers enjoy some advantages over admitted carriers. They have greater flexibility in designing and pricing products. Because they are not subject to state regulation, they can also change coverage forms and application protocols more quickly. However, they must pay an excess and surplus lines tax that is not levied on admitted carriers. They cannot participate in state guaranty funds, which help protect policyholders in the case of insurer insolvency

Non-economic Damages in civil litigation is compensation due the plaintiff for intangible harms (e.g., pain and suffering).

Nursing Home Liability Insurance is indemnification of nursing home providers against damages for negligent care and abuse.

Nursing Home Residents Rights Statutes are state and federal laws to protect each nursing home residents civil, religious and human rights.

Offshore Captives are captives located outside the United States. The most popular host states for offshore captives include Bermuda, Guernsey and the Cayman Islands.

Premium is the charge paid by a policyholder for insurance coverage.

Professional Liability Claims/Losses are amounts a nursing home liability insurer is legally obligated to pay as damages and associated claims and defense expenses to a plaintiff due to a negligent act, error or omission in a nursing home providers rendering or failure to render professional services.

Punitive damages in civil litigation means monetary compensation awarded by a judge or jury which exceeds the losses suffered by the injured party in order to punish the defendant.

Regulated Insurance Carriers are admitted carriers (see definition above).

Reinsurance is the practice of insurance carriers ceding risk to other firms, called reinsurance companies, in order to limit their liability exposure. Reinsurance companies essentially provide insurance to insurance companies. Instead of assessing the risk of individual policyholders, reinsurance companies assess risk on a broader scale, such as on the basis of a particular product-line (nursing home liability insurance) or a geographic region.

A Rent-A-Captive is a captive, usually formed by an insurance company, broker or captive manager, and rented out to users (in this case nursing home providers) who avoid the cost of funding their own captive. The user provides some form of collateral so that the rent-a-captive is not at risk from any underwriting loss suffered by the user.

Risk Management Programs are structured approaches to purposefully limit liability risk. They include systematic efforts to improve and maintain high standards for care quality, but can also include additional management techniques to minimize liability exposure, such as improving written documentation. They are often formalized within the management structure of nursing home providers in the form of Risk Management Committees, and/or a designated Director of Risk Management along with formal Risk Management plans that are implemented and monitored by senior management.

A Risk Retention Group (RRG) is an insurance company that is owned by its members. The members of an RRG come from the same industry. For instance, nursing home providers can form an RRG in order to obtain nursing home liability coverage.

A Settlement is an agreement reached between the legal counsel of the plaintiff and the defendant that terminates a civil litigation before a verdict is reached by the court.

Tort Reform generally means a movement intended to curb litigation and damages in the civil justice system. With respect to nursing home liability insurance, many states have enacted tort reform through legislation and it has changed the legal framework under which residents and/or family members can seek damages for negligent or abusive care practices. States also placed limits on the amount of damages that could be awarded to plaintiffs and/or their family members, particularly non-economic damages for pain and suffering.

Underwriting is the process by which an insurer assesses the risk of insuring a particular applicant for coverage. Risk retention groups also underwrite by assessing the risk of accepting a prospective member.

FIGURES

| FIGURE 1: Nursing Home Notices of Intent December 2002 - November 2004 |

|

| SOURCE: The State of Florida Agency for Health Care Administration at http://www.fdhc.state.fl.us/MCHQ/Long_Term_Care/FDAU/Reports.shtml. |

REPORTS AVAILABLE

- Recent Trends in the Nursing Home Liability Insurance Market (Main Report)

- HTML: http://aspe.hhs.gov/daltcp/reports/2006/NHliab.htm

- PDF: http://aspe.hhs.gov/daltcp/reports/2006/NHliab.pdf

- Nursing Home Liability Insurance Market: A Case Study of California

- HTML: http://aspe.hhs.gov/daltcp/reports/2006/NHliab-CA.htm

- PDF: http://aspe.hhs.gov/daltcp/reports/2006/NHliab-CA.pdf

- Nursing Home Liability Insurance Market: A Case Study of Florida

- HTML: http://aspe.hhs.gov/daltcp/reports/2006/NHliab-FL.htm

- PDF: http://aspe.hhs.gov/daltcp/reports/2006/NHliab-FL.pdf

- Nursing Home Liability Insurance Market: A Case Study of Georgia

- HTML: http://aspe.hhs.gov/daltcp/reports/2006/NHliab-GA.htm

- PDF: http://aspe.hhs.gov/daltcp/reports/2006/NHliab-GA.pdf

- Nursing Home Liability Insurance Market: A Case Study of Ohio

- HTML: http://aspe.hhs.gov/daltcp/reports/2006/NHliab-OH.htm

- PDF: http://aspe.hhs.gov/daltcp/reports/2006/NHliab-OH.pdf

- Nursing Home Liability Insurance Market: A Case Study of Texas

- HTML: http://aspe.hhs.gov/daltcp/reports/2006/NHliab-TX.htm

- PDF: http://aspe.hhs.gov/daltcp/reports/2006/NHliab-TX.pdf