Joshua M. Wiener, Galina Khatutsky, Nga Thach, Angela M. Greene and Benjamin Allaire

RTI International

Derek Brown

Washington University

Helen Lamont, William Marton and Samuel Shipley

Office of the Assistant Secretary for Planning and Evaluation

July 2015

Printer Friendly Version in PDF Format: http://aspe.hhs.gov/pdf-report/findings-survey-long-term-care-awareness-and-planning-research-brief (8 PDF pages)

| Using data from the 2014 Survey of Long-Term Care Awareness and Planning, a number of analyses were undertaken to better understand public knowledge about long-term care, concerns related to aging and disability, plans to address needs, and preferences about different aspects of long-term care insurance. The survey showed that knowledge of long-term care is low among the general population aged 40-70: most were not well-informed about long-term care costs, the role of Medicaid, or nursing home length of stay. Losing independence was the top concern followed by being a burden to one's family. Respondents were willing to undertake a number of actions if faced with a chronic disability. Most respondents believed that long-term care financing is largely an individual rather than government responsibility, and have a strong preference for voluntary initiatives, including private long-term care insurance and voluntary public long-term care insurance. However, when asked about specific insurance preferences, price, the length of coverage, and the daily benefit amount were rated as the most important attributes of long-term care insurance policies. |

Long-term care (LTC) is a range of services and supports to meet personal care needs. Most LTC is not medical care, but rather assistance with the basic personal tasks of everyday life, such as eating, dressing, and bathing (Congressional Budget Office, 2013). In 2011, 5.7 million people--about 16 percent of the elderly Medicare population --needed assistance with LTC according to a widely-used definition established by the Health Insurance Portability and Accountability Act of 1996 (Drabek & Marton, 2015). LTC can be very expensive, and Medicare and most private health insurance plans do not cover these costs. In 2014, nationally, the median cost of a semi-private room in a nursing home was $77,380 per year and the median cost of home health aide care was $20 per hour (Genworth Financial, 2014).

With the aging of the population and growing demand for LTC, it is important that Americans take steps toward preparing for LTC, both individually and as a society. This Research Brief summarizes findings from the 2014 Survey of Long-Term Care Awareness and Planning with the goal of contributing to our understanding of the concerns of people, plans to address needs, and preferences about different aspects of LTC insurance and financing.

Data and Methods

In 2014, the U.S. Department of Health and Human Services, Office of the Assistant Secretary for Planning and Evaluation contracted with RTI International and GfK Research to develop and field a Survey of Long-Term Care Awareness and Planning. A nationally representative sample of 15,298 non-institutionalized United States adults 40-70 years old completed the survey.

Respondents were asked to complete:

-

A survey containing questions on: (1) self-perceived longevity and the risk of needing LTC; (2) basic financial literacy and psychological characteristics such as risk tolerance; (3) LTC knowledge and LTC experience; (4) beliefs and concerns about LTC; (5) retirement and LTC planning; (6) LTC information gathering and decision making; (7) attitudes toward LTC financing options; and (8) core demographic and socioeconomic information.

-

A discrete choice experiment (DCE), a form of conjoint analysis, designed to elicit respondent preferences among various attributes of LTC insurance.

Findings

Self-Reported Longevity Risk and Risk of Moving to a Nursing Home

-

The majority of respondents had high expectations of their longevity, with 82.1 percent believing that they had at least a 50 percent chance of surviving to age 85 or older. More than one-fifth of respondents (21.8 percent) rated their chances of living to old age as 90-100 percent. Although there was not much difference by age, women were more likely to think that they would live to age 85 or older.

-

Despite high expectations of surviving to old age, not as many respondents expected to need nursing home services in the future. Although a significant proportion of respondents believed that there was a substantial risk of their using nursing home care, 42.9 percent assessed their chances of moving into a nursing home in the future as less than or equal to 20 percent. Only 3.8 percent believed they have a 90-100 percent chance of ever moving into a nursing home.

Concerns about Becoming Disabled

-

"Losing independence," was the top concern expressed by almost all respondents (90.6 percent), followed by "being a burden to your family" (83.5 percent), and "losing control and choice over LTC you might need" (83.3 percent). Being unable to depend on family/friends for care was the least of the seven concerns, although two-thirds (65.3 percent) still reported worrying about this possibility.

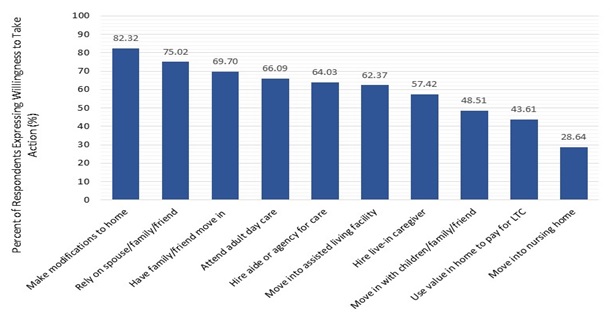

Willingness to Take Long-Term Care Actions

-

Respondents were asked about how willing they would be to take specific actions should they become disabled and need LTC (Figure 1). The highest proportions of respondents were willing to make modifications to their homes (82.3 percent); rely on a spouse, family member, or friend for care (75.0 percent); and have a family member or friend move in (69.7 percent). Fewer than half were willing to move in with children, family members, or a friend (48.5 percent), or use the value of their home to pay for LTC (43.6 percent).

-

Not surprisingly, moving into a nursing home was the least favored choice. Just over a quarter of respondents indicated that they would be willing to move into a nursing home if they became disabled (28.6 percent).

FIGURE 1. Willingness to Take Specific Actions in the Event of a Disability

(N=15,298)

SOURCE: RTI analysis of the 2014 ASPE Survey of Long-Term Care Awareness and Planning.

NOTES: Percentages are shares of respondents who reported being "very"/"somewhat" willing to take an individual action.

Experience, Knowledge, and Awareness of Long-Term Care

-

Americans do not have a good grasp of the high costs of LTC. Only about one-fifth of all respondents (20.2 percent) correctly estimated the average cost of a month of nursing home care in their state of residence, and 15.3 percent correctly estimated the average cost of one hour of home health aide care in their state. Aside from those who estimated nursing home and home health costs incorrectly, more than one-third (36 percent) did not know enough to choose a response (not shown).

-

Respondents also did not understand how LTC is currently financed. Only a quarter of all respondents (25.3 percent) correctly identified Medicaid as the government program that pays the most for LTC services in the United States.

Preferences for Long-Term Care Financing

-

Table 1 displays a portion of respondents' preferences for LTC financing options. Most supported individual responsibility and voluntary, largely private, options. Approximately three-fifths of respondents (58.7 percent) said they strongly agreed/agreed that it is the responsibility of individuals to finance their LTC; conversely, about a third of people (37.1 percent) stated that they strongly agreed/agreed that it is the responsibility of government to help pay for LTC.

-

Respondents were generally supportive of the concept of LTC insurance, but many had competing demands for their money. Almost two-thirds of respondents (66.4 percent) either agreed or strongly agreed that "knowing that I have some LTC insurance will give me peace of mind," but almost half (44.4 percent) reported that they had other priorities for their money than buying LTC insurance.

-

Respondents were most supportive of the government allowing LTC insurance purchase through tax policy and other funding sources. Nearly 70 percent of respondents either agreed or strongly agreed that the government should allow the purchase of LTC insurance with Individual Retirement Accounts (IRAs) and 401(k)s and over 60 percent felt that the government should promote the purchase of LTC insurance through taxes.

-

Overall, respondents favored voluntary programs, especially those that would promote private LTC insurance. Fully 62.9 percent of respondents supported a voluntary public LTC insurance program. In contrast, 18.4 percent of people supported a mandatory public LTC insurance program.

-

Most respondents (62.7 percent) either agreed or strongly agreed that they did not want the government to "tell me what to do about LTC insurance."

-

Although negative views were expressed of both private insurers and government, stronger negative views were expressed of the potential role for government. A slight majority of respondents (51.1 percent) strongly agreed/agreed that they do not trust the government to run a public LTC insurance program, while 32.3 percent did not trust private insurers.

| TABLE 1. Preferences for LTC Financing | |||

|---|---|---|---|

| Survey Questions | Strongly Agree/ Agree (percent) | Neutral (percent) | Strongly Disagree/ Disagree (percent) |

| It is important to plan now for the possibility of needing LTC services in the future. | 71.2 | 26.0 | 2.8 |

| Responsibility for LTC | |||

| Responsibility of individuals to finance their LTC | 58.7 | 32.6 | 8.7 |

| Responsibility of government to help pay for LTC | 37.1 | 37.9 | 25.1 |

| Government should: | |||

| Promote LTC insurance through taxes | 62.4 | 28.9 | 8.7 |

| Allow LTC purchase with IRAs and 401(k)s | 69.2 | 26.2 | 4.6 |

| Require all people to purchase LTC insurance | 15.7 | 35.2 | 49.1 |

| Pay LTC costs when insurance benefits run out | 40.9 | 40.0 | 19.1 |

| Offer voluntary, public LTC insurance plan | 62.9 | 26.7 | 10.4 |

| Establish mandatory, public LTC program | 18.4 | 34.4 | 47.3 |

| Personal involvement with LTC financing | |||

| Everyone should have LTC insurance and a mandatory, public program is the way to accomplish that | 19.5 | 34.4 | 46.1 |

| Everyone should have LTC insurance, but private companies should provide the insurance | 23.2 | 49.9 | 27.0 |

| Requiring people to buy LTC insurance is OK, if price is not too high | 40.5 | 25.5 | 34.1 |

| Knowing that I have some LTC insurance will give me peace of mind | 66.4 | 27.1 | 6.5 |

| Paying for LTC is individual responsibility, not government | 46.6 | 38.1 | 15.3 |

| Government should not tell me what to do about LTC insurance | 62.7 | 28.1 | 9.2 |

| I have other priorities for my money than buying LTC insurance | 44.4 | 41.9 | 13.8 |

| I do not trust government to run a LTC insurance program | 51.1 | 33.0 | 15.9 |

| I do not trust private insurers | 32.3 | 46.7 | 21.1 |

| SOURCE: RTI analysis of the 2014 ASPE Survey of Long-Term Care Awareness and Planning. NOTE: All results are presented weighted. | |||

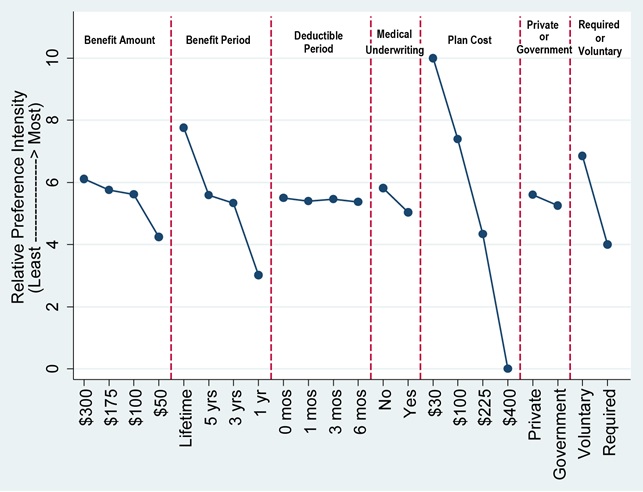

Relative Preferences for Long-Term Care Insurance Plan Features

As part of the DCE portion of the survey, respondents were asked to choose between a series of hypothetical LTC insurance policies with various attribute levels. The attributes included Daily Benefit Amount, Benefit Period, Deductible Period, Medical Underwriting, Plan Cost, Sponsorship and Required Enrollment.

The Deductible Period refers to the period during which you have to pay for care out of pocket before you are eligible to receive benefits from insurance. Sponsorship refers to what entity will offer the insurance--with the DCE, respondents were asked to choose between policies offered by private companies or the Federal Government. Finally, for Required Enrollment, respondents were asked if they prefer insurance to be Voluntary, that is you may buy the policy if you like, but you do not have to, or Universal, where everyone is required by law to purchase the insurance.

Figure 2 displays respondents' relative preferences for features of the hypothetical policies. The estimates in this table are scaled to show respondents' relative preferences among the various insurance attributes, with 10 being the highest (most desired) and 0 being the lowest (least desired). Figure 2 also shows the relative importance of these attributes across their full range. Specifically, those with the largest range (i.e., premium cost) were the most important overall in determining choice behavior, and those with the smallest range (i.e., deductible levels or sponsorship) were least important. A 5 in this table represents an average of all the features, so larger deviations from 5 indicate more importance--desirable above 5 and undesirable below 5.

FIGURE 2. Relative Preferences for LTC Insurance Plan Features

SOURCE: RTI International analysis of the 2014 ASPE Survey of Long-Term Care Awareness and Planning.

NOTES: Figure depicts results, rescaled in terms of relative importance to each other, 0 = least preferred, 10 = most preferred.

-

Respondents expressed strong preferences for voluntary, low-cost policies with long benefit periods and high benefit amounts. A $30 per month premium is the most desired attribute and a $400 per month premium was the least desired attribute. There was not much variation across deductible periods. Respondents exhibited strong preferences over the length of the benefit periods: one-year policies were strongly undesirable, while lifetime benefits were highly desirable. People strongly favored $300 a day benefits versus $50 a day benefits.

-

Another way to look at these preferences is to compare a simulated hypothetical insurance plan with the same features ($100 daily benefit amount and three-year duration and holding all other attributes constant) across a series of premium costs ($25, $50, $75, $125, $150 and $250 per month) and against the option of "no insurance." In a voluntary setting, predicted demand exceeds 50 percent at approximately the $50 per month premium cost. In other words, above this cost, less than half are expected to voluntarily choose LTC insurance.

Conclusion

Analysis of the Survey of Long-Term Care Awareness and Planning indicates that knowledge of LTC is low among the general population aged 40-70: most were not well-informed about LTC costs, the role of Medicaid, or nursing home length of stay. Respondents expressed a wide variety of concerns related to aging and disability with losing independence being the top concern. When asked what they would be willing to do if disabled, many said make modifications to homes; rely on a spouse, family/friend; or have family or a friend move in with them. However, a majority said they would not move in with family/friends, use the value in their home to pay for LTC, or use nursing home care. Respondent's opinion on the use of home equity may reflect the important role homes have in American culture and may reflect a desire either to leave an inheritance for their families or to preserve their major asset for some other adverse event.

In general, and when responding to the survey questionnaire, respondents favored individual responsibility over government responsibility for LTC financing. Moreover, respondents generally favored voluntary initiatives, both private and public, although they had a stronger preference for private LTC insurance. Mandatory public LTC insurance did not garner much support. Respondents also voiced substantial mistrust of how the government would manage a public LTC insurance program. However, when given an actual choice between hypothetical LTC insurance policies, respondents tended to focus almost exclusively on price, the length of coverage, and to a lesser extent, the daily benefit amount of the policies. Respondents had a preference for voluntary insurance, but not as highly as their preference for low price and extensive coverage. Compared to these preferences, respondents were much less concerned about the deductible period, medical underwriting, or sponsorship of the plan--whether by the government or private sector. Given the somewhat conflicting views of the public, the challenge for policymakers is to find a reform strategy that will both successfully address the problems of the LTC system and have broad political support.

References

Congressional Budget Office (2013). Rising Demand for Long-Term Services and Supports for Elderly People. http://www.cbo.gov/sites/default/files/private/cbofiles/attachments/44363-LTC.pdf.

Drabek J, & Marton W (2015). Measuring the Need for Long-Term Services and Supports Research Brief. ASPE unpublished data.

Genworth Financial (2014). Genworth 2014 Cost of Care Survey home care providers, adult day health care facilities, assisted living facilities and nursing homes. Richmond, VA: Genworth Financial. https://www.genworth.com/dam/Americas/US/PDFs/Consumer/corporate/130568_032514_CostofCare_FINAL_nonsecure.pdf.

This Research Brief was authored by Joshua M. Wiener, Galina Khatutsky, Nga Thach, Angela M. Greene and Benjamin Allaire (RTI International); Derek Brown (Washington University); and Helen Lamont, William Marton and Samuel Shipley (Department of Health and Human Services). It summarizes findings from the 2014 Survey of Long-Term Care Awareness and Planning with the goal of contributing to our understanding of the concerns of people related to aging and disability, plans to address needs, and preferences about different aspects of long-term care insurance and financing.

This Brief was prepared through intramural research by the U.S. Department of Health and Human Services, Office of the Assistant Secretary for Planning and Evaluation, Office of Disability, Aging and Long-Term Care Policy. For additional information about this subject, visit the DALTCP home page at http://aspe.hhs.gov/office_specific/daltcp.cfm or contact HHS/ASPE/DALTCP, Room 424E, H.H. Humphrey Building, 200 Independence Avenue, S.W., Washington, D.C. 20201, Helen.Lamont@hhs.gov, William.Marton@hhs.gov, or Samuel.Shipley@hhs.gov.