U.S. Department of Health and Human Services

Exploratory Study of Health Care Coverage and Employment of People with Disabilities: Literature Review

David Stapleton, Gina Livermore, Scott Scrivner, and Adam Tucker

The Lewin Group, Inc.

October 27, 1997

PDF Version: http://aspe.hhs.gov/daltcp/reports/1997/eshcclit.pdf (64 PDF pages)

This report was prepared under contract #HHS-100-96-0012 between the U.S. Department of Health and Human Services (HHS), Office of Disability, Aging and Long-Term Care Policy (DALTCP) and Lewin-VHI, Inc. For additional information about this subject, you can visit the DALTCP home page at http://aspe.hhs.gov/_/office_specific/daltcp.cfm or contact the office at HHS/ASPE/DALTCP, Room 424E, H.H. Humphrey Building, 200 Independence Avenue, S.W., Washington, D.C. 20201. The e-mail address is: webmaster.DALTCP@hhs.gov. The Project Officer was Kathleen Bond.

The opinions and views expressed in this report are those of the authors. They do not necessarily reflect the views of the Department of Health and Human Services, the contractor or any other funding organization.

TABLE OF CONTENTS

I. INTRODUCTION

A. Background

B. Overview of the Report

II. THE COMPLEX RELATIONSHIPS AMONG INSURANCE ACCESS, EMPLOYMENT, AND PROGRAM PARTICIPATION

A. The Decision to Seek Employment

B. The Decision to Leave Employment

A. Medicaid

B. Medicare

C. Self-Reports of the Importance of Health Insurance to Employment and Program Participation

A. Unmarried Mothers

B. Older Workers

C. The Elderly

V. HEALTH INSURANCE AND EMPLOYMENT OF PEOPLE WITH DISABILITIES

A. Employment and Program Participation of Persons with Disabilities

B. Health Insurance Coverage and Expenditures of Persons with Disabilities

VI. CONCLUSION

A. What We Know

B. Significant Gaps

C. Work in Progress

D. Recent Legislative Proposals

VII. REFERENCES

LIST OF EXHIBITS

EXHIBIT 1: Earnings and SSI and Medicaid Benefits for a Non-Married SSI Recipient Living in Pennsylvania, 1996

EXHIBIT 2: Relationship Between Earnings and SSI and Medicaid Benefits for an SSI Recipient Participating in 1619 (a) and (b)

EXHIBIT 3: Patterns of Disability and Work, 1990

EXHIBIT 4: Work Limitation and Work Status, 1989

EXHIBIT 5: Patterns of Employment by Education and Disability Status, 1990

EXHIBIT 6: Employment Status by Age and Disability Status, 1990

EXHIBIT 7: Incidence of Health Conditions among Those Described as Unable to Work, 1990

EXHIBIT 8: Ten Most Frequently Reported Conditions as Cause of Physical, ADL, or IADL Limitations Among Persons Aged 15-64 Reporting a Limitation, 1991-1992

EXHIBIT 9: Receipt of Benefit Payments by Disability Status and Gender (Percent), 1990

EXHIBIT 10: Work Limitation and Benefit Receipt, 1989

EXHIBIT 11: Mean Monthly Earnings by Age, Years of School Completed, and Disability Status, 1991

EXHIBIT 12: Activity Limitations, Employment Status, and Health Insurance (Percent Distribution), 1990

EXHIBIT 13: Health Insurance and Employment Status, 1990

EXHIBIT 14: Health Insurance Coverage of Persons 18-64, 1989

EXHIBIT 15: Percentage of Persons with Expenditures for Each Type of Health Care Service and Average Expenditure per User, Persons under Age 65, 1987

EXHIBIT 16: Percent of Persons with Expenditures for Each Type of Health Care Service and Average Expenditure per User, Persons Under Age 65, 1987

EXHIBIT 17: Incidence (Percent) of Catastrophic Expenditures Among Selected Population Subgroups for Three Alternative Measures, 1987

EXECUTIVE SUMMARY

This literature review examines empirical evidence on health care coverage, employment, and public program participation among people with disabilities. The review is part of a larger project investigating the relationship between health care coverage and the employment of people with disabilities contracted for by the Office of Disability, Aging, and Long-Term Care Policy (ODALTCP), Assistant Secretary for Planning and Evaluation (ASPE) in the U.S. Department of Health and Human Services with funds provided by the Office of Disability (OD) in the Social Security Administration (SSA). Other components of the overall project will include analyses of recent national data on employment and health care coverage, analyses of patterns of employment among SSI recipients in the work incentive program that allows health care benefits to continue after earnings are too high for receipt of cash benefits, and patterns of employment in two States where there have been expansions in the Medicaid program.

This is a time of intense discussion about reforms to federal programs that serve people with disabilities. People with disabilities cite fear of losing medical benefits and the services provided under Medicare and Medicaid as significant barriers to employment. Formal proposals for extending Medicare and Medicaid coverage to working people with disabilities have come from many sources including the National Council on Disability and the National Academy of Social Insurance. In addition, several bills that would extend health care coverage beyond that allowed under current law for working people with disabilities have been introduced in the Congress.

While most policy makers agree that current programs create substantial work disincentives for people with disabilities, there is much less agreement about the actual impact of the various disincentives and their relative importance. Advocates of expanded public insurance for people with disabilities are asked for empirical evidence of the actual "effect" of health care coverage on employment and program participation. The goal of this literature review is to synthesize information that may have direct value to policy makers; to provide background for the new research to be conducted under the project; and to identify gaps in knowledge about the importance of health care coverage in the employment and program participation decisions of persons with disabilities.

Major general findings of the literature review include the following:

-

Health care costs for people with disabilities are generally much higher than for those without disabilities. On average, total health expenditures for non-elderly people with disabilities are about six times greater than expenditures of their non-disabled counterparts, and out-of-pocket expenditures are three times greater. One study found that persons with disabilities are significantly more likely to experience catastrophic out-of-pocket expenditures than persons without disabilities.

-

The eligibility requirements for Medicare and Medicaid create financial incentives that discourage or encourage work, depending on the current status of the individual. For people with disabilities, qualification for Medicare and Medicaid is primarily contingent on participation in the Social Security Disability Insurance (SSDI) and Supplemental Security Income Insurance (SSI) programs which require that individuals not engage in substantial work, thereby creating a strong work disincentive for individuals with disabilities who lack health care benefits. For those on the programs, there are work incentive programs which allow for the continuation of health care benefits, but continued coverage is limited either in time (SSDI) or up to certain earnings levels (SSI). The programs thus create odd incentives for working persons with disabilities who lack insurance--they must reduce work to qualify for benefits, but subsequently may increase work and still maintain benefits, but only under limited circumstances.

-

Many SSDI and SSI beneficiaries say they would work, or work more, except that they are afraid of losing their Medicare or Medicaid benefits. There is a growing body of anecdotal and survey evidence that people with disabilities identify loss of health care coverage as an important reason for not working or not working enough to exit from SSI or SSDI. The review found several examples of studies in which persons with disabilities, when asked, have indicated that the loss of health care benefits provided through Medicare or Medicaid was a deterrent to work.

-

Health care coverage has substantial effects on the employment or program participation of other groups--single mothers, older workers, and the elderly. A number of studies find convincing evidence of a relationship between access to health care coverage and work and program participation decisions. Continued Medicaid coverage has been shown to have a positive effect on AFDC participation among singe mothers. A provision of the Medicaid program that allows elderly, low income Medicare beneficiaries to obtain Medicaid coverage without first having to be eligible for SSI is shown to significantly reduce SSI participation for that group. Access to post-retirement health insurance benefits is positively related to exits from the labor force among older workers.

In addition to reporting on the results of past research, the review provides statistics on patterns of disability and work using various definitions of disability. It also includes data on health insurance coverage and type of health care expenditures for persons with disabilities. A final section of the review identifies significant gaps in knowledge about health care coverage and employment, briefly reports on research in progress, and summarizes recent legislative proposals to extend public health care benefits to working persons with disabilities beyond what is allowed in current law.

I. INTRODUCTION

A. Background

The Office of the Assistant Secretary of Planning and Evaluation (ASPE) in the Department of Health and Human Services, using funds provided by the Social Security Administration (SSA), has contracted with The Lewin Group, Inc. to examine empirical evidence on the relationship between health insurance, employment, and program participation of people with disabilities. The Office of Disability, Aging, and Long-term Care (ODALTCP) in ASPE is directing the study. This literature review is a project report.

This study is being conducted during a time of intense debate about reforms to federal programs that serve people with disabilities. Most policymakers agree that the current programs create substantial work disincentives for people with disabilities, but there is much less agreement about the actual impact of the various disincentives and their relative importance. One set of policy options concerns changing the links between Medicare and the Social Security Disability Insurance (DI) program, and between Medicaid and the Supplemental Security Income (SSI) program. More generally, health insurance reforms that would expand access to health insurance for people with disabilities who are not DI or SSI recipients could have an impact on both employment and program participation. As we discuss further in Section II, however, the issue of how access to health insurance for people with disabilities will affect employment and program participation is more complex than it may first appear.

In another ASPE-supported project, we previously reviewed the literature on barriers and disincentives to employment for people with disabilities, including the literature on health insurance (Lewin-VHI, 1995b). We concluded that the disincentives posed by the ties between Medicare and Medicaid are large, providing reason to believe that there could be substantial labor force effects, but found no direct evidence of an impact on employment or program participation. We also found substantial evidence of links between health insurance access and both the employment and program participation of other populations (single mothers and older workers), and an independently conducted review reached substantially similar conclusions (Gruber and Kubik, 1995). The evidence reviewed supports the hypotheses of links for people with disabilities, but provides no information on the likely size of the impacts. The average person with severe disabilities has health care needs that are very high relative to those of the populations that were the subjects of these studies, but may also have other reasons not to respond to changes in insurance access--his or her health condition or impairments, disincentives associated with SSI/DI cash benefits, and perhaps others.

In this report, we present a review of the literature to update our previous findings. The report serves several purposes:

to synthesize information that may have direct value to policymakers;

to inform research to be conducted under this project; and

to identify gaps in our knowledge about the importance of health insurance in the employment and program participation decisions of persons with disabilities.

B. Overview of the Report

The report is organized as follows:

In Section II, we discuss the differences in incentives related to health insurance access between persons who are considering leaving employment and persons participating in disability programs who are considering entering employment. Policies that provide greater access to health insurance for persons with disabilities will have different effects on different groups of individuals with disabilities, depending on their employment or program participation status and their current access to health insurance coverage.

In Section III, we present the findings of studies that have examined the relationship between access to Medicare and Medicaid and program/labor force participation of persons with disabilities. For Medicaid, the studies we review have examined how the value of Medicaid benefits affect SSI participation, and the impact of Section 1619 provisions, which extend SSI and Medicaid eligibility for recipients who work, on the employment and work effort of SSI recipients. For Medicare, the studies we review estimate the potential impact of eliminating the two-year waiting period for Medicare on medical care costs to DI beneficiaries, and examine the effect of extending the period of Medicare eligibility and allowing Medicare buy-in on the work effort of DI beneficiaries. These sections are very limited, however, both in scope and methodology. In the final subsection, we present information on the importance of health insurance obtained through self-reports from persons with disabilities.

In Section IV, we review studies that have examined the effect of access to health insurance on the work effort of groups other than persons with disabilities. The studies we review examine the effect of Medicaid provision on the participation of unmarried mothers in the AFDC program; the provision of health insurance through continuation of coverage laws (COBRA) and through retiree health benefits on the work effort of older workers; and the effect of a Medicare beneficiary buy-in program for Medicaid on SSI participation among the elderly.

In Section V, we present and discuss the available information on the health insurance and employment status of persons with disabilities. This section provide a basis for the empirical analyses we will conduct using national survey and SSA administrative data, the findings for which will be presented in a subsequent report.

In Section VI, we conclude with: a summary of what we know about the relationship between access to health insurance and the employment and program participation patterns of persons with disabilities; a discussion of significant gaps in our knowledge; a description of research currently underway that explores this issue; and a summary of recent legislative proposals to expand health insurance to persons with disabilities.

II. THE COMPLEX RELATIONSHIPS AMONG INSURANCE ACCESS, EMPLOYMENT, AND PROGRAM PARTICIPATION

While many suggest that delinking health insurance access from DI and SSI would unambiguously increase employment of people with disabilities, the issue is complex. Actual effects will depend on how the delinking is accomplished, availability of insurance from other sources, variation in the benefits provided by various types of insurance, current employment or program status of the individual, the individual's work history, eligibility for other programs (e.g., Transitional Assistance for Needy Families (TANF), Veterans benefits, general assistance), health care needs, age, skills, education, etc. Benefit variation is very important for some people with disabilities. Medicaid, which was designed as a last resort for people with disabilities and other vulnerable groups, can provide the most comprehensive benefits, including such long-term benefits as personal assistance services and assistive devices. Private health insurance and Medicare often do not provide coverage for services that some people with disabilities use intensively.

When thinking about this issue, we find it helpful to differentiate between the decision to seek (or increase) employment by a disabled individual, and the decision to leave (or decrease) employment. The discussion in the following two subsections focuses on these groups and the importance of considering current insurance status when estimating the potential effects of expansions in public health insurance.

We assume in the following discussion that public insurance expansions do not affect the provision of private insurance. As discussed later in this report, there is some evidence that public insurance expansion "crowds out" private insurance, and a potential effect of an expansion of insurance to people with disabilities might be reduced private insurance coverage. While this is not central to the topic addressed by this report, employment and access to health insurance, we include a brief discussion of the topic at the end of the report because of its relevance to policies currently being considered for providing access to health insurance for people with disabilities.

A. The Decision to Seek Employment

For persons considering paid employment, it is helpful to distinguish between those who are DI or SSI recipients and those who are not.

The potential loss of public health insurance may well discourage DI and SSI program participants from seeking employment or increasing their employment earnings to a level that would jeopardize their public health insurance. It is this group of individuals that are most often considered when the issue of health insurance access and employment of people with disabilities is discussed. Expansion of public health insurance that would permit earnings at levels higher than the maximums allowed under DI or SSI would encourage employment and earnings for current DI and SSI recipients as well as encourage exits from these programs.

For disabled non-workers who are not DI or SSI recipients and are not privately insured, public health insurance expansions would likely reduce work incentives. One reason for such individuals to obtain a job is to obtain employer-provided insurance or obtain income to pay for health care directly. The number of non-working disabled persons for whom employment is a realistic route to insurance or health services is probably small, however. For those who are insured (e.g., as a dependent), public health insurance expansions would have little effect on the incentive to work unless the public insurance covered important services that are not covered by private insurers. Public coverage of such additional services would reduce the incentive to work, because in the absence of insurance coverage the individual might view earnings from work as a means to obtain those services.

B. The Decision to Leave Employment

Many workers with new, or progressive impairments have little choice but to leave their jobs. Others have a choice, and health insurance may be critical to that choice. Among these workers, it is helpful to distinguish between those in jobs with employer-provided health insurance and jobs without such insurance.

If the individual has health insurance through his/her employer, the effect of an expansion in public health insurance eligibility for those under the age of 65 will depend on the current availability of insurance after they leave their job. It is important to keep in mind that employer-provided health insurance is a strong work incentive for many workers. Thus, public insurance expansions that provide people with disabilities insurance whether or not they work have the potential to reduce employment of insured workers with disabilities.

Insured workers who leave jobs may obtain coverage immediately in several ways: through paying premiums to continue employer coverage for up to 18 months (COBRA continuation coverage); through the employer's disability or workers' compensation plan, through retiree health benefits; through a spouse's employer; from the Veterans Administration; and through Medicaid if they meet the SSI means and disability tests or qualify by other means. Medicare can be obtained only after 29 months and only if the worker is DI eligible (there is a five-month DI waiting period plus an additional 24 month waiting period for Medicare). Expansion of eligibility for Medicare (e.g. reducing the waiting period or providing a Medicare buy-in) would presumably have little effect on the decision of an insured worker who could obtain post-job insurance in some other way, but could have a substantial effect if other options are unavailable. Expanding Medicaid eligibility (e.g., through a less strict means test) would have similar effects, except that coverage of certain services by Medicaid might be an attractive reason to leave work for an individual who would otherwise have to pay for these services out-of-pocket. Public provision of these same services to those who continue employment would presumably reduce this effect, but even so, an important incentive to work would be removed.

The situation is different for disabled workers who are not insured. Faced with high health care costs, some such workers--particularly those with low earnings--may decide to leave work to obtain eligibility for public health insurance via DI and/or SSI. If, instead, the same worker could obtain public health insurance and continue to work, he or she might choose continued employment. Thus, low-earning, uninsured workers with disabilities would be more likely to continue working if they could do so and obtain public health insurance. Some uninsured disabled workers, especially those with very high earnings, might continue employment in order to be able to purchase health care out-of-pocket under the current system, and be induced to leave work if they could obtain public health insurance. The former case is much more prevalent than the latter, however.

III. DIRECT EVIDENCE OF THE RELATIONSHIP AMONG HEALTH INSURANCE, PROGRAM PARTICIPATION, AND EMPLOYMENT OF PEOPLE WITH DISABILITIES

In this section, we present the findings of studies that have examined the relationship between access to Medicare and Medicaid and program/labor force participation of persons with disabilities. For Medicaid, the studies we review have examined how the value of Medicaid benefits affect SSI participation, and the impact of Section 1619 provisions, which extend SSI and Medicaid eligibility for recipients who work, on the employment and work effort of SSI recipients. For Medicare, the studies we review estimate the potential impact of eliminating the two-year waiting period for Medicare on medical care costs to DI beneficiaries, and examine the effect of extending the period of Medicare eligibility and allowing Medicare buy-in on the work effort of DI beneficiaries. In the final subsection, we present information on the importance of health insurance obtained through self-reports from persons with disabilities.

With respect to Medicaid, we have identified only two studies that examine the relationship between Medicaid and SSI participation. One (Yelowitz, forthcoming) finds a very strong positive relationship between the value of Medicaid benefits and SSI participation, while the other (Lewin-VHI, 1995a) finds no effect. There have been a few studies of the effectiveness of the Section 1619 work incentive provisions. The studies generally conclude that the provisions seem to have a very negligible impact on the work effort of SSI recipients.

With respect to Medicare, the one study that estimated the effects of eliminating the two-year waiting period only focused on the medical care costs of the DI beneficiaries that would be affected by such a policy. We have not found any studies that attempt to estimate the impact on DI program participation. Regarding the DI work incentive provisions that extend Medicare eligibility and allow buy-in for beneficiaries who work, the studies we reviewed indicate that the presence of these work incentives do not have a large effect on the work effort of DI beneficiaries. The studies base their conclusions on evidence from self-reported reasons why beneficiaries return to work, and the finding that knowledge of the work incentive provisions was significantly and negatively associated with return to work among DI beneficiaries.

The information we have found regarding self-reported health insurance status at the time of disability application and self-reported reasons for not working among groups of persons with specific impairments indicate that a large proportion of persons who file for Social Security disability benefits do not have any health insurance, that those without insurance are more likely to be denied disability benefits, and that a sizable proportion of DI and SSI beneficiaries with specific disabilities report the fear of losing their health insurance as a reason for not working.

A. Medicaid

1. The Impact of Increases in the Value of Medicaid Benefits on SSI Participation

Since our earlier report, one study commissioned by ASPE and SSA under a related contract to Lewin has found a significant and strong relationship between the average Medicaid expenditures for disabled Medicaid enrollees in a state and SSI participation in the state using Current Population Survey data for multiple years during a period of rapid Medicaid expenditure growth (Yelowitz, forthcoming). Another study using SSA administrative data estimated a pooled time series model with state-level data for the same period, using the same Medicaid expenditure variable, but found no significant impact on SSI determinations or awards (Lewin-VHI, 1995a).1 The inconsistent findings have not been reconciled. A criticism that applies to both studies is that the value of Medicaid benefits to the typical disabled person may be unrelated to Medicaid expenditures; it is the access to insurance that matters, not payment rates to Medicaid providers (although the two may be related). Due to data limitations, neither study looks explicitly at how eligibility changes affect employment or program participation; even if we accepted Yelowitz's findings at face value, it would be problematic to use those results to infer the impact of eligibility expansions on employment or program participation.

Yelowitz (forthcoming) examines the relationship between the average Medicaid expenditures for disabled Medicaid enrollees in a state and SSI participation of working-age adults in the state using Current Population Survey data for 1987-1992, years of rapid Medicaid expenditure growth.2 Yelowitz pools individual data for the six-year period and uses a regression model, with SSI participation as the dependent variable, to control for the following: various characteristics of the individual; all state-level factors that are fixed over time (state "fixed effects"); factors that vary across years but are the same across states "year effects," such as nationwide changes in the SSI program itself; and some state-level variables that vary across years, such as the unemployment rate. His key explanatory variable is average Medicaid expenditures for disabled (but not blind) enrollees in the state. Because he uses state fixed effects, the estimated Medicaid coefficient reflects the relationship between changes in Medicaid expenditures and changes in SSI participation, holding constant changes in the other explanatory variables.

One important methodological problem with the regression specification is that the Medicaid expenditure variable may be "endogenous," that is, changes in the Medicaid explanatory variable may not be independent of changes in SSI participation (the dependent variable), but rather, partly determined by it. Yelowitz argues, specifically, that there may be a negative relationship between changes in average Medicaid expenditures and SSI growth because marginal disabled SSI recipients are likely to use fewer health services than the average recipient. If so, the estimated regression coefficient would understate the hypothesized positive effect of growth in the value of Medicaid on SSI participation. Yelowitz uses instrumental variables--average Medicaid expenditures for the blind and for the elderly--to correct for this.3

Yelowitz finds strong positive coefficients on the Medicaid expenditure variable, especially when the instrumental variables are used. If interpreted literally, the instrumental variable estimates imply that the Medicaid expenditure growth accounts for 25 percent of the growth in SSI participation by working-age adults over this period. There are two important reasons for being extremely cautious in accepting this interpretation, however.

First, the value of Medicaid benefits to the typical disabled person may be unrelated to Medicaid expenditures; it is the access to insurance that matters, not payment rates to Medicaid providers.4 Even after controlling for the compositional changes in Medicaid disability enrollees via the instrumental variables technique, changes in spending over this period may reflect many other things that have little relation to access--including changes in the policy environment that are not captured in the other state variables. As Yelowitz points out, research that examines Medicaid eligibility expansions for people with disabilities that are not linked to SSI expansions would be much more convincing, but opportunities to examine such expansions are very limited. In two studies that we will examine later, Yelowitz uses eligibility expansions to examine the impacts of Medicaid on SSI participation by the elderly and both AFDC and labor force participation of unmarried mothers. Interestingly, his results for that population are much stronger than results obtained by others who have used average Medicaid expenditures for AFDC families as the explanatory variable.

Second, the estimated coefficients on his state-level variables differ substantially in character from those obtained in a study that we conducted, using a related methodology and identical state variables over the five years from 1988 to 1992 (Lewin-VHI, 1995a). In this study we used data on all fifty states plus the District of Columbia to examine the relationship between SSI participation of working-age adults and a set of state explanatory variables. The main difference in the methodology is that we used aggregate state data on SSI applications and allowances for the dependent variables, rather than participation of individuals. That is, we looked at the flow of individuals onto SSI that were generated by changes in state-level explanatory variables, instead of the effect on the stock of beneficiaries. We would expect the flow to be much more sensitive to such variables than the stock, which is largely determined by the number of allowances and terminations in prior years. One other important difference is that we could not control for many individual-specific characteristics, because we did not have individual data, but we were able to control for changes in the age composition of the population and a few other population characteristics (e.g., immigration and the incidence of AIDS/HIV) through other means. The main explanatory variables we used were identical to those used by Yelowitz.

The coefficients we obtained for two of the state variables were markedly different than those reported by Yelowitz. First, we did not find a significant positive coefficient on the Medicaid expenditure variable, whether or not we used an instrumental variable. Second, we found very strong positive coefficients on a variable measuring cuts in general assistance (GA) programs over this period, while Yelowitz found a negative, and significant coefficient on the same variable. Seven states and the District of Columbia significantly cut their GA programs over the period, including Michigan, which essentially eliminated its program. Research conducted by Bound et al. (forthcoming) using SSA administrative data linked to GA data from Michigan, strongly confirmed that the termination of Michigan's program accounted for a very large share of SSI growth in that state over the period, and qualitative evidence obtained from other states also confirms our finding. This additional evidence gives us confidence that our own GA coefficient is capturing a real effect, and leaves us puzzled over the differences in the findings for both this variable and the Medicaid variable.

In summary, while Yelowitz's findings are intriguing and plausible, they need to be treated with substantial skepticism. Similarly, it would be a mistake to construe the absence of a significant effect in our own work as evidence that no effect exists; it may just reflect the limitations of the methodology--in particular the use of average Medicaid expenditures for people with disabilities as an estimate of the value of Medicaid benefits to those in that population.

2. Utilization of Extended Medicaid Benefits by SSI Recipients under Section 1619b of the Social Security Act

a) Early Research on 1619b

Rocklin and Mattson (1987) provide a discussion of the legislative history of Section 1619 through its permanent enactment in 1987. Section 1619 of the Social Security Act began as a three-year demonstration project authorized by the Social Security Disability Amendments of 1980. Effective on January 1, 1981, Section 1619(a) enabled blind or disabled SSI recipients who had completed the trial work periods and continued to engage in substantial gainful activity (SGA) to receive cash benefits, Medicaid coverage, and other social services available to Section 1611 (regular SSI) recipients. Cash payments under 1619(a) were calculated in the same manner as regular SSI payments. In addition, Section 1619(b) enabled working blind or disabled SSI recipients whose earnings precluded them from receiving 1611 or 1619(a) cash payments to retain their eligibility for Medicaid and other social services, so long as they:

-

continued to be blind or to have the disabling condition that caused them to be considered disabled;

-

would be entitled to cash payments except for their earnings;

-

would be seriously inhibited in continuing employment if they lost eligibility for Medicaid and social services; and

-

did not have earnings above a "threshold amount" that would allow them to provide a reasonable equivalent of the SSI payments, Medicaid , and social services they would have in the absence of earnings.5

As noted in Rocklin and Mattson (1987), the purpose of the demonstration project was to see if it was possible to assure SSI disability recipients that working would not disadvantage them without incurring too great a cost on the SSI or Medicaid programs.

Congress failed to reauthorize Section 1619 before it expired on December 31, 1983. Upon the urging of both House and Senate leaders, however, the Secretary of Health and Human Services authorized the temporary continuation of Section 1619 for individuals who were eligible for the provision in December 1983. Public Law 98-460, signed on October 9, 1984, reauthorized Section 1619 through June 30, 1987.

Even before the reauthorization of Section 1619, advocacy groups sought to make Section 1619 a permanent program. They believed that the temporary nature of the Section 1619 programs was actually deterring attempts to work by SSI recipients who feared joining a program whose future was uncertain. After several legislative initiatives in 1985 and 1986, Section 1619 became permanent on November 10, 1986 with the signing of the Employment Opportunities for Disabled Americans Act (Public Law 99-643).

As defined under Public Law 99-643, the current Section 1619 programs has several major differences from the demonstration project. First, in order to account for the potential failure of work attempts and a disabled individual's often erratic ability to work, the current program allows for seamless transitions between regular SSI, section 1619(a), and section 1619(b) eligibility. It also requires SSA to continue an individual's disability status for 12 months after his or her most recent eligibility for regular SSI, section 1619(a), or section 1619(b). However if an individual recovers medically, SSA requires the individual to submit a new application and undergo a new disability determination in order to establish a new period of eligibility.6 In addition to standard SSI disability reviews, SSA reviews section 1619 cases for medical improvement or the ability to work at SGA level when an SSI recipient becomes eligible for benefits under section 1619 or when there are changes in his or her 1619 status; however, such reviews are not to occur more often than once a year.7 The current program, unlike the demonstration project, does not require a trial work period. Public Law 99-643 also allows the SSA to include impairment-related work expenses (IRWEs), blind work expenses, a plan to achieve self-support (PASS), publicly funded attendant or personal care, and medical expenses in the determination of whether an individual's income could provide a "reasonable equivalent of benefits." Under the law, SSA must notify blind and disabled SSI recipients of their potential eligibility for benefits under Section 1619 at the time of the initial reward and when a recipient's earnings reach $200.8 Finally the Act assures that disabled individuals living in states that use Medicaid eligibility criteria other than the SSI eligibility standard can maintain their Medicaid eligibility so long as they were eligible for Medicaid in the month before they obtained 1619 eligibility status.9

One of the first studies of Section 1619 was conducted by the Department of Health and Human Services (SSA and HCFA) during the demonstration phase of Section 1619. The Congressional mandate for this study required the collection and analysis of data concerning the characteristics of individuals benefiting from Section 1619, the effect of Section 1619 on work effort, and health care utilization by Section 1619 beneficiaries. SSA (1986) is an abridged version of the HHS Report to Congress.

The HHS report made use of three main data sources. Analysis of SSI administrative files enabled HHS to review the histories of all Section 1619 participants who had participated at any time between May 1981 and May 1985. HHS also analyzed 1,660 responses to the 1985 SSI Medicaid Recipient Survey (The Survey). The Survey compiled specific demographic data about SSI recipients as well as their attitudes toward disability and employment. Finally, HHS used a HCFA study of Medicaid utilization in 11 states, a study encompassing nearly half of the Section 1619 population, to gauge Medicaid utilization by Section 1619 participants. Based on the analysis of these data sources, the HHS Report to Congress presented the following conclusions:

-

While point-in-time Section 1619 participation levels were low, the program had a very high turnover rate. Nearly 55,000 individuals were covered by Section 1619 for some period between May 1981 and May 1985.

-

In 1985 Section 1619 participants were, on average, younger than the SSI population at large,: 84 percent of 1619(a) eligibles and 79 percent of 1619(b) eligibles were under the age of 40 while only 39 percent of the overall SSI disabled population was under the age of 40. In addition, they were predominately white males, and the most common disability was mental impairment.

-

The Survey showed that average monthly earned income was $475 for Section 1619(a) participants and $674 for Section 1619(b) participants, compared to an average of $112 for all working SSI disabled recipients, and $1,169 for all working US residents ages 18 to 39.

-

The majority of participants were employed in service occupations by private employers. Two-thirds of 1619(a) participants and one-half of 1619(b) participants worked in all twelve months in 1985. In addition, 1619(b) participant were about twice as likely as 1619(a) participants to engage in sheltered work (27 percent versus 15 percent).

-

A significant number of 1619 participants had health care coverage from sources other than Medicaid. In 1985, one-third of 1619(b) participants had some private health insurance. Medicaid was the only health care coverage for one-half of 1619(a) and 28 percent of 1619(b) participants. Medicare was also a common source of health care coverage for 1619 participants.

-

Analysis of the HCFA study indicated that the Medicaid per capita expenditure rate for the entire disabled SSI population was 2.3 times greater than that for Section 1619 participants.

-

The 1985 Survey results suggest that the majority of 1619 participants would not reduce work effort in order to retain 1619 cash payments or Medicaid eligibility.

Based on the last three findings, the study concluded that there was not a strong relationship between health care coverage and work effort, and that the retention of Medicaid eligibility was less of an incentive than was commonly believed. However, it did suggest room for further research and acknowledged that the temporary nature of the 1619 program may have influenced the results of the study.

Andrews, et al. (1988) present the results of the HCFA research included in the Report to Congress cited above. Interestingly, Andrews, et al. (1988) suggest that Section 1619 provides a stronger work incentive than reported in SSA (1986). In addition to the conclusions cited above, the study found that the health care costs represent, on average, 13 percent of a Section 1619 enrollee's earnings. Citing the SSA (1986) finding that only 2.8 percent of Section 1619 enrollees were able to earn enough income to obtain Medicaid equivalent coverage, Andrews, et al. (1988) conclude that Section 1619 appeared to provide a significant benefit to people with disabilities who attempt to work.

Sizable changes in Section 1619 enrollment shortly after the effective date of the Employment Opportunities for Disabled Americans Act suggest that the initial temporary nature of Section 1619 did lessen its effectiveness as a work incentive. Between June 1987, the month before Section 1619 effectively became permanent, and December 1987, 1619(a) enrollment increased ten times from 1,436 to 14,559 participants. Section 1619(b) participation also increased during the same period, albeit less dramatically, from 12,470 to 15,632.10

In January 1990, the definition of SGA increased from $300 per month to $500 per month causing many Section 1619(a) participants to revert to regular SSI eligibility. Primarily as a result of this change and the accompanying reclassification of SSI recipients, Section 1619(a) enrollment decreased from 25,655 in December 1989 to 13,994 in December 1990.11

b) The Effect of 1619(a) and (b) on an SSI Recipient's Budget Constraint

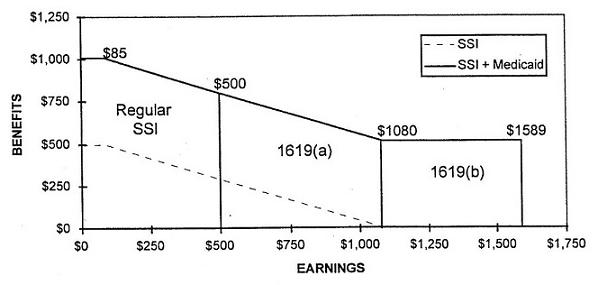

In this section, we present an example to illustrate the effect of Section 1619 provisions on an SSI recipient's eligibility status for SSI benefits and Medicaid. In Exhibit 1 and Exhibit 2 we present a simplified example of the relationship between earnings and SSI and Medicaid benefits for a non-married individual living in Pennsylvania in 1996.12 As shown in the exhibits, a disabled SSI recipient with no earnings would receive $497 in SSI cash payments ($470 federal payment and $27.40 state supplement) and, on average, $509 in in-kind Medicaid benefits, for a total of $1,006 in net benefits per month. The SSI benefit calculation disregards an individual's first $85 of earned income per month; thus, an individual may earn up to $85 without experiencing a decline in net benefits. Beyond $85 per month in earnings, the SSI recipient loses 50 cents for each additional dollar earned. Once a recipient earns $500 per month, the level of substantial gainful activity (SGA), he or she is no longer eligible for regular SSI, and must transfer to section 1619(a) to maintain SSI eligibility. Section 1619(a) eligibility allows individuals to increase their monthly earnings above SGA without completely losing their SSI cash payments. Under section 1619(a), an individual continues to loose 50 cents in benefits for each additional dollar earnings until his or her benefits have fallen to zero.

In 1996, a disabled SSI recipient living in Pennsylvania would lose all SSI cash benefits and transfer to section 1619(b) eligibility once his or her monthly earnings reached $1,080, the state's SSI "breakeven point." Section 1619(b) eligibility allows individuals to increase their monthly earnings above a state's "breakeven point" without losing their Medicaid benefit. Eligibility under section 1619(b) continues until an individual's monthly earnings reach a "threshold amount," beyond which a person loses Medicaid eligibility. For each state, this amount is equal to the state's SSI "breakeven point" plus the average Medicaid expenditures for disabled SSI cash recipients in the state. Pennsylvania's threshold amount was $1,589 in 1996.

| EXHIBIT 1: Earnings and SSI and Medicaid Benefits for a Non-Married SSI Recipient Living in Pennsylvania in 1996 | |||||

| Zero Earnings | SSI Disregard | SGA level | SSI Breakeven Point | Section 1619(b) Threshold | |

| Earnings | $0 | $85 | $500 | $1,080 | $1,589 |

| SSI | $497 | $497 | $290 | $0 | $0 |

| SSI plus Medicaid | $1,006 | $1,006 | $799 | $509 | $0 |

| EXHIBIT 2: Relationship between Earnings and SSI and Medicaid Benefits for an SSI Recipient Participating in 1619(a) and (b) |

|

c) Recent Statistics on 1619

Since the permanent authorization of Section 1619, total enrollment in both 1619(a) and 1619(b) programs has increased substantially. In December 1996, Section 1619(a) enrollment stood at 31,085 people while 51,905 individuals were eligible for Medicaid under Section 1619(b) provisions. However measured as a percentage of total SSI blind and disabled recipients, participation in Section 1619 programs has only increased from 1 percent of all SSI recipients in December 1987 to approximately 1.6 percent in December 1996.

GAO (1996) notes that a survey of 1,200 leaders of major disability constituencies conducted by the President's Committee on Employment of People with Disabilities identified the fear of losing Medicaid/Medicare as the greatest barrier to the employment of people on SSI or DI. Similarly, a 1995 OIG/HHS cited in GAO(1996) found that 79 percent of SSI applicants rated continued medical coverage as a major work incentive. While recognizing the work incentive created by Section 1619, GAO (1996) suggests the effectiveness of this incentive is limited. GAO (1996) argues that SSI beneficiaries who lose their Medicaid benefits because their earnings exceed the threshold amount are apt to be uninsurable or face prohibitively high insurance premiums. Thus, SSI beneficiaries who can work have strong incentive to work up to the section 1619(b) threshold, but much weaker, if any, incentive to work beyond the threshold. In addition, a former beneficiary might be subject to waiting periods or exclusion for preexisting conditions.

B. Medicare

1. The Two-year Medicare Waiting Period for DI Beneficiaries

Under current law, Social Security Disability Insurance beneficiaries must wait two years to obtain Medicare eligibility. The purposes of this waiting period are to restrict costs to the Medicare program during a time when workers often have health insurance from other sources and to ensure that only those persons whose disabilities are severe and long lasting receive coverage. Policymakers have frequently debated the reduction or elimination of the waiting period as a way to improve access to health care and to ease the burden of medical costs.

Analysis of the New Beneficiary Survey presented in Muller (1989) indicates that roughly 27 percent of disabled-worker beneficiaries in 1982 lacked health insurance coverage in the last 6 months of their waiting period. Some policymakers suggest that the reduction or elimination of the waiting period would improve a DI beneficiary's chances for medical recovery by increasing access to medical services shortly after the onset of the disability. This argument contends that if early and improved access to health care enables DI beneficiaries to return to work, the long-run savings in DI and Medicare payments might offset the initial increase in Medicare costs associated with the reduction or elimination of the waiting period.

Based on the analysis of SSA and HCFA data, Bye and Riley (1989) find that the elimination of the two-year waiting period for a 1972 cohort of new beneficiaries would have increased the costs for the cohort by 45 percent over the first 10 years. In addition, they find that nearly 30 percent of the additional cost is attributable to those who died within the first two years of DI eligibility. They estimate that only 3 percent of the increase in cost would be for beneficiaries who eventually recover. Bye and Riley (1989) conclude that the reduction or elimination of the waiting period is "very unlikely to be cost-beneficial in enabling beneficiaries to return to work" since the majority of the increased costs would be spent on those beneficiaries least likely to return to work. The study only examined the medical care costs of beneficiaries, and did not consider the extent to which labor force exits and DI claim allowances would be affected.

2. The Extended Period of Eligibility

The 1980 Social Security Disability Amendments created an extended period of eligibility (EPE) for cash benefits and Medicare coverage. The EPE protects DI beneficiaries who return to work by providing cash benefits during any month in the EPE in which earnings fall below the substantial gainful activity level. Initially, the EPE lasted 15 months beyond the completion of a beneficiary's nine-month trial work period. Subsequently, OBRA-1987 extended the EPE to 36 months. In addition to enacting the EPE, the 1980 Amendments instituted extended Medicare eligibility for working DI beneficiaries an additional 24 months beyond their EPE. OBRA-1987 extended the EPE to 36 months without changing the Medicare extension. Thus, the current extended period of Medicare eligibility is three months beyond the EPE. OBRA-1989 further increased access to Medicare by allowing individuals who continue to have a disability but have lost DI eligibility due to an SGA termination to "buy into" the Medicare program after their extended Medicare benefits expire. The buy-in's purpose is to provide access to health insurance to former DI beneficiaries who are unable to obtain other health insurance due to pre-existing conditions. In so doing, the buy-in seeks to encourage employment efforts of former beneficiaries who might otherwise lose access to health care if they work (Muller, 1992).

In a 1995 HHS Office of the Inspector General (OIG) survey of DI applicants cited in a recent GAO study (GAO, 1996), 75 percent of the applicants rated the continuation of health care coverage as very important to encouraging work. Recent research presented in Hennessey and Muller (1994) and Hennessey and Muller (1995) suggests, however, that extended Medicare eligibility and the Medicare buy-in option only marginally alleviate the fear of losing medical coverage. Hennessey and Muller (1994) report that only 3.7 percent of beneficiaries in the New Beneficiary Follow-up Survey who returned to work cite extended Medicare eligibility and the Medicare buy-in option as one of several factors influencing their decision to return to work. Furthermore, no beneficiaries cite these programs as the main reason for returning to work. In contrast, 81.4 percent and 57.6 percent of beneficiaries respectively report financial need and desire to work as a reason for returning to work. Similarly, 57.7 percent and 17.2 percent respectively report financial need and desire to work as the primary reason for returning to work.

Hennessey and Muller (1994) also note that knowledge of extended Medicare coverage by beneficiaries at the time of award is quite low. Of those beneficiaries surveyed, only 10.5 percent of beneficiaries reported knowing of extended coverage at the time of award. Furthermore, less than 1 percent of beneficiaries said knowledge of the extended coverage influenced their decision to pursue employment.

Hennessey and Muller (1995) model the effect of knowledge of the three major DI work incentives (trial work period, EPE, and extended Medicare coverage) on the decision to return to work. Using a Cox proportional hazards model, Hennessey and Muller (1995) obtain a coefficient for the knowledge of extended Medicare that is negative and statistically significant. This suggests that knowledge of extended Medicare coverage actually reduces effort to pursue employment. While this result is unexpected and counterintuitive, Hennessey and Muller (1995) postulate that beneficiaries might see the combination of the EPE, where the person receives no cash benefits, and the extended Medicare coverage as events leading to termination from the program. At the end of these periods, an individual must be self-supporting and covered by some form of health insurance. For some beneficiaries, the Medicare buy-in option may alleviate the concern of being refused health insurance. However, the monthly premiums, which exceeded $300 for full coverage in 1996, would discourage work efforts among beneficiaries with relatively low monthly earnings (i.e., just above the SGA amount of $500). The fear of future financial insecurity created by the potential loss of the EPE/Medicare safety net may override any work incentive these benefits might create.

C. Self-Reports of the Importance of Health Insurance to Employment and Program Participation

There is a growing body of anecdotal and survey evidence that people with disabilities identify loss of health insurance as an important reason for not working, or not working enough to exit SSI/DI. Policymakers and analysts are reluctant to rely on this type of evidence because people's statements about the factors behind their own behavior are often inconsistent with their actual responses to changes in those factors. Further, people with disabilities often report multiple reasons for limiting employment, and removal of one of the reported deterrents will not remove the others.

On two days in both 1992 and 1994, the Social Security Administration conducted field surveys of DI and SSI applicants. These surveys collected information on applicants' sex, age, reasons for filing for benefits, sources of referral, prior filing history, and current or recent participation in other government programs (SSA, 1994b). In both 1992 and 1994, slightly less than 60 percent had health insurance coverage at the time they filed for DI and/or SSI benefits. Overall, Medicaid accounted for 42 percent of this coverage in 1994, 18 percent among SSI applicants and 63 percent among DI applicants. The 1994 survey revealed significant differences in both DI and SSI allowance rates for applicants with health insurance at the time of application, versus those without coverage. Among DI applicants, the allowance rate for applicants with health insurance was 41 percent, compared to 30 percent for those without coverage. Similarly, the allowance rate for SSI applicants with health insurance coverage was 38 percent, versus 29 percent for applicants without coverage. A possible explanation for these differences is that those applicants without health insurance are generally less impaired than those with coverage, and that the primary impetus behind their application for disability benefits is access to the associated health care coverage.

Other studies have also found that a sizeable number of SSDI and SSI recipients rate the fear of losing medical insurance as a reason for not working. For example, a survey of 359 chronic dialysis patients reported that 79 percent of nonemployed and 78 percent of employed respondents viewed the loss of health insurance as a barrier to employment.13 Similarly, 54 percent of the unemployed respondents in a 1993 study of individuals with severe physical disabilities in Dane County, Wisconsin cited the potential loss of Medicaid or Medicare as a reason why they had chosen not to work reported that.14 Finally, a recent study of the Vocational Rehabilitation Service Program revealed that 42 percent of survey respondents receiving SSDI or SSI cited fear of losing medical insurance as a reason for not taking a job or working regularly.15

These findings are somewhat contradictory to the findings of Hennessey and Muller (1994) reported previously. In their study of DI beneficiaries in the New Beneficiary Follow-up Survey, only 3.7 percent of those who returned to work cited extended Medicare eligibility and the Medicare buy-in option as one of several factors influencing their decision to return to work. Most beneficiaries reported financial need and desire to work as their reasons for returning to work.

IV. EVIDENCE OF THE RELATIONSHIPS AMONG EMPLOYMENT, PROGRAM PARTICIPATION, AND ACCESS TO HEALTH INSURANCE FOR OTHER POPULATION

In this section, we review studies that have examined the effect of access to health insurance on the work effort of groups other than persons with disabilities. The studies we review examine the effect of Medicaid provision on the participation of unmarried mothers in the AFDC program; the provision of health insurance through continuation of coverage laws (COBRA) and through retiree health benefits on the work effort of older workers; and the effect of a Medicare beneficiary buy-in program for Medicaid on SSI participation among the elderly.

The more recent studies of Medicaid and AFDC participation among single mothers generally find a significant positive relationship between the value of Medicaid benefits and AFDC program participation. Earlier studies did not find a significant relationship, but this is mainly due to differences in the methodologies used to estimate the effects. The older studies rely on a very aggregate measure of the value of Medicaid. The more recent studies either use a measure that more accurately reflects the value of Medicaid to individuals based on their characteristics, or rely on the "natural experiment" offered by recent expansions in Medicaid that allow benefits to persons not participating in AFDC. Both of these approaches are superior to those used in the earlier studies.

There is a large body of literature that examines the labor force participation and retirement behavior of older workers. A fair number of these studies have addressed the issue of health insurance and its role in the retirement decisions of older workers. Most of the studies we reviewed have found a significant and positive effect of access to post-retirement health insurance on labor force exits among older men. As with the literature on the effects of Medicaid on the labor force and AFDC participation of single mothers, the studies that are able to more precisely measure the value of health insurance benefits to older workers tend to find a stronger relationship between access to health insurance and retirement behavior.

The study that examined the effect of the Medicare beneficiary buy-in program for Medicaid, the Qualified Medicare Beneficiary Program (QMB), on SSI participation of the elderly found that allowing some Medicare beneficiaries to qualify for Medicaid benefits without having to be eligible for SSI had a strong, negative effect on SSI participation among the elderly. The estimates imply that the savings in terms of reduced SSI benefit outlays virtually pay for the additional Medicaid expenditures of QMB participants.

A. Unmarried Mothers

In an earlier report to ASPE (Lewin, 1995b), we reviewed findings from research on the effects of Medicaid on program participation and employment of unmarried mothers. Gruber and Kubik (1995) independently reviewed the same body of literature, and reached essentially the same conclusions. The following discussion draws on both reviews.

There are more studies on this issue for unmarried mothers than there are for people with disabilities, although the number is still small. The authors of these studies have used a wide range of empirical methods and obtained a wide range of results. Although all the studies reviewed have potential flaws, we find that the methodology used by one study is much more compelling than that used by the others. This study, (Yelowitz, 1995), used a natural experiment offered by recent expansions in Medicaid coverage for children--similar in spirit to the approached used in Yelowitz (1996) to examine the impact of the Medicare buy-in program on SSI participation of the elderly.

Before 1987, almost all unmarried mothers with children had to be eligible for AFDC to obtain Medicaid. Legislation during the 1980s consistently required states to extend Medicaid coverage to pregnant women and young children in low income families. With these expansions, many unmarried mothers could obtain income in excess of AFDC limits and still retain their Medicaid benefits.

The natural experiment nature of the Medicaid expansions permitted Yelowitz to estimate their effects on the labor force and AFDC program participation decisions of single women for a sample of single mothers age 18 to 55 drawn from the March CPS, from 1989 through 1992. His treatment group is mothers who were covered by the expansions either because they were pregnant or because their children were young enough to qualify. His control group is similar mothers not covered by the expansions because they were not pregnant and their children were too old to qualify, but not too old for AFDC coverage. He also controls for observable differences between these groups such as age, education, family size and composition, and state of residence. His estimates are based on comparisons of changes in employment and AFDC participation of these two groups over the period of the expansions. A critical, but apparently reasonable, assumption is that the effects of changes in other factors on the program and employment outcomes for these groups were the same over this period. Yelowitz is able to use variation in the timing and nature of the expansions across states to examine the robustness of the findings, and the results of doing so provides support for the soundness of this approach.

Yelowitz estimates that a Medicaid expansion that increases the maximum income of recipients by 25 percent of the poverty line increases the labor force participation rate of single women subject to the expansion by 3.3 percent, and decreases the proportion receiving AFDC by 4.6 percent. Both estimates were highly significant and robust to many changes in specification and choice of sample.

Comparing these results to results obtained from other methodologies illustrates the promise of applying a similar approach to the same issue for people with disabilities if adequate natural experiments can be found, and also illustrates the limitations of alternative approaches. Two early studies, (Blank, 1988, and Winkler, 1990) use state-specific average Medicaid expenditures for AFDC families as a measure of the value of these services--as Yelowitz (1996) does for disabled SSI recipients.16 Both estimate models of program or labor force participation for unmarried mothers using survey data for a single year, and controlling for observable characteristics of the mother and her children. Neither study finds substantial effects, and almost all estimates are statistically insignificant. To accept these findings at face value, however, one needs to accept the proposition that cross-state variation in average Medicaid expenditure is a good proxy for cross-state variation in the value of Medicaid benefits for an individual with given characteristics. The relationship between the quality of services provided across states and what Medicaid pays for those services is likely very weak because of the great variation in Medicaid payment rules. Variation in the composition of AFDC families also has an impact on average expenditures, but this is irrelevant to a given family's valuation of Medicaid benefits. Finally, variation in Medicaid benefits likely reflects variation in other aspects of the policy environment that may have an impact on AFDC or labor force participation.

Three other studies take a different approach to valuing Medicaid benefits, and obtain findings that are substantially stronger than those obtained by Yelowitz (1995): Ellwood and Adams (1990), Moffitt and Wolfe (1992), and Wolfe and Hill (1995). In each case, the authors use family characteristics, including health problems and potential access to private health insurance coverage, to estimate expected health expenditures if the family is not Medicaid eligible.

A likely reason for the relatively strong findings is that variation in the estimated Medicaid values used in these studies captures, in part, variation in health status itself. If so, the estimates are biased upward because they are partly picking up the direct impact of health status on employment and program participation. The first two of these studies are not able to control for health status at all. Wolfe and Hill make some progress by incorporating health measures to capture the effect of the mother's self-reported health status, mother's functional limitations, and child disabilities on the labor supply decisions of single mothers, but it seems likely that the expected expenditure variable reflects variation in health status even after controlling for these measures of health.

B. Older Workers

1. Continuation of Employer Insurance

Continuation-of-coverage laws mandate that employers providing group health-insurance plans to their employees offer terminating employees and their families the option to continue their insurance through the employer's plan by paying the premiums themselves. These mandates effectively permit former workers, particularly older workers, to purchase private health insurance at rates well below rates they would have to pay in the market for individual coverage.17 Under the Consolidated Omnibus Budget Reconciliation Act of 1986 (COBRA-86), companies offering group health insurance are required to extend coverage to terminating employees for 18 months. Prior to COBRA-86, however, more than twenty states enacted their own continuation-of-coverage laws.

Gruber and Madrian (1994) consider the introduction of continuation-of-coverage mandates in a number of states between 1974 and 1984. The time of extended coverage varied across the states studied. Using samples of 55 to 64 year old men drawn from the 1980 to 1990 March Current Population Surveys (CPS) and the 1984 to 1987 panels of the Survey of Income and Program Participation (SIPP), the authors estimate that one year of mandated continuation benefits increases retirement rates by 30 percent. The estimate appears to be uniform at all ages in the 55 to 64 age group. While not analyzing the issue directly, the findings of Gruber and Madrian (1994) strongly support the inference that the provision of public insurance to non-workers would reduce the labor supply of older workers. Because the prevalence of disabilities is high among older workers, we would also expect such a coverage extension to increase DI applications and, to a lesser extent, allowances. The results are also consistent with the hypothesis that eliminating the two-year Medicare waiting period for DI beneficiaries would increase applications and allowances.

2. Employer-Provided Retiree Health Insurance

According to a survey conducted by the Health Insurance Association of America (HIAA), approximately 35 percent of all workers in 1989 worked for firms that offered retiree health benefits (Karoly and Rogowski, 1994). Similarly, a 1995 US Department of Labor study reports that approximately 30 percent of retirees had health insurance from a previous employer in 1994 (Department of Labor 1995). In recent years, several studies have examined the impact of employer-provided retiree health insurance availability on the decision to retire.

Gustman and Steinmeier (1994) use data from the 1969-1979 Retirement History Study (RHS), the 1977 National Medical Care Expenditure Survey (NMES), the 1983-86 Survey of Consumer Finances, and the 1988 CPS to estimate the impact of employer-provided health benefits on retirement. The authors utilize a life cycle model to estimate the combination of work and retirement that maximizes a workers lifetime utility. A comparison of the effect of retiree health insurance to that of health insurance for active workers reveals that retiree health insurance has a larger impact on the retirement decision. Health insurance for active workers has an effect on retirement comparable to a 6 percent increase in wage, a rather small increase relative to total compensation. When combined with the opposing effects from retiree health insurance before and after the age of eligibility, the overall effect of health insurance for active workers on the average retirement age appears to be modest. Although larger than the effect of health insurance for active workers, the effect of retiree health insurance remains small. Gustman and Steinmeier (1994) estimate that retiree health insurance delays retirement by 1.3 months if valued at the employer's cost, or 3.9 months if valued at the cost of purchase by an individual. The overall effect of retiree health benefits is to delay retirement until the age of eligibility for retiree health benefits, and then afterward, increase the likelihood of retirement.

Karoly and Rogowski (1994) find a much stronger effect for retiree health benefits than Gustman and Steinmeier (1994). Karoly and Rogowski (1994) utilize the 1984, 1986, and 1988 panels of the SIPP to estimate the effect of access to post-retirement health insurance on the early retirement decision of men. Using probit models of the retirement decision, the authors find that employer-provided retiree health benefits increase the probability of retiring by eight percentage points for men between the ages of 55 and 62. In percentage terms, this increase is 50 percent above the baseline probability of retiring. The authors also find that, prior to retirement, access to insurance coverage other than that offered by an employer increases the likelihood of early retirement. As noted by the authors, a drawback of this analysis is that the static model used in this study has limited use in discerning the factors that affect retirement, many of which vary through time.

Lumsdaine, Stock, and Wise (1996) attempt to determine the cause of the high age-65 retirement rate. In so doing, they explore the role that access to health insurance coverage plays in this phenomenon. The authors analyze six data sets: three from employment records of large Fortune 500 companies; the 1987 NMES; the 1984 SIPP with the Education and Work History Supplement (SIPP-EWH); and the 1984, 1985, and 1986 waves of the SIPP with the Characteristics of Job from Which Retired Supplement (SIPP-CJR). All six data sets reveal a spike in the retirement rate at age 65. Analyses of the three national data sets fail to show a significant difference between the retirement rates at age 65 for those with employer-provided retiree health insurance and those without such insurance. Lumsdaine, Stock, and Wise (1996), therefore, conclude that the high age-65 retirement rate is not a consequence of Medicare eligibility. They cite the fact that firms with the most generous retiree health insurance benefits also experience a high age-65 retirement rate as further support for this conclusion. Their inability to find any demographic attributes that would influence this spike in retirement rates leads the authors to attribute the high age-65 retirement rate to custom or accepted practice. A common criticism of Lumsdaine, Stock, and Wise (1996) is that their conclusion relies heavily on one firm and that to generalize to the entire "retirement-age" population is inappropriate.

Rust and Phelan (forthcoming) provide perhaps the most intricate and comprehensive analysis of the retirement decision to date. Using data from the 1969-1979 RHS, the authors utilize a dynamic programming model, accounting for the sequential nature of the retirement process, and individual uncertainty about future mortality, marital and health status, employment, income, and health expenditures. Rust and Phelan are critical of Gustman and Steinmeier (1993) and Lumsdaine, Stock, and Wise (1993) and their conclusion that Medicare has no significant impact on the labor supply of older men. They argue that both studies substantially underestimated the value of Medicare coverage. The two earlier studies add the expected value of Medicare reimbursements and employer contributions for retiree health insurance to an individual's monthly pension and Social Security retirement benefit. During the period of study, both Medicare reimbursements and employer contributions for retiree health insurance amounted, on average, to less than $1,000 each. Taken in the context of total income, these are small additions. Rust and Phelan point out that the distribution of health care expenditures is skewed to the right with a long tail illustrating the low risk of catastrophic health care expenditures. They argue: "If individuals are sufficiently risk averse, the certainty equivalent value of Medicare coverage will be substantially greater than the expected value of Medicare reimbursements and retiree health insurance premiums." To account for this risk aversion, Rust and Phelan explicitly model the distribution of health care risks in their analysis.

Rust and Phelan conclude that unequal access to private health insurance is key to the retirement peak at age 65 and why some individuals apply for Social Security at 62 and others wait until they qualify for Medicare at age 65. Individuals who do not have access to retiree health insurance place a very high value on the "Medicare option" and are twice as likely to apply for Social Security at age 65 than at age 62. Individuals who do have retiree health insurance are more than four times as likely to apply at age 62 than at age 65. Overall, Rust and Phelan find that individuals who are unhealthy, single, have lower average wages, are Medicaid recipients, have retiree health insurance, or have no public or private health insurance are significantly more apt to apply for Social Security early retirement benefits at age 62. Similarly, individuals who are healthy, married, have higher average wages, and those who have employer health insurance but no access to retiree health insurance, are more likely to continue working past age 62 and apply for benefits at age 65.

Using data from the more recent Health and Retirement Survey (HRS), Blau and Gilleskie (1997) estimate the effect of employer-provided retiree health insurance (EPRHI) on the rates at which men aged 51-62 enter and exit the labor force. The HRS provides more detailed and precise measures of retiree health insurance than data sources used in most previous studies. Blau and Gilleskie conclude that access to EPRHI, on average, increases the employment exit rate by two percentage points per year if the individual and the firm share the cost of insurance coverage. If the firm pays the entire cost, the exit rate, on average, increases by six percentage points. At age 61, the presence of EPRHI has its maximum effect, increasing the exit rate by 11 percentage points. Similarly, access to EPRHI increases the rate of labor force entry by three percentage points if the firm pays the entire cost. If the individual pays the entire cost of insurance, however, the rate of entry actually falls slightly. The impact of EPRHI on employment decisions estimated by Blau and Gilleskie (1997) is greater than the effects found in other studies. The more accurate and detailed health insurance measures found in the HRS appear to be responsible for at least part of the larger estimated impact.

Karoly and Rogowski (1996) summarize many of the studies discussed above and discuss the impact of proposed health insurance reform that would make health insurance more accessible to early retirees. Based on the recent economic literature, Karoly and Rogowski conclude that health insurance reform, ranging from market reforms to subsidies to individual mandates, is likely to narrow the gap between the pre- and post-retirement price of health insurance for many workers, thus increasing the incentive to retire. While all literature suggests that reform will increase the incentive to retire, the authors note that the size of the effect is still a matter of contention. Based on our review, we believe their conclusion to be appropriate.

C. The Elderly

Yelowitz (1996) uses the implementation of a Medicare beneficiary buy-in program for Medicaid (the Qualified Medicare Beneficiary Program, or QMB) as a natural experiment to examine the effect of the program on SSI participation for the elderly.

Before the QMB program, Medicare beneficiaries had to meet the SSI means test to qualify for Medicaid. Medicaid coverage for Medicare beneficiaries can be very valuable because it covers many services, such as drugs and long-term care, that have only very limited coverage under Medicare, and because Medicare has deductibles and coinsurance and requires beneficiaries to pay a premium to obtain physician and outpatient coverage. Under the QMB program, many low-income Medicare beneficiaries who do not meet the SSI means test qualify for limited Medicaid benefits--including payment of the Medicare Part B premium and payment of deductibles and coinsurance amounts. The hypothesis Yelowitz tests is that the introduction of the QMB program reduced the number of elderly SSI beneficiaries, presumably because fewer Medicare beneficiaries reduced their incomes (e.g., but stopping work) or spent down their assets to become SSI eligible.