U.S. Department of Health and Human Services

Brookings/ICF Long Term Care Financing Model: Model Assumptions

David L. Kennell and Lisa Maria B. Alecxih, Lewin-ICF

Joshua M. Wiener and Raymond J. Hanley, Brookings Institution

February 1992

PDF Version (75 PDF pages)

This report was prepared under contract between the U.S. Department of Health and Human Services (HHS), Office of Disability, Aging and Long-Term Care Policy (DALTCP) and the Lewin Group. For additional information about the study, you may visit the DALTCP home page at http://aspe.hhs.gov/daltcp/home.htm or contact the ASPE Project Officer, John Drabek, at HHS/ASPE/DALTCP, Room 424E, H.H. Humphrey Building, 200 Independence Avenue, SW, Washington, DC 20201. His e-mail address is: John.Drabek@hhs.gov.

TABLE OF CONTENTS

A. The Models' Structure

B. Organization of the Documentation

II. KEY DEMOGRAPHIC AND RETIREMENT INCOME ASSUMPTIONS

A. PRISM Modeling System

B. Demographic Assumptions

C. Labor Force and Economic Assumptions

D. Pension Coverage Assumptions

E. Social Security and the Retirement Decision

F. Employer Pension Plan Assumptions

G. Individual Retirement Account Assumptions

H. Assets in Retirement

I. Supplemental Security Income Program Benefits

III. DISABILITY AND MORTALITY OF THE ELDERLY

A. Disability

B. Mortality

IV. LONG TERM CARE UTILIZATION

A. Nursing Home Utilization

A. Nursing Home Care Financing

B. Financing of Home Care Services

ATTACHMENTS (separate file)

Memo 1 (2/14/89): 1988 Social Security Trustee's and Bureau of the Census Population Projections

Memo 2 (6/6/89): SIPP Data on Support for Adults Living in Nursing Homes

Memo 3 (7/14/89): Status Report on Analysis of SIPP Data on Assets of the Elderly

Memo 4 (7/14/89): Profile of the SIPP Elderly Who Responded in 1984 but not 1985

Memo 5 (8/11/89): Update on Savings Rate of Elderly Families, 1984-1985

Memo 6 (10/18/89): Induced Demand

Memo 7 (10/19/89): Disability and Income

Memo 8 (1/9/90): Income and Asset Distribution of Elderly Families

Memo 9 (1/10/90): Additional Information on the Income and Asset Distribution of Elderly Families

Memo 10 (1/12/90): Additional Information on the Income and Asset Distribution of Elderly Families

Memo 11 (7/18/90): Life Insurance Values Held by the Elderly

Memo 12 (4/9/91): Table Specs for Distribution of Assets and Income

Memo 13 (4/25/91): Living Arrangement and Disability

Memo 14 (5/16/91): Medigap Analysis Results Using the 1984 SIPP/CES Match File and the 1989 CES

LIST OF FIGURES

FIGURE 1. Brookings/ICF Long Term Care Financing Model

FIGURE 2. Flowchart for Utilization of Long Term Care Services

FIGURE 3. Utilization of Formal Home Care by the Elderly

TABLE 1. Labor Force Participation Rates

TABLE 2. Unemployment Assumptions

TABLE 3. Consumer Price Index Assumptions Used In Forecasts

TABLE 4. Assumed Real Earnings Differentials

TABLE 5. Percent Distribution of Workers by Industry of Employment Assumed in PRISM for Selected Years

TABLE 6. Pension Coverage Assumptions

TABLE 7. Probabilities That Married Individuals Will Choose to Elect the Joint and Survivors Option, by Size of Pension Benefit

TABLE 8. Savings Plan Participation Assumptions

TABLE 9A. Proportion of DC LSDs That Are Rolled Over to an IRA, Pre-TRA

TABLE 9B. Proportion of DC LSDs That Are Rolled Over to an IRA, Post-TRA

TABLE 10. IRA Adoption Assumptions for Non-Covered Workers, by Age and Family Earnings Level

TABLE 11. IRA Adoption Probabilities for Covered Workers in 1982 by Family Income and Age of Worker

TABLE 12. Probabilities of Contributing to an IRA in a Given Year Once Selected to Adopt an IRA

TABLE 13. Distribution of Elderly Persons by Personal Income and Asset Levels, 1984

TABLE 14. Disability Prevalence Rates for the Noninstitutionalized

TABLE 15. Annual Disability Transition Probability Matrices for the Noninstitutionalized Elderly

TABLE 16. Disability Prevalence Rates for Noninstitutionalized Disability Insurance Recipients Simulated to Continue Being Disabled at Age 65

TABLE 17. Mortality Rates for the Noninstitutionalized Elderly in 1985

TABLE 18. Mortality Adjustments Used in the Model

TABLE 19. Annual Probability of Nursing Home Entry

TABLE 20. The Probability of Nursing Home Length of Stay by Age of Entry and Marital Status

TABLE 21. Number of Nursing Home Days Assigned by Length of Stay Category

TABLE 22. Nursing Home Disability Prevalence Rates

TABLE 23. Nursing Home Discharge Disability Prevalence Rate

TABLE 24. The Probability of Nursing Home Length of Stay by Age of Entry and Marital Status for Persons Using Services Due to Induced Demand

TABLE 25. Annual Probability of Starting to Use Formal Home Care Services for the Noninstitutionalized Chronically Disabled

TABLE 26. Annual Probability of Starting to Use Formal Home Care for Persons Who are Noninstitutionalized and Nondisabled at the Start of the Year

TABLE 27. Disability Level Prevalence Rates for Chronically Disabled Users of Paid Home Care

TABLE 28. Distribution of Home Care Length of Use for the Chronically Disabled

TABLE 29. Monthly Number of Formal Visits by Formal Home Care Disability Level

TABLE 30. Medicare Reimbursed Home Health Visits

TABLE 31. Percentage of Noninstitutionalized Non-Chronically Disabled Persons Receiving Medicare Home Health Visits

TABLE 32. Informal Home Care Prevalence Rates for the Chronically Disabled

TABLE 33. Average Daily Rates for Nursing Home Care by Source of Payment

TABLE 34. Medicare Part B Premium and Monthly Medigap Premiums

TABLE 35. Home Sale Patterns of Single Nursing Home Entrants

TABLE 36. Probability of Reduced Assets Upon Admission to a Nursing Home

TABLE 37. Likelihood of Receiving Medicare SNF Coverage and Length of Coverage

TABLE 38. Revised Medicaid Home Care Coverage Probabilitiesa for Persons with Assets Below SSI Level

TABLE 39. Out-of-Pocket and Other Payer Home Care Financing Assignment

TABLE 40. Average Prices Per Visit for Home Care by Source of Payment in 1988

OVERVIEW OF THE PROJECT

In September of 1988, the Office of the Assistant Secretary for Planning and Evaluation (ASPE) contracted with Lewin-ICF and the Brookings Institution to develop a public use version of the Brookings/ICF Long Term Care Financing Model. Using microsimulation techniques, the model projects the utilization and sources of financing for nursing home and home care services among the elderly to the year 2020.

Under this contract, many of the assumptions used in the model were revised to reflect data and findings that had recently become available. As the need for alternative policy simulations arose, the capabilities of the model were expanded. Examples of the types of simulations modeled include: the purchase of new private long term care insurance products; the use of pension funds to purchase long term care insurance; and publicly sponsored programs, such as the long term care benefits proposed by the Pepper Commission.

One of the products of this project is a public use version of the model code and accompanying documentation. The documentation includes:

Model Assumptions, which presents the assumptions used in developing the model.

Designing and Using Model Simulations, which presents assumptions used in modeling alternative proposals and using the results of the model.

A User's Guide to Specifying Simulations, which details how to specify simulations using the model's parameters.

A Programmer's/Operator's Manual, which shows the code structure and operation of the model.

PREFACE

This report is one of four related to the Brookings/ICF Long Term Care Financing Model. It outlines the assumptions used in developing the model. The three other documents discuss: 1) assumptions used in modeling alternative proposals and using the results of the model; 2) how to specify simulations using the model's parameters; and 3) the code structure and operation of the model.

This documentation was prepared by David L. Kennell and Lisa Maria B. Alecxih of Lewin-ICF in collaboration with Joshua M. Wiener and Raymond J. Hanley of the Brookings Institution. John Drabek, serving as the project officer, and Paul Gayer of the Office of the Assistant Secretary for Planning and Evaluation provided invaluable comments.

This report was developed as part of the documentation of a public use version of the Brookings/ICF Long Term Care Financing Model for the Office of the Assistant Secretary for Planning and Evaluation. Other reports in this series include:

- Designing and Using Model Simulations

- A User's Guide to Specifying Simulations

- A Programmer's/Operator's Manual

Copies of the reports may be obtained by writing to:Brenda Veazey, Department of Health and Human Services, Room 424E, Humphrey Building, 200 Independence Avenue, S.W., Washington, D.C. 20201

I. INTRODUCTION

A. The Models Structure

The Brookings/ICF Long Term Care Financing Model simulates the utilization and financing of long term care services -- both nursing home and home care -- for elderly individuals through 2020. Nursing home services include care provided by skilled nursing facilities (SNFs) and intermediate care facilities (ICFs). Home care services include home health, homemaker, personal care, and meal preparation services. The model simulates the number of individuals receiving these services and the costs of these services which are financed by various public and private sources. The overall objective of the model is to simulate the effects of various financing and organizational reform options on future public and private expenditures for nursing home and home care.

The two principal components of the model are the Pension and Retirement Income Simulation Model (PRISM) and the Long Term Care Financing Model. PRISM simulates future demographic characteristics, labor force participation, income and assets of the elderly. The Long Term Care Financing Model simulates disability, admission to and use of nursing home and home care, and methods of financing long term care services. The model uses national data and does not take into account regional, state or local variations.

The model begins with a nationally representative sample of the adult population with a record for each person's age, sex, income, and other characteristics. The model simulates changes for each individual's characteristics in the sample population from 1986 to 2020, including age, economic status, disability status, utilization of long term care, and the method of paying for such care.

The model uses a Monte Carlo simulation methodology. The model simulates changes in an individual's status by drawing a random number between zero and one and comparing it to the fixed probability of that event occurring for an individual with a given set of socio-demographic characteristics. For example, the annual probability of death for an 85 year old noninstitutionalized female is .03 (i.e., three out of every 100 women age 85 who are not in a nursing home are expected to die each year). If the random number drawn by the model is less than or equal to .03 for this 85 year old woman, then the individual is assumed to die in that year. If the number drawn lies between .03 and 1.0, then the individual is assumed to continue to live during that year. In order to reduce random variation due to the Monte Carlo procedure, the model is routinely run with two separate random number sets and the results are averaged.

The model can be used to simulate long term care financing assuming changes in private financing methods (such as increased purchase of private long term care insurance) or new public financing programs. These simulations are greatly affected by the choice of assumptions about the economy (such as the rate of growth of the overall economy and nursing home prices) and individual behavior (such as rates of nursing home utilization, insurance purchases, and induced demand). The model can be used to make estimates using alternative assumptions to show how sensitive the results are to the assumptions chosen.

The current version of the model is a major revision of the model that was developed jointly by Lewin-ICF and the Brookings Institution in 1986. The model was revised in 1988 and 1989 using data from a number of newly available data sources, including the 1982-84 National Long Term Care Survey, the 1985 National Nursing Home Survey, the 1984 Survey of Income and Program Participation (Wave 4), and Medicaid and Medicare program data provided by the Health Care Financing Administration (HCFA).

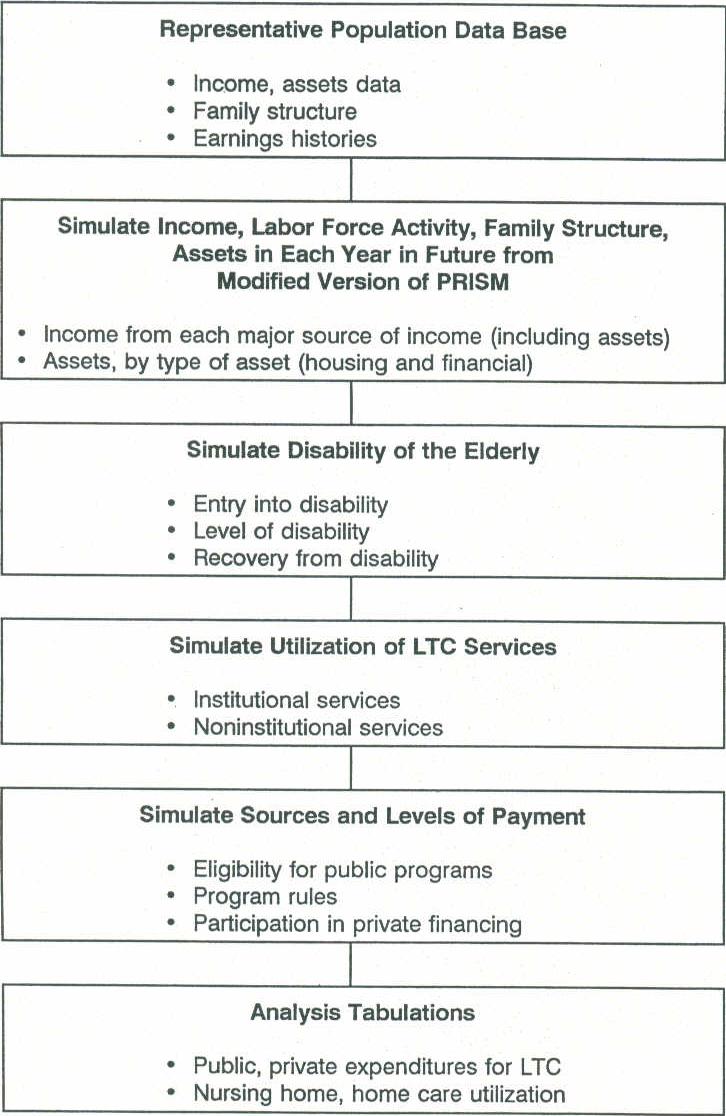

The six major components of the model are described below. A flowchart of these components is shown in Figure 1.

Population Data Base: Using data from the May 1979 Current Population Survey, the model uses information for a nationally representative sample of 28,000 adult individuals of all ages in 1979. This 1979 data base was chosen because it has been merged with social security earnings histories for each individual in the sample.

Income Simulator: The Pension and Retirement Income Simulation Model (PRISM) simulates labor force activity, marital status, income, and assets for each individual. The probabilities in this part of the model are based upon Census Bureau data on the likelihood of marriage, work, etc. for different demographic groups. The economic assumptions underlying the simulations are generally those used in Alternative 11-13 of the 1988 Social Security Trustee's Report. The model estimates retirement income from private sector defined benefit pension plans, public pension plans, social security, private sector defined contribution plans, Individual Retirement Accounts and Keoghs. The model also simulates the assets of elderly individuals including the value of home equity.

Disability of the Elderly: Using probabilities estimated primarily from the 1982-84 National Long Term Care Survey (NLTCS) and the 1985 National Nursing Home Survey (NNHS), this part of the model simulates the level of disability for persons age 65 and over. The model simulates the onset of disability, the level of disability, changes in disability, and recovery from disability.

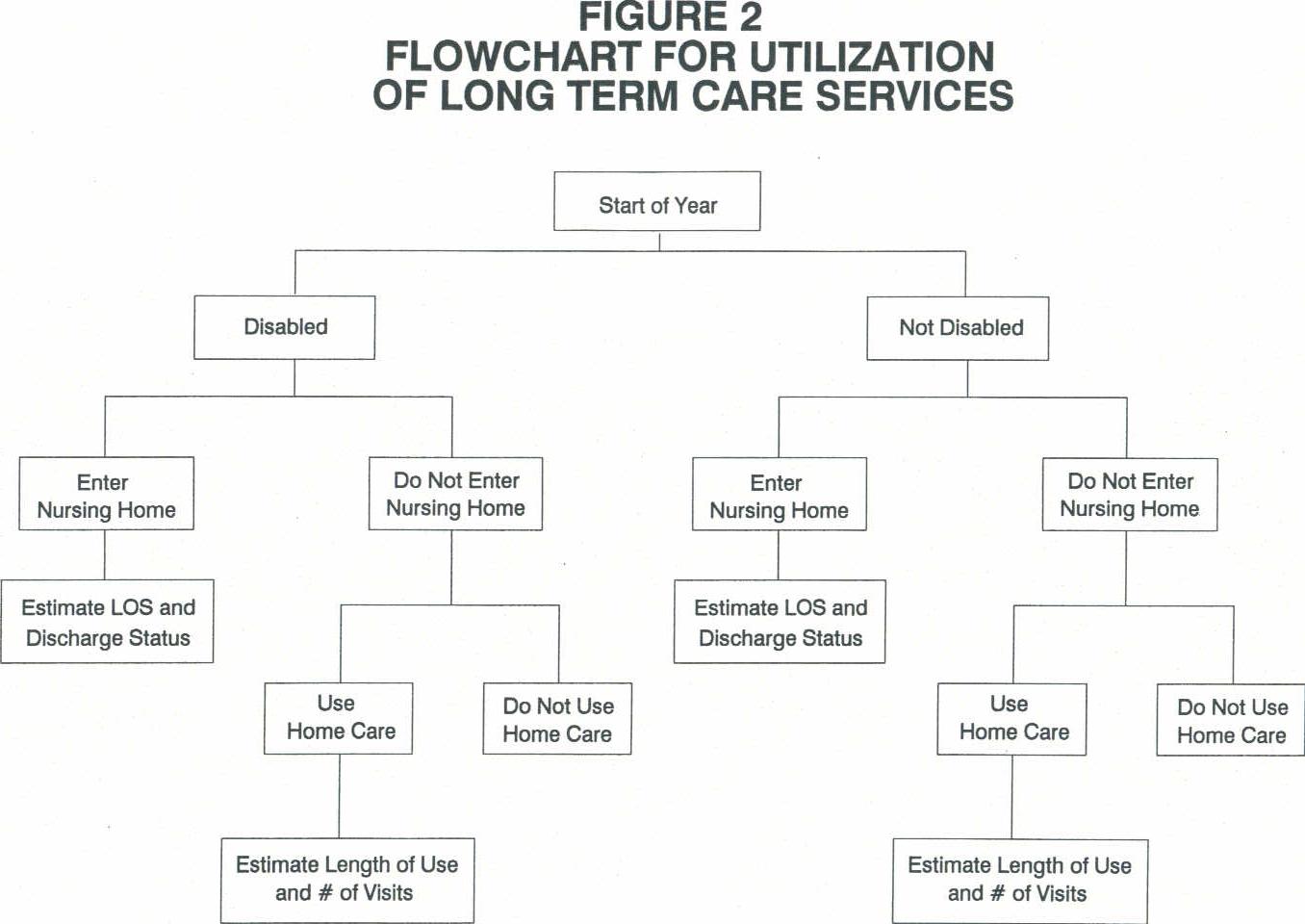

Utilization of Long Term Care Services: This part of the model uses probabilities estimated from the 1982-84 NLTCS and the 1985 NNHS to simulate admission to and length of stay in a nursing home. For noninstitutionalized persons, the model also simulates the use and length of stay for paid home care services using probabilities derived primarily from the 1982-84 NLTCS and Medicare program data.

| FIGURE 1. Brookings/ICF Long Term Care Financing Model |

|

Sources and Levels of Payment: The fifth component of the model simulates the sources of payment and the level of expenditures for each individual receiving nursing home or home care services. The model incorporates Medicare eligibility and coverage provisions and uses a set of uniform assumptions about the Medicaid program, including provisions from the Medicare Catastrophic Coverage Act that were not repealed. State Medicaid program variations are not modeled.

Aggregate Expenditures and Utilization: The sixth part of the model accumulates Medicare, Medicaid, private expenditures, and utilization for each simulated individual for each year. The final output file from the model provides detailed information for individuals age 65 and older, for each year from 1986 to 2020, on individuals' age, sex, marital status, disability, sources and amounts of income, assets, and use of and payment sources for nursing home and home care services. This file is tabulated to show aggregate long term care expenditures for various demographic groups and sources of financing.

B. Organization of the Documentation

This document describes both the retirement income simulation and the long term care financing portions of the model. The retirement income simulations are described in more detail separately (see David L. Kennell and John F. Shells, "The ICF Pension and Retirement Income Simulation Model (PRISM) with the Brookings/ICF Long Term Care Financing Model," September 1986). Section II of the documentation describes the key demographic and retirement income assumptions in the model. Section III describes the probabilities used in the model to simulate disability and mortality for the elderly. Section IV describes the simulation of utilization of nursing home and home care services. Section V describes the financing of nursing home and home care services. Memos on data analyses related to the model are included as attachments.

II. KEY DEMOGRAPHIC AND RETIREMENT INCOME ASSUMPTIONS

The Pension and Retirement Income Simulation Model (PRISM) develops future estimates of retirement income.1 The model simulates retirement incomes for a sample of individuals age 25 and older in 1979 obtained from the ICF Pension/Social Security Data Base. The sources of income modeled in PRISM include: social security, employer pensions, Individual Retirement Accounts and Keogh accounts, employment earnings, asset income, and Supplemental Security Income (SSI) program benefits. PRISM simulates retirement income for this sample of the individuals based upon: (1) the characteristics of individuals in 1979; (2) their family and work histories prior to 1979; and (3) simulations of the future workforce experience of these individuals.

In order to simulate the future workforce experience and retirement incomes of these individuals, the model requires a large number of assumptions concerning the likelihood of future events for each individual, such as the likelihood an individual will continue to work, whether he or she will become divorced or married, and whether he or she will contribute to an IRA. These assumptions are divided into eight major areas:

- demographic

- labor force and economic;

- pension coverage;

- social security and the retirement decision;

- employer pension provisions;

- Individual Retirement Accounts;

- housing and financial assets; and

- Supplemental Security Income benefits.

The key assumptions used in each of these areas are summarized below. We start by briefly summarizing the PRISM modeling system.

A. PRISM Modeling System

The Pension and Retirement Income Simulation Model (PRISM) simulates the distribution of retirement income from both public and private resources for elderly families. PRISM models income from social security, private and public employee retirement plans, Individual Retirement Accounts (IRAs) and Keogh accounts, earnings, assets, and the Supplemental Security Income (SSI) program. It also estimates taxes paid in retirement.

The model simulates the distribution of retirement income among households of various socioeconomic groups for a representative sample of individuals age 25 and older in 1979 obtained from the ICF Pension/Social Security Database. These data are an exact match of the Special Pension Supplement to the May 1979 Current Population Survey (CPS) and Social Security Administration (SSA) earnings history data for 1951 through 1977.

For each individual in the population data base, PRISM uses probabilities estimated primarily from recent Census data to simulate each individual's earnings, periods of employment, and family structure between 1979 and the date of retirement. To ensure that PRISM simulations of labor force participation and earnings are consistent with the projected aggregate growth of the economy, we linked PRISM to the September 1987 labor force projections made by the Bureau of Labor Statistics.

Using the simulated work histories, the model calculates the social security benefits and IRA accumulations for each individual, as well as SSI benefits and earning from employment once the individual reaches retirement age, When individuals are simulated to enter a pension-covered job, the model assigns them to an actual pension plan sponsor selected from a representative sample of private and public retirement plan sponsors (the ICF Retirement Plan Provisions Data Base). When these individuals meet the plans' eligibility standards, PRISM then calculates their benefits using the plans' actual benefit provisions. This process of matching a representative sample of individuals to a representative sample of plan sponsors is a unique feature of PRISM. The model also estimates the amount of individuals' assets in retirement based upon the distribution of assets reported in the 1984 Panel of the Survey of Income and Program Participation (SIPP). Separate amounts are estimated for financial assets and home equity. Individuals are assumed to receive income from their nonhousing assets.

B. Demographic Assumptions

PRISM simulates mortality, disability, child bearing, and changes in marital status. During each simulation year, individuals are simulated to die, become disabled, recover from disability, bear children, and become married or divorced. The model uses a variety of assumptions to estimate these events, most of which are consistent with the Alternative II-B assumptions used in the 1988 report of the Trustees of the Old Age and Survivors Insurance and Disability Insurance Trust Funds (1988 Trustees' Report). The major assumptions are discussed below.

-

Mortality -- PRISM uses the Alternative II-B mortality assumptions used in the 1988 Trustees' Report. Mortality rates vary by age, sex, disability status, and years since becoming disabled. Mortality rates vary for each simulation year to reflect projected improvements in mortality made by the Social Security Actuaries. As discussed in a later section, mortality adjustments are made for persons 65 and over to reflect differences in mortality between institutionalized and noninstitutionalized, disabled and nondisabled persons.

-

Disability -- For persons under 65, PRISM uses the rates of disability used in the 1988 Trustees' Report. These rates vary by age and sex and are assumed to remain unchanged over time. Disability for persons age 65 and over is discussed in Section III.

-

Recovery from Disability -- For persons under 65, PRISM uses rates of disability recovery developed by the Social Security Actuaries for 1979-1980. These rates vary by age, sex, and years since becoming disabled. These are the most recent rates available and are assumed to remain unchanged over time. Recovery from disability for the elderly is discussed in Section III.

-

Child Bearing -- Fertility rates in the model are based upon an analysis of Census Bureau data on women who gave birth to children during the 1976-1980 period. These fertility rates vary by age, marital status, employment status, and number of children. In the model, these rates are constrained to match the Alternative II-B assumptions of fertility in the 1988 Trustees' Report.

-

Marital Status -- All probabilities concerning marriage and divorce are obtained from Monthly Vital Statistics data developed by the National Center for Health Statistics. The aggregate rates match the Alternative II-B projections in the 1988 Trustees' Report. Divorce rates vary by the age of husband and wife. Marriage rates vary by age, sex and marital status (i.e., never married, divorced, or widowed) of the individual. In the model, individuals selected to become married are joined with a member of the opposite sex based upon data on the distribution of newly married individuals by age and education of husband and wife reported in Vital Statistics data. The marriage and divorce rates are assumed to remain constant in the future.

C. Labor Force and Economic Assumptions

PRISM simulates each individual's employment history from 1979 (the date of the May 1979 CPS survey) through the date of retirement. During each simulation year, the model simulates wage rates, hours worked, job change and industry of employment. The simulations were constrained to match September 1987 Bureau of Labor Statistics (BLS) projections of employment and industry composition, and the Alternative II-B assumptions from the 1988 Trustees' Report of average wage rates in future years. The major assumptions are as follows:

-

Employment Levels Over Time -- PRISM was constrained to simulate aggregate levels of employment consistent with BLS forecasts of labor force participation rates for 1987-2000 (see Table 1).2 Labor force participation rates after 2000 are assumed to remain constant for each age/sex group. These forecasts include: 1) trends in employment for men and women of various age groups; 2) projections of economic growth; and 3) trends in the age of retirement. Unemployment rates from the 1988 Trustees' Report for the years 1986-2020 were used (see Table 2). Actual participation rates and unemployment rates are used for 1979 through 1987.

-

Employment by Socio-Economic Group -- Given the levels of labor force participation for different age/sex groups, the model simulates the number of hours each individual will work during each simulation year based upon an analysis of Bureau of the Census data on employment patterns during the 1976-80 period. For each individual, the decision to work and the number of hours worked in a year varies by age, sex, hours worked in each of the three previous years, marital status, presence of children at various ages, pension receipt status, and social security benefit receipt status.

-

Inflation -- Consumer prices are assumed to increase at the rate specified under the Alternative II-B assumptions in the 1988 Trustees' Report. These price change assumptions are shown in Table 3.

-

Interest Rates -- Assets in all defined contribution plans and individual retirement accounts (IRAs) were assumed to earn interest at an average annual rate of 7.0 percent.

-

Wage Growth -- Aggregate changes in wage levels are assumed to increase at the rate assumed in the Alternative II-B assumptions of the 1988 Trustees' Report (see Table 4). In general, average wages are assumed to grow by 1.3-1.6 percentage points in excess of the inflation rate in each year after 1990. Actual wage growth rates are used during the 1979-87 period. Given these aggregate rates, the hourly wage rates for each individual in the model are adjusted during each year based upon an analysis of Census Bureau data on patterns of wage growth. Rates of wage growth vary by age, sex, and whether or not the individual changed jobs during the year.

-

Job Change -- The probability that an individual will change jobs is based upon an ICF analysis of Census Bureau data concerning job change patterns during 1979. Job change is modeled as a function of the age, part-time/full-time status and job tenure of each worker. These probabilities are assumed to remain constant over time.

-

Maternity Job Terminations -- Women who have children often leave the labor force. In some instances, these women may re-enter the labor force and resume working for the same employers they had prior to having the child. In PRISM, we assume that a woman who has a child and leaves her job in the same year will become reemployed on the same job if: 1) the woman re-enters the labor force within five years of having the child; and 2) the woman became employed in the same industry she was in prior to having the child.

-

Industry Changes -- PRISM assigns individuals to an industry of employment when they change jobs or enter the labor force. The industry assigned to these individuals varies with age, full time/part time status, and industry of prior job. As shown in Table 5, the model assumes that over time, a higher proportion of workers work in the services industries and a lower proportion of workers work in the manufacturing industry. These industry composition estimates are based upon November 1987 BLS projections for the 1987-2000 period. After 2000, industry composition is assumed to remain constant.

| TABLE 1a. Labor Force Participation Rates | |||||||||||||||||

| 1984 | 1985 | 1986 | 1987 | 1988 | 1989 | 1990 | 1991 | 1992 | 1993 | 1994 | 1995 | 1996 | 1997 | 1998 | 1999 | 2000andAfter | |

| MEN | |||||||||||||||||

| 16-17 | 43.5 | 45.1 | 45.3 | 45.6 | 45.8 | 45.9 | 46.1 | 46.5 | 46.7 | 46.9 | 47.2 | 47.4 | 47.7 | 47.9 | 48.3 | 48.6 | 48.7 |

| 18-19 | 68.1 | 68.9 | 68.3 | 68.5 | 68.9 | 69.1 | 69.3 | 69.5 | 69.8 | 70.1 | 70.4 | 70.7 | 71.0 | 71.3 | 71.5 | 71.9 | 72.2 |

| 20-24 | 85.0 | 85.0 | 85.8 | 85.9 | 86.0 | 86.2 | 86.3 | 86.5 | 86.5 | 86.7 | 86.8 | 86.8 | 86.9 | 87.1 | 87.3 | 87.3 | 87.5 |

| 25-34 | 94.3 | 94.7 | 94.6 | 94.3 | 94.2 | 94.2 | 94.1 | 94.0 | 94.0 | 93.9 | 93.8 | 93.9 | 93.7 | 93.7 | 93.7 | 93.6 | 93.6 |

| 35-44 | 95.4 | 95.0 | 94.8 | 94.6 | 94.4 | 94.4 | 94.4 | 94.3 | 94.2 | 94.2 | 94.1 | 94.1 | 94.0 | 94.0 | 94.0 | 93.9 | 93.9 |

| 45-54 | 91.2 | 91.0 | 91.0 | 90.9 | 90.8 | 90.8 | 90.7 | 90.7 | 90.7 | 90.6 | 90.6 | 90.6 | 90.5 | 90.4 | 90.3 | 90.2 | 90.1 |

| 55-59 | 80.2 | 79.6 | 79.0 | 78.6 | 78.3 | 78.1 | 77.8 | 77.6 | 77.4 | 77.0 | 76.8 | 76.6 | 76.3 | 76.0 | 75.8 | 75.5 | 75.2 |

| 60-61 | 68.1 | 68.9 | 67.7 | 66.9 | 66.4 | 66.0 | 65.5 | 65.0 | 64.5 | 64.0 | 63.5 | 63.2 | 62.8 | 62.1 | 61.7 | 61.3 | 60.9 |

| 62-64 | 47.5 | 46.1 | 45.8 | 44.9 | 44.3 | 43.7 | 43.0 | 42.5 | 42.0 | 41.5 | 40.9 | 40.4 | 39.9 | 39.4 | 39.1 | 38.6 | 38.2 |

| 65-69 | 24.5 | 24.4 | 25.0 | 24.2 | 23.7 | 23.0 | 22.5 | 22.1 | 21.5 | 20.9 | 20.5 | 20.1 | 19.7 | 19.2 | 18.7 | 18.3 | 17.9 |

| 70-74 | 16.0 | 14.8 | 14.3 | 14.0 | 13.6 | 13.2 | 12.9 | 12.5 | 12.1 | 11.7 | 11.3 | 11.0 | 10.6 | 10.2 | 10.0 | 9.6 | 9.3 |

| 75+ | 7.5 | 7.0 | 7.1 | 7.0 | 6.8 | 6.5 | 6.3 | 6.1 | 5.8 | 5.7 | 5.4 | 5.2 | 5.1 | 4.9 | 4.7 | 4.5 | 4.3 |

| WOMEN | |||||||||||||||||

| 16-17 | 41.2 | 42.1 | 43.7 | 44.7 | 45.1 | 45.6 | 46.1 | 46.6 | 47.1 | 47.5 | 48.0 | 48.3 | 48.7 | 49.1 | 49.3 | 49.6 | 49.7 |

| 18-19 | 61.8 | 61.7 | 62.3 | 62.7 | 63.3 | 63.8 | 64.1 | 64.4 | 64.9 | 65.4 | 65.9 | 66.3 | 66.8 | 67.2 | 67.7 | 68.1 | 68.6 |

| 20-24 | 70.4 | 71.8 | 72.4 | 72.6 | 73.1 | 73.6 | 74.2 | 74.6 | 75.1 | 75.5 | 76.0 | 76.4 | 76.7 | 77.3 | 77.7 | 78.0 | 78.4 |

| 25-34 | 69.8 | 70.9 | 71.6 | 72.4 | 73.3 | 74.3 | 75.2 | 76.0 | 76.9 | 77.6 | 78.4 | 79.2 | 79.8 | 80.5 | 81.1 | 81.7 | 82.3 |

| 35-44 | 70.2 | 71.8 | 73.1 | 73.9 | 74.9 | 75.9 | 76.9 | 77.8 | 78.7 | 79.5 | 80.3 | 81.0 | 81.7 | 82.4 | 83.0 | 83.7 | 84.2 |

| 45-54 | 62.9 | 64.4 | 65.9 | 66.4 | 67.3 | 68.1 | 69.0 | 69.7 | 70.5 | 71.2 | 72.0 | 72.7 | 73.4 | 73.8 | 74.4 | 74.9 | 75.4 |

| 55-59 | 49.8 | 50.3 | 51.3 | 51.5 | 51.8 | 52.1 | 52.4 | 52.7 | 53.1 | 53.3 | 53.6 | 53.9 | 54.2 | 54.5 | 54.7 | 55.0 | 55.3 |

| 60-61 | 40.0 | 40.3 | 40.0 | 40.2 | 40.3 | 40.3 | 40.3 | 40.4 | 40.4 | 40.4 | 40.5 | 40.5 | 40.5 | 40.6 | 40.6 | 40.6 | 40.6 |

| 62-64 | 28.8 | 28.6 | 28.5 | 28.7 | 28.8 | 28.8 | 28.8 | 28.9 | 28.9 | 28.9 | 28.9 | 28.9 | 28.9 | 28.9 | 29.0 | 29.0 | 29.0 |

| 65-69 | 14.2 | 13.5 | 14.3 | 14.0 | 13.8 | 13.6 | 13.4 | 13.3 | 13.1 | 12.9 | 12.7 | 12.5 | 12.3 | 12.1 | 11.8 | 11.6 | 11.4 |

| 70-74 | 7.3 | 7.6 | 6.9 | 7.1 | 7.1 | 7.0 | 7.0 | 6.9 | 6.9 | 6.8 | 6.7 | 6.7 | 6.7 | 6.6 | 6.6 | 6.5 | 6.5 |

| 75+ | 2.5 | 2.2 | 2.4 | 2.4 | 2.4 | 2.3 | 2.2 | 2.1 | 2.1 | 2.0 | 1.9 | 1.9 | 1.8 | 1.7 | 1.7 | 1.6 | 1.5 |

SOURCE: Howard N. Fullerton, Jr., "Labor Force Projections 1986-2000," Bureau of Labor Statistics' Monthly Labor Review, September 1987. | |||||||||||||||||

| TABLE 2. Unemployment Assumptions | |

| Year | Average AnnualUnemployment Rate |

| 1979 | 5.8% |

| 1980 | 7.1 |

| 1981 | 7.6 |

| 1982 | 9.7 |

| 1983 | 9.6 |

| 1984 | 7.5 |

| 1985 | 7.2 |

| 1986 | 7.0 |

| 1987 | 6.2 |

| 1988 | 6.0 |

| 1989 | 6.2 |

| 1990 | 6.1 |

| 1991 | 6.0 |

| 1992 | 5.9 |

| 1993 | 5.8 |

| 1994 | 5.8 |

| 1995 | 5.8 |

| 1996 | 5.8 |

| 1997-1999 | 5.7 |

| 2000 and later | 6.0 |

| SOURCE: Alternative II-B assumptions from the 1988 Annual Report of the Board of Trustees of the Federal Old Age and Survivors Insurance and Disability Insurance Trust Funds, April 1988. | |

| TABLE 3. Consumer Price Index Assumptions Used In Forecasts | |

| Year | Annual Change inConsumer Price Index |

| 1979 | 11.4 |

| 1980 | 13.5 |

| 1981 | 10.3 |

| 1982 | 6.0 |

| 1983 | 3.0 |

| 1984 | 3.4 |

| 1985 | 3.5 |

| 1986 | 1.6 |

| 1987 | 3.6 |

| 1988 | 3.9 |

| 1989 | 4.5 |

| 1990 | 4.3 |

| 1991 | 4.2 |

| 1992 | 4.0 |

| 1993 | 4.0 |

| 1994 and later | 4.0 |

| SOURCE: 1988 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Disability Insurance Trust Funds, Washington, D.C.: Social Security Administration, April 1988. | |

| TABLE 4. Assumed Real Earnings Differentials | |

| Year | Real EarningsDifferentiala |

| 1979 | -2.2% |

| 1980 | -4.4 |

| 1981 | -1.0 |

| 1982 | 0.6 |

| 1983 | 1.8 |

| 1984 | 2.3 |

| 1985 | 0.7 |

| 1986 | 2.8 |

| 1987 | -0.6 |

| 1988 | 0.9 |

| 1989 | 1.1 |

| 1990 | 1.1 |

| 1991 | 1.3 |

| 1992 | 1.7 |

| 1993 | 1.6 |

| 1994 | 1.6 |

| 1995 | 1.5 |

| 1996 | 1.5 |

| 1997 | 1.5 |

| 1998 | 1.4 |

| 1999 | 1.4 |

| 2000 and later | 1.4 |

SOURCE: Alternative II-B assumptions from the 1988 Annual Report of the Board of Trustees of the Federal Old Age and Survivors Insurance and Disability Insurance Trust Funds, April 1988. | |

| TABLE 5. Percent Distribution of Workers by Industry of Employment Assumed in PRISM for Selected Years | |||||

| Industry | 1980 | 1982 | 1984 | 1990 | 2000 andAfter |

| Mining | 0.59% | 0.95% | 1.30% | 0.88% | 0.78% |

| Construction | 4.53 | 4.20 | 4.44 | 4.81 | 4.62 |

| Manufacturing | 20.78 | 19.08 | 18.73 | 16.32 | 14.09 |

| Transportation | 5.02 | 5.03 | 5.32 | 4.96 | 4.74 |

| Trade | 18.71 | 19.24 | 19.26 | 19.86 | 20.58 |

| Finance | 5.09 | 5.32 | 5.38 | 6.09 | 6.06 |

| Service | 17.55 | 18.50 | 18.50 | 20.34 | 23.08 |

| State & Local | 12.96 | 12.96 | 12.61 | 12.29 | 11.73 |

| Federal | 3.28 | 3.28 | 3.26 | 3.07 | 2.79 |

| Self Employed | 9.55 | 9.85 | 9.63 | 10.06 | 10.45 |

| Agriculture | 1.64 | 1.65 | 1.55 | 1.29 | 1.07 |

| Total | 100.00% | 100.00% | 100.00% | 100.00% | 100.00% |

| SOURCE: Lewin-ICF estimates based upon George T. Silverstri and John M. Lukasiewicz, "A Look at Occupational Employment Trends to the Year 2000," Bureau of Labor Statistics' Monthly Labor Review, September 1987. | |||||

D. Pension Coverage Assumptions

For each job individuals have during the simulation, PRISM determines whether they are covered by a retirement plan and assigns covered workers to actual pension plan sponsors in the ICF Retirement Plan Provisions Data Base. Coverage rates were assumed to remain constant through time. The key assumptions are presented below.

-

Pension Coverage -- As workers change jobs or enter the labor force during the simulation, retirement plan coverage is simulated using coverage rates reported for job changers and labor force entrants in the May 1979 CPS. The model is further constrained to replicate coverage rates reported in the May 1983 EBRI/HHS CPS pension supplement. These coverage rates vary by the individual's industry of employment, full time/part time worker status, age, and real wage rate. Plan coverage on an industry basis is assumed not to change between 1983 and 1988 when the new nondiscrimination rules introduced in the 1986 Tax Reform Act became effective. The coverage rates assumed for 1979, 1983, and 1989 are presented in Table 6.

-

Impact of 1986 Tax Reform Act on Pension Coverage -- Internal Revenue Service's (IRS) pension plan nondiscrimination rules that became effective in 1989 stipulate that, in general, no more than 30 percent of a plan sponsor's employees could be excluded. Previously, employers could legally exclude up to 44 percent of their employees from the plan.3 The impact of this provision is modeled by estimating the number of persons in each industry who were not participating in a pension plan even though: (1) their employers sponsor a pension plan; and (2) they appear to meet the most restrictive age and service criteria allowed under ERISA (i.e., age 25 with at least 1,000 hours worked over a period of one year). In the model, the coverage rates for each industry are increased starting in 1989 so that no more than 30 percent of these individuals are not participating in their employer's plan (see Table 6).

-

Plan Assignment -- Individuals are assigned to plan sponsors in the ICF Retirement Plan Provisions Data Base in proportion to the number of individuals actually covered by that plan sponsor. PRISM assigns individuals to plans of similar industry, firm size, social security coverage status, union coverage status, multi/single employer plan status, and hourly/salary worker status. In addition, individuals are assigned only to plans which are consistent with the characteristics of the plan the individual reported he was covered by in the May 1979 CPS. To do this, the model takes into account the individual's reported participation and vesting status as well as plan contribution requirements and participation in a supplemental plan.

| TABLE 6. Pension Coverage Assumptions | |||

| Industry | Pension Coverage Rate | ||

| 1979 | 1983 | 1989 | |

| Federal Government | .93 | .93 | .93 |

| State & Local Government | .88 | .83 | .83 |

| Mining | .82 | .75 | .79 |

| Manufacturing | .76 | .70 | .73 |

| Transportation | .75 | .75 | .77 |

| Finance | .67 | .67 | .75 |

| Construction | .43 | .41 | .43 |

| Trade | .43 | .46 | .51 |

| Services | .43 | .47 | .52 |

| Agriculture | .19 | .22 | .22 |

| Self Employed | .14 | .14 | .14 |

| SOURCE: Coverage rates for 1979 were derived from an ICF analysis of the May 1979 Current Population Survey. Coverage rates for 1983 are based on an ICF analysis of the May 1983 EBRI/HHS CPS Pension Supplement. Coverage rates for 1989 were estimated by ICF by adjusting the 1983 coverage rates to reflect the potential impact of the nondiscrimination rules in the Tax Reform Act of 1986. | |||

E. Social Security and the Retirement Decision

The model simulates the acceptance of early, normal and late retirement benefits from both pension plans and social security. Current social security legislation provisions (including the 1983 amendments which increased the age at which unreduced benefits will be available) were assumed to be in place throughout the simulation. The important assumptions in the retirement decision are summarized below.

-

Social Security Benefit Acceptance -- PRISM simulates the age at which individuals start to receive social security benefits. These benefit acceptance rates vary by the age and sex of the individual. The rates were derived from social security benefit receipt data by age and sex during 1980. PRISM also assumes that eligible individuals age 62 or over will automatically accept benefits if they are disabled or unemployed or receiving an employer pension. These assumptions lead to an increase in social security early retirement because the number of individuals receiving pensions will increase over time in the simulations.

-

Social Security Survivors Benefits -- Individuals are simulated to accept social security survivors benefits in the first year they are eligible.

-

Employer Pension Benefit Acceptance -- PRISM determines when an individual is eligible to accept employer pension benefits and then simulates the decision to accept the benefit. Benefit acceptance rates were developed by ICF based upon an analysis of Census Bureau data on pension benefit recipients.

-

Impact of Eliminating Age 70 Mandatory Retirement -- Prior to 1987, employers could legally require workers to retire when they reached age 70. Legislation passed in 1986 made such regulations illegal for most employers. All plans in the ICF Retirement Plan Data Base were modified to eliminate mandatory retirement beginning in 1987. The BLS labor force participation projections take into account the expected impact of the elimination of mandatory retirement.

-

Acceptance of Deferred Vested Benefits -- Individuals who are vested and leave their job prior to their eligibility for early or normal retirement receive a deferred vested benefit. These benefits are assumed to go into pay status when the individual reaches the plan's normal retirement age.

F. Employer Pension Plan Assumptions

PRISM simulates the size of the benefit individuals will receive from each pension plan in which they earn a benefit during the simulation. PRISM uses the actual provisions of the plan to which the individual was assigned to determine each individual's eligibility and benefit amount. In general, pension plan provisions are assumed to remain unchanged over time except in instances where plan rules must be changed to be in compliance with the Retirement Equity Act of 1984 (REA) and the Tax Reform Act of 1986. The following assumptions are used:

-

Benefit Formulas -- The benefit formulas in defined benefit plans are indexed to changes in wages for flat and unit benefit formulas. Defined contribution plan salary bend points are also indexed to wage growth. Final pay defined benefit and all other parts of defined contribution plan formulas are held constant. No changes in participation, vesting or other plan provisions are assumed except where required by REA or the Tax Reform Act of 1986.

-

Impact of REA on Participation Rules -- REA mandated that starting in 1985, the minimum age requirement for participation would be reduced from 25 to 21 and that service between the age of 19 and 22 would be considered for determining vesting. Starting in 1985, the provisions of any private plans which were not already in compliance with these provisions are modified.

-

Impact of the Tax Reform Act of 1986 on Vesting -- The Tax Reform Act required private sector single-employer plans to vest benefits at least as rapidly as under the following two schedules: (1) full vesting upon completion of five years of service, or (2) 20 percent vesting after the completion of three years of service and 20 percent more for each subsequent year.4 Starting in 1989, the provisions of any private single employer plans which were not already in compliance with these provisions are modified.

-

Limits on Social Security Integration -- Private sector plans which integrate benefits with social security are required to limit their integration formulas. Although previous IRS regulations placed restrictions on how plans may integrate benefits, some low-wage workers had their pension benefits severely reduced or completely eliminated through integration. The Tax Reform Act retained and simplified IRS regulations on integration. In addition, the Act establishes additional restrictions on integration that apply separately to three types of integrated plans:

-

For defined benefit excess/step-rate (plans which calculate pension benefits at different rates on earnings above and below specified levels), the rate at which benefits are provided for pay up to the integration level of a plan (the compensation amount below which pension benefits are reduced) may not be less than 50 percent of the rate at which benefits are provided in excess of that level. In addition, the integration level may not be more than the social security wage and benefit base.

-

For defined benefit offset plans (plans where pension benefits are reduced by a stated percentage of the person's social security benefit), the offset may not reduce a participant's benefits by more than 50 percent.

-

For defined contribution plans (plans where the employer contributes a specified amount but does not guarantee a specified benefit), the provisions are similar except that they apply to the rate of employer contributions. In addition, for defined contribution plans, the rate for pay in excess of the integration level may not exceed the rate for up to that level by more than the OASDI tax rate.

-

-

Cost of Living Adjustments for Pensions -- The model assumes that benefits for private plan beneficiaries from defined benefit plans will be indexed at half of the rate of inflation up to a maximum of two percent per year. All early and normal retirement benefits from the Civil Service Retirement Plan are assumed to increase at the annual rates of inflation shown in Table 3. State and local government benefits are assumed to increase at the rate of inflation up to a maximum of four percent each year. These assumptions are based upon a prior ICF study which analyzed cost of living adjustments over a ten year period for a representative sample of pension plans. None of these plans are assumed to index deferred vested benefits.

-

Post-Retirement Survivors Benefit Option -- Table 7 presents the assumptions used to determine which married individuals choose to elect the post-retirement joint and survivors option. Because REA mandated that starting in 1985 spousal consent is required to waive survivors benefit coverage, the model assumes that the rate of joint and survivor election will increase after the act is implemented (see Table 7). Individuals who accept the post-retirement survivors option are assumed to receive a 50 percent joint and survivor's annuity. This annuity provides a surviving spouse with a benefit equal to half of that received by the deceased individual while living.

-

Pre-retirement Survivors Option -- Many plans automatically provide individuals with pre-retirement survivor's coverage. In these plans, all individuals are assumed to "elect" the pre-retirement survivors option. In the other defined benefit plans, the model assumes 60 percent of married individuals will elect the pre-retirement survivors option. Because REA mandated spousal consent for waiver of the survivors coverage, the model assumes that 85 percent of all married individuals elect this option after REA is implemented.

-

Vested Beneficial Survivors Benefits -- As mandated by REA, pre- retirement survivors coverage was extended to spouses of individuals who receive vested benefits. Thus, the model simulates survivors benefits for spouses of vested beneficiaries who die between the time they leave the job and the date the benefits would have gone into pay status. In all instances the survivors benefit is assumed to be a 50 percent joint and survivors annuity.

-

Maternity -- Under REA, workers who leave a pension plan may return to the job and retain their prior years of service for participation and vesting status provided the break in service was less than or equal to the greater of: (1) five years; or (2) the number of years of service prior to the break. Although both men and women may benefit from this provision, it was intended to assist women who leave their job for maternity. Because reemployment by the same employer is modeled in maternity cases only, this rule is applied only to women in the model who have children. In addition, due to further REA liberalizations in crediting service for maternity cases, working women who have a child are assumed to receive one year of credited service for the year the child is born, regardless of the number of hours they worked.

-

Participation in Savings, Thrift and 401(K) Plans -- Table 8 summarizes the assumptions on participation in supplemental thrift, savings and 401(K) plans for those individuals who are eligible to participate in them. The participation rates are a function of a worker's wage level and the employer matching rate.

-

Employee Contributions -- In plans which require employee contributions as a condition for plan participation, the model assumes individuals contribute the amount required to obtain the maximum employer contribution.

-

Lump Sum Payments -- In the current version of PRISM, individuals who are vested in a defined contribution plan and change jobs are selected to roll their lump sum payment into an IRA on the basis of lump sum rollover data obtained from an analysis of the May 1983 EBRI/HHS CPS Pension Supplement.5 The likelihood of a rollover varies by age, marital status, benefit level, and income. Among individuals age 55 or older, all lump sums over $1,750 are rolled over into an IRA and saved for retirement.

-

Impact of Tax Reform Act on Roll-Overs -- The Tax Reform Act eliminated 10 year averaging, thus increasing individuals' incentives to roll-over into an IRA lump sum distributions received from a pension plan. Individuals age 59½ or older are permitted to make a one-time election to use 5-year forward averaging for a lump sum distribution which is not rolled-over into an IRA. Also, individuals attaining age 50 prior to January 1, 1986, may also make a one time election to use 5 year averaging for a lump sum distribution. The proportion of individuals who roll-over lump-sum distributions and save these assets for retirements was increased by 20 percent to model the impact of these provisions. These assumptions are shown in Table 9A and Table 9B.

-

Lump Sum Payments at Retirement Income -- Individuals are assumed to draw upon their defined contribution lump sum payments (those which were not cashed out) in the form of an annuity. This annuity is assumed to start at the earlier of: (1) the age they accepted social security benefits or (2) the year they first started receiving a defined benefit pension, but not earlier than age 55.

| TABLE 7. Probabilities That Married Individuals Will Choose to Elect the Joint and Survivors Option, by Size of Pension Benefit | ||

| Pension Benfit Size(in 1980 dollars) | Probability of Choosing the Post-RetirementJoint and Survivor's Option | |

| Before REA | After REA | |

| Less than $3,000 | 25% | 75% |

| $3,000 or over | 65% | 80% |

| SOURCE: Lewin-ICF assumptions. | ||

| TABLE 8. Savings Plan Participation Assumptions | |||

| Hourly Wage Levela | Employer Match Rateb | ||

| Low | Medium | High | |

| Less than $4 | 20% | 25% | 30% |

| $4-$7 | 40% | 50% | 60% |

| More than $7 | 60% | 75% | 90% |

SOURCE: Lewin-ICF assumptions. | |||

| TABLE 9A. Proportion of DC LSDs That Are Rolled Over to an IRA, Pre-TRA | ||||||||||

| Earnings(1983 $s) | Under Age 30 | Age 30-34 | Age 45-54 | Age 55-61 | Age 62 or more | |||||

| $3,500 | $3,500+ | $3,500 | $3,500+ | $3,500 | $3,500+ | $3,500 | $3,500+ | $3,500 | $3,500+ | |

| NOT COLLEGE GRADUATE | ||||||||||

| $20,000 | 0.019 | 0.000 | 0.013 | 0.050 | 0.028 | 0.143 | 0.000 | 1.000 | 1.000 | 1.000 |

| $20,000+ | 0.024 | 0.000 | 0.041 | 0.091 | 0.105 | 0.211 | 0.000 | 1.000 | 1.000 | 1.000 |

| COLLEGE GRADUATE | ||||||||||

| $20,000 | 0.037 | 0.000 | 0.015 | 0.061 | 0.075 | 0.364 | 0.000 | 1.000 | 1.000 | 1.000 |

| $20,000+ | 0.040 | 0.154 | 0.051 | 0.178 | 0.120 | 0.450 | 0.000 | 1.000 | 1.000 | 1.000 |

| TABLE 9B. Proportion of DC LSDs That Are Rolled Over to an IRA, Post-TRA | ||||||||||

| Earnings(1983 $s) | Under Age 30 | Age 30-34 | Age 45-54 | Age 55-61 | Age 62 or more | |||||

| $3,500 | $3,500+ | $3,500 | $3,500+ | $3,500 | $3,500+ | $3,500 | $3,500+ | $3,500 | $3,500+ | |

| NOT COLLEGE GRADUATE | ||||||||||

| $20,000 | 0.023 | 0.000 | 0.016 | 0.060 | 0.034 | 0.172 | 0.000 | 1.000 | 1.000 | 1.000 |

| $20,000+ | 0.029 | 0.000 | 0.049 | 0.109 | 0.126 | 0.253 | 0.000 | 1.000 | 1.000 | 1.000 |

| COLLEGE GRADUATE | ||||||||||

| $20,000 | 0.044 | 0.000 | 0.018 | 0.073 | 0.090 | 0.437 | 0.000 | 1.000 | 1.000 | 1.000 |

| $20,000+ | 0.048 | 0.185 | 0.061 | 0.214 | 0.144 | 0.054 | 0.000 | 1.000 | 1.000 | 1.000 |

G. Individual Retirement Account Assumptions

PRISM models the accumulation of IRA savings. The assumptions used in this analysis are derived primarily from IRA participation data provided in the May 1983 EBRI/HHS CPS pension supplement. ICF recalibrated the assumptions used in these simulations so that PRISM assumptions are consistent with the 1983 estimates of: (1) the number of individuals participating in IRAs; and (2) the amount of IRA assets accumulated. The key assumptions in our IRA simulations are summarized below. In addition, we modified the IRA subroutine of PRISM to reflect the impact of the 1986 Tax Reform Act on IRA savings.

-

IRA Adoption for Non-Covered Workers -- Table 10 summarizes the assumptions used in modeling the adoption of IRAs by non-pension covered workers. These estimates do not include workers assumed to roll over vested benefits into IRA arrangements. ICF estimated these adoption rates using May 1983 EBRI/HHS CPS pension supplement data on non-covered individuals establishing an IRA during 1982.

-

IRAs for Covered Workers -- A separate set of IRA adoption probabilities were developed for individuals covered by a pension plan which apply only to 1982 (shown in Table 11). These probabilities were estimated using the May 1983 EBRI/HHS CPS pension supplement data on covered workers who established an IRA in 1982. In years after 1982, the IRA adoption rates for covered workers are assumed to be the same as for non-covered individuals (see Table 9), except as described below.

-

IRA Contributions -- Once an individual is selected to adopt an IRA, PRISM simulates his or her decision to contribute to the account for each year after the IRA is established. The model assumes that individuals contribute only if they are employed during the year. All individuals are assumed to contribute in the year the IRA is established. In succeeding years, individuals are randomly selected to contribute to their account based upon the probabilities presented in Table 12. These probabilities were estimated using May 1983 EBRI/HHS CPS pension supplement data on the number of individuals with IRA accounts who are currently contributing.

-

IRA Contribution Amount -- The amount that individuals are assumed to contribute to their IRA in a given year varies with family income, age, sex, and marital status. If an individual is selected to contribute to an IRA the model randomly selects the amount to be contributed based upon the distribution of IRA contributions reported in the May 1983 EBRI/HHS CPS pension supplement data for individuals in similar age, sex, income and marital status groups. The amounts of these contributions are indexed to real wage changes after 1983. The annual contribution is constrained not to exceed the maximum contribution allowed under the law. After 1986, the maximum contribution amounts specified in the law are indexed at 80 percent of the CPI over time (actual contribution limits are used for each year through 1986). Individuals who reported they had an IRA in 1979 were assumed to have an initial balance of $3,000 (in 1982 dollars) in their account.

-

Impact of Tax Reform Act of 1986 -- The Tax Reform Act modified the maximum tax deductible amount of contributions to IRAs for active participants in qualified pension, profit-sharing, stock-bonus, tax sheltered annuity or government plans. Beginning in 1987, the full contribution amount up to the amount deductible under prior tax law (typically $2,000) is deductible for individuals with Adjusted Gross Income under $25,000 ($40,000 for joint filers, $0 for married filing separately). The deductibility is phased out over the next $10,000 of AGI for the active participants. Anyone may make a non-deductible contribution to the extent that deductible IRA contributions are not allowed. The IRA deduction for all others is retained in its current form. Beginning in 1987, PRISM assumes that annual contributions to IRAs for pension plan participants are limited to the maximum deductible amount allowed for taxpayers at their income level (i.e., individuals will only contribute if the contribution is tax deductible).

| TABLE 10. IRA Adoption Assumptions for Non-Covered Workers, by Age and Family Earnings Level | ||||||

| Family Earnings Level | Age | |||||

| 25-34 | 35-39 | 40-44 | 45-54 | 55-59 | 60-65 | |

| Less than $15,000 | 0.24% | 0.24% | 0.48% | 0.48% | 0.72% | 0.96% |

| $15,000-24,999 | 0.96 | 0.96 | 1.20 | 1.44 | 1.68 | 2.16 |

| $25,000-29,999 | 1.20 | 1.32 | 1.44 | 2.40 | 2.40 | 3.60 |

| $30,000-34,999 | 1.80 | 2.40 | 3.60 | 4.20 | 4.80 | 6.00 |

| $35,000-49,999 | 3.60 | 3.60 | 4.20 | 4.80 | 6.00 | 8.40 |

| $50,000 or More | 6.00 | 6.00 | 6.00 | 6.00 | 12.00 | 12.00 |

| SOURCE: Lewin-ICF estimates, based in part upon the May 1983 EBRI/HHS CPS pension supplement data. | ||||||

| TABLE 11. IRA Adoption Probabilities for Covered Workers in 1982 by Family Income and Age of Worker | ||||||

| Family Earnings Level | Age | |||||

| 25-34 | 35-39 | 40-44 | 45-54 | 55-59 | 60-65 | |

| Less than $15,000 | 4.0% | 7.0% | 4.0% | 9.0% | 13.0% | 20.0% |

| $15,000-24,999 | 8.0 | 8.0 | 9.0 | 17.0 | 27.0 | 19.0 |

| $25,000-29,999 | 9.0 | 14.0 | 16.0 | 23.0 | 30.0 | 47.0 |

| $30,000-34,999 | 16.0 | 20.0 | 19.0 | 28.0 | 46.0 | 51.0 |

| $35,000-49,999 | 16.0 | 27.0 | 31.0 | 43.0 | 46.0 | 45.0 |

| $50,000 or More | 35.0 | 43.0 | 48.0 | 57.0 | 70.0 | 63.0 |

| SOURCE: Lewin-ICF estimates, based in part upon the May 1983 EBRI/HHS CPS pension supplement data. | ||||||

| TABLE 12. Probabilities of Contributing to an IRA in a Given Year Once Selected to Adopt an IRA | ||

| Family Earnings Level(in $ 1982) | Pension Coverage Status | |

| Covered | Not Covered | |

| Less than $25,000 | 48.0% | 60.0% |

| $25,000 or more | 84.0 | 90.0 |

| SOURCE: Lewin-ICF estimates, based in part upon the May 1983 EBRI/HHS CPS pension supplement. | ||

H. Assets in Retirement

For many individuals, assets are an important factor in financing long term care expenditures. Annual income from assets may be used to purchase needed services. In many instances, individuals also liquidate assets to obtain the funds required to pay for care. Consequently, we developed a procedure for estimating asset levels and asset income in retirement for individuals. Both housing and non- housing (financial) assets are simulated.

The model simulates the level of assets and the income from thes e assets for persons age 65 and over in four steps. The model (1) assigns assets to persons age 65 and over in 1979; (2) assigns assets to persons who reach age 65 after 1979; (3) adjusts assets during retirement; and (4) simulates income from assets.

Asset Assignment in 1979 -- First, in 1979, each family unit age 65 and over is assigned a level of assets. This level of assets is based upon a distribution of assets from an analysis of the 1984 Survey of Income and Program Participation (SIPP) Wave 4. The model assigns individuals in PRISM the level of assets of similar individuals from the 1984 SIPP on the basis of age, marital status, income level and pension status. Actual records from the 1984 SIPP, adjusted for inflation and underreporting, are assigned to individuals simulated in PRISM.6 (Table 13 contains an example of the SIPP data.) This allows a distribution of assets, rather than just an average amount for different demographic subgroups. The model imputes the distribution of the level of assets for two types of assets: home equity and all other financial assets. For persons age 65 and over in 1979, the level of net assets assigned is deflated by a factor to account for the growth in assets from 1979 to 1984. Assets in 1984 are deflated by a factor of 1.431 to account for the rate of change in the CPI from 1979 to 1984.

| TABLE 13. Distribution of Elderly Persons by Personal Income and Asset Levels, 1984(1990 dollars) | |||||

| Personal Assets | Personal Income | Total | |||

| Less than$7,500 | $7,500-14,999 | $15,000-29,999 | $30,000and over | ||

| HOME EQUITY | |||||

| $0 or less | 21.9% | 9.5% | 2.6% | 0.7% | 34.7% |

| $1-9,999 | 3.1 | 1.4 | 0.3 | 0.1 | 4.9 |

| $10,000-24,999 | 9.5 | 6.8 | 2.3 | 0.2 | 18.8 |

| $25,000-99,999 | 13.0 | 14.9 | 8.5 | 2.0 | 38.4 |

| $100,000 and over | 0.7 | 1.0 | 0.9 | 0.6 | 3.2 |

| Total | 48.2% | 33.6% | 14.6% | 3.6% | 100.0% |

| FINANCIAL ASSETS | |||||

| $0 or less | 12.2% | 1.5% | 0.2% | 0.0% | 13.9% |

| $1-9,999 | 22.0 | 10.1 | 2.1 | 0.2 | 34.4 |

| $10,000-24,999 | 7.4 | 7.5 | 2.5 | 0.3 | 17.7 |

| $25,000-99,999 | 6.2 | 12.9 | 7.2 | 1.4 | 27.7 |

| $100,000 and over | 0.4 | 1.6 | 2.6 | 1.7 | 6.3 |

| Total | 48.2% | 33.6% | 14.6% | 3.6% | 100.0% |

| TOTAL ASSETS | |||||

| $0 or less | 8.5% | 0.7% | 0.0% | 0.0% | 9.2% |

| $1-9,999 | 11.7 | 3.9 | 0.5 | 0.0 | 16.1 |

| $10,000-24,999 | 8.7 | 4.5 | 0.9 | 0.1 | 14.2 |

| $25,000-99,999 | 17.3 | 18.9 | 7.6 | 1.1 | 44.9 |

| $100,000 and over | 2.0 | 5.6 | 5.6 | 2.4 | 15.6 |

| Total | 48.2% | 33.6% | 14.6% | 3.6% | 100.0% |

| SOURCE: Lewin-ICF analysis of the 1984 Survey of Income and Program Participation (SIPP) (Wave 4). | |||||

Asset Assignment After 1979 -- A similar procedure assigns a level and distribution of assets to individuals who reach the age of 65 after 1979. These probabilities are based upon the distribution and level of assets of persons who were age 65-67 in 1984 in SIPP. Before 1984, assets are reduced by a factor equal to the actual rate of change in the CPI over the time period. The level of assets from 1984 to the present is increased by the actual rate of change in the CPI, and then by the projected rate of change in the CPI assumed under the Alternative II-B assumptions.

Saving and Dissaving During Retirement -- Once assigned a level of assets, the assets of elderly families are adjusted over time to reflect that some elderly save and some dissave during retirement and that real estate generally appreciates. The value of net housing assets is assumed to increase 1.0 percentage points faster than the CPI. Based on an analysis of SIPP data over time, elderly families are assumed to save/dissave as follows:

- 35 percent save at a real rate of two percent annually (financial assets increase two percentage points higher than the rate of change in the CPI);

- 25 percent neither save nor dissave in real terms (financial assets increase at the rate of change in the CPI);

- 40 percent dissave at a real rate of two percent annual (financial asset levels increase two percentage points less than the rate of change in the CPI).

Some individuals who use long term care services will use their assets to pay for these services. This will accelerate this assumed rate of decrease. If an individual dies, his or her spouse receives all assets.7

Income from Assets -- Finally, the model calculates an assumed level of income from non-housing assets for family units age 65 and over. The model assumes that income from non-housing assets is 7 percent prior to 1989, 6.5 percent from 1989 to 1994, and 6 percent in 1995 and after.

I. Supplemental Security Income Program Benefits

PRISM simulates the benefits from the Supplemental Security Income (SSI) program in three steps. The model (1) determines which families and individuals are eligible for SSI benefits using the SSI assets test, (2) estimates the annual benefit they would be entitled to receive from both the federal and state SSI programs, and (3) estimates which eligible families and individuals participate in the program. The SSI program is simulated in PRISM as described below.

Program Filing Unit -- To determine the size of program benefits, elderly individuals are first formed into program "filing units." Each single individual forms one filing unit. Both members of a married couple are treated as a single filing unit, even if one member of the couple is ineligible (i.e., less than age 65). An individual under age 65 is assumed to be potentially eligible for SSI benefits for disabled persons if they are simulated to be disabled under the SSA definition of disability.

Asset Eligibility -- From 1979-83, to be eligible for SSI, individuals must have countable assets no greater than $1,500 for single individuals and $2,250 for married couples. This includes stocks, bonds, countable assets, cash, personal effects in excess of $1,500 and other non-housing assets. Home equity is not included in countable assets. As mandated by the Deficit Reduction Act of 1984 (DEFRA), beginning in 1984, the asset limit for single individuals increases by $100 and the limit for married couples increases by $150 each year until 1989, when they are equal to $2,000 and $3,000, respectively. After 1989, the asset limits are assumed to increase at 50 percent of the rate of increase in the CPI. The model determines asset eligibility by comparing the SSI program filing unit's financial assets, estimated as discussed in the prior section, to the appropriate asset limit.

Benefit Computation -- PRISM calculates net countable income for SSI filing units by summing eligible individuals' monthly countable incomes and subtracting allowable deductions. Countable incomes include eligible individuals' cash income from earnings, social security, pensions, assets, and income of an ineligible spouse. Allowable deductions include: (1) $20 of unearned income; (2) the first $65 of earnings plus 50 percent of earnings above $65; and (3) earnings income of an ineligible spouse up to one-half the maximum monthly federal benefit for a couple. The benefit amount is equal to the positive difference between the maximum monthly benefit and this monthly net income value. The maximum benefit levels vary by marital status, living situation, the presence of an ineligible spouse, and state of residence (see below).8

State Supplementation -- Forty-one states also provide some form of supplementary SSI benefit to elderly families. However, only 26 of these states provide a supplement to most or all of those who participate in the Federal SSI program while the remaining 15 states that supplement benefits do so for only a limited number of elderly facing unusual hardships (e.g., extraordinary expenses such as fire or moving related costs). PRISM estimates supplemental benefits only for the 26 states which provide supplements to most or all eligible individuals. Supplemental payments in these 26 states account for about 90 percent of all state supplemental benefits. These 26 state programs, all of which are administered by the federal government, use the same benefit formula as the one described above, with the exception that the maximum benefit is higher in these states. We assume that the state supplement amounts are fully indexed to inflation by the CPI.

Participation -- Not all eligible individuals chose to participate in the SSI program. Thus, only a portion of those simulated to be eligible for SSI are selected to receive these benefits. The SSI participation rates used in PRISM were estimated so as to replicate administrative data on the number of aged SSI recipients by marital status, family income level, and size of potential benefit.

III. DISABILITY AND MORTALITY OF THE ELDERLY

As discussed in the previous section, disability and mortality are modeled in different ways for persons under age 65 and persons age 65 and over. This section of the documentation describes the modeling of disability and mortality for persons age 65 and over.

A. Disability

In the Brookings/ICF simulations, disabled individuals age 65 and over are defined as those who are unable to conduct at least one instrumental activity of daily living (doing heavy work, doing light work, preparing meals, shopping for groceries or other personal items, getting around inside, walking outside, managing money, and using the telephone) or unable to conduct at least any one of five activities of daily living (eating, bathing, dressing, toileting, and getting in and out of bed).9 In the model, when an individual turns 65 he or she will be assigned one of four disability levels: 1) a deficiency in one or more instrumental activities of daily living (IADL only); 2) a deficiency in one activity of daily living (1 ADL); 3) a deficiency in two or more activities of daily living (2+ ADLs); or 4) no disability.

The model measures the disability status of each individual at the start of each simulation year. During the year, a number of events occur which affect the number of disabled elderly persons:

- some persons become disabled;

- some disabled persons become more disabled;

- some disabled persons die;

- some disabled persons become less disabled or recover from their disability; and

- some disabled persons age 64 turn age 65.

The model only notes intra-year changes for persons who start to use nursing home or home care services and for persons who are discharged from nursing homes. All other changes in disability status are assumed to occur at the start of the next simulation year. The model simulates each of these events using the probabilities described below.

As discussed above, during the year, the model simulates changes in an individual's disability status at the time of admission to or discharge from a nursing home or starting to use noninstitutional services.10 At the start of each simulation year, the model also simulates transitions between disability levels for noninstitutionalized elderly persons, estimated from the 1982-1984 NLTCS (see Table 14). The model uses these transitions, but then controls to overall disability rater by simulating additional persons to become disabled each year to adjust for deaths or remissions from disability. In each simulation year, the model selects a sufficient number of individuals to become disabled so that the proportion of persons who are disabled in the community matches the disability prevalence rates shown in Table 14. These rates vary by level of disability, age, and marital status, and are assumed to hold constant over time.

The disability prevalence rates shown in Table 14 were calculated using data from the 1982-84 National Long Term Care Survey (NLTCS). The numerator of the disability prevalence rate in each age/disability level/marital status cell is equal to the number of disabled persons in that cell from the 1984 NLTCS. The denominator of the disability prevalence rate in each cell is equal to the total (disabled and non-disabled) number of persons in that cell from the 1984 NLTCS.

The transitions of non-institutionalized individuals from one disability level to another were estimated with data from the 1982-84 NLTCS. A set of transition matrices which estimate the probability that a person will be in one of the disability groups in 1984 based upon his or her disability status in 1982 were developed. Separate matrices for each of six age and marital status groups were estimated and the probabilities were then annualized.11 The annual disability transition probabilities for persons age 65 and over are shown in Table 15.

| TABLE 14. Disability Prevalence Rates for the Noninstitutionalizeda | ||||||

| IADL Only | 1 ADL | 2+ ADLs | ||||

| Married | Unmarried | Married | Unmarried | Married | Unmarried | |

| 65-69 | 3.79% | 4.96% | 1.74% | 2.69% | 3.45% | 3.67% |

| 70-74 | 5.01 | 6.62 | 2.68 | 3.73 | 5.11 | 4.66 |

| 75-79 | 6.90 | 8.64 | 3.24 | 5.77 | 7.71 | 7.15 |

| 80-84 | 10.34 | 11.25 | 6.03 | 8.07 | 12.93 | 11.35 |

| 85-89 | 11.36 | 13.64 | 7.57 | 11.21 | 21.77 | 15.81 |

| 90+ | 7.50 | 15.45 | 20.00 | 13.69 | 26.25 | 31.35 |

SOURCE: Brookings Institution and Lewin-ICF calculations using data from the 1982-84 National Long Term Care Survey. | ||||||

| TABLE 15. Annual Disability Transition Probability Matrices for the Noninstitutionalized Elderly | ||||||||

| Disability Level T1 | UnmarriedDisability Level T2 | MarriedDisability Level T2 | ||||||

| Non-Disabled | IADLOnly | 1 ADL | 2+ ADLs | Non-Disabled | IADLOnly | 1 ADL | 2+ ADLs | |

| AGE 65-74 | ||||||||

| Non-Disabled | 95.80% | 2.26% | 1.02% | 0.92% | 97.00% | 1.46% | 0.59% | 0.95% |

| IADL Only | 9.58% | 71.90% | 12.20% | 6.32% | 11.86% | 70.10% | 9.79% | 8.25% |

| 1 ADL | 4.27% | 25.15% | 49.70% | 20.88% | 7.01% | 18.55% | 56.30% | 18.14% |

| 2+ ADLs | 2.48% | 8.87% | 13.84% | 74.80% | 2.52% | 7.36% | 10.31% | 79.80% |

| AGE 75-84 | ||||||||

| Non-Disabled | 90.80% | 4.71% | 2.67% | 1.82% | 93.50% | 3.57% | 1.08% | 1.85% |

| IADL Only | 5.91% | 66.10% | 16.16% | 11.83% | 7.16% | 71.00% | 8.87% | 12.96% |

| 1 ADL | 3.13% | 19.10% | 59.60% | 18.16% | 4.36% | 19.20% | 48.50% | 27.93% |

| 2+ ADLs | 0.53% | 6.88% | 8.99% | 83.60% | 2.41% | 6.84% | 10.05% | 80.70% |

| AGE 85+ | ||||||||

| Non-Disabled | 25.30% | 28.51% | 24.50% | 21.69% | 82.60% | 7.51% | 3.75% | 6.14% |

| IADL Only | 0.45% | 69.10% | 15.23% | 15.23% | 2.37% | 69.20% | 11.85% | 16.58% |

| 1 ADL | 0.62% | 11.13% | 56.70% | 31.55% | 3.96% | 7.92% | 48.50% | 39.62% |

| 2+ ADLs | 0.46% | 2.77% | 7.37% | 89.40% | 0.00% | 6.40% | 8.00% | 85.60% |

| SOURCE: Lewin-ICF and Brookings calculations using the 1982-84 National Long Term Care Survey. | ||||||||

In the model, 60 percent of individuals receiving Disability Insurance (DI) program benefits at age 62 are assumed to be "disabled" upon reaching age 65 (using the above definition of disability for persons 65 and over).12 "Disabled" individuals under age 65 are defined to be persons who meet the Social Security Administration's work disability eligibility criteria for Disability Insurance program benefits. Although this definition of disability is appropriate for simulating the receipt of Disability Insurance benefits for persons under 65, it is an inappropriate definition to use in simulating disability for the elderly for the use of long term care services. When the 60 percent of DI recipients who are simulated to continue to be disabled at age 65 turn age 65, they are assigned one of the three disability levels using the prevalence rates in Table 16.13

B. Mortality

As discussed in the previous section, PRISM uses the Alternative II-B mortality assumptions from the 1988 Social Security Trustees' Report to estimate deaths for persons under age 65. Separate rates are used for disabled and nondisabled persons under age 65.

The Alternative II-B mortality assumptions are also used to determine the aggregate mortality rate by age and sex for persons age 65 and over. After individuals reach age 65, however, the model separately simulates mortality for three groups of people:

- individuals in nursing homes;

- noninstitutionalized disabled individuals (IADL only, 1 ADL, and 2+ ADLs); and

- noninstitutionalized, nondisabled persons.

Different procedures are required to estimate mortality for these groups in order to account for differences in mortality across institutionalized, disabled, and nondisabled individuals.

| TABLE 16. Disability Prevalence Rates for Noninstitutionalized Disability Insurance Recipients Simulated to Continue Being Disabled at Age 65a | ||

| Disability Level | Married | Unmarried |

| IADL Only | 42.20% | 43.81% |

| 1 ADL | 19.37 | 23.76 |

| 2+ ADLs | 38.43 | 32.42 |

| Total | 100.0% | 100.0% |

SOURCE: Brookings Institution and Lewin-ICF calculations using data from the 1982-84 National Long Term Care Survey. | ||

1. Mortality for Institutionalized Individuals

Each institutionalized individual is assumed to survive in the nursing home throughout the length of stay assigned by the model. As discussed below, when an individual is selected to enter a nursing home, the model uses data from the 1985 NNHS to simulate whether the individual is to be discharged alive or dead (Table 20). If the model indicates that the individual will die in the nursing home, the individual is assume d to die at the end of his or her nursing home stay.

2. Mortality for Noninstitutionalized Individuals

The model uses the Alternative II-B mortality assumptions to determine the overall mortality rate for individuals by age and sex for each year in the future. Table 17 shows these rates for 1985. The Alternative II-B assumptions include projected rates of improvement in mortality.14 The model uses these adjusted rates for future years. Once the model has determined the overall mortality rate for each age/sex group, the model subtracts the number of deaths in nursing homes from the aggregate rates. This produces an estimate of the number of deaths among the noninstitutionalized. The model then estimates the mortality of the noninstitutionalized by distributing the remaining deaths among them, according to separate mortality rates estimated for each of the four disability status groups for each age/sex group.

The relative mortality rates of the noninstitutionalized were estimated using data from the 1982-84 NLTCS and are shown in Table 18.15 A numerical example best illustrates the process. Assume the mortality rate for a 77 year old man is 7.4 percent. After accounting for deaths among 77 year old men in nursing homes, the remainder of deaths are divided among the noninstitutionalized. We estimate that the mortality rate for nondisabled men age 77 is 4.9 percent, that the rate for 77 year old men with only IADL deficiencies is 5.9 percent, that the rate for 77 year old men with one ADL deficiency is 7.3 percent, and that the rate for men with two or more ADL deficiencies is 10.3 percent.

| TABLE 17. Mortality Rates for the Noninstitutionalized Elderly in 1985 | |||||

| MALES | |||||

| Age | Overall | Non-Disabled | IADL Only | 1 ADL | 2+ ADLs |

| 65 | 0.02882 | 0.02375 | 0.04512 | 0.06174 | 0.09024 |

| 66 | 0.03152 | 0.02525 | 0.04797 | 0.06564 | 0.09594 |

| 67 | 0.03429 | 0.02660 | 0.05053 | 0.06915 | 0.10106 |

| 68 | 0.03709 | 0.02818 | 0.05355 | 0.07327 | 0.10709 |

| 69 | 0.03999 | 0.03005 | 0.05709 | 0.07812 | 0.11418 |

| 70 | 0.04311 | 0.03163 | 0.06010 | 0.08224 | 0.12020 |

| 71 | 0.04654 | 0.03286 | 0.06243 | 0.08543 | 0.12487 |