Updated January 8, 2015

Since open enrollment began on November 15, 2014, millions of Americans can once again shop for high-quality, affordable health care coverage in the Health Insurance Marketplace established by the Affordable Care Act.1 Our research indicates that the Affordable Care Act is working to enhance competition, expand choice and promote affordability among Marketplace health insurance plans in 2015.2

This year, the Marketplace is welcoming new consumers as well as encouraging those who enrolled last year to come back, update their information and select the plan that best meets their needs. All plans in the Marketplace cover essential health benefits and recommended preventive care, and do not exclude people based on preexisting conditions. Consumers can see detailed information about each health insurance plan offered in their area before they apply. Factors they may consider in choosing a health insurance plan include premiums, deductibles, out-of-pocket costs, provider network, formulary, customer service and more.3 Consumers may be eligible for financial assistance to help pay for the cost of premiums. In fact, 85 percent of consumers who selected a Marketplace plan in 2014 received financial assistance.4

This brief presents analysis of Qualified Health Plan (QHP) data in the Marketplace for 35 states, providing a look at the plan choice and premium landscape that new and returning consumers will see for 2015.5 It also examines plan affordability in 2015 after taking into account premium tax credits. The findings presented here include states for which sufficient plan data were available for both 2014 and 2015.

Key Findings

- The Affordable Care Act is increasing competition and choice among affordable Marketplace health insurance plans in 2015.

- There are over 25 percent more issuers participating in the Marketplace in 2015. About 91 percent of consumers will be able to choose from 3 or more issuers—up from 74 percent in 2014. Consumers can choose from an average of 40 health plans for 2015 coverage—up from 30 in 2014—based on analysis at the county level.

- Premiums for the benchmark (second-lowest cost) silver plan will increase modestly, by 2 percent on average this year before tax credits, while premiums for the lowest-cost silver plan will increase on average by 5 percent. The plans offering the lowest prices have sometimes changed from 2014 to 2015, so consumers should shop around to find the plan that best meets their needs and budget.

- More than 7 in 10 current Marketplace enrollees can find a lower premium plan in the same metal level before tax credits by returning to shop. To illustrate the significance of shopping we consider the following example: if all consumers switched from their current plan to the lowest-cost premium plan in the same metal level, the total savings in premiums would be over $2 billion. These savings represent the sum of savings to consumers and taxpayers.

- For customers returning to the Marketplace, the vast majority of enrollees have low cost plans available to them. If they look across all metal levels, fully 79 percent of current Marketplace enrollees can get coverage for $100 or less, after any applicable tax credits, in 2015.

- Sixty-five percent of current Marketplace enrollees can get coverage for $100 or less for 2015, after tax credits, if they shop for a more affordable plan within their current metal level, compared to 50 percent of current Marketplace enrollees who can get coverage for $100 or less, after any applicable tax credits, if they stay in the same plan in 2015.

1 The Health Insurance Marketplace includes the Marketplaces established in each of the states (and the District of Columbia) and run by the state or the federal government. This report addresses the individual market Marketplaces that use the HealthCare.gov eligibility and enrollment system in both 2014 and 2015.

2 It is important to note that this brief uses only information on individuals who selected a Marketplace individual market health plan, and the analysis excludes stand-alone dental plans.

3 This brief does not analyze consumers’ final expenses, after considering other health plan features, such as deductibles and copayments. Consumers may examine all elements of health insurance plans in order to estimate expected total out-of-pocket costs. Moreover, while premium tax credits can be applied to a plan in any metal tier with the exception of catastrophic plans, cost-sharing reductions are available only for silver plans.

4 This represents the percentage of individuals who selected a Marketplace plan and qualified for an advance premium tax credit (APTC), with or without a cost-sharing reduction. See: U.S. Department of Health and Human Services, “Health Insurance Marketplace: Summary Enrollment Report for the Initial Annual Open Enrollment Period,” ASPE Issue Brief, ASPE, May 1, 2014, available at: http://aspe.hhs.gov/health/reports/2014/MarketPlaceEnrollment/Apr2014/i…

5 The 35 states for which sufficient data in the individual market were available in both 2014 and 2015 for this analysis are listed in the methodology section at the end of this brief. References to the Marketplace in this report refer to the individual market Marketplaces that use the HealthCare.gov eligibility and enrollment system in both 2014 and 2015. The small group Marketplace, also known as SHOP, is not included in this brief.

"Consumer Choice among Health Insurance Issuers in 2014 and 2015

The Affordable Care Act is working to create a dynamic, competitive Marketplace, with more choice and affordable premiums in 2015. This offers new opportunities for consumers to comparison shop to select the plan that best meets their needs and budget. More choice also means more competition between plans that in turn results in downward pressure on premiums. Consumers who bought a 2014 plan and decide to shop actively for a comparable 2015 plan will often be able to find lower premiums.

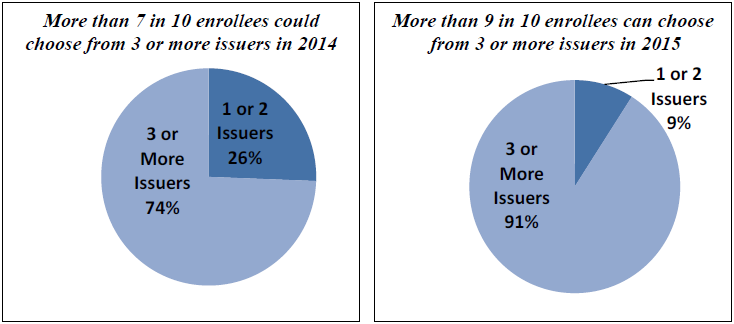

There are 25 percent more issuers participating in the Marketplace in 2015, compared with 2014.6 During the 2014 open enrollment period, 74 percent of the people who enrolled in a qualified health plan lived in counties with three or more issuers offering plans in the Marketplace; for 2015 this percentage has increased to 91 percent.

Figure 1 shows the distribution of the 2014 Marketplace enrollees by the number of issuers in their county.

FIGURE 1

Enrollee Choice of Marketplace Issuers in 35 States in 2014 and 2015

Source: Information on plans and issuers is from the plan landscape files as of November 2014 for 35 states.

Note: See “Methods and Limitations” section for more details regarding data and methods used. “Enrollees” refers to those people who selected a qualified health plan in the Marketplace in 2014 and is based on active plan selections in the CMS Multidimensional Insurance Data Analytics System (MIDAS) as of May 12, 2014. The number of issuers available to those who selected a Marketplace plan in 2014 is based on the number of issuers offering qualified health plans in 2015 in the county of residence of those persons.

Consumers can also choose from among more plans for 2015 coverage. On average, there are 40 plans available per county, including catastrophic plans. This is an increase from an average of 30 total plans per county last year. Note that previous ASPE issue briefs on plan choice and availability presented analyses at the rating area level. Because plans available in some part of a rating area are not always available in all parts of a rating area, conducting the analysis at the county level better captures the set of options consumers will see when they shop and thus more closely matches consumers’ shopping experience.

The average number of plans per county in the bronze, silver, gold, and platinum metal tiers—which signify different levels of plan actuarial value or how much of every claim dollar the plan covers—has also increased from 2014 (see Table 1).

TABLE 1

Summary of Marketplace Health Plans and Issuers for 35 States, 2014 and 2015

| 2014 Average | 2015 Average | |

|---|---|---|

| Issuers per State | 5 | 7 |

| Issuers per County | 3 | 4 |

| Total Qualified Health Plans (excluding catastrophic) | 28 | 37 |

| Total Health Plans | 30 | 40 |

| Catastrophic Plans | 3 | 2 |

| Bronze Plans | 9 | 12 |

| Silver Plans | 10 | 15 |

| Gold Plans | 8 | 9 |

| Platinum Plans | 1 | 2 |