Americans living at the bottom of the income distribution often struggle to meet their basic needs on very limited incomes, even with the added assistance of government programs. The following analyses describe the characteristics of the poor population; available income for those at the deepest levels of poverty; and average medical care needs among those living in poor and deep poor families (meaning those with incomes below 50 percent of the poverty threshold)2. The brief concludes with implications for medical cost sharing among those with few resources available. Analyses are restricted to those under the age of 65 and those in families headed by an adult under age 65.

Key findings include:

- Low-income individuals are especially sensitive to even nominal increases in medical out-of-pocket costs, and modest copayments can have the effect of reducing access to necessary medical care.

- Medical fees, premiums, and copayments could contribute to the financial burden on poor adults who need to visit medical providers.

- The problem is even more pronounced for families living in the deepest levels of poverty, who effectively have no money available to cover out-of-pocket medical expenses including copays for medical visits.

Who are the People Living in Poverty and Deep Poverty?

According to the most recent data from 2013, the official poverty rate is 14.5 percent of the population, with 45.3 million people officially poor. Among the poor, 19.9 million people are in deep poverty, defined as income below 50 percent of the poverty threshold. Of the total U.S. population, 6.3 percent are in deep poverty. Nearly 6.5 million children under the age of 18 are in deep poverty, making up about one-third of the deep poverty population.3

Table 1 describes the demographic and economic characteristics of the population in poverty by depth of poverty.

- Nearly two-thirds (64 percent) of working age adults with family incomes below 50 percent of the poverty threshold are adults that live with no children, while over one-third (36 percent) live in households with children.

- Among working age adults with family incomes between 50 and 100 percent of the poverty threshold, about one-third (33-34 percent) work part-time or part-year, compared with one-quarter (26 percent) of those with family incomes below 50 percent of poverty.

- Looking at those in deep poverty, for adults with family incomes between 25 and 50 percent of poverty, about half report no work hours, and for those with incomes below 25 percent of poverty, 81 percent report no work hours. Working age adults in deep poverty report illness or disability (23 percent), taking care of their family (27 percent), and attending school (21 percent) as the main reasons why they are not working.4

- Just above the poverty threshold, more than half (57 percent) of uninsured adults ages 19 to 64 who could gain Medicaid coverage (between 100 and 138 percent of poverty) work, and nearly three out of four (72 percent) live in a family with at least one worker.5

Table 1. Demographic and Economic Characteristics Distribution by Poverty Status

| Percentage of Poverty Threshold | In Deep Poverty (Below 50%) | In Poverty (Below 100%) | ||||

|---|---|---|---|---|---|---|

| 0-24% | 25-49% | 50-74% | 75-99% | |||

| Note: Columns add to 100 percent in each panel. Source: HHS-ASPE tabulations from the U.S. Census Bureau, Current Population Survey, 2014 Annual Social and Economic Supplement. | ||||||

| Race/Ethnicity (ages 0-64) | ||||||

| White, non-Hispanic | 42 | 39 | 37 | 40 | 41 | 39 |

| Black, non-Hispanic | 23 | 25 | 24 | 21 | 24 | 23 |

| Hispanic | 25 | 28 | 32 | 32 | 26 | 29 |

| Other | 9 | 7 | 7 | 7 | 9 | 8 |

| Family Household Type (ages 18-64) | ||||||

| Adults, no children in household | 70 | 51 | 52 | 56 | 64 | 59 |

| 1 Adult with child in household | 8 | 14 | 11 | 7 | 10 | 9 |

| 2+ Adults with child in household | 22 | 35 | 37 | 36 | 26 | 32 |

| Employment status (ages 18-64) | ||||||

| 30+ hours, full year | 2 | 7 | 12 | 20 | 4 | 10 |

| Part time or part year | 17 | 43 | 34 | 33 | 26 | 30 |

| No hours | 81 | 50 | 53 | 47 | 71 | 59 |

Income and Expenditures

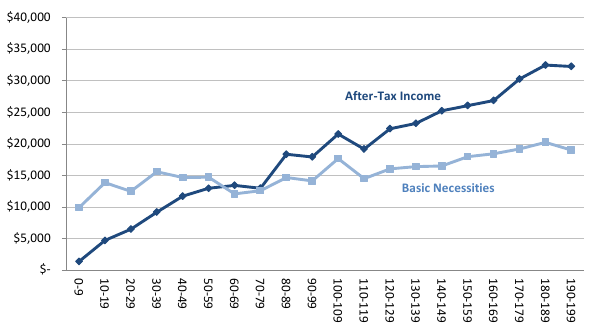

Many families living in poverty and deep poverty face difficulties making ends meet financially, as presented in Figure 1 and Table 2. The dark blue line in Figure 1 depicts families’ after-tax income, including benefits from the Supplemental Nutrition Assistance Program (SNAP) and tax credits such as the Earned Income Tax Credit (EITC). The light blue line depicts families’ actual spending on the most basic necessities, defined here as food, clothing, housing, and utilities. The definition of basic necessities for these figures is quite conservative, as it excludes expenditures on many other high-priority categories such as health care, transportation, education, and child care. In addition, as shown in Figure 1 and Table 2, families’ spending on these basic necessities rises with income, which suggests that families with low incomes would be spending more in these areas if they did not face such serious financial pressures. Thus, the estimates shown in Figure 1 and Table 2—which are based on families’ actual spending—may understate, potentially substantially, the actual income required to ensure that families can achieve a minimally adequate standard of living, even focusing solely on basic necessities.

Figure 1. After-Tax Incomes and Expenditures on Basic Necessities (Food, Clothing, Housing, and Utilities) for Non-Elderly Families by Poverty Status

Percentage of Poverty Threshold

Source: HHS-ASPE tabulations from the 2011 Panel Study of Income Dynamics.

Even under this conservative approach, the data displayed in Figure 1 show that poor families’ incomes are often not enough to cover even the most basic necessities. For example, a family with income between 40 and 50 percent of the poverty threshold spends on average $3,000 more on necessities than its income. For a family with income between 20 and 30 percent of the poverty threshold, expenditures on basic necessities exceed income by $6,000 on average. Families living in deep poverty have incomes that are below their expenditures for the most basic necessities and often must borrow or use savings to meet basic needs, before even considering the other types of high-priority spending noted above or accounting for the fact that these families may not be spending enough on basic necessities to ensure even a minimally adequate standard of living in these areas. Families in poverty but with slightly higher incomes still struggle to meet basic needs, as do many families above the poverty threshold.

Table 2. Average Annual After-Tax Incomes, and Incomes After Expenditures on Basic Necessities (Food, Clothing, Housing, and Utilities) for Non-Elderly Families by Poverty Status

| Percentage of Poverty Threshold | After-Tax Income | Expenditures on Basic Necessities | Income After Expenditures on Basic Necessities |

|---|---|---|---|

| Note: Dollar amounts are rounded to the nearest $100. Estimates are averaged across families of all sizes. Family heads are under age 65. Source: HHS-ASPE tabulations from the 2011 Panel Study of Income Dynamics. | |||

| 0-9% | $1,400 | $9,900 | -$8,500 |

| 10-19% | 4,700 | 13,900 | -9,200 |

| 20-29% | 6,500 | 12,500 | -6,000 |

| 30-39% | 9,200 | 15,600 | -6,400 |

| 40-49% | 11,700 | 14,700 | -3,000 |

| 50-59% | 13,000 | 14,700 | -1,800 |

| 60-69% | 13,400 | 12,100 | 1,400 |

| 70-79% | 13,000 | 12,600 | 400 |

| 80-89% | 18,400 | 14,700 | 3,700 |

| 90-99% | 17,900 | 14,100 | 3,800 |

| 100-109% | 21,600 | 17,700 | 3,900 |

| 110-119% | 19,200 | 14,500 | 4,700 |

| 120-129% | 22,400 | 16,100 | 6,400 |

| 130-139% | 23,200 | 16,400 | 6,800 |

| 140-149% | 25,200 | 16,500 | 8,700 |

| 150-159% | 26,100 | 18,000 | 8,100 |

| 160-169% | 26,900 | 18,400 | 8,500 |

| 170-179% | 30,300 | 19,200 | 11,100 |

| 180-189% | 32,500 | 20,200 | 12,200 |

| 190-199% | 32,300 | 19,000 | 13,300 |

Medical Care Among People in Poverty and Deep Poverty

In addition to the most basic necessities of food, clothing, housing, and utilities, poor and deep poor families also must consider their health and medical visit needs. Medical fees and copayments potentially contribute to a yet greater financial burden on people who visit their medical providers more frequently. Table 3 presents estimates of the average number of annual outpatient medical visits for working age adults living in poverty and covered by Medicaid. As indicated in the table, poor individuals have 6.6 medical visits per year on average. For those living in deep poverty, the average number of visits is similar (6.2). Out-of-pocket costs for these visits can put a substantial strain on household budgets. But the negative effects of out-of-pocket costs are even more pronounced, because the distribution of medical visits among adults covered by Medicaid is concentrated among some recipients who are even more burdened by out-of-pocket costs. One way to examine this distribution is to place adults covered by Medicaid into four quartiles based on number of annual visits (Table 3). When considering the average number of visits by quartiles for the poor, estimates indicate that those in the fourth quartile - and therefore most likely to visit the doctor— average 13.3 medical visits each year.

Table 3. Average Annual Number of Outpatient Medical Visits for Adults Ages 19-64 Covered by Medicaid

| Percentage of Poverty Threshold | Average annual visits | Distribution by Number of Medical Visits | |||

|---|---|---|---|---|---|

| First quartile | Second quartile | Third quartile | Fourth quartile | ||

| Source: HHS-ASPE tabulations from the Survey of Income and Program Participation 2011. | |||||

| 0-99% | 6.6 | 0.0 | 1.0 | 2.4 | 13.3 |

| 0-49% | 6.2 | 0.0 | 1.0 | 2.4 | 13.5 |

| 50-99% | 6.9 | 0.0 | 1.0 | 2.4 | 13.2 |

People with income at or slightly above the poverty threshold have little income to direct towards key goods and services like transportation, precautionary savings, and educational investments. Cost sharing through copayments and premiums for a necessity like medical care and health insurance will discourage use of needed care, including preventive services, and place significant strain on already limited household budgets.

Implications of Cost-Sharing for the Poor

The analysis above demonstrates that families living in poverty, and particularly those in deep poverty, have few resources available after they pay for the most basic necessities, even before other critical expenditures such as health care, child care, and transportation are taken into account (Table 2). Low-income adults tend to be less healthy than higher-income adults. About one-quarter of adults ages 19 to 64 living in poverty report fair or poor health, compared with about 8 percent of those living above 200 percent of the poverty threshold.6 When subject to copayments and premiums, low-income individuals must decide whether to go to the doctor, fulfill prescriptions, or pay for other basic needs like child care and transportation. As a result of these daily tradeoffs, low-income individuals are especially sensitive to modest and even nominal increases in medical out-of-pocket costs.

Research shows that increases in cost-sharing in the form of copayments can discourage individuals with low income from accessing necessary medical care, which can have negative health consequences. An analysis of the Oregon Health Plan redesign implemented between 2003 and 2005 found that increased out-of-pocket costs such as mandatory copayments are associated with unmet health care needs, reduced use of care, and financial strain for already vulnerable populations.7 A study of Utah’s Medicaid program found that $2 copayments for physician services resulted in Medicaid patients seeing doctors less often.8 The national RAND Health Insurance Experiment found that low-income individuals reduce their use of effective care by as much as 44 percent after being subject to copayments.9 The study also found that copayments lead to poorer health outcomes among low-income adults and children due to a reduction in the use of care, including worse blood pressure and vision and higher rates of anemia.10

Americans living in poverty have significantly constrained budgets that severely limit their ability to pay out-of-pocket health care costs; those in deep poverty have literally no available income after they pay for their most basic necessities each month, necessities which do not include health care, child care, or transportation. People in poverty tend to be less healthy than those with higher incomes and therefore need more medical care. But people in poverty are often unable to afford even nominal premiums and copayments, and research shows that they may forgo necessary medical treatment as a result of required cost-sharing.

Methodological Appendix

Current Population Survey (CPS)

The data for Table 1 come from the 2014 CPS Annual Social and Economic Supplement (ASEC), which sampled about 68,000 households for the newly redesigned income items. Income and poverty data are for the 2013 calendar year. Following Census Bureau methodology, calculations for determining poverty use pre-tax cash income. Poverty thresholds vary by family size and composition. Table 4 shows the poverty thresholds by family type, divided by poverty sublevel.

Table 4. Annual Poverty Thresholds by Family Type, 2013

| Family Type | Percentage of Poverty Threshold | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 10% | 20% | 30% | 40% | 50% | 60% | 70% | 80% | 90% | 100% | |

| Source: HHS-ASPE tabulations from the U.S. Census Bureau, Current Population Survey, 2014 Annual Social and Economic Supplement. | ||||||||||

| 1 adult | $1,212 | $2,424 | $3,636 | $4,848 | $6,060 | $7,271 | $8,483 | $9,695 | $10,907 | $12,119 |

| 2 adults | 1,560 | 3,120 | 4,680 | 6,240 | 7,800 | 9,360 | 10,920 | 12,480 | 14,040 | 15,600 |

| 1 parent, 2 children | 1,877 | 3,754 | 5,631 | 7,508 | 9,385 | 11,261 | 13,138 | 15,015 | 16,892 | 18,769 |

| 2 parents, 2 children | 2,362 | 4,725 | 7,087 | 9,450 | 11,812 | 14,174 | 16,537 | 18,899 | 21,262 | 23,624 |

| 1 parent, 4 children | 2,738 | 5,475 | 8,213 | 10,950 | 13,688 | 16,426 | 19,163 | 21,901 | 24,638 | 27,376 |

Panel Study of Income Dynamics (PSID)

The data for Figure 1 and Table 2 were calculated from the 2011 wave of the PSID, a national longitudinal survey that collects income and expenditure data on a sample of families in the United States.11 Previous research has found that average reported expenditures on the PSID are similar to expenditures reported on the Consumer Expenditure Survey.12 Basic necessities include expenditures on four categories that are widely believed to be basic necessities including: food, clothing, housing, and utilities. Utilities include expenditures on electricity, gas, water and sewer, telephone and Internet, and other utilities. The definition of basic necessities excludes expenditures on many other high-priority categories such as health care, transportation, education, and child care expenses.

Family income includes after-tax earnings, cash income transfers such as Social Security, disability payments, and Temporary Assistance for Needy Families (TANF), and near-cash benefits from the Supplemental Nutrition Assistance Program (SNAP), formerly called the Food Stamp program. It excludes income from capital gains, and other non-cash transfers such as the Women, Infants, and Children (WIC) nutrition program, the Low Income Home Energy Assistance Program (LIHEAP), and housing assistance. Taxes are measured using National Bureau of Economic Research’s TAXSIM model and include estimates of federal, state, and the employee’s portion of Social Security and Medicare taxes, as well as the value of tax credits such as the Earned Income Tax Credit (EITC). Percent of poverty is calculated by dividing each family’s pre-tax income by their corresponding poverty threshold. The analysis excludes families that were not living in the United States at the time of the survey, families living in institutions, and families headed by persons ages 65 and older. Estimates are averaged across families of all sizes.

Survey of Income and Program Participation (SIPP)

The data in Table 3 are from the 2008 SIPP, which sampled about 42,000 households starting in 2008 and interviewed all individuals in the household over the age of 15. Estimates of income and medical visits come from the tenth wave of the panel, reflecting the period from September – December of the 2011 calendar year. The number of medical visits is self-reported by all individuals. Specifically, respondents answered the question: “Not including contacts during hospital stays during the past 12 months, that is, since (interview month) 1st of last year, about how many times did you see or talk to a medical doctor, or nurse, or other medical provider about your health?” The responses ranged from zero to 366 visits. While the responses do not include hospital stays, they may include emergency room visits. The quartile analysis is conducted by dividing the sample into four ordered groups based on the number of self-reported medical visits, and estimating the mean value separately for each quartile.

1 Analysis conducted by Lauren Frohlich, Kendall Swenson, Sharon Wolf, Suzanne Macartney, and Susan Hauan.

2 For 2013, a single parent family with two children is in poverty if their income falls below 100 percent of the poverty threshold ($18,769) and deep poverty if their income falls below 50 percent of the poverty threshold ($9,385).

3 HHS-ASPE tabulations from the U.S. Census Bureau, Current Population Survey, 2014 Annual Social and Economic Supplement.

4 Additional reasons include inability to find work (15 percent) and retirement (8 percent). HHS-ASPE tabulations from the U.S. Census Bureau, Current Population Survey, 2014 Annual Social and Economic Supplement.

5 Kaiser Family Foundation, 2015. “Are Uninsured Adults Who Could Gain Medicaid Coverage Working?”

6 U.S. Census Bureau, Current Population Survey, 2014 Annual Social and Economic Supplement. CPS Table Creator, available at http://www.census.gov/cps/data/cpstablecreator.html.

7 Wright, Bill J. et al, 2010. Health Affairs. “Raising Premiums and Other Costs for Oregon Health Plan Enrollees Drove Many to Drop Out.”

8 Ku, Leighton et al., 2004. Center on Budget and Policy Priorities. “The Effects of Copayments on the Use of Medical Services and Prescription Drugs in Utah’s Medicaid Program.”

9 Newhouse, Joseph, 1996. Free For All? Lessons from the Rand Health Insurance Experiment, Cambridge: Harvard University Press; Ku, Leighton. Center on Budget and Policy Priorities, 2003. “Charging the Poor More for Health Care: Cost-Sharing in Medicaid.” Effective care refers to services the researchers judged to be clinically effective in improving health outcomes.

10 Id.

11 Andreski, Patricia et al., 2013. "PSID Main Interview User Manual: Release 2013."

12 Li, Geng et al., 2010. "New Expenditure Data in the Panel Study of Income Dynamics: Comparisons with the Consumer Expenditure Survey Data," Monthly Labor Review.