Submitted to:

Office of the Assistant Secretary for Planning and Evaluation (ASPE)

U.S. Department of Health and Human Services (HHS)

Alana Landey and Gretchen Lehman, Project Officers

Submitted from:

American Institutes for Research

Elizabeth Frentzel, Deepa Ganachari, Megan Bookhout, Marilyn Moon, Julia Galdo, and Sandra Robinson

Introduction

Consumer education regarding both financial and health decision making has been an important issue for many years. The U.S. Department of Health and Human Services (HHS) Office of the Assistant Secretary for Planning and Evaluation (ASPE) initiated this project to identify the intersections of financial literacy and health literacy, the lessons each has to impart, and how and where each influences the other as a step toward improving understanding of this complex field. This study identifies current financial and health literacy strategies, initiatives, and programs conducted by HHS, selected agencies external to HHS, and selected private organizations. We structured the study to address the following research questions:

- Which programs involve consumer education components that focus on health literacy and financial literacy?

- Are there similarities between the consumer education competencies measured and promoted in health literacy initiatives and in human services financial education programs?

- Are any components of health literacy initiatives translatable to financial literacy initiatives in the human services arena, and conversely, are any components of financial literacy translatable to health literacy?

- Which financial and health literacy approaches have been developed for different groups, such as older adults, immigrants, and other non-native English speakers, and very low-income audiences?

- What behavioral change research has been done on these topics?

- What are the definitions of efficacy and success, and what specific behaviors do they require of consumers?

- What is the evidence surrounding the effectiveness of Federal financial literacy and health literacy initiatives?

- Are there examples of initiatives or literacy curriculums in programs that integrate health literacy and financial education?

- Are there any examples of, or opportunities for, coordination of consumer education initiatives across HHS operating divisions and, potentially, with other federal programs external to HHS?

- What lessons can other major financial and health literacy programs provide to support HHS initiatives for strengthening consumer education programs? What core competencies do they share with HHS programs, and what can we learn from their successes and failures?

This report is organized into six sections: an introduction, a description of the policy context, an explanation of investigative methods, findings from the literature review, findings from the interviews, and a discussion of next steps and implications for the future.

Terms and Definitions

Our focus in this study was on financial and health literacy initiatives aimed at low-income individuals. Financial literacy is the ability to make informed judgments and manage money effectively (U.S. Government Accounting Office [GAO], 2006). Health literacy is the ability to obtain, process, and understand basic health information to make appropriate health-related decisions (HHS, 2010). Consumers encounter complex information and may need to understand not only information about their health condition but also information about the risks and benefits of different treatments, how and when to take medications, and how to understand test results.

Literacy includes three types of literacy prose, document, and quantitative because adults use different kinds of printed materials in their daily lives. These types of literacy include:

- Prose literacy: The knowledge and skills needed to perform prose tasks, (i.e., to search, comprehend, and use continuous texts). Examples include editorials, news stories, brochures, and instructional materials.

- Document literacy: The knowledge and skills needed to perform document tasks, (i.e., to search, comprehend, and use non-continuous texts in various formats). Examples include job applications, payroll forms, transportation schedules, maps, tables, and drug or food labels.

- Quantitative literacy or numeracy: The knowledge and skills required to perform quantitative tasks, (i.e., to identify and perform computations, either alone or sequentially, using numbers embedded in printed materials). Examples include balancing a checkbook, figuring out a tip, completing an order form, or determining the total amount that an item or items cost.

(Kutner, Greenberg, Jin, & Paulsen, 2006)

These three types of literacies are all used in health and financial literacy, but not necessarily to the same degree. Due to the sheer volume and rapidly growing nature of health literature and resources, it is likely that health literacy may include more prose literacy and document literacy compared to quantitative literacy. Financial literacy, on the other hand, has many stable concepts, but is far more likely to involve more document literacy, and especially quantitative literacy compared to prose literacy. If the literacy is used without modifier in this report, (i.e. financial or health) it is always referring to this definition.

Additional technical terms that are likely to be unfamiliar to persons in either the health or financial fields will be defined in footnotes.

Policy Context

The events of the last decade have underscored the challenges arising for consumers in both the financial and the health decision making areas. The recent economic crisis has strained the financial health of many households in the United States. Medical debt alone has contributed to bankruptcy: In one study of individuals filing for bankruptcy, almost 60% indicated that medical bills contributed to bankruptcy (Himmelstein, Warren, Thorne, & Woolhander, 2005). It will take years for many of these households to recover. On the health front, consumers are currently facing greater responsibility for decision making with regard to both insurance coverage and treatment for health problems, and in these two arenas, the consequences of poor choices can be devastating.

These challenging times have created an increasing awareness that a lack of financial and health literacy can serve as a major barrier to the well-being of individuals, families, and communities. Usually in very separate venues, a number of agencies have attempted to improve financial and health literacy. One point of debate is how much of the burden of choice should fall to the consumers themselves, and how much is the responsibility of better government regulation and oversight by financial and health entities. That balance will continue to be an issue as legislation passes in these areas and as the regulations supporting that legislation obtain substance. For example, the DoddFrank Wall Street Reform and Consumer Protection Act includes a number of protections for consumers, such as a bureau of consumer protection, which ensures that consumers receive clear and accurate information relating to mortgages, credit cards, and other financial products, and protects consumers from hidden fees, abusive terms, and deceptive practices. The Credit CARD Act of 2009 is taking effect, and HHS is involved in formulating regulations related to the Affordable Care Act of 2010, some of which will affect insurance offerings and information for consumers about the benefits of various treatments.

Consumer education initiatives, related to both financial and health literacy, continue to be important. Resources, whether public or private, will be limited as the country comes out of a severe recession. Thus, efforts to expand consumer information and education in financial and health literacy will have to show their effectiveness and to find ways to provide services in the least costly manner. It is therefore critical to examine both what works to promote financial literacy and health literacy, and whether there are lessons to be learned across the two areas.

In some ways, the financial literacy and health literacy areas raise very similar concerns: Both address complex questions that require some sophistication; both are vitally important to the well-being of households; and both may result in incomplete and often contradictory information for consumers from a variety of sources. Health and financial literacy also overlap in terms of the costs of health care services and insurance. For example, consumers are often faced with deciding among insurance plans that require choice between greater and lesser risk of out-of-pocket spending, and planning for retirement increasingly requires individuals to recognize that they must plan for a substantial amount of spending on noncovered health-related services during retirement (both from acute and long-term-care spending). It is useful, therefore, to look at both areas for lessons that can help to determine where to direct scarce resources in the future.

Another key policy question arises regarding where to direct attention in order to enhance educational and informational initiatives. Should the focus be on individuals with low educational and financial resources, who are likely to be the least knowledgeable and most at risk? Alternatively, should greater emphasis be on empowering those who will be assertive in making decisions and hence be more likely to change? For example, in the area of health insurance choices, some have advocated that everyone can and should be educated about their options. Others believe that it is necessary to work with people at their current level of ability and interest. Some consumers will need help from family members or formal intermediaries to make decisions for them. Other consumers, who either already actively manage their health care or are likely to be able to manage their health care, may need limited assistance. Initiatives should emphasize empowering consumers on the basis of their needs and abilities. In the area of health insurance choices, some economists have argued that only a minority of consumers need to press for changes in order to influence the market to respond. For example, if enough people leave a high-cost health plan, some economists believe that the market will respond by creating lower cost plans. Not all people who leave do so by choice, and the consequences can be devastating: A study of uninsured children and children insured by Medicaid reported that a change in the program reducing the enrollment rate by 10% would increase the health care costs for each person by $2,121 for each child that was excluded from the program (Rimsza, Butler, & Johnson, 2007).

To begin understanding the lessons learned regarding financial literacy and health literacy, this report defines both terms and explains the reasons why financial literacy and health literacy are important to the well-being of low-income individuals.

Financial Literacy

Financial literacy refers to the ability to make informed decisions about the use and management of financial resources (U.S. General Accounting Office [GAO], 2006). This includes managing risk, using credit responsibly, saving for desired goals, and avoiding transactions that can undermine financial stability. Every household has to make decisions about its finances; yet overwhelmingly, U.S. households have been shown to make poor financial choices and show a lack of financial literacy and financial planning. Although low financial literacy spans all demographic groups, it is more prominent among older adults, women of all ages, minorities of all ages, individuals with little education, and those who have had little exposure to economics while in school (Lusardi & Mitchell, 2009). The Financial Industry Regulatory Authority (FINRA) National Financial Capability Study found that measured financial capability is lowest among adults with no postsecondary education, households with incomes of $25,000 per year or less, and Hispanics and African Americans (Applied Research & Consulting, 2009).

Financial literacy is associated with an individuals financial outcomes. Those who have relatively high levels of financial literacy tend to have better financial outcomes, and correspondingly, those who have lower levels of financial literacy tend to have worse financial outcomes. Hilgert, Hogarth, and Beverly (2003) find that households with low scores on a cash management index (indicating that they had poor financial behaviors) also had lower financial knowledge scores than individuals with higher scores on the cash management index. They found the same effect for a credit management index, a savings index, and an investment index. In a review of the literature, Lusardi (2008) suggests that financial literacy has an impact on financial outcomes by affecting individuals ability to make decisions. Lusardi cites studies that show those who are more financially literate are more likely to invest in the stock market; those who are unable to calculate interest rates borrow more and accumulate lower amounts of wealth; those who underestimate compound interest are likely to experience difficulties repaying debt; financial literacy declines with age, with a commensurate increase in the need to make financial decisions; and women make more mistakes, particularly in relation to risk diversification. Results from the FINRA National Financial Capability Study, a survey of 1,488 individuals, reported an association between greater financial literacy and having an emergency fund and fewer incidents of credit card behavior that will lead to high-interest payments and fees (Applied Research & Consulting, 2009). However, these data were based on self-reports and may have response bias because of social desirability.

Many consumers experience financial strain. In the same FINRA study described above, almost half the respondents reported having trouble keeping up with monthly expenses and bills (Applied Research & Consulting, 2009), and low-income respondents faced even more financial challenges. While 33% of all respondents experienced a decline in income in the year preceding the summer of 2009, 41% of those earning less than $25,000 a year experienced a decrease. Hispanic respondents were also disproportionately affected, with 43% experiencing a decline in income. Not surprisingly, individuals reporting a decline in their income were more likely to report trouble making ends meet than were those who did not report such a decrease (Applied Research & Consulting, 2009).

While most consumers interact regularly with financial institutions, a significant minority of the population, particularly those with low incomes, does not. Overall, 12% of the population appears to lack both a checking and a savings account, while 15% lack a checking account and 28% do not have a savings account. In low-income communities, 31% of individuals were unbanked (i.e. had no bank account at the time of the survey) (Applied Research & Consulting, 2009; Seidman, Hababou, & Kramer, 2005). For both the low-income group and the general population, those without bank accounts were more likely to have lower incomes, lower education levels, and to be minorities than those with bank accounts (Seidman, et al., 2005; Applied Research & Consulting, 2009). The reasons the unbanked respondents gave for why they did not have accounts included not having enough income, not being able to afford the high cost of minimum balances, and living in communities with little need for checks (Seidman, et al., 2005; Applied Research & Consulting, 2009). Other reasons included not wanting to share personal information and having an aversion towards banks (Applied Research & Consulting, 2009).

However, interacting with financial institutions is not necessarily an indicator of financial literacy. Many individuals who hold rather complex financial instruments (such as mortgages, credit cards, or individual retirement accounts [IRA]) end up with problems when they overextend themselves or default on their obligations. Similarly, many individuals overdraw their bank accounts or incur penalty fees while using debit or credit cards. Low financial literacy, particularly related to the financial products and services being used, may be a factor in such circumstances.

Research suggests that financial literacy is a significant predictor of retirement behavior (Gonyea, 2007). Although 70% of American workers are saving for retirement, only 42% have calculated how much they will need for retirement (Helman, Greenwald, Copeland, & VanDerhei, 2006). Fifty-one percent of individuals have retirement accounts from their employers, 72% of which are defined contribution plans[1]. Twenty-eight percent of those individuals who have employer plans also have additional retirement accounts (Applied Research & Consulting, 2009). Only 51% of those between 45 and 59 years of age have thought about what they need for retirement (Applied Research & Consulting, 2009).

Fifty-five percent of low-wage workers reported maintaining some retirement savings. Within this group, approximately 25% had set aside less than $2,500, and another 25% had set aside only $2,500 to $10,000 (Gonyea, 2007). Those with a greater understanding of investment and savings options were 30% more likely to have started to build up their retirement funds; also, workers who understood their employers defined contribution plans were twice as likely to report having retirement funds as those who did not.

Studies demonstrate that lower levels of financial literacy can lead to poorer outcomes related to preparation for retirement. Lusardi and Mitchell (2006) suggest that financial literacy is strongly associated with financial planning, and those with less financial knowledge are far less likely to plan for retirement or succeed in their planning. These authors suggest that one reason people may fail to plan for their retirements is that they have low financial literacy. The authors also find that those who were more financially literate made more sophisticated investment choices and therefore were likely to accrue more money in the long run. Results from the FINRA National Financial Capability Study also demonstrated that individuals with greater financial literacy were more likely to plan for their retirement and less willing to take financial risks than less financially literate people (Applied Research & Consulting, 2009).

Health Literacy

According to Healthy People 2010, health literacy is the degree to which individuals have the capacity to obtain, process, and understand basic health information and services needed to make appropriate health decisions (HHS, 2000, page 11-20). A number of landmark health literacy pieces published over the past decade have been crucial in describing the state of health literacy, shaping recent and ongoing research on the topic, and creating the primary strategies that research has shown to be successful in helping to improve health literacy rates. These include the Institute of Medicines (IOM) Health Literacy: A Prescription to End Confusion; Healthy People 2010s section on Health Literacy; and Kutner, Greenberg, Jin, and Paulsens 2006 report, The Health Literacy of America's Adults: Results from the 2003 National Assessment of Adult Literacy. Much of this work has focused on the ability of individuals to understand the consequences of various medical treatments. However, there is also interest in helping individuals recognize the consequences of choosing different health insurance plans for example, whether a plan covers certain conditions, and what are the varying financial risks associated with high-deductible plans, compared with plans with higher premiums but lower out-of-pocket costs.

Low levels of health literacy are a significant problem for U.S. adults. According to the 2003 National Assessment of Adult Literacy, only 12% of U.S. adults are at a proficient level[2] of health literacy (Kutner et al., 2006). Fifty-three percent of U.S. adults are at an intermediate level of health literacy; 22% have a basic level of health literacy; and 14% have less than basic health literacy (Kutner et al., 2006). Similarly, a systematic review by Sudore and Schillinger in 2009 found that approximately half the U.S. adult population has low health literacy. This is particularly alarming because low levels of health literacy are associated with poorer health outcomes for individuals (Berkman, DeWalt, Pignone, Sheridan, Lohr et al., 2004; Kutner et al., 2006; IOM, 2004; HHS, National Institutes of Health [NIH], 2006; HHS, Office of Disease Prevention and Health Promotion [ODPHP], n.d.; Sudore & Schillinger, 2009). Those with low health literacy are at greater risk of hospitalization (HHS, 2000) than those with high health literacy. In addition, individuals with low health literacy have annual health care costs more than four times as great as those of the general population, and 75% of individuals diagnosed with chronic conditions fall into the limited (general) literacy group (HHS, 2000). Low health literacy is also associated with obtaining fewer preventive procedures, such as flu shots; waiting longer to see a doctor (until individuals are sicker) compared to individuals with higher levels of health literacy; and having poorly control chronic conditions (HHS, ODPHP, n.d.).

Although individuals across all demographic groups may have low levels of health literacy, individuals with low educational levels and adults living below the poverty line are more likely to have low levels of health literacy (Kutner et al., 2006). An expert panel report from 2009 on improving the health literacy of older adults also found that a majority of U.S. adults do not have the health literacy skills to understand what they are reading when they see health materials (HHS, Centers for Disease Control and Prevention [CDC], 2009a). Improving the health literacy of persons with inadequate or insufficient skills is one of the health-promotion objectives in Healthy People 2010.

It will be necessary to overcome multiple barriers in order to improve health literacy; these include, but are not limited, to stigma around health issues, language and cultural barriers, differing cultural and educational backgrounds of the providers and the patients, and fear and emotional barriers (IOM, 2004). Certain strategies are helpful in surmounting these obstacles. Healthy People 2010 notes that it is important to target a specific audience in order to frame information for individual use and make that information easily understandable. Many individuals with low health literacy are also those who are not native English speakers or who have lower educational levels (IOM, 2004; Kutner et al., 2006). Clear communication is therefore an important strategy in reaching these individuals and improving their health literacy. This includes the concept of plain language a method of writing and speaking designed to improve the accessibility of information for individuals who have low health literacy skills (HHS, ODPHP, 2005b). Specific strategies for clear communication include organizing information to list key messages first, segmenting the information into easy to understand portions, using white space, and simplifying language and avoiding technical jargon (HHS, ODPHP, n.d.). The use of plain language has been steadily moving into health care to help individuals better understand their health care diagnoses (HHS, ODPHP, 2005b). There is still work to do; more than 300 studies show that the majority of health materials currently in existence exceed the reading level of the average U.S. adult (IOM, 2004). When addressing health issues, it is imperative to consider all aspects of communication, including the source, message, channel, and receiver (HHS, NIH, 2006). Clearly communicating health information also extends beyond the use of linguistic terms into the realm of culture. To increase health literacy, it is important for providers and those who deliver interventions to be able to understand the best way to access individuals in terms of their own cultures (HHS, ODPHP, n.d).

Another barrier relates to current interest in using evidence-based health care to inform decision making. A qualitative and quantitative study found that few consumers understood terms such as medical evidence or quality guidelines (Carman et al., 2010). Many participants believed that higher utilization of care and of the newest technologies meant higher quality care. A third of the participants perceived that treatments that are more expensive were superior to less costly ones. These attitudes and beliefs are likely to present a barrier to developing initiatives for evidence-based decision making.

Another communication issue is the use of the internet and other electronic forms to disseminate health information (HHS, 2000). Electronic information has the capability to increase the dissemination of health resources and information, and thereby promote health literacy. However, it also has the disadvantage of widening the gap between those with enough income to have access to the internet and those who do not (HHS, 2000). This issue relates conversely to the goal of making information easily accessible to target audiences, including older persons, for whom low health literacy is a serious concern. Limited health literacy in older adults may be a function of reduced cognitive functioning, but this may be compensated for through training (HHS, CDC, 2009a). The best ways to present information to older adults include keeping the information focused, repeating the message, allowing time for processing, using face-to-face communication, emphasizing short-term benefits, and following up with individuals (HHS, CDC, 2009a). It is particularly important to work with older patients in translating information they receive into actions they can perform (HHS, CDC, 2009a). Recommendations that came out of CDCs Expert Panel on Improving Health Literacy for Older Adults (2009a) included:

- Using plain language

- Trying to simplify or bundle messages so that patients do not get overwhelmed

- Using multiple channels to disseminate information

- Working on finding ways to bridge the technological gap for older adults

- Improving websites to make them more user friendly

- Examining data for populations with special needs

While literature on how health literacy interventions might improve health outcomes is relatively scarce, studies that exist show promising results in improving health knowledge and/or outcomes (Berkman et al., 2004). Interventions designed to mitigate the effects of lower health literacy often improve outcomes more for those with lower health literacy than those with higher health literacy (HHS, NIH, 2006). Interventions for health literacy can be applied in a number of contexts, such as schools, workplaces, health care settings, and community settings (HHS, 2000). There are also multiple levels of interaction to consider when attempting to intervene in health literacy: the clinicianpatient level, which can include clear communication, teach-to-goal methods, and reinforcement; the health care organizationpatient level, in which clear health education materials, visual aids, and medication labeling are important; and the communitypatient level, in which lay health educators, adult education referrals, and the mass media are important (Sudore & Schillinger, 2009). Effective health programs also must target a communitys needs and take into account diverse populations (HHS, 2000).

Improving health literacy in the future will require approaching the issue from two different sides: the demand side, or what the health care system needs patients to understand and perform to improve the patients health, and the skill side, or what patients need to do to respond to the health care system (HHS, NIH, 2006). It will be necessary to overcome barriers, including the stigma that individuals with low health literacy can feel, the language and cultural barriers hindering effective communication, the complexity of health care systems preventing dialogue between providers and patients, the demands for literacy skills mismatched with individuals actual literacy skills, and fear and emotional barriers (IOM, 2004). Older adults may also feel embarrassed by their lack of knowledge about technology, although trainings on how to navigate web-sites have been successful (HHS, CDC, 2009a).

Various sources have made a number of recommendations for ongoing improvements in health literacy (HHS, ODPHP, 2005a; IOM, 2004; Rudd, 2004; HHS, ODPHP, n.d.). In general terms, these recommendations include (1) Implementing programs in schools and other adult education programs already in existence; (2) Having health care systems look into the most effective approaches to increasing health literacy; and (3)Exploring ways to better communicate health information.

Methodology

We generated the study findings synthesized in this report through a review of the research and evaluation literature and through interviews with federal officials, most of who worked for HHS agencies, to identify and describe financial and health literacy initiatives and the lessons learned. We conducted nine interviews with representatives of private organizations who directed exemplary financial and health literacy initiatives.

Scope

Our focus in this study was on financial and health literacy initiatives aimed at low-income individuals.

We define an initiative as any effort or program that seeks to educate individuals about financial or health issues and, more importantly, to engage individuals to improve their skills and behaviors relating to finances and health. These skills and behaviors may include, but are not limited to, proactive behaviors to prevent problems from occurring (e.g., budgeting to avoid overspending and monitoring blood glucose levels for diabetics to prevent high levels of glucose), general preventive behaviors that may or may not have a direct impact (e.g., reviewing ones credit scores and getting mammography screenings), managing problems (e.g., reducing debt and controlling asthma flare-ups), decision making (e.g., choosing mortgage options and health care treatments), and planning for the future (e.g., saving for expenses in retirement, including health care).

Finally, we focus on initiatives that target, or that would be valuable for, low-income individuals. Thus, we have included studies and initiatives that focus on specific income levels, that describe the setting as an underserved area, and that are likely to be valuable to all consumers, including those with low incomes. We have excluded initiatives that generally target persons with higher incomes (e.g., planning that involves paying financial planners).

Literature Review

The literature review consisted of evaluating studies from peer-reviewed and other literature. Below we describe the main methods of gathering and evaluating literature.

Peer-Reviewed Literature

The study team scanned the social science and medical peer-reviewed literature, including both qualitative and quantitative descriptive studies, using Academic Search Premier, Business Source Corporate, the Cumulative Index to Nursing and Allied Health Literature (CINAHL), Professional Development Collection, PsycInfo, PubMed, SocSci Index, and the Web of Science. We searched these databases, using keyword search terms and the Medical Subject Headings (MeSH) (in PubMed) for each category of interest and limiting our searches to resources developed domestically. Detailed information about search terms is presented in Appendix A.

We reviewed 166 abstracts related to financial literacy and 360 related to health literacy, for a total of 526 abstracts. On the basis of our review of the abstracts, we retrieved 178 full text articles. While we focused primarily on recent literature, we included articles or books from before 2005 if they were considered seminal in their field. We did not include research related to educational work for school grades from kindergarten through college, mostly because our goal was to focus on assessing programs that would be helpful to low-income adults.

| High Priority | Goal

Topics: financial literacy, health literacy, and consumer education Target audience: low-income consumers, including, in some cases, information that would be of value to these consumers Types of Data

Timeframe

|

|---|---|

| Excluded | Excluded from interviews and the literature review

Literature review-specific

|

Gray Literature

We defined gray literature as any non-peer-reviewed literature that met the studys inclusion criteria. This included presentations, articles, white papers, trade publications, issue briefs, and books. We did not include articles from magazines or newspapers.

To scan the gray literature, we examined the HHS web-site and the web-sites suggested by the project team. We also conducted a more targeted web search based on some of the findings from the peer-reviewed literature (see Appendix A for the list of web-sites we reviewed).

Data Abstraction and Analysis

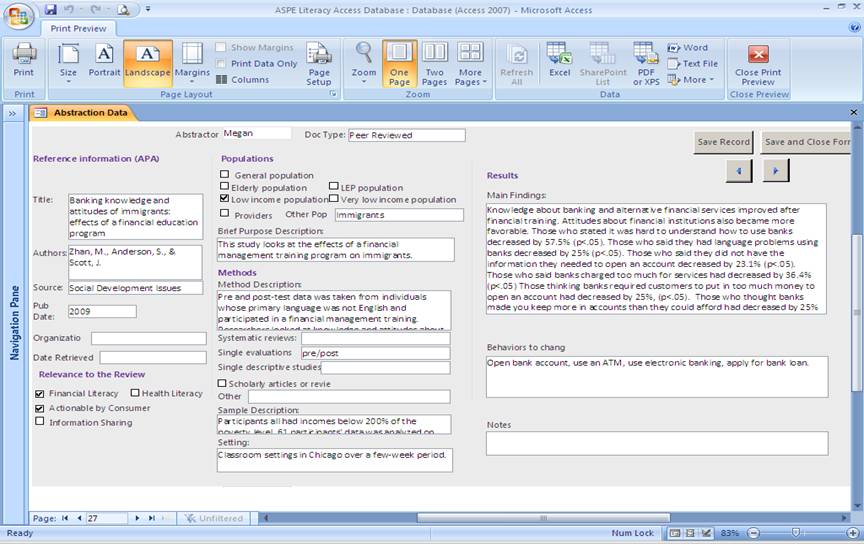

We entered all documents into a Microsoft Access database, and abstracted key features and identified key themes (see Appendix A for the data abstraction protocol). We developed an abstraction form in Microsoft Access for the peer-reviewed and gray literature (screen shots of the Access forms appear in Appendix A). The main elements of the abstraction form were document information, purpose, methods, and main findings. We also noted the type of documents that we found in the literature (e.g., systematic reviews and single descriptive studies).

Once we had abstracted the information, we synthesized it by main themes relating to financial literacy, health literacy, and the way in which each of these concepts informs the other.

Limitations to the Literature Review Methodology

The one major limitation in our study was the general scarcity of gray literature focusing on financial literacy among low-income populations. There is a fair amount of literature on how to become more financially literate; however, these documents did not specify a target population and did not evaluate the effectiveness of the tool or initiative used. Literature from behavioral economics is not included as it tends to focus on higher income populations.

Key Informant Interviews

To understand existing, completed, and planned federal initiatives associated with financial and health literacy, we conducted interviews with officials from HHS and additional federal agencies. We also interviewed individuals from eight external organizations focused on financial and/or health literacy to get a broader view of these fields. See Table 2 for the names of the agencies and organizations from which we drew our interviewees.

| HHS Agencies |

|

|---|---|

| Other Federal Agencies |

|

| Private Organizations |

|

To identify potential initiatives of interest for the study, we developed priorities for inclusion based on the projects focus on assisting low-income persons with financial and health decision making (see Table 2). Based on input from the chair of the HHS Health Literacy Work Group (HLWG) and a web scan of federal agencies, we developed a database of initiatives, including the agency or organization name, a description of the initiative, its focus on financial or health literacy (or both), target audiences, whether the initiative sought to change behaviors and/or improve skills, and links to information. The initial list contained 112 initiatives across 13 HHS agencies, six additional federal agencies external to HHS, and 12 private organizations. On the basis of input from the Task Order Officers and comparison of the list to initiative priorities, we narrowed the list to 59 initiatives that met the inclusion criteria.

We conducted a total of 35 interviews with 46 individuals during March through August 2010. On the basis of these interviews, we gathered information on a total of 38 initiatives from 13 federal agencies and eight private organizations. For two interviews, we grouped multiple initiatives if they lacked specific titles or if there were multiple similar initiatives at a given agency. For example, we grouped multiple consumer education initiatives and campaigns at AHRQ, since the participants described them in general terms. We also grouped CMSs Compare web-sites Nursing Home Compare, Hospital Compare, and Medicare Prescription Drug Plan Finder and considered them as a single initiative because of the similarity among their goals and methods. Our response rate for our interview requests was 84%.

For the interviews, we used a semi-structured protocol that covered the following topics: participants roles and responsibilities, background and goals of the initiative, target populations, behaviors that the initiative promoted, coordination with other government divisions, activities to determine effectiveness and success, lessons learned, unanticipated outcomes, and completed and ongoing research (see Appendix B for the protocol). We did not ask the same questions of more than nine nonfederal respondents, in compliance with Paperwork Reduction Act rules.

Each interview was audio recorded. A note taker was present and prepared a written transcript of the discussion. Information from the interview was then entered into a spreadsheet, organized by the specific topic areas in the protocol, and reviewed to identify themes, trends, and relationships among observations.

Limitations to the Interview Methodology

There were a few limitations to the interview methodology. With more time and resources, more government agencies could have been included. Notable exclusions from the list include the Social Security Administration, the National Institutes for Health, and the Veterans Administration. In addition, although we sought to obtain data on evaluations, most interview participants were not able to discuss specific evaluation data. However, in some cases, participants were able to provide documents or references to specific results and data.

Findings from the Literature

The literature review sought to identify strategies and interventions for improving financial and/or health literacy of consumers, particularly those with low incomes. In this section, we provide overviews to the research in financial and health literacy and a description of lessons learned based on target audiences, dissemination strategies, and sources of information.

Financial Literacy Research Overview

Financial literacy has been studied in three main settings: (1) as part of individual development account (IDA) programs; (2) financial education programs aimed at low-income audiences or underserved areas; and (3) secondary data analyses. IDAs are short-term, limited use, matched savings accounts that are typically bundled with services, such as financial education and peer mentoring, into a program intended to help low-income individuals purchase or develop assets, such as a home, a small business, or postsecondary training or education. While there are a number of studies examining IDAs, there are limitations: Self-selection into these programs which increases the likelihood of having characteristics that differentiate participants from the general public; inconsistency between financial education across IDA programs thus decreasing the comparability; the value of the financial education component as a secondary to the matched program thus limiting generalizability to other financial education programs; and none of the IDA research studies have a control group to evaluate the differences between those who receive financial education and those who do not.

Financial education has been evaluated in financial management courses directed at low-income audiences in community settings. Four of these studies were evaluations of specific training programs, All My Money (developed by USDA) (two studies) and the Financial Links for Low-Income Persons (two studies). Two evaluations examined credit counseling programs and one examined a mandatory financial education program in a low-income housing program. All My Money sought to provide a comprehensive financial education program to educate persons about spending choices, budgeting, planning, understanding credit, managing a checking account, and planning expenditures. Financial Links for Low-Income Persons sought to educate individuals about opening banking accounts, banking practices, credit use, savings, and in one program, potential public- and work- related benefits (Zhan, Anderson, & Scott 2009; Zhan, Anderson, & Scott 2006). Collins (2010) examined a similar program, only participants were required to take the financial education courses. None of these studies included a control group and all but one (Collins, 2010) allowed participants to select into the counseling, thus it is unclear whether self-selection or the program was the key factor in improving financial literacy.

The two credit counseling evaluations had different foci: Elliehausen, Lundquist, and Staten (2007) examined counseling relating to the financial goals, financial strengths and weaknesses, and examining the familys budget; Hatarska and Gonzalez-Vega (2006) examined counseling programs to improve spending, improving the use of credit, and consolidating debt. Both of these studies had limitations including self-selection; a lack of control-group for the Hatarska and Gonzalez-Vega study; and, although Elliehausen et al. included a control group, the participants were not randomly selected into either group. Elliehausen et al. (2007) discovered that counseling resulted in virtually no improvements in credit scores. It was the self-selection, not the counseling, which had produced financial improvements.

Finally, the literature review also examined research from data sets (Courchane, Gailey & Zorn, 2007). Using datasets from a 2000 Freddie Mac survey and 1.2 million mortgage loans, the authors examine the accuracy self-assessment of credit and the association between self-assessment of credit and the ability to obtain a mortgage loan. The limitation to this study is that the data do not combine consumers subjective assessments of their financial records with observed financial market outcomes in a later period. The definitive analysis of whether or not accurate self-assessment of credit improves financial outcomes likely awaits such data.

Health Literacy Research Overview

The research topics included in health literacy review covers, in order of prevalence, preventive cancer screenings, chronic disease, healthy living (including exercise, diet, and risk reduction), health management, and accessing health care services. The preventive cancer screenings included breast cancer and colorectal cancer. Most of preventive literature examined the comparison of trained providers, either a patient navigator (typically a nurse or social worker) or a clinician and sort of written material, such as a letter or a brochure. The other preventive literature focused on targeting specific ethnic groups (African American women and Hmong men and women) and comparing different modes and level of tailoring, for example, comparing video, print, interactive computer, and group learning sessions. These interventions had several limitations, the most common being small sample-sizes which decreased the precision of the study. Similar to financial literacy, self-selection into some of the studies posed a bias: self-selected participants may be more interested in self-care and health management and could be different from the general population. Other limitations included patient attrition from the study; differences between treatment and control group potentially confounding the findings; and a lack of control groups.

Health literacy has also been examined in the context of improving chronic conditions such as diabetes, heart failure, asthma, and hypertension. The modes of delivery for these studies were one-on-one education or counseling and group sessions. Where there was a control group, the control group typically received a pamphlet. These studies also had their own limitations, again the most common being small sample size. Lack of a random controlled design also limited findings for a few studies. Not all studies examined clinical outcomes which would have been valuable to ascertain the achievement of the initiative. Finally, two studies relied on self-selection into the study and self-report of behavior, increasing the likelihood of positive results.

Five health literacy studies examined health management, including patient-specific health improvement/risk reduction activities (e.g., fall prevention and medication management), diets, and general health improvement/risk reduction activities (e.g., smoking cessation, diet improvement, exercise), and drug allergy awareness. All but one of these studies, the drug allergy awareness study, examined a health educator and individual interaction, including counseling, phone support, and classes. The drug allergy awareness used a form only. The most common limitations to these studies included conducting the studies at a single health site decreasing generalizability; a lack of control group for comparison; self-selection into the study; and self-reporting behavior. Other limitations include participant attrition and poor recall for self-reported behaviors.

Similar to the financial literacy research, most of the studies focused on interventions involved interactions between a health educator and a patient. Of the health educator-patient interaction studies, less than half involved a clinical provider such as a physician, nurse, or social worker. The others used a trained educator, but it was unclear whether these educators had degrees related to the activity; in one case, it appeared they were trained graduate students. Several of the studies also examined the use of materials, whether as a usual source of information as part of the control group, or as a key source of providing or collecting information, such as collecting data on allergies. In only one case were alternate methods examined, such as the use of a video, interactive computer, and a pamphlet.

Unlike the financial literacy, there were no articles studying the same intervention, although in at least one case, such as Montz & Seshamanis article on WISEWOMAN, there are several publications on the program, but all were published prior to 2005.

Appendix C presents details of the studies and results in financial literacy and health literacy.

Lessons Learned Relating to the Target Audiences

Better long-term financial and health outcomes are associated with highly targeted and proactive counseling. Evaluations of financial and health literacy initiatives have shown that developing initiatives aimed at a specific audience or better yet, an individual are superior to initiatives aimed at a more general audience. In a literature review conducted by the Federal Reserve Bank of Cleveland, the authors found that highly targeted and proactive programs are more likely than more general ones to be effective in changing peoples financial behavior (Hathaway & Khatiwada, 2008). The authors also indicate the need for more rigorous study of financial education. Programs should target a specific audience, such as homeowners, and a specific area of financial activity, such as choosing among mortgages or mortgage modifications. In addition, the authors suggest that training should occur just before the related financial event, such as applying for a mortgage. This finding may explain other findings suggesting that financial education and counseling provide only modest financial improvements. Perhaps the reason for the modest financial improvements is that the financial education is general and not specific to a particular event, issue, or concern. The Federal Reserve Bank authors found that, in studies on counseling on homeownership and on credit card use, preemptive counseling, before the purchase of a home or a bad credit event, could improve outcomes by decreasing default rates or future loan delinquency, or by improving borrower skills and planning. In contrast, reactive counseling, such as postpurchase or crisis counseling, was not as effective as preemptive counseling at limiting bad credit outcomes or future problem behaviors. Similarly, both research studies by Zhan, Anderson, and Scott (2006 and 2009) suggest that focused information for small, targeted populations is likely to improve financial literacy. In the 2006 study, Zhan et al. reported that low-income participants were not aware of public benefits such as transitional Medicaid, subsidized child care, and the Earned Income Tax Credit (EITC), suggest the need for better dissemination of these important potential benefits when conducting financial education. Zhan et al.s 2009 study found that providing financial education to immigrants who were unfamiliar with banking and/or were skeptical of banks increased understanding about banks; for example, there was a 58% decrease in the number of people who found understanding how to use a bank hard.

Health literacy has a history of targeting small subpopulations and even tailoring information to individuals. Targeting is developing materials for a specific segment of the population, smaller than the general public, but still fairly broad, like minority women or older adults with heart disease. With tailoring, the aim is to develop information or an intervention for an individual on the basis of an assessment (HHS, 2000; Kreuter & Skinner, 2000).

To develop targeted or tailored and culturally appropriate materials that engage the desired audience and to determine the best method for disseminating the information, developers may use a variety of methods, such as focus groups, interviews, and observations. Many tailored initiatives in health literacy focus on a specific issue, such as asthma control, diabetes control, or increasing colorectal screening rates. An example of this is the Chicago Initiative to Raise Asthma Health Equity, developed by Martin et al. (2009), which used four educational activities and six home visits responsive to each participants own particular needs, to improve that individuals asthma self-management. Champion et al. (2006) examined different interventions to increase mammography rates. Examining pamphlets, videos, and an interactive computer-assisted instruction program that was tailored to the individuals own beliefs and readiness for mammography, the authors found that 52% of the interactive computer group either worked toward getting a mammogram or obtained a mammogram, compared with those in the pamphlet or video group. These data indicate that tailored, interactive approaches are more effective in increasing mammography rates among African American women. Similarly, Kagawa-Singer, Tanjasiri, Valdez, Yu, and Foo (2009) found that using a culturally customized intervention with Hmong women in California improved mammography rates by almost 30%. In a randomized study of ethnically and linguistically diverse low-income patients, Percac-Lima et al. (2008) found that a culturally tailored navigator program designed to overcome barriers to colorectal cancer screening could significantly improve patient colonoscopy rates. A trained navigator or community health worker met with patients and provided individually tailored interventions, including patient education, procedure scheduling, translation, explanation of preparation, and help with transportation and insurance coverage, resulting in twice the number of colonoscopy completions and colorectal cancer screenings. Smith and Wolleson (2010) also reported that individualized and tailored counseling to low-income pregnant women resulted in increases in health literacy scores and functional self-care literacy[3] scores. In a study of low-income patients receiving diabetes education while waiting in a doctors office, Drago (2009) reported that 92% of patients demonstrated improvement in health literacy skills due to short (15-minute to one-hour) training sessions. Montz and Seshamani (n.d.) examined data from 10,000 low-income and uninsured or underinsured women who participated in a tailored counseling program to improve their diet and exercise, reduce or stop smoking, and reduce other risks identified by study participants. The authors reported a 5% reduction in 10-year estimated chronic heart disease risk, an 8% reduction in 5-year estimated cardiovascular disease risk, and a 7% decline in smoking since the program began. It is important to consider both the target audience and the timing of delivering an educational message in order to have the greatest impact. If possible, tailoring messages to individuals, to address their specific needs at the time of need, could promote even greater behavior change.

Use of theoretical models on behavioral change have proved useful for developing initiatives. Health literacy has developed theoretical models to help develop interventions. These theoretical models, while untested by themselves, have proved valuable in developing a plan to address a health concern. Champion et al.s intervention to improve mammography rates was informed by the Prochaska and DiClementes (1984) Stages of Change Theory. This theory reasons that people tend to progress through different stages on their way to successful change. There are five stages: (a) precontemplation (not yet seeing that there is a problem behavior that needs to be changed), (b) contemplation (realizing a problem exists but not being ready to make a change), (c) preparation, (d) action (changing behavior), and (e) maintenance. The authors found that there was significantly more forward movement in mammography stage of readiness among participants in the interactive computer group, compared with those in the pamphlet or video group. These data indicate that tailored, interactive approaches are more effective in moving African American women forward in their mammogram stage of readiness. This finding could be modified to apply to financial literacy initiatives.

Similar to the Stages of Change Theory, some of the research in financial literacy has found that educating individuals at the time of their need is more effective than educating individuals after a negative financial event has occurred (Hathaway & Khatiwada, 2008). The objective of the study described in the literature review was to provide the information that individuals needed to know at the time when they needed it. For financial literacy, topics could include retirement planning, home ownership, obtaining a mortgage, or managing debt. The purpose of focusing the topic is to tailor the initiative to an individual at the time that would be most appropriate.

Another commonly used behavioral theory is the Health Belief Model. This theory examines (a) perceived susceptibility of a health condition, (b) perceived severity of a health condition, (c) perceived benefits of changing ones behaviors, (d) cues to action or strategies to facilitate embracing new behaviors, and (e) self-efficacy (Glanz, Rimer, & Lewis, 2002). For example, initiatives could increase perceived susceptibility to and severity of a poor financial outcome, the perceived benefits of changing ones behaviors, strategies to facilitate embracing new behaviors, and self-efficacy. Using the Health Belief Model, focus groups and interviews could examine perceived susceptibility to a specific negative financial outcome (e.g., loss of money from a bank), perceived severity of the negative financial outcome, perceived benefits of changing ones behaviors, and strategies to facilitate positive financial behaviors. This information could be used, for example, to develop an initiative that mitigates negative beliefs about banks, increases positive beliefs about banks, such as financial safety and ease of paying bills, and increases self-efficacy to perform positive financial behaviors.

The Theory of Planned Behavior has been used in both health and financial literacy (Ajzen, I, 1985). In the Theory of Planned Behavior, action is guided by behavioral beliefs (e.g., beliefs about the consequences of a behavior), normative beliefs (expectations about others), and control beliefs (e.g., beliefs about what may facilitate or impede the performance of a behavior). Collins 2010 study used the Theory of Planned Behavior to develop and examine a five-session financial education initiative. Based on the theory, it was expected that, compared with the control group, the housing voucher clients who completed a mandatory financial education program would improve in the following areas: (a) self-assessed knowledge of financial issues; (b) attitudes about saving and budgeting; and (c) objective measures of financial behavior, including credit reports and bank statements. Collins found that the knowledge of current interest rates and what is in a credit report increased by 29% and knowledge of managing money by 44% at follow-up. In a similar manner, at follow-up, the program led to a 25% increase in self-reported spending control, a 44% increase in timely bill payment, and a 35% increase in following a budget.

Self-perceptions are a poor reflection of health and financial literacy. This finding can be particularly important, since program evaluations often rely on self-assessments rather than direct observation of behaviors or records of behaviors. Among consumers who speak Spanish as their primary language, a significant number of patients who report English proficiency in fact have an inadequate level of English health literacy, as measured by the Rapid Estimate of Adult Literacy in Medicine (REALM) and the Short Test of Functional Health Literacy in Adults (STOFHLA). This fact suggests a need for a more liberal use of interpreters (Zun, Sadoun, & Downey, 2007). In addition, in Sarkar, Fisher, and Schillengers (2006) study of primary care patients, the authors found that health literacy levels were not a predictor of better self-management of diabetes[4].

Findings in financial literacy are similar. Courchane, Gailey, and Zorn (2007) analyzed the relationship between individuals (of all income levels) real credit records from 1.2 million mortgage loans and their self-assessments of their credit from a survey. These authors found that consumers perceptions of their credit quality did not always reflect their actual credit scores, although financial knowledge and literacy increased the accuracy of self-assessment. Those with low to moderate levels of knowledge about their personal credit scores often overestimated their level. Those with incomes of less than $35,000 also overestimated their credit scores. These findings suggest that individuals who inaccurately assess their own credit scores are likely to be denied credit, pay higher costs on mortgages, and/or have other negative financial outcomes.

Past behaviors are indicators of future behaviors. Within the financial literacy research, many personal characteristics indicative of stronger previous financial management, such as homeownership or having greater financial assets, are associated with better future financial decision making. In a study of a small IDA program, Grinstein-Weiss, Curley, and Charles (2007) found that home ownership upon entry into the IDA program was an important predictor of savings. In a similar manner, graduation from an IDA program emerged as a significant predictor of household savings, resulting in a $341 increase in household savings, compared with the savings of those who did not complete the IDA program (Loibl et al., 2008). The authors found that future orientation toward financial planning emerged as a main effect in predicting household savings. Loibl et al. also reported that participants with greater household financial assets were more likely to be employed full time or to own an investment account, and were more aware of the future consequences of their financial actions. These findings suggest that previous successes in financial management create financial dispositions and behaviors that provide long-term benefits. Over several years, the strict program structure and intensive financial training may help participants build the skills they need to achieve savings goals even after leaving the IDA program. As greater household financial assets are associated with considering future consequences, it is possible that individuals with better previous financial behaviors are more likely than program graduates to have better future behaviors (Loibl et al., 2008).

Higher self-efficacy is associated with better self-care and disease management. Self-efficacy is the belief in one's own ability to succeed at performing specific tasks. Individuals with high self-efficacy are likely to be more proactive about a situation because they believe that their actions matter, whereas people with low self-efficacy may have a sense of hopelessness or fatalism about a situation, feeling that nothing that they do will make a difference. Self-efficacy was originally defined by Bandura (1977) and is used to understand an individuals ability to perform activities, as well as to take initiative. Three recent studies examined the association between self-efficacy and managing chronic health conditions.

Sarkar, Fisher, & Schillinger (2006) conducted a study examining factors associated with better self-care and disease management of low-income patients at two primary care clinics. Across race/ethnicity and health literacy levels, people reporting higher levels of self-efficacy also tended to show a greater likelihood of following an optimal diet and an exercise regimen. Each 10-point increase in reported self-efficacy (out of a 100 point scale) was associated with a 16% higher likelihood of following an optimal diet and a 10% higher likelihood of following an exercise regimen. There were also significant relationships found between self-efficacy and self-monitoring of blood glucose and between self-efficacy and foot care.

In a smaller study of adults in Chicago who sought to improve asthma self-efficacy, the researchers randomized participants into a control group that received only education pamphlets and a treatment group that participated in four group sessions lead by a community social worker and received six home visits by community health workers (Martin et al., 2009). The 42 participants were predominantly African American and of low-income status, and had poorly controlled, persistent asthma. After the counseling, the treatment group reported significantly higher asthma self-efficacy at 3 months. At 6 months, the intervention group had improved asthma quality of life, compared with controls. Another study of 275 hospital patients found that the most significant predictor of low medication adherence was low self-efficacy (Gatti, Jacobson, Gazmararian, Schmotzer, & Kripalani, 2009). In other words, patients who did not believe that they could manage their medications were not likely to do so. Finally, in one study on information seeking by low-income pregnant women, Shieh, Mays, McDaniel, and Yu (2009) found that a significant barrier for women with low health literacy was low self-efficacy.

Although the direction of causality is unclear, whether certain behaviors cause self-efficacy or self-efficacy causes certain behaviors, there is evidence that self-efficacy is a predictor of self-management. This finding suggests that activities and information to increase self-efficacy could play a critical role in health and financial literacy. Thus, developing an initiative that attempted to increase an individuals self-efficacy as well as changing a behavior may increase the likelihood of success for an initiative.

The benefit from focusing on consumers with the poorest financial literacy could apply to health literacy initiatives. Low-income consumers have the most to gain from financial education if the education targets low-income-specific issues. Two recent studies also found that counseling provided the greatest benefit to those borrowers with the least demonstrated ability to handle credit at the time of counseling (Chang & Lyons, 2008; Elliehausen et al., 2007). In a similar manner, Hathaway and Khatiwadas (2008) literature review found two studies suggesting that education for low-income consumers should target financial issues particularly affecting low-income households, such as public and work-related benefits and predatory lending, although the authors did not provide specific data from the studies. Furthermore, the authors argue that, because of the variety of public benefits, financial educators must be knowledgeable about what is available in their area. Translating this finding into the health field, targeting persons with multiple chronic conditions or with significant disabling conditions may lead to better outcomes or better health stabilization than more general health literacy initiatives would. Targeting those with the greatest need is not a widespread practice in the health literacy field, although there are two such examples: The patient-centered medical home and the Chronic Care Model. A patient-centered medical home is an approach to providing comprehensive primary care that is patient centered; care is coordinated and integrated, and has a whole-person orientation. Patient-centered medical homes typically concentrate on persons with chronic conditions, and have been effective in preventing emergency room visits, reducing costs, and improving quality of care (Grumbach, Bodenheimer, & Grundy, 2009). The Chronic Care Model encourages more education and interaction between the provider and the patient (Wagner, 1999). First developed by Wagner in 1999, this model seeks to improve clinician interactions with patients, thereby encouraging patients to be informed, engaged, and active. Clinicians plan, educate, and provide decision making support. The model starts with changing the behavior of the health care team to tailor information to patients and train patients to take care of themselves and manage their own condition or conditions. In turn, patients have the necessary information and skills to make decisions and have confidence in making health care decisions later. In a study using the Chronic Care Model in the community, the researchers reported decreases in blood glucose levels, decreases in non-HDL cholesterol[5], and improvements in diabetes knowledge (Piatt, et al. 2006). Focusing on individuals with the greatest need could benefit health outcomes and could be a more effective use of resources under certain circumstances.

Lessons Learned Relating to the Channels of Information

Activities should be simple, enjoyable, and normalize positive behaviors. Audience-centered communication initiatives use the concept of fun, easy, and popular to develop initiatives (Smith, 2007). Fun refers to whether the target audience perceives a positive benefit to the behavior, as well as a lack of negative emotions, such as shame, frustration, and fear. Easy refers to whether the intended audience has the knowledge and skills to perform the behavior successfully. Popular refers to the need for participants to believe that the new behavior is normal and common among other individuals. Health literacy initiatives incorporate this concept into campaigns and information, developing activities that are easy to engage in and understand and acknowledging challenges that occur. One example of this type of initiative is the People Reducing Risk and Improving Strength through Exercise, Diet and Drug Adherence (PRAISEDD) intervention to improve diet, exercise, and medication adherence in a senior housing community (Resnick, Shaughnessy, Galik, Scheve, Fitten et al., 2009). The initiative held one-hour sessions over 12 weeks, and included exercise, motivation, and ongoing education, and then reported participants diet, exercise, and medication adherence in logs. The program was successful in getting participants to engage in education and exercise three times per week, and participants demonstrated improved outcomes in blood pressure.

One example of this approach to in financial literacy is making it easier to save for retirement through savings bonds. Starting next year, Americans have the option of using their refunds to purchase U.S. Savings Bonds by simply checking a box on their tax returns, even if the taxpayers do not have bank accounts (Retirement security for American families, n.d.). Another example of could be developing an initiative around obtaining a checking and savings account for new immigrants. The initiative could focus on positive benefits, such as having a central place for your money, checks to use for payments, and (potentially) automatic deposits from the employer, as well as potential gains in savings accounts. In addition, the initiative could reduce negative emotions, such as fear of banks and fear of loss of money, by describing what banking is, the ease of getting a bank account, the types of available bank accounts, and the rules for keeping money safe. To popularize the use of checking and savings accounts, videos of other immigrants similar to the target population could show the video participants indicating the benefits of using the banks. To emphasize the ease of using banks, the video could describe a typical banking process, acknowledging the discomfort the person might have about setting up an account.

Education assists in managing present difficulties and to prevent future problems. Both chronic care education and financial education consist of managing long-term issues or conditions, preventing potential problems, managing problems should they arise, and conducting regular checkups or check-ins about specific health or financial issues. In both cases, lack of knowledge and ability to maintain consistent positive behavior over time leads to poor outcomes, such as poor quality of life exemplified by emergency room visits, days spent at home, problems with credit, and lack of money. Where the chronic care education and the financial education initiatives differ are the outcomes when individuals manage their conditions or finances well. In chronic care, the positive outcome of managing their condition is the lack of deterioration and lack of problems, such as emergency room visits, surgery, or loss of eyesight. In financial education initiatives, the positive outcome is not only a lack of financial deterioration but, potentially, financial progress, such as increasing savings, owning a home, or improving credit.

Two studies examining chronic care self-management found that participants in the treatment group were more likely to do a better job of managing their health care, although the results on quality of life were mixed. In one study on asthma self-management in which the treatment group received four group sessions and six home visits by community health workers, compared with the control groups receipt of educational pamphlets, the treatment group was more likely to have asthma action plans at 3 months, and at 6 months. The treatment group had improved quality of life and improved asthma coping skills, compared with the control group (Martin, et al., 2009). Hostetter (2008) found that patients with coronary failure trained by health care providers about self-management were more likely than those in the control group to check their weight daily and watch for signs and symptoms that indicated worsening of heart failure. However, there were no significant differences in quality of life between the two groups. Finally, in a study implemented in underserved communities, patients in the intervention group, who received tailored and planned education from their clinicians, had significantly lowered blood sugar levels, improvements in non-high-density lipoprotein also known as non-HDL cholesterol levels, and higher frequency of self-monitoring, compared with the control group (Piatt et al., 2006).

Similar results were found in financial literacy evaluations that discussed skill building, including planning (Lyons, Chang, & Scherpf, 2006; Grinstein-Weiss et al., 2007). For example, Lyons, Chang, and Scherpf studied individuals who took part in an eight-session financial education program to train individuals on making spending choices, managing personal finances (e.g., bank accounts), managing credit problems, and planning expenditures. After the counseling sessions, 85% of participants reported improving financial management.

The concept of chronic care is so significant in health education that a field of study dedicated to the Chronic Care Model has emerged. First developed by Wagner in 1999, this model seeks to improve clinician interactions with patients, thereby encouraging patients to be informed, engaged, and active. Clinicians plan, educate, and provide decision making support. The model starts with changing the behavior of the health care team to tailor information for patients and train patients to take care and manage their own condition or conditions. In turn, patients have the necessary information and skills to make decisions and have confidence in making health care decisions later. In a study using the Chronic Care Model in the community, the researchers reported decreases in blood glucose levels, decreases in non-HDL cholesterol, and improvements in diabetes knowledge (Piatt, et al., 2006). One challenge to applying this model to the financial education field is that most individuals do not regularly interact with a trusted and credible financial educator, as people may with a health care provider.

Low health literacy and education levels and barriers to information predict the degree of information seeking. One way that individuals can increase their health literacy is through accessing information pertinent to their health condition, a critical step toward health

decision making and health management. Shieh, McDaniel, and Ke (2009) examined the information-seeking behaviors of pregnant women and found that information needs and information barriers predict womens degree of information seeking. Barriers to information were categorized as psychological (e.g., avoiding health decision making), demographic (e.g., minority status or low health literacy), interpersonal (e.g., lack of a support network), environmental (e.g., lack of libraries or internet services), and information source barriers (e.g., a providers disregard for prenatal health education). Even when controlling for first pregnancy, low-income level, and additional health issues, barriers to information were the most significant predictor of womens information-seeking behavior, not information needs. In a similar study conducted by Shieh, Mays, McDaniel, and Yu (2009), findings suggest that varying health literacy levels may contribute indirectly to health outcomes by affecting other information-seeking behaviors. The authors reported that only 14% of pregnant women with low levels of health literacy frequently used the internet as an information source, compared with 47% of those with high levels of health literacy. As the internet can be a significant source of information, this presents a huge gap for low-income pregnant women in terms of their information-seeking capabilities. At the same time, it is unclear whether individuals become more literate because of the internet or information-seeking individuals are more likely to use the internet.

Two studies found that the barrier of low health literacy was a more relevant predictor of health outcomes than was lower education, although it was still significant. Inadequate health literacy had a strong, independent association with mortality even after adjusting for sociodemographic characteristics, chronic conditions, and physical and mental health (Baker, et al., 2007). In addition, the extent of the association between inadequate health literacy and mortality was similar to the association between low annual income and mortality. Wolf, Gazmararian, and Baker (2005) also reported that individuals with inadequate health literacy had worse physical function and mental health than those with adequate health literacy levels.

At the same time, one study found a strong correlation between lower levels of education and less information seeking (Wiltshire, Roberts, Brown, & Sarto, 2009). Using the 20002001 Household Component of the Community Tracking Study, the authors observed that, compared with individuals with college or higher level education, respondents with less than a high school education were 74% less likely to seek information; high school graduates were 51% less likely, and those with some college were 29% less likely. When adjusting for variables, poverty is significantly associated with information seeking; the poor (those at less than 99% of the federal poverty level) were 13% less likely to seek health information, and the near poor (those at 100 to 199% of the federal poverty level) were 15% less likely, when compared with the non-poor (at 300% or more of the federal poverty level). This study did not examine health literacy, and thus it is unknown whether education level or the health literacy would be a greater barrier to information seeking.

Peer mentoring has been shown to improve outcomes. Peer mentoring may support behavioral change. Examples in the health field include the American Cancer Societys mentor program and Weight Watchers. These peer-mentoring programs are long term, with the expectation that individuals will participate although with the understanding that participation is voluntary. Some dieting behaviors are similar to financial management, such as reducing spending and financial planning, and have been found to be effective in one study. A randomized trial evaluating multiple diet plans, including Weight Watchers, which includes a peer-mentoring component to the program, found statistically significant reductions in weight and cardiovascular risk factors (Dansinger, Gleason, Griffith, Selker, & Schaefer, 2005).