U.S. Department of Health and Human Services

The Use of Nursing Home and Assisted Living Facilities Among Privately Insured and Non-Privately Insured Disabled Elders

Marc A. Cohen, Ph.D., and Jessica Miller, M.S.

LifePlans, Inc.

April 2000

PDF Version: http://aspe.hhs.gov/daltcp/reports/2000/nhalfuse.pdf (63 PDF pages)

This report was prepared under contract between the U.S. Department of Health and Human Services (HHS), Office of Disability, Aging and Long-Term Care Policy (DALTCP) and LifePlans, Inc. Additional funds were provided by the Robert Wood Johnson Foundation Home Care Research Initiative. For additional information about the study, you may visit the DALTCP home page at http://aspe.hhs.gov/daltcp/home.htm or contact the ASPE Project Officer, Pamela Doty, at HHS/ASPE/DALTCP, Room 424E, H.H. Humphrey Building, 200 Independence Avenue, SW, Washington, DC 20201. Her e-mail address is: Pamela.Doty@osaspe.dhhs.gov.

TABLE OF CONTENTS

- I. BACKGROUND

- II. PURPOSE

- III. METHOD

- A. Sample

- B. Data

- IV. FINDINGS

- A. Profiling Privately Insured Institutionalized Claimants

- B. Demographic Characteristics

- C. Examining Claimant Profiles and HIPAA Benefit Eligibility Criteria

- D. Service Use and Residence Before Current Residency

- E. Service Use and Cost in Long-Term Care Facilities

- F. Benefits Paid Under Insurance Contracts and Insurance Policy Design

- G. Claimant Satisfaction with Insurance Policy and Insurance Company

- H. Impact of Private Long-Term Care Insurance on Claimants

- I. Comparing Privately Insured and Non-Privately Insured Institutional Residents

- LIST OF FIGURES

- FIGURE 1: Distribution of Institutionalized Claimants by Residents

- FIGURE 2: Distribution of Claimants by Residence by Company

- FIGURE 3: Distribution of Claimants by Residence and Unit

- FIGURE 4: Self-Assessment of Health Status by Institutional Residence

- FIGURE 5: Primary Diagnosis at Admission by Residence

- FIGURE 6: Disability Status by Institutional Residence: Limitations in Activities of Daily Living (ADLs)

- FIGURE 7: ADLs for which Assistance is Provided by Residence

- FIGURE 8: Cognitive Impairment by Claimant Residence

- FIGURE 9: Help Received with IADLs by Residence

- FIGURE 10: Percentage of Claimants Meeting HIPAA Triggers by Site of Care

- FIGURE 11: Percentage of Claimants Not Meeting HIPPA Triggers by Company and Residence

- FIGURE 12: Use of Services before Current Institutionalization by Residence

- FIGURE 13: Residence before Current Institutionalization

- FIGURE 14: Average Daily Charges Billed for All Care by Level of Care by Residence

- FIGURE 15: Average Monthly Claims Payments by Residence

- FIGURE 16: Total Amount of Time on Claim by Residence

- FIGURE 17: Ratio of Daily Benefit Amount to Daily Charges by Residence

- FIGURE 18: Satisfaction with Long-Term Care Insurance by Residence

- FIGURE 19: Are Policy Benefits Meeting Current Care Needs?

- FIGURE 20: Ease of Filing Claim for Benefits by Institutional Setting

- FIGURE 21: Actions Insurer Might Have Taken to Help Claimant

- FIGURE 22: Impact of Policy Ownership on Movement between the Community and Current Residence

- FIGURE 23: Number of ADL Dependencies Among Disabled Nursing Home Residents

- FIGURE 24: Presence of Cognitive Impairment Among Disabled Nursing Home Residents

- FIGURE 25: Residence Before Current Institutionalization Among Disabled Nursing Home Residents

- FIGURE 26: Total Charges Billed for Previous Month in Nursing Home

- FIGURE 27: Number of ADL Dependencies Among Assisted Living Residents

- FIGURE 28: ADLs for which ALF Residents Receive Assistance by Insurance Status

- FIGURE 29: Presence of Cognitive Impairment Among Assisted Living Residents

- FIGURE 30: Residence before Current Residence in Assisted Living

- FIGURE 31: Average Monthly Charges for Assisted Living Residents

- LIST OF TABLES

- TABLE 1: Socio-Demographic Characteristics of Privately Insured Institutional Claimants Age 65 and Over

- TABLE 2: Services Received by Claimants Residing in Assisted Living Facilities and Nursing Homes

- TABLE 3: Primary and Secondary Payment Sources by Residence

- TABLE 4: Policy Design Features for Institutional Coverage

- TABLE 5: Socio-Demographic Characteristics of Privately Insured and Non-Privately Insured Disabled Nursing Home Residents Age 65 and Over

- TABLE 6: Services Received by Disabled Nursing Home Residents

- TABLE 7: Primary and Secondary Payment Sources of Nursing Home Residents

- TABLE 8: Socio-Demographic Characteristics of LTC Claimants and All Residents in Assisted Living Facilities

ACKNOWLEDGMENTS

This research could not have been completed without the assistance and guidance of many individuals both inside and outside of the long-term care insurance industry. We would like to gratefully acknowledge the assistance provided by Robert Glowacki, Carolyn Eickenberg, and Sharon O'Dell from Aegon, Roy Christianson and David Rogers from American Travellers, Ray Nelson and Leslie Peters from Bankers Life and Casualty, Carol McBrayer, Melissa Stinson, Steve French and Richard Garner from CNA Insurance, Dan Nitz from Fortis Long-Term Care, Roger Desjardins, Mary Katz and Armando Leiva from G.E. Capital Assurance, Linda Berg-Maney and Peter Bokjov from John Hancock, and Bonnie Davis and Jim DuEst from UnumProvident. All of these individuals devoted a significant amount of time to assure that the sample of home care claimants was representative, that data from administrative systems was uniform and accurate, and that the fieldwork could be completed successfully. We are grateful for their patience and good cheer during the entire research process.

The project's technical advisory group included Susan Morisato, FSA, Bankers Life and Casualty, Bob Yee, FSA, of G.E. Capital Assurance, Christopher Murtaugh, Ph.D., Center for Home Care Policy and Research, Vicki Freeman, Ph.D., Rand Corporation, Randy Brown, Ph.D., Mathematica Policy Research, Inc., Brenda Spillman, Ph.D., Agency for Health Care Policy and Research, Nancy Miller, Ph.D., Health Care Financing Administration. Along with Dr. Laurence Branch of Duke University, the committee provided critical input into the initial design of the project and its sampling strategy.

We would also like to acknowledge the assistance of Beth Jackson, Ph.D., and Laurie Meneades of Medstat in preparation of the 1989 and 1994 National Long-Term Care Survey Datasets.

Finally, we greatly appreciate the patience, guidance, and advice of our two project officers and financial sponsors: Pam Doty, Ph.D., at the Office of Disability, Aging and Long-Term Care Policy of the Department of Health and Human Services, Office of the Assistant Secretary for Planning and Evaluation and Penny Feldman, Ph.D., of the Robert Wood Johnson Foundation Home Care Research Initiative. Their unwavering support and encouragement enabled us to overcome many of the hurdles presented by a study of this magnitude.

Of course the contents of this report are the sole responsibility of its authors. Any errors are the authors alone.

EXECUTIVE SUMMARY

The dramatic growth in the number of Americans over age 75 coupled with the need to minimize the duration of expensive inpatient hospital care, portend continued reliance on nursing home care for a significant portion of the disabled population. Even in the presence of significant expansions in home and community-based care, the nursing home still remains a key provider of long-term care (LTC) services to more than 1.5 million people, most of whom are over age 65. Alternative institutional settings such as assisted living facilities (ALFs) are also growing in popularity. Today there are more than 28,000 such residences housing more than one million people, many of whom have limitations in activities of daily living (ADLs). Thus, institutional-based care has and will remain an important component of the long-term care service delivery system.

The costs associated with receiving long-term care in institutional settings are significant and pose a financial hardship to many individuals. To meet this hardship, a growing number of individuals are purchasing private long-term care insurance. Through a series of actions, the Federal government is also signaling its desire that individuals accept greater personal responsibility for planning and paying for their long- term care needs. Such actions include tax clarification of long-term care insurance contracts, a plan to implement a Federal employees long-term care insurance plan, and expenditures on education related to the risks and costs of long-term care.

While there is a growing body of knowledge about who buys policies and what motivates them to do so, there has been no systematic study of individuals in institutionalized settings who are receiving benefits under their long-term care insurance policies. On an industry-wide basis, no one knows whether claimants and/or their families feel they are getting good value for their premiums, and whether the presence of private insurance influences the type of care people receive in these settings.

The purpose of this report is to provide basic descriptive statistics on disabled private LTC insurance policyholders who have accessed long-term care benefits in institutional settings, and to compare such data and findings to non-privately insured institutionalized elders. We did this by interviewing 480 long-term care insurance claimants from seven participating companies receiving benefits under their policies and residing in nursing homes or assisted living facilities. Key findings of the study are presented below.

The Profile of Long-Term Care Insurance Claimants in Residential Care Facilities (Nursing Homes and Assisted Living Facilities)

-

The majority of claimants in residential care facilities -- 72% -- were residing in nursing homes, and 28% were receiving services in assisted living facilities.

-

There are few differences in the socio-demographic profile of nursing home and assisted living claimants.

-

Most claimants in residential care facilities are over age 80, female, unmarried, highly educated and have incomes greater than $30,000.

-

The average income had by these residential facility claimants was about $33,000.

-

Married claimants are more likely to be in nursing homes than in assisted living facilities.

-

Slightly less than one in three claimants with dementia who are in residential care settings receive their care in assisted living facilities. Typically, the costs associated with caring for individuals in these facilities are less than in nursing homes. Thus, for some cognitively impaired individuals, private insurance coverage for assisted living care substitutes for more costly nursing home care.

-

Claimants in assisted living are about twice as likely to assess themselves to be in excellent health compared to those in nursing facilities. A parallel finding is that, compared to assisted living claimants, nursing home claimants are twice as likely to describe their health as poor.

-

The differences in the prevalence of specific diagnoses between residents of nursing homes and assisted living facilities are not statistically significant. This suggests that it is not the underlying primary diagnosis that differentiates individuals in each of these service modalities, but, instead, the way the diagnosis manifests itself.

-

The average number of ADL limitations for nursing home claimants is 4.7, whereas for assisted living claimants, this figure drops to 2.8 -- 79% of current claimants have two or more ADL limitations.

-

Among the participating companies, the average number of ADL limitations among nursing home claimants ranged from 4.0 to 5.2; for assisted living claimants, the range for the average number of ADL limitations was from 2.6 to 4.7.

-

For each ADL, the proportion of nursing home claimants in need of assistance is greater than the corresponding proportion of assisted living claimants.

-

The prevalence of cognitive impairment (as measured by diagnosis and orientation) is higher among nursing home claimants than it is among assisted living claimants. Overall, claimants in the nursing home are 1.3 times more likely to be cognitively impaired than are those found in assisted living facilities.

-

The proportion of claimants with cognitive impairment in the nursing home ranges between 75% and 86%, whereas in assisted living, the range is between 47% and 81%.

Claimants in Residential Care Facilities and HIPAA Eligibility Criteria

-

At the time of the in-person interview, almost all nursing home claimants had two or more ADL limitations or were cognitively impaired.

-

Only 78% of assisted living claimants met the HIPAA benefit eligibility criteria.

-

Individuals who did not meet HIPAA triggers in the assisted living facilities were much more likely to be unmarried, slightly less educated, and had somewhat lower levels of income. They also resided in facilities with lower daily charges -- $86 compared to $92.

-

About half (46%) of the assisted living residents who did not meet HIPAA benefit eligibility triggers had no ADL limitations at all.

Prior Residence and Service Use

-

About three in five (63%) of all nursing home residents and three in four (73%) assisted living residents had either been a previous resident in an assisted living facility or nursing home or had used home care prior to entering their current facility.

-

Almost half of assisted living residents had been in a different assisted living facility or nursing home before moving to their current residence.

-

About one-quarter of the assisted living residents had been transferred to assisted living from a nursing home. This suggests movement in both directions along the continuum of care: from nursing homes to assisted living and from assisted living to nursing homes.

-

About two in five facility residents had accessed formal home care services before their current admission to the facility.

-

The probability of entering a nursing home from a hospital is more than twice as high as entering an assisted living facility directly from a hospital -- 25% compared to 11%.

-

Prior to entering a residential care facility, between 43% and 47% resided in the community either alone or with their families.

Service Use, Costs and Payment Sources in Residential Care Settings

-

Claimants residing in nursing homes receive an average of five types of services each month, compared to four service types for assisted living claimants. This is not surprising, given the greater level of disability among nursing home claimants.

-

Nursing home residents use more medical services, skilled nursing care, nutritional services and social services than do assisted living claimants. In contrast, assisted living residents are much more likely to use transportation services.

-

With the exception of charges for skilled care, charges for care provided at the intermediate, residential and Alzheimers level are significantly lower in assisted living facilities -- an average of 27% for these claimants.

-

Assisted living facilities enable Alzheimers patients to be cared for at a lower cost than care provided in a nursing home. For this block of claimants, the associated savings of being able to access cognitive-related care in an assisted living facility instead of a nursing home are16%.

-

Depending on institutional setting, the insurance is the primary payment source for between 70% and 80% of these claimants. What is not paid for by the insurance is typically funded from personal resources.

-

An average of 73% of the long-term care liability is paid for by insurance. For nursing home claimants, 67% of the costs are covered, whereas for assisted living residents, the average daily benefit pays for most (88%) of the incurred costs.

-

In cases where insurance is not the primary payment source for nursing home claimants, the average daily benefit is lower, there is less likelihood of having a policy with inflation protection, and the difference between the daily charge and the daily benefit is greater.

Benefits Paid Under Insurance Contracts and Insurance Policy Designs

-

The average monthly insurance benefit paid to claimants is $2,141.

-

Monthly nursing home benefits are about 23% higher than assisted living benefits -- $2,251 versus $1,827.

-

These claimants have already used an average of $29,000 in insurance benefits per person -- $34,000 for nursing home residents and $16,000 for assisted living residents.

-

Most of these individuals (85%) have reimbursement policies covering four or more years of care at around $83 per day.

-

About two in five are eligible to receive over $100 per day in benefits for institutional care services; 45% of the claimants have policies that include some level of inflation protection.

-

The average value of available benefits is $161,000 and these individuals have thus far used up about 18% of their benefits.

-

Most individuals have been on claim for about 17 months.

-

About 45% of nursing home residents have been receiving benefits for more than a year-and-a-half; the comparable figure for assisted living residents is 25%.

Claimant Satisfaction with Insurance Policy and Insurance Company

-

The vast majority of claimants are satisfied with their policy, with most being very satisfied.

-

The vast majority (85%) had no difficulty understanding what their policy covered.

-

Roughly four out of five assisted living claimants felt that the benefits were adequate, given their care needs; the corresponding figure for nursing home claimants was about three out of five residents.

-

Most individuals -- more than 70% -- found the process of filing a claim to be easy.

-

Assisted living claimants were more likely -- 1.7 times more likely -- to find the process of filing a claim to be difficult.

-

About 90% of all individuals filing claims had either no disagreements with their insurance companies or had a disagreement(s) that was resolved satisfactorily. About 4% of claimants felt their disagreement was not resolved satisfactorily.

Impact of Private Long-Term Care Insurance on Claimants

-

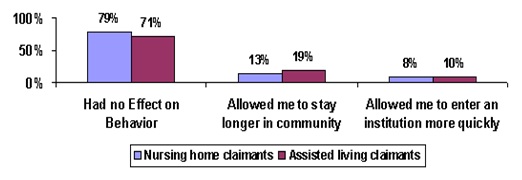

For about three-quarters of claimants, the presence of insurance was not viewed as having had an influence on service-seeking behavior.

-

One in five assisted living claimants, and one in eight nursing home claimants, indicated that the presence of insurance allowed them to delay their entry into an institution.

-

Roughly one in ten individuals indicated that they entered an institution sooner than they otherwise would have, given the presence of their insurance benefits. An analysis of the profile of these individuals suggests that they are typically older, have higher incomes, and are somewhat less ADL dependent than are those who did not change their behavior and enter an institution sooner.

-

Data suggests that, for some claimants, entry into the institution is motivated by social concerns as well as by a desire to be in a protective environment should additional declines in functioning occur.

Comparing Privately Insured and Non-Privately Insured Institutionalized Disabled Claimants1

Nursing Home Residents

-

On average, disabled nursing home residents with long-term care insurance are somewhat younger than their non-privately insured institutionalized counterparts: the proportion of privately insured claimants age 85 and over is only half that found in the general population of nursing home residents.

-

There also tends to be a greater proportion of privately insured male residents compared to other residents.

-

Residents with private long-term care insurance are 2.8 times more likely to be married than are those without such insurance.

-

Compared to non-privately insured nursing home residents, insured residents are four times as likely to be college educated and about 3.2 times more likely to have incomes greater than $20,000.

-

The privately insured sample is slightly more impaired compared to other residents. The average number of limitations for disabled long-term care insurance claimants is 4.9; this compares to between 4.4 and 4.7 limitations among non-privately insured residents.

-

The vast majority of disabled residents have some degree of cognitive impairment, although insured residents are somewhat less likely to be cognitively impaired.

- Privately insured disabled residents appear to receive fewer services than do other residents -- 5.4 services per month versus 6.7.

-

The non-insured resident population has somewhat greater medical or skilled care needs. This is borne out by their greater use of skilled nursing and medical services.

-

Non-privately insured residents have an average of 4.0 medical diagnoses whereas for claimants, the number is 3.0.

-

Data presented here suggests that, after gaining admission to a nursing home, the privately insured appear to use fewer services than that seen for other residents. Thus, if the costs associated with room and board are similar between privately insured and other residents, the former would be more profitable for two reasons: (1) the daily rate paid is likely to be higher than what is paid by other residents; and (2) service use is lower.

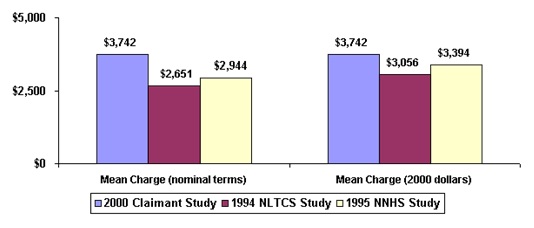

-

In nominal terms, the average charge among privately insured residents ($3,742) was between 27% and 40% higher than for other residents. After accounting for the impact of inflation, the difference narrows somewhat to between 10% and 22%.

-

For the privately insured, long-term care insurance and personal resources account for the major payer sources, whereas for the non-privately insured, Medicaid and personal resources comprise the primary payer sources.

Assisted Living Residents

-

Compared to other residents in assisted living, long-term care insurance claimants are somewhat younger, more likely to be male, and much more likely to be married. They also have somewhat higher income levels.

-

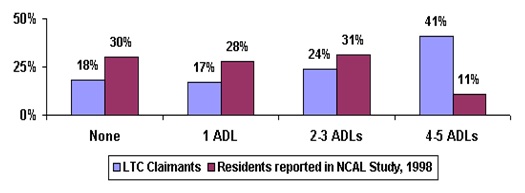

Long-term care insurance claimants in assisted living facilities have more disabilities than do non-privately insured residents. The average number of disabilities among claimants is 2.8, whereas among non-insured residents the comparable figure is 1.7.

-

About 75% of all assisted living residents have two or fewer ADL limitations. Among the privately insured, only 35% have fewer than two limitations.

-

For each ADL, higher proportions of insured residents exhibit dependency.

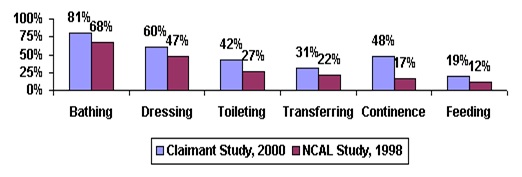

-

The greatest differences between the two groups relate to continence and toileting where claimants are between 1.8 and 2.8 times more likely to require assistance in these basic activities of daily living.

-

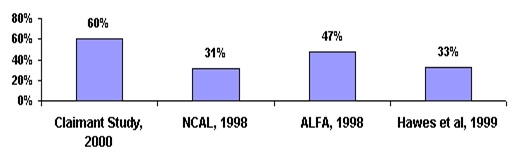

Assisted living residents with long-term care insurance are about twice as likely to be cognitively impaired, compared to all assisted living residents.

-

The monthly costs of care for insured residents ($2,700) are roughly 1.3 to 1.8 times higher than for other residents.

Whereas one might have thought that the continuum of care moves from home care to assisted living to nursing home care, the data present a more complicated picture. For some individuals, assisted living may actually substitute for remaining in the home and relying on formal home care services. Other claimants in assisted living facilities faced the alternative of nursing home care. Either way, it appears that, in the presence of comprehensive insurance coverage, one can expect greater use of lower intensity and more home-like institutional settings like assisted living. This presents opportunities to a sub-set of policyholders who would otherwise face more costly nursing home care.

Given the rapidly changing landscape of the service delivery network, insurers will need to continue to emphasize flexibility in their products. Along with such flexibility, however, is the need to keep consumers informed about the relationship between benefit levels and future service costs. This is particularly true for those accessing costly nursing home services. Here policy benefits cover a smaller fraction of the costs than in either the home or assisted living setting. While the presence of insurance will certainly alter service utilization patterns, few individuals seem to be drawn more quickly to seek institutional alternatives just because they have insurance. What the insurance does allow is the ability for disabled individuals to access a variety of services in alternative settings and to do so in a way that leaves these people very satisfied with their coverage.

I. BACKGROUND

The dramatic growth in the number of Americans over age 75, coupled with the need to minimize the duration of expensive inpatient hospital care, portend continued reliance on nursing home care for a significant portion of the disabled population. Between 1987 and 1996, the number of nursing homes and the number of nursing home beds both increased by almost 20% (Rhoades and Krauss, 1999). Yet, the growth in the elderly population over this time period outpaced the growth in nursing home beds. The fact that the number of beds did not keep pace with the growth in the elderly population is due to a number of factors. These include the imposition of restrictions on supply through Certificate of Need (CON) programs, an expanding home and community-based care network, growth in assisted living facilities, and a decline in age-specific rates of disability (Bishop, 1999; Lewin-VHI, 1991; Wiener, et al, 1998). Even though there has been a decline in nursing home use, however, the nursing home still remains a key provider of long-term care services to more than 1.5 million people, most of whom are over age 65.

Another institutional setting growing in popularity and serving disabled elders is assisted living. Assisted living facilities typically offer a combination of housing, health care, personal assistance and supportive services. The term "assisted living" refers to a type of care that combines housing and services in a homelike environment that strives to maximize the individual functioning and autonomy of the frail elderly and other dependent populations (Lewin-VHI, 1992). Today, there are more than 28,000 assisted living residences in the U.S., housing more than one million people; the typical assisted living resident is 83 years old, female, and slightly disabled, having limitations in 1.7 activities of daily living (National Center for Assisted Living, 1998).

There are substantial variations in the range of services that assisted living facilities provide and in the type of populations they serve. For the most part, individuals living in assisted living facilities are medically stable and do not require 24-hour nursing care. Most facilities provide or arrange for some level of personal care services for those individuals who may require them. In fact, about 70% of assisted living residences contract with a home health agency to provide skilled nursing, and 65% of residences contract with a hospice provider for hospice services (National Center for Assisted Living, 1998).

The growth in assisted living facilities reflects consumer demand for supportive living environments that closely parallel a "home-like" atmosphere. In addition, the growth in the sub-acute market may have begun to create a vacuum in the provision of traditional low-technology, facility-based long-term care that assisted living beds are designed to fill. Assisted living costs can range from 30% up to 100% of skilled nursing care costs (Raskin, 1995). Moreover, recent research suggests that transferring certain Alzheimer's patients from nursing homes to assisted living facilities could save up to 14% of long-term care costs (Leon, et al, 1999). These facilities may also achieve economies of scale in the delivery of home health care to frail elders that would be difficult to achieve if living alone in their own homes. Because elders overwhelmingly prefer to stay in their own homes or reside in congregate living situations compared to nursing homes, the assisted living modality is likely to continue to grow and expand.

Expenditures on institutional care are significant. As of 1997, the average private pay daily rate for nursing home care was $125 and the average nursing home cost approximately $50,000 per year (AARP, 1998). The average daily charge for assisted living was about $60 or $22,000 per year (ALFA, 1998). Not surprisingly, long-term care expenditures on nursing homes and related facilities now account for a growing share of total personal health expenditures. Among people aged 65 and older, expenditures on institutional care account for about 25% of personal health expenditures. The primary payers of long-term care institutional services include disabled elders and their families and the Medicaid program. In 1997, Medicaid spent over $32 billion on nursing home care (Burwell, 1998). This represents roughly 43% of the total nursing home bill, which was nearly $75 billion in that year. Currently, about 35 states cover, or plan to cover, assisted living or board and care as a Medicaid service (NIC, 1997). When the costs of assisted living are included, expenditures on institutional care settings reach $100 billion (Burwell, 1998; National Center for Assisted Living, 1998).

Historically, exposure to catastrophic cost risks of this nature has stimulated demand for private insurance, expanded public financing -- or both. Over the past decade, the potential of private long-term care insurance to become a significant source of financing for formal long-term care services has been much debated (See Cohen et al, 1987; Rivlin and Wiener, 1988; Friedland, 1990; Families USA, 1993; Crown, et al, 1992). Even as the debate continues, the individual and employer-group markets continue to grow significantly. Long-term care insurance is one of the fastest growing health insurance business lines; in 1999 alone, growth in premium from new sales was 13% (LifePlans, Inc. 2000). More than 5.5 million people will have at one time or another acquired a policy (HIAA, 1998).

Recent actions suggest that the federal government has now shifted much of its focus to private insurance to help address the long-term care financing problem. On August 5, 1999, the Senate and the House of Representatives approved the Taxpayer Refund and Relief Act of 1999 (H.R. 2488), which among other things proposed changing the tax status of premiums paid for long-term care (LTC) insurance contracts. Currently, individuals can deduct their insurance premiums if they itemize their deductions and their medical expenses exceed 7.5% of adjusted gross income. Under the new legislation, which was subsequently vetoed by President Clinton, individuals would have been able to take an "above the line deduction" of LTC insurance premiums. Individuals purchasing LTC insurance could have deducted the full amount of their premium payment from adjusted gross income, whether or not they itemized deductions or had medical expenses above the 7.5% threshold. The purpose of the proposed legislation was to use the tax code to encourage individuals to acquire private insurance to cover the potentially catastrophic costs of long-term care.

In his 1999 state of the union message, the President recommended that a new long-term care insurance program be established for federal employees. Moreover, in recognition of the financial burden imposed by informal caregiving, this year the President recommended that a tax credit of up to $3,000 per year be available to those caring for disabled relatives. With these actions, the federal government is continuing to signal its desire that individuals accept personal responsibility for planning and providing for their long-term care needs.

Questions remain, however, about whether private long-term care insurance represents a "good buy." Proponents of private long-term care insurance argue that its purchase is the only viable alternative to out-of-pocket spending or reliance on informal family caregiving for elders with incomes and assets above the means-tested eligibility levels for most publicly-funded long-term care service coverage. Critics question both the affordability of private long-term care insurance to the target market of middle-aged and "young-old" individuals and whether the product will meet the needs of those who purchase it.

Given anticipated changes in Federal policy with respect to Medicare and Medicaid, as well as recent attempts to further clarify the tax status of long-term care insurance, it is likely that the market will continue to expand. Yet, while there is a growing body of knowledge about who buys policies and what motivates them to do so (ACLI, 2000; HIAA, 1992 & 1995), there has been no systematic study of individuals in institutionalized settings who are receiving benefits under their long-term care insurance policies. On an industry-wide basis, no one knows whether claimants and/or their families feel they are getting good value for their premiums, and whether the presence of private insurance influences the type of care people receive in these settings.

The current study of institutionalized claimants is part of a larger study on Long-Term Care Insurance Claimants, funded by the Office of the Assistant Secretary for Planning and Evaluation (ASPE), Office of Disability, Aging and Long-Term Care Policy and the Robert Wood Johnson Foundation. The principal report was completed in April 1999 and is entitled: "A Descriptive Analysis of Patterns of Informal and Formal Caregiving among Privately Insured and Non-Privately Insured Disabled Elders Living in the Community." Two supplemental reports about the informal caregivers of these community-dwelling disabled elders and the use of multivariate modeling to understand service use were completed in December 1999. The current report focuses on the experiences of institutionalized claimants, that is, those who are receiving care in nursing homes and in assisted living facilities.

II. PURPOSE

The purpose of this research is to provide basic descriptive statistics on disabled private LTC insurance policyholders who have accessed long-term care benefits in institutional settings and to compare such data and findings to non-privately insured institutionalized elders. We intend to:

- provide detailed descriptive information on the socio-demographic and service utilization profile of disabled claimants residing in institutions receiving benefits under their LTC insurance policies;

- characterize the level and mix of services among disabled institutionalized claimants and compare this to a nationally representative sample of non-privately insured disabled elders residing in institutions;

- identify any factors associated with observed differences between the insured and non-insured groups in relation to the utilization of services;

- evaluate claimant and or family perceptions regarding the value of the LTC policy; and,

- discuss the implications of findings on the service delivery system as well as on the design of private and public LTC policies and programs.

Obtaining answers to these questions is important from a public policy and regulatory standpoint. The vast majority of LTC policies cover care provided in a variety of modalities. Thus, their proliferation in the market will affect the level and mix of publicly funded long-term care services. In the absence of "hard data" about the experience of claimants, it is difficult to develop targeted regulatory and consumer protection strategies related to claims issues. Also, if state and Federal governments wish to encourage development of the long-term care insurance market, it is important that there be adequate information about how the product is performing from the perspective of claimants and their families. This will assist the government in assessing the future potential of long-term care insurance.

Such information is also of interest to private insurers, who are trying to increase the market for long-term care insurance, and actuaries who are responsible for pricing long-term care insurance products. Often, the only information available to actuaries on a national basis is derived from uninsured experience among the general population of disabled elders (e.g. 1985 and 1995 National Nursing Home Survey and 1994 National Long-Term Care Survey). Information from these surveys may not accurately represent experience in an insured context. Thus, it is important to determine whether, and in what ways, the utilization of institutional services differs in the presence of long-term care insurance. This has implications for the way policies are designed, priced, and marketed.

III. METHOD

A. Sample

The study relied on the development of three analytic samples. These included:

- Privately insured institutionalized individuals who are accessing benefits under their LTC insurance policies (Institutional Claimants);

- Disabled institutionalized Medicare beneficiaries who do not have private LTC insurance (1994 National Long-Term Care Survey -- 1994 NLTCS sample);

- A sample of 1,409 nursing homes and 8,056 of their current residents (1995 National Nursing Home Survey -- 1995 NNHS).

Institutional Claimants

To be included in the privately insured claimant sample, individual claimants had to meet the following criteria:

- They had to be age 65 and over;

- They had to be classified as an active claim with at least one payment for institutional services; and

- They had to have a policy that covered both nursing home care and home and community-based services.

We asked each company to provide a sample of claimants who met these criteria. We focused on individuals with "dual-coverage" policies, rather than on those with policies covering only institutional care, because roughly 80% of all policies currently selling in the market cover services in at least these two modalities. By doing so, we could assure that study findings would be applicable in the future as well as in the present. Together, these eight companies provided an institutional claimant block of 583 eligible institutionalized individuals of whom 82% or 480 participated in the study.

The 1994 National Long-Term Care Survey

The 1994 National Long-Term Care Survey (NLTCS) was designed to collect data about the health and function of the Medicare beneficiary population age 65 and older. The questions were meant to identify persons who had certain disabilities or health problems lasting three months or longer. In general, the institutional section of the survey includes persons who were in the community in previous waves of the survey (i.e. 1982, 1984, 1989), both those screened in as disabled and those who did not pass the disability screen in a previous year. A sample of nursing home residents was included as well, so that the entire sample is representative of nursing home residents nationwide. The total 1994 NLTCS sample of institutionalized elders consisted of 1,335 individuals.

The 1995 National Nursing Home Survey

The 1995 National Nursing Home Survey is a two-stage design with a probability sample of 1,500 nursing facilities in the first stage and up to six current residents per facility in the second stage of sampling. The facilities included in the universe were nursing and related care homes in the United States that had three or more beds, were staffed for use by residents, and routinely provided nursing and personal care services. The sample of current patients was obtained by randomly selecting up to six residents who were on the rolls of nursing homes as of midnight the night prior to the day of the survey. In total, 1,409 nursing homes participated in the study, and there is data available on 8,056 of their residents.

B. Data

Sources of Information

Seven of the largest LTC insurance companies in the U.S. participated in the study and contributed a sample of claimants residing in institutional settings. These companies also provided data from their administrative and claim systems to supplement information collected directly from claimants.

The participating companies included: (1) Aegon; (2) American Travellers; (3) Bankers Life and Casualty; (4) CNA Insurance; (5) Fortis Long-Term Care; (6) G.E. Capital Assurance; and (7) UnumProvident. Together their claimant blocks comprise more than 80% of all open institutional claims. These companies also represent diverse market segments and policy designs, and employ differing underwriting and claims management strategies.

As mentioned, in addition to the information provided by the LTC insurance industry, we analyzed information from the 1994 National Long-Term Care Survey (1994 NLTCS).2 This data allowed us to make comparisons between privately insured and non-privately insured disabled elders living in the community. Questions on the claimant survey were designed to mirror those on the 1994 NLTCS; this assured that accurate comparisons between the privately insured and non-privately insured samples could be made. Many of the questions on the claimant survey were also designed to correspond to those found on the 1995 National Nursing Home Survey. This enabled us to compare the types of facilities and service packages used by the privately insured and the non-privately insured.

Data Collection

We gathered data from all privately insured institutionalized claimants via in-person interviews conducted by trained nurses and social workers with at least two years of geriatric experience. Each interviewer underwent comprehensive training to assure inter-rater reliability. Information garnered from these interviews was then linked to policy design and claim information generated from the administrative systems of the participating insurance companies. Most often, we conducted interviews with proxies, primarily family members including spouses and children. When necessary, we gathered information from a claimant's chart or the nurse most familiar with their care. In some instances, where the claimant was found to be cognitively intact, we conducted the interview with the claimant themselves. We also collected a great deal of administrative and billing information pertaining to charges, bed classification, facility licensure, and payer source. We completed the fieldwork between January 1999 and January 2000. It is important to note that each completed survey underwent a detailed quality review by home-office staff. In some cases, surveys had to be returned to the field either because certain data elements were not complete or because of the presence of clinical discrepancies.

IV. FINDINGS

A. Profiling Privately Insured Institutionalized Claimants

Residence

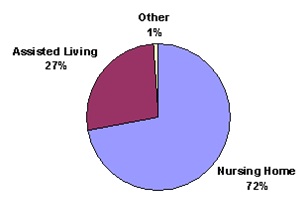

Figure 1 shows the distribution of claimants by institutional setting. As shown, the majority of individuals (72%) were residing in nursing homes, although a significant percentage was receiving services in assisted living facilities.

| FIGURE 1: Distribution of Institutionalized Claimants by Residence |

|

| SOURCE: 2000 National Claimant Study. |

Given the fact that the assisted living industry experienced its rapid growth only over the past five to ten years, this represents a particularly high percentage of individuals using this service. Because there are major differences between assisted living facilities and traditional nursing homes, almost all subsequent analyses will distinguish between the two.

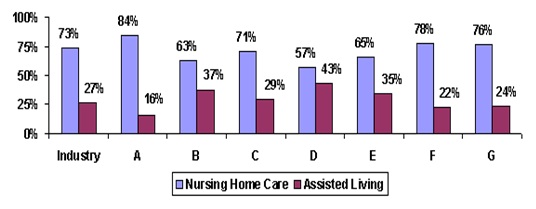

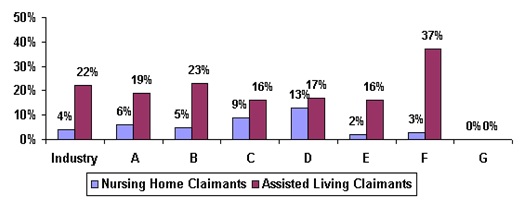

Figure 2 shows that there is a great deal of variation across the participating companies regarding the use of nursing and assisted living facilities among claimants.3, 4

| FIGURE 2: Distribution of Claimants by Residence by Company |

|

| SOURCE: 2000 National Claimant Study. |

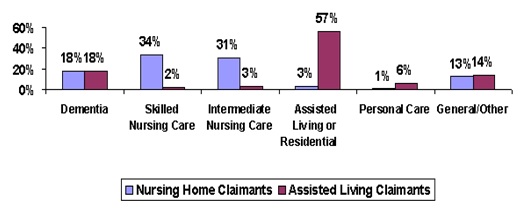

The next figure shows the distribution of claimants by the type of unit in which they reside. Again, data is presented for claimants in nursing homes and in assisted living facilities. Most striking is the fact that about 30% of dementia patients receive their care in assisted living facilities. As shown in Figure 3, about 18% of private long-term care claimants in both nursing homes and assisted living facilities are in specialized dementia units within these facilities. Typically, the costs associated with caring for individuals in these facilities are less than in nursing homes (Leon, et al, 1999). Thus, for some cognitively impaired individuals, private insurance coverage for assisted living care substitutes for more costly nursing home care.

Also noteworthy is the fact that most claimants are not receiving skilled care services but intermediate and personal care services. This finding supports the notion that private long-term care insurance is designed to pay for chronic care needs rather than post-acute recuperative needs. Data on bed classification at the time of assessment also support this proposition -- less than half of all institutional claimants were receiving skilled care or rehabilitation/sub-acute care.

| FIGURE 3: Distribution of Claimants by Residence and Unit |

|

| SOURCE: 2000 National Claimant Study. |

Not shown in the figure is the fact that 60% of nursing home claimants and 82% of assisted living claimants reside in for-profit facilities.

B. Demographic Characteristics

The table below displays the demographic profile of institutional claimants.

| TABLE 1: Socio-Demographic Characteristics of Privately Insured Institutional Claimants Age 65 and Over | ||

| Socio-Demographic Characteristics | Nursing HomeClaimants(n=338) | Assisted LivingClaimants1(n=128) |

| Average Age | 81 years | 81 years |

| 65-69 | 2% | ---- |

| 70-74 | 13% | 11% |

| 75-79 | 27% | 20% |

| 80-84 | 32% | 38% |

| 85+ | 26% | 31% |

| Gender | ||

| Male | 34% | 28% |

| Female | 66% | 72% |

| Marital Status | ||

| Never married | 5%* | 5% |

| Married | 44% | 34% |

| Divorced/separated | 4% | 2% |

| Widowed | 47% | 59% |

| Race | ||

| White (not Hispanic) | 99%** | 96% |

| Non-White | 1% | 4% |

| Education Level | ||

| Less than High School Graduate | 17% | 11% |

| High School Graduate | 22% | 27% |

| Technical/Trade/Business | 12% | 7% |

| Some College | 17% | 20% |

| College Graduate | 32% | 35% |

| Total Annual Income | (n=228) | (n=92) |

| Up to $20,000 | 30% | 29% |

| $20,000 - $39,999 | 51% | 45% |

| $40,000 - $59,999 | 11% | 9% |

| $60,000 - $74,999 | 3% | 9% |

| $75,000 - $100,000 | 3% | 3% |

| Greater than $250,000 | 4% | 5% |

| Estimated Current Value of Home | (n=137) | (n=38) |

| Less than $75,000 | 20% | 21% |

| $75,000 - $99,999 | 23% | 18% |

| $100,000 - $149,999 | 29% | 34% |

| $150,000 - $199,999 | 13% | 13% |

| $200,000 - $249,999 | 4% | --- |

| Greater than $250,000 | 11% | 13% |

SOURCE: 2000 National Claimant Study.NOTE: * Significant at the .10 level; ** Significant at the .05 level.

| ||

For the most part, there are few differences in the socio-demographic profile of nursing home and assisted living claimants. While it appears that there are slightly more females in assisted living than in nursing homes, the difference is not statistically significant. A surprising finding is that married claimants are more likely to be in nursing homes than in assisted living facilities. This may reflect the fact that if one member of a couple becomes disabled the spouse may choose to remain in their home rather than move to an assisted living facility. For the disabled individual, the difference between being alone in an assisted living facility versus a nursing home may not be so great. Given that most elders who become disabled do experience additional declines, the opportunity to move once, rather than twice, may also be a contributing factor explaining this finding. It may also be the case that married individuals in nursing homes are more disabled than married individuals in assisted living facilities.

Regarding race, a slightly higher proportion of non-white claimants reside in assisted living. Finally, in terms of education level, income and estimated value of housing (for individuals who still own a home), there were few differences between the groups. The average income had by these institutional claimants was about $33,000.

Health Status

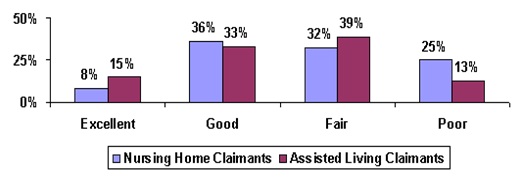

Respondents were asked a number of questions relating to their health status. The figure below illustrates how claimants assessed their health status at the time of the in-person interview. Not surprisingly, claimants in assisted living are about twice as likely to assess themselves to be in excellent health compared to those in nursing facilities. A parallel finding is that compared to assisted living claimants, nursing home claimants are twice as likely to describe their health as poor. These differences are significant at the .01 level.

| FIGURE 4: Self-Assessment of Health Status by Institutional Residence |

|

| SOURCE: 2000 National Claimant Study.NOTE: Differences are significant at the .01 level. |

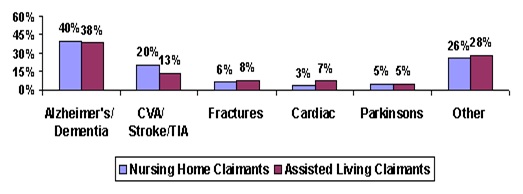

An additional measure for the overall health status of individuals is the presence of particular diagnoses at admission to a facility. Almost all individuals had at least one medical diagnosis at admission to a facility. Figure 5 shows that roughly 70% of claimants in either nursing homes or assisted living facilities had one of five major primary diagnoses. Dementia related diagnoses were present in about 40% of all claimants. The differences in the prevalence of specific diagnoses between residents of nursing homes and assisted living facilities are not statistically significant. This suggests that it is not the underlying primary diagnosis that differentiates individuals in each of these service modalities, but instead the way the diagnosis manifests itself.

| FIGURE 5: Primary Diagnosis at Admission by Residence |

|

| SOURCE: 2000 National Claimant Study. |

Disability Status

The next three figures illustrate the extent of disability among privately insured institutional claimants. Disability is measured in three ways: (1) the number of limitations in ADLs; (2) whether or not someone is cognitively impaired, as determined by medical diagnosis, or their orientation to person, time and place; and (3) the presence of limitations in higher order functions or selected instrumental activities of daily living (IADLs).

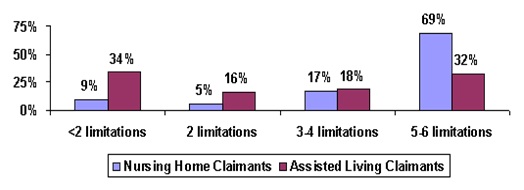

Most currently available LTC policies require an individual have at least two ADL limitations or be cognitively impaired in order to qualify for benefits. All currently issued tax-qualified policies have such a requirement. Older and non-tax qualified policies do, however, enable an individual to access benefits if LTC services were deemed by a physician to be "medically necessary".5 Seventy-nine percent of current claimants in residential facilities have two or more ADL limitations. As shown in Figure 6, 91% of claimants in nursing homes and 66% of claimants in assisted living facilities have at least two ADL limitations. The average number of ADL limitations for nursing home claimants is 4.7, whereas for assisted living claimants this figure drops to 2.8. Not shown in the diagram is the fact that, among the participating companies, the average number of ADL limitations among nursing home claimants ranged from 4.0 to 5.2; for assisted living claimants the range for the average number of ADL limitations was from 2.6 to 4.7.6

| FIGURE 6: Disability Status by Institutional Residence: Limitations in Activities of Daily Living (ADLs) |

|

| SOURCE: 2000 National Claimant Study.NOTE: Differences are significant at the .01 level. The Activities of Daily Living measured include bathing, dressing, toileting, transferring, continence and feeding. |

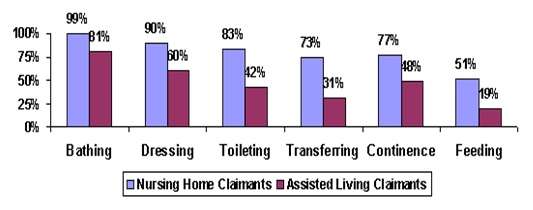

Figure 7 displays the specific ADLs for which assistance is needed. As shown, for each ADL, the proportion of nursing home claimants in need of assistance is greater than the corresponding proportion of assisted living claimants. These differences are statistically significant at the .01 level. The figure also demonstrates the hierarchical nature of ADL loss. With the exception of continence, the typical pattern of loss begins with bathing and then moves to dressing, toileting, transferring and feeding. This is exactly the pattern observed among claimants in each of these institutional residences.

| FIGURE 7: ADLs for which Assistance is Provided by Residence |

|

| SOURCE: 2000 National Claimant Study. |

It is also important to note that most nursing facilities do not allow individuals to bathe on their own. Therefore, by regulation all residents receive assistance in bathing.

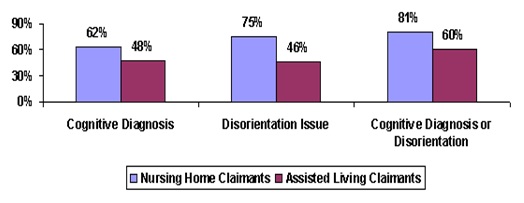

Figure 8 displays the claimant sample by cognitive status. The prevalence of cognitive impairment (as measured by diagnosis and orientation) is higher among nursing home claimants than it is among assisted living claimants. Overall, claimants in the nursing home are 1.3 times more likely to be cognitively impaired than are those found in assisted living facilities. It is also true that orientation problems are less prevalent among assisted living residents.

How does this finding correspond to the earlier result that roughly 18% of claimants in both assisted living and nursing homes are in dementia units? Data presented in Figure 8 suggests that while roughly five in eight assisted living claimants has some level of cognitive impairment, many would only be considered moderately or mildly impaired. Thus, they are not residing in dementia/Alzheimer's units. Regarding the nursing home claimants, many with cognitive impairment are actually treated in other units for medical and personal care issues. Thus, most of them are also not residing in a specialty care unit for the cognitively impaired.

| FIGURE 8: Cognitive Impairment by Claimant Residence |

|

| SOURCE: 2000 National Claimant Study.NOTES: Differences are significant at the .01 level. Cognitive impairment is measured either by having a cognitive diagnosis at admission or at the time of the interview, or being oriented to person, time or place only sometimes or never. |

Because companies use different underwriting techniques to identify individuals who may be at high risk for becoming cognitively impaired, there is a great deal of variation between companies in the number of claimants with cognitive impairment issues. The proportion of claimants with cognitive impairment in the nursing home ranges between 75% and 86% whereas in assisted living, the range is between 47% and 81%. Some companies conduct more intensive in-person assessments during the policy application process, while others rely more heavily on medical records or phone interviews. Clearly, some companies are more successful than others at identifying the risk of cognitive claims. Also, policy designs and claims adjudication procedures may lead to variability in the number of claimants with cognitive impairment.

Another measure of one's disability status is the ability to perform IADLs. These higher order activities must also be performed as part of independent living. Such activities typically include shopping, laundry, light housework, outdoor mobility, managing medications, managing money, getting to places out of walking distance, and meal preparation. Loss of the ability to perform these activities is usually a precursor to loss of ADL function.

While useful in tracking levels of functional capacity, there are shortcomings with this measure. One difficulty with relying on IADLs to measure disability is that many of them are role-related. That is, an individual may never prepare meals because his or her spouse has always prepared them. Not being able to prepare a meal would not necessarily be indicative of one's lack of ability to do so. Also, in institutional settings, as a matter of routine, many IADLs are performed for individuals by staff. Therefore, a more specialized list has been developed to measure disability in these higher order functions for individuals in institutional settings. We asked claimants whether or not they receive any personal help or supervision in:

- Managing money;

- Caring for personal possessions such as clothing, toiletries, etc.;

- Securing personal items such as newspapers, toilet articles, or snack food; and

- Using the telephone (dialing or receiving calls).

Figure 9 shows that for each of these activities, a greater proportion of nursing home claimants receive help than do assisted living claimants. With the exception of telephone use, the majority of claimants receive some level of assistance in these activities.

| FIGURE 9: Help Received with IADLs by Residence |

|

| SOURCE: 2000 National Claimant Study.NOTE: Differences are significant at the .01 level. |

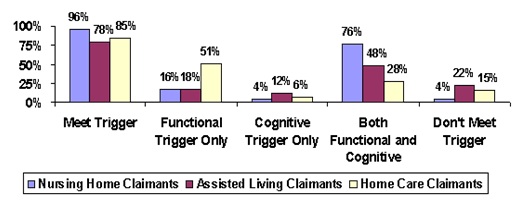

C. Examining Claimant Profiles and HIPAA Benefit Eligibility Criteria

In the HIPAA (i.e. Kennedy-Kassebaum) legislation, long-term care insurance policies are tax qualified if access to benefits is limited to (1) individuals with at least two ADL limitations or (2) individuals who are moderately or severely cognitive impaired. Figure 10 shows that, at the time of the in-person interview, almost all nursing home claimants met these criteria. Only 78% of assisted living claimants met the criteria. Taken together, these findings suggest that, depending on site of care, somewhere between 4% and 22% of claimants would not have met HIPAA triggers at the time of the in-person interview. By way of comparison, we also provide data on home care claimants. Additional analysis does reveal, however, that most of these individuals were either on their way to becoming more disabled or were in the process of improving in function.

| FIGURE 10: Percentage of Claimants Meeting HIPAA Triggers by Site of Care |

|

| SOURCE: 2000 National Claimant Study. |

Figure 11 shows that there is a high degree of variation among companies regarding the proportion of institutionalized claimants who at the time of the interview did not meet HIPAA benefit eligibility triggers.7

| FIGURE 11: Percentage of Claimants Not Meeting HIPAA Triggers by Company and Residence |

|

| SOURCE: 2000 National Claimant Study. |

Individuals who did not meet HIPAA triggers in the assisted living facilities were much more likely to be unmarried, slightly less educated, and had somewhat lower levels of income. They also resided in facilities with lower daily charges -- $86 compared to $92. Finally, 46% of the assisted living residents had no ADL limitations.

D. Service Use and Residence before Current Admission

For the most part, when individuals enter institutional settings it is only after alternatives have been tried in the community. That is, unless there has been a severe acute event (e.g. stroke) that leads to significant functional limitations necessitating immediate institutionalization, many individuals first experience declines in the community before entering an institution. Only after informal support networks or paid care can no longer meet an individual's needs in the community do individuals tend to move to institutional settings.

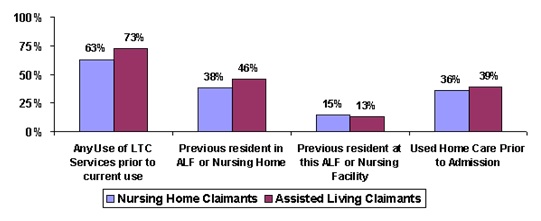

All claimants in this sample have insurance policies that cover home and community-based care services as well as institutional services. We asked whether or not they had received any home or community-based services or whether they had resided in other long-term care institutions prior to their current residence. Figure 12 summarizes results.

| FIGURE 12: Use of Services before Current Institutionalization by Residence |

|

| SOURCE: 2000 National Claimant Study. |

The majority of individuals had accessed long-term care services before entering their current institution. In fact, 63% of all nursing home residents had either been a previous resident in an assisted living facility or nursing home or had used home care prior to entering their current facility. The comparable figure for assisted living claimants is 73%. Given that entry to a nursing home is often precipitated by an acute incident, it is not surprising that fewer nursing home residents accessed long-term care services before entering a nursing home.

Almost half of assisted living residents had been in a different assisted living facility or nursing home before moving to their current residence; about one-quarter of the assisted living residents had been transferred to assisted living from a nursing home. This suggests movement in both directions along the continuum of care: from nursing homes to assisted living and from assisted living to nursing homes. It also indicates a very high "moving rate" among these individuals.

About two in five institutionalized residents had accessed formal home care services before their current admission to the facility. The proportion is slightly higher among assisted living residents, again suggesting that a greater number of nursing home residents had likely experienced an acute incident that necessitated immediate institutionalization in a nursing facility.

Given that these claimants had policies that covered both home care and institutional care services, it is surprising that less than half had used home care benefits. There are a number of possible explanations for this. First, it may be that these individuals want to conserve their insurance benefits to pay for the care that carries with it the greatest financial risk -- institutional care. They may be able to rely on informal caregivers to provide the level of care needed in the community. Second, although the financing may be in place, the service infrastructure may not be available to provide significant amounts of home and community-based care. Finally, it may also be the case that these claimants did not fully understand that their policies covered home care services.

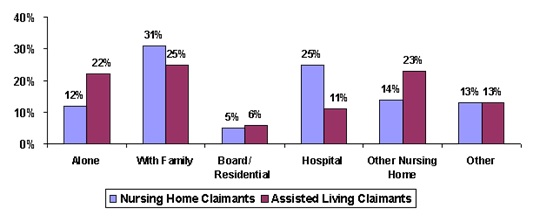

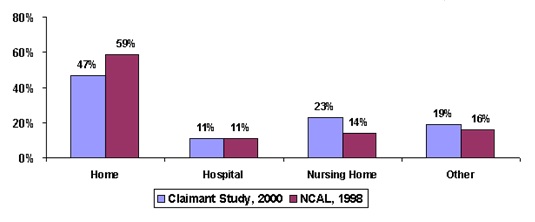

Figure 13 shows that the probability of entering a nursing home from a hospital is more than twice as high as entering an assisted living facility directly from a hospital. Data also indicate that prior to entering an institution, between 43% and 47% resided either alone or with their families.

| FIGURE 13: Residence before Current Institutionalization |

|

| SOURCE: 2000 National Claimant Study. |

E. Service Use and Cost in Long-Term Care Facilities

Long-term care services are often classified as being either home or community-based or institutional in nature. Analyses of individuals' use of home care services typically focus on the type of service (e.g. home health aide, therapist, nurse, etc) and its frequency and duration of provision. Such is not the case when it comes to institutional alternatives. For the most part, the discussion stops with the observation that an individual has moved into a nursing home or assisted living facility. Few researchers have adequately focused attention on the service packages that are provided -- as opposed to offered -- to residents once in a facility.

In Table 2, we show the proportion of residents receiving various services related to their long-term care, social and acute care needs. Claimants or their proxies were asked the following question:

In the last month (since date one month ago), which of these services did you receive, either inside or outside this facility?

The assessor was also instructed to refer to the insured's medical and administrative chart and verify and/or obtain the information requested. As shown in Table 2, claimants residing in nursing homes received an average of five types of services during the previous month; this compares to about four types for assisted living claimants.

| TABLE 2. Services Received by Claimants Residing in Assisted Living Facilities and in Nursing Homes | ||

| Services | Nursing Home | Assisted Living |

| Average number of services received | 5.4*** | 3.9 |

| Dental care | 22% | 23% |

| Equipment or devices | 41%** | 30% |

| Medical services | 71%*** | 46% |

| Mental health services | 7% | 6% |

| Skilled nursing services | 56%*** | 15% |

| Nutritional Services | 50%*** | 26% |

| Occupational Therapy | 9%* | 5% |

| Personal Care | 87%*** | 64% |

| Physical Therapy | 23%** | 15% |

| Medicines (prescribed or non-prescribed) | 93%*** | 83% |

| Social services | 31%*** | 11% |

| Transportation | 31% | 48%*** |

| SOURCE: 2000 National Claimant Study.NOTE: * Significant at the .10 level; ** Significant at the .05 level; *** Significant at the .01 level. | ||

Given their greater level of disability, this finding is not surprising. The greatest differences relate to nursing home residents' greater use of medical services, skilled nursing care, nutritional services and social services. In contrast, assisted living residents are much more likely to use transportation services. This likely reflects their greater ability to move about outside of their facility. Excluding medications, the most commonly used service among assisted living claimants is personal care.

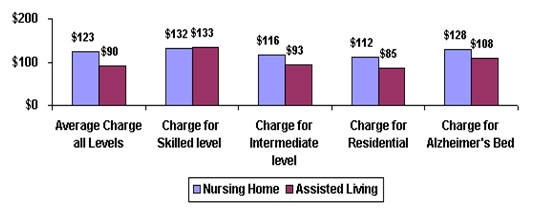

The charges associated with the services provided in these institutional settings vary greatly.8 Recent data suggests that the average private pay rate in a nursing home is about $125 (AARP, 1998). Figure 14 shows the average charges for these claimants according to the type of bed in which they resided. As shown, the average charge for nursing home claimants is similar to the AARP figure of $125 per day.

| FIGURE 14: Average Daily Charges Billed for All Care by Level of Care by Residence |

|

| SOURCE: 2000 National Claimant Study. |

The data clearly indicate that with the exception of charges for skilled care, charges for care provided at the intermediate, residential and Alzheimer's level are significantly lower in assisted living facilities -- an average of 27% for these claimants.9 The finding regarding care for Alzheimer's patients is particularly striking, given that such patients have traditionally been cared for in nursing homes and that they represent a significant proportion of institutional claimants. Assisted living facilities have enabled such patients to be cared for at a lower cost to the claimant as well as to the insurance company. Other recent research found that among non-privately insured individuals, care for Alzheimer's patients is cheaper -- by about 14% -- when provided in assisted living facilities as opposed to a nursing home (Leon et al, 1999). For the privately insured claimants in this study, the associated "savings" of being able to access assisted living instead of nursing home care for cognitive-related needs are 16%.

We asked claimants what was their primary source of payment for their previous month's charges. We also asked them about their secondary sources of payment. Table 3 summarizes results.

Long-term care insurance is not the primary payment source at admission to a nursing home or assisted living for most (70%) of these claimants. The insurance is only accessed at a later point either when individuals have completed their elimination period, or when individuals have reached a point of functional or cognitive decline that would allow them to access benefits from the policy. Depending on institutional setting, the insurance does become the primary payment source for between 70% and 80% of these claimants. What is not paid for by the insurance is typically funded from personal resources. Medicare is only a significant payment source for about one-third of nursing home residents, but only at initial admission. Within a few months, Medicare ceases to be a meaningful payer of services in the nursing home.

| TABLE 3. Primary and Secondary Payment Sources by Residence | ||||||

| Sources of Payment | Primary Payment Source at Admission | Primary Payment Source Last Month | Secondary Payment Sources Last Month | |||

| Nursing Home | Assisted Living | Nursing Home | Assisted Living | Nursing Home | Assisted Living | |

| LTC Insurance | 31% | 32% | 71% | 80% | 24% | 20% |

| Other private insurance | 1% | 5% | 1% | 1% | 6% | 6% |

| Own Income and Assets | 37% | 56% | 21% | 19% | 67% | 58% |

| Medicare | 28% | 4% | 2% | ---- | 3% | 4% |

| Other government | ---- | 2% | 2% | ---- | 2% | ---- |

| Other payment source | ---- | ---- | ---- | ---- | 1% | 3% |

| Don't know | 3% | 1% | 2% | 1% | 4% | 6% |

| SOURCE: 2000 National Claimant Study.NOTE: The percentages for the primary and secondary payment sources do not always sum to 100% because some indivduals do not know which is there primary and which is their secondary payment source. | ||||||

It is surprising that for roughly 30% of nursing home claimants, insurance is not their primary payment source. In most of these cases, the insurance benefit represents less than half of the daily charge associated with care. Additional analysis reveals that, in cases where insurance is not the primary payment source for nursing home claimants, the average daily benefit is lower, there is less likelihood of having a policy with inflation protection, and the difference between the daily charge and the daily benefit is greater. These individuals also tend to be somewhat more ADL impaired, are more likely to be cognitively impaired, and are less likely to be married.

F. Benefits paid under Insurance Contracts and Insurance Policy Designs

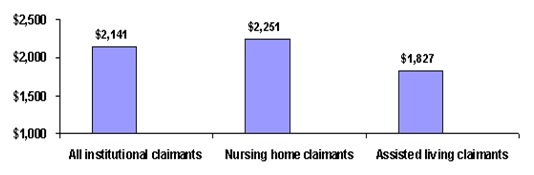

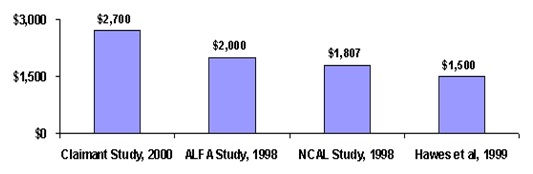

In these institutional settings, claimants are receiving significant amounts of care. Much of this care is paid for by insurance benefits. In fact, for more than 70% of claimants, insurance pays the majority of the costs of care. Figure 15 shows that the average monthly insurance benefit paid to claimants is $2,141. Monthly nursing home benefits are about 23% higher than assisted living benefits -- $2,251 versus $1,827.

These figures must be viewed with caution, because they are derived by taking the current claim's total dollar expenditure and dividing this by the amount of time that the individual was on claim. The total dollar expenditure is a function of submitted bills by the claimant or the institution. In some cases, claimants (or their families) may aggregate or hold bills for a few months before submitting them for payment to the insurance company. Given our method of calculation, we may actually underestimate the average monthly claim payment by residence. A completely accurate accounting would require us to focus on the experience of closed claims, something that is outside the scope of the current inquiry.

| FIGURE 15: Average Monthly Claims Payments by Residence |

|

| SOURCE: 2000 National Claimant Study. |

Not shown in the diagram is the fact that, as of the interview date, this sample of claimants had already used an average of $29,000 in insurance benefits per person -- $34,000 for nursing home residents and $16,000 for assisted living residents. Given that most of these individuals (60%) have policies covering four or more years of care at around $83 per day -- about $161,000 in available benefits -- these individuals have thus far used up about 18% of their benefits (see Table 4). There is greater variation in monthly benefit payments among assisted living residents than among nursing home residents. The range in average monthly benefit payments across the companies for nursing home care is from a low of $1,714 to a high of $2,722; for assisted living the range is between $1,207 and $2,575.

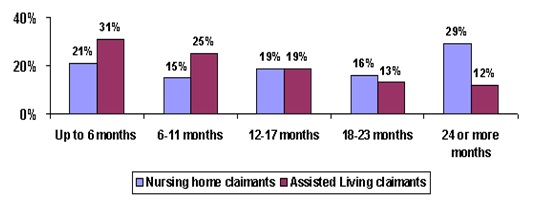

Most individuals have been on claim for about 17 months (see distribution in Figure 16). About 45% of nursing home residents have been receiving benefits for more than a year-and-a-half; the comparable figure for assisted living residents is 25%.

| FIGURE 16: Total Amount of Time on Claim by Residence |

|

| SOURCE: 2000 National Claimant Study. |

Table 4 summarizes the typical policy design features of this study's institutional claimants. In general, there are three types of benefit designs:

-

Indemnity model, which pays a fixed level benefit when an individual becomes disabled and long-term care expenses are incurred. The payment may be larger or smaller than the actual cost of services and bears no direct relationship to such expenses.

-

Reimbursement model, which reimburses costs of covered services for eligible individuals up to a maximum daily amount. In this model, insurance benefits are directly related to the incurred long-term care costs.

-

Disability model, which pays benefits directly to the insured when the individual becomes disabled, whether or not long-term care expenses are incurred. The insured has the freedom to spend the disability payment on whatever services he/she deems appropriate.

| TABLE 4. Policy Design Features for Institutional Coverage | |

| Policy Design Feature | Distribution |

| Payment Method | |

| Reimbursement | 85% |

| Indemnity | 14% |

| Disability | 1% |

| Institutional Care Daily Benefit Amount | |

| $50 | 14% |

| $51 to $74 | 26% |

| $75 to $99 | 22% |

| $100 to $124 | 33% |

| $125 or greater | 5% |

| Average | $83 |

| Institutional Care Coverage Duration | |

| 1 year | 3% |

| 2 year | 16% |

| 3 year | 20% |

| 4 year | 19% |

| 5 year | 7% |

| 6 year | 5% |

| Lifetime Coverage | 30% |

| Average | 5.3 Years |

| Elimination period | |

| 0 day | 26% |

| 1 - 20 days | 18% |

| 30 - 50 days | 15% |

| 60 - 90 days | 18% |

| 100 day | 23% |

| Average | 45 days |

| Percent with Inflation Protection | 45% |

| SOURCE: 2000 National Claimant Study.NOTE: Policies with lifetime coverage are assessed as covering 10 years of service costs. | |

The most conservative -- although from a claims standpoint less predictable -- of these policy designs is the reimbursement model. Almost all of the institutional care benefits in the policies held by these claimants are paid on a reimbursement basis (85%). Almost none of the institutional claimants in this sample have accessed benefits through a disability policy design. Almost all claimants have either a reimbursement or indemnity policy design.

The average daily benefit for institutional coverage in the sample is $83 and about two in five are eligible to receive over $100 per day in benefits for institutional care services. It is also noteworthy that 45% of the claimants have policies that include some level of inflation protection.

In terms of coverage duration, more than half of the claimants have policies that cover the equivalent of daily care for a five-year period. Such durational coverage should provide payments for the total duration of care for all but 15% of nursing home claimants.10 Given the lack of information about the average length of stay in assisted living, we cannot be certain that durations will cover most of these residents.

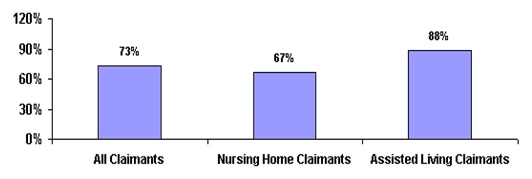

An important issue is the extent to which the daily benefit amount covers the daily cost of care. Figure 17 shows that among all claimants, an average of 73% of the long-term care liability is paid for by insurance. For nursing home claimants, 67% of the costs are covered, whereas for assisted living residents the average daily benefit pays for most of the incurred costs in this institutional setting.11 In terms of daily costs, this implies that the uncovered liability faced by nursing home residents is about $1,144 per month. The vast majority of individuals use their own income and assets to cover these costs.

| FIGURE 17: Ratio of Daily Benefit Amount to Daily Charges by Residence |

|

| SOURCE: 2000 National Claimant Study. |

G. Claimant Satisfaction with Insurance Policy and Insurance Company

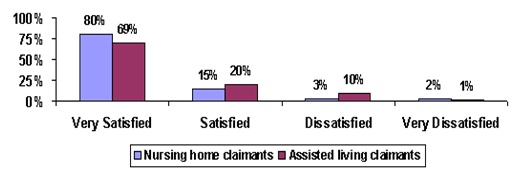

We asked claimants or their proxies a series of questions related to general satisfaction with their insurance policy as well as with various insurer claims management practices.12 The results are summarized in Figure 18. The vast majority of claimants are satisfied with their policy, with most being very satisfied. On the other hand, while relatively low, the proportion of assisted living claimants who are dissatisfied with their policy is more than double that for nursing home claimants. This difference is statistically significant at the .05 level.

| FIGURE 18: Satisfaction with Long-Term Care Insurance by Residence |

|

| SOURCE: 2000 National Claimant Study. |

Given the relatively complex nature of long-term care insurance contracts, an issue of concern to consumer groups and the industry alike is whether or not claimants actually understand what they are buying. Claimants/proxies were asked whether they had any problems understanding what was and was not covered by their policy. The vast majority (85%) had no difficulty understanding what their policy covered. There were no differences between nursing home and assisted living claimants. Nor were there significant differences across companies.

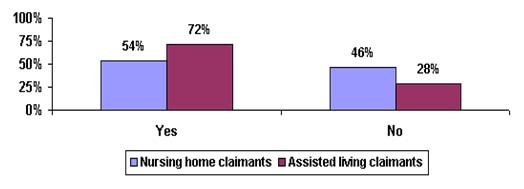

We asked claimants and their proxies whether the benefits paid by their insurance policy were sufficient to meet their care needs in the institutional setting. This question begins to focus on the issue of adequacy vis-à-vis benefit levels chosen by the insured. Figure 19 shows that roughly three in four assisted living claimants felt that the benefits were adequate, given their care needs. Over half of nursing home claimants considered their benefits enough to meet their care needs. The lower percentage of claimants in nursing homes who feel their benefits are adequate is not surprising, given that nursing home residents have a somewhat smaller proportion of their total costs covered by their insurance benefits.

| FIGURE 19: Are Policy Benefits Meeting Current Care Needs? |

|

| SOURCE: 2000 National Claimant Study. |