Eric Goplerud, Ph.D.

NORC at the University of Chicago

This report was prepared under contract between the U.S. Department of Health and Human Services (HHS), Office of Disability, Aging and Long-Term Care Policy (DALTCP) and NORC at the University of Chicago. For additional information about the study, you may visit the DALTCP home page at http://aspe.hhs.gov/office_specific/daltcp.cfm or contact the ASPE Project Officer, Kirsten Beronio, at HHS/ASPE/DALTCP, Room 424E, H.H. Humphrey Building, 200 Independence Avenue, SW, Washington, DC 20201. Her e-mail address is: Kirsten.Beronio@hhs.gov.

Acronyms

| ABA | applied behavioral analysis |

|---|---|

| ABD | adverse benefit determination |

| ASAM | American Society of Addiction Medicine |

| BLS | DOL Bureau of Labor Statistics |

| CBO | Congressional Budget Office |

| CHIP | Children's Health Insurance Program |

| CMS | HHS Centers for Medicare and Medicaid Services |

| DOL | U.S. Department of Labor |

| DRG | diagnosis-related group |

| E&M | evaluation and management |

| ECT | electroconvulsive therapy |

| EHB | essential health benefit |

| EOB | explanation of benefit |

| ER | emergency room |

| ERISA | Employee Retirement Income Security Act |

| FEHBP | Federal Employee Health Benefit Plan |

| GAO | U.S. Government Accountability Office (previously General Accounting Office) |

| HHS | U.S. Department of Health and Human Services |

| HRET | Health Research and Education Trust |

| IFR | Interim Final Rule |

| IOP | intensive outpatient program |

| IP INN MH | Inpatient In-Network Mental Health |

| IP INN SUD | Inpatient In-Network Substance Use Disorder |

| IP OON MH | Inpatient Out-of-Network Mental Health |

| IP OON SUD | Inpatient Out-of-Network Substance Use Disorder |

| KFF | Kaiser Family Foundation |

| MBHO | managed behavioral healthcare organization |

| MH | mental health |

| MHPAEA | Mental Health Parity and Addiction Equity Act |

| NAICS | North American Industry Classification System |

| NCS | National Compensation Survey |

| NQTL | non-quantitative treatment limitation |

| OOP | out-of-pocket |

| OP INN MH | Outpatient In-Network Mental Health |

| OP INN SUD | Outpatient In-Network Substance Use Disorder |

| OP OON MH | Outpatient Out-of-Network Mental Health |

| OP OON SUD | Outpatient Out-of-Network Substance Use Disorder |

| OP OV INN MH | Outpatient Office Visit In-Network Mental Health |

| OP OV INN SUD | Outpatient Office Visit In-Network Substance Use Disorder |

| OP OV OON MH | Outpatient Office Visit Out-of-Network Mental Health |

| OP OV OON SUD | Outpatient Office Visit Out-of-Network Substance Use Disorder |

| OP-Other INN MH | Outpatient-Other In-Network Mental Health |

| OP-Other INN SUD | Outpatient-Other In-Network Substance Use Disorder |

| OP-Other OON MH | Outpatient-Other Out-of-Network Mental Health |

| OP-Other OON SUD | Outpatient-Other Out-of-Network Substance Use Disorder |

| PBM | pharmacy benefits management |

| PCP | primary care physician |

| PDD | Plan Design Database |

| PHS Act | Public Health Service Act |

| PMPM | per member per month |

| PPACA | Patient Protection and Affordable Care Act |

| QTL | quantitative treatment limitation |

| RFI | Request for Information |

| RTF | residential treatment facility |

| Rx | prescription drug |

| SCP | specialty care physician |

| SMI | serious mental illness |

| SNF | skilled nursing facility |

| SPD | summary plan description |

| SUD | substance use disorder |

| UCR | usual, customary, and reasonable |

Introduction

The Paul Wellstone and Pete Domenici Mental Health Parity and Addiction Equity Act (MHPAEA) of 2008 was signed into law on October 3, 2008, and became effective for plan years beginning on or after October 3, 2009.6 For employers and group health insurance plans with more than 50 employees that offer coverage for mental illness and substance use disorders (SUDs), the law requires that coverage be no more restrictive than that for other medical and surgical procedures covered by the plan. MHPAEA does not require group health plans to cover mental health (MH) and SUD benefits, but when plans do cover these benefits, they must be covered at levels that are comparable to coverage levels for medical and surgical benefits offered by the plan. Specifically, MHPAEA renewed a preexisting requirement that employers and group health insurance plans eliminate more restrictive annual and lifetime dollar limits on MH coverage and MHPAEA added this requirement to SUD coverage as well. Furthermore, MHPAEA requires that employers and group health plans that provide both MH/SUD services and medical/surgical benefits ensure that:

The financial requirements applicable to such MH or SUD benefits are no more restrictive than the predominant financial requirements applied to substantially all medical and surgical benefits covered by the plan (or coverage), and there are no separate cost-sharing requirements that are applicable only to MH or SUD benefits.7

The treatment limitations applicable to such MH or SUD benefits are no more restrictive than the predominant treatment limitations applied to substantially all medical and surgical benefits covered by the plan (or coverage) and there are no separate treatment limitations that are applicable only to MH or SUD benefits.8

MHPAEA also includes requirements that group health plans make available information related to MH/SUD medical necessity criteria and reasons for any denials for MH/SUD services. If requested, medical necessity criteria must be provided to plan administrators (or offerors), potential participants, beneficiaries, and contracting providers. In addition, if requested, explanations of denials must be provided to participants or beneficiaries.9

After extensive public comment, the U.S. Department of Health and Human Services (HHS), the U.S. Department of Labor (DOL) and the Department of the Treasury released an Interim Final Rule (IFR)10 on February 2, 2010. The IFR provided guidance on the application of parity to financial, quantitative, and non-quantitative treatment limitations (NQTLs) and went into effect for plan years beginning on or after July 1, 2010. The IFR clarified several uncertainties:11

Deductibles and out-of-pocket limits. The IFR prohibited separately accumulating (separate but equal) financial requirements (e.g., deductibles) and quantitative treatment limitations (QTLs).

Separate coverage or benefits packages. Even though behavioral health benefits are sometimes carved out and administered by a separate insurer, each combination of plan offerings must have parity in behavioral health benefits when considered as a whole.

Financial requirements and quantitative treatment limitations (i.e., limits that can be expressed numerically as a dollar, a percentage, or number of visits or episodes). The compliance standard is that a particular type of financial requirement or QTLs (e.g., copays vs. coinsurance or limits on the number of outpatient visits) must apply to substantially all (i.e., at least two-thirds) of the medical/surgical benefits in a classification before it may be applied to MH/SUD benefits in that classification. If the requirement applies to at least two-thirds of all medical/surgical benefits in a classification, the permissible level of that financial requirement or treatment limit is set by determining the predominant level that applies to at least 50% of the medical/surgical benefits subject to that type of requirement or limit.

Non-quantitative treatment limitations (i.e., limits not expressed numerically that otherwise limit the scope or duration of benefits). NQTLs include but are not limited to medical management standards; prescription drug formulary designs; standards for provider admission to participate in a network; determination of usual, customary, and reasonable (UCR) amounts; requirements for using lower-cost therapies before a plan will cover more expensive therapies; and conditional benefits based on completion of a course of treatment. The IFR requires that any processes, strategies, evidentiary standards, or other factors used in applying an NQTL to MH or SUD benefits must be comparable to, and applied no more stringently than, the processes, strategies, evidentiary standards, or other factors used in applying the limitation to medical/surgical benefits, except to the extent that recognized clinically appropriate standards of care may permit a difference.

Classification of benefits. Six benefit classifications are specified in the IFR, with parity required for each: inpatient in-network, inpatient out-of-network; outpatient in-network; outpatient out-of-network; emergency care; and prescription drugs. On July 1, 2010, DOL released "safe harbor" guidance that allows for the creation of office visit and outpatient/other (non-office visit) sub-classes within the outpatient classifications of benefits.

Interaction with state insurance laws. MHPAEA does not supersede state parity law unless state law prevents the application of a MHPAEA requirement.

Availability of Plan Information. The IFR specifies that group plans governed by the Employee Retirement Income Security Act (ERISA) must follow the ERISA claims procedure regulations that provide, for example, that such reasons for claims denials must be provided automatically and free of charge. Other plans are encouraged to follow the ERISA requirements.

Application of the MHPAEA to Insurance and Health Plan Markets. Whether the MHPAEA applies to a particular insurance or health plan market depends both on whether the governing law applies its terms to the insurance market in question and on whether exemptions apply.12

ERISA-governed fully-insured group health benefit plans and ERISA-governed self-insured group health benefit plans. MHPAEA applies to all ERISA-governed group health plans and health insurance offered in connection with group health plans that offer coverage for both medical and surgical benefits and MH or substance abuse disorder benefits.13 MHPAEA also applies to group health plans and health insurance offered in connection with such plans in the non-ERISA market.14 Thus, MHPAEA applies to group health plans sponsored by private and public sector employers with more than 50 employees, including self-insured as well as fully-insured arrangements. MHPAEA also applies to health insurance issuers who sell coverage to employers with more than 50 employees. MHPAEA exempts small employers (i.e., employers having an average of 50 or fewer employees).15 Under the Patient Protection and Affordable Care Act (PPACA), the small employer exemption in the Public Health Service (PHS) Act is increased to 100 or fewer employees.16 DOL has determined that this upward revision in the PPACA of the size of small employer groups for PHS Act purposes does not affect ERISA-governed plans, whose small employer exemption remains at 50.17

State-regulated insurance products sold in the small group health or individual markets. HHS has proposed18 to incorporate the MHPAEA requirements into the essential health benefit (EHB) requirements for coverage of MH and SUD benefits under the PPACA.19 According to this interpretation, the MHPAEA compliance will be a required feature of all health insurance plans sold in the individual and small group markets starting in 2014.20

The state health insurance exchange market established under the PPACA. Because PPACA applies MHPAEA to all qualified health plans, health plans sold in state health insurance exchanges will be required to comply with federal parity requirements.

The Medicaid market, consisting of Medicaid fee-for-service, Medicaid managed care, Medicaid benchmark plans, and the separately administered Children's Health Insurance Program (CHIP) market. MHPAEA is incorporated by legislative reference into Medicaid, but only for certain forms of Medicaid coverage such as Medicaid Managed Care. MHPAEA also is incorporated by legislative reference into CHIP, although in states in which CHIP operates as a Medicaid expansion, the Medicaid expansion component of CHIP would be subject to Medicaid standards rather than to standards applicable to separately administered CHIP programs.21 MHPAEA also applies to Medicaid benchmark (a.k.a. alternative benefit plans) that will be offered by states that opt to extend Medicaid coverage to the low-income childless adult population as authorized by the PPACA.

The Medicare Market, including the fee-for-service market and the Medicare Advantage market. MHPAEA is not incorporated by reference into the Medicare statute. A limited provision aimed at removing Medicare's longstanding more restrictive treatment limitation for outpatient treatment of MH conditions was enacted into law by section 102 of the Medicare Improvements for Patients and Providers Act of 2008. This provision amended Medicare to phase out the law's historic outpatient MH treatment limitation over a 5-year period between 2010 and 2014.22 As the Centers for Medicare and Medicaid Services (CMS) notes in interpretive policies, this change means that beginning January 1, 2014, Medicare will pay 80% of the physician fee schedule for covered services and 80% of the encounter rate for covered treatments in federally qualified health centers and rural health clinics subject to their upper payment limit.23 With respect to the Medicare Advantage market, CMS interpretive regulations24 clarify that Medicare Advantage organizations offering special needs plans will be expected to comply with parity requirements. Whether the CMS definition of parity for Medicare Advantage Special Needs Plan purposes parallels that adopted in the IFR rule is not clear. MHPAEA does not apply to "stand alone" Medicare Advantage plans or Medicare fee-for-service plans.

Church plans. Because of their ERISA exemption, church plans are not affected by the MHPAEA's ERISA requirements. However, to the extent that an ERISA-exempt church purchases a product through a state health insurance exchange, or a state-regulated group insurance product governed by the PHS Act, the product would be subject to parity requirements, unless the church is otherwise exempt under state law.

Non-Federal Government health plans offered to state and local public employees. Non-Federal Government health plans are likewise ERISA-exempt, but their coverage would be subject to the MHPAEA's PHS Act provisions, whose scope reaches both the insurance market and non-Federal Government plans. At the same time, the law permits non-federally administered self-insured government health plans to opt out of these provisions.25

TriCare (the health program for uniformed service members, retirees, and their families) and the Federal Employee Health Benefit Plan (FEHBP). Although there is not a specific legislative requirement applying MHPAEA to the FEHBP program, these requirements do apply to the FEHBP through Executive Order and incorporation of these requirements into the purchasing and coverage standards issued by the Office of Personnel Management. MHPAEA does not generally apply to TriCare. The U.S. Department of Defense has not incorporated the MHPAEA's provisions into their purchasing and coverage standards.

Table 1 summarizes the applicability of the MHPAEA to 14 distinct insurance and health plan markets.

TABLE 1. Legal Application of the MHPAEA to 14 Distinct Public and Private Insurer/Employer-Sponsored Health Plan Markets

| Market | Yes/No |

|---|---|

| 1. ERISA-governed self-insured health benefit plans | Yes, MHPAEA and ERISA amendments apply; cost exemptions may apply, and size exemptions would apply in the case of small ERISA plans (fewer than 50 employees) that self-insure. |

| 2. ERISA-governed fully-insured health benefit plans | Yes, MHPAEA, PHS Act, and ERISA amendments apply; employer size and cost exemptions apply. |

| 3. State-regulated group and individual insurance markets | Yes, MHPAEA applies to health insurance issuers who sell coverage to employers with more than 50 employees and MHPAEA standards will extend to both the small group and individual markets through PPACA provisions and EHB requirements. |

| 4. Medicaid fee-for-service | No, CMS Medicaid standards apply. |

| 5. Medicaid managed care | Yes, CMS Medicaid managed care standards apply. |

| 6. Medicaid benchmark plans | Yes, CMS benchmark standards apply. |

| 7. Separately administered CHIP plans | Yes, MHPAEA standards apply. |

| 8. Medicare fee-for-service market | No, CMS Medicare standards apply. |

| 9. Medicare Advantage | No, CMS Medicare standards apply. |

| 10. State health insurance exchanges | Yes, MHPAEA standards apply. |

| 11. FEHBP | No, but FEHBP policies apply; FEHBP has explicitly adopted MHPAEA. |

| 12. TriCare | No, TriCare standards apply; MHPAEA not adopted. |

| 13. Church plans | No, churches are exempt from ERISA requirements, but PHS standards would apply to insured products unless churches have a state exemption. |

| 14. Non-federal public employee health benefit plans | Yes, covered by the MHPAEA's PHS Act provisions, but plan sponsors may opt out. |

MHPAEA Public Law 110-343.

See 75 Fed. Reg. 5410-5451 (February 2, 2010). See 45 C.F.R. §146.136(a) defining the scope of parity in relation to both qualitative and quantitative treatment limits.

Melek S. Implementing parity: Investing in behavioral health. Milliman Healthcare Reform Briefing Paper, May 20, 2010.

Rosenbaum SR, Goplerud EG, McDowell M, Jacobus-Kantor L, Melek S. Mental Health and Addiction Treatment Parity Across Public and Private Insurance Markets: An Analysis of Federal Laws. Presented to the Office of the Assistant Secretary of Planning and Evaluation, July 2012.

29 U.S.C. §1185a(a)(3).

42 U.S.C. §330(g)(2).

29 U.S.C. §1185a(c)(1).

42 U.S.C. §300gg-91(e)(4) as applied to MHPAEA by PPACA §1563(c)(4).

See U.S. Department of Labor, FAQs about Affordable Care Act Implementation Part V and Mental Health Parity Implementation, Q. 8. Available at: http://www.dol.gov/ebsa/faqs/faq-aca5.html. Accessed May 5, 2012.

Patient Protection and Affordable Care Act: Standards Related to Essential Health Benefits, Actuarial Value, and Accreditation; Proposed rule, 77 Fed. Reg. 70644-70677 (amending 45 CFR Parts 147, 155, and 156) (November 26, 2012).

42 U.S.C. §18022, added by PPACA §1302.

42 U.S.C. §300gg-6(a).

42 U.S.C. §1397cc(c)(6).

Social Security Act §1833(c)(1), 42 U.S.C. §1395l(c)(1).

CMS Manual System Pub. 100-02, Transmittal 114, Medicare Benefit Policy.

76 Fed. Reg. 54600, 54605 (September 1, 2011).

PHS Act §2722(a)(2), 42 U.S.C. §300gg-21(a)(2).

Brief Review of the Existing Literature

Necessity of Compliance Testing. The history of parity legislation shows that implementation of requirements in this area is not always straightforward and ensuring equitable treatment of MH and SUD treatment is often complicated. Experience with implementation of the Mental Health Parity Act of 199626 is a case in point. The 1996 Act mandated elimination of unequal annual and lifetime dollar limits on MH coverage in employer-sponsored and group health insurance plans. Compliance monitoring found that most health plans complied by eliminating dollar limits but increased restrictions on the number of hospital days or outpatient visits for MH services.27 Findings reported by the U.S. Government Accountability Office (GAO) are representative. Of 863 employer plans responding to its 1999 survey:

- 14% of employers had not complied with the law by 1999.28

- 51% reduced the number of outpatient visits covered.

- 36% reduced hospital days covered.

- 20% increased outpatient visit copayments.

- 18% increased the cap on enrollee out-of-pocket costs.29

Research studies focusing on implementation of previous parity requirements such as those applied to FEHBP can complement our other sources of information and enhance our understanding of the impact of MHPAEA.

FEHBP Parity. Monitoring of FEHBP parity implementation30, 31 revealed that all FEHBPs complied with parity, that no plan reported major problems implementing parity, and that no plan left the program to avoid implementing the policy. Plans enhanced their pre-parity MH/SUD benefits as required by the policy change (84% enhanced MH, 75% enhanced SUD benefits)32 and were more likely to carve-out the behavioral health benefit. Other expected changes (e.g., increased gate keeping at the primary care provider level, reduced provider networks, concurrent or retrospective review, use of disease management programs for MH/SUD care, and increased financial risk sharing) occurred infrequently.

Evaluations of FEHBP parity found no significant increase in total behavioral health spending. Nor did evaluations find an increased probability of any MH/SUD service utilization resulting from parity.33 In fact, the quantity of MH/SUD services patients received may have decreased slightly after parity was introduced. A recent study by Goldman and colleagues found that beneficiaries in plans that were subject to FEHBP parity demonstrated larger reductions in overall behavioral health visits, medication management visits, psychotherapy visits, and prescriptions for behavioral health medications (which the authors assume resulted from increased use of utilization management techniques by plans) following the introduction of parity than did a matched comparison group not subject to FEHBP parity.34 However, introduction of FEHBP parity was associated with a significant decrease in out-of-pocket spending for MH/SUD services.35, 36, 37

A separate study of the impact of parity on substance abuse treatment in FEHBP plans found that although the rate of out-of-pocket spending declined significantly for substance abuse treatment and more patients had new diagnoses of a SUD, there were no differences in rates of initiation and engagement in treatment under parity and total plan spending per user and average utilization of substance abuse services did not change.38

Researchers have examined the effects of FEHBP parity on specific populations, services, and diagnoses. A recent study examined utilization and costs for individuals having one of three diagnoses representing a continuum of condition severity: bipolar disorder, which was classified as both severe and chronic in nature; major depression, whose severity and chronicity vary considerably in the population; and adjustment disorder, which was classified as a less severe, non-chronic condition.39 Results suggested that, compared to a matched control group, enrollees having each of these conditions demonstrated no significant changes in utilization associated with medication management, inpatient days, or prescriptions following the implementation of parity. In the adjustment disorder group, there was a small, but statistically significant, reduction in psychotherapy utilization. Additional analyses revealed no changes in total behavioral health spending for individuals with bipolar disorder or major depression and small decreases in spending associated with individuals diagnosed with adjustment disorder.40 Out-of-pocket spending related to MH/SUD treatment decreased across all three diagnostic categories vs. the matched control group.

Another recent study of FEHBP parity attempted to identify specific subpopulations of beneficiaries who benefited most from the introduction of parity. Applying growth mixture modeling techniques to FEHBP data, Neelon and colleagues concluded that the effects of parity differed depending on an individual's pre-parity utilization patterns. Three distinct subgroups emerged: "low-spenders," (who had low levels of utilization of MH/SUD services in the pre-parity period) -- their utilization of MH/SUD services declined in the post-parity period; "moderate-spenders," (who had moderate pre-parity spending) -- their spending increased following the implementation of parity; and "high-users," (who had high MH/SUD spending during the pre-parity) -- their spending continued to be high in the post-parity period.41 Another study found that among enrollees who received MH treatment for a severe mental illness (e.g., schizophrenia, bipolar disorder, depression), the odds of using any MH/SUD services in subsequent years were more than 1.3 times greater than two matched control groups.42 The relative odds of using inpatient MH/SUD services in the parity group were 0.67 times that of the control groups, a decrease consistent with the hypothesis that managed care organizations might have guided patients toward more outpatient services in treating their severely ill enrollees. Prescription usage under parity appears to have increased. Individuals covered under FEHBP parity were 1.4 times more likely to fill any behavioral health prescription compared to their non-FEHBP counterparts. An analysis of the impact of FEHBP parity on rates of treatment for depression found no significant changes in rates of diagnosis of depression following introduction of parity and very little change in measures of the quality of care.43

Several additional evaluations of FEHBP parity have focused on the effects of the program on children and adolescents. Azrin and colleagues concluded that, following the introduction of FEHBP parity, children enrolled in the FEHBP program showed no significant increase in MH/SUD utilization compared to a matched control group.44 These findings are consistent with analyses of the impact of state parity laws that show no significant impact on access for children and adolescents.45 In evaluating only children and adolescents with high MH/SUD expenditures in the pre-parity period, a recent study concluded that compared to a matched control group, children enrolled in the FEHBP showed similar patterns of MH/SUD expenditures following the introduction of parity, but a statistically significant reduction (approximately $258 in 2011 dollars) in average out-of-pocket spending associated with MH/SUD services.46

In general, these studies of FEHBP parity found no significant increases in overall MH/SUD utilization rates, initiation or engagement rates, or total MH/SUD spending following the implementation of parity but significant decreases in out-of-pocket costs did result.

Vermont. Compliance monitoring of the MHPAEA can also be guided by the findings of studies examining the effects of state-level parity, such as Vermont.47 The Vermont Parity Act took effect January 1, 1998.48 The Vermont legislation mandated group health insurance to cover MH/SUD treatment equitably with other covered medical treatments (ERISA-governed self-insured plans are exempt from state parity legislation). An evaluation of the law's effects found an increased probability of an individual receiving any outpatient MH services and a decreased likelihood of an individual receiving any substance abuse services following the introduction of parity. The percentage of beneficiaries receiving outpatient MH services increased by a range of 6%-8%. The percentage of individuals receiving any substance abuse services decreased by a range of 16%-29%.49 Results also indicated that, in general, consumer cost-sharing for MH and substance abuse treatment services declined, from 27% to 16% of total costs, following the implementation of parity. The evaluation of the Vermont law's effects found little evidence that the introduction of parity resulted in employers dropping health coverage or switching to self-insured plans to avoid complying with the regulation. Only 0.3% of Vermont employers reported that they dropped health coverage for their employees primarily due to the parity law, and only 0.1% of employers reported that parity played a role in their decision to self-insure (to avoid complying with state law).50

Use of managed care techniques increased following Vermont's implementation of parity. Although one of the two major health plans already used managed care before the implementation of parity, the other health plan also shifted most of its members to a managed behavioral health care carve-out. In one plan, spending increased modestly by 19 cents per member per month (PMPM). Nonetheless, MH/SUD services accounted for only 2.5% of total spending in that plan after parity compared to 2.3% before parity. The other plan experienced a 9% decrease in spending for MH/SUD services following implementation of the state parity law. This decrease in spending was largely attributed to a decrease in SUD treatment service utilization.

Employers' knowledge of the parity law remained low, even after its implementation. A survey conducted 2 years after the implementation of parity suggested that approximately 50% of all fully-insured employers in Vermont had never heard of the parity law and that nearly three-fifths of all employers had little to no knowledge of the parity law.51 Small and medium-sized businesses were least likely to be familiar with the law, with approximately 70% of those employers having little to no knowledge of the law. Although the two major health plans in Vermont complied with the law on paper, lack of information, confusion, and mistakes by the state's largest plan generated complaints from beneficiaries and providers that led to changes in administration and consumer education in succeeding years.52

Oregon. Oregon's parity law, implemented January 1, 2007,53 mandated that group health insurance plans provide coverage for MH and substance abuse treatment services at the same level as other medical conditions. Results from Oregon are particularly informative for the current project in that the Oregon law, like the MHPAEA, went beyond the regulation of financial and QTLs and specified that plans cannot utilize unequal, NQTLs for MH and substance abuse treatment services compared to medical/surgical services. A recent analysis of the Oregon law suggested that each of the four plans studied made substantial changes to their MH and substance abuse treatment benefits following the implementation of parity. Each plan removed coverage limits related to inpatient and outpatient MH/SUD treatment services. After implementation of the NQTL provisions in the Oregon law, the use of management techniques stayed the same or decreased in the insurance plans studied. These changes were made without significant increases in total MH/SUD treatment spending. Importantly, the researchers found that these effects were achieved without the increased use of utilization management techniques.54 The authors also found no evidence of meaningful change in the rates of any behavioral health care service use.

In a separate analysis of only substance use spending, McConnell55 found that expenditures for alcohol treatment services increased significantly and spending on other drug abuse treatment services did not. The introduction of parity was associated with a small, but not statistically significant, increase in overall substance use treatment spending. In another study analyzing the impact of parity in Oregon on access to various behavioral health specialists, McConnell found that parity was associated with a slight increase (from 0.5% to 0.8%) in behavioral health treatment initiations with masters-level specialists, and relatively few changes for generalist physicians, psychiatrists, and psychologists. Patients were particularly sensitive to distance for non-physician specialists:56 the greater the distance between an individual and a non-physician specialist, the less likely that individual was to receive treatment. Following the introduction of parity, distance to the nearest psychiatrist, masters-level therapist, or psychologist tended to decrease.

California. California's Mental Health Parity Bill, which became effective on July 1, 2000, mandated that all group and individual health plans offer MH coverage as part of their overall health benefits and outlawed the use of MH treatment limitations and cost-sharing requirements that were more restrictive than those for physical health conditions.

The law required that health plans provide MH services to seriously mentally ill (SMI) adults and all children with serious emotional disturbances. Nine specific SMI diagnoses were included in the mandate: anorexia nervosa, bulimia nervosa, bipolar disorder, major depression, obsessive-compulsive disorder, panic disorder, pervasive developmental disorder/autism, schizophrenia, and schizoaffective disorder. SUDs were not covered by the California Parity Act. To assess health plan compliance with the Mental Health Parity Bill, the California Department of Mental Health undertook an intensive review of health plans that included an onsite survey, reviews of claims files, utilization review files, and internal management and performance reports. The report identified several areas of non-compliance. Six out of seven California plans that were subject to the legislation were incorrectly denying coverage for emergency room (ER) visits; five out of seven plans were failing to monitor whether beneficiaries had reasonable access to after-hours services; and five out of seven plans failed to include required information in claim denial letters.57

Trends in MH/SUD Spending and the Costs of Parity. An analysis by Mark and colleagues examined trends in behavioral health spending between 2001 and 2009 for a sample of over 100 large, self-insured employer plans. Results concluded that the average contribution of behavioral health care spending to total health care spending across each of the years examined was 0.3%, and only 2% of employers experienced a rate increase of more than 1% per year attributable to behavioral health costs.58

Given the small contribution of behavioral health care costs to overall health care costs, MHPAEA is expected to result in only very modest increases total health care expenditures. The Congressional Budget Office (CBO) estimated that MHPAEA itself would result in very modest cost increases, approximately 0.4%, in employer-sponsored group health care premiums and 0.2% in Medicaid payments to managed care plans.59 Recent analyses by Mark and colleagues utilizing MarketScan data are consistent with the CBO's estimate. Their analyses have suggested that an overwhelming majority of privately insured beneficiaries who utilized behavioral health care benefits in the pre-parity era did so at a rate that was far below pre-parity health care limits.60 Using econometric models to estimate the detailed effects of the MHPAEA on high-utilization beneficiaries who are likely to use its expanded coverage, these researchers estimated that the MHPAEA will likely increase total health care costs by 0.4%.

Early MHPAEA Compliance Analysis. In November 2011, GAO issued an early report on MHPAEA compliance in response to a statutory requirement.61 One hundred sixty-eight employers responded to a GAO survey asking detailed questions about changes in their behavioral health benefits between 2008 and 2010/2011 out of 707 employers who received the survey. Although the findings from this survey are not generalizable given the response rate of 24%, the survey did generate information on some questions regarding diagnoses covered not addressed in other studies. The vast majority of responding employers offered MH/SUD coverage in both 2008 and in 2010/2011, and most employers reported covering the same broad range of MH/SUD diagnoses in their current plan year as they also did in 2008. The remaining employers reported including more broad diagnoses.

In keeping with findings in other studies, employers responding to the GAO survey reported reducing their use of MH/SUD office visit and inpatient day limitations. In 2008, a significant percentage of these employers reported utilizing office visit limitations for SUDs. In 2010/2011, far fewer of these employers reported having such limitations. Likewise, in 2008, a significant percentage of employers reported utilizing limitations on inpatient days related to behavioral health conditions. By 2010/2011, the percentage of employers reporting using such limitations had dropped. The GAO did not assess NQTLs used by employers and health plans. While the results of the GAO survey should be interpreted with caution due to its small sample size and low response rate, the results from the survey suggest that employers were generally able to implement changes required by MHPAEA with little disruption to the insurance market.

P.L. 104-204.

Allen KG. Mental Health Parity Act: Employers' mental health benefits remain limited despite new federal standards. Testimony before the Committee on Health, Education, Labor and Pensions, U.S. Senate. Washington, DC: General Accounting Office, May 18, 2000. (Document no. GAO/T-HEHS-00-113.)

Burnam MA, Escarce JJ. Equity in managed care for mental disorders. Health Aff. 1999; 18:22-31.

Hennessy KD, Goldman HH. Full parity: Steps toward treatment equity for mental and addictive disorders. Health Aff. 2001; 20:58-67.

Allen KG. Mental Health Parity Act: Employers' mental health benefits remain limited despite new federal standards. Testimony before the Committee on Health, Education, Labor and Pensions, U.S. Senate. Washington, DC: General Accounting Office, May 18, 2000. (Document no. GAO/T-HEHS-00-113.)

Goldman HH, Frank RG, Burnam A et al. Behavioral health insurance parity for federal employees. N Engl J Med. 2006; 354:1378-1386.

Lichtenstein C et al. Evaluation of parity in the Federal Employees Health Benefits (FEHB) program: Final Report. Presented to the U.S. Department of Health and Human Services Administration, Office of the Assistant Secretary Planning and Evaluation, 2004. Available at: http://aspe.hhs.gov/daltcp/reports/parity.htm.

Goldman HH, Frank RG, Burnam MA et al. Behavioral health insurance parity for federal employees. N Engl J Med. 2006; 354:1378-1386.

Goldman HH, Barry CL, Normand ST, Azzone V, Busch AB, Huskamp HA. Economic grand rounds: The price is right? Changes in the quantity of services used and prices paid in response to parity. Psychiatr Serv. 2012; 63:107-109.

Goldman HH, Frank RG, Burnam MA et al. Behavioral health insurance parity for federal employees. N Engl J Med. 2006; 354:1378-1386.

Azrin ST, Huskamp HA, Azzone V, et al. Impact of full mental health and substance abuse parity for children in the Federal Employees Health Benefits Program. Pediatrics 2007; 119:452-459.

Azrin ST, Huskamp HA, Azzone V et al. Impact of full mental health and substance abuse parity for children in the Federal Employees Health Benefits Program. Pediatrics 2007; 119:452-459.

Azzone V, Frank R, Normand S, Burnam A. Effect of insurance parity on substance abuse treatment. Psychiatr Serv. 2011; 62:129-134.

Busch A, Yoon F, Barry C et al. The effects of parity on mental health and substance use disorder spending and utilization: Does diagnosis matter? Am J Psych. In press.

Busch A, Yoon F, Barry C et al. The effects of parity on mental health and substance use disorder spending and utilization: Does diagnosis matter? Am J Psych. In press.

Neelon B, O'Malley AJ, Normand ST. A Bayesian two-part latent class model for longitudinal medical expenditure data: Assessing the impact of mental health and substance abuse parity. Biometrics 2011; 67:280-289.

Yoon FB, Huskamp HA, Busch AB, Normand ST. Using multiple control groups and matching to address unobserved biases in comparative effectiveness research: An observational study on the effectiveness of mental health parity. Stat Biosci. 2011; 3:63-78.

Huskkamp HA. The impact of parity on major depression quality in the Federal Employees Health Benefit Program. Med Care 2006; 44:506-512.

Azrin ST et al. Impact of full mental health and substance abuse parity for children in the Federal Employees Health Benefits Program. Pediatrics 2007; 119:452-459.

Barry CL, Busch SH. Caring for children with mental disorders: Do state parity laws increase access to treatment. J Ment Health Policy Econ. 2008; 11:57-66.

Azrin ST et al. Impact of full mental health and substance abuse parity for children in the Federal Employees Health Benefits Program. Pediatrics 2007; 119(2):452-459.

Rosenbach M, Lake T, Young C et al. Effects of the Vermont Mental Health and Substance Abuse Parity Law. DHHS Pub. No. (SMA) 03-3822. Rockville, MD: Center for Mental Health Services, Substance Abuse and Mental Health Services Administration, 2003.

Vermont State Legislature. (2000) Section 4089, Mental Illness. Available at http://www.leg.state.vt.us/statutes/titles08/chap107.htm.

Rosenbach M, Lake T, Young C et al. Effects of the Vermont Mental Health and Substance Abuse Parity Law. DHHS Pub. No. (SMA) 03-3822. Rockville, MD: Center for Mental Health Services, Substance Abuse and Mental Health Services Administration, 2003.

Rosenbach M, Lake T, Young C et al. Effects of the Vermont Mental Health and Substance Abuse Parity Law. DHHS Pub. No. (SMA) 03-3822. Rockville, MD: Center for Mental Health Services, Substance Abuse and Mental Health Services Administration, 2003.

ORS 743.556; OAR 830-053-1404, 1405, 1325, 1330; SB 1.

McConnell KJ, Gast SH, Ridgely MS et al. Behavioral health insurance parity: Does Oregon's experience presage the national experience with the Mental Health Parity and Addiction Equity Act? Am J Psychiatry. 2012; 169:31-38.

McConnell KJ, Ridgely MS, McCarty D. What Oregon's parity law can tell us about the federal Mental Health Parity and Addiction Equity Act and spending on substance abuse treatment services. Drug Alc Depend. 2012; 124:340-346.

McConnell KJ, Gast SH, McFarland BH. The effect of comprehensive behavioral health parity on choice of provider. Med Care. 2012; 50:527-533.

California Department of Managed Health Care. Mental Health Parity in California. Mental Health Parity Focused Survey Project: A Summary of Survey Findings and Observations. Available at: http://www.hmohelp.ca.gov/library/reports/med_survey/parity/sfor.pdf.

Mark TL, Vandivort-Warren R, Miller K. Mental health spending by private insurance: Implications for the Mental Health Parity and Addictions Equity Act. Psych Serv. 2012; 63(4):313-318.

Congressional Budget Office. Congressional Budget Office Cost Estimate: S558. March 20, 2007.http://www.cbo.gov/sites/default/files/private/cbofiles/ftpdocs/78xx/doc7894/s558.pdf.

Mark TL, Vandivort-Warren R, Miller K. Mental health spending by private insurance: Implications for the Mental Health Parity and Addictions Equity Act. Psych Serv. 2012; 63(4):313-318.

For its 2012 parity study, the GAO surveyed a stratified random sample of 707 small, medium, large, and very large employers about the MH/SUD covered in their health plans that covered the greatest number of lives for the most current plan year -- either 2011 or 2010 -- as well as for 2008. A total of 168 employers submitted usable survey responses, for a response rate of 24%. It may be difficult to generalize from this sample to the universe of employers and health plans subject to MHPAEA and the IFR.

Study Background and Purpose

Project Objective. NORC at the University of Chicago led a research team that included Milliman Inc., Aon Hewitt, Thomson Reuters/Truven Health Analytics, and George Washington University to perform an analysis of compliance with the MHPAEA and the IFR62among ERISA-governed employer-sponsored group health plans and health insurance coverage offered in connection with such group health plans. Our analysis includes information from a variety of existing and complementary data sources. Information on coverage provided by large health plans and insurers was provided by testing databases compiled by both Milliman Inc. and Aon Hewitt as well as data from Aon Hewitt's Plan Design Database (PDD) which contains more than 10,000 unique plan designs for more than 300 employer clients. Taken together, information from these sources was used to track health plan coverage in this market and estimate changes in coverage that apply to the 111 million covered lives that are included in this large employer market. Health plan offerings provided by midsized establishments was assessed using information from Summary Plan Descriptions (SPDs) of midsized establishments obtained from the DOL Bureau of Labor Statistics (BLS). Information from the BLS SPDs was used to track changes in health plan coverage that apply to approximately 39 million lives that are covered in the midsized market. Additional information on both markets was provided by published and unpublished data from national employer health benefits surveys conducted by the Kaiser Family Foundation and Health Research and Educational Trust (KFF/HRET)63 and Mercer.64 To assess plan responses to the MHPAEA's disclosure requirements, semi-structured interviews were conducted with a small number of health plan representatives who were responsible for their plans' compliance with MHPAEA.

Table 2 presents the study's key research questions and the data sources used to address each question.

TABLE 2. Key Research Questions and Data Source Used to Address Each Question

| Research Question | Data Sources |

|---|---|

| 1. What types of financial requirements (e.g., copays, coinsurance) do group health plans use for MH and SUD benefits, and are such requirements consistent with the new MHPAEA standards for calculating the predominant level that applies to substantially all medical and surgical benefits? |

|

| 2. What types of QTLs (e.g., day limits, visit limits) do group health plans use for MH and substance use conditions, and are such limitations consistent with the MHPAEA standards? |

|

| 3. What types of NQTLs are commonly used by plans and issuers for MH and/or substance abuse disorders and how do these compare to NQTLs in place for medical/surgical benefits? |

|

| 4. Are group health plans and insurers using separate deductibles for MH and/or SUD benefits? |

|

| 5. Have financial requirements and treatment limits on medical/surgical benefits become more restrictive in order to achieve parity (instead of requirements and limits for MH and substance use becoming less restrictive)? |

|

| 6. How many plans have eliminated MH and/or substance abuse treatment coverage altogether instead of complying with the MHPAEA? |

|

| 7. How have plans responded to the MHPAEA's requirements regarding the disclosure of medical necessity criteria and reasons for claim denials? |

|

See 75 Fed. Reg. 5410-5451 (February 2, 2010). See 45 C.F.R. §146.136(a) defining the scope of parity in relation to both qualitative and quantitative treatment limits.

KFF/HRET annually surveys a random, stratified sample of employers to assess year-to-year changes in health benefits. Employers are stratified by industry and employer size. For the most recently completed annual survey -- conducted from January 2010 to May 2010 and published in September 2010 -- 2,046 employers responded to the full survey, a 47% response rate.

Mercer surveys a stratified random sample of employers annually through mail questionnaires and telephone interviews. Mercer selects a random sample of private sector employers from a Dun & Bradstreet database, stratified into eight categories, and randomly selects public sector employers -- state, county, and local governments -- from the Census of Governments. A total of 2,833 employers responded to the 2010 survey. By using statistical weights, Mercer projected its results nationwide and for 4 geographic regions. The Mercer survey report contains information for large employers -- those having >500 employees -- and for categories of large employers with certain numbers of employees as well as information for small employers -- those having fewer than 500 employees. Mercer used the same methodology for its 2008 survey, which was published in 2009.

Overview of Key Data Sources and Methodologies

Milliman Compliance Testing Database. Information from Milliman's MHPAEA compliance testing database was used to evaluate 2010 plan design data for adherence to MHPAEA standards. This database includes detailed quantitative financial requirements and treatment limitations for post-parity, pre-IFR benefit levels for medical/surgical benefits and MH/SUD benefits. It also contains details regarding any NQTLs when they could be identified through SPDs.

Of approximately 1,500 plans available in the database, 124 were analyzed to obtain an unbiased and representative distribution of large group plans by geographic region and industry, including self-insured and fully-insured plans. To obtain sufficient information for testing, detailed plan documents and benefit descriptions were requested to identify any financial requirements or treatment limits by detailed service category. To test plan designs for adherence to the quantitative aspects of the legislation, we utilized Milliman's testing model that completes the "substantially all" and "predominant" tests described in the IFR for quantitative financial requirements and treatment limitations. The actuarial-based model relies on Milliman's Health Cost Guidelines for health plans or employers whose membership is not large enough to be statistically reliable, and it includes specific adjustments for variables that impact health care costs such as geographic area, provider contract arrangements, and degree of health care management. If the health plan's or employer's membership was large enough to be statistically reliable (typically more than 10,000 members), the compliance testing model was based on the health plan's or employer's claim costs, usually on a book-of-business basis.

If plan or group-specific costs were used, detailed health care cost data for the most recent complete plan year were requested from the health plan or offeror. Either total allowed dollars or allowed dollars on a PMPM basis were acceptable. Participating health plans and plan sponsors were provided with a template for the level of detail requested by service category, which align with the service categories in Milliman'sHealth Cost Guidelines. Approximately 50 different medical/surgical categories are included.

Quantitative testing was performed on an allowed claim dollar basis (before application of any financial requirements). After the testing model was set up with the costs by detailed health care service category, each medical/surgical service category is mapped into one of the six classifications as prescribed by the IFR, including the two outpatient sub-classifications. Detailed financial requirements and treatment limits by service category were then entered into the model and calculations were performed to determine which quantitative financial requirements (deductibles, coinsurance, copays, and so forth) and treatment limitations (calendar year limits, lifetime limits, other quantity limits, and so forth) meet the "substantially all" criteria required by the IFR. For those quantitative financial requirements and treatment limitations that met this test, the "predominant" level was identified. The results identified the benefit plan changes that are necessary in each benefit classification to be consistent with MHPAEA requirements. To confirm that the MH and SUD coverage was complete in all classifications, covered MH and SUDs were reviewed to determine if coverage is provided in all classifications where medical/surgical benefits are provided.

When a scope of service issue (such as the exclusion of residential treatment for substance use rehabilitation) was identified, it was discussed with the health plan or plan sponsor as being currently acceptable under the IFR, but potentially capable of becoming non-compliant if rules on required scope of services are enacted. In addition to the quantitative testing, detailed plan documents were reviewed to identify potential compliance problems with NQTLs. The IFR is less specific regarding where the line for non-compliance is drawn for NQTLs. Different interpretations exist among health plans and employers on what is allowable and compliant. Plan documents often contain details for some, but not all, NQTLs. Sometimes, information can be found on precertification requirements, step therapies, prescription drug formulary design, and conditioning benefits on the completion of a course of treatment. When this information is in the plan documents, we determined whether it appeared that the plan applied them in a "comparable" manner and in a manner "no more stringently" than those applied to medical/surgical benefits.

Aon Hewitt Compliance Testing Database. Aon Hewitt plan designs were reviewed to assess compliance with MHPAEA and the IFR standards. The plan design review and compliance testing was conducted in 2010, based on the plan designs each employer expected to implement in the 2011 plan year.

The Aon Hewitt testing database encompasses plan designs from more than 60 employers, ranging in size from 400 to more than 300,000 employees and representing 230 plan options. Each plan option represented a single combination of benefits (a combination of medical/surgical and MH/SUD benefits) that is available to an employer's participants. Plans whose adherence could not be assessed through a review of summary plan documents were subjected to detailed testing procedures. Of the 230 plan options reviewed, 140 required detailed testing to determine the benefit design that would apply to MH/SUD benefits. Plans that used identical coverage criteria for both MH/SUD and medical surgical services were considered to adhere to MHPAEA standards, and did not required detailed testing.

For most employer plans, the benefit type and level within the inpatient in-network and out-of-network, outpatient out-of-network, prescription drug, and emergency care classifications were consistent for both medical/surgical and MH/SUD and, as a result, demonstrated consistency with the parity regulations. For these benefit classifications, detailed testing was not required. Benefit design for the outpatient in-network classification, however, most frequently required detailed testing across employer programs. Within this classification, employer programs typically applied a variety of benefit types (copay or coinsurance) and benefit levels (primary care, specialty care, other). Detailed testing was required within this benefit classification to determine whether benefits met the "substantially all" and "predominant" requirements for MH/SUD services.

For each plan option requiring detailed testing, Aon Hewitt requested the employer's program administrator (vendor) to submit plan costs associated with each covered service category within the classification or sub-classification included in the testing process.

We first conducted the "substantially all" test for each plan option to determine which benefit type represents at least two-thirds of the plan costs in the benefit sub-classification. Plan cost data were grouped according to benefit type (e.g., copay, coinsurance, etc.) and were evaluated to determine the percentage of the total plan costs represented by each type. Once the benefit type representing "substantially all" was determined, we grouped the plan cost data associated with each benefit level (e.g., $15, $20, etc.) within that benefit type to determine the predominant benefit level in that sub-classification.

Aon Hewitt's Plan Design Database. Information obtained from Aon Hewitt's PDD included a review of 2009, 2010, and 2011 plan design data to determine how group health plan and employer-sponsored plan designs have evolved since federal parity was enacted in 2008. The information contained in the PDD allowed us to report on the plan designs that were in place before the implementation of federal parity in 2009 and evaluate how plan designs have changed since the implementation of the MHPAEA and the IFR. For most employers, the MHPAEA legislative requirements were implemented effective January 1, 2010. Further changes were made to employer plan designs effective January 1, 2011, to comply with the February 2010 IFR.

Information obtained from the database allows us to evaluate trends in how employer plan designs have changed since the implementation of the MHPAEA. The 2009 plan year serves as the baseline year, as the MHPAEA was not in effect until October 2009. Plan options in the 2010 plan year reflect plan designs that were in effect after the implementation of the MHPAEA. The plan options included in the 2011 plan year reflect plan designs that were in effect after the release of the IFR, which went into effect for most employers on January 1, 2011.

A total of 12,384 plan options, reflecting 252 employers, were included in the 2009, 2010, and 2011 plan design analysis. Of those options, 2,983 plan options (24.1%) were in the database in all three plan years. Not all plan options are reflected in the database all 3 years for a number of reasons, such as the option was terminated or the option was added in 2010 and 2011.

For many plan options, information on all fields included in this review was available. However, for some plan options certain information was unavailable, the information was unclear, or the information was potentially inaccurate. Therefore, the data for those plan options were excluded from our analyses. Therefore, although 12,384 plan options were included in the database, the actual number of plan options considered valid and used in the analysis for each comparison is much lower. We have reported the size of the sample included in each plan design analysis in Appendix C.

Summary Plan Description Data Provided by BLS. To supplement parity information from large employers that are heavily represented in the Aon Hewitt and Milliman databases, we analyzed a sample of 240 SPDs from midsized employers (establishments between 51 and 500 employees) collected by the BLS between 2008 and 2011 as part of the National Compensation Survey (NCS).65 Under ERISA, employers are required to provide their employees with SPDs of their health, pension, and welfare benefit plans. SPDs must include:

- Any cost-sharing provisions, including premiums, deductibles, coinsurance, and copayment amounts.

- Any annual or lifetime maximums or other limits on benefits.

- The extent to which preventive services are covered.

- Whether and under what circumstance existing and new drugs are covered.

- Whether, and under what circumstance, coverage is provided for medical tests, devices or procedures.

- Any provisions requiring preauthorization or utilization review as a condition of obtaining a benefit or service under the plan.

BLS requests that employers participating in the NCS submit full SPDs. However, many only provide summary tables of benefits, a more circumscribed description of benefits than the complete SPDs. BLS permitted NORC to abstract data from plan documents submitted by midsized employers between 2008 and 2011 to assess changes since the introduction of the MHPAEA and the IFR. The total sample size of abstracted documents was 240. One hundred sixty-seven covered the pre-parity era (plan years 2008-2009), and 73 covered the post-parity era (plan years 2010-2011). Not all documents included every data element of interest, but, when available, information related to the provision of quantitative limits (e.g., copays, coinsurance, and deductibles) was abstracted and analyzed. Observation level characteristics provided by BLS for each SPD was limited to principal industry. In order to increase the generalizability of the information obtained from the SPDs, analysis weights were constructed for each observation.66

To create the analysis weights, the sample was first divided into pre-parity observations (plan year 2008-2009; n = 167) and post-parity observations (plan years 2010-2011; n = 73) subsamples. Each subsample was treated as a separate sample with respect to weight construction. Within each subsample, the observations were assigned to one of seven industry categories based on the observation's North American Industry Classification System (NAICS) code.67

It should be noted that the utility of our analyses is limited by several factors. Many of the documents submitted to BLS were in fact not full SPDs, but brief tables of benefits that lacked many of the elements necessary to carefully track changes in financial requirements and treatment limitations. Our ability to construct weights to analyze the data that was abstracted was further limited by the lack of detailed establishment information available from the plan documents. Ideally, the weights would have been created using information including the number of workers at each establishment, detailed industry classification, and the physical location of the establishment. We were only provided information on basic industry categories. Therefore, we believe the weights as created, and applied in our analyses, are insufficient to remove all potential bias from the sample, and appropriate caution should be exercised when interpreting these results.

Employer Surveys. We reviewed the results of published national employer surveys from the KFF/HRET and Mercer. These surveys provided generalizable information on employers' coverage of MH/SUD. The 2010 KFF/HRET survey included 2,046 randomly selected public and private employers with more than three workers. The sample is randomly selected from a sample frame constructed by Survey Sampling Incorporated from Dun & Bradstreet's listing of public and private employers. KFF/HRET then stratifies the sample by industry and employer size. The 2010 Mercer Health Benefits Survey is also a random survey of employers identified from Dun & Bradstreet. The 2010 survey included 1,977 employers that offered health benefits. The survey uses sampling weights to calculate estimates both nationwide and for four geographic regions. The Mercer survey contains information for large employers (i.e., those with 500 or more employees), and for smaller employers (i.e., those with fewer than 500 employees).

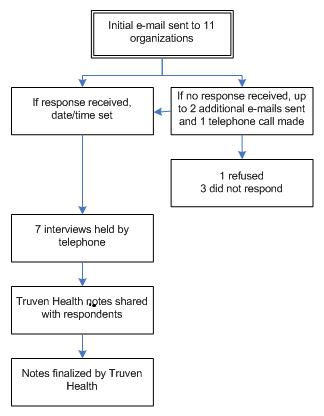

Semi-structured Interviews with Health Plan Representatives. Lastly, we conducted detailed interviews with a non-generalizable sample of senior health plan officials who are responsible for seven major health insurers' compliance with the MHPAEA. The purpose of the interviews was to obtain specific information about plans' disclosure policies and practices required by the MHPAEA. Two behavioral health plan associations, the Association for Behavioral Health and Wellness and the National Behavioral Consortium recruited health plans to participate in the interviews.

Each of the seven individuals interviewed is a senior staff member responsible for leading the company's review of policies and procedures to bring the plan into compliance with MHPAEA and the IFR. The seven companies that participated collectively provide coverage for more than 100 million individuals and are among the largest health plans in the nation. Several of the plans exclusively provide behavioral health care services, and others provide behavioral health services within a larger health plan covering health, disability, and other benefits as well. Collectively, the companies operate in all 50 states, serving self-insured employers and employers purchasing fully-insured group health insurance products. Each interview elicited detailed information about:

- The use of medical necessity criteria for medical and MH/SUD services.

- The process for informing beneficiaries of reasons for claim denials for medicaland MH/SUD services and any changes in the processes for informing beneficiaries since implementation of the MHPAEA.

- The use of utilization management techniques formedical and MH/SUD services and any changes in the use of utilization management techniques.

- The management of out-of-network care.

- The presence of any unmet demand for residential and intensive outpatient substance abuse services since the implementation of the MHPAEA.

- The management of prescription medications, if the company is involved in this service.

Methodology for sample selection and technical specifications at http://www.bls.gov/ncs/ebs/smb_health.htm. The sample for the NCS is selected on the basis of a three-stage design. The first stage involved the selection of areas consisting of 152 metropolitan and non-metropolitan areas. In the second stage, the sample of establishments is drawn from a sampling frame comprised of state unemployment insurance reports within sampled areas. The third stage is a probability sample of occupations within a sampled establishment. BLS field economists visit sampled establishments or contact them by telephone to collect data for the survey. To reduce the reporting burden, field economists ask respondents to provide Summary Plan Provision documents for health and retirement plans. Approximately 3,300 establishments provide data for each annual NCS.

The analysis weights were calibrated to establishment and worker counts from the 2010 County Business Patterns created by the Department of Census. The end result is two sets of weights -- an establishment and a worker weight for pre-parity and an establishment and a worker weight for post-parity. The weight sums for the respective weights are identical between pre-parity and post-parity. Following describes the detailed process used to construct analysis weights.

Step 1: Calculate the proportion of observations within each subsample and industry such that:

rpi = npi Σinpi Where n = number of observations within subsample p and industry i.

Step 2: Calculate the share of establishments within each industry such that:

Ri = Ni ΣiNi Where N = the number of establishments from the 2010 County Business Patterns within industry i.

Step 3: Calculate the share of workers within each industry such that:

RWi = NWi ΣiNWi Where NW = the number of workers from the 2010 County Business Patterns within industry i.

Step 4: Calculate the final weights as the ratio of the share of establishments or workers within each industry and the proportion of observations within each subsample and industry such that:

Establishment Weight = Ri rpi Worker Weight = RWi rpi Where rpi = the proportion of observations within each subsample and industry, Ri = the share of establishments within each industry, and RWi = the share of workers within each industry.

The sum of both the establishment weight and the worker weight within each subsample equals the sample size within each subgroup. Each weight has a different impact on analyses. For example, the health care industry tends to have more workers as a share of the total workforce than establishments as a share of total establishments. Thus, the worker weight will grant health care observations more influence on an estimate than will the establishment weight. Comparisons of results obtained using both sets of weights demonstrated very minimal differences between the two sets of estimates. The estimates presented in this report were calculated using the establishment weights.

The industry categories are as follows: (1) Agriculture, Mining, Utilities, Construction, and Manufacturing (NAICS = 11, 21, 22, 23, 31, 32, 33); (2) Wholesale (NAICS = 42); (3) Retail (NAICS = 44, 45); (4) Transportation and Information (NAICS = 48, 49, 51); (5) Finance, Real Estate, Professional Services, and Management (NAICS = 52, 53, 54, 55, 56); (6) Health care (NAICS = 62); and (7) Education, Recreation, Food Service and Other (NAICS = 61, 71, 72, 81).

Study Results

Research Question #1: Health Plan and Employer Use of Financial Requirements

What types of financial requirements (e.g., copays, coinsurance) do group health plans use for MH and SUD benefits and are such requirements consistent with the new MHPAEA standards for calculating the predominant level that applies to substantially all medical and surgical benefits?

According to the IFR regulations, a plan must meet two testing requirements within each benefit classification in order to comply with parity financial requirements:

-

Substantially all. A requirement or limitation applies to substantially all if it applies to at least two-thirds of the benefits in that classification. If a type of requirement or limit does not apply to at least two-thirds of the medical/surgical benefits in a classification, then it cannot be applied to MH/SUD benefits in that classification.

-

Predominant. A requirement or limitation is considered predominant if it applies to at least one-half of the benefits in that classification.

Determination of "substantially all" and "predominant" is based on the dollar amount of all plan payments for medical/surgical benefits in the classification that are expected to be paid under the plan for the plan year. Plan design compliance must be assessed within the six benefit classifications specified by the regulations. Regulatory guidance defined two sub-classifications for outpatient services. The classifications and sub-classifications recognized by the regulations are:

- Inpatient in-network

- Inpatient out-of-network

- Outpatient in-network

- Office visits

- All other outpatient items and services

- Outpatient out-of-network

- Office visits

- All other outpatient items and services

- Emergency care

- Prescription drugs

Detailed testing was performed for each of these six classifications and two sub-classifications. Results for each of the six classifications are presented here, and results pertaining to the "office visit" and "other services" sub-classifications and the Safe Harbor provision can be found in Appendix A.

It should be noted that the testing models used in these analyses are based on Milliman's and Aon Hewitt's interpretation of provisions outlined in the IFR. The development of these models required Milliman and Aon Hewitt to make interpretations on issues that were not entirely settled by the IFR, or may be interpreted differently by regulators.

Results of the testing illustrate both the substantial changes that most plans have made since 2008 to comply with the MHPAEA's financial parity requirements and the specific areas where a small proportion of plans must still make changes to be consistent with MHPAEA standards. Milliman and Aon Hewitt data were analyzed using similar, though not identical, testing procedures. The two analyses provide glimpses into two successive time slices: The Milliman database included information on 2010 benefits, whereas the Aon Hewitt database included information on 2011 benefits. It should be noted that the IFR became effective for plan years beginning on or after July 1, 2010. Thus for calendar year plans, the IFR was not effective until January 1, 2011. Therefore, our 2010 testing results do not suggest that plans failing to meet the "substantially all" or "predominant" tests were non-compliant with MHPAEA requirements at the time, only that they were required to make additional changes in order to be consistent with MHPAEA standards going forward.

2010 Inpatient Financial Requirements

TABLE 3. Financial Requirements: Percentage of Plans in 2010 Requiring Changes to Inpatient Benefits to the Consistent With MHPAEA

| Deductible | Out-of-Pocket Maximum |

Copay | Coinsurance | |

|---|---|---|---|---|

| Inpatient in-network MH services | 6.7% | 8.7% | 6.7% | 7.5% |

| Inpatient out-of-network MH services | 1.0% | 7.8% | 0% | 5.8% |

| Inpatient in-network SUD Services | 6.7% | 8.4% | 6.7% | 7.6% |

| Inpatient out-of-network SUD services | 1.0% | 8.7% | 0% | 5.8% |

SOURCE: Milliman's Testing Data of 2010 plan designs.

Analyses of Milliman's data focused on identifying specific areas where a plan needed to make changes in its 2010 benefits to achieve consistency with MHPAEA. Analyses of Milliman's inpatient benefit designs found that overall, approximately 10% of plans offering inpatient MH/SUD benefits needed to make some changes to their 2010 inpatient financial requirements in order to be consistent with MHPEA standards. Table 3 presents the percentage of participating plans that appeared to offer benefits that were not consistent with MHPAEA's financial requirements (deductibles, out-of-pocket maximums, copays, and coinsurance). Relatively few plans needed to modify copays for inpatient in-network MH/SUD benefits, and no plans needed to make changes to their inpatient out-of-network MH or SUD benefits. Approximately one plan in 12 needed to change its member out-of-pocket maximums for inpatient MH and SUD to be equivalent to its medical/surgical inpatient maximums.

2010 Outpatient Financial Requirements

Analyses of Milliman's 2010 data suggest that substantially more plans required changes to their outpatient MH/SUD benefits than required changes to their inpatient benefits. More than one-quarter of plans were required to change deductible limits, one-third required changes to copays or coinsurance, and one-fifth needed to change out-of-pocket maximums. An almost identical pattern was found for in-network outpatient SUD treatment. A much smaller percentage of plans, less than 10%, needed to change out-of-network financial limitations. Table 4 presents the percentage of participating plans that were required to change outpatient financial requirements in order to be consistent with MHPAEA standards.

TABLE 4. Financial Requirements: Percentage of Plans in 2010 Requiring Changes to Outpatient Benefits to the Consistent With MHPAEA

| Deductible | Out-of-Pocket Maximum |

Copay | Coinsurance | |||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Outpatient in-network MH services | 26.7% | 21.7% | 33.3% | 34.2% | ||||||||||||||||||||

| Outpatient out-of-network MH services | 3.9% | 8.7% | 1.0% | 10.7% | ||||||||||||||||||||

| Outpatient in-network SUD services | 26.1% | 18.5% | 31.9% | 33.6% | ||||||||||||||||||||

| Outpatient out-of-network SUD services | 3.9% | 9.7% | 1.0% | 8.7% |

SOURCE: Milliman's Testing Data of 2010 plan designs.2010 Emergency Care and Prescription Drug Financial Requirements

Analyses of 2010 benefit designs suggest that the vast majority of plans offered emergency and prescription drug benefits that were consistent with MHPAEA's financial requirements. Table 5 presents the percentage of participating plans that needed to make changes in their emergency and prescription drug benefits in order to be consistent with MHPAEA's financial parity requirements. Fewer than 1% of plans needed any changes to their prescription drug benefits. But one-fifth needed to change coinsurance rates for behavioral health emergency care, and a smaller proportion needed to make changes in copay and deductible benefits.

TABLE 5. Financial Requirements: Percentage of Plans in 2010 Requiring Changes in ER and Prescription Drug Benefits to the Consistent With MHPAEA

| Deductible | Out-of-Pocket Maximum |

Copay | Coinsurance | |||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Emergency care -- MH/SUD | 5.6% | 0% | 7.2% | 19.2% | ||||||||||||||||||||

| Prescription drugs -- MH/SUD | 0% | 0% | 0% | 0% |

SOURCE: Milliman's Testing Data of 2010 plan designs.

2011 Inpatient Financial Requirements

Analyses of Aon Hewitt inpatient plan designs suggest that by 2011, the vast majority of health plans appeared to meet MHPAEA's financial requirements. As shown in Table 6, only a very small percentage of plans utilized inpatient financial requirements that did not comply with MHPAEA standards. None needed to modify copay or coinsurance levels, and less than 2% required modifications of their deductibles or out-of-pocket maximums.

Comparison of the 2010 Milliman data and the 2011 Aon Hewitt data indicates that most large employer plans met the inpatient financial parity standards by 2011. Small, but consistent improvements can be seen in each area tested.

TABLE 6. Financial Requirements: Percentage of Plans in 2011 Requiring Changes to Inpatient Benefits to the Consistent With MHPAEA

| Deductible | Out-of-Pocket Maximum |

Copay | Coinsurance | |||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Inpatient in-network MH services | 1.3% | 1.3% | 0% | 0% | ||||||||||||||||||||

| Inpatient out-of-network MH services | 1.3% | 1.3% | 0% | 0% | ||||||||||||||||||||

| Inpatient in-network SUD services | 1.3% | 1.3% | 0% | 0% | ||||||||||||||||||||

| Inpatient out-of-network SUD services | 1.3% | 1.3% | 0% | 0% |

SOURCE: Aon Hewitt Compliance Testing Database of 2011 plan designs.

2011 Outpatient Financial Requirements

Analyses of 2011 outpatient benefit designs suggest that nearly all large employer plans appeared to meet parity's financial requirements for deductibles, out-of-pocket maximums, and coinsurance requirements. However, nearly one-fifth had outpatient in-network copay requirements for MH and SUD that appeared not to conform to MHPAEA's financial parity requirements.

Comparison of the 2010 outpatient data to the 2011 data again suggests substantial improvement between the two periods. For example, the 2010 data indicated that more than one-third of plans had outpatient coinsurance requirements that appeared not to conform to MHPAEA standards. By 2011, that number had dropped to less than 4%. Likewise, more than 25% of 2010 plans were required to make changes to their outpatient in-network deductible benefits in order to be consistent with MHPAEA's standards. By 2011, the data suggested that less than 2% of plans still appeared to offer benefits that were not consistent with MHPAEA standards. However, adherence to MHPAEA standards was not universal. Although there was clearly improvement in the proportion of plans that appeared to conform to MHPAEA's outpatient in-network copay requirements, nearly one-fifth of 2011 plan designs continued to offer benefits that appeared not to conform to MHPAEA's financial requirements.

TABLE 7. Financial Requirements: Percentage of Plans in 2011 Requiring Changes to Outpatient Benefits to the Consistent With MHPAEA Standards

| Deductible | Out-of-Pocket Maximum |