U.S. Department of Health and Human Services

Report to the Secretary on Private Financing of Long-Term Care for the Elderly

Technical Work Group on Private Financing of Long-Term Care for the Elderly

November 1986

PDF Version: http://aspe.hhs.gov/daltcp/reports/pfltce.pdf (243 PDF pages)

This paper was prepared by U.S. Department of Health and Human Services (HHS), Office of Social Services Policy (now Office of Disability, Aging and Long-Term Care Policy (DALTCP)) and the Brookings Institution. For additional information about this subject, you can visit the DALTCP home page at http://aspe.hhs.gov/_/office_specific/daltcp.cfm or contact the office at HHS/ASPE/DALTCP, Room 424E, H.H. Humphrey Building, 200 Independence Avenue, S.W., Washington, D.C. 20201. The e-mail address is: webmaster.DALTCP@hhs.gov. The Project Officer was Paul Gayer.

The opinions and views expressed in this report are those of the authors. They do not necessarily reflect the views of the Department of Health and Human Services, the contractor or any other funding organization.

TABLE OF CONTENTS

CHAPTER 1. INTRODUCTION

A. Background of the Report

B. Structure of the Report

CHAPTER 2. AN OVERVIEW OF LONG-TERM CARE

A. Long-Term Care and Catastrophic Costs

B. The Long-Term Care Population and Its Service Needs

C. Growth of the Elderly Population and the Demand for Long-Term Care Services

D. Characteristics of the Long-Term Care Services System

E. Long-Term Care Expenditures and Financing

F. Public Long-Term Care Financing Programs

G. The Impact of Health, Social, and Economic Trends on the Demand for Long-Term Care

CHAPTER 3. ANALYSIS OF PRIVATE MECHANISMS FOR FINANCING LONG-TERM CARE OF THE ELDERLY

A. Introduction

B. General Approaches to Private Financing of Long-Term Care

C. Analysis of Specific Financing Mechanisms

D. Special Analysis of IMAs, Long-Term Care Insurance, and Combination Approaches

CHAPTER 4. THE RELATIONSHIP OF MEDICAID TO PRIVATE FINANCING OF LONG-TERM CARE

A. Medicaid Eligibility for Long-Term Care

B. Implications of Medicaid for Private Financing Mechanisms

C. Possible Areas for Medicaid Reform

APPENDICES

APPENDIX 1: Description of National Surveys Related to Long-Term Care

APPENDIX 2: Examples of Long-Term Care Insurance Policies

APPENDIX 3: Home Equity Conversion

APPENDIX 4: Induced Demand

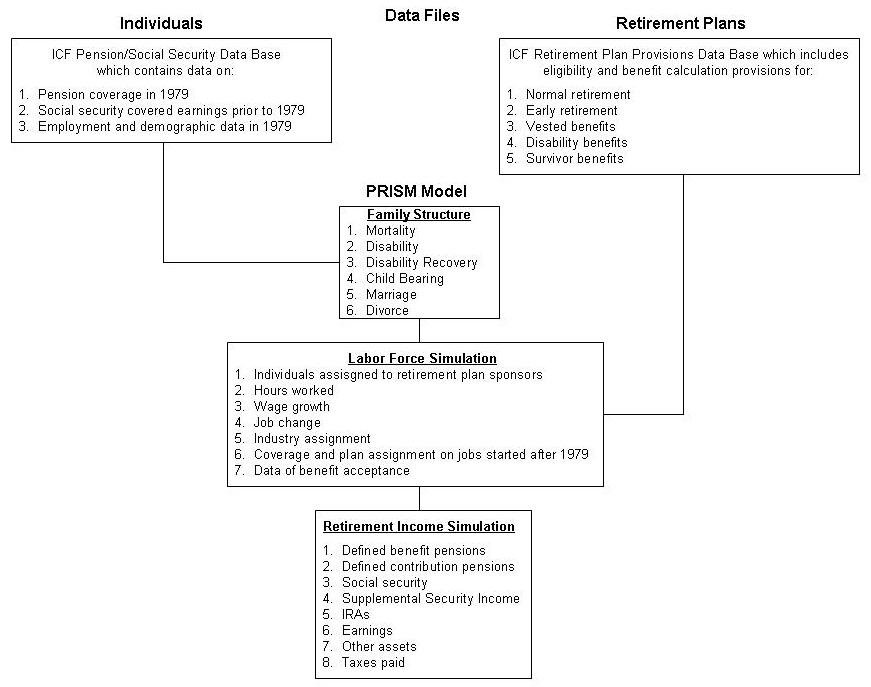

APPENDIX 5: Description of Brookings/ICF Microsimulation Model

LIST OF FIGURES

FIGURE 2-1: Personal Health Care Expenditures for the Elderly by Type of Service -- 1984

FIGURE 2-2: Out of Pocket Health Care Expenditures for the Elderly by Type of Service -- 1984

FIGURE 2-3: Nursing Home Expenditures by Source of Payment -- 1984

FIGURE A5-1: Brookings/ICF Long-Term Care Financing Model

FIGURE A5-2: PRISM Flowchart

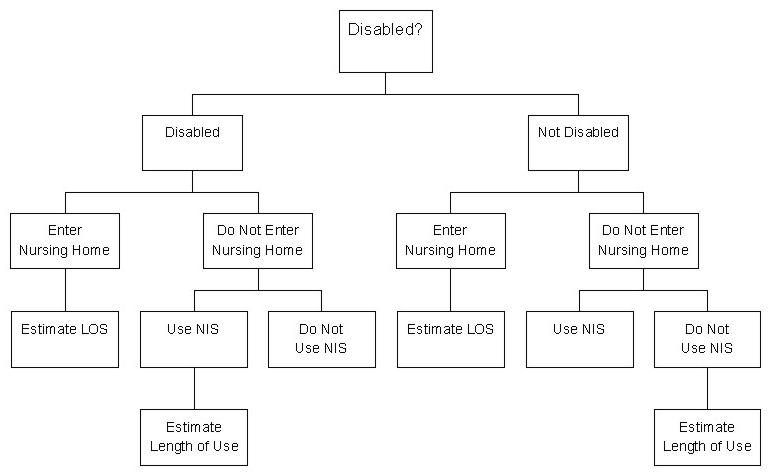

FIGURE A5-3: Flowchart for Utilization of Long-Term Care Services

LIST OF TABLES

TABLE 2-1: U.S. Population 65 Years of Age or Over and Percent of Total Population: Selected Years and Projections 1950-2030

TABLE 2-2: Percent Increases in U.S. Population for 10-year Intervals, by Age Groups: Selected Years and Projections 1950-2010

TABLE 2-3: Projections of Long-Term Care Population in Nursing Homes and in the Community

TABLE 2-4: Percent Distribution of Helpers and Helper Days, by Sex and Relationship to Individuals 65 Years of Age or Over with Limitations in Activities of Daily Living

TABLE 2-5: U.S. Total Expenditures for Nursing Home Care and Annual Percent Change: Calendar Years 1960-84

TABLE 2-6: Long-Term Care as Percent of Total Federal and State Medicaid Expenditures, by Type of Service: Fiscal Years 1974-84

TABLE 2-7: Medicaid Long-Term Care Expenditures and Percent Change, by Type of Service: Fiscal Years 1977-84

TABLE 2-8: Actual and Projected Growth of the Older Population: United States, 1990-2040

TABLE 2-9: Probability of Selected Medical Conditions as the First Reported Cause of Chronic Disability among Disabled Persons, 85 Years and Older: United States, 1982

TABLE 2-10: Average Incomes of the Elderly and Nonelderly, 1969 and 1984

TABLE 2-11: Median Per Capita Income for the Elderly by Sex and Marital Status: 1984

TABLE 2-12: Median Per Capita Income of the Elderly by Age, Race, and Sex: 1984

TABLE 2-13: Percent of Older Persons in Poverty by Age and Sex: 1984

TABLE 2-14: Percent of the Elderly Below Poverty by Race, Sex, and Living Arrangements: 1984

TABLE 2-15: Percentage Distribution of Income by Source For Elderly in Different Income Groups, 1984

TABLE 2-16: Asset Holdings, by Type of Asset and Age of Family Head; United States: 1983

TABLE 2-17: Home Equity Among the Elderly: 1984

TABLE 2-18: Annual Expenditures as a Percentage of Income, by age of Householder and Budget Item: United States: 1982-1983

TABLE 2-19: Projections of Average Income of Elderly Families and Singles By Age Group: Baseline

TABLE 2-20: Projections and Income Distribution for Families and Singles Aged 65 to 71: Baseline

TABLE 2-21: Projections of Number and Income Distributions for Families and Singles Aged 72 and over: Baseline

TABLE 2-22: Projections of Elderly with Inadequate Income, by Family Status and Age: Baseline

TABLE 3-1: Tax Returns with IRA Contributions by Adjusted Gross Income Class, 1984

TABLE 3-2: Tax Returns with Maximum IRA Contributions as a Percentage of all Tax Returns with IRAs by Total Positive Income Class, 1983

TABLE 3-3: Summary of Services Offered by CCRCs: Percent of CCRCs Including Services in Fees

TABLE 3-4: Combined Annual Rate of Interest for a 70-year-old Borrower When Initial Home Value Equals $70,000

TABLE 3-5: Estimated Initial Annual Savings to Pay for Expected Nursing Home Utilization, by Age

TABLE 3-6: Projections of Persons 65 & Over Who Would Have Contributed $3,000 to an IRA in One or More years, and Rates of Contribution, By Sex, Marital Status, and Homeownership, 1986, 2000, 2018

TABLE 3-7: Projections of Population in Nursing Homes by Age 1986, 2000, & 2018

TABLE 3-8: Projections of Total Nursing Home Expenditures for the Elderly For Two Different Assumptions in the Rate of Specific Inflation, 1986, 2000 and 2018

TABLE 3-9: Inflation and Payment Source for Nursing Home Expenditures for the Elderly in 2018

TABLE 3-10: Base Case Projection: Total Nursing Home Expenditures for the Elderly, by Source of Payment in Years 1986, 2000, 2018

TABLE 3-11: Expanded IRA Projection: Total Nursing Home Expenditures for the Elderly by Source of payment In Years 1986, 2000, 2018

TABLE 3-12: Impact of Expanded IRAs: Total Nursing Home Expenditures for the Elderly By Source of Payment In 2018

TABLE 3-13: Impact of IMAs: Total Nursing Home Expenditures for the Elderly by Source of Payment in 2018

TABLE 3-14: Premium Estimates for a Level Premium, Level Benefit Indemity Policy

TABLE 3-15: Premium Estimates for a Indexed Premium, Indexed Benefit Indemnity Policy Index Rate: 5% per year

TABLE 3-16: Estimated Unisex Contribution/Premium Rates for Nursing Home Coverage Starting at Age 65 of $50 Daily Coverage Indexed by 5.8 Percent After Year of Issue With Contributions Indexed by 5.8 Percent After Year of Issues: Assumed Antiselection/Induced Demand = 37%

TABLE 3-17: Estimated Unisex Contribution/Premium Rates for Nursing Home Coverage Starting at Age 65 of $50 Daily Coverage Indexed by 4.4 Percent After Year of Issue With Contributions/Indexed by 4.4 Percent After Year of Issue: Assumed Antiselection/Induced Demand = 37%

TABLE 3-18: Annual Premium at Issue for Nursing Home Coverage of $50 per Day Starting at Age 65 with 90-Day Elimination Period, 5.8 Percent Annual Indexing of Coverage and Lifetime Premiums After Issue, and Waiver of Premium for Nursing Home Residents Over Age 64

TABLE 3-19: Projections of Total Nursing Home Expenditures for the Elderly by Source of Payment and Insurance Option in 2018

TABLE 3-20: Potential Effect of Induced Demand on Nursing Home Expenditure Patterns in 2018: One Percent of Income Option

TABLE A2-1: Long-Term Care Insurance Examples: Policy Features of Insurance Companies

TABLE A2-2: Annual Premium Rates per $100 Monthly Benefits for Firemans Fund Policies Original Policy

TABLE A2-3: Annual Premium Rates for Federated American Policy

TABLE A2-4: Annual Premium Rates for Massachusetts Indemnity Policies

TABLE A2-5: Annual Premium Rates for Great Republic Policy

TABLE A2-6: Annual Premium Rates for United Equitable Policies

TABLE A2-7: Annual Premium Rates per $5 Daily Benefits for Health Insurance Corporation Policy

TABLE A2-8: Annual Premium Rates for Equitable Life Policies

TABLE A2-9: Annual Premium Rates for Transport Life Insurance Company

TABLE A2-10: Annual Premium Rates for Kemper Group Policies

TABLE A2-11: Annual Premium Rates for Merchants and Manufactures Policy

TABLE A2-12: Annual Premium Rates for National Foundation Life Insurance Policy

TABLE A2-13: Annual Renewal Premium Rates for Mutual Protective/Medico Life Insurance Company Policies

TABLE A2-14: Annual Premium Rates per $10 a Day for Columbia Life Insurance Company

TABLE A2-15: Annual Premium Rates for Blue Cross of North Dakota Policies

TABLE A4-1: Assumed Induced Demand Levels for Various Levels of Nursing Home Insurance Coverage

CONTRIBUTORS TO THE REPORT

Steven A. GrossmanChairmanTechnical Work Group on Private Financing of Long-Term Care for the Elderly

Public Health Service

John Marshall, Ph.D.

James O. Mason, M.D., Dr.P.H.T.

Franklin Williams, M.D.

Gene D. Cohen, M.D., Ph.D.

Miriam Davis, Ph.D.

James Friedman

Marcy Lynn Gross

James Kaple, Ph.D.

Mark Meiners, Ph.D.

Jay Moskowitz, Ph.D.

James Scanlon

Amy Taylor, Ph.D.

Joan Van Nostrand

Health Care Financing Administration

Bartlett S. Fleming

Pam Doty, Ph.D.

Thomas Gustafson, Ph.D.

Office of the Assistant Secretary for Planning and Evaluation

Arnold Tomkins

Michele Adler

Robert Clark

Paul Gayer

Mary Harahan

Office of the General Counsel

Terry Coleman

Office of Human Development Services

Carol Fraser Fisk

G. Sandra Fisher

Social Security Administration

Bruce Schobel

Stephen Goss

Michael Staren

Support Staff

Joan Carr

With the Assistance of: Van Jewell Graham Peggy Rohrbaugh Carol Sweeney Sandra Tolpin

Contractors

Brookings Institution

Joshua Weiner, Ph.D.

Duke University

Kenneth Manton, Ph.D.

ICF, Inc.

David Kennell

Project Hope

Burton Dunlop, Ph.D.

Joe Kutzin

Sandra Yamishiro

Urban Institute

Korbin Liu, Ph.D.

EXECUTIVE SUMMARY

INTRODUCTION

The economic welfare of older persons in 1986 is better than at any point in our history, and most older persons can expect their senior years to be healthy and independent. However, the next 50 years will see the number of people age 65 and over almost double as a proportion of the population--reaching over 21 percent in the year 2030. The number of very old--people age 85 and over--will almost quadruple. Since the incidence of chronic health problems and disabling conditions which require long-term care significantly increases with age, few believe that the current system of financing and delivering long-term care services is adequate for the challenge ahead.

The great majority of older persons who need long-term care receive the support they need from friends and family members. Nevertheless, in 1985 the Nation spent over $35 billion a year on nursing home care, about 75 percent of that on the elderly. Nursing home care represents about 8 percent of total health care expenditures, and it is the leading cause of catastrophic out-of-pocket expenditures for the elderly. This is true for several reasons:

-

The lifetime risk of needing nursing home care is between 20 and 45 percent. While only about half of those who enter nursing homes will stay over 90 days, for this subgroup the average stay is over two years. Despite the improved economic status of older persons, few can afford the high cost of an extended nursing home stay (averaging $22,000 per year).

-

Unlike acute health care, there is virtually no private insurance for long-term care. Consequently, there are only two significant sources of payments--out-of-pocket payments by the elderly and/or their families, and the Medicaid program.

-

Although the Medicaid program provides public financing for nursing home care, it is a welfare-based system that does not provide assistance to individuals until all other financial resources have been consumed. Approximately half of all Medicaid recipients in nursing homes were not initially poor, but "spent down" their income and resources as a result of their nursing home stay.

On February 4, 1986, President Reagan directed the Secretary of the Department of Health and Human Services, Dr. Otis Bowen, to report to him by the end of the year on how Government and the private sector can work together to address catastrophic health care needs in the United States.

The purposes of this report are to:

- Describe the characteristics of elderly people who need long-term care and how these characteristics will change over time;

- Assess the potential of private financing mechanisms to lessen the catastrophic impact of nursing home and home care expenses which can wipe out individual and family savings; and

- Develop actions that would increase the availability and use of private financing mechanisms for the long-term care of older persons.

This report addresses only one critical part of the problem of long-term care, albeit a highly neglected part. The focus on private financing strategies is not to deny the very real needs of persons who must rely on public programs to provide their long-term care because they cannot afford private alternatives. Such persons are and will continue to be the legitimate concern of government.

However, Federal, State, and local governments are already significant partners in sharing the costs of long-term care--paying almost half of all costs through Medicaid and other programs. The direct, out-of-pocket resources of individuals pay almost all the rest. The protective mechanisms relied upon for other types of health care expenses, such as private insurance and charitable sources, pay less than 2 percent of costs. There need to be suitable, effective and widely available private financing mechanisms for the elderly who want to protect themselves at a reasonable cost against the high costs of long-term care.

The findings of this report are based on a review of the existing literature, as well as analyses undertaken specifically for this report.

For the purposes of this report, the terms "elderly" and "older persons" refer to persons aged 65 and older. It is recognized, however, that these terms do not adequately reflect the diversity of this population.

OVERVIEW

Long-Term Care and Catastrophic Expenses. Long-term care refers to a wide range of medical, health related, and social services for persons who, because of chronic mental or physical illness and disability, need personal assistance in caring for themselves over an extended period of time. While long-term care services can be provided in a variety of formal and informal settings, the majority of all long-term care is provided in the recipient's own home by family and friends.

A number of factors play a role in determining whether or not the need for long-term care will result in catastrophic expenses. These factors include: the severity of a person's disability; the type and duration of services needed; the living arrangements and the availability of family support; the source of payment (i.e., whether insurance or government will pay for services or whether they must be paid out-of-pocket); and the level of personal resources (income and assets) that are available; and the cumulative financial effect of previous acute or chronic care expenses.

Most people who require long-term care do not experience a catastrophic financial burden. This is because the greatest portion of long-term care (71 percent) is provided in the home or community, rather than in the higher cost setting of a nursing home; and most home and community care (about 70 percent) is provided totally without payment by family members and friends. Among the disabled elderly living in the community who do receive some combination of formal (paid) and informal home and community care services, only a small percentage incur any significant out-of-pocket expense for their care.

High out-of-pocket expenditures for long-term care are most strongly associated with nursing home care. However, even when nursing home care is used, it is important to note that approximately one-half of those who enter a nursing home will stay less than 90 days, and about 38 percent will stay less than 30 days.

The Long-Term Care Population and Service Needs. Approximately five percent (1.4 million) of the 65 and over population resides in nursing homes. In addition, about 16 percent (4.6 million) of the elderly are disabled and living in the community. The great majority (3.7 million) of such disabled persons in the community need assistance because of limitations in what are termed "Activities of Daily Living (ADLs)": eating, using the toilet, mobility, bathing, and dressing. The rest have less severe limitations but need assistance with activities such as shopping, cooking and performing chores.

The number of older persons, and therefore the demand for long-term care, is expected to grow significantly in the future. In 1984, there were about 28 million persons age 65 or older in the U.S. By the year 2030, this number will grow to almost 65 million. In addition, the elderly population is itself becoming older. Between 1980 and 1990, the 75 to 84 year age group will increase twice as fast as the 65 to 75 year age group; and, in the subsequent two decades, the group 85 years and over will increase three to four times as fast as the general population. Since the likelihood of needing nursing home care increases with advancing age (as well as with being female, and with living alone), these demographic changes are likely to translate into significant increases in the demand for long-term care services.

Although it is difficult to estimate lifetime risks, most recent studies indicate that an individual's chance of spending some time in a nursing home during his or her life ranges between 20 and 45 percent. The average length of stay in a nursing home is estimated to be 456 days. However, the nursing home population is a mix of short-term stayers, i.e., terminally ill patients, convalescent or rehabilitative patients who return to the community, and long-term stayers, i.e., patients with chronic illnesses such as Alzheimer's disease, who often remain in a nursing home for many years.

If advances from medical research and changes in prevention and treatment do not decrease the proportion of the population that becomes disabled, the number of elderly in nursing homes is projected to grow to 1.6 million by 1990, 2.1 million in the year 2000, and 4.4 million in 2040. Similarly, the number of older persons with ADL limitations living in the community will rise to 4.2 million by 1990, 5.1 million by the year 2000, and 10.2 million by 2040.

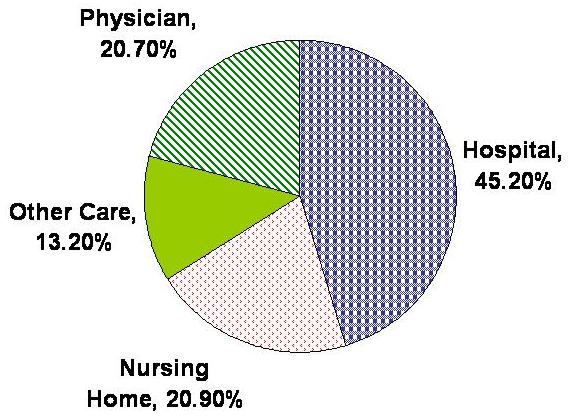

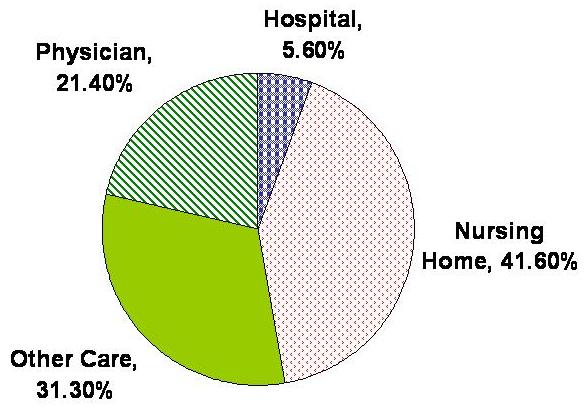

Long-Term Care Expenditures. Total health care expenditures for persons aged 65 and older exceeded $119 billion in 1984. The largest category was hospital care (45 percent), followed by nursing home care (21 percent). However, in terms of direct out-of-pocket expenditures, nursing home care constituted the largest single expense category for the elderly, accounting for about 42 percent of total out-of-pocket health care expenditures. In contrast, hospital care accounted for only 5.6 percent of total out-of-pocket payments.

Separate estimates of the cost of home and community care services for the long-term care of the elderly are not currently available. However, 1983 industry estimates put home care costs for the elderly in the approximate range of $3.0 billion.

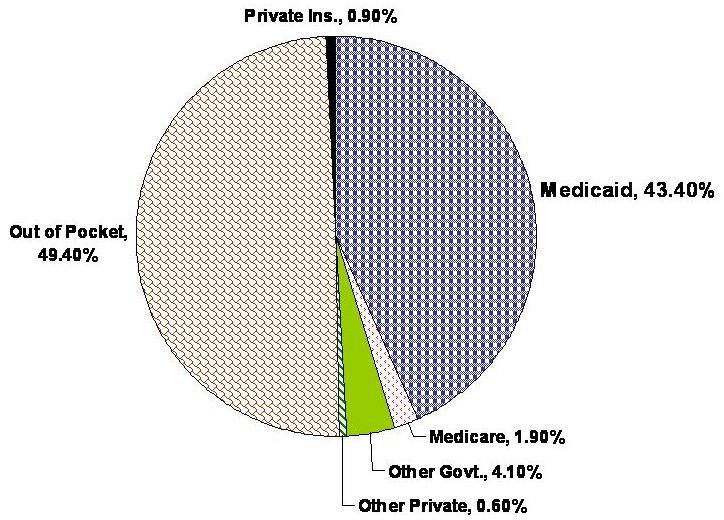

Institutional Long-Term Care. In 1984, $32 billion were spent for nursing home care for persons of all ages, accounting for 8.3 percent of total national health expenditures. Detailed information for 1985 is not yet available, but preliminary estimates indicate that 1985 total nursing home expenditures were $35.2 billion, about three-fourths of which was for nursing home services for the elderly. The 1984 nursing home care expenditures were almost equally divided between public and private sources. Approximately $15.8 billion of the $16.3 billion spent in 1984 from private sources was out-of-pocket; and $13.9 billion of the $15.7 billion spent in.1984 from public sources was spent by Medicaid.

Home Health and Community-Based Services. According to the 1982 Long-Term Care Survey, 1.1 million of 4.6 million disabled elderly living in the community received some formal services from paid caregivers. Of these, about 600,000 individuals (12 percent) were estimated to have paid for some of their home care directly out-of-pocket, with median expenses being $40 a month and the average being $164 per month. Approximately 10 percent of the persons who had any out-of-pocket expenditures (i.e., 60,000 persons), had payments for home care services of over $400 per month.

Public Financing Programs. While personal, family and private charitable resources are an essential and often dominant element of the long-term care system, Federal, State and local government programs also have a major effect on the nature, availability and costs of such services. In addition to Medicaid and Medicare, long-term care services and/or support are provided by the Veterans Administration (VA), the Office of Human Development Services (OHDS), and numerous State and local programs.

THE IMPACT OF HEALTH, SOCIAL AND ECONOMIC TRENDS

Trends in Chronic Disease and Disability. The diseases which cause chronic disability are generally not those which lead to high mortality. About three-fourths of all disability is caused by dementia, arthritis, peripheral vascular disease, cerebrovascular disease and hip and other fractures. Conversely, the major killers, such as heart disease and cancer, cause less than two percent of chronic disability.

As mentioned previously, if current age-specific rates of disability continue, the number of disabled Americans with ADL limitations living in the community will grow from 3.7 million persons in 1984 to about 10.2 million persons in 2040. For example, with respect to Alzheimer's disease, it is estimated that perhaps only 1 percent of those under 65 have the disorder, while 15 percent of those over 85 are afflicted. In the absence of major treatment and prevention breakthroughs, the combination of chronic mental and physical disabilities will significantly increase the need for long-term care as the population ages.

Continuing technological advances may help to limit the impact of disabilities often associated with the need for long-term care services. Technological advances are currently under development in such areas as accident prevention, hip replacement, prevention of hearing loss, urinary incontinence devices, and assistance-summoning devices.

Societal Changes. In addition to increased longevity, several other societal factors also may affect the future demand for long-term care. Between 1960 and 1984, the proportion of noninstitutionalized elderly living alone has increased from 19 percent to 30 percent. The majority of these people are older women who have outlived their spouses.

The major source of long-term care support for these widowed elderly is their children. While the increase in childbearing occurring over the past decade is expected to continue in the short-term, when the baby boom generation nears age 65 (around the year 2010), fewer elderly women are likely to have children to care for them. Another factor which affects the availability of family care is the geographic proximity of the parent and child. Between the 1960s and the 1970s, the number of elderly moving from one State to another increased by 50 percent.

The willingness of adult children to provide support to their elderly parents is a major issue in projecting the need for formal long-term care. The increasing participation by women in the work force suggests that middle-aged daughters may have less time to provide assistance to their elderly parents. Nevertheless, the research that is available has found that middle-aged daughters who also work will make considerable personal sacrifice to care for elderly parents and that the commitment of young women to care for their parents remains strong.

Economic Status of the Elderly. The economic status of the elderly has improved dramatically over the past two decades. The proportion of elderly living below the poverty line has decreased from 25 percent to 12 percent. However, a significant number of the elderly are "near-poor" and are highly vulnerable to being poor. Poverty rates remain higher among elderly women, persons who live alone, the oldest old (85+) and minority populations, some of the very groups at highest risk for long-term care. In 1984, the average income of elderly families was $26,000; for unrelated elderly individuals, average income was $10,800.

Social Security benefits were the largest source of income for the elderly in 1984, averaging 37.6 percent of income for couples and 44.5 percent for individuals. Money from assets (savings, IRAs and stocks) was the second largest source of income for the elderly, averaging 27.6 percent for couples and 30.6 percent for individuals. Earnings and pensions also are significant sources of income for the elderly.

Home equity is the largest asset of older persons. In 1984, 75 percent of older persons owned their homes, and about 83 percent of this group owned them free and clear. The most recent figures from the U.S. Census indicate that the average home equity for persons aged 65 and over was $54,700 in 1984.

ANALYSIS OF PROVIATE FINANCING MECHANISMS FOR LONG-TERM CARE OF THE ELDERLY

Although there are several ways in which individuals can use their private resources to protect against the high costs of long-term care, the existing options for private financing are neither well developed nor widely used. It is the underlying premise of this report that private financing options for long-term care can play a larger role in our society than is currently the case.

General Approaches to Private Financing. This report considers three basic approaches to the financing of care: cash accumulation, risk pooling and resource mobilization techniques. The strengths and weaknesses of various caregiver support strategies are also considered. Lastly, the report presents the results of special analyses which explore the potential of combinations of approaches.

Cash accumulation strategies refer to savings mechanisms that encourage individuals to increase the resources available for future long-term care needs. The principal cash accumulation strategy examined in this report is the long-term care Individual Medical Account (IMA), which would provide Federal or State tax advantages for savings deposited in accounts earmarked for long-term care expenses.

Risk Pooling refers to mechanisms which pool the resources of a large group of individuals at risk to pay for long-term care services which will be needed by a relatively small but unknown subset of the group. Three types of risk pooling mechanisms are examined:

- Long-term care insurance, which pools the premiums of a group of beneficiaries to cover the risk of needing extended nursing home care, intermediate care or home health services

- Social health maintenance organizations (SHMOS), which use the pre-paid, capitated (i.e., set fee per person), case management approach of health maintenance organizations to provide long-term care benefits to groups of individuals

- Continuing care retirement communities (CCRCs), which typically provide older persons with a package of benefits that includes residential, health, social and custodial services, in return for an entrance fee and monthly charges

Resource mobilization refers to financing mechanisms that enable individuals to convert non-liquid resources to cash, thus enhancing an individual's ability to pay for long-term care services. Two types of resource mobilization approaches are considered:

-

Home equity conversion (EEC) plans allow a homeowner to convert the equity in a home into a stream of income without having to move or make immediate repayment.

-

Employee benefit options for retirees refer to the addition of long-term care benefits as an option in the package of pension or health benefits offered employees.

Caregiver support strategies refer to mechanisms designed to strengthen and expand the existing informal network of long-term care provided by families in the home and in the community. This network is essential to the success of private financing mechanisms because home and community-based services usually are provided at no cost to the patient and because it keeps disabled older persons with their families, where most persons would prefer to be. Two types of caregiver support strategies are examined:

- Tax allowances for home care, which provide special tax credits, deductions, or cash subsidies to assist family members in providing home care services for an elderly dependent

- Volunteer systems, in which organizations and individuals assist others in providing unpaid long-term care services to older persons in the community

- Combination financing approaches are designed to improve the effectiveness of one financing mechanism by blending its attractive features with that of another. This report analyzes the potential of a variety of combinations, including the development of long-term care IMAs that have a risk pool feature.

ANALYSIS OF SPECIFIC PRIVATE FINANCING MECHANISMS

Long-Term Care Individual Medical Accounts (IMAs)

A variety of proposals have been advanced which would permit individuals to establish tax-favored accounts dedicated, in whole or in part, to the purchase of long-term care health services. In May 1986, Colorado became the first State to enact legislation creating a tax-favored IMA and is in the process of implementing its planned program.

Because IMA proposals are new, analysts assessing the potential impact of various IMA proposals have used the Federal experience with Individual Retirement Accounts (IRAs) as a base for estimating the number of persons likely to establish an IMA if given an opportunity (i.e., the participation rate) and for estimating the amounts likely to be saved.

Although participation rates varied considerably by income level, only 15.4 percent of all tax returns showed a contribution to an IRA in 1984. About 9.5 percent of all taxpayer returns contributed the maximum tax-favored amount. The Treasury Department estimates revenue losses of $14.4 billion in 1986 from IRAs, some of which will be recovered in later years as future withdrawals are taxed.

Most analysts consider the IRA participation and savings rates to be an upper limit on a voluntary IMA program. This is because IMA proposals place more restrictions on the use of funds by the saver and, therefore, are less flexible and less attractive to the public as a savings device. The financial incentives of IMA proposals will be altered by the tax reform legislation. The legislation affects deductions for medical expenses and IRA contributions, as well as overall rates of taxation.

A critical issue in considering IMA proposals is the amount a person must save to pay for future long-term care should it be needed. Individual savings must be sufficient to cover the high costs of nursing home care (which averaged $22,000 in 1984). The problem is compounded by inflation rates, which are rising faster in the nursing home sector than in the general economy. A significant amount must be saved every year if a person wishes to accumulate sufficient funds to cover the average nursing home stay. Yet, the majority of persons are likely to need no paid long-term care services.

Because of this latter phenomenon, called "target inefficiency", IMA proposals which have a risk pooling dimension (such as that proposed by Bowen and Burke in Federation of American Hospitals Review, December 1985) are somewhat more promising. As discussed below, such combinations lower the amount individuals need to save.

Freestanding Long-Term Care Insurance

Freestanding long-term care insurance is insurance that provides payment for long-term care services in an institution or a person's home. The policy covers chronic care services needed for an extended period of time, rather than the acute, recuperative or rehabilitative care covered by Medicare and medigap policies. Beneficiaries are free to select their own provider within general qualifying guidelines.

The market for long-term care insurance is still in an early stage of development. According to the American Health Care Association, there were about 25 long-term care insurance products being sold in 1986, many of which were new entries into the market. Most policies have been sold on an individual rather than a group basis. Estimates of the total number of policies sold range from 50,000 to 300,000.

Although there is considerable diversity among the long-term care insurance products, all focus on nursing home care, with only limited (or no) custodial and home care benefits. Benefits are structured as indemnity plans, paying fixed amount per day (usually not indexed for inflation), with waiting periods before coverage begins and coverage from two to six years.

Products have traditionally been sold to persons of retirement age, although marketing for a few newer products has been expanded to earlier age groups. Premiums differ substantially among companies. According to a Money Magazine article that appeared in March 1986, a 65 year old person could pay from $174 to $1,451 for policies that cover differing ranges of skilled and custodial care.

The principal strengths of freestanding insurance as a mechanism for financing long-term care include: 1) long-term care insurance addresses the major cause of catastrophic expense among the elderly by focusing primarily on the nursing home risk; 2) long-term care insurance provides affordable protection for many individuals; and 3) long-term care insurance can potentially relieve upward cost pressures on Medicaid by slowing or eliminating the spend-down process for insured persons.

The weaknesses of the mechanism include: 1) existing products reinforce the bias toward institutional care, a bias that is both costly and contrary to the preference of most older persons for home care services; 2) the insurance does not provide complete catastrophic coverage and generally pays fixed benefits that can be eroded by inflation; 3) at present, the premium levels for complete coverage are higher than many older persons can afford; 4) the freestanding product, which separates long-term care from acute care, reduces the incentive to manage the total spectrum of care and leads to the marketing of two insurance products, with possible overlap and confusion for purchasers; and 5) marketing to individuals rather than groups raises premium costs and can more easily lead to adverse selection.

Research indicates that there is substantial room for growth in the long-term care insurance market. Two major studies have estimated the number of persons over age 65 who could afford long-term care insurance. One placed the number in the range of 4.7 million elderly, and the other placed the number in the range of about 7.0 million elderly. However, because neither study factored in the effects of inflation over time, the estimates may be high. Various linkages have been proposed to enhance the marketability of long-term care insurance including:

- Medicare Super Supplements that include both acute and long-term care benefits and create an opportunity to coordinate benefits

- Medicare-HMOs in which HMOs integrate an optional long-term care insurance package with their traditional acute care services for Medicare beneficiaries and provide appropriate case management for all services

- Medicare Vouchers under which Medicare beneficiaries would have the option of receiving a voucher covering the Medicare part of the cost of purchasing private insurance that not only covers Medicare acute care services but could include long-term care benefits

- Retirement Community Reinsurance with CCRCs establishing joint ventures with insurance carriers to underwrite the CCRCs' chronic care guarantee

- Continuing Care at Home models that enable participants to buy into a long-term care risk pool that has a managed care component

- Combined Life and Long-Term Care Insurance to balance different lifetime risks and encourage the purchase of long-term care protection at younger ages

Several States including Washington, California and Colorado, have initiated programs which help consumers select long-term care insurance protection. Developing an appropriate regulatory environment has been difficult for States because of the unfamiliarity of long-term care insurance, which combines features of both health and life insurance. Efforts to protect consumers have sometimes inadvertently worked to stifle the market. A recent study by the National Association of Insurance Commissioners may help clarify issues and serve as a basis for model laws and regulations.

Social Health Maintenance Organizations

A social health maintenance organization (SHMO) is a managed system of health and long-term care services in which a single provider entity assumes responsibility for a full range of acute and chronic care under a fixed budget that is prospectively determined. At present, development of the SHMO concept is highly experimental, being tested by the Health Care Financing Administration (HCFA) in four demonstrations that began operation in March 1985. The demonstrations, selected to represent different organizational possibilities, includes sites in Portland, Oregon; Brooklyn, New York; Minneapolis, Minnesota; and Long Beach, California.

The benefit package offered includes all Medicare benefits, plus a range of long-term care and other supplemental benefits. Copayments for long-term care services are required and long-term care benefits are subject to annual dollar maximums which range from $5,000 to $12,000. The financing arrangements of the demonstrations vary but include capitated payments (which are pooled) from Medicare (for all enrollees), Medicaid (for eligibles) and private enrollees (for non-Medicaid enrollees).

Although SHMOs may have the potential of reaching a large target population, they are still in the early stages of development and can only be operated by explicit statutory waivers of existing program requirements. An independent evaluation of the SHMO demonstration program is being conducted by the University of California, San Francisco and will be completed in 1990.

Continuing Care Retirement Communities

The continuing care retirement community (CCRC) is a financially self-sufficient residential community for the elderly that offers medical and nursing services in specialized facilities. It is based on a lifetime contract between the CCRC and each resident that defines each party's financial and service obligations.

Ordinarily, one of the requirements for admission to a CCRC is that the resident be covered by Medicare and own a medigap insurance policy. As a consequence, nursing home care is the key service added and guaranteed as part of the basic CCRC arrangement. Most CCRCs have their own nursing home facilities within the community. Increasingly, however, CCRCs are contracting with outside facilities to provide needed nursing home care. CCRCs are also beginning to contract with private insurance companies to insure or reinsure nursing home services.

The number of CCRCs is relatively small, with estimates ranging from 300 to 400 communities, serving 100,000 to 200,000 persons. The industry is growing rapidly, with the potential of developing 1,500 more communities by 1990, housing a total of 500,000 persons or two percent of the older population.

Entrance fees range from $15,000 to $175,000, depending in part on the size of the residential unit and the extent of the health care services guaranteed. Monthly service fees range from $300 to upwards of $2,000. Some CCRCs offer contracts in which fees are totally or partially refundable to residents who leave or to their heirs upon death.

CCRCs have attracted the middle class almost exclusively, often former professionals with pensions. Research indicates that 10 to 20 percent of older persons could afford CCRC residence.

Many of the early CCRCs guaranteed total health care for life to residents and were known as "life care communities". Due to inflation, high interest rates and poor actuarial estimates, the costs of providing such guaranteed health care exceeded revenues and led to financial problems in a number of CCRCs, as well as to a few bankruptcies. Although the terms "life care community" and CCRC often are used interchangeably, the newer CCRCs guarantee a more limited range of health care services, with additional services being billed separately.

A number of States have developed legislation aimed at defining life care communities, regulating contracts between communities and residents, and requiring financial disclosure. States without specific life care legislation often review requirements for nursing home beds to be built in CCRCs or implement other State health planning requirements. In addition, the American Association of Homes for the Aging, which represents the predominant non-profit sector, is developing rigorous accreditation standards to safeguard the quality and financial integrity of CCRCs.

Home Equity Conversion Plans

Home equity conversion (HEC) plans are designed to allow a homeowner to convert the equity in a home into a stream of income, without having to move or make immediate repayment. HEC plans differ from home equity loans, which require the homeowner to begin repayment immediately. The assets freed through the HEC plan can be used for any purpose, including the purchase of long-term care services. Although HEC plans have been available since 1961, in 1985 fewer than 1,000 bank or mortgage company financed HEC loans are thought to exist nationwide.

The equity held is usually the older persons most important financial asset, yet it may be difficult to use without having to sell and move from the home. Seventy-five percent (13.4 million) of households headed by older persons in 1984 were homeowners, and most (83 percent) owned their homes free of debt. According to the Census Bureau, the average home equity for persons aged 65 and over was $54,700 in 1984. The aggregate home equity held by the elderly is estimated at $700 billion.

There are three basic types of HEC plans in use. Open term reverse mortgages, the most common commercial type, pay monthly cash advances to the homeowner until he or she dies, reaches age 100 or moves. The effective annual interest rate for this type of mortgage depends on how long the borrower lives in the home and the home's rate of appreciation. In general, the interest rate is very high for loans repaid after a short term but tends to decline the longer the borrower is able to remain in the home.

The second type of HEC mechanism is the sale plan, which enables the owner to sell his home while retaining occupancy rights. The city of Buffalo, New York has been a major public developer of a life estate form of sale plan. Under Buffalo's program, elderly homeowners sell their house to a non-profit entity established by the city in return for a monthly cash annuity for life or lump sum payment. The entity also rehabilitates, maintains and pays the taxes on the house until the owner's death. Through 1985, the program had undertaken about 650 contracts.

Special purpose loans are a third type of HEC plan used by a number of States to provide older homeowners with low interest home equity loans that do not have to be repaid until the borrower dies or sells the home. As used to date, the loans have been designed to help older persons remain in their homes, rather than to pay for long-term care expenses or insurance.

Research findings on the utility of HEC mechanisms for long-term care needs are mixed. One major study by researchers at ICF, Inc. concluded that annuities paid out by HEC plans are not sufficient to generate substantial increases in the number of elderly able to afford long-term care insurance. A study by Jacobs and Weissert in 1983, which adopted different assumptions, concluded that about 5.1 million homeowners could pay for insurance with their home equity payments. Preliminary analyses by Manton and Liu indicate that HEC payment levels would pay the out-of-pocket home care costs for a large number of disabled elderly.

From the point of view of financing long-term care, a major weakness of HEC mechanisms is that is that use of the funds is entirely discretionary (except special purpose HEC loans) and may not end up being used for long-term care expenses. In addition, the mortgage arrangements are complex for both lender and homeowner and older persons have demonstrated strong reluctance to borrow against their home.

Employee Benefit Options for Retirees

The addition of long-term care coverage as a option in the package of pension or health insurance benefits offered to retirees has been suggested as one approach to private financing of long-term care for the elderly. A majority of workers are covered by an employer-sponsored pension plan and a significant number of companies provide health insurance after retirement.

Few companies are now offering long-term care benefits. While there is some suggestion of corporate, employee and labor interest in changing this situation, major barriers exist and a combination of legal, accounting and statutory changes will probably be necessary before many companies will get involved.

The barriers to progress in this area are several. First, employers are increasingly concerned about their large and unfunded liabilities for retiree health and welfare benefits. Benefits are not only becoming a significant percent of payroll but, due to an accounting change under consideration, may soon be required to be disclosed as unfunded liabilities on the financial disclosure statement of companies. Adding to the reluctance to expand benefits are recent court rulings indicating that employers may not be permitted to terminate or cut back on any defined health benefit promised to retirees.

These factors combine to make employers wary of adding any new benefit for long-term care, where demand and costs are expected to grow substantially in the future, unless it is pre-funded. However, recent policy changes under the Deficit Reduction Act of 1984 eliminated the tax advantages of pre-funding retirement health benefits by subjecting investment earnings on retirement health plan assets to current income taxation.

Despite these very real problems, employers could develop long-term care insurance options for retirees. For example, insurance for long-term care could be provided by employers as an additional fringe benefit choice, or employers could simply help form a group so that interested employees could purchase insurance. In this regard, the Federal Government might well be in a position to provide leadership through its Federal Employees Health Benefits Program.

The principal immediate strength of employer-based groups for long-term care financing lies in its potential to expand the market for long-term care insurance. Insurance offered through employer groups would be likely to carry significantly lower premiums, since the risk of adverse selection and marketing costs are minimized in this approach.

Employers could also establish programs which help support employees caring for disabled family members or which help retirees obtain the services they need. A restructuring of pension payout plans to allow for lump sum withdrawals is another way of assisting retirees meet their long-term care expenses.

Tax Allowances for Family Caregiving

Currently, family caregivers provide most of the long-term assistance given to functionally disabled persons living in the community. Public policy support for family caregivers is advocated on the grounds that it can prevent costly institutionalization by reducing the incidence of family "burnout"; relieve the excessive financial and emotional burden on caregivers; and ease the conflicts between work and caregiving responsibilities.

Subject to a number of restrictions, current federal tax policy provides three tools for targeting subsidies to taxpayer households in which dependent elderly persons are living: 1) a $1,000 exemption permitted for each elderly dependent supported by the taxpayer; 2) deductions for medical expenses of dependents if expenses exceed 7.5 percent of income; and 3) a tax credit given employed taxpayers for the care expenses of a disabled spouse or dependent, under the Child and Dependent Care Credit provisions of the current tax code.

None of these tools are widely used by taxpayers nor, as presently structured, are they considered very influential on a family's decisions about whether or not to institutionalize an elderly person. Social and emotional factors typically weigh more heavily than the financial burden in such decisions.

There are numerous Congressional proposals pending which propose further tax benefits for family caregivers. Most build on the child and dependent care credit and attempt to remove or reduce some of the limitations such as the requirement that all taxpayers in the household must be gainfully employed.

Some of the more substantial ideas for assisting family caregivers through the tax system have been developed by the States. Arizona has adopted an unusual variation which permits taxpayers to deduct eligible medical expenses for any elderly person, whether or not they are a relative, living in the State.

Tax subsidy approaches typically assist working caregivers, rather than persons who drop out of the workforce in order to provide another's care. The caregivers who leave or reduce their employment pay a price in foregone earnings and probably also in lower future earnings, both of which will lower his or her later Social Security benefits. To offset this, proposals have been put forward to allow family caregivers to deduct those years in which they provided care from the usual total earning period (35 years) mandated for other Social Security beneficiaries.

Family caregiving may also be assisted by changes in employment policies. More flexible work and leave policies, counseling programs and work-based caregiver support groups have started to attract the attention of business and other groups. A 1985 study by Traveler's Insurance Company found that about 1 in 5 of all company employees over aged 30 had caregiving responsibility for an elderly relative. Other research indicates that the conflict between work and caregiving responsibilities shows up in greater tardiness, lower productivity, and more depression.

Volunteer Systems and Service Exchange

Volunteer work is work or assistance performed without compensation except for expenses incidental to performing the volunteer role, such as supervision, training costs or assistance with transportation. Volunteerism is an important component of the Nation's public and private services systems. Surveys indicate that almost half of all Americans do some sort of volunteer work. Many of these volunteers are over age 65 and the number of older volunteers is expected to increase at twice the rate of growth for the older population itself.

Although many charitable organizations assist with the needs of the elderly, the continuum of long-term care is not a traditional focus for most organized volunteer services. In attempting to envision how volunteers can play an increasing role in meeting the long-term care needs of the dependent elderly, several principles emerge:

-

Volunteer approaches will vary widely because they need to be developed and supported by individuals and community organizations to fit community needs.

-

Volunteers serve to complement paid staff and cannot replace the specialized expertise of professional caregivers.

-

Additional knowledge is needed to support the widespread involvement of volunteers in long-term care, e.g., to identify appropriate assignments and to strike a proper balance between paid staff and volunteers.

-

Volunteer efforts cost time and money, especially those done well. While the value of volunteer efforts can far exceed operational costs, financial assistance is needed for coordination, training and other related costs.

-

Future approaches need to build on existing organizations and systems, rather than create new ones. There are a number of volunteer programs providing services for the disabled elderly, with national, State and local sponsors.

Special Analysis of Individual Medical Accounts (IMAs). Long-Term Care Insurance and Combined Financing Strategies

In March 1986, the Department initiated a series of special analyses designed to assess the potential of IMAs, long-term care insurance and insurance combinations for protecting consumers against the expenses of nursing home care. A total of seven financing prototypes and scenarios were developed and their likely future impact on out-of-pocket and Medicaid expenditures was explored using economic simulations and projections up to the year 2018. The following approaches and scenarios were examined:

- an expansion of the current limit on IRAs to include dedicated savings for long-term care;

- replacement of current IRAs with IMAs;

- long-term care insurance based on an existing private market policy;

- IMAs combined with an insurance (i.e., risk pool) feature;

- long-term care insurance on a wide scale, provided as an employee (pension) benefit;

- limited coverage long-term care insurance purchased by medigap policyholders; and

- varying coverage long-term care insurance, with premiums targeted to 1 percent of income.

It is emphasized that the work performed in developing these projections was highly experimental and the findings should be viewed accordingly.

The special analyses were limited to study of nursing home care expenditures only, primarily because nursing home care is the major cause of catastrophic health expenditures for the elderly. In addition, however, there are no national data on home care expenditures by source of payment to provide a reasonable base for prototype assumptions.

In order to assess the future impact of financing proposals, several prototypes were designed with specific features incorporated. Assumptions were made about who would participate, how much it would cost for what kind of coverage, and how factors such as inflation and induced demand would be factored. To the extent that these assumptions ultimately prove realistic, the simulation findings may be a valid approximation of the possibilities of each proposal.

It should be noted, however, that several of the prototypes and simulations were designed for exploratory purposes only and were not designed to test "realism". Rather, they were intended to give the researchers a general indication of the "upper bound", or maximum, limits of a particular approach. Further analysis of more realistic variations was undertaken only when the upper bound results showed promise.

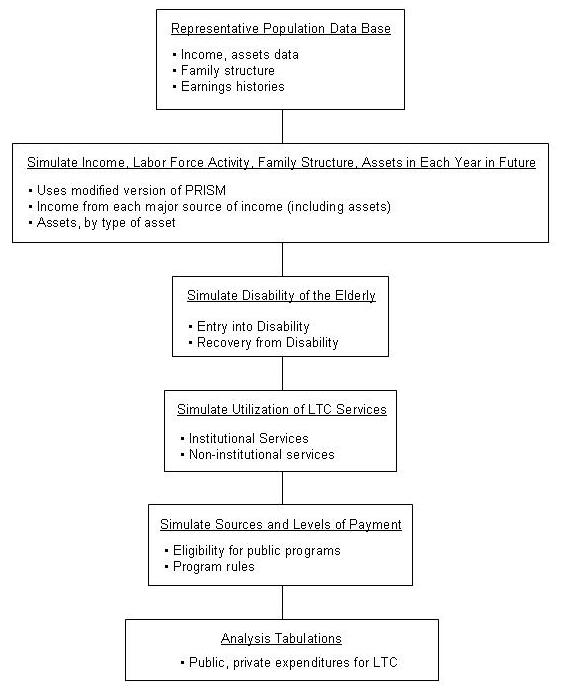

The micro-simulation model used to estimate the impact of the various financing approaches was developed by the Brookings Institution and ICF, Incorporated. The model is based on data and assumptions that allow the user to estimate patterns of earnings, asset accumulation, and disability, and the effect of these factors on the utilization and financing of long-term care over the years 1986 to 2020. One significant limitation of the model is that it does not cover the likely peak disability Years of the "baby boom" generation born between 1945 and 1960. Some important simplifying assumptions included in the model are:

-

Supply is assumed to adjust to demand. Trends in the supply of nursing home beds have been erratic and no readily available methods exist to forecast supply. This assumption is thought to be fairly reasonable for the long modeling period used;

-

The findings discussed below assume a 5.8 percent per year increase in nursing home charges, the same as given in the Old Age Survivors and Disability Insurance and Health Insurance (OASDI and HI) Trustees Reports, Alternative II-B. The general inflation rate assumed is 4.0 percent per year, again the same estimate used in the OASDI and HI Trustees Report;

-

The age-specific rates of utilization of nursing home services were held constant, with only minor adjustments to the 1977 data used to develop the rates.

-

The model assumes that persons will first spend their current income for long-term care-then their assets, and finally will draw on Medicaid. No divestiture of assets to others to qualify for Medicaid is assumed.

The baseline estimates, which provide the basis for comparing the results of the options analyzed, project nursing home expenditures for the elderly as follows (in 1987 dollars):

| Total 1986 expenditures | $29.7 billion |

| Medicaid | $12.9 billion |

| Out-of-pocket | $16.1 billion |

| Total 2018 expenditures | $98.1 billion |

| Medicaid | $46.2 billion |

| Out-of-pocket | $50.3 billion |

FINDINGS OF THE SPECIAL ANALYSES

Expanded IRA Prototype Under this option, the tax-favored savings limit of current IRAs would be increased by $1,000, raising the maximum contribution to $3,000 for an individual and $6,000 for a working couple.

- The additional $1,000 is treated as an individual medical account for nursing home expenses;

- After age 65, funds may be withdrawn from the IRA to pay for nursing home expenses without payment of taxes. Withdrawals for other purposes would continue to be taxed at current marginal rate;

- The requirement that individuals begin withdrawals from their IRA savings by age 70 1/2 is removed and contributions are permitted indefinitely;

- It is assumed that all those who save the additional $1,000 would leave it untouched until the need for long-term care arises, or until death;

- It is assumed that 90 percent of those who saved the maximum in 1983 would save to the new maximum of $3,000.

Projected Impact

- Some IMA funds would be held by 28 percent of persons aged 65 and over by the year 2018;

- Additional IMA savings would pay for about 3.0 percent ($2.9 billion) of total nursing home costs by 2018;

- Out-of-pocket spending would be reduced by 4.3 percent compared to the base case;

- Medicaid spending would be reduced by 1.3 percent.

Replacement IMA Prototype This prototype was developed as a gross "upper bound" model, to explore the possibilities of IMAs in the event that Congressional tax reform actions eliminate IRAs for those with pensions. It is considered useful only as an general order-of-magnitude probe.

- Assumes that IRAs are eliminated entirely;

- IMAs for long-term care would be established, with a maximum contribution of $2,000 per year tax deduction;

- Assumes that everyone who currently participates in IRAs would contribute the same amount to an IMA;

- Tax treatment of contributions and earned interest is unchanged;

- The amounts saved would be tax free if used for long-term care purposes after age 65.

Projected Impact

- IMA savings would pay for 8.5 percent ($8.4 billion) of total nursing home expenditures by the year 2018;

- Out-of-pocket expenditures would be reduced by 11.9 percent;

- Medicaid expenditures would be reduced by 3.9 percent.

Long-Term Care Insurance--Private Market Policy This option modeled a new policy recently issued by Fireman's Fund which offers 6 years of long-term care coverage, with an optional inflation-adjusted benefit. Other features include a 100 day deductible, $50 per day benefit, and a three day prior hospitalization requirement. A very limited home benefit is included. The annual premium charged at age 65 is $506.

- Persons were assumed to buy the insurance if they could afford it for less than 5 percent of their income and if they have $10,000 or more in assets;

- It is assumed that, in 1986, persons aged 67 to 81 will purchase the policy. After 1986, policies will be purchased at age 67.

- No one who is disabled will be allowed to purchase the policy. Persons who become disabled will continue to hold the policy;

- Once a policy is purchased, coverage is continued as long as premiums are less than 7 percent of income and the person has $10,000 in assets;

- Induced demand is reportedly factored into premiums but, due to proprietary considerations, the rate is not known.

Projected Impact

- About 23 percent of those age 65 and over would own the Fireman's Fund policy in the year 2018;

- About 7 percent of total nursing home expenditures would be paid by insurance by 2018;

- Out-of-pocket expenditures would decline by about 12 percent;

- Medicaid expenditures would decline by less than 2 percent.

IMA Combined with a Risk Pool (Insurance) Feature Under this option, a variation of the Bowen-Burke proposal, IMAs would be established with all contributions deposited into an individual account, along with one-half the interest earned. The other half of the interest is placed in a pooled fund and is used to pay a $50 per day benefit to persons with long-term care needs who have exhausted their own account. All interest on the pooled fund remains in the pooled fund. Amounts remaining in the account at death go to the estate.

- It is assumed that 90 percent of all persons who contributed the IRA maximum in 1983 will contribute an additional sum to the IMA;

- Without an induced demand factor, the initial annual contribution necessary for a person age 40 would be $943, and for a person age 60 would be $2,628, over and above the IRA maximum.

- If induced demand is factored in (37 percent), the initial annual contribution necessary for a person age 40 would be $1,497 and, for a person age 60 would be $3,603, over and above the IRA maximum;

- The level of necessary contributions would rise at the rate of inflation, currently estimated at 5.8 percent for the nursing home sector;

- The level of contributions necessary to assure solvency of the pooled fund were calculated by the Department's Office of the Actuary;

- Contributions are waived while an individual is in a nursing home at age 65 or older.

Projected Impact

- About 29 percent of those age 65 and over would have a combination IMA account in 2018;

- Funds saved in the combination accounts would pay about 8 percent of total nursing home expenditures in 2018;

- Out-of-pocket expenses would be reduced about 11 percent;

- Medicaid expenditures would be reduced about 4 percent.

Long-Term Care Insurance Linked to Pension Benefits This scenario linking insurance to pension benefits was developed as a preliminary upper bound test of significantly broader-based participation than is now the case for long-term care insurance models. It is not considered 'realistic, in the near term because of the barriers to broadening pension benefits discussed earlier in the analysis.

- It was assumed that, beginning in 1987, all persons aged 65 and older who start to receive pension benefits of $1,000 or more per year would receive a long-term care insurance policy. The policy would cover a 2 year nursing home stay, have a 90 day deductible period and pay $50 per day in 1986 dollars for nursing home care;

- One half of the cost of the insurance is deducted from the pension;

- Induced demand is not factored into premium estimates.

Projected Impact

- Under these assumptions, about 35 percent of those age 65 and over would have a long-term care insurance policy in the year 2018;

- Insurance would pay about 11 percent of total nursing home expenditures in 2018;

- Out-of-pocket expenditures would decline by 11 percent;

- Medicaid expenditures would decline by nearly 8 percent.

Limited Coverage Long-Term Care Insurance Purchased by Medigap Policyholders This prototype investigated the impact of limited coverage long-term care insurance if purchased by persons who have already demonstrated a willingness to supplement their acute care coverage, i.e., medigap policyholders. Surveys indicate that the percentage of older persons who purchased one or more medigap policies ranged from about 53 percent for persons just above the poverty level, to 77 percent for upper income groups.

- It is assumed that, beginning in 1987, persons aged 67 and over who had purchased a medigap policy, also purchased a 1 year long-term care insurance policy with a $50 per day benefit and 90 day deductible;

- Induced demand is not factored into premiums.

Projected Impact

- About 55 percent of those aged 65 and over would have a one year policy in the year 2018;

- Insurance would pay about 18 percent of total nursing home care expenditures;

- Out-of-pocket expenditures would be reduced about 12 percent;

- Medicaid expenditures would be reduced about 18 percent.

Varying Coverage Long-Term Care Insurance with Premiums Targeted at 1 Percent of Income Assuming some long-term care insurance coverage might be better than no protection, this prototype simulates the impact of providing persons with varying levels of insurance, depending on what they could purchase with 1 percent of income.

- It is assumed that, beginning in 1987, persons age 30 and over purchase the maximum coverage available (1 to 6 years or unlimited) that costs no more than 1 percent of their income. Policies would pay $50 per day benefit, with a 90 day deductible period;

- If premium exceeds 2 percent of income for three consecutive years while under age 65, the coverage is dropped by 2 years (or from no limit to 6 years;

- Persons aged 65 or over in 1987 are assumed to purchase the longest coverage that costs no more than 3 percent of income, if assets are $10,000 or more. If premiums exceed 5 percent of income for three consecutive years, then the coverage is dropped by 2 years;

- Induced demand is not factored into premiums.

Projected Impact

- Under these assumptions, about 63 percent of those aged 65 and over would own an insurance policy in 2018;

- Insurance would pay about 17 percent of total nursing home expenditures in the year 2018;

- Out-of-pocket expenditures would decline by about 18 percent;

- Medicaid expenditures would decline by about 12 percent.

The Effect of-Induced Demand on Projected Impacts

Experience has shown that when the direct cost of a health service is reduced for a consumer, either due to lower costs or increased payment by a third party (insurance), demand for that health service increases. Although the decision to enter a nursing home is generally considered a 'last resort, decision, it is reasonable to assume that financial considerations play some role. Should nursing home insurance (public or private) become more widely available, the financial barriers will be reduced and entry into nursing homes will be facilitated. Utilization rates for nursing homes can be expected to rise.

The problem for researchers and insurance companies is, "What level of additional induced demand will be generated by widespread use of long-term care insurance mechanisms?" No reliable data are available for the precise determination of what the rate should be.

Most persons agree that induced demand in the nursing home sector will be less than has been the case with acute care, because of the biases against entering a nursing home. The level will also be affected by the broadness of the coverage offered, i.e., the cost to the consumer of using the policy. Factors such as up-front deductibles (elimination periods) and copayments (benefits may cover all or only part of the daily cost) can be expected to significantly affect the induced demand factor.

The factors used in this report are based on the expert judgement of the Office of the Actuary (Social Security Administration) and could arguably be more or less. Detail concerning the effect of induced demand on premiums or contributions is provided in the full report.

An example of the effect of induced demand can be seen by comparing the results of the last option cited above (Long-Term Care Insurance/Premiums Targeted at 1 Percent) with the projected impact of the same option when induced demand is factored at 11 percent. When induced demand is considered, overall expenditures for nursing home care increase by 2.3 percent. The amount of total nursing home expenditures paid by insurance is 15 percent, rather than 17 percent; out-of-pocket expenses are reduced by 14 percent, rather than 18 percent; and, Medicaid expenditures are reduced by about 9 percent, rather than 12 percent.

THE RELATIONSHIP OF MEDICAID TO PRIVATE FINANCING MECHANISMS

Medicaid was established in 1966 as a joint Federal-State program to provide medical assistance to certain groups of low-income individuals. About half of total Medicaid expenditures in 1984 were for long-term care, including skilled, intermediate, home care, and mental health services as well as services for the mentally retarded.

Medicaid is a welfare-based system. Medicaid eligibles include the low-income aged, the blind, the disabled and those eligible for Aid to Families with Dependent Children (AFDC). States may also cover benefits for "medically needy" individuals and nursing home residents with incomes up to 300 percent of the Supplementary Security Income (SSI) payment level.

There has been some concern that Medicaid acts as a disincentive to the purchase of private protection. The issue has two related aspects: that because Medicaid is available, people will not give serious attention to long-term care insurance and other privately financed protection; and that people with resources will "game" the system by passing their assets along to others or protecting them in a trust, thus becoming eligible for Medicaid benefits.

A recent critique of these issues concludes that these concerns may be considerably overemphasized. The analysis presented in Chapter 4 of the report suggests that while incentives for people to alter their behavior to qualify for State-supported benefits do exist, it is not at all clear that significant numbers of people are responsive to such incentives.

First, the public's understanding of how long-term care is paid for and what coverage people actually have is very poor. A recent national survey of members of the American Association of Retired Persons revealed that 79 percent of those who expected at some point to have an extended nursing home stay, thought that Medicare would pay for all or part of this care. About one-third of those with private medigap insurance coverage incorrectly believed that their policies would cover extended nursing home care.

A second consideration in evaluating Medicaid's impact on private financing mechanisms is evidence that middle-class people are generally not disposed to rely on a welfare-based program for long-term care expenses. For example, a recent study by the National Center for Health Services Research of 4,000 older persons in six states found that only 19 percent said they would not purchase long-term care insurance because they viewed Medicaid and other welfare coverage as adequate.

The degree to which the elderly are aware of and willing to use methods of circumventing Medicaid's asset restrictions is also unknown. However, asset protection requires considerable advance planning and an awareness of Medicaid eligibility rules and, in general, is both difficult and expensive to accomplish.

The considerations mentioned above suggest that Medicaid is not currently a significant barrier to private financing of long-term care. However, this does not preclude the possibility that changes in Medicaid could have a positive impact on private financing mechanisms. As a consequence the report describes, but takes no position on the merits of, several approaches which would make it more difficult for persons who can afford to pay for their own long-term care costs to become eligible for Medicaid. These proposals would:

- Severely restrict Medicaid eligibility to prevent persons from qualifying for Medicaid benefits if they could once have afforded to provide for long-term care insurance in a prior period;

- Permit States to require spouses of Medicaid recipients to contribute to the cost of their spouse's care;

- Allow States greater flexibility in use of liens imposed on recipients, property before death; and

- Require States to restrict Medicaid eligibility of people with assets sheltered in trusts.

Another approach currently receiving some attention (but not advocated by the report) would waive Medicaid spend-down requirements for persons who financed their own care for a fixed period, e.g., one or two years. Medicaid would pay for the full costs after the consumer paid the front-end long-term care costs. The point of this would be to increase the marketability of private financing strategies such as insurance.

This approach would build on the fact that there is a significant effect on the affordability of insurance premiums when the period of coverage is limited. For example, a two year, $50 a day nursing home policy purchased at age 65 costs approximately $650 per year. A lifetime policy (no limit on nursing home coverage) purchased at the same age would cost about $1400.

One critical issue is whether the increased affordability of a limited nursing home policy, in combination with waiving spend-down, would expand participation under an insurance option enough to offset the drain on Medicaid. The intuitive answer is that it would not. The analyses done to date suggest that the people who would purchase long-term care insurance are not the people who end up on Medicaid. Therefore, picking up the Medicaid costs for everyone at the end of one or two years would end up increasing Medicaid costs over current projections. If one factors-in induced demand, the problem for Medicaid is worse.

Another major problem with this proposal is the issue of equity. Persons at higher income levels who could afford insurance would have their assets protected. Persons at lower income levels who could not afford insurance would lose everything. In essence, such a proposal would create a new Federal long-term care benefit, but only for those who are already well-off.

CONCLUSIONS

Federal, State and local governments pay almost half the costs of long-term care services received by older persons in the United States. Almost all the rest is paid directly by individuals or families who are largely unprotected by insurance or other types of mechanisms that shield the individual from catastrophic health expenses. It is evident that the vast majority of older Americans would greatly benefit if suitable and effective private financing mechanisms for long-term care were more widely available, at a reasonable cost.

This report has analyzed the feasibility and effectiveness of a broad range of private financing strategies which can assist persons in paying for long-term care. Of particular interest has been the extent to which these strategies can be expected to attract broad participation and help limit the out-of-pocket expenditures for individuals.

Clearly, the private financing strategies discussed in this report cannot solve all of the problems associated with catastrophic long-term care costs, especially for those at the low end of the income scale. There will continue to be a need, regardless of the potential of private solutions, for a public role in assisting people who need formal long-term care services and who cannot afford private means of protection. Further, there will continue to be a need to assist those individuals and families who, despite advance planning and private financial protection, encounter long-term care expenses that are well beyond ordinary means.

Nevertheless, private financing mechanisms can help a substantial number of individuals protect themselves and their families against the high costs of nursing home and other long-term care expenses. However, these options for private financing are neither well-developed nor widely known. This report is intended to serve as both a summary of what is presently known about the need for and costs of long-term care, as well as to promote a better understanding of the potential of private financing mechanisms and of how their use might be further developed.

The report has determined that the potential for expanding private financing mechanisms is significant and should be carefully nurtured. The analysis has demonstrated the potential of private mechanisms. However, the analysis also indicates that, while the economic status of the elderly is improving, one of the central problems in realizing the potential is the affordability of the private financing approaches.

The report also stresses that the great majority of elderly will not require extended nursing home stays during their lifetime. Those that do, encounter expenses that can easily deplete the savings of a lifetime. The challenge to private financing mechanisms is to bring the cost of protection within the means of a wider segment of the older population. This will enable the elderly to translate their resources into protection from financial ruin.