U.S. Department of Health and Human Services

October 2011

Prepared by:

The Offices of CLASS, ASPE, and the General Counsel

For additional information, you may visit the DALTCP home page at http://aspe.hhs.gov/_/office_specific/daltcp.cfm or contact the office at HHS/ASPE/DALTCP, Room 424E, H.H. Humphrey Building, 200 Independence Avenue, SW, Washington, DC 20201. The e-mail address is: webmaster.DALTCP@hhs.gov.

"Introduction

The Community Living Assistance Services and Supports (CLASS) Act was enacted as Title VIII of the Patient Protection and Affordable Care Act (ACA), P.L. 111-148 (Mar. 23, 2010), which amended the Public Health Service Act, 42 U.S.C. section 201 et seq., by adding the CLASS Act as Title XXXII. The law was designed to establish a voluntary, national insurance program for American workers to help pay for long-term services and supports they may need in the future. The CLASS program seeks to help enrollees live independently in the community and to give them considerable freedom to determine the necessary services and supports they purchase with their coverage. By statute, CLASS benefits must be funded entirely through enrollee premiums; there is no taxpayer subsidy. Appendix A includes a description of the Act that was prepared by the CLASS Office to guide their work.

There is a critical need to find ways to help Americans prepare for their long-term care needs. Almost seven out of ten people turning age 65 today will experience, at some point in their lives, functional disability and will need some paid or unpaid help with basic daily living activities. While most people who need long-term care are in their 70s and 80s, young people also can require care, with 40 percent of long-term care users today between the ages of 18 and 64.

Long-term care is also expensive. While costs for nursing home care vary widely, they average about $6,500 per month, or anywhere from $70,000 to $80,000 per year. People who receive long-term care services at home spend an average of $1,800 per month. Expected lifetime long-term care spending for a 65 year old is $47,000; sixteen percent will spend $100,000 and five percent will spend $250,000. Medicare does not cover long-term care services. Medicaid pays for such services only for people with limited financial means; qualifying for Medicaid often means exhausting all other resources.

Furthermore, few private mechanisms are available to help people plan ahead to pay for their future care. Long-term care insurance, by far the most popular private option available, can be costly and difficult to purchase for those with pre-existing health conditions or disabilities. Only about 2.8 percent of Americans have a policy. For workers who already experience a disability and a need for long-term services and supports, the options are even fewer.

The CLASS Act would add a new option for people who are employed. Among the unique and attractive features that differentiate it from long-term care insurance products available on the private market are that it offers lifetime benefits, is not underwritten, and provides a cash benefit.

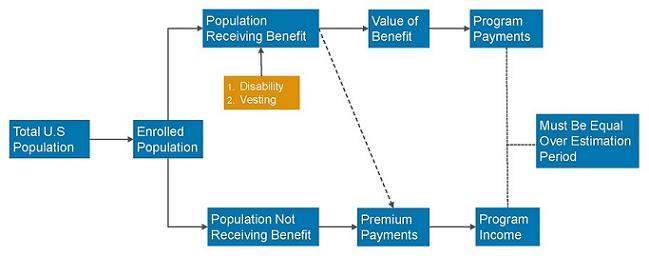

The CLASS Act directs the Secretary of the Department of Health and Human Services (HHS), “in consultation with appropriate actuaries and other experts, [to] develop at least 3 actuarially sound benefit plans as alternatives for consideration for designation by the Secretary as the CLASS Independent Benefit Plan under which eligible beneficiaries shall receive benefits under” the law. The Act requires that each of the plan alternatives be designed to provide the benefits specified in the law consistent with a set of requirements, also specified in the law, concerning, among other things, premiums, the vesting period, benefit triggers, and the cash benefit. Of particular significance, the Act makes clear that the Secretary shall establish premiums for each plan “based on an actuarial analysis of the 75-year costs of the program that ensures solvency throughout such 75-year period.”

Consisting of two parts, this report documents the work undertaken by the Department of Health and Human Services (HHS) to fulfill the Secretary’s responsibilities under the law. Part One describes the organizational, analytical, policy, and implementation steps taken by HHS to develop the CLASS plan alternatives and prepare for implementation. Part Two provides legal analysis of the plans undertaken by the Office of the General Counsel.

This report also includes numerous links to material posted on the Web and over 200 pages of appendices. These materials more fully describe ideas that are only summarized in the report for the sake of brevity and readability. Complete descriptions of all the CLASS benefit designs that were considered can be found in the report of the CLASS Chief Actuary in Appendix O. We also include links to influential research briefs and analyses that helped shape the thinking behind the policies that are discussed in the report. In the interest of openness and transparency, we have also included relevant information about consultations and meetings with experts and stakeholders.

Part I: Developing the Class Program

This Part describes the organizational, analytical, policy, and implementation steps taken by HHS to develop the CLASS plan alternatives and prepare for implementation. It consists of seven sections. Section One outlines the offices and divisions within HHS and the roles played by them, and the functions and status of two federal advisory committees created by the CLASS Act. Section Two briefly outlines the HHS process used for identifying policy issues and enumerates the issues identified. Significant documents (both internally and externally developed) that informed policy and implementation discussions are noted. Section Three lists public presentations, along with links to the relevant Congressional hearing record. Section Four discusses the work undertaken to draft proposed regulations. Section Five presents the activities conducted to support marketing the program to employers and individuals, as well as consumer research. Sections Six and Seven describe the development of two actuarial models for conducting estimates for CLASS premiums and the plan options that were developed and modeled, respectively.

Section One: HHS Management

Pre-Enactment

The Office of Disability, Aging and Long-Term Care Policy in the Office of the Assistant Secretary for Planning and Evaluation (ASPE) led the analytical work relating to CLASS prior to enactment. For 30 years, ASPE has maintained the only office in the federal government dedicated to long-term care (LTC) policy research and analysis. ASPEs LTC research portfolio includes, among other topics, an extensive array of projects on LTC reform, planning and awareness, insurance, community services and financing. ASPE originated and managed the Cash and Counseling demonstration, on which the CLASS cash benefit is based.

In the months leading up to the passage of the ACA, the Department was asked to provide technical assistance on the CLASS program to Members of Congress and staff. That technical assistance was provided by senior staff from the Administration. The technical assistance was based, in part, on analyses conducted by HHS using pre-existing actuarial and economic studies of CLASS and similar proposals (including analyses by the CMS Actuary, http://www.cms.gov/ActuarialStudies/Downloads/HR3962_2009-11-13.pdf, http://www.cms.gov/ActuarialStudies/Downloads/S_PPACA_2009-12-10.pdf http://www.cms.gov/ActuarialStudies/Downloads/S_PPACA_2010-01-08.pdf and the American Academy of Actuaries, http://actuary.org/pdf/health/class_july09.pdf), data on disability rates among workers, and data based on state experiences with various LTC financing initiatives. These senior leaders were asked to brief House and Senate Committee members and their staff in person and by telephone during the fall of 2009.

In October 2009, prior to enactment, ASPEs Deputy Assistant Secretary for Disability Aging and Long-Term Care Policy discussed the bill at a meeting held by the Kaiser Family Foundation. There he emphasized the Departments support for the program but also recognized that it faced significant challenges that would need to be addressed (http://www.kff.org/healthreform/kcmu102009pkg.cfm).

In September and December 2009, HHS met with House and Senate staff about CLASS. During this same period, HHS also met to discuss CLASS with the Actuary for the Centers for Medicare and Medicaid Services (CMS) and with staff of the Congressional Budget Office (CBO). HHS also held meetings with the American Academy of Actuaries and the Social Security Administration (SSA) Actuary. In December and January, Senate staff asked HHS to begin developing a list of technical corrections to the bill, to address concerns on which there was broad consensus.

Post-Enactment

Upon enactment of the ACA, the Secretary established implementation work groups, including the Long-Term Care Work Group, which was charged with overseeing the identification and analysis of policy issues related to CLASS and the multiple Medicaid long-term care provisions of the ACA. With participation from across HHS, this group was co-chaired by ASPEs Deputy Assistant Secretary for Disability, Aging and Long-Term Care Policy and the Director of the CMS Disabled and Elderly Health Programs Group. More details about the work group are provided below under Identification, Analysis, and Discussion of Policy Issues.

On April 22, 2010, the CMS Actuary issued a memo on the estimated financial impact of the ACA. Regarding the CLASS program, he asserted that after fiscal year 2025:

The new Community Living Assistance Services and Supports (CLASS) insurance program would produce an estimated total net savings of $38 billion through fiscal year 2019. This effect, however, is due to the initial 5-year period during which no benefits would be paid. Over the longer term, expenditures would exceed premium receipts, and there is a very serious risk that the program would become unsustainable as a result of adverse selection by participants.1

In late spring 2010, Secretary Sebelius asked Kathy Greenlee, Assistant Secretary for Aging, to take the lead on implementing CLASS.2 ASPE worked closely with the HHS Assistant Secretary for Administration to develop alternative designs for the location and structure of the CLASS office.

CLASS staff recruiting began in October 2010. A detailee from the U.S. Office of Personnel Management who had experience implementing and managing the Federal Long-Term Care Insurance Program led the effort. Also during this time, one staff person from the HHS Office of Medicare Hearings and Appeals (OMHA) began a three month detail to work at ASPE on the policy and implementation issues related to CLASS appeals. The first non-detailed CLASS staff member was hired September 27, 2010, the CLASS Chief Actuary began work in January 2011, and approximately 14 FTEs were hired by May 2011. As of October 15, 2011, there are seven individuals assigned part or full time to the CLASS office.

In late 2010 HHS decided to place the CLASS Office within the Administration on Aging (AoA), and published a notice of reorganization in the Federal Register on January 28, 2011 (Appendix C). The basis for that decision was that it would be the most cost-effective way of implementing and running the CLASS program. At that time, the Assistant Secretary for Aging was named the Administrator of the CLASS program. The Long-Term Care Work Group was disbanded in March 2011.

ASPE continues to conduct policy analysis and research to inform CLASS implementation and, most significantly, to maintain and run the two actuarial models that were developed to generate CLASS premium and participation estimates. Details on ASPEs research and on the actuarial models appear in subsequent sections of this report.

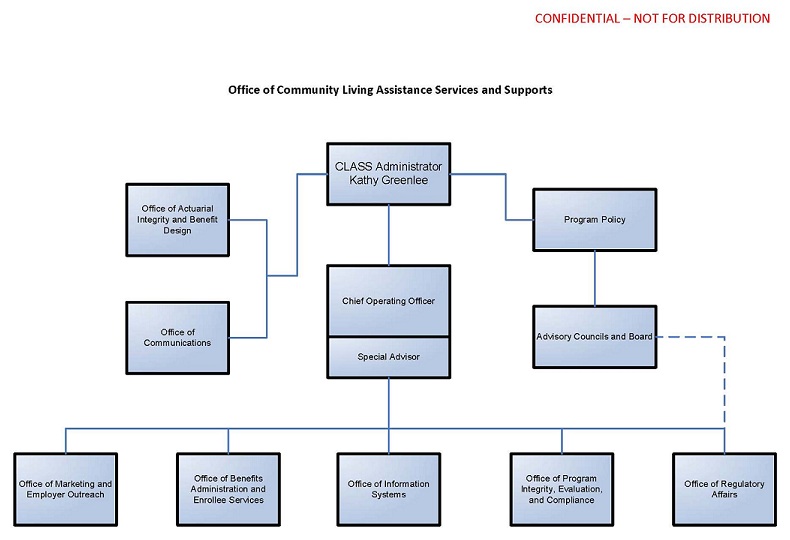

Organization of the Class Office

The CLASS Office was originally organized into six divisions:

- Actuarial Integrity and Benefit Design

- Benefits Administration and Enrollee Services

- Regulatory Affairs

- Information Systems

- Marketing and Employer Outreach

- Program Integrity, Evaluation, and Compliance

An organizational chart is located in Appendix D. Each division developed work plans, delineating the steps and products necessary to move to full program implementation. These work plans were put together in a flow chart so that CLASS management could be coordinated across many functions. (Appendix E contains the summary flow chart.)

Class Federal Advisory Committees

The CLASS Act authorizes two Federal Advisory Committee Act panels: the CLASS Independence Advisory Council and the Personal Care Attendants Workforce Advisory Panel. The CLASS Office has a contract in place to plan and manage the meeting logistics for both committees.

-

CLASS Independence Advisory Council

Secretary Sebelius signed the charter for the CLASS Independence Advisory Council on November 9, 2010. This Council is charged with advising the Secretary on matters of general policy in administering the CLASS program and formulating regulations. A notice appeared in the Federal Register on November 16, 2010 announcing the establishment of the Council and soliciting nominations. (Appendix F) The nomination period was open from November 16, 2010 to December 1, 2010 and the CLASS Office received over 140 nominations. The Council has not been named yet.

-

Personal Care Attendants Workforce Advisory Panel (PCAWAP)

The PCAWAP was authorized in the CLASS Act but is not directly related to the CLASS benefit. The purpose of the Panel is to examine and advise the Secretary and the Congress on workforce issues related to personal care attendant workers. Secretary Sebelius signed the charter for the PCAWAP on June 4, 2010. A notice establishing the Panel and a call for nominations appeared in the Federal Register on June 16, 2010.

An initial nomination package was sent to the Office of the Secretary (OS) in October 2010. Upon review, the list of proposed panel members was revised and a new nominations package was sent to the Secretary in April 2011. Secretary Sebelius approved the nominations and sent letters of invitation to the nominees. Thirteen of the fifteen nominees accepted, and those members have completed the HHS Human Resources on-boarding process required for Special Government Employees. Additional nominees have been identified to fill the two open seats, but final selections have not been made. Appendix G contains the PCAWAP announcement and membership list.

Section Two: Identification, Analysis, and Discussion of Policy Issues

Long-Term Care Work Group

In addition to its chairs, ASPEs Deputy Assistant Secretary for Disability, Aging and Long-Term Care Policy and the Director of the CMS Disabled and Elderly Health Programs Group, membership in the Long-Term Care Work Group included representatives from: the Immediate Office of the Secretary; the Administration on Aging; the Offices of the Assistant Secretaries for Legislation, Financial Resources, and Administration; the Office on Disability; the Administration on Developmental Disabilities; the Office of the General Counsel; the Office for Civil Rights; the Substance Abuse and Mental Health Services Administration; the Indian Health Service; the National Institutes of Health; and the Executive Secretariat.

Members of the group took responsibility for preparing policy papers and presenting their work at weekly meetings. The groups primary purpose was to review the CLASS statute thoroughly, and to identify all of the policy issues that needed to be addressed. Leaders of the group briefed senior HHS leaders.

The issues presented and discussed are summarized below; the full papers are contained in Appendix H.

Enrollment and Vesting. This discussion covered five significant enrollment issues: (1) opt out and payroll deductions; (2) alternative enrollment processes; (3) penalties for lapsing; (4) delays in CLASS enrollment; and, (5) the definition of active employment. The group noted that both CBO and the Business Roundtable had identified the issue that the law mandated automatic enrollment only for employees whose employer had elected to participate in CLASS and that it was not likely that many employers would do so. Other options for enrollment such as employers offering information or a yes/no choice were discussed. Group members analyzed the implications of policy holders lapsing, or skipping multiple payments. Thus, individuals could strategically (and legally) game the program, threatening financial stability. The group considered a variety of strategies for addressing the lapsing issue. The group also considered different ways to approach the earnings requirement during the vesting period. The group discussed whether individuals would be required to pay premiums while in benefit status. In an early meeting with representatives from the IRS, HHS officials learned that the IRS code had not been amended to cover payroll deductions for CLASS premium payments so that the protections that addressed the potential failure of employers to pay money withheld from other payroll deductions would not apply to the automatic withholding of CLASS premiums. Enrollment options were discussed to address this concern.

Indexing of Premiums. Based on internal analyses and discussions with outside experts, there was a concern that structural imbalances created by the statutory requirement to index benefits but not premiums would result in threats to take-up and solvency. The group analyzed and discussed the implications of both indexing and not indexing premiums.

Eligibility. The group discussed a number of eligibility issues, including the definition of a licensed health care professional and how limitations in activities of daily living (ADLs) would be assessed for individuals with dementia and other non-physical impairments. The group suggested that the actuaries model the program using as eligibility triggers two and three ADLs to support future decision making. The group also noted that the tiering provisions in the CLASS Act, which provide that there must be at least two levels of cash benefits depending on the individuals functional limitations, could create incentives to overstate ADL limitations. It was therefore important to consider the design of the benefit tiers carefully. The group also commissioned a paper on assessment of people with cognitive impairments. This paper is discussed under Additional Analyses, below.

Cash Benefits. The work group discussed cash benefits -- including their structure and management and consumer privileges, responsibilities and issues related to using debit cards for cash benefits. Much of the analysis was based on extensive ASPE sponsored research on cash benefits and consultation with experts from other nations that use cash benefits for long-term services and supports.

Protection and Advocacy and Advice and Assistance. The group suggested that protection and advocacy (P&A) and advice and assistance services, which are required benefits under the CLASS Act, should be targeted to beneficiaries once they are in claim status.

Administrative Expenses. The group discussed various ways to analyze and implement the statutory three percent cap on administrative expenses provision. ASPE directly analyzed data from regulatory filings from several states, obtained information from outside actuaries and contracted for additional actuarial analyses from the Actuarial Research Corporation (ARC). It concluded that the range of administrative costs is six to twenty percent in the private LTC insurance industry.

Interaction with Medicaid. The group discussed how the Department could address the multiple interactions between Medicaid and the CLASS program.

Additional staff analyses provided to the work group on marketing and information systems are discussed in detail elsewhere in this report.

Additional Analyses

ASPE procured four immediate analyses in order to address issues related to CLASS policy development and implementation; in addition, consistent with ongoing long-term care planning and awareness research done over the past eight years, ASPE contracted for a consumer survey and series of focus groups about LTC planning. The CLASS Office published a Request for Information on enrollment and premium administration systems (see Appendix I); no contracts have been awarded for administration systems.

The four analyses procured by ASPE, found in Appendix J, are:

-

A paper on underwriting (specifically, on individuals who are typically precluded from buying private LTC insurance policies because of underwriting) from LifePlans. This paper provided insight into a potential target market, individuals who are interested in purchasing LTC coverage but are unable to do so due to underwriting. The paper concluded that additional research would need to be conducted on this pool of likely buyers to ensure that their risk profile is taken into account in setting program premiums.

-

A paper on assessment instruments and procedures for identifying ADL impairment equivalents in individuals with cognitive impairments, by Katie Maslow, an independent consultant and nationally recognized expert in dementia. This work provided a thorough review of strategies for assessing the eligibility of people with dementia for LTC programs.

-

A Strategic Analysis of HHS Entry into the LTC Insurance Market, in which business experts analyzed the LTC insurance industry and the CLASS statute and offered their views on how CLASS could be positioned and how private industry might respond. The authors noted the possibility that private companies might begin offering CLASS-like products.

-

An exploration by Univita (a private company that provides administrative and management support to LTC insurance companies) about cash benefits in the private LTC insurance market. This paper concluded that consumers prefer cash for the flexibility it offers, but that cash benefits are more expensive to administer because of the recordkeeping involved.

Review of Key External Papers and Analyses

In addition to commissioning papers and conducting internal analyses, HHS staff and leaders reviewed a large number of papers and reports written outside the Department. These included:

- Kaiser Family Foundation briefs on CLASS

- A National Health Policy Forum brief on CLASS

- A series of papers commissioned by the SCAN Foundation (http://www.thescanfoundation.org/commissioned-supported-work/class-technical-assistance-briefs)

- An actuarial analysis by Milliman (http://publications.milliman.com/publications/healthreform/pdfs/perspectives%20on-community-living.pdf)

- The experience of the California Public Employees Retirement System

- An actuarial analysis of an earlier formulation of CLASS that had been commissioned by AARP.

Meetings with Experts and Stakeholders

To inform the policy development process, HHS staff met with a wide range of experts and stakeholders with an interest in CLASS, as well as others with related interests. These included:

- Groups focused on providers of aging and disability home and community based services

- Consumer organizations representing long-term care users with disabilities (including groups focused mainly on seniors and multiple subgroups within the disability community)

- Nursing home and other provider organizations

- Organizations representing the long-term care workforce, including organized labor

- Representatives of the insurance industry

- Foundations interested in long-term care

- Payroll management and support companies

- State Medicaid, mental health and intellectual disabilities officials and the associations that represent them

- Actuaries with expertise in disabilities or long-term care.

A detailed listing of these meetings can be found in Appendix K.

Section Three: Public Presentations

The Department presented and discussed its work on CLASS in numerous public meetings and Congressional hearings following enactment. Public presentations included forums and meetings sponsored by AcademyHealth, Alliance for Health Reform, AARP, the Long-Term Care Discussion Group, and the Kaiser Family Foundation (where Secretary Sebelius spoke about CLASS in February 2011; the speech can be accessed at http://www.hhs.gov/secretary/about/speeches/sp20110207.html).

CLASS leaders and staff spoke at national meetings (e.g., 17th Annual Policy Briefing of the National Association of Area Agencies on Aging, Intercompany LTC Insurance Conference) in March, April and May 2011. Administrator Greenlee spoke about CLASS to the American Health Lawyers Association in February 2011 and to the Society of Professional Benefits Administrators in March 2011.

In addition, CLASS was the focus of a hearing held by the House Energy and Commerce Committee, Subcommittee on Health on March 17, 2011. (Written testimony can be accessed at http://republicans.energycommerce.house.gov/Media/file/Hearings/Health/031711/Greenlee.pdf) Secretary Sebelius also discussed CLASS at a March 30, 2011 hearing before the Senate Finance Committee.

Section Four: Regulation Development

The CLASS Office began developing CLASS Act implementing regulations in January 2011, building on the policy option papers prepared by the LTC Work Group and legal advice from the HHS Office of General Counsel (OGC).

The CLASS Office prepared the CLASS Regulations Development Plan (CLASS RDP) document in February 2011. The CLASS RDP established a framework for rulemaking and compiled documents describing: the roles and responsibilities of the various entities participating in the regulation development process; the Secretarys rulemaking authorities and requirements; rulemaking steps; development activities; and other considerations.

Also in February 2011, the CLASS Office began forming the CLASS Regulations Project Team, an interdepartmental group of subject matter experts that included representatives from ASPE, the Centers for Medicare and Medicaid Services (CMS), the Office on Disability (OD), the Office for Civil Rights (OCR), and the Office of the General Counsel (OGC). The team was tasked with providing initial informal review of draft regulations. Ultimately the CLASS Office determined that additional actuarial and legal work was required prior to drafting the appropriate regulatory language needed for the Notice of Proposed Rulemaking (NPRM). After the CLASS Chief Actuary was hired, the CLASS Office recognized that several critical issues needed to be more fully developed internally before regulations could be developed.

Many of the regulations related solely to operational aspects of the CLASS program have been drafted. For example, the CLASS staff has made significant progress in drafting regulations in the following areas: enrollment; waiver of automatic enrollment; lapse in enrollment and disenrollment; reenrollment; payment of premiums; and benefit eligibility. The draft regulations did not address key benefit design issues because policy and legal analysis were still underway.

Section Five: Marketing Research and Ltc Planning

Secretary Sebelius and Administrator Greenlee have clearly stated on multiple occasions that the CLASS program will not go forward unless it is solvent, sustainable, and consistent with the law. Program solvency depends on premiums, benefit payouts, and take-up rates -- enough people buying CLASS policies. Attracting enrollees with lower health risks, people who pay premiums over a long period of time before needing long-term services and supports, is also critical. Achieving sufficient take-up rates and attracting an average mix of enrollees with respect to their health status both depend heavily on marketing.

To prepare for implementing the CLASS program, the Department made a targeted set of investments in consumer awareness and marketing of possible CLASS benefit options that are described below. Not all of the findings from the marketing research are available yet. The research will provide an understanding of: how potential buyers think about long-term care planning; how they make decisions about what and when to buy and how much they are willing to spend; and, how employers think about whether to offer LTC coverage and how they would respond to the opportunity to offer CLASS to their employees. HHS commissioned this research in order to understand whether potential CLASS plan designs would be attractive to a large enough group of buyers. The observations about marketing that are made later in this report rest on preliminary analyses of the marketing research conducted thus far or consultations that HHS has had with experts in long-term care insurance.

In addition, HHS has conducted research for the past fifteen years to understand consumers knowledge about long-term care, their experiences arranging or providing care, their attitudes about planning ahead, and their assessment of their own risk for needing long-term care. HHS has considered findings from this research in formulating and modeling premiums and take-up rates for the proposed plan options.

Initial CLASS Marketing Strategy. Initial planning for a CLASS marketing strategy identified two primary sets of customers -- employers and consumers. For CLASS to obtain a sufficient level of enrollment, marketing campaigns would have to target both groups. To determine how best to market to each group, HHS sought to learn more about their respective attitudes and preferences, then identify those within each group who were most likely to participate in the CLASS program. To prepare for developing marketing strategies for both groups, several research and message development procurements were conducted by ASPE and the CLASS Office in the three following areas: Consumer Research, Employer Research and Long-Term Care Awareness Activities.

Long-Term Care Awareness Survey. In 2010, ASPE awarded a contract to RTI International to design a large, nationally-representative survey to study the attitudes, experiences, opinions and actions of Americans related to planning for long-term care services. The data collection contract was awarded to Knowledge Networks. At the time of contract award, ACA had not yet passed and the purpose of the contract was to gain knowledge for future phases of existing long-term care policy (such as the Own Your Future campaigns). Upon passage of ACA, ASPE expanded the scope of the project to include background research for CLASS. The survey, which is not yet completed, will also employ a discrete choice experiment that will measure individuals preferences for various attributes of plans at specific price points.

Qualitative Research. ASPE contracted with Thomson Reuters to conduct a number of in-person focus groups and interactive discussions as part of the background research for both the CLASS program and the larger survey effort. Participants in the focus groups, which took place in three cities (Baltimore, MD, St. Louis, MO and Edison, NJ) considered the value to consumers of various CLASS program proposals, consumers cost/benefit analyses and their reaction to federal government sponsorship. The research sought to help identify factors that facilitate or inhibit planning for long-term care. Knowledge Networks convened the interactive discussions using members of their KnowledgePanel®. The data from the interactive discussions informed hypothetical questions for the design and administration of the survey mentioned above. Each interactive and in-person discussion solicited from participants reactions, opinions and ideas related to various aspects of long-term care planning and awareness.

Highlights of the findings from the focus groups include: (1) women are more likely to believe that they will need care in their older years compared to men; (2) the belief that one will need long-term care does not necessarily translate into purchasing LTC insurance; (3) many people believe that postponing the purchase of insurance will save money; and (4) many people think that an insurance policy should cover all costs of care; anything less is inadequate. Respondents reacted negatively to vesting periods and complicated benefit plans. Respondents reacted positively to the absence of underwriting, and the option of a cash benefit. Reasons for not purchasing insurance involve cost, first and foremost, but also involve other expenses (such as college tuition and weddings), a perception that insurance is akin to gambling, and the lack of a perceived need for it (particularly among men). Respondents also believed that there should be incentives to purchase long-term care insurance, such as tax deductions.

Development of a Strategic Brand for CLASS. The CLASS Office released a solicitation to develop a strategic brand for CLASS, but no procurement was awarded.

Employer Research. The CLASS Office released a solicitation to assess the potential for employers of all types and sizes to sponsor the CLASS program as a voluntary employee benefit, but no procurement was awarded.

Long-Term Care Awareness Activities

The CLASS Office released a solicitation to design a plan for a national long-term care awareness campaign to be implemented over a five-year period and to enhance and continue the operation of the National Clearinghouse for Long-Term Care Information (Clearinghouse) as authorized by Section 6021 (d) of the Deficit Reduction Act of 2005, and extended by Section 8002 (d) of the Affordable Care Act. The Clearinghouse Procurement represents the Departments longstanding effort to increase consumer awareness of the need to plan ahead for long-term care. This procurement will facilitate consideration of a broader awareness effort while also enhancing the Departments existing awareness activities. Clearinghouse enhancements include a transition from direct mail to web-based outreach, and a refinement of the long-term care planning calls to action.

Section Six: Actuarial Model Development

By April 2010, it became clear that existing actuarial models that had been used before enactment of the CLASS Act (both those already relied on by HHS and those being developed by outside groups such as Boston College) would be insufficient to provide CLASS estimates and new models would have to be developed. Actuarial modeling of the CLASS program was undertaken by staff in ASPE, and reviewed by the CLASS Office. The model development and modeling were largely supported through a long-standing contract between Actuarial Research Corporation (ARC) and ASPE, and a new contract with AvalereHealth that began in September 2010. The rationale for developing two models was to compare premiums and other program dynamics using different methodological approaches and data and to assess the sensitivity of results to varying model assumptions. This is standard practice in the insurance industry when developing new products. Further, the ARC model does not include Medicaid offset estimates, while the Avalere model does. The key economic and demographic/actuarial assumptions are largely the same. This section briefly describes the two actuarial models, and model development and estimation across three phases: early model development and estimation; model refinement and development of preliminary benefit options; and final model development and estimation.

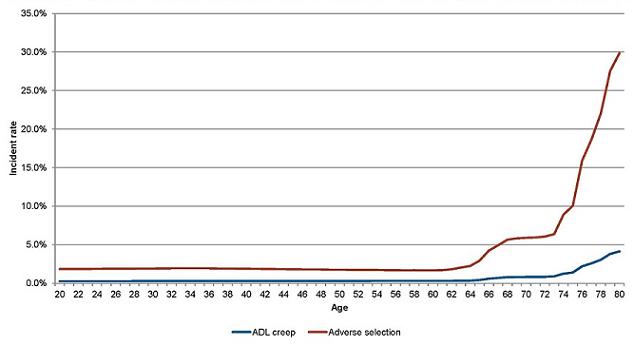

Both models adopted conservative assumptions that would tend to produce higher premiums and lower take-up rates than the best existing empirical evidence might suggest. For example, in modeling adverse selection it was assumed that potential enrollees would sort themselves perfectly by health status and join CLASS in reverse order (the most disabled first). The models used conservative assumptions because the existing empirical evidence is relatively sparse and there is great uncertainty around the existing estimates.

Summary of Actuarial Research CorporationS Long-Term Care Premium Model

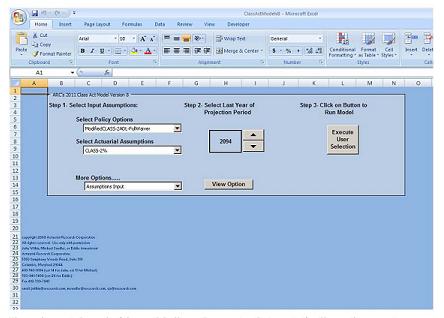

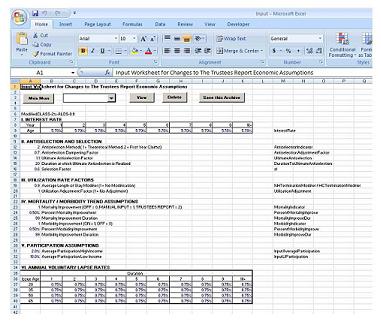

The ARC Long-Term Care Premium Model is designed to calculate long-term care insurance premiums for a government-operated, self-financing program and to project cash flow to assist policymakers in understanding program dynamics (see Appendix L for an in-depth description of the model). It can model various CLASS benefit structures under user-selected assumptions related to: program options, economic and demographic/actuarial assumptions (including antiselection/adverse selection), and long-term care utilization. The latter two sets of assumptions do not vary according to the program options, but are parameters used in the formulas to calculate premiums. Input and output are in Microsoft Excel Worksheets with program calculations performed in Visual Basic for Applications (VBA). The computer code underlying these calculations can be viewed by simply opening Excels Visual Basic Editor.

The key program options that can be modeled include alternative formulations of the following provisions of the CLASS program:

- vesting and work requirements

- earnings requirements

- benefit triggers

- daily benefit amount

- duration of benefits

- scheduled increase in premiums (i.e., indexing to a specific percentage increase or none);

- waiver of premium while on claim (full, partial, or none)

- participation rate

- administrative expense load on premiums.

Two approaches to adverse selection are built into the model: a theoretical approach and a first-year assumption regarding additional claims (a.k.a. the first-in method). The theoretical approach is based on a formula that assumes that adverse selection is greatest at the time of issue and declines the longer an individual is enrolled in the program. The second approach is based on observed data and an estimate of the number of people who are immediately eligible to enroll in the program and who also meet the ADL or cognitive requirement to qualify for benefits. This alternative method assumes that 100 percent of the population with limitations in ADLs or severe cognitive impairment would: (1) choose to enroll in the CLASS program the first year policies are offered, (2) survive the 5-year vesting period, (3) meet the work requirements during the vesting period, and (4) file a claim as soon as possible. After the first year in which benefits are paid, incidence rates for policyholders are assumed to be the same as general population incidence.

The model uses the 2011 OASDI Trustees Report, the Current Population Survey (CPS), the National Health Interview Survey (NHIS), the National Long-Term Care Survey (NLTCS), and the National Nursing Home Survey (NNHS). The model uses the 2011 OASDI Report and the CPS to set input parameters related to future inflation, mortality, interest rates, and labor force participation. The model uses the NHIS, NLTCS, and NNHS to estimate initial long-term care utilization by age and sex. Program options, economic and demographic/actuarial assumptions, and utilization can be saved and retrieved so that estimates can be replicated easily, and the impact of individual assumptions, or sets of assumptions, can be determined.

Summary of Avalere HealthS Revised Long-Term Care Policy Simulator

Avalere Healths Revised Long-Term Care Policy Simulator (LTC-PS) is an Excel-based model that tracks age-specific groups of CLASS program enrollees for 75 years (see Appendix M for an in-depth description of the model). The LTC-PS builds off a long-term care premium calculator originally developed under a grant from The SCAN Foundation. ASPE contracted with Avalere Health in the fall of 2010 to expand the capacity of the original model to incorporate key features of the CLASS program and a wider set of assumptions.

The basic approach to estimating premiums is similar to ARCs Long-Term Care Premium Model in that the present value of total expected costs of the program (including administrative costs) must equal the present value of total expected income (premiums plus interest on accumulated reserves). The estimated premium represents the average premium required in the initial year for each age of enrollment to accomplish an actuarially balanced model. The model estimates the impact on premiums of different benefit triggers and benefit amounts, program enrollment rates, low-income premium subsidies, and various benefit structures (including cash vs. service reimbursement).

The model incorporates adverse selection through an approach that is a hybrid of that used in the ARC model. Specifically, the LTC-PS estimates the number of people by age that will develop a severe disability over the next five years, and given a rate of assumed overall participation in the program, compares the number of people that would enroll in the program against the total estimated incidence of disability for the entire eligible population over the next five years. Under a pure adverse selection scenario, the model assumes that all people who would develop a severe disability will enroll in the program; this is similar to the ARC first-in method. However, because perfect adverse selection is unlikely to occur, the model builds in several factors that dampen the impact of adverse selection at initial enrollment and over time.

The LTC-PS uses many of the same sources of data as the ARC Long-Term Care Premium Model. For example, the model bases key economic and demographic assumptions on the 2011 OASDI Trustees Report, and uses data from the NNHS and NLTCS on the older population with disabilities, both living in the community and institutions. However, unlike the ARC model that relies on the CPS and NHIS for labor force participation and core disability data, the LTC-PS uses the American Community Survey and the Survey of Income and Program Participation.

Phase I. Early Model Development and Estimation (March 23, 2010 to September 22, 2010)

EARLY WORK ON THE ARC LONG-TERM CARE PREMIUM MODEL

ARC began preliminary modeling of CLASS in late 2009 to help HHS and other federal staff understand how premiums would vary based on different levels of participation and program options that were being considered by Congress at that time. Most of this work relied on an existing premium calculator that ARC had previously developed for a different purpose, and had quickly revised to model the major program features of the CLASS Act. Following passage of the ACA, ARC began to systematically review previous assumptions and premium calculations for accuracy. Major revisions to the model were undertaken through early summer 2010 to incorporate several aspects of the program that were not previously modeled in-depth, most notably the impact of the nominal premiums for low income persons and full-time students. In addition, staff at ARC began to update program parameters, the approach to adverse selection, demographic and actuarial assumptions, and input data. The ARC staff made these revisions with the goal of having independent technical experts review the methodology, assumptions, and data used in the model during the summer of 2010.

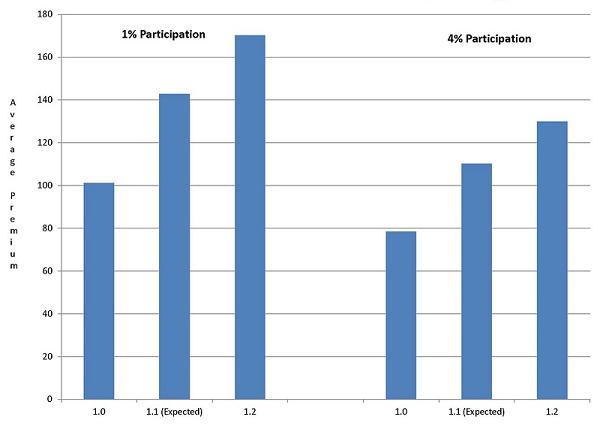

The first draft describing the model was produced in early April 2010 and preliminary premium estimates were completed in late August. At that point, the estimated baseline average premium at 2 percent program participation for a $50/day benefit based on a 2+ ADL trigger (or similar level of cognitive impairment) with full waiver of premium while in claim was $354/month. Changing the parameters of the program to increase the work and earning requirements during the vesting period, and indexing the premium reduced the premium to an average of $134/month. The impact on premiums of other changes to the program (e.g., increasing the vesting period to seven years; having enrollees continue to pay premiums if receiving home care; changing the duration of the benefit to seven years; and adding a 90 day elimination period) were also explored.

EARLY WORK ON THE AVALERE HEALTH MODEL

In early 2009, ASPE staff learned that Avalere Health was developing a long-term care premium calculator under a grant from The SCAN Foundation. Although the calculator was not intended to directly model the CLASS program, many of the components could be adapted to develop a more robust model that could more fully analyze aspects of CLASS. This was recognized by ASPE staff following the passage of the ACA as an opportunity to develop an alternative model to compare output from ARC, and to better understand how differences in methodology, assumptions, and input data affected premium estimates and CLASS program dynamics. After briefly considering revising the model in-house, ASPE decided to pursue a contract with Avalere Health directly. ASPE developed the Statement of Work and other contract documents over the summer of 2010; the contract was formally awarded to Avalere Health on September 17, 2010. The first contract activity was for staff at Avalere Health to attend a meeting five days later at HHS on actuarial modeling of the CLASS Act.

CLASS ACT MODELS MEETING

A half-day meeting of technical experts was held on September 22, 2010 to discuss progress on modeling the CLASS program (see Appendix N for the agenda, list of participants, and presentations). Participants included actuaries, economists, and analysts in health and long-term care in HHS, and members of several outside organizations, both public and private. The purpose of the meeting was threefold: (1) to describe the updated ARC Long-Term Care Premium Model and critically review the methods, assumptions and data underlying the model; (2) to describe and review Avalere Healths Long-Term Care Policy Simulator developed for The SCAN Foundation and plans for its revision to better model the CLASS program; and (3) to discuss outstanding technical issues and get feedback on such critical questions as:

-

Do the models incorporate realistic assumptions related to incidence/continuance of functional limitations and trends in disability? Are the assumptions related to the prevalence and trends in cognitive impairment reasonable?

-

Are there alternative approaches to modeling the relationship between CLASS participation and premiums?

-

Is potential adverse selection adequately incorporated into the models?

Because the models were still being developed, the preliminary premiums that ARC produced in late August were not presented; the discussion was focused exclusively on how the two models could be improved going forward. Several suggestions that were raised in the meeting led to substantive changes in the models. For example, ARC expanded its approach to adverse selection, adding a second approach that eventually became the first-in method. Staff at ARC also further revised and updated key assumptions and data on long-term care utilization. Suggestions for ways to improve the Avalere Health models estimation of age-specific participation were also eventually incorporated.

Phase II. Model Refinement and Development of Preliminary Benefit Options (September 23, 2010 to June 22, 2011)

Actuarial work over this period focused on further revisions and testing of the ARC model, and the completion of a revised LTC-PS that could more completely model the CLASS program. HHS sought to have both models in near final condition (with extensive documentation) so that preliminary benefit options could be developed and tested, and a Technical Expert Panel (TEP) could thoroughly vet both models in spring 2011.

During this time period, the CLASS Office hired its Chief Actuary, also known as the Director of Actuarial Integrity and Benefit Design. He began developing potential plan designs to mitigate the effects of adverse selection. He also worked to review and understand the ARC and Avalere models and provided his perspective on those. He focused on program provisions having a significant influence on the benefit design, including that: (1) participation in CLASS is voluntary; (2) actuarial soundness is a requirement; (3) any successful benefit design must present a clear value proposition to attract enrollees; (4) no underwriting other than age can be used to set premiums or prevent enrollment; and, (5) CLASS is not an entitlement program. The CLASS Office brought in an actuary from the U.S. Office of Personnel Management on a temporary detail. He and the Chief Actuary coauthored a report, Actuarial Report on the Development of CLASS Benefit Plans (see Appendix O), which discusses their analyses and findings, and describes benefit plans that have the potential of being actuarially sound.

PROGRESS ON THE ARC LONG-TERM CARE PREMIUM MODEL

Staff at ARC continued to revise the model and update the input data based on suggestions made by the CLASS Chief Actuary and the participants in the CLASS Act Models Meeting in September 2010. In early January 2011, another set of baseline premiums was estimated along with several benefit options with various work and earnings requirements during the vesting period (at this point almost all estimation assumed that premiums would be indexed, i.e., increase according to a fixed schedule such as CPI-U). The estimated baseline average (indexed) premium was now slightly lower: $339/month assuming 2 percent program participation for a $50/day lifetime benefit that used a 2+ ADL trigger (or similar level of cognitive impairment) with full waiver of premium while in claim. Increasing both the work requirement (to five years instead of three of five years) and earning requirement (to $12,000 per year instead of $1,120 per year) during the vesting period produced a slightly lower average premium compared to the $134 estimate from April 2010: $127/month. These premium estimates were forwarded to the Chief Actuary at the CLASS Office on February 17, 2011. Contemporaneously, staff in ASPE and the CLASS Office began to explore alternative benefit options that might lead to reduced premiums. Several of these were formally modeled (discussed further below and in the Actuarial Report on the Development of CLASS Benefit Plans which can be found in Appendix O) and eventually presented at the TEP meeting. Analyses of the implications of changes to key economic and demographic/actuarial assumptions continued in preparation for the TEP meeting as well as the development of final estimates to present to the TEP.

PROGRESS ON AVALERE HEALTHS LTC-PS

Because the original LTC-PS was not designed to model CLASS, work by staff at Avalere Health concentrated on developing a thorough CLASS baseline prior to the planned TEP meeting and building in as much flexibility to model alternatives as possible. The first preliminary estimates were produced in late January 2011. The average premiums were very similar to those being estimated by the ARC model, although the distribution of premiums by age was different. Actuarial work in late winter and the spring, as well as drafting documentation, focused on preparation for the TEP Meeting which was scheduled for June 2011.

TECHNICAL EXPERT PANEL MEETING ON ACTUARIAL MODELING OF THE CLASS PROGRAM

The full-day meeting of the TEP took place on June 22, 2011 (see Appendix P for the agenda and meeting materials). As with the previous meeting, participants included actuaries, economists, experts in disability data, and analysts in health and long-term care; none of the formal members of the TEP were federal employees, although participants included the CLASS Chief Actuary, actuaries from SSA and CMS, and other technical experts. Time during the morning was devoted to presentations on the two models and a review of methods, assumptions, and data. The agenda in the afternoon consisted of a review of the premiums produced by each model under different sets of assumptions and alternative benefit designs. The TEP reached consensus that the models methods and demographic/actuarial assumptions were credible and that the estimates were plausible. There was some debate as to whether the incidence rates in the ARC model were too high, and thus premium estimates also too high. The TEP also extensively discussed issues of adverse selection and suggested follow up work to improve the models handling of adverse selection; however, TEP members reiterated that there was no definitive way to determine the impact of participation and adverse selection a priori because CLASS is such a unique program, and CLASS modeling would thus be inherently uncertain. The discussion of alternative benefit designs was brief and there were no strong opinions voiced one way or the other about specific options.

Phase III. Final Model Development and Estimation (June 23, 2011 to Present)

Model development at this stage has focused on further improvements to the ARC Long-Term Care Premium Model to take into account situations of extremely low enrollment (e.g., under 1 percent), modeling of an alternative benefit design contained in the Actuarial Report on the Development of CLASS Benefit Plans (Appendix O and further described in the next section), and additional reviews of both models calculations and assumptions. Two independent actuaries are undertaking the latter effort as part of ASPEs ongoing contract with Avalere Health. The CLASS Actuary also explored an alternative approach based on information derived from Genworths net premium rates, with adjustments (see page 14 of the Actuarial Report on the Development of CLASS Benefit Plans, Appendix O).

FEDERAL ACTUARIES MEETING

The CLASS Actuary convened a meeting of government actuaries on June 28, 2011 to discuss actuarial modeling on CLASS and alternative plan options. Attendees included actuaries from the CMS Office of the Actuary and the Center for Consumer and Insurance Oversight, the Social Security Administration, and the Office of Personnel Management. Additional attendees included CLASS and ASPE staff members. The group discussed plans outlined in detail in the next section of this report. The consensus was that some benefit options under consideration could theoretically reduce adverse selection and have the potential to be actuarially sound. However, concerns were raised about: how to interpret the three percent administrative cost provision contained in the law; the policy and administrative complexities associated with some of the options; the unique marketing challenges of offering a federal benefit to large employer groups; and the very high level of uncertainty around assumptions in the actuarial models.

Section Seven: Plan Options

Since the passage of the ACA, numerous CLASS plan options have been considered (see the Actuarial Report on the Development of CLASS Benefit Plans, Appendix O, for the CLASS Chief Actuarys description of several of the benefit options). Those plan options whose parameters could be well-specified were modeled using the actuarial models described above, or by the Chief Actuary of the CLASS Office, under various assumptions about adverse selection, and different economic and demographic/actuarial parameters. Although a large number of plans have been modeled, the options can be grouped into roughly three categories: (1) those that are closest to the natural reading of the CLASS statute (benefit plan option one below); (2) benefit options that vary in limited, but important ways from the baseline (benefit plan option two below); and (3) benefit designs that vary much more from the baseline, either because of the sheer number of changes or because of modifications to key features of the program (benefit plan options three through eight).

The models described above estimate premiums for plans under a set of specific assumptions. The most critical of these assumptions are the assumptions around participation rates and adverse selection. Given these assumptions, the estimated premiums are, by definition, actuarially sound. However, the question of long-term solvency of the program depends on whether the assumptions around take-up and adverse selection, as well as other model assumptions, are plausible. As neither the CLASS program nor any other program like it has existed before, there is much greater uncertainty around these assumptions than is the case around the corresponding assumptions for either private long-term care insurance or existing programs, such as Social Security and Medicare. As a consequence, less confidence can be placed in actuarial judgments about the long run solvency of the CLASS program than about corresponding assessments of private insurance or existing government programs.

Existing data sources provide an uncertain picture of what the CLASS claims experience would be. Survey data, such as those used in the ARC and Avalere models, provide information on the entire population but do not provide information on the future claims experience of the CLASS program. Private insurers claims data provide information for those who qualify for private insurance (either underwritten or large group) but do not provide information for the CLASS benefit, which is very different from the typical private market product and targets a more diverse population.

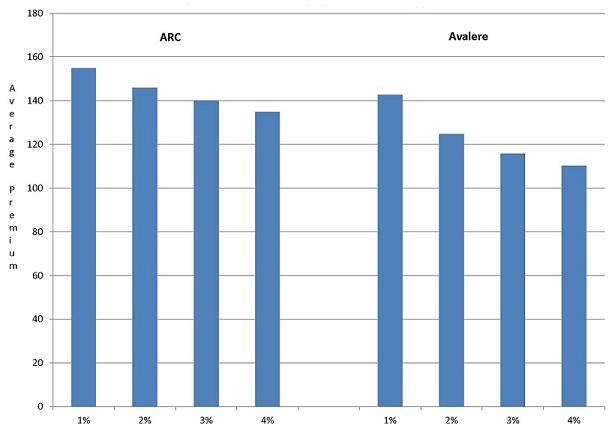

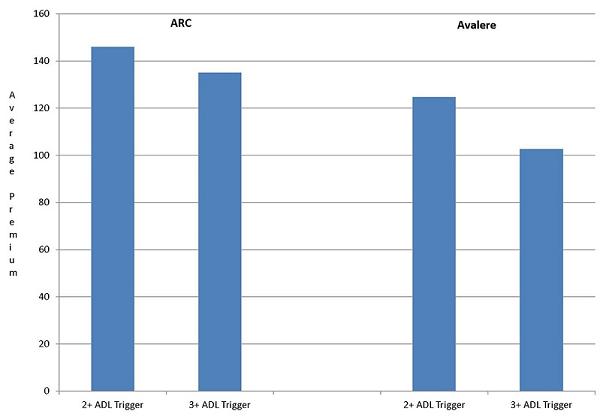

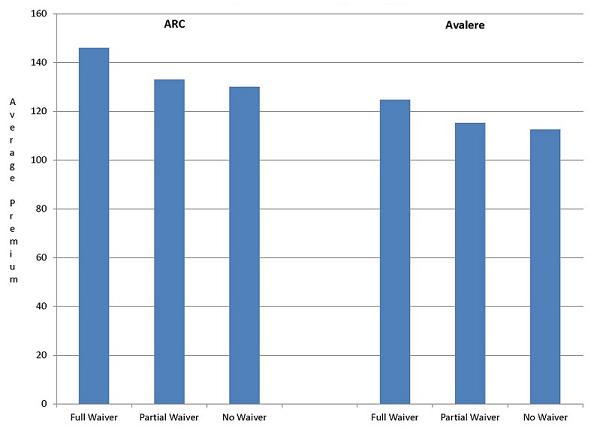

Table 1 presents a summary of the actuarial model estimates for four representative plan options (Options 1-4) that were either modeled for the TEP meeting in June 2011 and the federal actuaries meeting convened by the CLASS Chief Actuary or estimated over the last few months. Because of the uncertainty around parameter assumptions, a range of average premiums is presented rather than a point estimate. Below, we describe each of these benefit plans, provide estimates of premiums, discuss actuarial soundness, and summarize points made in the discussion of these plan options.

| Program Features | 1. | 2. | 3. | 4a. | 4b. | ||

|---|---|---|---|---|---|---|---|

| Enhanced CLASS Plan | Family of Options: Variation 1 | Family of Options: Variation 1 | Family of Options: Variation 2 | Family of Options: Variation 2 | |||

| Basic CLASS | Modified CLASS | w/Phased Enrollment1 | Modified CLASS | Increasing Benefits (CLASS Partnership) | Enhanced CLASS Plan w/Phased En.1 | Increasing Benefits (CLASS Partnership) | |

| Enrollment Requirements: | |||||||

| Age 18+ | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Taxable Wages/Income | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Actively Employed | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Not in Institution | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Coverage/Benefits: | |||||||

| Primary Benefit | Cash | Cash | Cash | Cash | Cash | Cash | Cash |

| Daily Benefit Amount (DBA) | $50 (Average) | $50 (Average) | $57.5 (Average)2 | $50 (Average) | Varies - Up to $1503 | $57.5 (Average)2 | Varies - Up to $1503 |

| Unit of Payment | Daily or Weekly | Daily or Weekly | Daily or Weekly | Daily or Weekly | Daily or Weekly | Daily or Weekly | Daily or Weekly |

| Minimum Duration in Years | NA - Lifetime | NA - Lifetime | NA - Lifetime | NA - Lifetime | 3 Years | NA - Lifetime | 3 Years |

| Total Value | TBD | TBD | TBD | TBD | $164,250 | TBD | $164,250 |

| Inflation Protection | CPI-U (2.8%) | CPI (2.8%) | CPI (2.8%) | CPI (2.8%) | CPI (2.8%) | CPI (2.8%) | CPI (2.8%) |

| Advocacy Services | Yes | Yes | TBD | Yes | TBD | TBD | TBD |

| Advice and Asst. Counseling | Yes | Yes | TBD | Yes | TBD | TBD | TBD |

| Eligibility for Benefits: | |||||||

| 5 Year Vesting Period | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Work Req. Over Vesting Period | At Least 3 Years | 5 Years | 5 Years | 5 Years | 5 Years | 5 Years | 5 Years |

| Earnings Req. Over Vesting Period | $1,120/ Year | $12,000/ Year | $12,000/ Year | $12,000/ Year | $12,000/ Year | $12,000/ Year | $12,000/ Year |

| 24 Months of Prior Prem. Payment | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Minimum Benefit Trigger | 2 or 3 of 6 ADLs4 | TBD | TBD | TBD | TBD | TBD | TBD |

| Tiered Benefit | Yes | Yes | Yes | Yes | TBD | Yes | TBD |

| Elimination Period in Days | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Presumptive Eligibility | Yes - if in Inst.5 | Yes - if in Inst.5 | Yes - if in Inst.5 | Yes - if in Inst.5 | Yes - if in Inst.5 | Yes - if in Inst.5 | Yes - if in Inst.5 |

| Administrative Expenses | 3% | 3% | 3% | 3% | 3% | 3% | 3% |

| Monthly Premium: | |||||||

| Underwritten (Other Than Age) | No | No | No | No | No | No | No |

| Increasing Premium (Indexed) | No | Yes (2.8%) | Yes (2.8%) | Yes (2.8%) | Yes (2.8%) | Yes (2.8%) | Yes (2.8%) |

| Low Income Premium | Yes | No | No | No | No | No | No |

| Full Time Student Premium | Yes | No | No | No | No | No | No |

| Waiver of Premium | TBD | TBD | TBD | TBD | TBD | TBD | TBD |

| Level Premium | After Age 656 | After Age 656 | After Age 656 | After Age 656 | After Age 656 | After Age 656 | After Age 656 |

| 1 Initial enrollment limited to group (employer) settings first; individual enrollment will begin after meeting target goals in the group market | |||||||

| 2 Initial $50/day cash benefit for persons with 2-3 ADLs; $60/day cash benefit for persons with 4+ ADLs or cognitive impairment; cash benefit is reduced by 80% after five claim years | |||||||

| 3 The inflation-adjusted DBA increases over a 25-year period to the final amount: years 0-10=0%; years 11-15=5%; years 16-20=10%; years 21-25=29.5% | |||||||

| 4 Or equivalent level of cognitive impairment | |||||||

| 5 An active enrollee is presumed to be eligible for benefits if they are a patient in a long-term care hospital, nursing facility, intermediate care facility for the mentally retarded, or an institution for mental disease and are in the process of being discharged, or are within 60 days from the date of discharge | |||||||

| 6 Enrollees age 65 and older who have paid premiums for enrollment for 20 years and are not actively employed are exempt from premium increases | |||||||

-

BASIC CLASS PLAN

This plan option is based on the most natural reading of the statute and incorporates the key features of the plan described in law (e.g., eligible enrollees must be at least 18 years old and actively employed; there is no underwriting required for enrollment; the primary benefit is a lifetime $50/day [on average] cash payment; before being eligible to receive a benefit, enrollees must wait five years and meet certain work and earnings requirements; etc.). Estimates for this option were produced by ARC and Avalere Health, and are described in Column 1 of Table 1 (baseline). Though the plans cash benefit would increase by the annual percentage change in the consumer price index for all urban consumers (CPI-U), the plan modeled by the actuaries assumes that the cash benefit would increase annually by a fixed percentage, 2.8 percent, which is equal to the long-range inflation forecast published in the 2011 OASDI Trustees Report. The actuaries did this because actuarial models cannot easily estimate future costs when benefits increase by an unknown and variable amount. It is important to emphasize that the 2.8 percent inflation adjuster is for actuarial modeling purposes only; for this option it is contemplated that CPI-U would be used for ongoing program operations.

Under the set of assumptions designated as Scenario II (Expected) (see Appendix Q for Table 2) discussed at the June 2011 TEP meeting, the average premium for a $50/day lifetime benefit with a 2+ ADL trigger (or similar level of cognitive impairment) with full waiver of premium while in claim range from $235/month to $391/month. These estimates are based on a take-up assumption of 2 percent.

In the current private long-term care insurance market, most buyers choose products that provide a substantial daily benefit (e.g., $150/day to $200/day) for three to five years of coverage--daily benefit amounts that are significantly higher than the $50/day lifetime benefit. This could be an issue for marketing CLASS to a broad population as participants in focus groups specifically mentioned that they preferred a benefit that covered more of the total cost of long-term care. Moreover, premiums for products similar to the CLASS benefit, when they are sold to an underwritten population in the private market, would cost much less than the estimated premiums above. Thus, most discussion of this Basic CLASS Plan suggested that the assumed take-up rates used to compute premiums could not be achieved and were not plausible.

-

MODIFIED CLASS PLAN OPTION

The benefit plan shown in Column 2 modifies three key aspects (highlighted in yellow [ROWS are "Eligibility for Benefits"/"Work Req. Over Vesting Period" and "Earnings Req. Over Vesting Period", COLS are 2 through 4b]) of the baseline CLASS benefit: first, the work requirement during the vesting period is increased from at least three of five years to five of five years; second, the earnings requirement during the vesting period is increased from $1,120 per year to $12,000 per year (the amount of earnings that SSA uses to determine whether a nonblind person is engaged in substantial gainful activity); and finally, the monthly premium is increased annually by a fixed percentage (modeled at 2.8 percent in this example). The latter feature is sometimes referred to as an increasing premium schedule or indexed premium.

Increasing the work and earnings requirement over the vesting period significantly mitigates adverse selection, thus reducing the average premium. In addition, moving to an indexed premium instead of a constant (level) premium lowers the initial premium required to balance expected costs and expected income.

Under the set of assumptions designated as Scenario II (Expected) discussed at the June 2011 TEP meeting, the average premium for a $50/day lifetime benefit with a 2+ ADL trigger (or similar level of cognitive impairment) with full waiver of premium while in claim declines significantly; premium estimates range from $114/month to $160/month. These estimates assume a take-up rate of 2 percent.

The reduction in premiums achieved under this option make the take-up assumption more plausible for the Modified CLASS Plan than for the Basic CLASS Plan. However, the ultimate take-up level is still unknown. The daily benefit amount remains lower than what is prevalent in the private market, which likely increases the risk of low participation rates, especially by those who are able to purchase private policies. In addition, as the federal actuaries noted, the statutory 3 percent limit on administrative costs could make it very challenging to market the product and achieve the expected level of participation. Thus, while the assumed take-up rate used to compute premiums under this model is plausible, there is a high degree of uncertainty about the long-run solvency of this option.

-

ENHANCED CLASS PLAN WITH PHASED ENROLLMENT

Column 3 of Table 1 shows the key features of a benefit option described in detail in the Actuarial Report on the Development of CLASS Benefit Plans. In various documents it is referred to as the Enhanced CLASS Plan with Phased Enrollment or simply Phased Enrollment. This benefit plan builds off the Modified CLASS Plan, but differs in two important respects (highlighted in blue [ROW "Coverage/Benefits"/"Daily Benefit Amount", COLUMNS "Phased Enrollment"]). First, it uses an explicit two-tiered benefit structure for the first five years that a person is on claim:

- an initial $50/day cash benefit for persons with 2-3 limitations in ADLs

- an initial $60/day cash benefit for persons with 4+ limitations in ADLs or cognitive impairment.

After the fifth year, the daily benefit amount declines by 80 percent. Beneficiaries would therefore receive $10/day and $12/day for the above two tiers, respectively. For modeling purposes, it is assumed that the amount of the cash benefit is equivalent to a lifetime $57.50 daily benefit.

The second difference between the Modified Class Plan and the Enhanced CLASS Plan is that initial enrollment in the program would be limited to certain group settings first, such as large employers; individual enrollment would begin after group enrollment meets a pre-set threshold, explained in more detail by the CLASS Chief Actuary on page 10, Actuarial Report on the Development of CLASS Benefit Plans, Appendix O).

Early modeling of the Enhanced CLASS Plan with Phased Enrollment using the ARC Long-Term Care Premium Model produced an average indexed premium that ranges from $99/month to $106/month for a $57.50/day lifetime benefit with full waiver of premium. A preliminary comparison of age-specific premiums is also shown on p. 14 of the Actuarial Report on the Development of CLASS Benefit Plans.

As observed by the CLASS Chief Actuary, this plan achieves a greater reduction in premiums than does the Modified CLASS Benefit. The range of estimated premiums is also more similar to what is observed in the private LTC insurance market, although the daily benefit is lower in CLASS. Successfully marketing the program remains a serious challenge due to the changing benefit amounts for beneficiaries. The phased enrollment approach could substantially reduce the degree of uncertainty around the rates of enrollment by healthier individuals. By opening the program to individual subscribers only when take-up has reached a threshold level, this approach could manage the risk of adverse selection and potential insolvency.

-

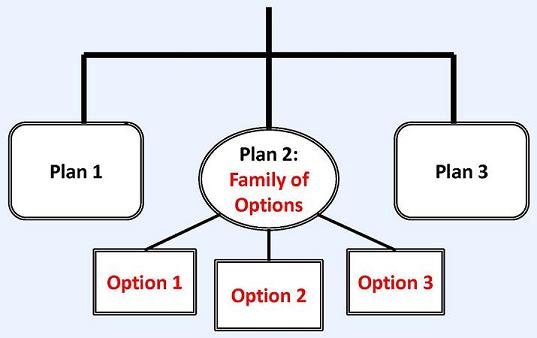

FAMILY OF OPTIONS: MODIFIED CLASS PLAN & SCHEDULED INCREASING BENEFITS

Columns 4a and 4b of Table 1 describe a set of benefit plans referred to as the Family of Options. One of the options would be consistent with the CLASS statute (e.g., the Modified CLASS Plan in the case of Variation 1). The structure of the other options would vary more extensively, but would continue to incorporate similar requirements for enrollment; a primary benefit that is cash; a five year vesting period; and no underwriting except for age. The Family of Options would be structured to offer either one or two tiers of eligibility for benefits. The Family of Options would be actuarially sound, either at the individual option level or, through cross-subsidization in their entirety. Finally, one of the options within the family would be designed so that purchasers could buy a private (underwritten) insurance product to wrap around this option and provide a higher level of benefit.

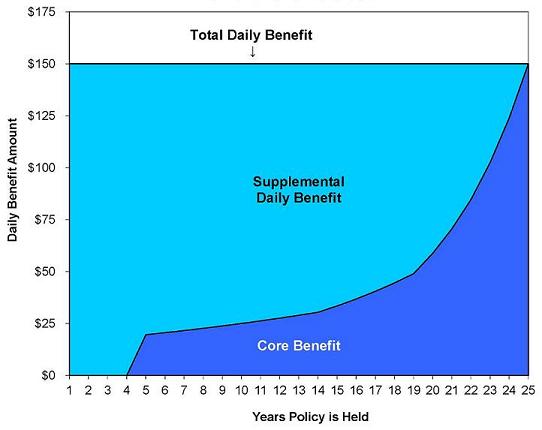

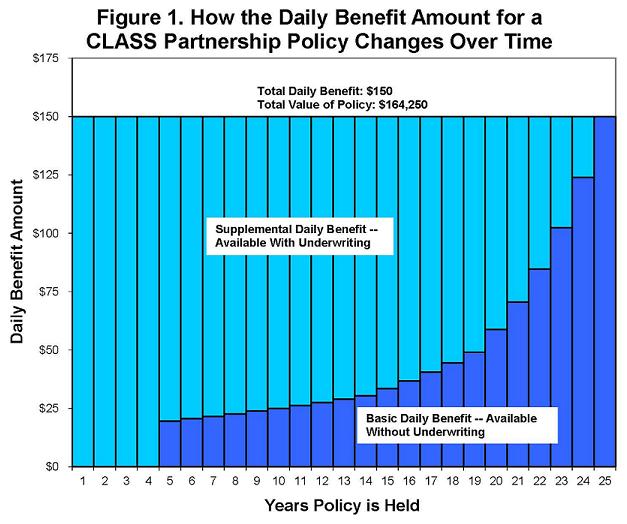

Column 4a shows one variation of the Family of Options that includes the Modified CLASS Plan and the Scheduled Increasing Benefits Plan discussed above. (Column 4b shows the corresponding Family of Options with the Enhanced Class Plan with Phased Enrollment paired with the increasing benefit option.) Several features of this plan (highlighted in orange [ROWS "Coverage/Benefits"/"Daily Benefit Amount" and "Minimum Duration in Years", COLUMNS "Family of Options: Variation 1: Increasing Benefits" and "Family of Options: Variation 2: Increasing Benefits"]) differ from aspects of the plans presented in Column 1 and Column 2. Specifically, the daily benefit amount increases the longer the CLASS policy is held without going into claim, rising from approximately $20/day after the vesting period to $150/day after 25 years. Also, the duration of coverage is limited to three years, although the expected payout for this benefit option could be designed in such a way as to be actuarially equivalent to that of the Modified CLASS Plan.

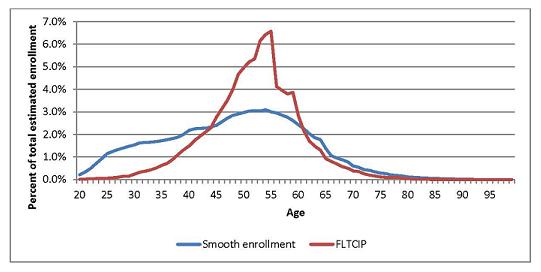

Figure 1 illustrates how the basic daily benefit amount (dark blue area) increases over a 25-year period to $150/day (see Appendix R for Figure 1). This plan is sometimes referred to as the CLASS Partnership because the structure of the benefit provides an opportunity for private insurers to develop products that would naturally wrap around and supplement the underlying basic benefit (light blue area in Figure 1).

If there is no subsidization across benefits options, then the individual plans that make up any set of Family of Options can be priced independently (although specific assumptions related to participation and adverse selection could be adjusted to take into account expected interactions). The range of estimates for an average premium at 2 percent participation assuming a 2+ ADL trigger (or similar level of cognitive impairment) with full waiver of premium is $112 per month to $148 per month. These estimates do not include the cost of a supplemental policy. The total cost of an initial combined policy, for example, for a 50 year old enrollee who could pass underwriting, is currently estimated to be $154 per month ($118 per month for the basic policy and $36 per month for the supplement).

This model achieves a somewhat greater reduction in premiums than does the Modified CLASS Plan. Because of the choice of benefit structure, this option offers benefits more similar to those available in the private market. With private supplementation, purchasers could achieve coverage comparable to that in the private market at similar prices. The design significantly mitigates adverse selection, and premiums do not vary much even under alternative assumptions about take-up rates.3 There were varying opinions about the marketability of the Family of Options design. Some believed that offering choice would be attractive; others thought that it would be burdensome and confusing, especially since the low administrative load for marketing permitted under CLASS would limit the ability to explain the plan. The great uncertainty about the marketability of this option means that uncertainty about the long run solvency of this option is very high.

-

TEMPORARY EXCLUSION PLAN

This benefit option addresses adverse selection through the claims process rather than the enrollment process. Specifically, any person who meets the enrollment requirements could join CLASS, but no benefits would be paid for the first fifteen years in the program if a limitation in ADLs or cognitive impairment during this period resulted from a serious medical condition that existed at the time of enrollment. The CLASS program would provide enrollees with a list of possibly exclusionary medical conditions, but no health information would be collected at enrollment. Only when a person sought benefits would a review of medical records occur to ensure that the limitation was not the result of an underlying condition at enrollment. Existing data available to the modeling team did not provide sufficient longitudinal information about underlying conditions and subsequent disability to model this option.

This plan would likely reduce premiums substantially because potential buyers with existing health conditions would recognize that they would not be able to claim for pre-existing conditions for fifteen years. There was concern that uncertainty about future benefit receipt would make it challenging to market this option (as purchasers could not be certain that a subsequent disability would not be tied to an underlying condition). Those who could meet an underwriting standard would likely prefer to buy a policy where there was no subsequent uncertainty. See Appendix O (Actuarial Report on the Development of CLASS Benefit Plan) for additional information on this plan option.

-

TEMPORARY EXCLUSION PLAN WITH PHASED ENROLLMENT

This benefit option combines the features of Temporary Exclusion with phased enrollment as described above. Because the Temporary Exclusion Plan was not modeled, this option was not modeled either. Clearly, the combination of temporary exclusion and phased enrollment would provide substantial protection for the program against actuarial risk. It might, however, be challenging to market this package. See Appendix O (Actuarial Report on the Development of CLASS Benefit Plan) for additional information on this plan option.

-

LIMITED INITIAL BENEFIT PLAN WITH PHASED ENROLLMENT

This benefit option is analogous to the Enhanced CLASS Plan with Phased Enrollment but has a different benefit structure. While the Enhanced CLASS Plan has a two-tiered benefit that is reduced after five years on claim, this benefit option starts with a low daily benefit amount (e.g., $5 per day or $10 per day) for a fixed period of time (e.g., 20 years) before increasing to its ultimate $50 per day value.

This plan was not formally modeled. While the approach would certainly mitigate adverse selection to a great extent, the initial low benefit and extended period before the benefit increases are unlikely to be very attractive, especially to healthy older workers. See Appendix O (Actuarial Report on the Development of CLASS Benefit Plan) for additional information on this plan option.

-

PRE-PAID BENEFIT PLAN

Under extreme levels of adverse selection when 100 percent of the enrolled population is eligible for benefits, the monthly premium is essentially the amount that is required for enrollees to pre-pay their future benefit. Because the cost of a pre-paid plan is too high to make it marketable, it is not a viable benefit design. However, the exercise of determining the cost of a pre-paid plan can be instructive, since it provides us with the high end of the range of costs for a plan. The Chief Actuary of the CLASS Office estimated that a pre-paid plan would cost approximately $3,000 per month in premiums. Because enrollees are essentially pre-paying their future long-term care costs, this plan does not include a nominal premium for low income persons and full-time students. See Appendix O (Actuarial Report on the Development of CLASS Benefit Plan) for additional information on this plan option.

In addition to evaluating the formal benefit options discussed above, HHS staff also considered several features, either individually or together, to determine their impact on premiums and program dynamics. The goal was to add specific aspects that would mitigate adverse selection, lower premiums, and increase the marketability of the CLASS program. These features included adding incentive payments for delaying claim, combining CLASS with disability insurance, using variable inflation protection for the benefit instead of a fixed percentage, and possibly returning all or a portion of an enrollees accumulated premiums if he or she died at an early age before going on to claim. Most of the features were eventually discarded because they either did not significantly lower premiums or were deemed to be too complicated to implement.

Part II: Legal Analysis