LifePlans, Inc.

This policy brief was prepared under contract between the U.S. Department of Health and Human Services (HHS), Office of Disability, Aging and Long-Term Care Policy (DALTCP) and LifePlans, Inc. For additional information about the study, you may visit the DALTCP home page at http://aspe.hhs.gov/_/office_specific/daltcp.cfm or contact the ASPE Project Officer, Hunter McKay, at HHS/ASPE/DALTCP, Room 424E, H.H. Humphrey Building, 200 Independence Avenue, SW, Washington, DC 20201. His e-mail address is: Hunter.McKay@hhs.gov.

| This literature review was commissioned, along with six data briefs, by the Department of Health and Human Services, Office of the Assistant Secretary for Planning and Evaluation to analyze survey data collected by Long Term Care Partners from members of the federal family regarding the long-term care insurance offering available to them. This paper summarizes findings from a comprehensive review of the literature and published data about buyers and non-buyers of private long-term care insurance, including members of the federal family. The remaining briefs address: a Profile of Buyers; a Profile of Non-Buyers; a Profile of Non-Responders; a Comparison of Active and Retired Buyers, Non-Buyers and Non-Responders; a Comparison of Engagement and Participation among Buyers, Non-Buyers and Non-Responders; and a Multivariate Analysis of Buyers and Non-Buyers. |

I. BACKGROUND

One of the more ambitious proposals for encouraging growth in the private insurance market was the passage of the Long Term Care Security Act (Public Law 106-265). This act was passed in the summer of 2000 and was signed into law on September 19th of that year. It authorized the U.S. Office of Personnel Management (OPM) to contract for a long-term care (LTC) insurance program for federal employees. Medically underwritten coverage was made available to active federal employees and annuitants (civilian retirees), as well as active and retired members of the uniformed services. It was also made available to 'other qualified relatives,' who would include current spouses of employees and annuitants, including surviving spouses of members and retired members of the uniformed services who are receiving a survivor annuity, adult children of living employees and annuitants, and parents, parents-in-law, and stepparents of living active employees. Because this coverage is medically underwritten, certain medical conditions prevented some people from being approved for coverage. OPM expected that, like the health and life insurance programs it administers, the Federal Long-Term Care Insurance Program (FLTCIP) would become the largest employer-sponsored LTC insurance program in the nation.

Naturally it was expected that implementation of the program would spur additional interest and growth in the market. The program began in earnest in July of 2002, which constituted the beginning of the open enrollment period. The carriers underwriting the program -- John Hancock and MetLife -- formed a joint venture called Long Term Care Partners, LLC, which is devoted exclusively to administering the program.

Long Term Care Partners conducted one of the largest LTC educational campaigns ever. More than one million people requested enrollment kits. As of August 2003, 273,000 applications had been received. About 64% of enrollees were active employees and spouses, 31% annuitants and their spouses, and another 5% surviving spouses, parents/in-laws and adult children. Thus, in relatively short order, the FLTCIP became the largest group programs in the United States. In part this was due to the significant marketing and enrollment activities including more than 2,100 educational meetings, briefings to human resources staff and outreach programs to affinity groups.

The large number of enrollments affords a unique opportunity to better understand the attitudes and perspectives of both working and retired individuals regarding LTC concerns, the importance of planning, and the role that insurance may (or may not) play in meeting the needs of disabled individuals. An examination of such attitudes can assist policymakers as well as insurers to better understand marketplace opportunities and barriers, and devise strategies to encourage growth in the market.

II. PURPOSE

The purpose of this project is to analyze survey data collected by Long Term Care Partners from members of the federal family regarding the LTC insurance offering available to them. The analysis focuses on the attitudes, opinions and motivations of both active employees and retirees who have enrolled in the program ("buyers"), those who have expressed an interest in the program but chosen not to enroll ("non-buyers"), and those who are members of the federal family but have not enrolled or expressed any interest in doing so ("non-responders"). As part of this project, we also compare the results to available data from other studies of non-federal buyers and non-buyers in both the individual and group markets. In this way we are able to determine the extent to which there are significant differences, which could influence both the marketing and future design of LTC insurance. Finally, we examine specific issues within each of the three sample groups.

The purpose of this brief is to present summary findings from a comprehensive review of the literature and published data about buyers and non-buyers of private LTC insurance, including members of the federal family. Understanding the motives behind peoples' choices can help to inform public policy as well as focus current and future market strategies. We summarize the findings of a variety of studies on the subject conducted between 1987 and 2003.

III. METHOD

In reviewing the literature, we classify studies into one of two categories: (1) empirical and (2) descriptive studies. Empirical studies focus on isolating the independent impact or effect of a particular characteristic (demographic, health, attitudinal, financial, etc.) on the probability of buying LTC insurance while holding all other characteristics constant. Descriptive studies, on the other hand, examine how buyers and non-buyers differ with regard to a particular characteristic but these studies do not control for other characteristics that may explain the purchase/non-purchase decision. For example, while it may be the case that being married is associated with being a buyer, it may also be the case that most married buyers tend to be young. Therefore, in understanding the purchase decision, it is difficult to know whether age or marital status is the primary trait related to the purchase decision -- something that one could not "tease out" in a descriptive study. Only when controlling for age can we identify the independent impact of marital status on the purchase decision and vice versa. This is what the empirical literature examines. Both types of research are important and taken together provide a comprehensive view of what is known about buyers and non-buyers.

In the sections that follow, we describe existing studies and focus on the findings that are consistent across studies. We examine the factors that are important to the decision of buyers to buy LTC insurance and those that are important to the decision of non-buyers not to buy. We also summarize the features that may make non-buyers more likely to become purchasers. The Appendix provides a summary table of the major findings of the studies reviewed herein.

IV. FINDINGS

A. Study Descriptions

Each of the studies reviewed here focus on one of two sample groups from distinct markets: (1) the individual market and, (2) the group market -- typically employer or group association. While the individual market comprises the bulk of LTC insurance sales -- roughly 85% -- the group market has shown the greatest rates of growth over the past five years. Of the 15 studies included in this review, six focus on the group market and the other nine examine purchase trends in the individual market.

The Health Insurance Association of America (HIAA) conducted descriptive studies of LTC insurance buyers and non-buyers in the employer group market in 1990 and 2001. The sample was drawn from eleven employers. These studies provide descriptive analyses on more than 3,800 employed buyers and non-buyers of group LTC insurance. Stum et al. (2001) analyzed the purchase decision of 830 employees of the State of Minnesota and the University of Minnesota who in the fall of 2000 were offered group LTC insurance. The study provides both descriptive and empirical analyses. In 2000, the American Council of Life Insurers (ACLI) conducted a study of roughly 500 individuals across a number of different employers that focused on the link between retirement planning and the purchase of insurance (ACLI, 2001). In 1999, the Long Term Care Group (LTCG) studied the buying behavior of 500 buyers and 500 non-buyers of the CalPERS program with respect to LTC insurance in response to their 1998 campaign. Finally, a recent study of purchase behavior among federal employees represents the largest group surveyed with more than 10,000 individuals participating in the study (DHHS, 2003a).

The remaining nine studies focus on the buying behavior of retirees. Six of these studies provide descriptive analyses and three provide empirical analyses. The descriptive studies are the 1986/87 AARP study, the 1990, 1995 and 2000 HIAA studies, the ACLI study and the Ritchey et al (1991) study. The 1986/87 AARP study looks at the purchase decision of 3,900 AARP members ages 55 to 79, who in 1985 and in 1986 were offered LTC insurance covering care at home or in a nursing home. The HIAA individual studies and the ACLI study draw their samples of more than 15,000 buyers and non-buyers age 55 and over, from between eight to ten of the largest LTC insurance companies selling policies. Ritchey et al. (1991) surveyed roughly 600 randomly selected retired teachers in Ohio who became eligible in July 1990 to purchase LTC insurance through the State Teachers Retirement System of Ohio. The three empirical studies that examine the purchase decision of retirees include: Lee (1999), McCall et al. (1998) and Kumar et al. (1995). Lee (1999) uses data from the Asset and Health Dynamics Among the Oldest Old survey comprised of 7,200 individuals age 70 and over. McCall et al. (1998) focus on identifying the factors that are important determinants of the purchase of Partnership policies. The Partnership program was an initiative of the Robert Wood Johnson Foundation and four states -- California, Connecticut, New York and Indiana -- that combined private and public (Medicaid) insurance for the financing of LTC. The program was designed to promote the sale of LTC insurance to middle-income customers. The 1,050 non-purchasers in the sample were between the ages of 55 and 75 and the 1,467 purchasers were selected at random. Finally, Kumar et al. (1995) base their empirical analysis on the 1995 HIAA study of retirees age 55 and over. All of the studies use logistic regressions to identify the factors that have an impact on the probability of buying LTC insurance.

B. Demographic Characteristics related to the Purchase Decision

The demographic characteristics that are common to both the descriptive and the empirical analyses include: age, gender, marital status, health status, level of education, income, liquid assets, and the presence of children and their distance from the respondent. Table 1 summarizes the results of the descriptive studies showing whether a particular demographic characteristic distinguishes between buyers and non-buyers among retirees (individual market) and employees (group market). (Note that the Appendix summarizes results on all variables for each individual study.)

| TABLE 1: Demographic Characteristics that Distinguish between Buyers and Non-Buyers | ||

|---|---|---|

| Characteristics | Employees | Retirees |

| Average age: buyers are younger | No | Yes |

| Gender: buyers are more likely to be female | Contradictory evidence | Not significant |

| Marital status: buyers less likely to be married | Not significant | Not significant |

| Education: buyers more likely to have a college degree | Yes | Yes |

| Income: buyers have higher income | Yes | Yes |

| Assets: buyers more likely to have more assets | Yes | Yes |

| Health: buyers more likely to cite health as excellent | No | Yes |

| Children: buyers less likely to have children nearby | N.A. | Yes |

Among retirees, advancing age is associated with non-purchase. In contrast, among the employee-group market, advancing age is associated with purchase. There are two factors that explain what might seem to be contradictory trends. First, as employees age, they are more likely to think about and plan for retirement. Having a LTC insurance policy is often considered to be part of a prudent retirement plan. Also, many of these individuals may have lower family expenses as children graduate from college and mortgages are reduced. Therefore, "older" employees may be more aware of LTC challenges and may also have greater financial wherewithal to do something about it. With respect to retirees, older age is associated with rapidly increasing premiums. Given the fact that many retirees are on fixed incomes, the ability to pay for the product becomes more limited at older ages. For this reason, younger retirees are more likely to purchase policies than older retirees.

With respect to gender, there is contradictory evidence across the studies regarding whether it distinguishes between employees and there is agreement that it is not an important differentiator in the retiree market. In general, levels of education, income and assets are highly correlated. In the employer market, a higher level of these variables is associated with being a buyer. Given the expense of the product it is not surprising that as wealth increases, so too does the probability of being a buyer. This holds across both market segments. In contrast, higher education status is not a significant differentiator in the retiree market.

In the retiree market, those who report their health to be excellent are more likely to buy a policy than those who do not. This is likely related to their younger age and it may also reflect economic status. In the employee-group market, this factor is not important. In part, this is because there is very little variation in self-reported health status. Finally, retired buyers are also less likely than retired non-buyers to have children living nearby. Given that a primary purpose for having the insurance is to enable individuals who become disabled to remain in their homes, it is not surprising that those who do not have family supports, are more likely to find the insurance attractive.

Empirical study results related to demographic characteristics are displayed in Table 3. Being female, being single, having higher income and assets and having children who live far away increase the probability of buying insurance. Being younger, having a college degree and perceiving your own health status to be excellent result in an increasing probability of buying insurance in some of the studies -- primarily those focused on the retiree market -- and in a decreasing probability to buy insurance in other studies -- those focused on the employer-group market.

C. LTC Attitudes and Experience

One would expect that people's attitudes toward and experience with LTC would influence their thinking about the potential value of having a private policy. Table 2 displays whether certain attitudinal or experiential variables distinguish between buyers and non-buyers of the product.

| TABLE 2: Attitudes and Experiences that Distinguish between Buyers and Non-Buyers | ||

|---|---|---|

| Attitudes | Employees | Retirees |

| Buyers are more likely to perceive their risk of needing LTC to be high | Yes | Yes |

| Buyers more likely to have prior experience with LTC, primarily as caregivers | Yes | Yes |

| Buyers indicate less willingness to rely on family if they need care | Yes | Yes |

| Buyers more likely to say it is important to plan ahead for the possibility of needing care | Yes | Yes |

| Buyers worry more about how to pay for LTC expenses if they need care | Contradicting evidence | Contradicting evidence |

| Buyers are more likely to view themselves at personal financial risk if they should need LTC | Yes | Yes |

| Buyers less likely to believe that the government will pay for care if they need it | Yes | Yes |

| Buyers less likely to believe that major public payers -- Medicare or Medicaid will pay for care if it is needed | Not significant | Yes |

Buyers, both employed and retired, are much more likely to see themselves at risk of needing LTC either in a nursing home or in their homes. Given that insurance is designed to substitute an unknown potentially catastrophic risk for a certain ongoing payment, it is not surprising that those who perceive themselves to be at higher risk are also more likely to purchase a policy. Buyers are also more likely than non-buyers to have had prior experience with LTC -- primarily as caregivers. That direct personal experience has shown them that LTC can be needed, that it is expensive, and that it is not fully covered by medical insurance, Medicare or Medicaid. They have also learned that LTC needs can be best met when they are planned for.

Buyers in both markets also indicate that they are less willing to rely on their children to provide long term care or to help them with the expenditures associated with it. They also point out that it is important to plan ahead for the needs that may arise in the future. There is no significant difference in the degree to which buyers and non-buyers worry about paying for LTC. The 1990 HIAA individual and group studies and the 1986/87 AARP studies find that buyers worry more than non-buyers about how to pay for LTC, while the two subsequent HIAA individual studies of 1995 and 2000 and the HIAA group study of 2001 find that buyers worry less than non-buyers about that. The change in results over time may suggest an increasing confidence among buyers in the product they have purchased and an increasing awareness of non-buyers about the risk of needing LTC and the need to plan ahead for its financing. Among federal employees and retirees, this variable does not distinguish buyers from non-buyers.

Buyers -- primarily in the individual market -- also show a greater understanding of the fact that government programs are not likely to pay for most LTC costs and that in the absence of insurance, the primary responsibility for paying for LTC will rest with the family. While many buyers in the employee market do not fully understand public coverages, they are more likely to know something about how LTC will be paid than are non-buyers.

Table 3 summarizes the results of empirical studies. Holding all other variables constant, if one believes that there is a high risk for needing care, and that if care is needed, the government will not pay for most of it, one is more likely to purchase a policy. In addition, two of the empirical studies report that having a personal experience with LTC increases the probability of being a buyer. One however, shows the opposite to be true. It should be noted, however, that most of the LTC policies selling at the time of the survey used in the latter study did not include significant home health care coverage and were viewed primarily as policies for nursing home coverage. Because caregiving experience typically occurs in a community setting, it is not surprising the that such experience did not influence the probability of buying insurance mainly viewed to provide nursing home coverage.

| TABLE 3: Summary of Empirical Results | |

|---|---|

| Characteristics | Significance |

| Being younger | Contradicting evidence |

| Being female | Increases the probability of buying |

| Being single | Increases the probability of buying |

| Having a college degree | Contradicting evidence |

| Having higher income | Increases the probability of buying |

| Having more assets | Increases the probability of buying |

| Citing health as excellent | Contradicting evidence |

| Having children who live far away | Increases the probability of buying |

| Having experience with LTC | Contradicting evidence |

| Considering own risk of needing LTC as high | Increases the probability of buying |

| Thinking that self/family, not the government will pay | Increases the probability of buying |

| Thinking that Medicare/Medicaid will pay | Decreases the probability of buying |

D. The Decision Making Process

There are significant differences between buyers and non-buyers with respect to how they learned about LTC and the process by which they decided to buy or not to buy coverage. Retired buyers are more likely to have heard about LTC insurance from a trusted source. For example, in the Ritchey et al. (1991) study, the State Teacher's Retirement System (STRS) offered LTC insurance to retired teachers in Ohio, and the buyers were more likely than non-buyers to identify STRS as a source of information. Both working and retired buyers are also more likely to have had a financial advisor or planner; to have attended meetings at work and to cite them as a source of information; to read on their own (enrollment kit and booklet); to utilize websites; and to recall elements of the educational campaign (DHHS, 2003; HIAA, 2001; Stum et al., 2001; Lee, 1999; Ritchey et al., 1991; LTCG, 1999; AARP, 1986/1987). Buyers are also more likely than non-buyers to discuss the enrollment or purchase decision with others such as spouses/partners and co-workers/friends (Stum et al., 2001; Ritchey et al., 1991; LTCG, 1999), but they are less likely than non-buyers to cite television as a source of information (Ritchey et al., 1991). Finally, with respect to comparison shopping, buyers are more likely to comparison-shop than non-buyers.

Much of the empirical work in this area supports the descriptive findings. For example, Stum et al. (2001) find that discussing the decision to purchase insurance with others (e.g., spouses or partners and co-workers or friends), attending a seminar or a meeting at work, and using other information sources increase the probability of buying LTC insurance. McCall et al. (1998) found that talking with a specialist or financial planner increases the probability of purchasing insurance. The Lee (1999) study does not find this to be the case. This lack of consensus may likely reflect differences in the samples of populations studied.

E. The Impact of a Maturing Market

In general, the demographic and attitudinal characteristics of buyers and non-buyers discussed heretofore have not changed markedly between 1986 and 2003. The most notable difference occurs in the income and asset level of buyers, which increased dramatically throughout the nineties. This likely reflects the booming state of the economy and the high returns to stock market investments. The percentage of buyers who are college graduates and the average age of working buyers also increased through that time. There is also a noticeable decrease in the percentage of buyers who worry about how to pay for LTC. This trend may reflect the growing confidence of buyers in the insurance industry.

F. Buying Behavior

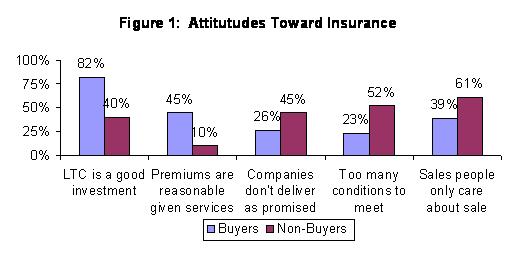

Figure 1 summarizes specific attitudes of buyers and non-buyers towards LTC insurance as reported by Ritchey et al. (1991). Clearly, buyers have different attitudes about insurance than non-buyers: they are more likely to believe that the insurance is a good investment and that premiums are reasonable given the services provided. In contrast, non-buyers are more likely to believe they would do better saving on their own.

|

| Source: |

Buyers also have confidence that the insurance will pay benefits as promised whereas non-buyers are more likely to distrust insurance companies. These differences also persist in relation to attitudes toward insurance agents. Buyers are less likely to think that agents are only interested in the sale. Slightly less than two-in three non-buyers believe that agents are only interested in making a sale. These strong attitudinal differences go a long way in explaining how it is that individuals with relatively similar socio-demographic characteristics sort themselves into buyers and non-buyers.

As Table 4 shows how the motivations for purchasing LTC insurance have, or have not, changed over time. These historical trends are based on the three HIAA studies conducted over the last decade. The reasons mentioned most often and which have stayed relatively consistent over the last decade, are to protect savings, to assure adequate income for a spouse, to assure the affordability of services, and to avoid being a burden on family. Reasons which are important, but less so than those cited above, relate to the freedom to choose services, to avoid depending on government programs, and to leave an estate.

| TABLE 4: Reasons to Buy LTC Insurance | |||

|---|---|---|---|

| Very Important Reasons to Buy | 2000 | 1995 | 1990 |

| Protect assets | 71% | 67% | 72% |

| Not be burden to family | 69% | 69% | 75% |

| Can afford needed health care services | 68% | 66% | 70% |

| Adequate income will remain for the spouse if costly services are needed | 62% | 59% | 74% |

| Freedom of choice with respect to services | 58% | 59% | 74% |

| Government will not cover the care that may be needed | 54% | 54% | 54% |

| Will not have to depend on any of the programs for the needy | 45% | 50% | 52% |

| Leave an estate to family/friends | 43% | 43% | 38% |

| The benefits payable are not considered taxable | 20% | N.A. | N.A. |

G. Non-Buying Behavior

Almost all studies reviewed cite policy cost as the main reason why people do not buy coverage for LTC needs. Table 5, which tracks buyers over the last decade, summarizes the important reasons given for not purchasing a policy (HIAA, 1990, 1995, 2000).

| TABLE 5: Reasons Not to Buy LTC Coverage | |||

|---|---|---|---|

| Very important reason not to buy | 2000 | 1995 | 1990 |

| Costs too much | 54% | 57% | 58% |

| Waiting for better policies | 28% | 32% | 41% |

| Too many conditions to be met before receiving benefits | 25% | 30% | N.A. |

| Confusion about which policy is the right one | 18% | 28% | 54% |

| The spouse could not get a coverage | 17% | 11% | 20% |

| Don't believe insurers will pay as promised | 15% | 21% | 36% |

| Do not mind using own income to pay for LTC | 11% | 15% | 22% |

| Do not think will ever need services | 10% | 9% | 15% |

| Believe Medicaid will pay | 9% | 12% | 20% |

| Can rely on family to help with LTC | 6% | 8% | 9% |

Waiting for a better policy and having to meet too many conditions are also primary obstacles for buying insurance. However as a non-purchase reason, the latter has diminished over time. This suggests that either potential buyers today are spending more time researching the market and are therefore happier with their choice, or that insurance companies are offering better policies than they once did, or that both of these conditions are true. Confusion about which policy is the right one and believing that Medicaid will pay for LTC have also diminished in importance over time. It seems that the individuals examining the insurance have become more educated about the different policies on the market and are more aware about who pays for LTC (in the absence of private insurance).

The percentage of people who say they do not believe the insurer will pay as promised has also decreased over the last decade, this indicating that there is an increase in consumer confidence in the product. This may be a function of enhanced consumer protection standards and more uniform coverage brought about by passage of the Health Insurance Portability and Accountability Act.

H. Converting Non-Buyers to Buyers

It is evident from recent federal and state activity that the public sectors support growth in the private LTC insurance market. While the LTC insurance market grew dramatically in the last decade, fewer than 10% of all elderly Americans and an even smaller percent of working age Americans have coverage. Finding out what would make the product more attractive to consumers or what would make consumers more attracted to the product is, therefore, very important. Given that most non-buyers cite cost as an important barrier to purchase, it is not surprising that when asked, most non-buyers (across all studies) say that they would be much more interested in buying a policy if it was cheaper. As well, most non-buyers indicate that they would be more likely to purchase a policy if the government also participated in a "partnership-type" arrangement (e.g., pay benefits after private insurance runs out), or if they perceived that they were at higher risk for needing protection.

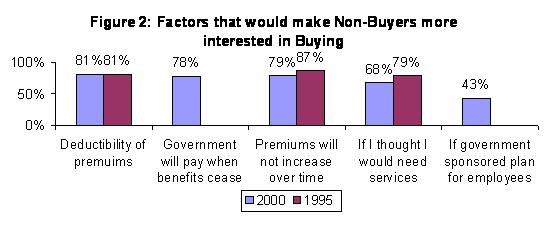

To gauge whether there have been changes over time in the attitudes of non-buyers, we present findings from the 1995 and 2000 HIAA surveys of non-buyers. The results displayed in Figure 2 indicate that non-buyers would be much more interested or more interested in buying insurance if (a) the premiums could be deducted from taxes; (b) if the government were to provide a stop-loss coverage once their private insurance benefits run out, and (c) if premiums do not increase over time. These results are consistent with findings among non-buyers in the federal market (DHHS, 2003b). In the year 2000, non-buyers also indicated that they would be much more likely to buy if the government sponsored an insurance plan and offered it to its employees. Given that this is precisely what has taken place, one can expect some positive impact on the buying behavior of individuals not associated with the federal family.

|

| Source: |

V. CONCLUSIONS

The literature reviewed here suggests that there are some key differences between buyers and non-buyers in terms of their demographic and attitudinal characteristics and that attitudes emerge as much more important factors associated with buying behavior than do demographic characteristics. With respect to demographic characteristics, buyers in general, have higher income and assets. In terms of their attitudes, however, buyers are more likely to see the risk of needing LTC, to have had prior experience with LTC, to be less willing to rely on their children for help with LTC, to put higher emphasis on planning and to be more likely to think that they themselves, rather than the government should pay for care. In addition, when making the purchase decision, buyers are more likely to comparison shop and to talk with family, friends or colleagues. Buyers are also more likely than non-buyers to have a financial planner and to actively seek information about LTC.

An important finding from the studies reviewed is that people decide to buy and not to buy insurance for various reasons. The reasons to buy insurance range from wanting to protect assets to ensuring the affordability of services and the choice of service modality, to avoiding burdening the family. The reasons for not buying insurance range from high costs to confusion about which is the right policy, to believing that Medicare will pay and not believing that the insurer will pay as promised. Even though some of these reasons have changed over time to reflect the increased awareness and understanding among non-buyers of LTC insurance, there is still work to be done on educating the consumer and enhancing his or her confidence in the insurer and the product.

REFERENCES

American Council of Life Insurers (2001). Long Term Care Insurance at Work. The Retirement Link and Employer Perspectives. Research Findings. Washington, D.C. July.

American Council of Life Insurers (2001). Making the Retirement Connection. The Growing Importance of Long Term Care Insurance in Retirement Planning. Research Findings. Washington, D.C. March.

AARP/Prudential Operations (1986). "Results of AARP/Prudential Long Term Care Insurance Test Mailing Study Among Buyers and Non-buyers." Washington, D.C.

AARP/Prudential Operations (1987). "Long Term Care Study (Wave II)."

American Council of Life Insurers (2001). Long Term Care Insurance at Work. The Retirement Link and Employer Perspectives. Research Findings. Washington, D.C. July.

American Council of Life Insurers (2001). Making the Retirement Connection. The Growing Importance of Long Term Care Insurance in Retirement Planning. Research Findings. Washington, D.C. March.

Cohen A.M., and J.S. Miller (2000). "Long Term Care Insurance and Retirement Planning: The Road to Retirement Security." LifePlans, Inc. Waltham, MA.

Department of Health and Human Services (2004a). Data Brief #1: A Demographic and Attitudinal Profile of Buyers of the Federal Long-Term Care Insurance Program. Washington, D.C. August. (http://aspe.hhs.gov/daltcp/reports/buyprof.htm)

Department of Health and Human Services (2004b). Data Brief #2: A Demographic and Attitudinal Profile of Non-Buyers of the Federal Long-Term Care Insurance Program. Washington, D.C. August. (http://aspe.hhs.gov/daltcp/reports/nonbuyprof.htm)

Health Insurance Association of America (2000). "Who Buys Long Term Care Insurance in 2000? A Decade of Study of Buyers and Nonbuyers." Washington, D.C.

Health Insurance Association of America (1990). "Who Buys Long Term Care Insurance?" Research Findings. Washington, D.C.

Health Insurance Association of America (1995). "Who Buys Long Term Care Insurance? 1994-95 Profiles and Innovations in a Dynamic Market." Washington, D.C.

Kumar N., M.A. Cohen, C.E. Bishop and S.S. Wallack (1995). "Understanding the Factors Behind the Decision to Purchase Varying Coverage Amounts of Long-Term Care Insurance." Health Services Research 29(6), 653-678.

Lee D. (1999). "Who Purchases Long Term Care Insurance: Factors in the Purchase of Private Long Term Care Insurance." Empirical Research Paper, University of Massachusetts, Boston, Boston, MA.

Long Term Care Group (1999). "CalPERS Long Term Care Program: Buyer vs. Non-Buyer Survey." Research Findings. May.

McCall N., S. Mangle, E. Bauer and J. Knickman (1998), "Factors Important in the Purchase of Partnership Long term Care Insurance." Health Services Research 33(2), 187-204

Ritchey L.H., R.C. Atchley and M.M. Seltzer (1991). "To Buy or Not To Buy: Considerations in the Decision to Purchase Long Term Care Insurance." Scripps Gerontology Center, Oxford, Ohio.

Stum M.S., V.S. Zuiker, E. Pelletier and L. Hope (2001). "To Buy or Not To Buy: Examining Long Term Care Insurance Decision-Making From the Employee Perspective." Department of Family Social Science, University of Minnesota.

APPENDIX

| TABLE A-1: Summary of Research Findings: Differences Between Buyers and Non-Buyers -- Demographics | ||||||||

|---|---|---|---|---|---|---|---|---|

| AARP | HIAA 1990 Individual | HIAA 1990 Group | HIAA 1995 | HIAA 2000 | HIAA 2001 Group | Ritchey Atchley | LTCG/ CalPERS | |

| DESCRIPTION OF STUDY | ||||||||

| Year | 1986/87 | 1990 | 1990 | 1995 | 2000 | 2001 | 1991 | 1999 |

| Author | The Data Group Incorporated | LifePlans Inc. | LifePlans Inc. | LifePlans Inc. | LifePlans Inc. | LifePlans Inc. | Ritchey L., R. Atchley, M. Seltzer | LTCG |

| Population surveyed | Buyers & non-buyers of LTC insurance | Buyers & non-buyers of LTC insurance | Buyers & non-buyers of group LTC insurance | Buyers & non-buyers of LTC insurance | Buyers & non-buyers of LTC insurance | Buyers & non-buyers of group LTC insurance | Retired buyers & non-buyers of LTC insurance | Retired & active buyers & non-buyers of LTC insurance |

| Sample size | 502 buyers, 978 non-buyers (1986); 1098 buyers, 1319 non-buyers (1987); ages 50-79 | 8009 buyers, 1680 non-buyers; age 55 and older | 1607 buyers, 874 non-buyers; age 64 and younger | 2601 buyers, 1245 non-buyers; age 55 and older | 2728 buyers, 638 non-buyers; age 55 and older | 1018 buyers, 315 non-buyers | 118 buyers, 498 non-buyers; median age 60 | 500 buyers & 500 non-buyers |

| Information collection technique | Mail survey-buyers, telephone survey-non-buyers | Mail survey | Mail survey | Mail survey | Mail survey | Mail survey | Mail survey | Telephone survey |

| Analytical method | Descriptive | Descriptive | Descriptive | Descriptive | Descriptive | Descriptive | Descriptive | Descriptive |

| DEMOGRAPHICS | ||||||||

| Average age: buyers are younger | Yes | Yes | No | Yes | Yes | No | n.s.* | Yes |

| Gender: buyers are higher % female | Yes | Yes | No | Yes | n.s. | n.s. | n.s. | n.s. |

| Marital status: buyers less likely to be married | Yes | n.s. | n.s. | No | n.s. | n.s. | Yes | n.s. |

| Education: buyers have higher education | Yes | n.s. | Yes | n.s. | Yes | Yes | n.s. | n.s. |

| Income: buyers have higher income | Yes | Yes | Yes | Yes | Yes | Yes | n.s. | Yes |

| Assets: buyers have more assets | n.s | Yes | Yes | Yes | Yes | Yes | ||

| Savings: buyers more likely to have IRAs, MR or Annuities | Yes | |||||||

| Children: buyers less likely to have kids nearby | Yes | n.s. | ||||||

| Health: buyers more likely to cite as excellent | Yes | Yes | ||||||

| * n.s. not statistically significant | ||||||||

| TABLE A-1 (continued) | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Kumar Cohen | McCall Mangle | Lee | ACLI Group | ACLI | Stum Zuiker | Federal Program Active | Federal Program Retired | |||

| DESCRIPTION OF STUDY | ||||||||||

| Year | 1995 | 1998 | 1999 | 2000 | 2000 | 2001 | 2003 | 2003 | ||

| Author | Kumar N, M. Cohen, C. Bishop and S. Wallack | McCall N., S. Mangle, E. Bauer and J. Knickman | Lee | LifePlans Inc. | LifePlans Inc. | Stum M., V. Zuiker, E. Pelletier and L. Hope | LifePlans Inc. | LifePlans Inc. | ||

| Population surveyed | buyers & non-buyers of LTC insurance | buyers of the RWJ Found. Partnership Policy & randomly selected non-buyers | participants in the AHEAD survey | buyers & non-buyers of LTC insurance | buyers & non-buyers of LTC group insurance | buyers & non-buyers of LTC group insurance | active buyers & non-buyers of the FLTCIP | retired buyers & non-buyers of the FLTCIP | ||

| Sample size | 6545 buyers, 1248 non-buyers; age 55 and older | 1467 buyers, 1050 non-buyers; ages 55-75 purchasers, non-purchasers selected randomly | 187 buyers, 7022 non-buyers; age 70 and older | 1614 buyers, 803 non-buyers | 126 buyers, 378 non-buyers | 149 buyers, 681 non-buyers; mean age 48 | 642 buyers, 575 non-buyers | 1114 buyers, 586 non-buyers | ||

| Information collection technique | Mail survey | Telephone survey | Data from the AHEAD survey | Mail survey | Mail survey | Mail survey | Mail survey | Mail survey | ||

| Analytical method | Empirical | Empirical | Descriptive & empirical | Descriptive | Descriptive | Descriptive & empirical | Descriptive | Descriptive | ||

| DEMOGRAPHICS | ||||||||||

| Desc. | Emp. | Desc. | Emp. | |||||||

| Average age: buyers are younger | Yes | No | Yes | Yes | n.s. | No | No | n.s. | Yes | |

| Gender: buyers are higher % female | Yes | Yes | n.s. | n.s. | Yes | n.s. | n.s. | Yes | n.s. | |

| Marital status: buyers less likely to be married | No | n.s. | n.s. | No | n.s. | n.s. | Yes | n.s. | ||

| Education: buyers have higher education | No | Yes | Yes | Yes | n.s. | n.s. | Yes | Yes | Yes | |

| Income: buyers have higher income | Yes | Yes | Yes | Yes | n.s. | n.s. | Yes | Yes | Yes | |

| Assets: buyers have more assets | n.s. | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | |

| Savings: buyers more likely to have IRAs, MR or Annuities | ||||||||||

| Children: buyers less likely to have kids nearby | Yes | Yes | Yes | Yes | Yes | n.s. | ||||

| Health: buyers more likely to cite as excellent | Yes | Yes | Yes | No | No | n.s. | Yes | |||

| TABLE A-2: Summary of Research Findings: Differences Between Buyers and Non-Buyers -- LTC Attitudes and Experiences | ||||||||

|---|---|---|---|---|---|---|---|---|

| AARP | HIAA 1990 Individual | HIAA 1990 Group | HIAA 1995 | HIAA 2000 | HIAA 2001 Group | Ritchey Atchley | LTCG/ CalPERS | |

| DESCRIPTION OF STUDY | ||||||||

| Analytical method | Descriptive | Descriptive | Descriptive | Descriptive | Descriptive | Descriptive | Descriptive | Descriptive |

| LTC ATTITUDES & EXPERIENCES | ||||||||

| Buyers less willing to rely on kids | Yes | Yes | Yes | Yes | ||||

| Buyers more likely to have LTC experience | Yes | n.s. | Yes | |||||

| Buyers worry more about how pay for LTC | Yes | Yes | Yes | No | No | No | ||

| Buyers less likely to say government will pay | Yes | Yes | Yes | Yes | n.s. | n.s. | Yes | |

| Buyers more likely to say it is important to plan | Yes | Yes | Yes | Yes | Yes | Yes | Yes | |

| Buyers more likely to see risk of needing LTC | Yes | Yes | Yes | Yes | Yes | Yes | Yes | |

| Buyers more aware that self/ family will pay | Yes | Yes | Yes | Yes | Yes | Yes | n.s. | Yes |

| Buyers less likely to say Medicare/ Medicaid will pay | Yes | Yes | Yes | Yes | n.s. | n.s. | ||

| Buyers less likely to say "don't know" re: how pay | Yes | Yes | Yes | Yes | Yes | |||

| TABLE A-2 (continued) | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Kumar Cohen | McCall Mangle | Lee | ACLI Group | ACLI | Stum Zuiker | Federal Program Active | Federal Program Retired | |||

| DESCRIPTION OF STUDY | ||||||||||

| Analytical method | Empirical | Empirical | Descriptive & empirical | Descriptive | Descriptive | Descriptive & empirical | Descriptive | Descriptive | ||

| LTC ATTITUDES & EXPERIENCES | ||||||||||

| Desc. | Emp. | Desc. | Emp. | |||||||

| Buyers less willing to rely on kids | Yes | |||||||||

| Buyers more likely to have LTC experience | No | Yes | n.s. | n.s. | Yes | Yes | Yes | n.s. | n.s. | |

| Buyers worry more about how pay for LTC | n.s. | n.s. | ||||||||

| Buyers less likely to say government will pay | Yes*** | Yes | Yes | |||||||

| Buyers more likely to say it is important to plan | ||||||||||

| Buyers more likely to see risk of needing LTC | Yes** | Yes | Yes | Yes | Yes | Yes | n.s. | |||

| Buyers more aware that self/ family will pay | Yes*** | n.s. | n.s. | Yes | No | Yes | Yes | |||

| Buyers less likely to say Medicare/ Medicaid will pay | Yes | Yes | n.s. | Yes | ||||||

| Buyers less likely to say "don't know" re: how pay | Yes | n.s. | n.s. | n.s. | ||||||

| ** Buyers perceive they have a higher risk of nursing home use, but lower risk of receiving care at home *** Buyers were more likely to say that they and not the government should pay for LTC |

||||||||||

| TABLE A-3: Summary of Research Findings: Differences Between Buyers and Non-Buyers -- Decision Making Process | ||||||||

|---|---|---|---|---|---|---|---|---|

| AARP | HIAA 1990 Individual | HIAA 1990 Group | HIAA 1995 | HIAA 2000 | HIAA 2001 Group | Ritchey Atchley | LTCG/ CalPERS | |

| DESCRIPTION OF STUDY | ||||||||

| Analytical method | Descriptive | Descriptive | Descriptive | Descriptive | Descriptive | Descriptive | Descriptive | Descriptive |

| DECISION-MAKING PROCESS | ||||||||

| Buyers more likely to discuss with others (spouse, colleagues, children, etc.) | Yes | Yes | ||||||

| Buyers more likely to have attended seminars/ meetings/ use information sources | Yes | |||||||

| Buyers more likely to have talked with specialist | Yes | |||||||

| Buyers more likely to have heard about LTC from trusted sponsor | Yes | |||||||

| Buyers less likely to have heard about it on TV | Yes | |||||||

| Buyers more likely to have comparison shopped | Yes | Yes | ||||||

| TABLE A-3 (continued) | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Kumar Cohen | McCall Mangle | Lee | ACLI Group | ACLI | Stum Zuiker | Federal Program Active | Federal Program Retired | |||

| DESCRIPTION OF STUDY | ||||||||||

| Analytical method | Empirical | Empirical | Descriptive & empirical | Descriptive | Descriptive | Descriptive & empirical | Descriptive | Descriptive | ||

| DEMOGRAPHICS | ||||||||||

| Desc. | Emp. | Desc. | Emp. | |||||||

| Buyers more likely to discuss with others (spouse, colleagues, children, etc.) | Yes | Yes | ||||||||

| Buyers more likely to have attended seminars/ meetings/ use information sources | Yes | Yes | Yes | Yes | Yes | |||||

| Buyers more likely to have talked with specialist | Yes | Yes | n.s. | |||||||

| Buyers more likely to have heard about LTC from trusted sponsor | ||||||||||

| Buyers less likely to have heard about it on TV | ||||||||||

| Buyers more likely to have comparison shopped | ||||||||||