Briefing for ASPE Long-Term Care Financing Colloquium

Melissa Favreault

Washington, DC

"Acknowledgments

- This is joint work with many colleagues

- Urban team: Owen Haaga, Paul Johnson, Richard Johnson, Karen Smith, Brenda Spillman, Douglas Murray

- Milliman: Al Schmitz, Chris Giese, Jill Bruckert; ARC

- Medical expenses: Harvard Medical School, Health Care Policy: Michael Chernew, Laura Hatfield, Tom McGuire

- Thanks to ASPE/HHS for comments and support

- Judith Dey, Pamela Doty, John Drabeck, William Marton, and Samuel Shipley

- Thanks to other funders: AARP, Leading Age, National Institute on Aging, the SCAN Foundation, University of Hawaii

- Thanks to review panels/reviewers:

- Chris Giese, Harriet Komisar, Al Schmitz, Brenda Spillman, Anne Tumlinson, and Josh Wiener

Summary

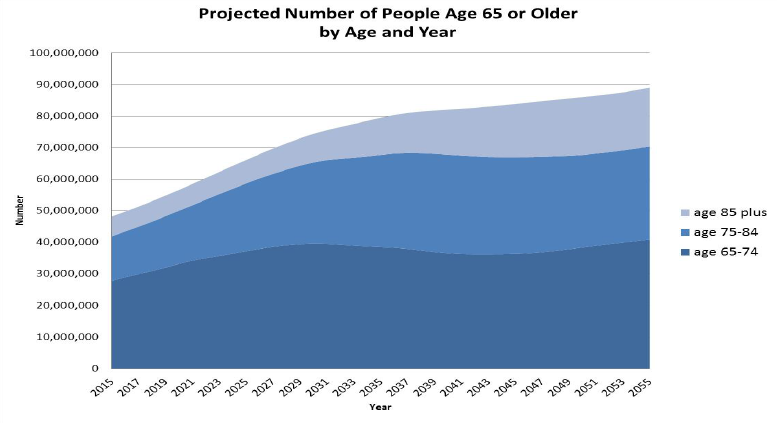

- Population aging--particularly rapid growth in those ages 85 and older--will lead to increased demand for LTSS

- Especially steep increases anticipated starting about 10 years from now; 2024-2044 should be a period of growing strain.

- Risk of needing LTSS is common: about half of people who survive to age 65 will eventually need HIPAA-level LTSS

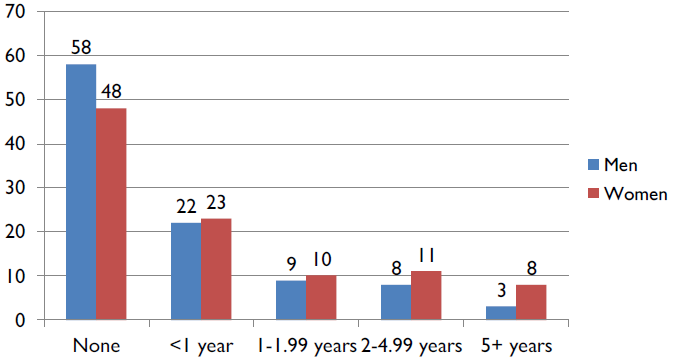

- On average, need lasts about two years, and formal use lasts about one year--more than double for users; informal supports are extremely important.

- About 14% need help >= 5 years; 6% use formal services >= 5 years

- Some population subgroups face higher than average risk

- Women, unmarried people; complex risks by socioeconomic status

- Government and families are the main LTSS payers

-

Medicaid (state and federal) and out of pocket

-

An Aging Population Will Raise the Demand for LTSS

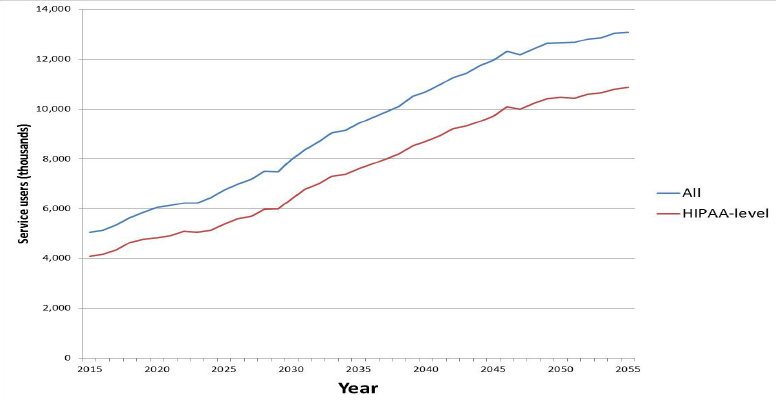

We project that formal LTSS use and costs will roughly track the growth in the aged population

Lifetime Risk Estimates

Key Definitions

- Most results today are for adults turning age 65 between 2015 and 2019

- We project formal care, which includes the following:

- nursing home care

- paid home care

- residential care

- We focus on HIPAA level of need -- formal focus

- need help with two or more ADLs, or

- severe cognitive impairment

- We project present discounted value of costs at age 65, in 2015 constant dollars

- finances required to cover all expected future costs, given assumed interest rate

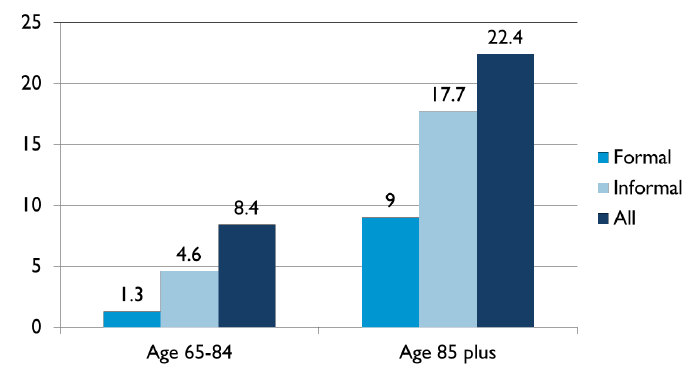

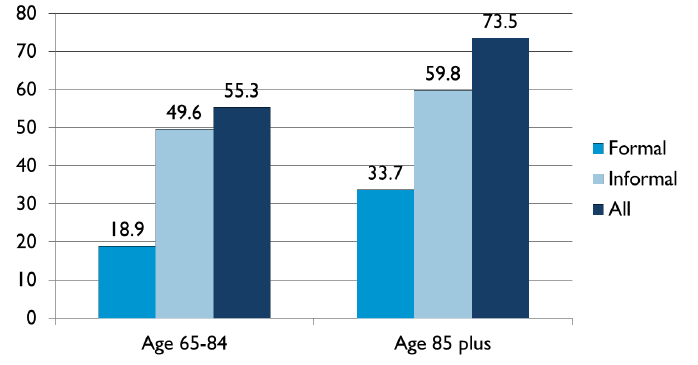

Context: Much home care is informal and provided to individuals not meeting HIPAA criteria, especially at older ages…

At HIPAA disability level, care is more prevalent… and typically more intensive

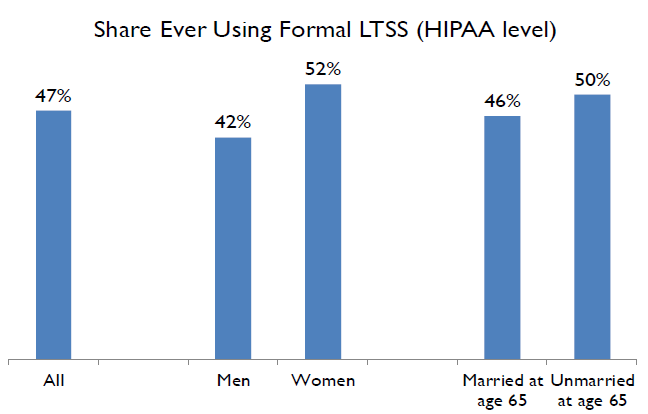

About half of adults surviving to age 65 can expect to use formal HIPAA LTSS before they die

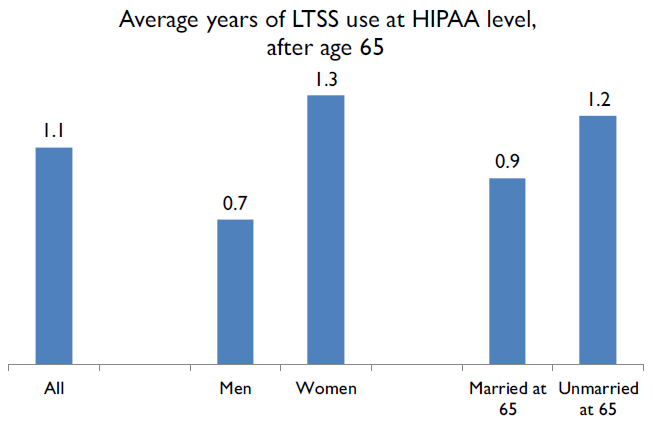

On average, formal LTSS lasts about one year

The average masks a lot of variation

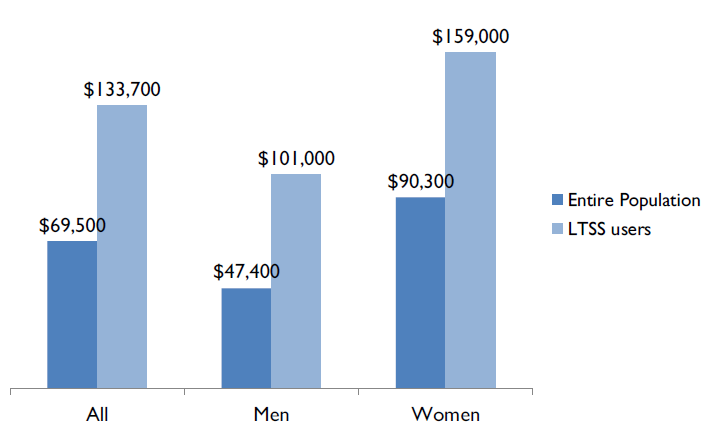

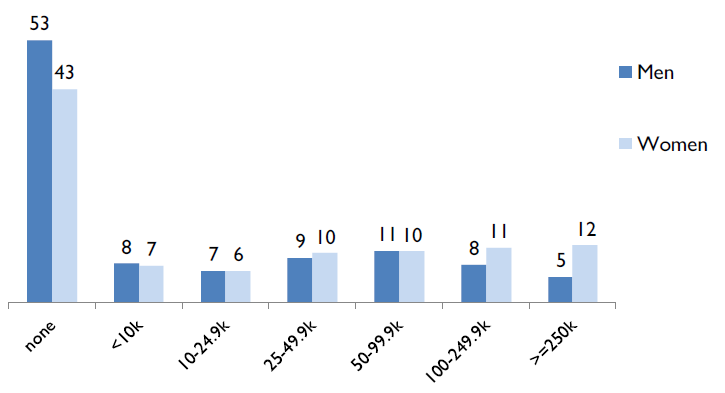

Expected present discounted value of formal LTSS costs ($2015) at age 65 (HIPAA level)

Lifetime costs vary widely over the full population

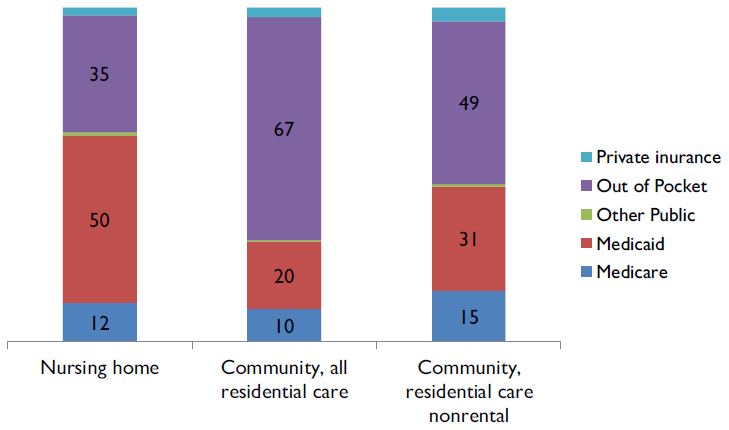

Payers Vary Sharply by Setting

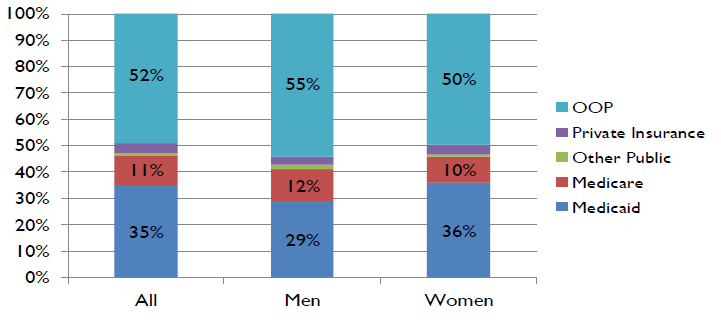

Medicaid Pays a Larger Share of LTSS Costs for Women than Men

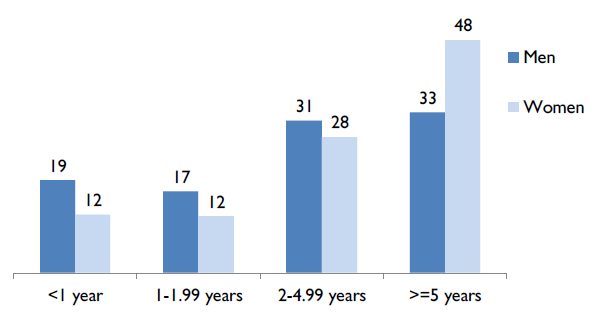

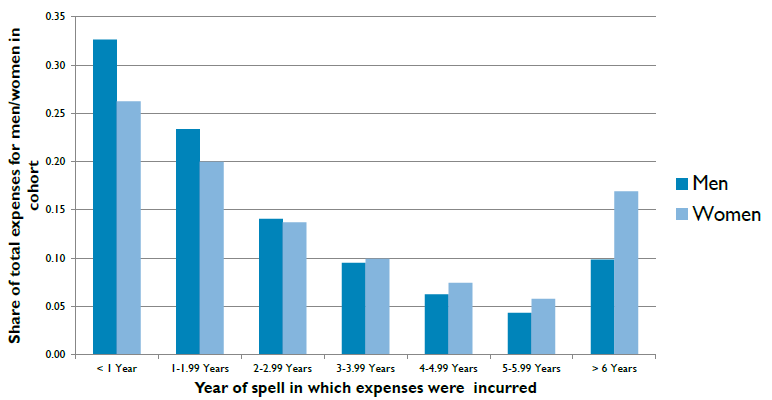

Those disabled for a long time account for a large share of total formal LTSS expenditures

Most LTSS expenses are incurred within two years, but an important share occur later

Payer mix varies by income, length of disability spell

- Medicaid LTSS users are concentrated in the lowest income quintile

- Brenda and Tim’s analyses

- LTSS users paying large amounts out of pocket are more likely to be in the highest income quintile

- Costs for shorter disability spells are disproportionately paid out of pocket

- Medicaid pays proportionately more for longer disability spells

Policy challenges

- Tradeoffs between costs and comprehensiveness

- Cover expected costs of all or expected costs of users?

- People want comprehensive coverage and low cost

- If LTSS financing proposal is to help the maximum number of people, front-end coverage may be preferable

- Hawaii is pursuing this approach

- Help at transitional time

- If LTSS financing proposal is to help those with the largest expenses, back-end coverage may make sense

- Consistent with insuring against longevity risk

- May generate more Medicaid savings

- Complicated by greater longevity for those with higher status

Caveat: Results Sensitive to Many Choices

- Lifetime need estimate is higher when one includes lower levels of needs (e.g., multiple IADLs but no ADLs, moderate cognitive impairment)

- Closer to 70 percent will ever have LTSS needs

- Lifetime costs and payer mix are sensitive to whether you include rental component of residential care

- Payer mix is sensitive to whether you focus on characteristics of payments or of people

- Lifetime expenses are sensitive to whether you consider interest payments that a lump sum could accrue (present value) or whether you consider payments as they arise

- Appendix versus body of brief

- Lifetime expenses are sensitive to treatment of lower disability in nursing homes