U.S. Department of Health and Human Services

The Past, Present and Future of Managed Long-Term Care

Paul Saucier, Brian Burwell and Kerstin Gerst

Thomson/MEDSTAT and University of Southern Maine, Muskie School of Public Service

April 2005

This policy brief was prepared under contract #HHS-100-97-0019 between the U.S. Department of Health and Human Services (HHS), Office of Disability, Aging and Long-Term Care Policy (DALTCP) and the MEDSTAT Group. For additional information about the study, you may visit the DALTCP home page at http://aspe.hhs.gov/_/office_specific/daltcp.cfm or contact the ASPE Project Officer, Hunter McKay, at HHS/ASPE/DALTCP, Room 424E, H.H. Humphrey Building, 200 Independence Avenue, SW, Washington, DC 20201. His e-mail address is: Hunter.McKay@hhs.gov.

The opinions and views expressed in this report are those of the authors. They do not necessarily reflect the views of the Department of Health and Human Services, the contractor or any other funding organization.

TABLE OF CONTENTS

- 1. BACKGROUND

- Issue Summary

- Methods

- History of Managed Long-Term Care

- Current Status of the Managed Long-Term Care Market

- 4. WHAT VALUE DOES MANAGED LONG-TERM CARE OFFER?

- Access

- Costs

- Quality

- 5. THE FUTURE OF MANAGED LONG-TERM CARE

- Key Issues Affecting Growth

- Supply Side Issues

- Summary

- APPENDIX 1: METHOD FOR DERIVING THE SIZE OF THE PUBLIC LONG-TERM CARE MARKET

SUMMARY

A decade ago, managed long-term care appeared poised for dramatic growth, but despite significant activity in a handful of states, today only 2.3% of persons using public long-term care services are receiving those services in managed care programs, and Arizona remains the only state that provides all long-term care through managed care. The number of enrollees in managed long-term care is likely to grow in the next few years. Texas has proposed a large expansion of its initiative. Other states with established programs, including Florida, Minnesota and Massachusetts, also expect growth but more incrementally and on a smaller base than Texas. States with plans to add managed long-term care initiatives in the near future include California (San Diego County), Washington, Hawaii and Maryland.

Managed long-term care suppliers are largely local non-profit plans or provider organizations that evolved specifically to respond to a single state's procurement. However, two national commercial HMOs, Evercare and AmeriGroup, have multi-state presence and account for a substantial portion of all managed long-term care enrollment.

Several factors have contributed to the slow growth of managed long-term care, including complex program design choices (including payment methodology), relatively long planning and start-up periods, resistance of long-term care providers and advocates, difficult state-federal policy issues, the need for a substantial population base, limited interest among potential suppliers, and inadequate state infrastructure in an era of government downsizing.

Despite these challenges, managed long-term care is popular in states where it is established and is likely to grow in the future. Studies of managed long-term care programs have been largely positive, finding high consumer satisfaction levels, lower utilization of institutional services and increased access to home- and community-based services. Cost studies have been more mixed, with no clear consensus emerging as to whether managed long-term care saves money for public purchasers. Savings notwithstanding, the budget predictability that comes with capitated payments is appealing to state policymakers as growing numbers of long-term care consumers place increasing pressure on Medicaid budgets. Evolving legal authority has resulted in simplified program designs and faster federal approval. Supply may expand as commercial HMOs experience aging members and add products to retain them, local plans attempt replication in new states, and Medicare Advantage plans experiment with the specialized plan provision of the Medicare Prescription Drug, Improvement, and Modernization Act of 2003.

1. BACKGROUND

Issue Summary

In 2003, about 3.1 million older persons and persons with physical disabilities received Medicaid-financed longterm care services (Table 1).1 Just over half (55%) were in nursing homes and the remainder received services in community-based settings, either through the Medicaid home and community-based waiver services program or through a state Medicaid plan benefit, such as personal care services. A large majority of them were also eligible for Medicare. Total combined Medicaid and Medicare expenditures for these 3.1 million persons were approximately $132 billion in 2003. Although Medicare does not pay for long-term care, its acute and post-acute care expenditures are much higher for long-term care users. Average expenditures for Medicare beneficiaries with ADL limitations (an indicator of long-term care need) are four times higher than for persons with no ADL limitations.2 The number of people using long-term care and their public expenditures promise to rise more rapidly in the coming decades as the baby boomers age and the number of non-elderly adults with disabilities increases.

Long-term care users need a variety of services across numerous settings (e.g., home, doctor's office, hospital, day center, nursing home), but in the Medicaid and Medicare fee for service systems, no single person or organization is responsible for or can impact all needed care, resulting in services that are often characterized as fragmented, uncoordinated and rife with unintended financial incentives. State home-and community-based services (HCBS) programs almost always provide case management, but the management does not extend into the hospital or nursing home when someone is admitted. Often, a community case manager learns about a hospital discharge after the fact, with no ability to ensure a smooth transition across settings. Avoidable hospital admissions, unnecessary use of nursing home care, and medication mismanagement are among the risks faced by the population.

The application of managed care strategies to aged and disabled long-term care beneficiaries holds intrinsic appeal. In the mid-1990s, many states were actively planning initiatives that would build on their Medicaid managed care experience to create managed long-term programs, but by 2004, less than 3% of the publicly-funded long-term care population received their long-term care benefits through a managed care program.

| TABLE 1: Estimated Size of the Public Long-Term Care Market, 2003 | ||

| Beneficiaries | In Nursing Homse | 1,700,000 |

| In HCBS Waiver Programs | 550,000 | |

| Receiving Personal Care Services | 830,000 | |

| TOTAL | 3,080,000 | |

| Expenditures | For Institutionalized Beneficiaries: | |

| Medicaid NF Expenditures | $44.8 billion | |

| Other Medicaid Expenditures | $19.2 billion | |

| Medicare Expenditures | $22.5 billion | |

| TOTAL | $86.5. billion | |

| For Community-Based Long-Term Care Beneficiaries: | ||

| HCBS Waiver Expenditures | $4.1 billion | |

| Personal Care Expenditures | $5.0 billion | |

| Other Medicaid Expenditures | $10.6 billion | |

| Medicare Expenditures | $26.1 billion | |

| TOTAL | $45.8 billion | |

| NOTE: These are preliminary estimates. Estimates only include aged and disabled Medicaid beneficiaries receiving long-term care benefits. Excludes persons with developmental disabilities and/or severe mental illness. | ||

Why has the market grown so slowly, and where is it headed? This study assesses the state of the managed long-term care market from the perspective of purchasers (states) and suppliers (managed long-term care contractors), addressing the following questions:

- What is the current state of the managed long-term care market?

- What value do managed long-term care products offer relative to the fee-for-service system?

- What is the market outlook in terms of future demand from state purchasers and supply from existing and new organizations?

Methods

We define managed long-term care as any arrangement in which a Medicaid program contracts with an organization to provide a package of benefits which includes at least some long-term care benefits on a risk basis. The focus of the study is Medicaid-financed long-term care, though the discussion includes Medicare since most Medicaid long-term care beneficiaries are dually eligible. Thus the study includes both Medicaid-only programs and integrated programs that manage both Medicaid and Medicare benefits. We focused on older persons and persons with physical disabilities, and excluded programs that are primarily targeted to persons with developmental disabilities or severe and persistent mental illness.

We collected data from a number of sources. Site visits were conducted to programs in three states, in which state officials and managed care organization officials were interviewed. Telephone interviews were held with key informants in four additional states and at several national organizations. A literature review was conducted to identify studies of managed long-term care programs. Finally, descriptive information was gathered at the managed care organization level for all programs that met our definition.

Due to the sensitive nature of the information gathered, the responses of individuals remain confidential.

History of Managed Long-Term Care

Most states have similar histories and concerns with Medicaid-funded long-term care. The 1970s were marked by large increases in nursing home expenditures and growing concern about the sustainability of a long-term care system dominated by institutional care. In 1981, Congress created the home- and community-based waiver option (HCBS waiver), allowing states to create flexible community-based services and cover them under the same financial and clinical eligibility provisions as nursing home benefits. The HCBS waiver program grew rapidly, from six states spending $3.8 million in 1982 to 48 states spending just under $1.7 billion in 1991.3 However, Medicaid nursing home expenditures continued to grow in the 1980s, from $10.5 billion to $17.9 billion, making it clear that HCBS waiver programs would not alone control the growth of institutional care. Despite efforts to control the supply of nursing homes and ease consumer entry into community-based services with "single entry point" systems, nursing home expenditures in the 1990s continued to grow more rapidly than Medicaid expenditures generally, limiting states' fiscal capacity to expand HCBS options.

By the early 1990s, managed care had become the dominant mode of acute health care financing and delivery in commercial markets, and states were enrolling substantial numbers of women and children in Medicaid managed care plans. A few early managed long-term care programs (Arizona's Long Term Care System, Florida's Frail Elder Option and initial PACE replication of San Francisco's On Lok program) had been implemented in the 1980s. The Social HMO, a Medicare demonstration that added a limited long-term care benefit to Medicare, had also been implemented in the late 1980s.

In the 1990s, a number of states wanted to build on their Medicaid managed acute care experience to add long-term care. Minnesota, Colorado and Wisconsin were among the states that provided leadership by developing innovative models that borrowed concepts from PACE, ALTCS and S/HMO. Minnesota was the first state to implement a fully integrated model that combines both Medicare and Medicaid financing for the entire spectrum of older people, from well to frail. After many years in development, the Minnesota Senior Health Options (MSHO) program was implemented in 1997 under a combined Section 1115 Medicaid demonstration waiver and Section 222 Medicare payment waiver. A key design feature of MSHO is the employment of a single contract between the state and the MSHO plans for both Medicare and Medicaid terms and conditions. A significant effort was made during the MSHO development process to "align" Medicare and Medicaid managed care requirements into a comprehensive and uniform contract. (Based on its experience with MSHO, Minnesota implemented a similar program for people with physical disabilities--the Minnesota Disability Health Options (MnDHO) Program--in 2001.)

Many states demonstrated considerable interest in launching Minnesota-like initiatives in the mid-1990s, and the Robert Wood Johnson Foundation supported a number of planning and development grants in this area through the Medicare/Medicaid Integration Program (MMIP) at the University of Maryland, which served as a focal point for research and collaboration among states for program development activities.

With funding from the Commonwealth Fund, New York State supported demonstration programs in managed long-term care beginning in 1994. In 1997, New York consolidated its PACE and other managed long-term care plans under one legislative authority. The legislation is flexible, and plan sponsors can develop varying models of delivery and financing. Currently, there are 15 separate managed long-term care plans operating under the authority. Four of the 15 are fully certified PACE sites, and a fifth is a partially capitated "pre-PACE" site. With the exception of the plan operated by the Visiting Nursing Service of New York, with an enrollment of 3,700 members, most of the New York plans have fewer than 500 members.

In 1995, the Texas Legislature authorized the development of managed long-term care pilot programs, which led to the implementation of Texas Star+Plus in 1998, the second mandatory program after ALTCS, but only in a single county (Harris). Unlike Minnesota, Texas decided to begin its Star+Plus initiative as a capitated Medicaid program, while providing beneficiaries with access and incentives to join optional companion Medicare managed care plans. This was a conscious decision by state program administrators to quickly bring Texas Star+Plus to scale as a mandatory Medicaid program, but incorporate mechanisms to integrate Medicare incrementally.

In 1996, Wisconsin began implementing its Partnership Program, a variation on PACE that includes both older and younger people with disabilities and allows beneficiaries to bring their existing doctors into the program network. Partnership began operating as a partially capitated Medicaid managed care program and added capitated Medicare benefits in 1999. When the Partnership Program was held out as a model for statewide comprehensive redesign of the long-term care system, advocates and counties opposed the move, and in 2000, the state instead piloted the Family Care Program, which capitates only long-term care funding. A unique feature of the Family Care program is that counties serve as the managed care contractor, accepting financial risk for meeting the needs of all persons requiring long-term care services in the county.

The creation of the Florida Diversion Program in 1998 added another managed LTC option to the already existing Frail Elder Option that had operated in Southeast Florida since 1987. The voluntary Diversion program was initially implemented in four Florida counties. In 2003, the Florida legislature granted additional funding to expand the program to cover 25 counties, and in 2004, it further mandated that the Frail Elder Option be folded into the newly expanding Diversion program.

While a number of states successfully launched managed long-term care initiatives in the 1990s, there were quite a few initiatives in other states that were not successful. A number of states announced their intention to implement managed long-term care programs, either on a demonstration basis or on a larger statewide basis, only to have the initiative cease at some point during the development stage. Two major challenges were: (1) resistance from long-term care providers and the aging network; and (2) lack of willing suppliers, particularly in rural areas. Long-term care providers, particularly nursing home providers, often saw the selective contracting aspect of managed care as an economic threat. Providers were also concerned about the delegation of Medicaid rate setting authority from state agencies to private contractors. Elderly advocacy organizations were often unconvinced that improved care coordination could lead to better outcomes for program participants. They feared that managed care contracting would result in reduced access to medical and long-term care services or that plans would pull out as they had done in the Medicare managed care market. Another occasional source of resistance was state workers, particularly if the initiative involved the outsourcing of case management jobs or other administrative positions to managed care contractors.

During the late 1990s, and early in the new millennium, there was very little activity in the managed long-term care market. Some wondered whether managed long-term care was an idea whose time had come and gone. But then after almost eight years of development, Massachusetts and CMS finally issued a procurement for the Senior Care Options (SCO) program in 2003. A key factor in these negotiations concerned the risk adjuster that would be used for Medicare capitation payments for SCO members with long-term care needs. CMS agreed to use the PACE risk adjuster of 2.39 for this group. Another key provision of the agreement was that CMS and Massachusetts would jointly negotiate the Medicare contracts with the participating plans. In 2003, Massachusetts selected three plans to participate in the SCO program, and enrollment in the program began in early 2004.

Current Status of the Managed Long-Term Care Market

Table 2 presents estimated enrollment in managed long-term care programs in 2003-2004. The estimates include only persons who are receiving long-term care benefits in the designated programs. For example, total enrollment in the Texas Star+Plus Program is approximately 60,000 members, but the majority of the members are SSI Disabled beneficiaries who do not receive long-term care benefits under the program. Similarly, the Minnesota Senior Health Options Program enrolls "well" elderly persons as well as persons with long-term care needs. The Table 2 estimates also include only aged individuals and adults with physical disabilities enrolled in managed long-term care programs, and do not include persons with developmental disabilities or persons with severe mental illness enrolled in managed long-term care.

| TABLE 2: Estimated Enrollment in Managed Long-Term Care Programs, 2004 | |

| MLTC Program | LTC Enrollment |

| ALTCS | 23,427 |

| Texas Star Plus | 10,671 |

| NY MLTC | 7,0781 |

| PACE and "Pre-PACE"2 | 8,419 |

| Wisconsin Family Care | 6,998 |

| MSHO | 3,910 |

| Florida Frail Elder Program | 3,070 |

| Florida Diversion | 2,800 |

| Wisconsin Partnership | 1,644 |

| Massachusetts SCO | 100 |

| TOTAL | 68,117 |

Estimated enrollment only includes aged or disabled Medicaid beneficiaries receiving long-term care benefits. Does not include persons with developmental disabilities or severe mental illnesses. | |

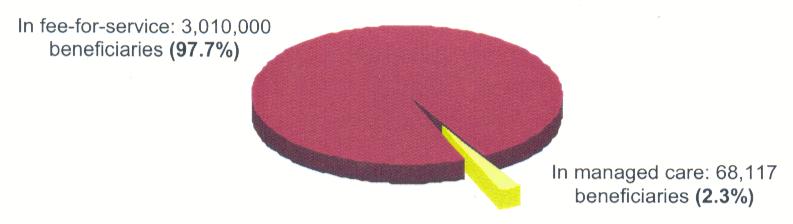

As shown in Figure 1, we estimate that just under 70,000 of the approximately 3.1 million Medicaid beneficiaries receiving long-term care benefits were in risk-based managed long-term care programs in 2004.4 This equals a managed care penetration rate of only 2.3%. Clearly, the managed long-term care market is still at a very early stage of development.

| FIGURE 1: Managed Care Penetration of Medicaid Long-Term Care Market |

|

2. STATE DEMAND FOR MANAGED LONG-TERM CARE

Between passage of the Balanced Budget Act of 1997 and the Medicare Modernization Act of 2003, demand for managed long-term care came from 9 state-developed programs in 7 states and 40 PACE or "pre-PACE" sites in 17 states.5 Outside of PACE, program characteristics vary greatly, as summarized in Table 3.

Target populations vary. Several of the programs examined include older people and younger people with disabilities. The most population-inclusive of these is the Texas Star+Plus program, which includes all adults who qualify for Medicaid by virtue of SSI status (Aged, Blind or Disabled). Other programs enroll only older people (Massachusetts, Florida Diversion, MSHO, PACE).

Another important population distinction is functional need. All of the programs include persons with very high functional needs who are eligible for traditional home- and community-based services (HCBS) waiver programs. These are persons at the high end of community services and costs. Some programs (ALTCS, Wisconsin Partnership, New York, Florida Frail Elder and Diversion, PACE) include only such persons, while others (MSHO, MnDHO, Star+Plus, SCO) include persons with the entire range of needs, including those with no existing long-term care need. Wisconsin's Family Care program falls in between, serving persons who have a range of existing long-term care needs, including but not limited to those whose needs rise to the level of HCBS waiver programs.

Geographical scope varies, but the primary focus is on urban areas. With the exception of Arizona, none of the programs covers all areas of its state. Most are limited to a county or multiple counties with urban centers. Most state and plan officials consulted believe that managed long-term care needs an urban base to be viable. Plans want a sufficiently large target group to ensure adequate volume, particularly in voluntary programs. They also rely on an adequate supply of long-term care providers to establish networks. In Arizona, rural counties are generally limited to one ALTCS plan, and it is almost always operated by county government.

Breadth of managed care benefit package. With the exception of Wisconsin Family Care and the New York Managed Long Term Care Plans, programs capitate Medicaid-funded primary, acute and long-term care benefits for enrolled members. In Family Care and the New York plans, long-term care contractors are expected to coordinate with primary and acute providers but do not receive capitated payment for those services and are not responsible for them. Other service-specific variations exist. For example, Texas has a third party prescription drug vendor that it uses to reimburse all Medicaid prescription drugs, so the benefit is carved out of Star+Plus and administered separately by that vendor.

| TABLE 3: Characteristics of Selected Managed Long-Term Care Programs | ||||||

| Program | Implementation Date | Population Eligible | Voluntary/ Mandatory for Medicaid | Geographical Coverage | Medicaid Payments | Medicare Payments |

| PACE (includes "pre-PACE) | 1983 (On Lok) | 55+ with NF-level LTC needs | Voluntary | 40 urban programs in 17 states | Capitated primary, acute and LTC; rate structure varies | Capitated |

| Florida Frail Elder Option | 1987 | Aged and disabled; NF-level LTC needs | Voluntary | 2 urban counties in Southeast Florida | Capitated primary, acute and LTC; three rate cells | FFS |

| Arizona Long Term Care System (ALTCS) | 1989 | Aged and disabled; NF-level LTC needs | Mandatory | Statewide (urban and rural) | Capitated primary, acute and LTC; single blended rate | FFS1 |

| Wisconsin Partnership Program | 19952 | Aged and disabled; any LTC needs | Voluntary | 6 counties (rural and urban) | Capitated primary, acute and LTC; multiple rate categories | Capitated |

| Minnesota Senior Health Options (MSHO) | 1997 | All aged | Voluntary | 7 urban and 3 rural counties | Capitated primary, acute and LTC (NF limited to 6 mos.); multiple rate cells | Capitated |

| New York MLTC Plans | 1997 | Aged and disabled with NF-level LTC needs (aged/ disabled varies by plan) | Voluntary | Multiple counties (rural and urban, but mostly urban) | Capitated LTC only (primary and acute FFS); multiple rate cells | FFS |

| Texas Access Reform (Star) + Plus | 1998 | All aged and disabled | Mandatory | 1 urban county; statewide urban expansion proposed | Capitated primary, acute and LT (NF limited to 1 mo.; Rx not in cap); multiple rate cells | FFS1 |

| Florida Diversion | 1998 | Aged with NF-level LTC needs | Voluntary | 25 urban and contiguous counties | Capitated primary, acute and LTC; single rate | FFS |

| Wisconsin Family Care | 2000 | Aged and disabled; NF-level LTC needs | Mandatory | 5 counties (rural and urban) | Capitated LTC only (primary and acute FFS); two rate cells | FFS |

| MnDHO | 2001 | All physically disabled | Voluntary | 4 urban counties | Capitated primary, acute and LTC (NF limited to 6 mos.); multiple rate cells | Capitated |

| Mass Health Senior Care Options (SCO) | 2004 | All aged | Voluntary | Nearly statewide (rural and urban) | Capitated primary, acute and LTC; multiple rate cells | Capitated |

| ||||||

MSHO, Wisconsin Partnership, SCO and PACE programs include fully capitated Medicare benefits in addition to Medicaid benefits. These programs were designed to include comprehensive care coordination for dually eligible members, who typically comprise more than 90% of elderly Medicaid beneficiaries and as much as 50% of younger people with disabilities. Most state officials interviewed expressed interest in the more comprehensive approach but cited long development time as a significant obstacle. There are also significant differences among the fully capitated programs, particularly in how they relate to providers. MSHO relies on participating plans to interact with and manage provider practice across extensive networks, while PACE more closely resembles a staff-model HMO, in which the key providers (members of the Interdisciplinary Team) are employees of the managed care contractor and are directly implementing the integrated care. The Wisconsin Partnership Program falls somewhere in between, with core team members on staff (like PACE) but including a network of independent practice physicians who must be oriented to the philosophy and practice of the program, and whose services must be integrated with those of long-term care providers via communication and education (as opposed to co-location).

Most programs are voluntary, but a large majority of members are in mandatory programs. Most of the programs studied are voluntary for Medicaid beneficiaries, meaning they can opt instead for the state's traditional long-term care services. Many factors impact a state's decision on this controversial issue, including:

- Adequate enrollment levels. A managed care organization's ability to manage risk depends in part on being able to spread risk across a large number of members. The three mandatory programs studied (Wisconsin Family Care, Texas and Arizona) are also the largest in terms of enrollment, ranging from 7,000 long-term care consumers in Wisconsin to over 23,000 in Arizona.6 Also important is having a program of sufficient size to warrant the investments in state infrastructure that must be made to design, implement and monitor these programs.

- Consumer and provider concerns. Consumers and long-term care providers often argue for voluntary programs. Consumers of long-term services often have established relationships with providers and fear that mandatory programs would force them into new relationships. Providers fear losing their ability to bill the state directly for services and being required to build new business relationships with managed care plans.

- Medicare. As previously mentioned, PACE, MSHO, Wisconsin Partnership and SCO were all designed with the specific intent to integrate long-term care with acute services, making Medicare inclusion paramount. Freedom of choice may not be waived in Medicare, so programs including Medicare must be voluntary.

Some states protect traditional long-term care infrastructure. States also differ on how they treat traditional long-term care providers (including counties) under managed care. Most states expressed ambivalence on this question. A pure market approach would dictate an open and competitive procurement of managed care organizations and would give MCOs discretion to select and pay network providers as they see fit, allowing the state to focus more on outcomes and less on processes and structures. On the other hand, given the experience with Medicare HMO retrenchment in the late 1990s, states want to ensure that an adequate supply of long-term care providers will remain if managed care fails as a strategy. A few programs, like MSHO and the Wisconsin Partnership, have not provided any policy protection for long-term care providers. Texas, addressing early concerns of traditional long-term care providers, gave them three years of transitional protection. During that period, the Texas Star+Plus plans were required to contract with any willing provider that had been providing Medicaid long-term care services in the fee-for-service system. In Massachusetts, Senior Care Organizations are required to subcontract with at least one Aging Services Access Point (ASAP), the State's traditional portal for community long-term care services.

Another approach to protecting existing long-term care infrastructure is to ensure that traditional providers (including counties) can themselves become risk-bearing managed care organizations. ALTCS and Wisconsin Family Care both give counties, which had substantial stakes in those states' long-term care systems, first right of refusal to be MCOs. In Arizona, counties had been the primary funders and operators of long-term care services prior to implementation of ALTCS, and in Wisconsin, they had administered long-term care programs at the local level. In Florida and New York, certain long-term care providers were made eligible to become program contractors, giving them an opportunity to compete with HMOs and other managed care entities.

A seller's market to date. Variation in the processes used by purchasers to select plan contractors belies the assertion that nearly all states have found managed long-term care to be a seller's market. Some states issue RFPs and others do not, but in most states, substantial behind-the-scenes work has transpired to ensure that states get an adequate number of bidders. Many states have had concerns during the development phase that "no one would come to the party." Some states have structured interim rates (to minimize start-up risk), some have developed special insurance rules to reduce capitalization requirements, and others have explicitly or implicitly linked bids on managed long-term care to more popular and profitable TANF or SCHIP contracts. There are signs, also, that future procurement may be more competitive. Officials in two states with planned expansions report that several new organizations have expressed interest in bidding on future rounds.

Why so much program variation? The early managed long-term care experience reflects the variation found across state Medicaid programs generally. Despite sharing similar challenges in their long-term care systems, states are experimenting with several approaches. Several local factors appear to have influenced the policy and program designs of the ten programs studied.

When did planning for the program occur? In the early 1990s, the Minnesota Senior Health Options and Wisconsin Partnership initiatives attracted much attention and excitement from other states. Both states proposed models that would fully integrate acute and long-term care by combining Medicaid and Medicare financing streams, and both experienced protracted planning phases of more than five years, in part because of difficult negotiations with HCFA (now CMS) regarding Medicare payments, complicated by Office of Management and Budget (OMB) concerns that the proposed payments would not be cost neutral. By the time Wisconsin and Minnesota implemented their programs in the late 1990s, states like Texas and Florida were considering alternatives to the fully integrated financing model that would allow them to implement programs in the short-term. By taking Medicare off the table and working with CMS to develop unprecedented approaches to HCBS waivers, these states were able to implement programs within a few years of beginning their planning. Rather than shutting the door on Medicare altogether, Texas included incentives for dually eligible consumers to join companion Medicare+Choice plans (now Medicare Advantage). About 3000 Star+Plus members are enrolled in the one companion Medicare plan that is currently offered by Evercare. Table 4 shows how states have moved from more complex demonstration waivers to more mainstream statutory authority over time.

| TABLE 4: Legal Authority of Managed Long-Term Care Programs | ||

| Program | Medicaid Authority | Medicare Authority |

| PACE | State plan optional service under §1934 of Social Security Act (enacted in Balanced Budget Act of 1997) | §1894 (enacted in Balanced Budget Act of 1997) |

| Florida Frail Elder Option | Began as §1115 waiver-converted to 1915(a) and (c) in 1990 | NA |

| Arizona Long Term Care System (ALTCS) | §1115 waiver | §1853* |

| Wisconsin Partnership Program | Began in 1995 as a prepaid health plan (no waiver) until §1115 waiver was awarded (1999) | §222 waiver (since 1999) |

| Minnesota Senior Health Options (MSHO) | Began as §1115 waiver-converted to 1915(a) and (c) in 2000 | §222 waiver |

| New York MLTC Plans | §1915(a) and (c) | NA |

| Texas Access Reform (Star) + Plus | §1915(b) and (c) | §1853* |

| Florida Diversion | §1915(a) and (c) | NA |

| Wisconsin Family Care | §1915(b) and (c) | NA |

| MnDHO | §1915(a) and (c) | §222 waiver |

| Mass Health Senior Care Options (SCO) | §1915(a) | §222 waiver |

| * Some beneficiaries in Arizona and Texas have access to a companion Medicare+Choice (now Medicare Advantage) plan initially authorized under §1853 of the Social Security Act, but most receive Medicare services in the fee-for-service system. | ||

What role has the aging network played? The impact of advocacy from the aging network is clearly visible in a few of the programs. In Wisconsin, Area Agencies on Aging and Councils on Aging are operated by counties, which also administer local eligibility systems for long-term care benefits. When the State Department of Health and Family Services released its plan for long-term care reform based on the Partnership model of fully integrated acute and long-term care, aging and disability advocates organized strong opposition at a series of public hearings. They were concerned that integrated plans would be dominated by medically-oriented HMOs, and the aging network would lose its role in the system. The Department withdrew its plan, and the Family Care program was developed instead, featuring a prominent role for counties and limiting the program to long-term care. In Massachusetts, a network of Aging Services Access Points (ASAPs) serves a number of roles. Several are designated Area Agencies on Aging, and several are providers of care coordination, home care, and other long-term care services. Like the counties in Wisconsin, the ASAPs saw Massachusetts Senior Care Options program as a threat to their existing role and feared that it would be a medical model that would take long-term care in the wrong direction. The ASAPs appealed directly to the state legislature and emerged with a change to the program design that requires SCO contractors to subcontract with one or more ASAPs to provide community care coordination, in cooperation with the primary care team that will oversee members' care plans.

How active were long-term care providers? Long-term care providers have had varying levels of influence on the design of managed long-term care programs. Early in the implementation of Star+Plus, Texas nursing home providers successfully lobbied to have their payments removed from the managed care plans' capitation rates for long-term admissions (longer than 30 days). Other Texas providers (including adult day health and personal care providers) had expressed concerns that they would go out of business if the health plans chose not to contract with them, so the State required that plans contract for at least three years with all willing long-term care providers who had been participating in the State's Medicaid fee-for-service program. (Texas officials note that Star+Plus plans actually contract with more long-term care providers now than they did during the 3-year transition period.) In New York State, provider agencies were actively involved in developing the state's statutory framework authorizing managed long-term care, and all of the state's 15 managed long-term care plans are sponsored by provider organizations. In Florida, certain long-term care providers are statutorily eligible to become diversion program contractors by virtue of their state provider licensure status.

3. THE SUPPLY SIDE: WHAT HAS EMERGED IN THE MARKET?

While purchasers (states) may be showing growing interest in the use of managed care models to purchase Medicaid benefits for long-term care populations, the future success of the market also depends upon the development of organizations that can provide what purchasers want to buy. This section examines the supply side of the managed long-term care marketplace.

In developing managed long-term care programs, states are seeking business relationships with managed care entities with expertise in the clinical and social management of long-term care populations. Traditional health plans do not possess expertise in long-term care, nor do their existing networks include the range of long-term care providers needed to serve persons with long-term care needs. On the other hand, organizations with expertise in providing services to long-term care populations tend to have little or no experience in managed care. Therefore, successful development of the supply side of the market requires the merging of managed care expertise with experience in the management of long-term care populations.

Consequently, two kinds of managed long-term entities are emerging in the marketplace: (1) managed care companies that are expanding into the long-term business; and (2) long-term care companies that are expanding into the managed care business. To date, the marketplace is dominated by the latter and this has had important effects on the overall success of the market.

We identified 67 different organizations providing long-term care services to aged and disabled Medicaid beneficiaries under risk contracts (Table 5). The vast majority are small private nonprofit plans with total enrollments under 1,000 members. This includes all of the PACE and "pre-PACE" sites, as well as the Prepaid Health Plans participating in the New York Managed Long Term Care Demonstration. Most serve both aged and disabled populations, and a high percentage of the members enrolled in the plans are dually eligible for Medicaid and Medicare. Table 5 also shows that most plans serve an enrolled population that largely resides in community-based setting, not in nursing homes. It is fair to say that the current managed long-term care market is concentrated on the management of long-term care beneficiaries in community-based settings, not on the management of people residing in nursing homes.

There are only two major for-profit players currently participating in the market--EverCare and Amerigroup. Evercare, an affiliate of UnitedHealth Group, is the dominant player in the managed long-term care marketplace. It is the one commercial company that has clearly made a long-range investment in this product line. Evercare focuses exclusively on products related to the care management of frail elders and persons of all ages with physical disabilities. Its business strategy reflects a firm belief that government purchasers (CMS and state Medicaid programs) will increasingly turn to managed care purchasing strategies for providing integrated medical services and long-term care supports to frail elders, and Evercare's business strategy anticipates this trend. Evercare is aggressively pursuing new market opportunities in managed long-term care across the entire country, and is also working actively at the state and federal levels to increase market demand. Currently Evercare holds managed long-term care contracts (or subcontracts) in Arizona, Texas, Minnesota, Florida and Massachusetts, and is expected to bid on the upcoming expansions of Texas Star+Plus and the Florida Diversion Program.

| TABLE 5: Managed Long-Term Care Supplier Characteristics | ||

| (N) | Percent | |

| Type of Organization | ||

| For-profit | (9) | 13% |

| Not for-profit | (47) | 70% |

| Local Government Agency | (10) | 15% |

| State Government Agency | (1) | 1% |

| TOTAL | (67) | 100% |

| Geographic Coverage | ||

| Multiple Counties | (32) | 48% |

| One County | (35) | 52% |

| TOTAL | (67) | 100% |

| Enrollment | ||

| 100 | (4) | 6% |

| 101-1,000 | (12) | 18% |

| 1,001-5,000 | (32) | 48% |

| 5,001+ | (2) | 3% |

| Unknown | (17) | 25% |

| TOTAL | (67) | 100% |

| Percent in Nursing Homes | ||

| 51+% | (2) | 3% |

| 25-50% | (7) | 10% |

| 25% | (38) | 57% |

| Unknown | (20) | 30% |

| TOTAL | (67) | 100% |

| Percent Dually Eligible | ||

| 90+% | (34) | 51% |

| 50-89% | (19) | 28% |

| 50% | (1) | 1% |

| Unknown | (13) | 19% |

| TOTAL | (67) | 100% |

| Population Served | ||

| Aged only | (16) | 24% |

| Disabled only | (3) | 4% |

| Both aged and disabled | (47) | 70% |

| Other | (1) | 1% |

| TOTAL | (67) | 100% |

On the for-profit side, Amerigroup has emerged as Evercare's primary competitor, with contracts in Texas Star+Plus and the Florida Diversion Program. Unlike Evercare, managed long-term care is not the core product line of Amerigroup. Rather, Amerigroup is a publicly traded company focused almost exclusively on the Medicaid market, with a total Medicaid membership of over 850,000 in 2003. Amerigroup's first entry into the managed long-term care market occurred in 1997 with the award of one of the Texas Star+Plus contracts in Harris County, where Evercare and Amerigroup are the only two remaining contractors (a third contractor dropped out of the program). Amerigroup also has a small plan in the Florida Diversion Program, through acquisition. Thus, Amerigroup represents a Medicaid specialty plan with a core focus on the "moms and kids" Medicaid business, but which has expanded into the Medicaid SSI and managed long-term care markets, building off its basic Medicaid infrastructure. Many of the managed care tools employed by Amerigroup in its managed long-term care contracts are variants of the tools developed for its acute care Medicaid business.

Minnesota state law requires health plans to be non-profit, and accordingly all three MSHO plans--Medica Health Plans, Metropolitan Health Plan, and UCare Minnesota--are non-profit. (Evercare participates as a subcontractor, in part because its for-profit status precludes it from contracting directly with the state.) All are Minnesota-based plans, which do not appear interested in expanding their managed long-term care business beyond Minnesota's borders. Medica is one of the largest health plans in the state, serving over 10,000 employers in Minnesota and bordering states. Metropolitan Health Plan and UCare Minnesota are smaller plans that are more focused on public programs, with Metropolitan being a spin off of Hennepin County government. While these three plans will probably continue to respond to future expansions of MSHO in Minnesota, they are not likely to seek contracts in other states.

Most organizations that have gotten into the managed long-term care business are provider-based organizations that have developed a managed care capacity. All 40 current PACE and "pre-PACE" providers are not-for-profit provider-sponsored organizations, generally integrated health care systems. All 15 plans participating in the New York Managed Long Term Care Program (5 of which are PACE or pre-PACE programs) are provider-sponsored plans, including hospitals, nursing homes, home health care agencies, and integrated health care systems. Similarly, the four plans in the Wisconsin Partnership Program are all community-based multiservice agencies that have decided to accept risk for the members they serve. Mercy Health Plan, one of three contractors in Maricopa County under the ALTCS program, also grew out of an integrated health care system, although it had some prior managed care experience.

A final group of plans participating in the managed long-term care market are publicly-owned plans. Pima Health System (Tucson) and Maricopa Long Term Care System (Phoenix) are the two largest contractors in the ALTCS program. Initially, these two plans were awarded exclusive contracts in their respective counties by legislative mandate. In October 2000, the Arizona legislature opened up Maricopa County to competitive bids, and now Maricopa Long Term Care System vies with two competing private sector plans (Mercy Health Plan and Evercare) for members. Three other county-based plans provide ALTCS services in six additional Arizona counties. In Wisconsin, all five Family Care program contractors are county-based plans.

It is interesting to note that two out of the three plans submitting bids on the recently-launched Senior Care Options program in Massachusetts are start-up organizations. Senior Whole Health is a for-profit start-up company backed with venture capital, while Commonwealth Care Alliance is a start-up non-profit organization capitalized largely with charitable contributions. Both were incorporated for the specific purpose of bidding on the Massachusetts SCO contract.

In summary, the supply side of the managed care marketplace is still in the early stages of development. The market is dominated by one large commercial plan (Evercare) that is actively pursuing managed long-term care business on a national scale. Its primary commercial competitor--Amerigroup--builds off its core competency in Medicaid acute managed care, but tends to only compete in states where it has already established a large market presence on the "moms and kids" side of the market. Otherwise, the managed long-term care market is made up of a large number of relatively small provider-sponsored plans, as well as a number of public plans, largely county-based. There is no evidence that any of these small local plans, whether they are PACE providers or other provider-based organizations, have entrepreneurial ambitions to leverage their local expertise in other markets. On the other hand, the purchasers with the largest managed long-term care initiatives (Arizona, Texas, and Florida) tend to rely on for-profit plans to serve their markets.

4. WHAT VALUE DOES MANAGED LONG-TERM CARE OFFER?

Some observers have questioned whether managed long-term care offers value relative to traditional HCBS services. In traditional fee-for-service programs, long-term care is typically coordinated by a case manager who is involved in the development and management of a care plan. So what exactly does a managed care organization add to the equation? Information available from evaluations, studies and interviews with program officials remain inconclusive, but some important positive patterns are emerging. Most studies have found and officials report that managed long-term care programs reduce the use of institutional services and increase the use of home- and community-based services relative to fee-for-service programs, and that consumer satisfaction is high. Undesirable outcomes, such as higher death rates or preventable admissions, have not emerged as a concern. Cost findings are mixed and more difficult to summarize, though in general studies that examined the costs of Medicaid-only programs have found them to be cost-effective more consistently than studies looking at both Medicaid and Medicare costs for integrated programs. While a few state officials were confident that their programs produce savings, most were more circumspect, citing possible favorable selection (in voluntary programs), inability to capture savings through existing payment structures, and lack of adequate cost data as concerns.

Inconclusive results notwithstanding, state officials consulted for this study were largely positive about their experiences with managed long-term care and believe that it offers value.

Access

Less inpatient care. One clear outcome across several studies and interviews is that managed long-term care, like managed acute care, reduces the use of high cost services, including emergency rooms, hospitals and nursing homes. In an evaluation for CMS of the Minnesota Senior Health Options program, Kane et al. found that MSHO reduced preventable emergency room admissions, hospital length of stay and short-stay nursing home admissions.7 Similarly, an Abt Associates evaluation of PACE found decreased inpatient hospital admissions and days, and decreased nursing home days.8

Similar findings emerge from Medicaid-only programs. The Wisconsin Family Care program includes only long-term care services; an independent assessor found in a pre/post study that hospital length of stay significantly decreased following enrollment in Family Care (although no change in hospital admission rates).9 A Texas Star+Plus study focusing on Medicaid-only SSI beneficiaries receiving Day Activity and Health Services or Personal Assistance Services found reduced hospital length of stay and fewer emergency room visits.10

Greater access to HCBS services. There is also evidence that managed long-term care increases access to HCBS waiver and other community services. The ALTCS program has progressively increased the use of HCBS services over time by adjusting its rates to assume diminishing nursing home use. The Wisconsin Family Care independent assessment found that waiting lists for long-term care in Family Care counties were eliminated while the waiting lists in comparison counties continued to increase. The Florida Legislature has chosen to expand funding for the Diversion program while cutting funds for Florida's traditional HCBS waiver programs, reportedly out of frustration that past increases to the traditional programs have not had a proportional impact on waiting lists. The Massachusetts SCO program will maintain benefits that have been cut from the FFS MassHealth program, including vision, dental, podiatry and hearing services. The MnDHO program has assisted 61 persons with physical disabilities leave nursing homes by providing alternative community services. In Star+Plus, plans are required to screen every new member and have as a result identified and addressed unmet LTC needs.

People enrolled in managed LTC programs are generally not subject to caps on the number of "slots" available for HCBS waiver services. Plans have the flexibility to provide LTC services to members who need them when they need them, and have incentives to do so when community services can prevent or reduce institutional use. In contrast, a recent national survey of 171 traditional HCBS waiver programs found that 69 of them had waiting lists. Among those reporting the length of wait, the average length was 10.6 months.11

More flexible services, including consumer-directed care. State officials report that capitated financing allows more flexibility in services than FFS. Examples include provision of pest extermination and air conditioners, items not generally covered in FFS systems. At least five programs (Wisconsin Family Care and Partnership, MSHO, MnDHO and Star+Plus) allow members to select and direct their own personal care attendants, creating a self-direction option within a managed care program without a need for additional waivers. In FFS, self-direction generally operates as a free-standing program that consumers must choose to the exclusion of other programs.

Lower consumer costs. Until recently, savings to consumers have not been a widespread benefit of managed LTC, because many Medicaid programs offered full benefits without cost sharing in FFS. Recent fiscal challenges have made cost sharing more widespread and benefits less expansive in Medicaid. Minnesota and Massachusetts, for example, both enacted new cost sharing requirements in their FFS programs in 2003, but MSHO and SCO providers have agreed to maintain full access without charging co-payments. Another example is PACE, which does not require Medicaid beneficiaries to make co-payments, regardless of a state's fee-for-service cost sharing policy.

Streamlined access to care. The most commonly cited goal among state managed long-term care program administrators is ease of access. Long-term care consumers find the fee-for-service system difficult to understand and navigate. Managed long-term care generally includes a care coordination mechanism to assist consumers and families with the system. While this is generally also true in fee-for-service HCBS programs, HCBS programs generally are not responsible for consumers when an acute episode results in hospitalization, often the time when coordination is most important. Managed LTC contractors, on the other hand, usually have financial incentives to manage transition periods because of their ongoing risk. (The incentive is greatest in programs with the most comprehensive risk designs.)

Costs

Cost studies are inconclusive. In the first evaluation of ALTCS, McCall et al. found overall savings of 6% and 13% in 1990 and 1991, but nearly all of the savings were attributable to members with developmental disabilities, and the study was limited by its use of a different state (New Mexico) for the comparison group.12 Weissert et al. took a different approach, developing a complex model that estimated nursing home savings resulting from the expansion of HCBS services in the ALTCS program and concluding that about 35% ($4.6 million) of estimated nursing home costs had been saved, net of added HCBS costs.13 A recent analysis conducted for the Texas Health and Human Services Commission by The Lewin Group estimated substantial Star+Plus savings if the program were expanded to 51 counties in metro areas of the state. Higher savings (8.6%) were projected for SSI beneficiaries under 65 years of age than for older people (5%).14 In the Wisconsin Family Care Program, savings were found in four out of five Family Care counties ($113 per member per month less than FFS comparison counties), but overall state savings disappeared when the fifth Family Care county (Milwaukee) was included in the analysis. In all three of these studies, only Medicaid costs are considered. Given the high proportion of dually eligible enrollees, it is possible that Medicaid savings derive from higher FFS Medicare costs.

Cost studies that include Medicare are more difficult to interpret and no more conclusive. The MSHO evaluation found that Medicare capitation payments were higher than FFS payments among comparison group members, but State officials have pointed out the study was conducted in the post-Balanced Budget Act period. The BBA effectively decoupled Medicare managed care rates from fee-for-service, allowing capitated payments to rise above average FFS expenditures. In the Abt PACE evaluation, combined Medicare and Medicaid payments to PACE were found to be comparable to the fee-for-service expenditures of the comparison group. Analyzed separately, Medicare payments were found to be lower for PACE enrollees than for the comparison group, and Medicaid payments were found to be higher. However, the cost analysis was limited to the first year of enrollment. A subsequent evaluation is analyzing costs over a longer period of time.

Payment systems are imperfect. Most of the state officials interviewed felt that they had not yet fully refined their payment systems. Texas has had concerns that plans within Star+Plus might experience adverse or favorable selection relative to one another. In 2003, the state implemented risk adjustment based on Adjusted Clinical Groups (ACGs), and in 2004 switched to the Chronic Disability Payment System. Florida reduced Diversion Program payment rates after determining that favorable selection resulted in overpayment, and has notified contractors that further reductions may be forthcoming. New York State believes that more study is needed to determine whether its managed long-term care programs are cost effective. Clearly, payment is an area of concern, but states believe that rates can be fine-tuned as better technology is developed. As long as utilization patterns move from higher-cost to lower-cost services (as they appear to be doing in most studies), the total costs of delivering care are probably declining. The challenge becomes one of appropriate pricing, in order to allow both purchasers and suppliers to share in the savings.

Budget predictability is a key attribute. As the baby boomers move into retirement, states are searching for ways to better manage a growing and uncertain liability for future LTC costs. Managed care models allow states to share the risk of budgetary cost increases with its managed care contractors. As the number of people in the long-term care FFS system increases over time, a state's aggregate risk increases.

Quality

Clinical indicators mixed. The ALTCS evaluation concluded that long-stay nursing home care was of lower quality in ALTCS than in the comparison group in New Mexico, based on incidence of decubitus ulcers, fevers and catheter insertions, though the authors note that the need to use another state for comparison was a serious limitation of the study. The MSHO evaluation found that quality indicators for nursing home residents were similar for MSHO and comparison groups, and that in general, MSHO resulted in modest benefit for enrollees compared to control groups.15 The Abt PACE evaluation was very positive, finding improved quality of life, satisfaction and functional status. The study also found that PACE enrollees lived longer and spent more days in the community than members of the comparison group.16 It is important to note that of all the programs mentioned, PACE has the tightest managed care model, including both Medicare and Medicaid and using a staff model to deliver most services.

Satisfaction mostly high. Most of the programs have found consumer satisfaction levels to be high. MSHO, ALTCS and the New York Managed Long Term Care programs all report high overall levels of satisfaction.17, 18, 19 Satisfaction levels in Texas Star+Plus have been slightly lower but still favorable overall, and Star+Plus satisfaction levels have been higher than those of other Texas mandatory managed care programs that do not include long-term care or care coordination.20

Enhanced accountability. State Medicaid officials value being able to hold plans accountable, and being able to work with plans in a systematic way on quality goals, something that is not possible in fee-for-service, where multiple providers are providing care, but none are responsible for overall quality outcomes. In managed long-term care, a negative quality indicator in one year can be turned into a focused quality improvement effort in the next. By comparison, little is known about quality outcomes in the traditional HCBS program.

5. THE FUTURE OF MANAGED LONG-TERM CARE

After a lull in managed long-term care development activities over the last 6-7 years, there appears to be renewed interest among states. The Texas Health and Human Services Commission proposed a large expansion of the Star+Plus program to seven additional metropolitan counties and a request for proposals for bidders was issued in 2004. However, as of April 2005, the Star+Plus expansion was still being debated by the Texas Legislature in the face of strong opposition from hospitals, which claim they will lose significant Medicaid revenue under the plan. If the Star+Plus expansion were to proceed, it alone could double the number of persons enrolled in managed long-term care nationally.

Florida has also received legislative authorization to increase enrollment in its Diversion Program by another 3,000 members in 2004. Minnesota will also be adding a long-term care benefit to its mandatory managed care program for the aged and disabled (PMAP), which will make PMAP similar to the specifications of the MSHO program, except it will not attempt to integrate Medicare. At the same time, Minnesota is considering expansions of the MSHO program into additional counties. The Massachusetts Senior Care Options Program began enrolling members late in 2004 and, as of March 2005 had just under 1000 members. The Maryland state legislature also recently passed legislation for the development of two managed long-term care pilots programs that are under development in 2005. Hawaii is seeking federal waivers to enroll all of its older beneficiaries and persons with physical disabilities into capitated managed care arrangements. Washington state is pursuing two programs that will include managed long-term care in the near future. Thus, we are seeing new states entering the market, as well as significant expansions in states that have successfully implemented managed long-term care programs on a demonstration basis.

Key Issues Affecting Growth

Issues for Purchasers

While there is renewed interest among states in managed long-term care expansions, they face important design decisions in shaping the structure of their managed long-term care programs. The question for states is not only whether to use managed care purchasing models for long-term care benefits, but also what kind of models work best. A number of these design questions are discussed below.

-

Complex policy and design questions. The managed long-term care programs that have been implemented by states and PACE programs are highly diverse. Benefit packages, payment methodologies, target populations, types of managed care suppliers, degree of competition, whether enrollment is voluntary or mandatory, and coordination with Medicare-covered benefits all vary from program to program. True to the nature of Medicaid in general, each state has developed its own model specifications based upon local exigencies. Given this diversity, states do not yet have the benefit of clear, replicable program models to consider. Arizona offers an excellent example. Despite having 15 years of experience managing and improving a statewide program, other states generally do not view the Arizona Long Term Care System (ALTCS) as a transferable model. Since Arizona never had a Medicaid-financed fee-for-service system prior to the implementation of ALTCS, it did not have to deal with the kinds of political issues that other states typically run into during managed long-term care program development. Furthermore, ALTCS still relies heavily on counties as suppliers, an infrastructure that does not exist in most states.

-

Legal authority. Legal authority for managed long-term care programs has evolved in a positive direction from states' perspectives, but difficult issues will continue to complicate program development. Medicaid authority has largely been streamlined through the use of section 1915(a), (b), and (c) waiver authorities, which allow states to meet most of their program objectives without having to go through the far more rigorous requirements of section 1115 demonstration waivers. For states that want to integrate Medicare-covered benefits for dually eligible beneficiaries, negotiations with CMS over special Medicare payments may cease to be an issue if CMS implements the Medicare Frailty Factor for all Medicare Advantage plans in 2007 as has been stated as a goal by CMS. The Frailty Factor has recently been applied to Medicare payments in the PACE, MSHO, MnDHO, Wisconsin Partnership and Massachusetts SCO programs. (The Frailty Factor is not applied to populations under age 55.) Consensus appears to be emerging within these programs that the frailty factor works reasonably well for older beneficiaries with long-term care needs, and that it could become a mainstream alternative to negotiating Medicare rates program by program. However, less likely to be resolved is the issue of whether states can design programs that mandate managed care enrollment for both Medicare and Medicaid. Many states believe mandatory enrollment is necessary to ensure adequate volume and to attract suppliers. Although states can require mandatory enrollment for Medicaid-covered benefits, it is not permitted under current Medicare law.

-

Payment challenges. Payment rates remain a controversial and technically challenging area. States with existing programs consistently identify this as an area in which they expect to make further refinements in the future. At issue is how a state can set a fair price in managed care when the model is expected to change utilization patterns, making the historical FFS data inadequate for setting price. If a supplier successfully provides care more cost-effectively but is paid based on FFS experience, the state may not capture the savings. Alternatively, if a state sets the price too low, it could jeopardize program viability. When Medicare is included, a similar dynamic exists between states and CMS, with each payer concerned that it pays more than its share in an integrated program. One option is to create shared risk arrangements, in which states, CMS and suppliers all agree to share profits or losses in pre-established risk corridors. This issue is fundamentally about how risk should be distributed across purchasers and suppliers.

-

Constituent concerns. Political resistance to managed long-term care from established constituencies in the fee-for-service system has been strong. Some in the aging network have expressed concerns that "private contracting" of the long-term care system will lead to reduced access to services and lower quality of care.

-

Infrastructure Issues. Most states have not made the infrastructure investments needed to implement managed long-term care programs effectively. In managed care, it is particularly important for states to diligently monitor member outcomes, to ensure that managed care contractors are not cutting services and costs inappropriately. Unfortunately, managed care is often viewed by policymakers as a way of privatizing services and reducing state infrastructure. As one state administrator put it, "we are not going to take on a big new complicated program when we're losing staff and are under pressure to find immediate Medicaid savings." Managed long-term care may require states to increase administrative costs. For example, Arizona's AHCCCS program has higher administrative costs, but lower overall costs, than comparable fee-for-service Medicaid programs.

Supply Side Issues

Suppliers of managed long-term care have and will continue to be a diverse group. The type of supplier a state uses will continue to depend on program model, political factors, and availability in the local market.

-

Local provider-sponsored plans. The majority of managed long-term care suppliers are small provider-affiliated plans that have decided to enter the market for local reasons. In the case of PACE, new programs are often initiated by the provider organizations themselves, not in response to state purchasing strategies. In some states, providers have applied political pressure directly to legislatures to ensure a role in a managed care program. In other states, the implementing agency deliberately creates a role for provider-based plans to ensure that traditional infrastructure does not evaporate, to attract an adequate supply or to take advantage of the long-term care expertise in those provider organizations. The challenge is to regulate entities that generally have very little experience managing risk and very little capital to establish reserves. Continued reliance on provider-sponsored plans may result in the market being dominated by many small plans with low enrollments.

-

Start-up plans. There is evidence that venture capitalists are willing to invest in managed long-term care, but new capital will not flow to this market unless investors believe that the level of risk is acceptable, and there are reasonable opportunities for profitability. For this to happen, investors must develop confidence in states as reasonable business partners. Shared risk arrangements may be a useful strategy for attracting new capital to this market. Also, venture capitalists are more interested in developing managed long-term care products that can be more easily replicated across states. Managed long-term care programs that are so state-specific that they cannot be leveraged in other markets will not be as attractive to investors.

-

County plans. The participation of county-based plans in the managed long-term care marketplace is not surprising, given the historical role of county governments in the administration of long-term care and social service programs in some states. The concept of "risk" in county-based models such as the Wisconsin Family Care Program is an odd one though, since it is presumably county taxpayers (or politicians) who are at risk if costs exceed revenues in those plans. While county-based plans appear to be viable suppliers in states with a history of county involvement, their further development remains local by definition and does not increase the number of suppliers who are active on the national market.

-

National firms. Only two companies have entered this market on a national scale--Evercare and Amerigroup, with Evercare having a much larger market presence. Why aren't more managed care companies interested in this product line? First, entry into this market requires a strong commitment to learning the business of long-term care. Managing long-term care is a totally different business from managing general health care, and requires a considerable investment of resources to develop the kind of management expertise needed to be successful. Second, profitability in this market is, at present, fairly unpredictable, given uncertainties about payment rates and the abrupt Medicaid policy changes that can occur, especially during periods of state fiscal stress. Third, there is no assurance that this market will grow to a mature level, given its history to date. We are not likely to see more national companies venturing into this market until there is a significant increase in demand from states.

-

Medicare Advantage plans. Many observers predicted that the managed long-term care market would grow primarily from Medicare managed care plans developing "wrap-around" agreements with states to serve dually eligible beneficiaries. While several Medicare plans have negotiated premium arrangements with states to cover primary and acute cost sharing, none has bid on managed long-term care products. The Medicare Modernization Act now offers a new opportunity in the form of "specialized plans," authorized under the Act to limit enrollment to dually eligible individuals (normal Medicare Advantage rules requires that plans be open to all Medicare beneficiaries.) This provision of the Act provides new opportunities for states to integrate Medicaid and Medicare benefits for long-term care populations, without the extensive use of waivers.

Summary

After over 20 years of development, the Medicaid managed long-term market is still in a very early stage with less than 3% of the potential market enrolled in managed care. Although interest among states in managed long-term care purchasing strategies has been high, they have faced numerous barriers in efforts to implement managed long-term care programs, and many initiatives have been terminated during the development process. However, states which have been successful in implementing managed long-term care programs are pleased with the outcomes they have achieved, and are seeking further program expansions. After a recent lull in managed long-term care program development, it appears that there may be a significant expansion in the market over the next two years. The Medicare Modernization Act also provides states with new opportunities to more easily integrate Medicaid and Medicare-covered benefits for dually eligible populations.

On the supply side, the managed long-term care market is dominated by small provider-sponsored plans with small enrollments that have not, to date, demonstrated intent to expand beyond their current state borders. If the managed long-term care market is to expand to a mature level, it will have to attract more national companies that can operate in multiple states and manage programs with large enrollments.

NOTES

-

See Appendix 1 for an explanation of how Table 1 estimates were derived.

-

Komisar, H.L., Hunt-McCool, J. and Feder, J. "Medicare Spending for Elderly Beneficiaries Who Need Long Term Care." Inquiry 34 (Winter 1997/98): 302-310.

-

Miller, N.A. "Medicaid 2176 Home and Community-Based Care Waivers: The First Ten Years." Health Affairs (Winter 1992): 162-171.

-

Note that there are additional aged and disabled long-term care beneficiaries enrolled in Medicaid acute managed care, but whose long-term care benefits are not included in the managed care benefit package.

-

The National PACE Association reports that, as of 6/1/04, there were 32 fully capitated and certified PACE sites and 8 partially capitated "pre-PACE" sites.

-

These enrollment figures for Wisconsin and Arizona exclude persons with developmental disabilities.

-

Kane, R.L., and Homyak, P. Minnesota Senior Health Options Evaluation Focusing on Utilization, Costs, and Quality of Care. Minneapolis, MN: Division of Health Services Research and Policy, University of Minnesota School of Public Health. Final Version (Revised August 2003). Prepared under HCFA Contract No. 500-96-0008 Task Order 3.

-

Chatterji, P., Burstein, N.R., Kidder, D., and White, A.J. The Impact of PACE on Participant Outcomes. Cambridge, MA: Abt Associates, 1998.

-

APS Healthcare, Inc. Family Care Independent Assessment: An Evaluation of Access, Quality and Cost Effectiveness For Calendar Year 2002. December 2003.

-

Aydede, S.K. The Impact of Care Coordination on the Provision of Health Care Services to Disabled and Chronically Ill Medicaid Enrollees (Texas Star Plus Focus Study). University of Florida, Institute for Child Health Policy, November 2003.

-

Reester, H., Missmar, R., and Tomlinson, A. Recent Growth in Medicaid Home and Community-Based Service Waivers. Prepared by the Health Strategies Consultancy for the Kaiser Commission on Medicaid and the Uninsured. April 2004.

-

McCall, N., Korb, J., Paringer, L., Balaban, D., Wrightson, C.W., Wilkin, J., Wade, A., and Watkins, M. Evaluation of Arizona's Health Care Cost Containment System Demonstration, Second Outcome Report. San Francisco, CA: Laguna Research Associates, 1992.

-

Weissert, W.G., Lesnick, T., Musliner, M., and Foley, K.A. "Cost Savings from Home and Community-Based Services: Arizona's Capitated Medicaid Long-Term Care Program." J. of Health Politics, Policy and Law, 22(6) (December 1997): 1329-57.

-

The Lewin Group. Actuarial Assessment of Medicaid Managed Care Expansion Options. Prepared for the Texas Health and Human Services Commission. January 21, 2004 (amended version).

-

Kane, R.L., Homyak, P., Bershadsky, B., Lum, Y., and Siadaty, M.S. "Outcomes of Managed Care of Dually Eligible Older Persons." The Gerontologist 43(2) (2003): 165-74.

-

Chatterji, P., Burstein, N.R., Kidder, D., and White, A.J. The Impact of PACE on Participant Outcomes. Cambridge, MA: Abt Associates, 1998.

-

Minnesota Health Data Institute. Minnesota Senior Health Options 2002 Consumer Assessment of Health Care: MSHO Nursing Home Population. August 2002. Accessed at http://www.dhs.state.mn.us/HealthCare/pdf/Final-Report-Appendices.pdf.

-

Arizona Health Care Cost Containment System. Arizona Long Term Care System (ALTCS): Consumers Speak Out. 2002. Accessed http://www.ahcccs.state.az.us/Publications/Reports/ALTCSurveyProject/200....

-

NYS Department of Health. New York State Managed Long-Term Care, Interim Report. Report to the Governor and Legislature. 2003.

-

Texas Department of Health. Comparing Medicaid Managed Care Plans in Texas, 2000. Star+Plus Dually Eligible Consumer Study Technical Report. November 28, 2001. Accessed at http://www.hhsc.state.tx.us/medicaid/mc/about/reports/2000annrpts/2000co....

APPENDIX 1: METHOD FOR DERIVING THE SIZE OF THE PUBLIC LONG-TERM CARE MARKET (as presented in Table 1)

Estimates of the potential size of the Medicaid managed long-term care market in FY 2003 are presented in Table 1. The estimates are of the total number of aged and physically disabled Medicaid beneficiaries receiving long-term care services either in nursing homes or in community-based settings, as well as associated Medicaid and Medicare expenditures for these persons. The vast majority of this population is comprised of persons over the age of 65 who are dually eligible for Medicaid and Medicare.

We have excluded from these estimates persons under the age 21 receiving long-term care benefits, as well as persons with developmental disabilities or serious mental illness. About 90% of all Medicaid beneficiaries in nursing homes are over the age of 65. The age distribution of Medicaid beneficiaries receiving community-based HCBS waiver and personal care services is more difficult to estimate, but most likely includes a somewhat higher percentage of non-elderly persons.

In 2003, there were about 3.1 million aged and disabled beneficiaries of Medicaid-financed long-term care services. About 55% of this population received long-term care services in nursing homes, while 45% were receiving long-term care supports in community-based settings, either through the Medicaid home and community-based waiver services program or through the regular state Medicaid option personal care services benefit.