Abstract

Section 2002 of the Affordable Care Act makes the tax concept of Modified Adjusted Gross Income (MAGI) the basis for determining Medicaid and CHIP eligibility for nondisabled, nonelderly individuals, effective January 1, 2014. The Center for Medicare and Medicaid Services State Health Official/State Medicaid Director Letter re Conversion of Net Income Standards to MAGI Equivalent Income Standards, issued on December 28, 2012 (http://www.medicaid.gov/Federal-Policy-Guidance/downloads/SHO12003.pdf) recommended that states and territories adopt the Standardized MAGI Conversion Methodology for converting existing Medicaid and CHIP net income standards to MAGI. This ASPE White Paper summarizes the work that ASPE, CMS, RAND, and SHADAC did to develop the Standardized MAGI Conversion Methodology.

Introduction

The Affordable Care Act extends Medicaid to low-income adults and provides tax credits for coverage through the new Affordable Insurance Exchanges (Exchanges).1 A key component of these coverage expansions is the use of the tax concept of Modified Adjusted Gross Income (MAGI) to assess financial eligibility for Medicaid and the Children’s Health Insurance Program (CHIP) and for applicants for Advanced Premium Tax Credits and Cost Sharing Subsidies in the Exchanges.2 To make the transition to MAGI-based eligibility for Medicaid, states must convert their existing net income standards to equivalent standards based on MAGI. States are required to submit MAGI-based Medicaid eligibility standards to the Department of Health and Human Services (Department) for approval by the Centers for Medicare and Medicaid Services (CMS).

To assist states with this conversion effort, the Department developed the “Standardized MAGI Conversion Methodology” as the recommended option for states to develop their standards. This recommendation was the product of more than a year’s work within the Department and with states, including 10 pilot states, to test the feasibility of potential conversion methodologies. This paper provides an overview of the recommended method, as well as alternative conversion methods considered. The paper is intended to provide insight into the complexity of the conversion process and context for individuals, states, and interested groups seeking to understand how the Department developed the recommended method, and illustrate the analytic challenges encountered by the Department while testing these methods. This paper will also provide additional context for states that are considering proposing alternative conversion methodologies to CMS3 for approval.

The recommended Standardized MAGI Conversion Methodology converts current state net income standards to equivalent MAGI standards by taking the average disregard amount for all individuals within a band consisting of 25 percentage points of FPL below the current net income standard and adding that amount to the current net income standard to produce the MAGI standard. This methodology is also referred to as the “Marginal Disregard Methodology.” However, states may propose and implement other methodologies and processes for MAGI conversion with federal approval. Guidance from the CMS to state health officials on the conversion of net income standards to MAGI equivalent income standards was published on December 28, 2012 (“CMS Guidance”).4 As noted in that guidance, states have flexibility to develop an alternative method. Because states have unique knowledge of their specific circumstances, the Department will consider for approval alternative methodologies that meet the criteria for evaluation that the Department applied in developing its recommended method, as discussed in more detail below.

Key terms

To assist with the discussion of Medicaid eligibility standards and the analytic work behind the Department’s “Standardized MAGI Conversion Methodology,” key terms are defined as follows:

- Gross Income: Gross income is the total of all types of income included under a state’s Medicaid/CHIP definition of income in place on March 23, 2010. Gross income is measured before incorporating disregards and includes income types such as earned income, child support income, and other income as applicable under state rules.

- Disregard: A disregard is a portion of gross income that is not included in net income.5 Within federal statutory and regulatory provisions, each state sets its own rules about what income is disregarded for purposes of Medicaid eligibility. Under pre-Affordable Care Act law, states may choose to disregard a percentage of an individual’s income or certain categories of income, such as child care expenses.

- Net Income: Net income is the income remaining after applicable disregards are subtracted from gross income and any state and eligibility category specific income counting and household composition rules are applied. The definition of net income is guided by federal law but varies by state. Today (that is, before the effective date of the new Medicaid eligibility rules in the Affordable Care Act), Medicaid eligibility is determined by comparing net income to the applicable income eligibility standard.

- MAGI Income: MAGI is the total of all types of income as defined under Section 36B(d)(2) of the Internal Revenue Code of 1986. MAGI income as defined for Medicaid eligibility in the Notice of Proposed Rulemaking (NPRM) published on August 17, 2011, is largely aligned with although not exactly the same as the tax code definition of MAGI.6 The definition of MAGI does not vary by state. Effective January 1, 2014, Medicaid eligibility for most groups of individuals will be determined by comparing MAGI-based income to the applicable income eligibility standard. As noted in Footnote 11 below, the Department’s analysis of conversion methodologies focused primarily on the household composition and income counting rules of MAGI.

- Income Counting: Under the Medicaid rules in effect prior to January 2014, certain types of income are included, or counted, for purposes of determining eligibility for coverage and benefits. Examples of types of countable income include earned income, child support, workers’ compensation, and other income sources.

- Household Composition: Both current Medicaid rules and new MAGI-based rules use the concept of a household unit to determine whose income within the household must be counted toward the applicant’s or beneficiary’s income. However, the current rules and new rules have different definitions of household. Current Medicaid rules generally prohibit counting income from anyone other than the person seeking coverage or an individual who is legally responsible for that person (such as a parent or spouse). Under MAGI, a “household” generally includes the primary tax payer and his or her tax dependents (e.g., children), and “household income” is defined as the sum of the MAGI of the primary taxpayer and of each dependent who is required to file a tax return for income tax purposes.

- Net Income Standard: The net income standard is the income eligibility standard for Medicaid and CHIP eligibility under the eligibility rules in effect prior to MAGI conversion. This varies by state and eligibility group. As used in this paper, this term has the same meaning as pre-MAGI Medicaid standard or pre-ACA Medicaid standard.

- Converted Standard: The converted standard is the new eligibility standard that results from adjusting for the MAGI definition of income mandated by the Affordable Care Act. As used in this paper, this term means the new standard resulting from application of the conversion methodology.

- SIPP Data: The Survey of Income and Program Participation (SIPP) is administered by the US Census Bureau and provides information on cash and non-cash income types, household composition, familial relationships, and other administrative and enrollment variables relevant to implementation of MAGI conversion.

- State Data: These data are extracted from the eligibility systems of states and territories. State data generally include information about applicants or enrollees that is needed to make a Medicaid eligibility determination. State data vary widely because they are based on the unique eligibility rules and system designs of each state.

- Federal Poverty Level (FPL): This document uses FPL as a shorthand to refer to the federal poverty guidelines issued by the Department.7 For many eligibility groups, states set a net income standard based on a certain FPL. For example, in Arizona, children under age 1 whose household income does not exceed 140% of FPL are eligible for Medicaid.

Background

Pre-MAGI Medicaid and CHIP financial eligibility standards vary among states and territories. Currently, subject to federal standards, states set their own rules with respect to income and the level of assets that qualify applicants for Medicaid. As part of this flexibility, states can determine sources and amounts of income that are counted when determining an individual’s financial eligibility for Medicaid or CHIP. The resulting net income is compared to an income eligibility standard (the “net income standard”) to determine eligibility for Medicaid or CHIP.

Under the law in effect prior to January 2014, states and territories may deduct or “disregard” from gross income certain amounts of earnings, and child support received, as well as other types of income, and they may adopt additional disregards at their discretion, when determining income for Medicaid and CHIP financial eligibility. Disregards vary by state, eligibility category, and income source. For example, when counting income for parents and children, states typically disregard $90 of earnings per worker in a household and disregard at least $50 in child support payments received.8

In addition to income disregards, states may also deduct certain expenses from counted income and may augment these deductions. In the case of determining eligibility for parents and children, states commonly deduct between $175 and $200 of monthly child care expenses (based on the age of the child) from counted income.

State net income eligibility standards and methodologies for determining Medicaid and CHIP income eligibility vary widely, primarily due to differences in the application of income disregards. In part because each state currently has considerable discretion to define its disregard rules, an individual financially qualifying for Medicaid in one state would not necessarily qualify for Medicaid in another state, even if the two states had the same net income standard, because of differences in state disregards.

Section 2002 of the Affordable Care Act requires states, beginning in 2014, to determine income eligibility for CHIP and for most nonelderly, nondisabled Medicaid beneficiaries by using Modified Adjusted Gross Income (MAGI) as the basis for determining income. As explained more fully in the CMS Guidance, the primary objective in establishing a methodology to convert from the current net income standard for a particular state and eligibility group to the converted standard for the same state and eligibility group is to produce no change in aggregate eligibility, though some individuals might gain or lose eligibility, or move from one eligibility group to another. The conversion process should not systematically increase or decrease eligibility overall.

Section I: Methods Considered by the Department for Income Conversion

The Department evaluated a number of potential conversion methodologies. To inform this evaluation, it consulted with states, solicited public comments through a request for information (“Solicitation”) in June 2012, and worked with 10 pilot states to test the feasibility of potential conversion methodologies, including analyzing the impacts of proposed methodologies using state data. The Department used the following criteria to assess the proposed methods for income conversion:

- Unbiased: Across all eligibility categories, the method does not systematically increase or decrease the number of eligible individuals within a given eligibility group or systematically increase or decrease the costs to states.

- Accuracy: To the extent possible, the method minimizes changes in eligibility status by minimizing losses and gains in eligibility for a given category of coverage.

- Precision: The converted standard must be stable and repeatable. In other words, if the methodology to arrive at the converted standard were repeated, it would arrive at the same result. For example, if a sampling methodology is used, the sample size must be large enough to ensure that the conversion method, if calculated on another sample, would in general yield the same converted standard.

- Data Quality: The data used to conduct the conversion method are representative of the income and disregards of the population so as not to bias the converted standard due to poor data quality.

- Administrative Burden: The method minimizes demands on state administrative resources and capacity.

The Department evaluated two broad categories of methodologies: “Disregard Methods” and “Disregard combined with Household Composition/Income Counting Methods” (“Disregard/HCIC Methods”). There are three potential components of a MAGI-based conversion: disregards; household composition; and income counting. Disregard Methods establish converted standards incorporating the effects of disregards only. Disregard/HCIC Methods attempt to account for differences in household composition and income counting rules as well as disregards. Each category has three methods, listed below:

Disregard Methods:

- Same Number Net and Gross (SNNG)

- Average Disregard Method (ADM)

- Marginal Disregard Method (MDM/25)

Disregard/HCIC Methods:

- Same Number Net and MAGI (SNNM)

- Average Difference

- Marginal Difference

As discussed below, the Department’s analysis led to a recommendation of the Marginal Disregard Methodology as the Standardized Conversion Methodology with the margin defined as 25 percentage points below the existing net income Medicaid standard for each eligibility category in a state.

The Department used both survey data and state administrative data in developing and analyzing the methods.

The survey data came from the Survey of Income and Program Participation (SIPP), conducted by the Census Bureau.9 The SIPP was selected because it contains data on monthly (rather than annual) income. It also has the level of detail needed to distinguish income sources that may be treated in different ways and to model certain disregards currently available for a given state and eligibility group. The SIPP provides detailed data on characteristics such as age and family relationships that are needed to place respondents in the appropriate eligibility categories. SIPP data for development of the MAGI methodologies came primarily from the April 2010 Cross Section of the 2008 panel. As in any longitudinal survey, individuals move in and out of the sample depending on whether they complete the questionnaire in a particular month.

A limitation of the SIPP is that sample sizes are roughly proportional to state populations, and therefore can be fairly small for smaller states. Considering that many SIPP respondents are above the Medicaid or CHIP income standards, or age 65 and older, the effective number of cases available for the conversion analyses in a particular state from that state’s respondents will be even smaller. Moreover, although state identifiers are available in the public-use data, the survey is not designed to be representative of the low-income population at the state level.

In order to improve the accuracy of the state-specific analyses, the Department reweighted the SIPP data. In essence, the full national sample is made to resemble any given state by placing more or less weight on each individual in the sample in proportion to the extent that the state differs from the nation. For example, in a relatively low-income state, low-income individuals in the national sample will be given more weight.

For more information on the preparation and use of SIPP data for income conversion see the HHS document “Data Sources for Modified Adjusted Gross Income (MAGI) Conversions” available at http://aspe.hhs.gov/health/reports/2013/sipp/ib.cfm.

State administrative data on Medicaid and CHIP enrollees were provided by pilot states that agreed to serve as partners with the Department in the development of MAGI methods.10 The Department tested the methods using the most complete data available at the time from the pilot states.

Finally, whether based on SIPP data or state data, all tables, numbers, and thresholds contained in this paper are illustrative. They should not be interpreted to represent the actual threshold that will apply for any state or eligibility category. All states, including the 10 pilot states, have the option of choosing either the Standardized MAGI Conversion Methodology or an alternative method that is approved by CMS. In addition, the tables and numbers in this paper do not reflect the final weighting of the SIPP that will be used to calculate converted thresholds. While the final converted numbers and thresholds may therefore differ from those in this paper, the methodology used for the calculations will not change. It is the Standardized MAGI Conversion Methodology as defined below.

Section II: Disregard Methods

This section of the paper summarizes the Department’s analysis of the potential methods to reflect varying state disregards, and the reasons for its selection of the Standardized MAGI Conversion Methodology. The Disregard Methods convert a state’s current Medicaid net income standard to an equivalent standard that accounts for disregards. The Department evaluated three types of Disregard Methods: the Same Number Net and Gross Method, the Average Disregard Method, and the Marginal Disregard Method.

Same Number Net and Gross: The Same Number Net and Gross (SNNG) Method uses the assumption that the new converted standard is based only on gross income, defined as net income plus disregards. (However, in 2014, the rules for assessing eligibility will account for other adjustments besides disregards; therefore, this method does not actually achieve the goal of establishing a standard where the same number of people are eligible in 2014 as were eligible under the existing standard.) Under the SNNG method, the converted income standard is set so that the same number of people are eligible under a gross income standard, as defined above, as would be eligible under the existing net income standard. This method uses SIPP data to estimate the number of individuals eligible in a particular state and category according to the current income eligibility rules. All individuals in that state and category are then ranked from lowest to highest gross income, which is defined as the sum of net income plus disregards, and the converted standard is set at the point at which the number of individuals eligible based on gross income is equal to the number eligible under the existing rules. This method is illustrated in the text box on the following page.

SNNG Example (Tables A and B)

The example relates to a specific eligibility category within a state. Under March 23, 2010 eligibility rules, 3 individuals in a group of 6 individuals are eligible for Medicaid: Person 1, Person 2, and Person 3 (see Table 1). When the gross income is ranked from lowest to highest and the new converted standard is drawn, 3 individuals are still eligible. However, these are not the same 3 individuals who were eligible under the net income standard (see Table 2).

Eligibility Using State-Eligibility Category Specific Net Income Standard on March 23, 2010 | ||

|---|---|---|

Individual | % FPL using Net Income | Eligible under net income standard of 100% FPL? |

Person 1 | 70% | Yes |

Person 2 | 85% | Yes |

Person 3 | 90% | Yes |

Person 4 | 110% | No |

Person 5 | 120% | No |

Person 2 | 130% | No |

Eligibility Using State-Eligibility Category Specific Converted Gross Standard | |||

|---|---|---|---|

Individual | % FPL using Net Income | %FPL using Gross Income | Eligible under converted income standard of 110% |

Person 1 | 70% | 90% | Yes |

Person 2 | 85% | 105% | Yes |

Person 4 | 110% | 110% | Yes |

Person 3 | 90% | 120% | No |

Person 5 | 120% | 130% | No |

Person 6 | 130% | 150% | No |

In this example, the converted standard would be 110% FPL. The bolded observations in Table 2 represent individuals who changed eligibility status. This method can only be implemented with SIPP data because state administrative data include information only about individuals who apply and/or are enrolled in Medicaid.

The SNNG method does not ensure that the exact same individuals retain eligibility, but aims to ensure that the same number, in the aggregate, would be eligible if gross income were used to assess eligibility. For example, Person 4 gains eligibility under the converted standard of 110% FPL based on gross income, but was not eligible under the net income standard of 100% FPL. Because his income level does not change in this example, whether it is calculated as net income or gross income, Person 4 had no disregards. However, Person 3 loses eligibility under the converted standard because his gross income exceeds 110%, whereas his net income of 90% made him eligible under the net income standard of 100%. This implies that Person 3 has disregards that affect his eligibility. Under the converted standard, Person 4 gains eligibility while Person 3 loses eligibility, but they balance each other in the aggregate.

The SNNG Method has three important limitations:

- The method can only be used with SIPP data. It cannot be used with state administrative data because state data do not provide any information on individuals who are not enrolled in Medicaid or CHIP.

- The accuracy of the SNNG Method is heavily dependent on the accuracy of the eligibility simulations on which it is based. While this is true to some extent for all the methods the Department analyzed, it is truer for the SNNG Method. The SNNG approach depends on accurately approximating more target numbers than the other methods. In addition, there are not good benchmarks for setting many of these targets. Appendix 3 describes in detail the difference between SNNG and the Department’s recommended Standardized MAGI Conversion Methodology.

- The SNNG only accounts for disregards and does not address the impact of adjustments for other MAGI rules, such as household composition and income counting. Because eligibility in 2014 will be determined using these other MAGI rules, SNNG does not set the converted standard at the point where the same number who are eligible under current rules will be eligible under 2014 rules.

Average Disregard Method: The Average Disregard Method (ADM) takes the value of disregards assigned to each individual, converts this disregard across all individuals to a percentage of the FPL (where the FPL is determined based on household size), sums up the individual’s disregards expressed as a percent of FPL, and then divides this number by the total number of eligibles or enrollees in that state and eligibility category. This method can be implemented using either SIPP or state data. If SIPP data are used, eligible individuals are evaluated. If state data are used, enrolled individuals are evaluated.

ADM Example

The current net income standard for a specific eligibility group is 100% FPL. Among a group of eligible (or enrolled) individuals, the average value of the disregards is 3% of the FPL. The converted standard is 100% + 3% = 103% FPL.

The ADM has two strengths: First, it adjusts for disregards, which are a major component underlying the difference between current net income standards and MAGI-based standards. Second, it can be implemented using either SIPP or state data, at the option of the state. Moreover, for the eligibility categories examined, the ADM produced eligibility standards that were generally consistent with the results produced by other methods. (See Table 5 below, summarizing the income standards resulting from each method for various eligibility categories.)

However, the Department concluded that the ADM is likely to produce a systematically biased result in which, on average, more people lose eligibility than gain eligibility as a result of the conversion. This bias exists because, as shown below, there is a systematic relationship between the average size of the disregard and net income. People with higher levels of net income have, on average, higher disregards. In contrast, the amount of the disregard is irrelevant for most people with low levels of net income. They will be eligible regardless of the size of the disregard. The people for whom the size of the disregard is most likely to affect eligibility are the people whose income is a bit above the net standard. Because, as shown below, average disregards are greater for these people than for those with lower levels of net income, the average disregard method systematically estimates a lower average disregard than a method that captures disregards for those on the “margin,” and causes the converted threshold to be biased downwards from the level needed to be unbiased.

The income disregard amounts for individuals whose income is within a relatively small margin of the eligibility standard may be higher than the income disregard amounts for individuals whose income is well below the eligibility standard, for at least two reasons:

- Certain income disregards, such as child care expenses and work expenses, are only available for individuals with earned income.

- States do not always collect complete disregard information for all individuals. When states are assessing eligibility for individuals whose income is significantly below the net income standard, states have little or no reason to collect full disregard information. The applicant’s income is low enough to meet the eligibility standard regardless of whether he or she has applicable disregards. While not collecting complete information reduces both the state’s administrative burden and the burden on applicants, it results in a potentially biased converted standard if the average disregard method is used.

For these reasons, the Department refined the Average Disregard Method by examining bands of income and taking the average disregard only for individuals for whom disregards affect eligibility.

Marginal Disregard Method (selected as the Department’s recommended method): The Department tested the hypothesis that disregards are positively correlated with income and confirmed that a positive correlation exists. As shown in Appendix 1, there is a correlation between level of income and level of disregards. Higher income individuals tend to have higher disregards. Therefore, the Department concluded that the conversion methodology should focus on those individuals for whom disregards are most likely to affect their Medicaid eligibility. These are the individuals whose net income falls just at or below the current Medicaid eligibility standard. It is this group for which the amount of their disregards is most important in determining whether they are eligible.

This refinement of the Average Disregard Methodology is called the Marginal Disregard Method (MDM). It is similar to the Average Disregard Method in that disregards are expressed as a percentage of FPL and are totaled and divided by the number of enrollees (if state data is used) or eligibles (if SIPP data is used). The difference between the methods is that, for the Marginal Disregard Method, this calculation is performed only for a subset of enrollees or eligibles. The Marginal Disregard Method, like the Average Disregard Method (and unlike the SNNG Method), can be used with either state or SIPP data.

MDM/25 Example

Assume the current net income standard is 100% FPL. Using SIPP data and analyzing only those individuals with net incomes between 75% and 100% FPL, the average amount of disregarded income is 10% FPL. This results in a converted standard of 110% FPL.

Selecting a Marginal Income Band: The Department used two criteria to select an appropriate income band:

- The income band should reasonably capture individuals whose eligibility is affected by disregards.

- The population, or sample size included in the income band, should be large enough to precisely measure the average. In other words, the sample size used to compute the “marginal” average should be large enough that the converted standard is valid and reliable.

The Department analyzed the average size of disregards to understand how many individuals have disregards that could affect eligibility and to determine the marginal band size that would produce the most precise converted standard.

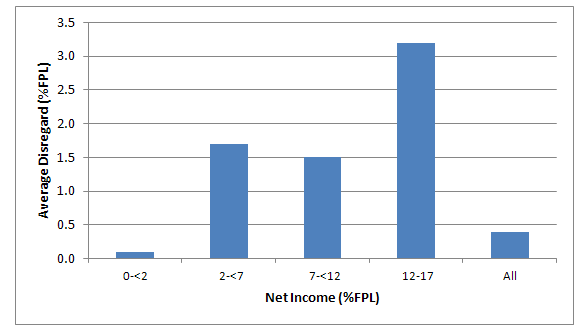

Table 1 shows the percentile distribution of individuals’ disregards for a sample of 16 eligibility categories from the pilot states. For each eligibility category, at least 5% of individuals have no disregards, and for all states and eligibility categories shown, except for Nebraska CHIP children, at least 25% have no disregards. For 12 of the 16 categories, at least 50% of the individuals have no disregards. This shows that within most eligibility categories, disregards do not affect eligibility for at least 50% of individuals.

For example, the first category shown in Table 1 is Arizona children less than age one. Of the 490 observations in this category, more than 245 (the 50th percentile) have zero disregards. The disregard for the 367th observation (the 75th percentile) is 5.9% of FPL. The disregard for the 441stobservation (the 90th percentile) is 7.4% of FPL. In summary, Table 1 shows that very few individuals have disregards, and of those who do, the size of the disregard is less than 25% of FPL for almost all observations.

Category | Number of Observations | Min. | 1st pctl. | 5th pctl. | 10th pctl. | 25th pctl. | Mean | 50th pctl. | 75th pctl. | 90th pctl. | 95th pctl. | 99th pctl. | Max. |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

AZ: Children < 1 | 490 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 3.1 | 0.0 | 5.9 | 7.4 | 9.8 | 19.0 | 40.4 |

AZ: Children 1-5 | 2879 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 3.2 | 3.3 | 4.9 | 8.0 | 9.8 | 14.8 | 40.4 |

AZ: Children 6-18 | 5684 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 3.0 | 0.0 | 4.9 | 8.4 | 10.7 | 15.1 | 44.5 |

AZ: Parents | 4171 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 3.0 | 0.0 | 4.9 | 8.4 | 11.5 | 17.4 | 44.5 |

AZ: CHIP | 1881 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

NE: Children < 1 | 500 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 3.7 | 0.0 | 6.6 | 9.3 | 10.9 | 22.7 | 41.2 |

NE: Children 1-5 | 2831 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 3.7 | 3.6 | 6.6 | 8.2 | 10.9 | 16.5 | 80.3 |

NE: Children 6-18 | 5248 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 3.2 | 0.0 | 5.4 | 9.3 | 11.1 | 16.5 | 80.3 |

NE: Parents | 2430 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.8 | 0.0 | 0.0 | 6.6 | 9.3 | 16.5 | 49.4 |

NE: CHIP | 2085 | 0.0 | 0.0 | 0.0 | 2.9 | 5.4 | 7.4 | 6.6 | 9.3 | 13.1 | 14.0 | 19.7 | 70.0 |

NY: Children < 1 | 575 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 3.1 | 3.3 | 4.9 | 7.4 | 8.8 | 15.7 | 40.4 |

NY: Children 1-5 | 2812 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 3.2 | 0.0 | 4.9 | 7.4 | 10.3 | 17.4 | 79.6 |

NY: Children 6-18 | 6294 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 2.9 | 0.0 | 4.9 | 7.4 | 10.3 | 15.7 | 79.6 |

NY: Parents | 5633 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.5 | 0.0 | 0.0 | 5.9 | 7.4 | 15.7 | 61.6 |

NY: CHIP | 2395 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

WV: Parents | 1616 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.4 | 0.0 | 0.0 | 0.0 | 3.9 | 9.8 | 39.3 |

Source: Analysis of SIPP Data | |||||||||||||

The Department chose the marginal band of 25 percentage points of FPL for two primary reasons:

- For all eligibility categories examined, most individuals have disregards of less than 25 percentage points of FPL.

- A band of 25 percentage points creates a large enough sample of individuals for the converted standard to be stable.

Because at least 99% of individuals have disregards less than 25 percentage points of FPL, the marginal band should capture virtually everyone who could be made eligible by disregards. In addition, because the SIPP is a sample of individuals, further reducing the number of individuals used for conversion could adversely affect the stability of the conversion pools.

The Department considered using a band smaller than 25 percentage points of FPL. However, as shown in Tables 4A, 4B, 4C, 4D, 4E, and 4F in Appendix 4, within the 25% band, there is no systematic relationship between net income and the size of the disregard. That is, people with income within 5 percentage points of the income standard do not have larger disregards than the average person within the 25% band. Therefore, a band of 25 percentage points is broad enough to ensure that it captures virtually all of those for whom disregards matter, while a smaller band might have omitted some of them. Also, as noted above, a broader band creates a large enough sample to ensure that the converted standard is stable.

The Department concluded that the Marginal Disregard Method with a band of 25 percentage points of FPL (MDM/25) results in a converted income standard that is not systematically biased and that focuses on those individuals for whom disregards matter. For these reasons, the Department recommended this method as the “Standardized MAGI Conversion Method” in the December 28, 2012 CMS Guidance. As noted in the CMS Guidance, the preferred method can be used with either SIPP data or state administrative Medicaid and CHIP data. States can choose which data they prefer to use. States may also suggest an alternative methodology, entitled “State Proposal Option.”

Section III: Methods that Account for Disregards Combined with Household Composition and Income Counting (HCIC) Methods

The Department also considered a number of methods that adjust for the income counting and household composition differences between MAGI and gross income. Key Disregard/HCIC methods examined were:

- Same Number Net and MAGI (SNNM)

- Average Difference

- Marginal Difference

For each of these methods, the analytic approach is similar to that of the disregard only method, with the following exceptions:

Same Number Net and MAGI (SNNM) versus Same Number Net and Gross (SNNG): Similar to the SNNG method, the SNNM method begins by estimating the number of individuals eligible in a particular state and category according to current income eligibility rules. Then all individuals who fit into that eligibility category (using non-income criteria) are ranked from lowest to highest MAGI income. The converted standard is set at the point at which the number of individuals eligible based on MAGI income is equal to the number of eligibles under the existing rules.

Average Difference versus Average Disregard: The Average Difference Method takes the difference between MAGI income (calculated by accounting for household composition and income counting rules, as well as disregards)11 and net income for all eligible or enrolled individuals, and adds this average to the existing net income standard. The method differs from the Average Disregard Method because the value added to the net standard is based on the difference between MAGI income (calculated as specified above) and net income, as opposed to the difference between gross and net income.

Marginal Difference versus Marginal Disregard: Similar to the Marginal Disregard Method, the Marginal Difference Method computes the average disregard for individuals within an income band of 25 percentage points below the existing net standard and adds this average disregard to the existing net standard. In addition, this method incorporates a mean-based adjustment for the average difference between MAGI income and gross income. In contrast, the Marginal Disregard Method does not include an adjustment for the mean difference between MAGI and gross income.

After analysis of these methods, the Department decided not to incorporate an adjustment for MAGI income counting and household composition rules in its preferred methodology. There were three main reasons for this decision:

- Little or no change in income: While the household composition and income counting rules that will be used in January 2014 to determine Medicaid eligibility differ from current Medicaid rules, the analysis shows that gross income and MAGI income are the same for approximately 80% of low-income individuals.

- Confidence Intervals: The confidence intervals around the estimated adjustments for household composition and income counting are, for many states and eligibility categories, large enough that we cannot be confident the adjustment is significantly different from zero. In other words, for many categories, the adjustment for household composition and income counting should be zero, meaning that there is no difference between the converted standard using disregards only and the standard that also adjusts for household composition and income counting.

- Accounting for Young Adults: In some cases where it appears that the adjustments might make a difference, the results are extremely sensitive to assumptions about whether adult children will be claimed as tax dependents by their parents, and there are no reliable data to inform estimates about how many adult children are likely to be claimed. See Appendix 2 for additional discussion of the impact of MAGI household composition and income counting rules on income.

Another complication in adjusting the conversion methodology for MAGI rules regarding income counting and household composition is that such a methodology cannot be done using state data only. Many state Medicaid and CHIP agencies do not collect or retain information on income that can be disaggregated into the components of MAGI, nor do they collect data on people who are not included in the household under current rules. Therefore the Disregard/HCIC Methods can either be applied using SIPP data for all components, or taking a hybrid approach that uses state data for the disregard component, and SIPP data for the income counting and household composition components. The Department preferred to recommend as the Standardized Methodology a method that could be applied using only state data, if a state so chose.

We provide the supporting analysis for each of these three points below.

1. Little or no change in income

Table 2 below uses SIPP data to demonstrate the percentage of individuals whose income is affected by MAGI rules. In all 16 categories examined, more people experience a decrease in income when applying the MAGI rules (see Column 1) than an increase in income (see Column 3). However, depending on the eligibility category, 73 - 83% of individuals experience no change in income due to income counting and household composition rules (see Column 2). A category-wide adjustment based on the mean change would affect all individuals in the category. Because approximately 80% of the people in each category experience no change, the decision to include no adjustment for household composition and income counting rules better reflects the overall experience of the target population of each eligibility category.

State | Eligibility Group | Negative Change MAGI < Net (% of people) (1) | No Change MAGI = Net (% of people) (2) | Positive Change MAGI > Net (% of people) | Average Change (% of FPL) (4) |

|---|---|---|---|---|---|

Children under 1 | 15.9 | 78.4 | 5.7 | 2.29 | |

Children 1-5 | 15.4 | 79.6 | 4.9 | 3.15 | |

Children 6-18 | 14.6 | 73 | 12.4 | 15.56 | |

Parents | 16.7 | 79.6 | 3.7 | -0.07 | |

Arizona | CHIP | 16.4 | 78.4 | 5.2 | -0.33 |

Children under 1 | 19 | 78.3 | 2.7 | -1.17 | |

Children 1-5 | 18.7 | 79.8 | 1.5 | -2.97 | |

Children 6 -18 | 21.3 | 73.7 | 5 | -1.49 | |

Parents | 21.3 | 75.2 | 3.5 | -0.19 | |

Nebraska | CHIP | 22.8 | 73.9 | 3.3 | -4.94 |

Children under 1 | 18 | 79.6 | 2.3 | -2.04 | |

Children 1-5 | 18.5 | 80.2 | 1.4 | -2.87 | |

Children 6-18 | 21.3 | 75 | 3.7 | -2.61 | |

Parents | 18.7 | 77.6 | 3.7 | -0.98 | |

New York | CHIP | 20.8 | 75.4 | 3.8 | -4.19 |

West Virginia | Parents | 14.6 | 83.1 | 2.3 | 0.54 |

Source: Analysis of SIPP data. | |||||

2. Confidence Intervals

Table 3 below shows the average difference between MAGI and gross income with 95% confidence intervals for 22 eligibility categories. A negative mean indicates that on average, MAGI income is lower than gross income; similarly, a positive mean indicates that on average, MAGI income is higher than gross income.

Table 3: Confidence Intervals (Note: The numbers for pregnant women assume that pregnant women are “not claimed” as tax dependents under MAGI.)

For 14 of the 22 eligibility categories, the confidence intervals around the mean encompass 0, meaning we cannot determine if MAGI income is significantly different from gross income.

For 1 of the remaining 8 eligibility categories (Arizona Children 6-18), the mean is positive, indicating an adjustment for household composition and income counting rules would increase the converted standard.

For the 7 remaining eligibility categories, the average is negative, indicating that a mean-based adjustment for household composition and income counting rules would decrease the converted standard. While the adjustment would be negative, the data in Table 4 show, for example, that among children’s groups with a significant negative adjustment, the overwhelming majority of children (close to 80%) experience either no change in income, or a positive change. In fact, given these underlying trends in the data, it is not surprising that a median-based adjustment for MAGI rules would have been 0 for each eligibility category analyzed in Table 4.12

Another trend apparent in these data is that of the categories with a significant MAGI change, 6 of the 8 categories were children’s groups. For 5 of the 6 children’s groups the MAGI adjustment was negative, meaning a MAGI adjustment could lower the converted standard. Adjusting the converted standard downward for children’s groups is inconsistent with the intent of the statute, where children’s groups are specifically protected:

“The Secretary shall ensure that the income eligibility thresholds proposed to be established using modified adjusted gross income and household income, …and the methodologies and procedures proposed to be used to determine income eligibility, will not result in children who would have been eligible for medical assistance under the State plan or under a waiver of the plan on the date of enactment of the Patient Protection and Affordable Care Act no longer being eligible for such assistance.”13

Given that approximately 80% of children do not have a negative difference between MAGI income and gross income, a decision to adjust the converted standard for MAGI rules seems inconsistent with this section of the statute. In the most extreme case, a downward adjustment for MAGI would lead to a converted standard that is lower than a state’s existing net income standard. This result is observed for the New York CHIP group.

Overall, household composition and income counting rules appear to affect less than one quarter of the eligible population. Both the direction and magnitude of these changes are variable. As such, a single adjustment for household composition and income counting rules at the eligibility category level does not accurately represent the income changes experienced by most people.

3. Accounting for Young Adults

Accounting for the impact of the presence of young adults on a household’s size and income poses particular challenges. A methodology adjusting for young adults in the size and income of the household must rely on assumptions for which there are no data. Two groups raise particular problems: students and young pregnant women.

Under current Medicaid eligibility rules, a parent’s income counts in determining the eligibility of 19 and 20 year-olds, even if the 19 or 20 year-old is not considered part of the parent’s household or tax unit. For a young adult age 21 or older, the parent’s income is not counted for determining the young adult’s eligibility, even if the young adult lives with one or both parents. Moreover, the young adult’s household size, which affects the Federal Poverty Level applied for determining eligibility, does not include the parents. Similarly, for pregnant women under age 21, the parent’s income counts for determining eligibility, unless the state explicitly allows a disregard of parental income for pregnant minors under 21.

Under MAGI-based rules, however, individuals from age 19 up to (but not including) age 24 can be claimed as qualifying children if they are students, live at home for half the year, and have not provided more than half of their own support. Older children can be claimed as qualifying relatives if they have income under $3800 per year and the parent provides at least half of their support.14 If a parent claims a young adult, the parent will be counted in determining the young adult’s household size, and the parent’s income will be counted for determining the young adult’s Medicaid eligibility.

Parental claiming of young adults for tax reasons, therefore, may lead to young adults not qualifying for Medicaid under MAGI-based rules, even though they qualified for Medicaid under current rules. Excluding young adults from their parents’ household always lowers income for these young adults, but the effects of exclusion on the eligibility of other family members can vary. Adding a young adult to the family unit increases family size, which increases eligibility if the young adult brings no income to the family unit. However, if the young adult has earnings, the additional income may make the household ineligible.

Estimates of the number of young adults who will be eligible for Medicaid in 2014 are extremely sensitive to assumptions about whether the young adults will be claimed as tax dependents by their parents. However, the Department is unaware of any method to reliably estimate the extent to which these young adults will be claimed. As a result, any adjustment for household composition is likely to introduce substantial error into the conversion process.

Because of the lack of data to support assumptions that are necessary to adjust a conversion methodology for the MAGI-based rules affecting household composition and income counting, as well as the likelihood of introducing error into the process, the Department decided against recommending any methodology that included such adjustments.

The Department’s decision to recommend the Marginal Disregard Method, with the margin defined as a band of 25 percentage points of FPL at or below the current net income standard, is supported by the data in Tables 4 and 5 below. 15

Impact of Methodologies on Converted Standards: Table 4 provides a comparison of the converted standards resulting from each of the six methods previously discussed. For most of the 19 eligibility categories analyzed, the six converted standards are all within a range of 10 percentage points. In a few cases, the range is much larger, while in others this range is much narrower, closer to five percentage points.

A few trends merit particular attention. First, based on analysis of a limited number of eligibility categories and states, the Marginal Disregard Method (MDM/25) with SIPP data is rarely more than 10 FPL percentage points removed from the original net standard.

Second, in 15 of the 19 eligibility categories in Table 4, the converted standards produced using the MDM/25 with SIPP data (column 2) are within five percentage points of the standard computed using the SNNM method (column 5). The difference between these two methods is close to 11 percentage points for one of the remaining categories, and much larger for the three categories with the largest differences.

The information used to rank individuals under the SNNM method (an individual’s net income and MAGI income) is the person-level information that is also used to assess the number of individuals gaining eligibility, the number losing eligibility, and the net change in eligibility reported in Table 5 (Comparison of Methods on Income Standards and Eligibility Categories). Therefore, when the SNNM and MDM/25 methods produce similar converted standards, we would expect to observe a small net change in eligibility. When the methods produce converted standards that are more varied, we would expect a larger net change in eligibility. Even in the cases where the difference between these two methods is larger than five percentage points, the overall impact on eligibility is limited.

Finally, Table 4 shows that converted standards using the SIPP sample are similar to the converted standards using state data.16

| Net Income Standard | MDM 25 (SIPP Data) | MDM 25 –(State Data) | Same Number Net and Gross | Same Number Net and MAGI | MDM 25 – Full MAGI | Average Disregard Method | |

|---|---|---|---|---|---|---|---|

| Arizona: Kids <1 | 140 | 147.55 | . | 150.07 | 150.07 | 146.74 | 143.12 |

| Arizona: Kids 1-5 | 133 | 139.38 | . | 140.42 | 142.7 | 140.76 | 136.22 |

| Arizona: Kids 6-18 | 100 | 105.79 | . | 106.17 | 116.38 | 113.88 | 103.02 |

| Arizona: CHIP | 200 | 200 | . | 200 | 200.98 | 198.48 | 200 |

| Arizona: Parents | 100 | 105.56 | 106.3 | 105.77 | 103.74 | 102.66 | 104.89 |

| Arizona: Pregnant | 150 | 159.66 | 157.58 | 105.85 | 132.69 | 153.92 | |

| Nebraska: Kids <1 | 150 | 158.33 | 162.1 | 159.58 | 156.64 | 154.37 | 153.7 |

| Nebraska: Kids 1-5 | 133 | 139.79 | 145.3 | 141.25 | 137.61 | 134.85 | 136.69 |

| Nebraska: Kids 6-18 | 100 | 105.94 | 108.7 | 106.95 | 101.73 | 101.01 | 103.22 |

| Nebraska: CHIP | 200 | 208.17 | . | 209.23 | 203.8 | 201.87 | 207.41 |

| Nebraska: Parents | 50.3 | 55.41 | . | 54.41 | 50.74 | 49.88 | 55.92 |

| Nebraska: Pregnant | 185 | 196.31 | 199.1 | 199.75 | 163.96 | 180.24 | 191.32 |

| New York: Kids <1 | 200 | 206.47 | . | 206.96 | 206.96 | 200.84 | 203.14 |

| New York: Kids 1-5 | 133 | 138.64 | . | 139.69 | 136.5 | 134.1 | 136.18 |

| New York: Kids 6-18 | 133 | 138.21 | . | 138.85 | 134.82 | 132.05 | 135.87 |

| New York: CHIP | 400 | 400 | . | 399.67 | 396.1 | 392.25 | 400 |

| New York: Parent | 87 | 86.92 | . | 87.31 | 85.44 | 83.53 | 88 |

| New York: Pregnant | 200 | 206.66 | 205.98 | 156.59 | 195.94 | 204.05 | |

| West Virginia: Parents (1931) | 18 | 18.17 | 17.9 | 21.3 | 0.49 | 18.62 | 18.43 |

| Source: Analysis of April 2010 SIPP data and analysis of selected state data | |||||||

Impact on eligibility: Table 5 below provides a detailed assessment of the impact of each conversion method on eligibility, at both the individual level and in the aggregate (eligibility category) level. The table includes the converted standards produced using each of the previously discussed methods, and also reports the following information:

- Number originally eligible

- Number eligible after conversion

- Number and percent losing eligibility

- Number and percent gaining eligibility

- Net change in eligibility

- Percent (net) change in eligibility

Table 5 shows that for the MDM/25 using SIPP data (column 4), the percent change in eligibility reported for each category ranges from -5.01% to 11.06%. Overall, for 7 of 19 categories, the percent change in absolute terms is below 1%. In 12 of these 19 categories, the percent change is below 2%. Of the remaining 7 categories, 3 have a change of less than 3%. The estimates reported in Table 5 assume that pregnant women are claimed under MAGI, while tables and figures elsewhere in the report assume that pregnant women are not claimed.

Overall, these data show that the MDM/25 using SIPP data produces a small change in the aggregate levels of eligibility. Aggregate changes reported in this table are both positive and negative: in some cases the MDM/25 with SIPP data leads to an overall gain in eligibility, while in other instances this method leads to an overall reduction in eligibility. However, while the rules for eligibility vary widely among categories and states, the magnitude and range of net eligibility changes introduced by the MDM/25 using SIPP data are relatively small.

Conclusion

n conducting this study, the Department examined alternative conversion methods in an attempt to identify a single method that could accurately convert each state’s current net income standards for Medicaid and CHIP to a MAGI-based equivalent, as required by the Affordable Care Act. The Department determined that the MDM/25, using either state or SIPP data, is best suited for converting existing net income standards. This methodology focuses on those individuals for whom disregards are most likely to affect their eligibility. The Department also concluded that an adjustment for household composition and income counting rules would, for many eligibility categories, not significantly change the income standard resulting from the MDM/25. More generally, the Department’s analysis indicated that such an adjustment might make the methodology less accurate than the MDM/25.

While the Department recommends the MDM/25 as its Standardized MAGI Conversion Methodology, the CMS Guidance provides flexibility for states to develop an alternative method. Because states have unique knowledge of their specific circumstances, the Department will consider for approval alternative methodologies that meet the criteria for evaluation that the Department applied in developing its recommended method.17

Eligibility Category (Net Standard) | SNNG (GROSS) (1) | SNNG (MAGI) | Marginal 25 - HCIC correction (3) | Marginal 25 – disregards (4) | Average Disregard (5) | State Marginal 25 (6) | |

|---|---|---|---|---|---|---|---|

Note: While this table reports FPL standards, West Virginia and Nebraska use fixed dollar categories to assess eligibility in the 1931 parent groups. In practice, the FPL standards would be converted back to dollar values. Additional Notes: Asset tests are not applied. Five percent disregard is not applied. Young adults, age 19 and older, are not assumed to be claimed by parents for tax purposes. Pregnant women, aged 19-20, are assumed to be claimed by their parents for purposes of taxes if they are students or have incomes less than $3800. This assumption surrounding claiming of pregnant women in Table 5 is different from the assumption used in the other tables of the report. Other estimates and tables in the report assume that pregnant women are not claimed under MAGI. | |||||||

Arizona: CHIP (200%) | Converted Standard | 200 | 200.98 | 198.48 | 200 | 200 | . |

Weighted Population | 217329 | 217329 | 217329 | 217329 | 217329 | . | |

Number Originally Eligible | 122530 | 122530 | 122530 | 122530 | 122530 | . | |

Number Losing Eligibility | 3798 | 3798 | 4551 | 3819 | 3819 | . | |

Percent Losing Eligibility | 3.10% | 3.10% | 3.71% | 3.12% | 3.12% | . | |

Number Gaining Eligibility | 3529 | 3991 | 3485 | 3529 | 3529 | . | |

Percent Gaining Eligibility | 2.88% | 3.26% | 2.84% | 2.88% | 2.88% | . | |

Net Change in Eligibility | -270 | 193 | -1066 | -290 | -290 | . | |

Percent Change in Eligibility | -0.22% | 0.16% | -0.87% | -0.24% | -0.24% | ||

Arizona: Children 1-5 (133%) | Converted Standard | 140.42 | 142.7 | 140.76 | 139.38 | 136.22 | |

Weighted Population | 536770 | 536770 | 536770 | 536770 | 536770 | . | |

Number Originally Eligible | 281415 | 281415 | 281415 | 281415 | 281415 | . | |

Number Losing Eligibility | 6681 | 5917 | 6536 | 6940 | 8459 | . | |

Percent Losing Eligibility | 2.37% | 2.10% | 2.32% | 2.47% | 3.01% | . | |

Number Gaining Eligibility | 3863 | 5974 | 3878 | 1981 | 1427 | . | |

Percent Gaining Eligibility | 1.37% | 2.12% | 1.38% | 0.70% | 0.51% | . | |

Net Change in Eligibility | -2818 | 57 | -2659 | -4958 | -7032 | . | |

Percent Change in Eligibility | -1.00% | 0.02% | -0.94% | -1.76% | -2.50% | ||

Arizona Children 6-18 (100%) | Converted Standard | 106.17 | 116.38 | 113.88 | 105.79 | 103.02 | |

Weighted Population | 1176629 | 1176629 | 1176629 | 1176629 | 1176629 | . | |

Number Originally Eligible | 482450 | 482450 | 482450 | 482450 | 482450 | . | |

Number Losing Eligibility | 39604 | 33863 | 34968 | 39604 | 42962 | . | |

Percent Losing Eligibility | 8.21% | 7.02% | 7.25% | 8.21% | 8.90% | . | |

Number Gaining Eligibility | 15618 | 33978 | 28505 | 15445 | 11776 | . | |

Percent Gaining Eligibility | 3.24% | 7.04% | 5.91% | 3.20% | 2.44% | . | |

Net Change in Eligibility | -23986 | 116 | -6463 | -24159 | -31186 | . | |

Percent Change in Eligibility | -4.97% | 0.02% | -1.34% | -5.01% | -6.46% | . | |

Arizona Children <1 (140%) | Converted Standard | 150.07 | 150.07 | 146.74 | 147.55 | 143.12 | . |

Weighted Population | 106130 | 106130 | 106130 | 106130 | 106130 | . | |

Number Originally Eligible | 60321 | 60321 | 60321 | 60321 | 60321 | . | |

Number Losing Eligibility | 1015 | 1015 | 1119 | 1080 | 1555 | . | |

Percent Losing Eligibility | 1.68% | 1.68% | 1.86% | 1.79% | 2.58% | . | |

Number Gaining Eligibility | 1248 | 1248 | 407 | 716 | 407 | . | |

Percent Gaining Eligibility | 2.07% | 2.07% | 0.67% | 1.19% | 0.67% | . | |

Net Change in Eligibility | 232 | 232 | -713 | -364 | -1148 | . | |

Percent Change in Eligibility | 0.38% | 0.38% | -1.18% | -0.60% | -1.90% | ||

Arizona Parents, Expanded (100%) | Converted Standard | 105.77 | 103.74 | 102.66 | 105.56 | 104.89 | 106.3 |

Weighted Population | 1293698 | 1293698 | 1293698 | 1293698 | 1293698 | 1293698 | |

Number Originally Eligible | 427766 | 427766 | 427766 | 427766 | 427766 | 427766 | |

Number Losing Eligibility | 9124 | 10429 | 12672 | 9339 | 9681 | 9124 | |

Percent Losing Eligibility | 2.13% | 2.44% | 2.96% | 2.18% | 2.26% | 2.13% | |

Number Gaining Eligibility | 16008 | 10542 | 10149 | 15470 | 14110 | 16338 | |

Percent Gaining Eligibility | 3.74% | 2.46% | 2.37% | 3.62% | 3.30% | 3.82% | |

Net Change in Eligibility | 6884 | 113 | -2523 | 6131 | 4430 | 7214 | |

Percent Change in Eligibility | 1.61% | 0.03% | -0.59% | 1.43% | 1.04% | 1.69% | |

Nebraska: CHIP (200%) | Converted Standard | 209.23 | 203.8 | 201.87 | 208.17 | 207.41 | |

Weighted Population | 56608 | 56608 | 56608 | 56608 | 56608 | . | |

Number Originally Eligible | 34183 | 34183 | 34183 | 34183 | 34183 | . | |

Number Losing Eligibility | 426 | 1109 | 1533 | 509 | 672 | . | |

Percent Losing Eligibility | 1.25% | 3.24% | 4.48% | 1.49% | 1.97% | . | |

Number Gaining Eligibility | 1445 | 1121 | 1000 | 1331 | 1260 | . | |

Percent Gaining Eligibility | 4.23% | 3.28% | 2.93% | 3.89% | 3.69% | . | |

Net Change in Eligibility | 1019 | 12 | -533 | 822 | 589 | . | |

Percent Change in Eligibility | 2.98% | 0.04% | -1.56% | 2.40% | 1.72% | ||

Nebraska Children 1-5 (133%) | Converted Standard | 141.25 | 137.61 | 134.85 | 139.79 | 136.69 | 145.3 |

Weighted Population | 129883 | 129883 | 129883 | 129883 | 129883 | 129883 | |

Number Originally Eligible | 45252 | 45252 | 45252 | 45252 | 45252 | 45252 | |

Number Losing Eligibility | 460 | 683 | 1436 | 536 | 917 | 138 | |

Percent Losing Eligibility | 1.02% | 1.51% | 3.17% | 1.18% | 2.03% | 0.30% | |

Number Gaining Eligibility | 1358 | 700 | 607 | 1090 | 651 | 2613 | |

Percent Gaining Eligibility | 3.00% | 1.55% | 1.34% | 2.41% | 1.44% | 5.77% | |

Net Change in Eligibility | 898 | 18 | -828 | 555 | -266 | 2475 | |

Percent Change in Eligibility | 1.98% | 0.04% | -1.83% | 1.23% | -0.59% | 5.47% | |

Nebraska Children 6-18 (100%) | Converted Standard | 106.95 | 101.73 | 101.01 | 105.94 | 103.22 | 108.7 |

Weighted Population | 330571 | 330571 | 330571 | 330571 | 330571 | 330571 | |

Number Originally Eligible | 79474 | 79474 | 79474 | 79474 | 79474 | 79474 | |

Number Losing Eligibility | 2314 | 3943 | 4374 | 2681 | 3425 | 2034 | |

Percent Losing Eligibility | 2.91% | 4.96% | 5.50% | 3.37% | 4.31% | 2.56% | |

Number Gaining Eligibility | 4758 | 3969 | 3844 | 4649 | 4060 | 5281 | |

Percent Gaining Eligibility | 5.99% | 4.99% | 4.84% | 5.85% | 5.11% | 6.64% | |

Net Change in Eligibility | 2444 | 27 | -530 | 1968 | 634 | 3246 | |

Percent Change in Eligibility | 3.08% | 0.03% | -0.67% | 2.48% | 0.80% | 4.08% | |

Nebraska Children <1 (150%) | Converted Standard | 159.58 | 156.64 | 154.37 | 158.33 | 153.7 | 162.1 |

Weighted Population | 25122 | 25122 | 25122 | 25122 | 25122 | 25122 | |

Number Originally Eligible | 10429 | 10429 | 10429 | 10429 | 10429 | 10429 | |

Number Losing Eligibility | 107 | 156 | 233 | 156 | 233 | 38 | |

Percent Losing Eligibility | 1.03% | 1.50% | 2.23% | 1.50% | 2.23% | 0.36% | |

Number Gaining Eligibility | 362 | 236 | 102 | 262 | 102 | 499 | |

Percent Gaining Eligibility | 3.47% | 2.26% | 0.98% | 2.51% | 0.98% | 4.78% | |

Net Change in Eligibility | 255 | 80 | -131 | 106 | -131 | 461 | |

Percent Change in Eligibility | 2.45% | 0.77% | -1.26% | 1.02% | -1.26% | 4.42% | |

Nebraska Parents (50.3%) | Converted Standard | 54.41 | 50.74 | 49.88 | 55.41 | 55.92 | |

Weighted Population | 349838 | 349838 | 349838 | 349838 | 349838 | . | |

Number Originally Eligible | 41784 | 41784 | 41784 | 41784 | 41784 | . | |

Number Losing Eligibility | 1609 | 2784 | 2841 | 1436 | 1426 | . | |

Percent Losing Eligibility | 3.85% | 6.66% | 6.80% | 3.44% | 3.41% | . | |

Number Gaining Eligibility | 3604 | 2721 | 2606 | 3891 | 4043 | . | |

Percent Gaining Eligibility | 8.63% | 6.51% | 6.24% | 9.31% | 9.68% | . | |

Net Change in Eligibility | 1996 | -63 | -235 | 2455 | 2617 | . | |

Percent Change in Eligibility | 4.78% | -0.15% | -0.56% | 5.88% | 6.26% | ||

New York: CHIP (400%) | Converted Standard | 399.67 | 396.1 | 392.25 | 400 | 400 | . |

Weighted Population | 488444 | 488444 | 488444 | 488444 | 488444 | . | |

Number Originally Eligible | 429447 | 429447 | 429447 | 429447 | 429447 | . | |

Number Losing Eligibility | 1055 | 1473 | 3152 | 1055 | 1055 | . | |

Percent Losing Eligibility | 0.25% | 0.34% | 0.73% | 0.25% | 0.25% | . | |

Number Gaining Eligibility | 1794 | 1794 | 1794 | 1794 | 1794 | . | |

Percent Gaining Eligibility | 0.42% | 0.42% | 0.42% | 0.42% | 0.42% | . | |

Net Change in Eligibility | 739 | 320 | -1358 | 739 | 739 | . | |

Percent Change in Eligibility | 0.17% | 0.07% | -0.32% | 0.17% | 0.17% | ||

New York: Children 1-5 (133%) | Converted Standard | 139.69 | 136.5 | 134.1 | 138.64 | 136.18 | . |

Weighted Population | 1272558 | 1272558 | 1272558 | 1272558 | 1272558 | . | |

Number Originally Eligible | 579891 | 579891 | 579891 | 579891 | 579891 | . | |

Number Losing Eligibility | 2148 | 4920 | 11688 | 2148 | 6770 | . | |

Percent Losing Eligibility | 0.37% | 0.85% | 2.02% | 0.37% | 1.17% | . | |

Number Gaining Eligibility | 10763 | 5567 | 5320 | 7703 | 5429 | . | |

Percent Gaining Eligibility | 1.86% | 0.96% | 0.92% | 1.33% | 0.94% | . | |

Net Change in Eligibility | 8616 | 646 | -6368 | 5556 | -1341 | . | |

Percent Change in Eligibility | 1.49% | 0.11% | -1.10% | 0.96% | -0.23% | ||

New York: Children 6-18 (133%) | Converted Standard | 138.85 | 134.82 | 132.05 | 138.21 | 135.87 | . |

Weighted Population | 3115259 | 3115259 | 3115259 | 3115259 | 3115259 | . | |

Number Originally Eligible | 1223346 | 1223346 | 1223346 | 1223346 | 1223346 | . | |

Number Losing Eligibility | 13146 | 27250 | 37793 | 13370 | 26084 | . | |

Percent Losing Eligibility | 1.07% | 2.23% | 3.09% | 1.09% | 2.13% | . | |

Number Gaining Eligibility | 36999 | 27801 | 26202 | 34859 | 28488 | . | |

Percent Gaining Eligibility | 3.02% | 2.27% | 2.14% | 2.85% | 2.33% | . | |

Net Change in Eligibility | 23853 | 551 | -11591 | 21489 | 2404 | . | |

Percent Change in Eligibility | 1.95% | 0.05% | -0.95% | 1.76% | 0.20% | ||

New York: Children <1 (200%) | Converted Standard | 206.96 | 206.96 | 200.84 | 206.47 | 203.14 | . |

Weighted Population | 248383 | 248383 | 248383 | 248383 | 248383 | . | |

Number Originally Eligible | 147682 | 147682 | 147682 | 147682 | 147682 | . | |

Number Losing Eligibility | 303 | 303 | 1010 | 303 | 471 | . | |

Percent Losing Eligibility | 0.21% | 0.21% | 0.68% | 0.21% | 0.32% | . | |

Number Gaining Eligibility | 795 | 795 | 106 | 106 | 106 | . | |

Percent Gaining Eligibility | 0.54% | 0.54% | 0.07% | 0.07% | 0.07% | . | |

Net Change in Eligibility | 493 | 493 | -904 | -196 | -365 | . | |

Percent Change in Eligibility | 0.33% | 0.33% | -0.61% | -0.13% | -0.25% | ||

New York: Parents (87%) | Converted Standard | 87.31 | 85.44 | 83.53 | 86.92 | 88 | . |

Weighted Population | 4068108 | 4068108 | 4068108 | 4068108 | 4068108 | . | |

Number Originally Eligible | 1132154 | 1132154 | 1132154 | 1132154 | 1132154 | . | |

Number Losing Eligibility | 45648 | 49747 | 62276 | 48138 | 41950 | . | |

Percent Losing Eligibility | 4.03% | 4.39% | 5.50% | 4.25% | 3.71% | . | |

Number Gaining Eligibility | 57011 | 49968 | 38281 | 53020 | 58785 | . | |

Percent Gaining Eligibility | 5.04% | 4.41% | 3.38% | 4.68% | 5.19% | . | |

Net Change in Eligibility | 11363 | 221 | -23995 | 4881 | 16834 | . | |

Percent Change in Eligibility | 1.00% | 0.02% | -2.12% | 0.43% | 1.49% | ||

West Virginia: Parents, 1931 (18%) | Converted Standard | 21.3 | 0.49 | 18.62 | 18.17 | 18.43 | 17.9 |

Weighted Population | 348792 | 348792 | 348792 | 348792 | 348792 | 348792 | |

Number Originally Eligible | 45540 | 45540 | 45540 | 45540 | 45540 | 45540 | |

Number Losing Eligibility | 1451 | 5572 | 1538 | 1550 | 1550 | 1554 | |

Percent Losing Eligibility | 3.19% | 12.24% | 3.38% | 3.40% | 3.40% | 3.41% | |

Number Gaining Eligibility | 7104 | 5581 | 6600 | 6587 | 6600 | 6515 | |

Percent Gaining Eligibility | 15.60% | 12.26% | 14.49% | 14.46% | 14.49% | 14.31% | |

Net Change in Eligibility | 5653 | 8 | 5062 | 5037 | 5050 | 4961 | |

Percent Change in Eligibility | 12.41% | 0.02% | 11.12% | 11.06% | 11.09% | 10.89% | |

Arizona: Pregnant Women (150%) | Converted Standard | 158.07 | 158.07 | 151.62 | 159.33 | 153.98 | . |

Weighted Population | 48825 | 48825 | 48825 | 48825 | 48825 | . | |

Number Originally Eligible | 23146 | 23146 | 23146 | 23146 | 23146 | . | |

Number Losing Eligibility | 858 | 858 | 1217 | 858 | 1217 | . | |

Percent Losing Eligibility | 3.71% | 3.71% | 5.26% | 3.71% | 5.26% | . | |

Number Gaining Eligibility | 887 | 887 | 717 | 887 | 717 | . | |

Percent Gaining Eligibility | 3.83% | 3.83% | 3.10% | 3.83% | 3.10% | . | |

Net Change in Eligibility | 29 | 29 | -499 | 29 | -499 | . | |

Percent Change in Eligibility | 0.13% | 0.13% | -2.16% | 0.13% | -2.16% | ||

Nebraska: Pregnant Women (185%) | Converted Standard | 199.51 | 193.14 | 201.7 | 196.2 | 191.32 | 199.1 |

Weighted Population | 14652 | 14652 | 14652 | 14652 | 14652 | 14652 | |

Number Originally Eligible | 6575 | 6575 | 6575 | 6575 | 6575 | 6575 | |

Number Losing Eligibility | 169 | 268 | 152 | 238 | 360 | 238 | |

Percent Losing Eligibility | 2.57% | 4.08% | 2.31% | 3.62% | 5.48% | 3.62% | |

Number Gaining Eligibility | 410 | 287 | 435 | 344 | 287 | 410 | |

Percent Gaining Eligibility | 6.24% | 4.37% | 6.62% | 5.23% | 4.37% | 6.24% | |

Net Change in Eligibility | 241 | 19 | 283 | 106 | -73 | 173 | |

Percent Change in Eligibility | 3.67% | 0.29% | 4.30% | 1.61% | -1.11% | 2.63% | |

New York: Pregnant Women (200%) | Converted Standard | 205.93 | 205.01 | 194.02 | 206.56 | 204.05 | |

Weighted Population | 158950 | 158950 | 158950 | 158950 | 158950 | . | |

Number Originally Eligible | 92579 | 92579 | 92579 | 92579 | 92579 | . | |

Number Losing Eligibility | 1913 | 3487 | 5633 | 1641 | 3621 | . | |

Percent Losing Eligibility | 2.07% | 3.77% | 6.08% | 1.77% | 3.91% | . | |

Number Gaining Eligibility | 4059 | 4059 | 3446 | 4059 | 3446 | . | |

Percent Gaining Eligibility | 4.38% | 4.38% | 3.72% | 4.38% | 3.72% | . | |

Net Change in Eligibility | 2145 | 571 | -2187 | 2417 | -175 | . | |

Percent Change in Eligibility | 2.32% | 0.62% | -2.36% | 2.61% | -0.19% | ||

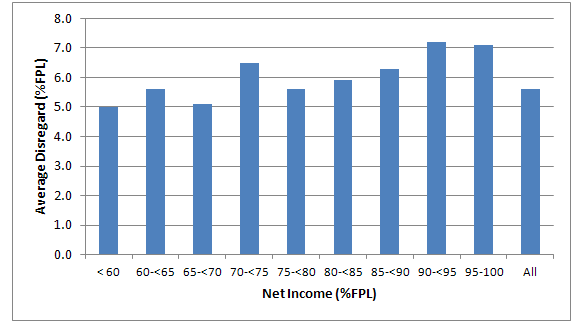

Appendix 1: Distribution of Disregards by Net Income for Selected State and Eligibility Categories

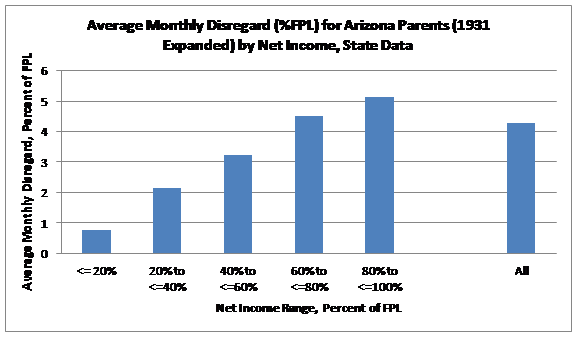

Tables 1A and 1B support the hypothesis that net income and the amount of monthly disregards are correlated. Table 1A uses Arizona state data to show the distribution of average monthly disregards by income levels for Arizona parents who are in the expanded eligibility category permitted by Section 1931 of the Social Security Act.19 Note that the net income standard for this group varies across states. For Arizona, the net income standard is 100% of FPL. For this group, Table 1A shows that as income increases, disregards also increase. It also shows that the average amount of disregards for people between 60% and 100% of FPL are higher than the aggregate average disregard. As discussed further in the main paper, this demonstrates support for the Marginal Disregard Method with 25 percentage point band (MDM/25), which will focus the analysis of disregards on those populations for which it is most likely to have an impact on eligibility.

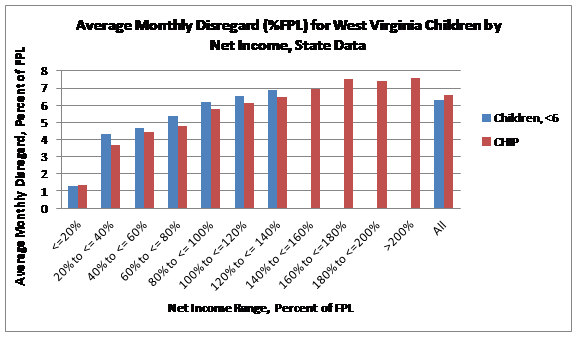

Table 1B uses West Virginia state data to show the distribution of average monthly disregards by net income levels for children under age 6 and children eligible for CHIP. For children under age 6, the net income standard is 133% of FPL; for children eligible for CHIP, the net income standard is 250% of FPL. This table implies that the state may not have recorded all disregard information for individuals with net incomes below 20% of FPL, as evidenced by the very low average disregard amount for that group, compared to higher net income groups. This table also shows that as income increases, so do disregards. These two key points demonstrate support for MDM/25.

Table 1A. ARIZONA PARENTS (1931 EXPANDED) DISTRIBUTION OF MONTHLY DISREGARDS BY NET INCOME: STATE ADMINISTRATIVE DATA

| Average Disregard as % of FPL | Count of Records | Percent of Total Count | |

|---|---|---|---|

Parents, 1931 Expanded | |||

<=20% | 0.76 | 2,373 | 3.09 |

20% to <= 40% | 2.13 | 41,472 | 5.41 |

40% to <= 60% | 3.23 | 189,036 | 24.65 |

60% to <= 80% | 4.53 | 257,039 | 33.52 |

80% to <= 100% | 5.15 | 277,004 | 36.19 |

All | 4.29 | 766,924 | 100.00 |

Table 1B. WEST VIRGINIA DISTRIBUTION OF MONTHLY DISREGARDS BY NET INCOME: STATE ADMINISTRATIVE DATA

| Average Disregard as % of FPL | Count of Records | Percent of Total Count | |

|---|---|---|---|

| Children, <6 | |||

| <=20% | 1.26 | 120 | 2.72 |

| 20% to <= 40% | 4.33 | 75 | 1.70 |

| 40% to <= 60% | 4.64 | 122 | 2.76 |

| 60% to <= 80% | 5.38 | 174 | 3.94 |

| 80% to <= 100% | 6.19 | 342 | 7.74 |

| 100% to <= 120% | 6.51 | 2,368 | 53.61 |

| 120% to <=140% | 6.86 | 1,216 | 27.53 |

| All | 6.31 | 4,417 | 100.00 |

Net Income Standard: Children 0-6: 133% FPL

Source: Analysis of West Virginia Administrative Data.

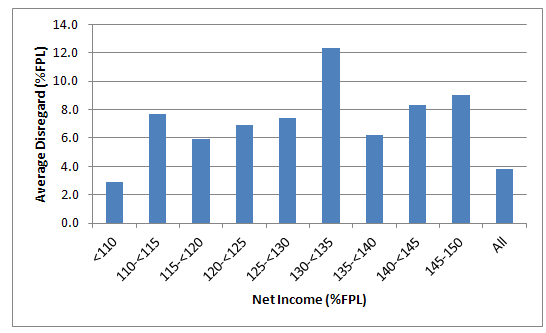

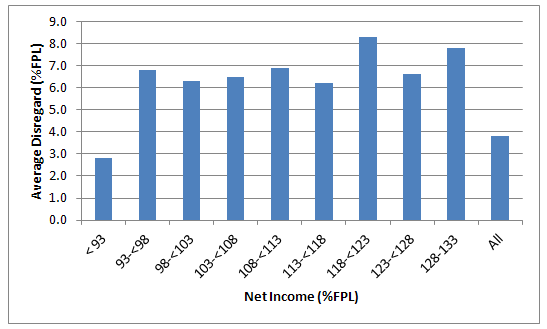

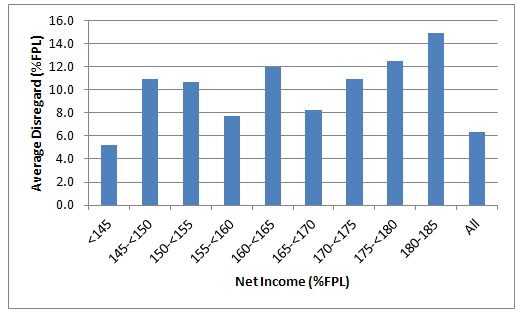

Tables 1C, 1D, and 1E indicate that SIPP data, like state data, also show a clear relationship between income level and the size of disregards in most of the eligibility categories tested.

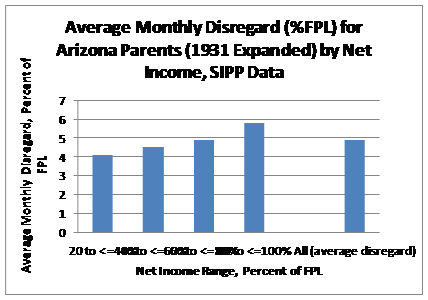

- Table 1C shows the distribution of average monthly disregards by net income level for Arizona parents in the 1931 expanded group. Similar to Arizona state data, the SIPP data in Table 1C show that as income rises, the amount of monthly disregards also rises.

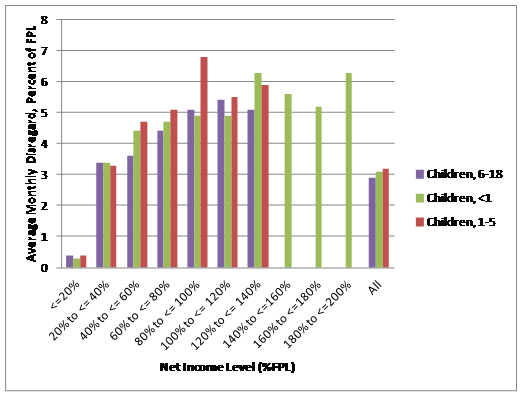

- Table 1D uses SIPP data to show the distribution of average monthly disregards by net income level for children less than age 1, children between the ages of 1 and 5, and children between the ages of 6 and 18 in New York. Table 1D shows that, in most cases, as income rises, the amount of monthly disregards also rises.

- Table 1E uses SIPP data to show the distribution of average monthly disregards by net income level for children less than age 1, children between the ages of 1 and 5, and children between the ages of 6 and 18 in Nebraska. Similar to previous analyses, these data demonstrate the correlation between net income and the amount of disregards.

All three tables support the use of the MDM because the total average disregard amount is heavily influenced by very low income individuals who have few disregards. These people are not at risk for losing eligibility due to the conversion, and therefore should not be incorporated in the calculation.

Table 1C. ARIZONA PARENTS (1931 EXPANDED) DISTRIBUTION OF MONTHLY DISREGARDS BY NET INCOME: SIPP DATA

| Average Disregard | Sample Size | Weighted Count of Records | Percent of Sample | |

|---|---|---|---|---|

| 20% to <= 40% | 4.1 | 384 | 36,279.4 | 16.13 |

| 40% to <= 60% | 4.5 | 567 | 60,717.8 | 23.81 |

| 60% to <= 80% | 4.9 | 728 | 74,736.3 | 30.58 |

| 80% to <= 100% | 5.8 | 702 | 58,690.9 | 29.48 |

| All | 4.9 | 2381 | 230,424.3 | 100.00 |

Net Income Standard: 100% FPL, Parents

Source: Analysis using SIPP data

Table 1D. NEW YORK CHILDREN DISTRIBUTION OF MONTHLY DISREGARDS BY NET INCOME: SIPP DATA

| Average Disregard as % of FPL | Sample Size | Weighted Count of Records | Percent of Sample | |

|---|---|---|---|---|

| Children, 6-18 | ||||

| <=20% | 0.4 | 2,406 | 477,258.5 | 38.23 |

| 20% to <= 40% | 3.4 | 539 | 118,755.4 | 8.56 |

| 40% to <= 60% | 3.6 | 685 | 133,461.3 | 10.88 |

| 60% to <= 80% | 4.4 | 792 | 155,147.7 | 12.58 |

| 80% to <= 100% | 5.1 | 785 | 152,327.7 | 12.47 |

| 100% to <=120% | 5.4 | 644 | 108,084.4 | 10.23 |

| 120% to <=140% | 5.1 | 443 | 78,311.2 | 7.04 |

| All | 2.9 | 6294 | 1,223,346.2 | 100.00 |

| Children, 1-5 | ||||

| <=20% | 0.4 | 1,142 | 239,750 | 40.61 |

| 20% to <= 40% | 3.3 | 224 | 50,090.5 | 7.97 |

| 40% to <= 60% | 4.7 | 305 | 63,010.8 | 10.85 |

| 60% to <= 80% | 5.1 | 349 | 78,437.2 | 12.41 |

| 80% to <= 100% | 6.8 | 285 | 52,525.9 | 10.14 |

| 100% to <= 120% | 5.5 | 277 | 49,538.1 | 9.85 |

| 120% to <=140% | 5.9 | 193 | 41,626.7 | 6.86 |

| All | 3.2 | 2812 | 579,890.7 | 100.00 |

| Children, <1 | ||||

| <=20% | 0.3 | 230 | 59,949.7 | 40.00 |

| 20% to <= 40% | 3.4 | 39 | 9,732.8 | 6.78 |

| 40% to <= 60% | 4.4 | 34 | 9,898.7 | 5.91 |

| 60% to <= 80% | 4.7 | 50 | 12,103.7 | 8.70 |

| 80% to <= 100% | 4.9 | 42 | 9,102.1 | 7.30 |

| 100% to <= 120% | 4.9 | 40 | 9767 | 6.96 |

| 120% to <= 140% | 6.3 | 46 | 12,439.9 | 8.00 |

| 140% to <=160% | 5.6 | 33 | 8,705.9 | 5.74 |

| 160% to <=180% | 5.2 | 23 | 6,029 | 4.00 |

| 180% to <=200% | 6.3 | 38 | 9,952.8 | 6.61 |

| All | 3.1 | 575 | 147,681.6 | 100.00 |

Net Income Standard: Children <1: 200%; Children 1-5: 133%; Children 6-18: 100%.

Source: Analysis using SIPP data.

Table 1E. NEBRASKA DISTRIBUTION OF MONTHLY DISREGARDS BY NET INCOME: SIPP DATA

| Average Disregard as % of FPL | Sample Size | Weighted Count of Records | Percent of Sample | |

|---|---|---|---|---|

| Children, 6-18 | ||||

| <=20% | 0.7 | 2428 | 36,403 | 46.27 |

| 20% to <= 40% | 4.7 | 533 | 8,573.1 | 10.16 |

| 40% to <= 60% | 4.4 | 664 | 9,883.2 | 12.65 |

| 60% to <= 80% | 5.6 | 833 | 11,436.9 | 15.87 |

| 80% to <= 100% | 6.2 | 790 | 13,177.4 | 15.05 |

| All | 3.2 | 5248 | 79,473.6 | 100.00 |

| Children, 1-5 | ||||

| <=20% | 0.6 | 1191 | 18,461.1 | 42.07 |

| 20% to <= 40% | 3.8 | 213 | 3,250.2 | 7.52 |

| 40% to <= 60% | 5 | 275 | 4,363.5 | 9.71 |

| 60% to <= 80% | 5.4 | 374 | 5,287.7 | 13.21 |

| 80% to <= 100% | 6.8 | 303 | 5,088.1 | 10.70 |

| 100% to <= 120% | 6.5 | 281 | 4,942.1 | 9.93 |

| 120% to <= 140% | 6.7 | 194 | 3,859.1 | 6.85 |

| All | 3.7 | 2831 | 45,251.8 | 100.00 |

| Children, <1 | ||||

| <=20% | 0.4 | 231 | 4,532.6 | 46.20 |

| 20% to <= 40% | 5 | 40 | 793.8 | 8.00 |

| 40% to <= 60% | 4.9 | 33 | 702.4 | 6.60 |

| 60% to <= 80% | 5 | 49 | 914.7 | 9.80 |

| 80% to <= 100% | 5.7 | 42 | 894.4 | 8.40 |

| 100% to <=120% | 6.9 | 43 | 1,049.8 | 8.60 |

| 120% to <=140% | 7.9 | 47 | 1,097.8 | 9.40 |

| 140% to <=160% | 8.7 | 15 | 443.2 | 3.00 |

| All | 3.7 | 500 | 10,428.7 | 100.00 |

Net Income Standard: Children <1: 150%; Children 1-5: 133%; Children 6-18: 133%

Source: Analysis using SIPP data.

Appendix 2. Primary Differences between Magi under Medicaid/Chip Eligibility Rule and the Internal Revenue Code

The concept of MAGI is adapted from the context of federal income taxes and is defined in Section 36B(d)(2) of the Internal Revenue Code of 1986. MAGI for purposes of Medicaid and CHIP eligibility under Section 2002 of the Affordable Care Act is closely aligned with, although not exactly the same as, MAGI for tax purposes. MAGI for tax purposes, like other federal income tax concepts, is based on annual income and adjustments. Section 2002(a)(14)(H)(i), in contrast, specifically continues the current Medicaid/CHIP practice of determining eligibility based on “an individual’s income as of the point in time at which an application for medical assistance under the State plan or a waiver of the plan is processed,” which is closer to current monthly income. The March 23, 2012 Final Rule on Eligibility Changes Under the Affordable Care Act explicitly incorporates other changes to the tax concept of MAGI.20

| Medicaid and CHIP MAGI | IRC MAGI | |

|---|---|---|

| Pregnant Women | Counted as a household of 1 plus the number of expected children. | Always counted as a household of 1. |