Joshua M. Wiener, Galina Khatutsky, Angela M. Greene, Trini Thach, and Benjamin Allaire

RTI International

Derek Brown

Washington University

July 30, 2015

ASPE Policy Forum

Contact Information

- Joshua Wiener jwiener@rti.org

- Angela M. Greene amg@rti.org

- Trini Thach tthach@rti.org

- Galina Khatutsky gkhatutsky@rti.org

- Benjamin Allaire ballaire@rti.org

- Derek Brown dereksbrown@wustl.edu

Disclaimer

- This research was supported by the Office of the Assistant Secretary for Planning and Evaluation/U.S. Department of Health and Human Services under Contract #HHSP23320100021WI.

- We gratefully acknowledge the contributions of Samuel Shipley, William Marton, Judith Dey, Pamela Doty, and John Drabeck to the design and analysis of the survey.

- The views expressed in this presentation are those of the authors and do not necessarily represent the views of the U.S. DHHS or RTI International.

Research Questions

- What is the general public’s knowledge, experience, and concerns about long-term services and supports?

- What are public’s preferences for a range of public policy options for long-term care financing reform?

- What are individuals’ preferences for specific key features of long-term care insurance policies and what are people willing to pay for these features?

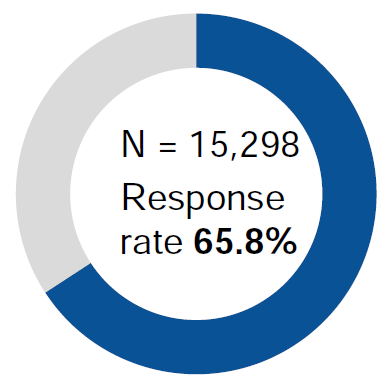

Survey Background

- 2014 Survey of Long-Term Care Awareness and Planning, sponsored by the Office of the Assistant Secretary for Planning and Evaluation/U.S. Department of Health and Human Services (DHHS)

- Designed, cognitively tested, and analyzed by RTI International, with input from ASPE and TEP

- Fielded by GfK Custom Research, LLC

- Data collected August–September 2014

Data

- Two distinct survey components

- General survey items, including long-term care knowledge and experience, attitudes and concerns, preferences on public policy options for long-term care financing, and core sociodemographic characteristics

- Discrete Choice Experiment (DCE) involving choice of long-term care insurance policies with different features and prices

Survey Sample

Ongoing Internet panel maintained by GfK Custom Research KnowledgePanel®

Participation in panel by invitation only

Nationally representative sample of noninstitutionalized adults 40-70 years old residing in the United States

Weighted to represent general population age 40-70

LTSS Knowledge and Experience

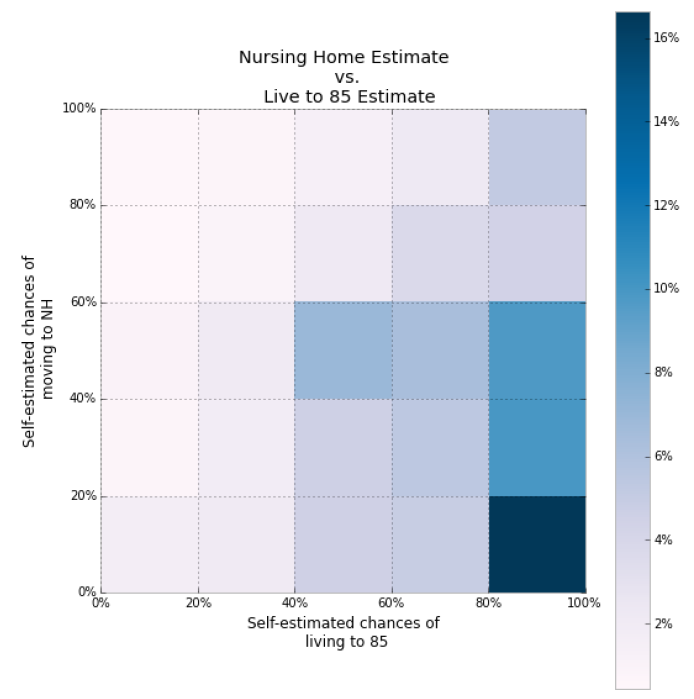

Longevity Risk and Nursing Home Use Expectations

Source: RTI International Analysis of the 2014 Survey of Long-Term Care Planning and Awareness.

Currently providing LTC To family member/friend

| Have you or has someone you know ever: | |

|---|---|

| required LTC because of a disability or illness? | 52.8% |

| received paid in-home care for ADLs? | 31.3% |

| been a resident in a nursing home/assisted living facility? | 44.2% |

Source: RTI International Analysis of the 2014 Survey of Long-Term Care Planning and Awareness.

Knowledge of LTC Services and Costs

| Knowledge of LTC | % Correct |

|---|---|

| Source: RTI International Analysis of the 2014 Survey of Long-Term Care Planning and Awareness. | |

| Cost of 1 month of nursing home care | 20.2 |

| Cost of 1 hour of home health aide care | 15.3 |

| Medicaid is primary government LTC payer | 25.3 |

| Average nursing home LOS < 5 years | 34.9 |

Knowledge of LTC Insurance

- Familiarity with LTC Insurance Policies

- LTC insurance premiums increase with age: 66.7% Correct

- Good health is generally required to purchase LTC insurance policy: 41% Correct

Source: RTI International Analysis of the 2014 Survey of Long-Term Care Planning and Awareness.

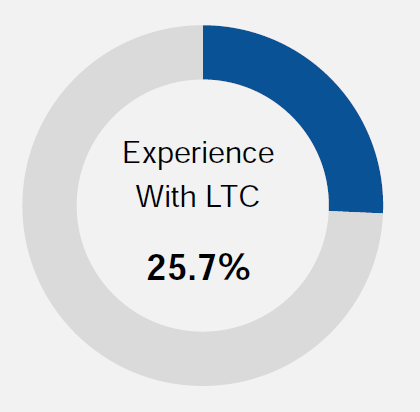

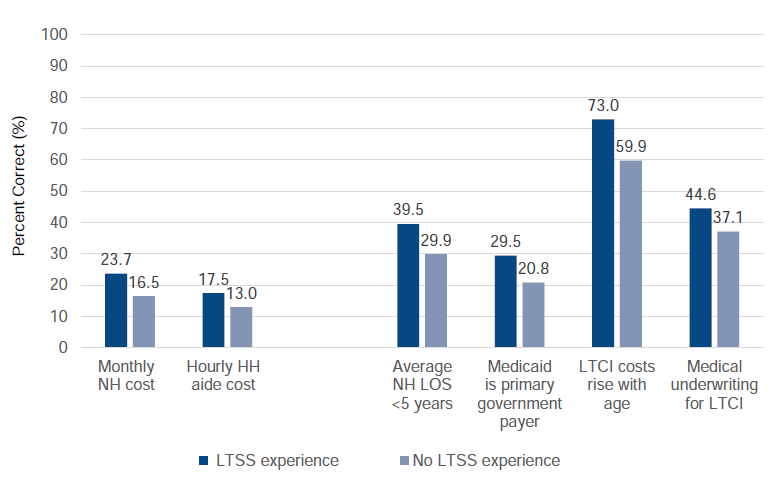

LTSS/LTCI Knowledge by LTSS Experience

Source: RTI International Analysis of the 2014 Survey of Long-Term Care Planning and Awareness.

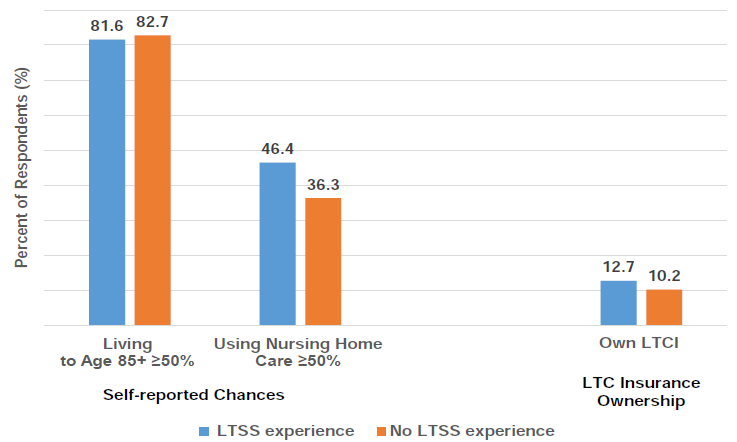

Longevity/Nursing Home Use Risk and LTCI Ownership by LTSS Experience

Source: RTI International Analysis of the 2014 Survey of Long-Term Care Planning and Awareness.

LTSS Concerns and Actions

Main Concerns About LTC

| Concerns | % Very/Somewhat Concerned |

|---|---|

| Source: RTI International Analysis of the 2014 Survey of Long-Term Care Planning and Awareness. | |

| Losing independence | 90.6 |

| Being a burden on family | 83.5 |

| Losing control/choice over LTC | 83.3 |

| Being unable to afford high quality care | 82.0 |

| Using up savings/income | 81.1 |

| Becoming poor/relying on Medicaid | 78.9 |

| Being unable to depend on family/friends | 65.3 |

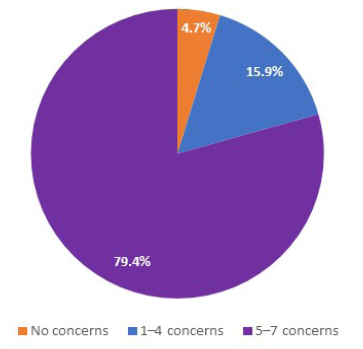

Number of Concerns About LTC

Source: RTI International Analysis of the 2014 Survey of Long-Term Care Planning and Awareness.

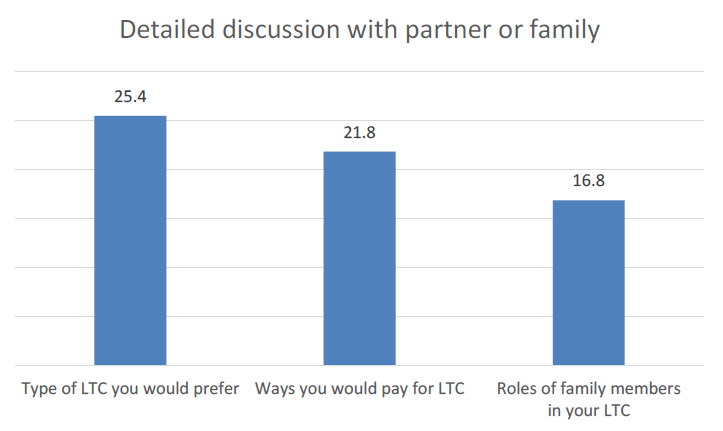

Talking About LTC

Source: RTI International Analysis of the 2014 Survey of Long-Term Care Planning and Awareness.

Preferred Actions if Need LTC

| If you became disabled, how willing would you be to do the following? | % Very Willing/Somewhat Willing |

|---|---|

| Source: RTI International Analysis of the 2014 Survey of Long-Term Care Planning and Awareness. | |

| Make home modifications | 82.3 |

| Rely on spouse/family/friend | 75.0 |

| Have family/friend move in | 69.7 |

| Attend adult day care | 66.1 |

| Hire aide or agency for care | 64.0 |

| Move into assisted living facility | 62.4 |

| Hire live-in caregiver | 57.4 |

| Move in with children/family/friend | 48.5 |

| Use value in home to pay for LTC | 43.6 |

| Move into nursing home | 28.6 |

Willingness to Use Home Equity Among Homeowners

| Very Willing/Somewhat Willing N = 5,391 Percent (%) | |

|---|---|

| Source: RTI International Analysis of the 2014 Survey of Long-Term Care Planning and Awareness. | |

| Total | 43.6 |

| Children None None within 10 miles One or more within 10 miles | 50.3 41.3 41.9 |

| Marital Status Married Unmarried | 42.1 47.7 |

| Household Savings and Assets No assets Less than $100,000 Greater than or equal to $100,000 | 32.7 42.1 46.9 |

Responsibility for LTSS and Financing Reforms

Attitudes Toward LTC Responsibility

- Responsibility for LTC

- 71.2% Strongly Agree/Agree: It is important to plan now for LTC services in the future

- 11.5%: Own private long-term care insurance policy

- 58.7% Strongly Agree/Agree: Responsibility of individuals to finance their LTC

- 17.4% Strongly Agree/Agree: Responsibility of children/family to finance LTC

- 37.1% Strongly Agree/Agree: Responsibility of government to help pay for LTC

Source: RTI International Analysis of the 2014 Survey of Long-Term Care Planning and Awareness.

Trust of the Government and Insurers

- Attitude

- I do not trust government to run an LTC insurance program: 51.1% Strongly Agree/Agree

- I do not trust private insurers: 32.3% Strongly Agree/Agree

Source: RTI International Analysis of the 2014 Survey of Long-Term Care Planning and Awareness.

Government Role in LTC Financing

| Government Should | % Strongly Agree/Agree |

|---|---|

| Source: RTI International Analysis of the 2014 Survey of Long-Term Care Planning and Awareness. | |

| Allow LTC insurance purchase with IRAs and 401(k)s | 69.1 |

| Offer voluntary, public LTC insurance plan | 62.9 |

| Promote LTC through tax incentives | 62.4 |

| Pay LTC costs when insurance benefits run out | 40.9 |

| Establish mandatory, public LTC program | 18.4 |

| Require all people to purchase LTC insurance | 15.7 |

LTC Insurance Ownership

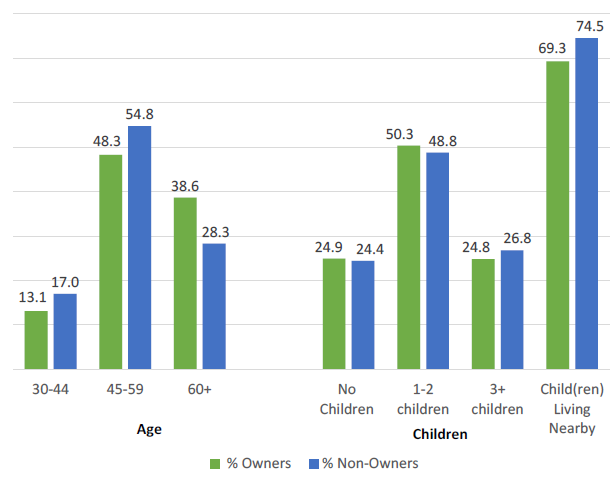

LTC Insurance Ownership by Age and Potential Informal Care by Children

Source: RTI International Analysis of the 2014 Survey of Long-Term Care Planning and Awareness.

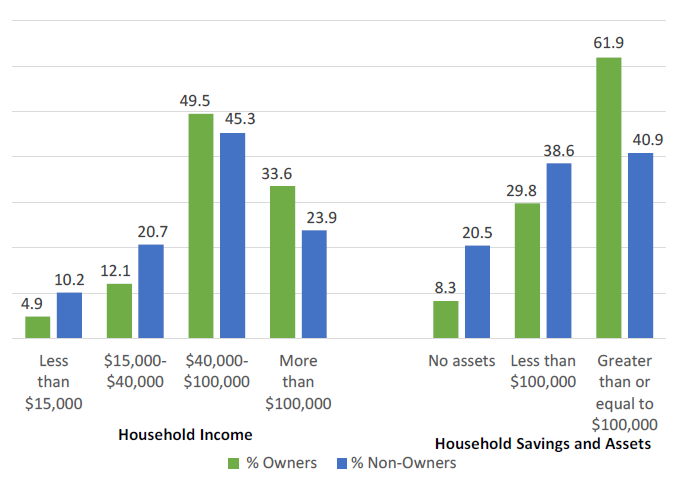

LTC Insurance Ownership by Income and Assets

Source: RTI International Analysis of the 2014 Survey of Long-Term Care Planning and Awareness.

Long-Term Care Awareness and Planning Survey Discrete Choice Experiment

Goals of the DCE Analysis

- Gather data on respondents’ preferences about long-term care insurance to better understand what factors are more and less important to them

- To test these preferences, we developed a series of paired comparisons of alternative long-term care insurance plans

Background and Methods

- DCE origins in marketing research:

- Given a choice of alternatives, what do people want?

- Why?

- How much do they want it?

- Data analysis:

- Conditional logit model (with clustering) of respondents’ stated choices for the final results

Overview of the DCE

- Form of conjoint analysis

- Used to estimate the relative importance that respondents place on the different features of an individual product

- Basic premise is that products or services can be characterized by a series of features or “attributes”

- Each attribute has a defined set of usually two to four levels or choices

Methods

Respondents to the DCE section of the survey completed two types of choice tasks

- SET I: Respondents evaluated plans described by six attributes

- daily benefit

- benefit period

- deductible period

- health requirements

- type of insurer (government or private insurer)

- premium cost

- SET II: Respondents evaluated plans described by seven attributes--the same six:

- daily benefit

- benefit period

- deductible period

- health requirements

- type of insurer (government or private insurer)

- premium cost

- ...plus:

- mandatory vs. voluntary enrollment

Asked to choose between plans A, B, and no insurance plan

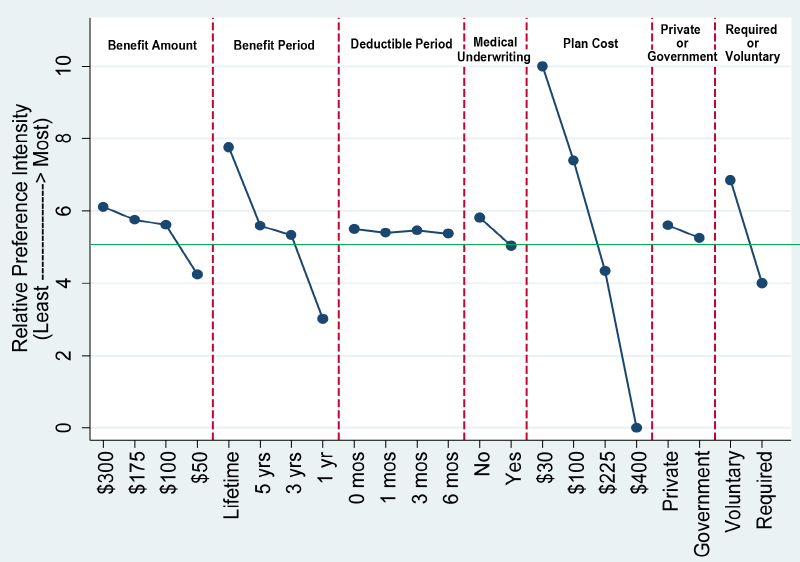

Relative Preferences for LTC Insurance Plan Features: DCE 2

Source: RTI International Analysis of the 2014 Survey of Long-Term Care Planning and Awareness.

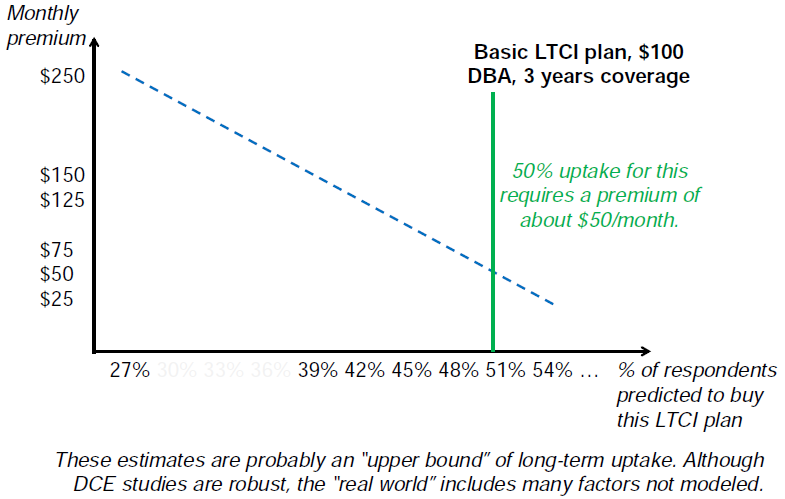

Estimated Potential Market Demand: DCE1

- The preference estimates from the figures enter a statistical model that predicts choice behavior

- Given a choice between alternatives, what do respondents’ stated choices tell us about how many would pick each?

- Suppose respondents had only 2 options:

| No LTC Insurance | Basic LTC Insurance |

|---|---|

| $100 daily benefit amount | |

| 3 years of coverage | |

| No deductible | |

| Various prices |

Source: RTI International Analysis of the 2014 Survey of Long-Term Care Planning and Awareness.

Estimated Marginal Willingness to Pay for Changes in LTC Insurance Plans

- Economists frequently scale the figure of preference estimates earlier according to respondents’ sensitivity to price (marginal value of $)

- Doing so yields the following estimates of “willingness to pay”

- These represent a dollar estimate of how intensely a given LTC plan feature was valued by respondents

| Marginal Change | Estimate (DCE 2) |

|---|---|

| Source: RTI International Analysis of the 2014 Survey of Long-Term Care Planning and Awareness. | |

| Daily benefit $300 (vs. $50) | $68.85 |

| Daily benefit $175 (vs. $50) | $55.68 |

| Daily benefit $100 (vs. $50) | $51.28 |

| Duration lifetime (vs. 1 year) | $175.38 |

| Duration 5 years (vs. 1 year) | $94.83 |

| Duration 3 years (vs. 1 year) | $85.37 |

| No deductible (vs. 6 months) | -$0.32 (NS) |

| 1 month deductible (vs. 6 months) | -$3.54 (NS) |

| 3 month deductible (vs. 6 months) | -$0.37 (NS) |

| No health requirements (vs. requirements) | $27.91 |

| Private insurer (vs. federal government) | $12.16 |

| Universal plan (vs. voluntary plan) | -$105.81 |

DCE summary

- Strongest preferences (in order) for

- Cost (monthly premium)

- Benefit period (“lifetime” highly desired)

- Voluntary enrollment

- Benefit amount (mostly to avoid to the lowest level)

- Potential demand for a basic LTCI plan only slightly about 50%, even at very low cost

- Preferences may reflect some lack of knowledge about LTC needs (e.g., lifetime benefit)

- Perceived negativity of required enrollment can be offset by improvements in other desired features

- Preference figure shows more & less effective policy levers

Conclusions

- Understanding of LTSS system is low, especially Medicaid; knowledge of LTC insurance basics is better

- Multiple concerns about becoming disabled, chief being losing independence

- People willing to use some services, but prefer free informal care to services that cost money

- Many people do not have firm opinions on how LTC should be financed, but most people think LTC is an individual, rather than government, responsibility

- People favor voluntary initiatives and support policies that promote private LTC insurance, although they also support voluntary public insurance

- Little support for mandatory public LTC insurance

- The most important LTC insurance features to consumers are plan cost, benefit period, and daily/monthly benefit amounts

- Deductible period, medical underwriting, and whether the insurer is private or government are less important

- With $50-100 per month of additional benefits or subsidy people would be indifferent regarding a mandatory public plan compared with a voluntary private insurance plan