Ronald J. Ozminkowski, Ph.D., Mark W. Smith, Ph.D., Rosanna M. Coffey, Ph.D., Tami L. Mark, Ph.D., Cheryl A. Neslusan, Ph.D., and John Drabek, Ph.D.

The MEDSTAT Group

"This report was prepared under contract #HHS-100-95-0044 between the U.S. Department of Health and Human Services (HHS), Office of Disability, Aging and Long-Term Care Policy (DALTCP) and the MEDSTAT Group. For additional information about this subject, you can visit the DALTCP home page at http://aspe.hhs.gov/office_specific/daltcp.cfm or contact the ASPE Project Officer, John Drabek, at HHS/ASPE/DALTCP, Room 424E, H.H. Humphrey Building, 200 Independence Avenue, S.W., Washington, D.C. 20201. His e-mail address is: John.Drabek@hhs.gov.

The opinions and views expressed in this report are those of the authors. They do not necessarily reflect the views of the Department of Health and Human Services, the contractor or any other funding organization.

I. INTRODUCTION

A. Background

This report describes research conducted by The MEDSTAT Group for the Department of Health and Human Services, Office of the Assistant Secretary for Planning and Evaluation (hereafter referred to as ASPE). The primary aim of this study has been to explore and document the experience of persons with potentially disabling health conditions in private-sector indemnity and managed care plans. Other than general descriptive information from population-based surveys, little is currently known about this subject. This report fills a major gap in our research knowledge by presenting descriptive findings from a study of the insured populations of two large employers. Both descriptive and multivariate analyses were used to estimate the impact of managed care on health care use by privately insured populations with potentially disabling chronic conditions.

The use of managed health care by private and public payers of health care continues to grow in the United States. For example, enrollment in health maintenance organizations (HMOs) increased by about 85 percent from 1990 to 1996. By 1996 an estimated 67.5 million people (about one in four Americans) were enrolled in HMOs (American Association of Health Plans, 1998).

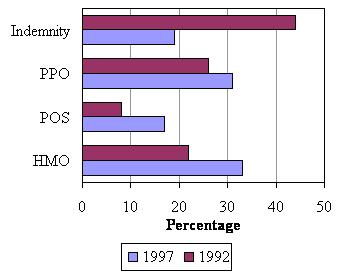

In the private sector today, more than 70 percent of workers in small and large firms choose a managed care plan (KPMG Peat Marwick, 1997; Jensen, 1997). Among firms with more than 200 employees it is now more common for a firm to offer various types of managed care plans than it is to offer traditional indemnity health insurance. Between 1992 and 1997 the percentage of enrollees covered by indemnity plans offered by large firms declined significantly from 45 percent to less than 20 percent. Conversely, U.S. employers saw substantial increases in enrollment in all types of managed care plans (Figure 1-1).

The growth of managed care has not been without concerns and complaints in recent years. Much of the shift to managed care for employees has not been optional (Center for Studying Health System Change, 1997), and some research has indicated that managed care may not be appropriate for those with special needs, such as the frail elderly and the disabled (Luft, 1991).

Despite concerns about the ability of managed care plans to meet the needs of special populations, certain aspects of managed care can offer better treatment to those with special needs. A single case manager or gatekeeper, for example, may help coordinate the myriad of patient services that is often required by persons with chronic illness or disability, and provide a better match between patient needs and service use (Batten et al., 1994). Managed care may also result in closer monitoring of the patients disease, and more appropriate use of preventive and disease management services that limit complications of disease. If successful, closer patient management may also limit the cost of care while enhancing its quality.

| FIGURE 1-1: Employees in Large Firms Covered by Managed Care and Indemnity Plans |

|---|

|

| SOURCE: KPMG Peat Marwick (1997). |

B. Why This Study Was Conducted

According to the 1989 National Health Interview Survey, about 48 percent of those with disabling conditions were treated in private-sector indemnity and managed care plans. However, very little is known about how persons with potentially disabling conditions fare in private-sector plans. Information on their demographics, case mix, service use, and outcomes is scarce in the health services literature. The ASPE Private Payers Study was conducted to learn more about how chronically ill, potentially disabled people fare in managed care plans in comparison to indemnity plans offered by large employers.

Using data from the two employers health plans, this report first illustrates similarities and differences between those covered by indemnity and managed care plans. Second, we present findings on the impact of managed care on health care utilization and expenditures for those with potentially disabling chronic conditions. Third, we illustrate the impact of various methods of risk-adjustment, in order to make inferences about the financial incentives that managed care plans faced to attract or avoid persons with chronic illness.

It is our hope that the information produced by the Private Payers Study will contribute important empirical findings to a small but growing knowledge base, so that policy makers and employers will better understand the characteristics and service needs of those with potentially disabling chronic illness. Policy makers and employers will also better understand the financial incentives and likely impact of managed care for persons with disabilities. This information will provide clues about the potential consequences of expanding managed care options in a variety of both private-sector and public-sector settings.

C. How The Study Was Conducted

Two large employers contributed data for the Private Payers Study. Employer A specializes in communications and electronics, and has offices in 30 cities around the country. Employer B is a large northeastern state government. The data used for this study included (1) health plan enrollment information for members of both employers indemnity and managed care plans, and (2) claims-based information on inpatient, outpatient and pharmacy services used in 1995 by persons covered in these managed care and indemnity plans. More information about the employers and their health plans can be found in the next chapter of this report.

One of the challenges addressed by this study was the difficulty of using only health insurance claims or encounter data to identify chronically ill persons who may be disabled. No survey data were available to identify those with functional limitations in our sample. To address this issue, a physician and clinical coding specialist identified ICD-9-CM diagnosis codes that may be associated with chronic, potentially disabling illness. After subsequent review by ASPE staff and some reconsideration of a first draft, over 320 chronic physical and mental health conditions were identified as potentially leading to serious disability. About 30 additional illnesses were identified as potentially disabling if coupled with high service use. Chapter 3 describes in more detail the process used to identify persons with these conditions.

After we identified chronically ill and potentially disabled persons in the inpatient and outpatient data bases provided by the two employers for this study, we compared the demographic characteristics, case mix, and service use of this group according to their type of coverage. For purposes of this study, managed care refers to health maintenance organizations (HMOs), point of service (POS) plans, and preferred provider organizations (PPOs). The characteristics of these plans are described in Chapter 2. Potentially disabled persons with chronic illnesses who were covered by these plan types were compared to similar persons in the indemnity plans offered by each employer. Chapter 5 presents the descriptive results of these comparisons.

Simple comparisons of demographics, case mix, and service use were supplemented with multiple regression analyses designed to estimate the impact of managed care coverage on service use and health care expenditures, controlling for other factors that may also affect utilization and expenditures. We present the managed care impact estimates in Chapter 6.

Finally, we investigated the application of risk adjustment methods for persons with potentially disabling chronic illnesses. These regression analyses were designed to estimate how much more of the variation in health care expenditures could be accounted for by different methods of measuring the case mix of the group of potentially disabled persons. We conducted separate risk adjustment analyses for physical health problems and mental health problems. The results of these analyses are described in Chapter 7 and Chapter 8, respectively.

D. How This Report is Organized

The rest of this report is divided into seven chapters.

-

Chapter 2 provides information about the indemnity and managed care plans offered by the two employers who contributed data for this study. Chapter 2 also describes earlier research on the impact of managed care for persons with disabilities.

-

Chapter 3 provides the details of the methods used to identify chronically ill, potentially disabled persons with claims and encounter data. The implications of using those methods instead of survey-based approaches are also noted.

-

Chapter 4 describes the research plan for all four analyses conducted in the Private Payers Study. These include the descriptive study noted above, along with the managed care impact study and the two risk-adjustment studies.

-

Chapter 5, Chapter 6, Chapter 7 and Chapter 8 describe the four studies in detail, offering information about rationale, data sources, methods, results, and implications.

In addition to these chapters, several appendices and a detailed reference section are included as supplementary material to the main report.

II. INDEMNITY INSURANCE AND MANAGED CARE FOR PEOPLE WITH DISABILITIES

This chapter provides background information on indemnity and managed care plans. It describes characteristics of managed care in general, provides detail on the plans offered by the two employers who contributed data for the study, and illustrates the relative costs of indemnity insurance and managed care for a hypothetical employee situation.

A. Characteristics of Managed Care

The term managed care means different things to different people. Because of this, its definition may seem somewhat vague and its operational features in one site may be quite different than its operational features in another site. The Managed Health Care Dictionary (Rognehaugh, 1996) defines managed care as "any method of health care delivery designed to reduce unnecessary utilization of services, contain costs, and measure performance, while providing accessible, quality, effective health care" (page 109). Rognehaughgoes on to note that managed health care plans do the following:

- "integrate the financing and management with the delivery of health care services to an enrolled population;

- employ or contract with an organized provider network which delivers services and which either shares financial risk or has some incentive to deliver quality, cost-effective services; and

- use an information system capable of monitoring and evaluating patterns of members' use of medical services and the cost of those services" (p. 110).

Because the methods used to produce managed care vary widely and are limited only by fairly broadly written statutes or regulations, the term 'managed care' should not be viewed as a binary (yes or no) construct. Peter Fox (1997) notes that, in reality, very little care offered in the United States is unmanaged. Today, even traditional indemnity plans typically use some care management techniques, such as precertification for hospital use, second opinion programs for surgical treatment, or other utilization review methods.

The lack of a binary distinction between various forms of managed care and indemnity plans can be seen in Table 2-1. The table notes important characteristics of the managed care and indemnity plans offered by the two employers who contributed data for the Private Payers Study. The information presented here reflects the continuum of managed care; certain types of plans fall closer to one end of the spectrum or another. For example, HMOs and POS plans tend to offer the highest degree of integration of financing and delivery, with less integration in the PPO plan and less still in the indemnity plans. Similarly, risk sharing between health plans and providers tends to be more prominent in the HMOs, less prominent in the POS and PPO plans, and nonexistent in the indemnity plans. For other measures there are more distinct differences between the managed care and indemnity plans. For example, the managed care plans use established networks of providers and either disallow or penalize out-of-network use; this is not the case for the indemnity plans. Because of the variety of methods used to integrate administrative, financial, and delivery aspects of treatment, it is often more appropriate to treat each plan type separately when analyses are completed. This is the approach we adopted in many of the analyses completed for the Private Payers Study.

| TABLE 2-1: Features of the Managed Care and Indemnity Plans in this Study | ||||

|---|---|---|---|---|

| Feature | Health Maintenance Organization (HMO) | Point-of-Service (POS) Plan | Preferred Provider Organization (PPO) | Indemnity Plan |

| Degree of organization/integration of financing and care delivery | High | High | Medium | Low |

| Plan shares financial risk with providers | Yes | With some but not all providers | With some but not all providers | No |

| Capitation is used to pay providers | Some (e.g., primary care) | Some | None | None |

| Fee-schedules or volume discounts are arranged with providers | In some but not all HMOs | In some but not all POS plans | Yes | No |

| A formal network of providers exists | Yes | Yes | Yes | No |

| Out-of-network care is paid for | No | Yes, but with penalty | Yes, but with penalty | Not applicable |

| A primary care gatekeeper is assigned | Yes | Yes | No | No |

| Specialists can be seen without gatekeeper approval | No | No | Yes | Yes |

| Pre-certification or other utilization review is applied | Yes | Yes | Yes | Yes |

| Strong emphasis on disease management programs and/or use of clinical practice guidelines | Yes | Yes | No | No |

| Strong emphasis on preventive services and wellness programs | Yes | Yes | No | No |

B. Features of the Plans Offered by the Two Employers

Two employers contributed inpatient and outpatient data for this study. Employer A is a large firm specializing in various forms of electronic products, media and communications equipment. Although it has offices in more than 30 cities across the U.S., the structure of health insurance benefits is very similar across locations. Each location offered an indemnity plan and a POS plan. The benefits offered in these plans were the same, but the POS plan required lower co-payments and deductibles and offered a wider array of preventive services than does the indemnity plan. Over 403,000 people were covered by Employer A's health plans in 1995.

| TABLE 2-2: Employer A's Medical Benefit Options, 19951 | ||

|---|---|---|

| Feature | Plan Type | |

| Point of Service (POS) | Indemnity | |

| Deductible | ||

| Individual | $0 in network $250-$850 out of network1 | $125-300 |

| Family | $0 in network $500-$1,700 out of network1 | $300-$600 |

| Copayment/Coinsurance | ||

| Individual | $15 in network 20% out of network | 20% |

| Family | $15 in network 20% out of network | 20% |

| Prescription Drug Copayment/Coinsurance | ||

| Retail Pharmacy | In network: $12 for generic, $12 plus price difference between generic and brand name Out of network: 100% | In network: 20% Lower prescription prices Out of network: 20% Higher prescription prices |

| Mail order | $4 for generic $11 for brand name | $4 for generic $11 for brand name |

| Annual Employee Out-of-Pocket Limit2 | ||

| Individual | $1,250-$2,750 out of network1 | $1,100-$2,3501 |

| Family | $2,500-$5,500 out of network1 | $1,100-$2,3501 |

| Lifetime Maximum Benefit | $1.2 million | $1.2 million |

| Yearly employee contributions | ||

| Individual | $147.76-$461.76 employees1 $0-$312 COLA and retirees1 | $174.20-$486.20 employees1 $0-$312 COLA and retirees1 |

| Family | $249.08-$548.08 employees1 $249.08 COLA and retirees | $299.08-$598.00 employees1 $249.08 COLA and retirees |

| ||

Employer B is a large state government in the northern United States. It offered an indemnity plan, a PPO plan, and ten HMO plans. Seven of the ten HMOs were available to every employee. About 205,000 people were covered by this employer's health plans in 1995. Since relatively few potentially disabled persons were found in the PPO plan in 1995, most analyses reported in subsequent chapters excluded the PPO plan members.

| TABLE 2-3: Employer B's Medical Benefit Options, 1995 | ||

|---|---|---|

| Feature | Plan Type | |

| HMOs | Indemnity | |

| Deductible | ||

| Individual | $0 | $75 $150 per admission |

| Family | $0 | $150 $150 per admission |

| Copayment/Coinsurance | ||

| Individual or Family | $10 | $5 visits 1-15 , $0 visits 16+$0 |

| Prescription Drug Copayment/Coinsurance | ||

| Retail Pharmacy | $3-$10 for generic, $10-$15 brand name | In network $5 generic $10 brand name Out of network 20% after $75 or $150 drug deductible is met for individual or family, respectively. |

| Mail order | $6 for generic $12 for brand name | |

| Annual Employee Out-of-Pocket Limit | ||

| Individual or Family | $250 | N.A. |

| Lifetime Maximum Benefit | None | Unknown |

| Yearly employee contributions | ||

| Individual | $289.92-$377.28 employees1 $193.20-$251.40 COLA and retirees1 | $495.12-$668.40 employees1 $329.28-$502.56 COLA and retirees1 |

| Family | $700.20-$885.36 employees1 $466.60-$590.28 COLA and retirees | $1115.64-$1516.80 employees1 $741.84-$1143.00 COLA and retirees |

| ||

Medical benefit options for each employer's health plans are described in more detail in Table 2-2 and Table 2-3. The annual contributions (premiums) were quite similar for Employer A's two plans. Deductibles and coinsurance rates for Employer A's out-of-network POS plan were higher than the indemnity plan but the in-network rates were substantially less than those of the indemnity plan. Employer B's indemnity plan was more costly than its HMOs, charging higher deductibles, copayments, and premiums. The HMOs did not cover out-of-network care, however, so someone seeking care outside the HMO network would be responsible for the entire payment.

A few notable plan features do not appear in Table 2-2 and Table 2-3. Employer A used the same carve-out program for mental health services in 1995 for everyone, regardless of whether the indemnity or the POS plan was chosen. In contrast, Employer B offered two mental health plans, one for the indemnity and PPO plan members, and a second plan for all HMO members. Both employers used physician gatekeepers to monitor and approve service utilization in the managed care plans. However, pre-admission approval for hospital services was required in all plans. Finally, neither Employer A's nor Employer B's indemnity plans put providers at financial risk for the services they provide to plan members. Risk assumption by providers was minimal in Employer A's POS plan, but in some of the HMOs offered by Employer B providers assumed greater financial risk.

C. Indemnity Plan versus POS Plan: An Example

There is a common misperception that enrollees will necessarily have lower out-of-pocket expenditures in managed care plans than in indemnity plans. In general, managed care plans will cost less only to the extent that the enrollee receives care from providers within the plan's network. The following example uses data on Employer A's plans to illustrate how the decision to seek care outside a provider network can substantially raise out-of-pocket expenses.

Employer A's indemnity plan had a 20 percent coinsurance rate, meaning that the employee paid 20 percent of covered health care expenses beyond the deductible. The 20 percent coinsurance rate applied to pharmacy expenses as well. The deductible ranged from $125-$300 for individual coverage to $300-$600 for family coverage, depending on the employee's salary. The annual contribution (or premium) ranged from $175-$487 for individuals and $300-$599 for families, again scaled to income.

Employer A's POS plan had a $15 copayment for care received within its network. Outside the network, there was a 20 percent coinsurance rate beyond a deductible of $250-$850 for individual coverage and $500-$1700 for family coverage, scaled to the employee's salary. That is, an employee seeking care outside the POS network had to pay the entire deductible before the POS plan contributed anything; beyond the deductible, the employee paid 20 percent of remaining out-of-network costs. The annual premium varied from $148-$462 for employees with individual coverage to $249-$548 for those with family coverage, based on salary.

Consider the hypothetical situation illustrated in Table 2-4. A chronically ill, female employee has family coverage and $1650 of eligible expenses. These include $250 for four 90-day prescriptions purchased at a pharmacy, five visits to specialists and five visits to general practitioners or other providers. Assume she has an average salary and thus has midpoint values for the deductible and premium that she faces. Under the indemnity plan, her annual expenses would be the sum of the premium ($449), the deductible ($450) and the copayment ($240), a total of $1139. Now suppose that the woman belongs to the POS plan and receives all of her care within its network. Then her annual expenses would be the sum of the premium ($399), the deductible ($0) and the copayments (which are the sum of $150 for ten in-network visits and $48 for four prescriptions), a total of $597. This is little more than one-half the cost for care under the indemnity plan.

Suppose instead that the woman prefers to receive care by a specialist who does not belong to the POS plan list of preferred providers. Let the five visits to the specialist account for $1000 of the $1400 in non-prescription expenses. What will the total yearly cost be now? Assume that her deductible for out-of-network providers is $1100, the midpoint between $500 and $1700. The $1100 deductible exceeds the $1000 in actual out-of-network specialist costs, so she will pay the entire $1000 out of her own pocket. Her total yearly expenditures will be the sum of that deductible ($1000), copayments for the five remaining in-network visits ($75) and copayments for the four prescriptions ($48), a total of $1522. This exceeds the cost of care under the indemnity plan by 34 percent. Thus we see that the cost difference between POS and indemnity plans depends on the employee's willingness to visit only those providers in the POS network.

| TABLE 2-4: Expenditures under Indemnity and POS Plans: An Example | |||

|---|---|---|---|

Hypothetical Situation

| |||

| INDEMNITY | Premium: Deductible: Coinsurance: Total | $449 $450 $240 $1139 | [ = 0.20 * ($1650 - 450)] |

| POS IN-NETWORK ONLY | Premium: Deductible: Coinsurance: Total | $399 $0 $198 $597 | [ = (10 * $15) + (4 * $12)] |

| POS SOME CARE OUT-OF-NETWORK | Premium: Deductible: Coinsurance: Total | $399 $1000 $123 $1522 | [ = (5 * $15) + (4 * $12)] |

D. Conclusion

Both employers' health plans used a variety of requirements and case management procedures to manage care. Since all persons covered by any given plan were subject to the same requirements, one cannot determine from the data used in this study which particular feature had the most influence on service utilization or expenditures. Data from many more plans would be required for such a study. Moreover, in order to determine which plan features have the most influence on service use and costs, such plans would have to share some common features but differ with regard to other important features. In the same vein, without such a rich data source we are unable to determine which specific plan features may be most useful and appropriate for a chronically ill population.

The analyses conducted under the Private Payers Study will show the impact of managed care at an aggregate plan-type level, combining the influence of all of the managed care features of a given plan type under the same 'managed care' rubric. This procedure is typical of the indemnity versus managed care plan comparisons reported in the health services literature.

III. OPERATIONAL MEASUREMENT OF CHRONIC ILLNESS AND POTENTIAL DISABILITY FOR THE PRIVATE PAYERS STUDY

The Private Payers Study was undertaken to compare the characteristics, health service utilization patterns, and expenditures of people with potentially disabling chronic conditions in managed care and indemnity insurance plans. An important issue is the appropriate definition of potential disability that underlies all empirical analyses conducted for this project. The health services literature offers a variety of definitions of the term disability, and this chapter begins with a description of those definitions. We then relate those definitions to methods chosen for this project to define people with potentially disabling chronic conditions using claims data. In concluding this chapter, we describe several additional options for defining potentially disabled people, and note our reasons for not using these options for this study.

A. Defining Disability

LaPlante (1989) and others (Haber, 1967; Nagi, 1976) define disability as a limitation, caused by one or more chronic physical or mental health conditions, in performing activities that people of a particular age are generally expected to be able to perform. For children, these activities might include playing and going to school. For adults, these activities might include employment or running a household.

LaPlante (1989) notes that chronic conditions are the antecedents of disability, yet there are many chronic conditions that differ in terms of functional limitations, prognosis, care management, and rehabilitative potential--factors that relate to or describe the nature of a disability. Because of differences in age, other physical and socioeconomic factors, motivation levels, environmental factors, treatment resources, duration of the underlying illness, and care management patterns, two people with the same chronic condition of equal severity may not have equal levels of disability. For example, severe arthritis may be devastating for a surgeon, but not as much of a limitation for a writer who has a computer and voice recognition software. Thus, the mere existence of a chronic condition is not sufficient to specify the degree of disability that people face in their own situations.

Because of the range of factors that influence perceptions of disability, disability research frequently relies on surveys. Some examples, cited by Irvin et al. (1994), include the Current Population Survey, the Survey of Income and Program Participation, and the National Medical Expenditure Survey. LaPlante (1989) describes the usefulness of the National Health Interview Survey for disability studies. As Irvin et al. (1994) note, disability research relies on self-reports of health-related limitations in activities and work based on these surveys, and on participation in government programs for disabled people that require certain medical or functional status criteria to be met (see, for example, Burkhauser,Haveman, and Wolfe, 1992; Haveman, Wolfe, Buron, and Hill, 1992; Wolfe and Haveman, 1990; Haveman and Wolfe, 1983; and Colvez and Blanchet, 1981). With the exception of the National Health Interview Survey, the surveys that support this body of research often do not provide information about the pathology or impairment underlying the self-report, or they do not link functional limitations to specific conditions (Irvin, et al., 1994).

While survey data are necessary for assessing the degree of disability that individuals face, one formidable obstacle to the use of survey data should be noted--survey respondents may not always respond accurately or in the expected manner. This may be due to confusing wording of survey questions, lack of complete response categories, a respondent's unwillingness to divulge information, or other problems. In their own study and in many other studies which they reviewed, Fowles et al. (1998) note that the accuracy of self-reported data on the existence of chronic diseases varies substantially with the type of disease. Although the Fowleset al. study does not deal specifically with disabling conditions, the tendency of respondents to underreport chronic conditions is likely to translate into an underestimate of disabling conditions as well.

Using medical records data as a gold standard, Fowles et al. found that low sensitivity (i.e., underidentification of those with a disease) was particularly problematic, usually more often for self-reported data than for data coming from insurance claims. However, some conditions are not well defined in that article (e.g., alcohol abuse, digestive problems, joint problems) and most conditions had a low frequency of occurrence.

Irvin et al. (1994) note that research incorporating both self-reported limitations and specific medical conditions has broadened operational definitions of disability. These broader definitions attempt to capture the multi-dimensional nature of disability. Nagi(1969, 1979) argues that this multi-dimensional nature should include the elements of "pathology" (the presence of a physical or mental malfunction), "impairment" (physiological, anatomical, or mental losses or abnormalities that limit a person's capacities and level of functioning), and "disability" (inability or limitations in performing roles and tasks that are socially expected). Haveman, de Jong, and Wolfe (1991) consider the multi-dimensional nature of disability using a disability index.

Irvin, et al. (1994) used data from the National Medical Expenditure Survey to identify four different groups of disabled people. These groups were not mutually exclusive. The first group included those with chronic conditions and impairments reported during a medical visit. A second group included those who self-reported one or more limitations in activities of daily living (e.g., bathing, toileting) and those who reported that their health limited moderate or vigorous physical activity. A third group of disabled people was defined as those respondents who reported that their health limited the kind or amount of work they could perform. A fourth group included respondents who reported that their health prevented them from working at all. When all four groups were combined, Irvin et al. (1994) found that they represented approximately 40 percent of the 1987 National Medical Expenditure Survey sample of working age individuals. Irvin et al. (1994) note that definitions of disability range from broad constructs reflecting social and economic conditions and self-perceptions to tightly defined physical and mental conditions entailing the application of strict medical criteria. However, all of these measures are based on subjective measures of pathologies or impairments.

LaPlante (1989) cites research showing that about one-half of the U.S. population aged 18-64 has at least one chronic physical or mental health condition, but only about 15 percent of that group have one or more activity limitations. Thus, LaPlante notes: It is a simple fact that most people with chronic conditions are not limited in activity, nor do most conditions cause disability (page 20).

B. Using Claims Data to Define Potentially Disabling Chronic Conditions

Survey data were not available for the Private Payers Study, so the identification of potentially disabled people was based primarily on information available in the insurance claims databases contributed by the two participating large employers. Claims data contain a wealth of information on individual utilization of health care services, expenditures, diagnosis codes, and procedure codes that can be used as indicators of potential disability status. Although there is much literature focusing on the health care utilization and expenditures of Medicaid and Medicare beneficiaries, the use of claims data to study the health care utilization of people who may be disabled is much more limited.

Previous studies of the health care utilization of Medicaid and Medicare beneficiaries with disabilities have generally focused on program eligibility status (e.g., Medicare enrollees under age 65 or Supplemental Security Income (SSI) beneficiaries) as the indicator of disability. Recently, however, studies using Medicaid claims data have attempted to identify disabled people using criteria beyond program status alone (e.g., Crown et al., 1998a, 1998b; Kronick, et al., 1995). These studies focused on diagnosis codes and utilization criteria for identifying people with disabilities. Diagnosis code and utilization criteria are particularly appropriate for the Private Payers Study because these criteria can be used to identify people with potentially disabling chronic conditions from private health insurance claims, where program eligibility criteria, such as SSI or Social Security Disability Insurance (SSDI) status, are lacking.

The use of claims data for studying the health care utilization of potentially disabled people has several advantages. First, it enables researchers to study very large samples, and sometimes even entire populations, rather than relatively small samples of populations. This can be important when focusing upon certain types of disability which may be very rare. Second, health care claims data are not subject to self-reporting biases on the part of individuals (although they may be subject to other reliability problems). Third, and most importantly, claims data provide the opportunity of studying the total pattern of health services and expenditures of people who may be disabled.

The use of claims data for studying the health care utilization of disabled people does have limitations. For example, diagnosis codes may not always indicate the nature of a person's disability (e.g., an individual with severe mental retardation might have an office visit for an inner ear infection, with the former not noted as a diagnosis on the claim). In some situations, it is possible to address this problem by linking with other data sets. For example, by linking Medicaid data for SSI recipients with Social Security data on impairment codes, it is often possible to identify type of disability for many individuals even though it is not indicated in the claims. On the other hand, this linkage solution may not be feasible for employer health insurance data due to confidentiality restrictions and because very few enrollees are covered by SSI or SSDI. Even so, one would expect to see severe disabilities reflected in diagnosis codes over a longer period of time, such as a year.

A second limitation of claims data is that they generally contain very limited socioeconomic or demographic information on the individuals represented in the claims. This can place limits on the range of policy questions that can be addressed. For example, information on race is not available in the two employer data sets used for the Private Payers Study. Studies of race-related differences in access to care or treatment patterns among disabled people are therefore precluded.

A third limitation relates to reporting practices used by diagnosis coders. Like survey respondents, clinicians may hesitate to report the existence of sensitive conditions, such as mental or emotional problems.

Finally, as noted earlier, insurance claims which denote the existence of a chronic condition generally cannot be used to estimate the degree of disability associated with that condition. Thus, for the Private Payers Study, we refer to the samples included in the empirical analyses as those having potentially disabling chronic conditions, rather than using the more definitive-sounding term, disabled.

C. Overview of Approach with Claims Data

Because the data source for the Private Payers Study includes health insurance claims from employers, the criteria used to define those with potentially disabling chronic conditions rely heavily on diagnosis codes available from the claims data. In an earlier paper for the Private Payers Study, Crown et al. (1998a) developed criteria to identify disability using both physical and mental health criteria. Many diagnosis codes for physical and mental conditions indicate a potentially disabling chronic condition by themselves. Others indicate disability only in the presence of corroborating patterns of utilization. Although there are broad areas of overlap in the criteria for children and adults, some conditions are specific to each group.

To develop the lists of particular diagnoses that indicate potentially disabling chronic conditions we used the following process. First, a clinical coding specialist selected conditions thought to potentially result in partial or total disability. Any conditions known to be invariably terminal within six months were excluded from consideration because the focus of this research was on chronic conditions expected to last for a long time, and because the managed care literature rarely focuses on plan type comparisons for those with terminal illnesses. The rationale for the selections made by the clinical coding specialist was her clinical knowledge as well as data gleaned from leading medical reference texts. Her preliminary list of conditions was forwarded to a consulting physician for review of the appropriateness of inclusion. The physician was an internist in clinical practice with experience in making disability determinations on a regular basis. Together, the clinical coding expert and the internist attempted to identify all conditions that may, in and of themselves or as a result of their complications, lead to permanent or temporary disability and inability to perform regular gainful employment. For children, the conditions are those that restrict their usual daily activities, such as play and school attendance.

As they make disability determinations for their patients, most primary care physicians make these same types of judgments about restriction of activity on a daily basis. After review by ASPE staff and subsequent review by the MEDSTAT clinical coding specialist and internist, a few modifications to the list of qualifying diagnoses were made.

According to this approach, potential disability may be on the basis of either mental or physical problems that result in loss of normal functioning. Considerations taken into account when making disability determinations for patients with mental disorders typically include whether the patient is capable of conducting work independent of supervision or direction, of making sound judgments, and of being sufficiently independent to take care of one's own grooming and daily needs. Potential physical disability is a physical problem that meaningfully interferes with the patient's ability to conduct his/her usual work, and often is based on changes in endurance, coordination, strength, flexibility, or because of chronic pain or severe chronic illness. Severity of illness and disability varies among the coded disability conditions and cannot be assessed by the code alone. For some conditions, other factors such as health service utilization patterns are noted to help increase the likelihood that the existence of the condition is disabling.

1. People with Potentially Disabling Chronic Physical Illness in This Study

Table 3-1 (from Crown et al., 1998a) provides a summary of the diagnoses and utilization criteria used to identify children and adults with potentially physically disabling chronic conditions. The diagnostic summary in Table 3-1 refers to the detailed list of ICD-9-CM codes in Appendix A that indicated the presence of severe and potentially disabling chronic physical conditions.1 These diagnoses are presented for children and adults separately. The set of per se disabling diagnoses is noted by a Yes in the third column of Appendices A-1 through A-4.

| TABLE 3-1. Physical Disability Criteria |

|---|

| Diagnoses Alone (Per Se Disabling Conditions) Has at least one of 328 diagnosis codes for severe and chronic conditions, as either primary or secondary diagnoses. The composition of these diagnosis codes differs for children and adults. (See Appendix A-1 and Appendix A-2) |

| Diagnoses with Utilization Criteria Has a primary diagnosis of asthma in combination with 2 or more hospitalizations, or 3 or more emergency room visits with a primary diagnosis of asthma; or Has a primary diagnosis of epilepsy in combination with 1 or more hospitalizations, or has 3 or more emergency room visits with a primary diagnosis of epilepsy; or Has any of selected adult primary diagnoses (noted in Appendix A-1) in combination with 1 or more hospitalizations or 3 or more emergency room visits. |

The second set of criteria in Table 3-1 refers to diagnoses of asthma and epilepsy in conjunction with utilization criteria. Children or adults with asthma were considered as potentially disabled only if they had at least two hospitalizations or at least three emergency room visits with a primary diagnosis of asthma. Similarly, adults and children with epilepsy were considered disabled only if they had one or more hospitalizations or three or more emergency room visits with a primary diagnosis of epilepsy.

2. Potentially Disabling Chronic Mental Illness in This Study

Exhibit 3-2 outlines diagnosis code and utilization criteria that were used to identify children and adults with potentially disabling chronic mental illness. As with physical disabilities, certain mental diagnoses such as schizophrenia or moderate, severe, or profound mental retardation are nearly always disabling. Other diagnoses such as depression or panic disorders are generally only disabling if they occur in conjunction with comorbidconditions or if the severity of the diagnosis is indicated by utilization criteria. Thus, Table 3-2 includes two mental health disability screens based on a broader set of mental health diagnoses in conjunction with utilization criteria. The specific ICD-9-CM mental illness diagnoses used for these criteria are listed in Appendix A-3 and Appendix A-4.

| TABLE 3-2. Mental Disability Criteria |

|---|

| Diagnoses Alone (Per Se Disabling Conditions) Schizophrenic or schizoaffective disorder Manic depression or bipolar disorder Psychoses with origin specific to childhood Mental retardation: moderate, severe, profound Anorexia nervosa |

| Diagnoses With Comorbid Conditions Depression with anxiety disorder Substance abuse with secondary psychiatric disorder Panic disorders with substance abuse |

Diagnoses With Utilization Criteria Depression with any of these:

|

D. Taking Advantage of Survey-Based Information

In addition to the method above based on clinical judgment, we also used a method based on survey responses to identify activity-limiting conditions. A subset of potentially disabling chronic conditions highly correlated with disability was identified in LaPlante's (1989) analysis of the National Health Interview Survey. In LaPlante'sanalyses, disability was based upon limitations in daily activities or work, or the inability to work. He determined the most common chronic conditions, in terms of disability risk, for children and adults in 1983-1986. Those conditions are noted in the fourth column of Appendices A-1 through A-4 of this report. In the Private Payers Study, people with these activity-limiting conditions were identified on the basis of their ICD-9-CM diagnosis or condition codes. Chapter 5 notes that, depending upon the plan type considered, about 30-60 percent of the analytic sample members used in the empirical analyses for the Private Payers Study had one or more of the activity-limiting conditions.

LaPlante's conditions for children and adults differ from each other for the most part, as may be seen in Appendices A-1 through A-4. Only four conditions appear among the top 20 for both children and adults: mental retardation, cerebral palsy, epilepsy, and other heart conditions. For both age groups, mental retardation was the condition most likely to lead to disability. Musculoskeletal impairments appeared to be more common among adults, while asthma and impediments of speech and hearing appeared to be more problematic for children. Because of these differences, analyses of children and adults were conducted separately in the Private Payers Study.

E. Alternative Approaches Not Used

Three other options were considered but not adopted to identify people with potentially disabling chronic conditions for the Private Payers Study. These included the method used by the Social Security Administration (SSA) to define disability, the International Classification of Impairments, Disabilities, and Handicaps (World Health Organization, 1980), and a method used in earlier research by Altman and Barnett (1996). These methods were not used either because ICD-9-CM mappings could not be made or because the method could not be applied to all ICD-9-CM codes. These methods might be relevant in the future for other studies, however, so we describe them briefly below.

1. The Social Security Administration Approach

Another option which does not rely on survey data is the list of medical problems used by the SSA to identify those with disabling conditions (SSA, 1995). This condition list--approximately 150 pages long--is divided into separate sections for each body system--patients with any of these conditions meet SSA requirements regarding the disabling nature of their medical problems. One problem with this list is that SSA has not assigned ICD-9-CM diagnosis codes to the condition on the list. Furthermore, many of the SSA criteria are much more specific than the ICD-9-CM coding system, making a one-to-one translation impossible. Therefore it is not possible to replicate the SSA approach with the data contributed by the two employers who took part in the Private Payers Study.

2. The International Classification of Impairments, Disabilities, and Handicaps

The International Classification of Impairments, Disabilities, and Handicaps (ICIDH) was developed in the 1970s and released by the World Health Organization in 1980. The ICIDH was developed to classify patients according to the consequences of their diseases or conditions (World Health Organization, 1980). Clinicians who use the ICIDH must ask probing questions about the nature of patients' problems and how those problems limit social and functional status. Thus, the ICIDH holds some potential as a means of bridging the gap between the type of information available from ICD-9-CM diagnosis codes and the information requested on many disability surveys.

Unfortunately for the Private Payers Study, the ICIDH is still considered a work in progress. It is in the process of being updated to better address the potential for negative consequences associated with the use of the term handicap, and it is not in widespread use by clinicians in the United States. Because it was not used by providers affiliated with the employers who contributed data for the Private Payers Study, the ICICH could not be used to identify potentially disabled people for this study.

3. The Altman and Barnett (1996) Approach

Another example of methods that may be used to identify those with potentially disabling chronic conditions was described recently by Altman and Barnett (1996). Altman and Barnett developed a list of life-threatening conditions, chronic conditions, mental health conditions, impairments, and conditions with severe pain, and then related these conditions to variations in employment status. Altman and Barnett provided a list of ICD-9-CM diagnosis codes to define these types of disabling conditions. They also defined other types of disabling conditions that require the use of survey data. Their work showed a high degree of variation in employment history according to the definition of disability chosen. Altman and Barnett did not recommend a single best way to define disability status, and implicit in their work is the message that a variety of ways should be tested to determine the sensitivity of results according to the definitions chosen.

The Altman and Barnett approach is attractive because of its recognition that the various types of disabilities they define are likely to influence health care service use differently. Their approach is also helpful in that they found a useful way to group a wide variety of chronic conditions for analysis. Applying the Altman and Barnett approach for the Private Payers Study would require additional work, however, because their approach was based only on the diagnoses found in the National Medical Expenditure Survey; other diagnoses not defined by the National Medical Expenditure Survey respondents were not covered. Depending upon the scope of diagnoses identifiable in the National Medical Expenditure Survey, a substantial amount of clinical input may be required to make their approach more comprehensive. For our study, however, we considered the added value of that effort to be limited, since MEDSTAT clinical staff had already reviewed the entire ICD-9-CM manual to identify disabling conditions.

F. Diagnoses with Utilization Criteria and Disability Status

The claims-based disability indicators described earlier for some conditions included combinations of diagnosis codes and utilization measures to define potential disability status. However, circularity may be problematic in cross-sectional analyses of utilization or expenditures that compare fee-for-service versus managed care samples if many of those sample members were selected for the study mainly on the basis of utilization criteria. Circularity would be problematic if utilization-based factors drove the plan choice, if subsequent utilization were not controlled well by the plan, and if utilization indicators were used to cast judgments about plan efficiency or outcomes. Inferences about the impact of utilization on plan choice can be made by disaggregating the sample into those identified as potentially disabled solely on the basis of diagnosis and those identified on the basis of diagnosis and utilization criteria. Separate analyses can be conducted for these groups and comparisons across groups can be made to see if the impact of managed care on utilization and expenditures differs for people who were potentially disabled solely because of their diagnoses versus people whose potential disabilities depended upon utilization criteria. In Chapter 6, Chapter 7 and Chapter 8 we study a range of conditions, some identified as potentially disabling on the basis of a diagnosis alone, and others on the basis of both diagnosis and utilization. An alternative approach would be to exclude those whose potential disabilities were defined according to diagnosis and utilization factors (as was done in Chapter 6), but this approach would not have allowed useful comparisons to be made.

G. Summary

The Private Payers Study analyzed the health care utilization and expenditures of people with potentially disabling chronic conditions in private health plans. We chose two alternative methods to define this group. Both used medical claims data to identify utilization and illness. One method relied on the clinical judgment of health care experts to identify diagnosis codes and utilization patterns that indicate probable future disability. The second method drew on a national survey to determine diagnosis codes corresponding to ability-limiting conditions--that is, those conditions often accompanied by limitations in activities of daily living. By comparing results from these two sources, the Private Payers Study presented a reliable picture of the experiences of people with potentially disabling chronic illness and illustrated how the choice of definition altered the estimated prevalence in the privately insured populations we studied.

IV. RESEARCH OVERVIEW: FOUR STUDIES OF MANAGED CARE FOR PEOPLE WITH POTENTIALLY DISABLING CHRONIC CONDITIONS

A. Introduction

Chapter 1 noted that nearly half of those with disabilities are enrolled in private sector health care plans, yet little research has been conducted on their experiences in those plans. Managed care has been touted as having great potential for those who have disabling chronic illness, since one case manager or gatekeeper can take responsibility for guiding patients through the maze of services and providers that may be necessary to treat chronic conditions. Managed care has also been equated with managed cost, however, implying that more consideration is given to reducing the cost of providing care than to the needs of the patient. Both goals--reducing inefficiencies to control costs and managing care to promote quality--are laudable and not necessarily conflicting. To judge whether managed care is beneficial for people with chronic illness, it is important to have a clear understanding of their experiences in private sector health plans.

There are relatively few studies of the experience of people with disabilities in private sector indemnity and managed care plans, and thus we start by addressing basic issues. The insights gained will lead to more focused questions to be examined in subsequent research. The next four chapters of this report describe studies we conducted with data provided by two large employers. A brief overview of these studies is offered below.

B. The Four Studies

The four studies we conducted were designed to illustrate how people with potentially disabling chronic conditions fare in private sector indemnity and managed care plans. Specifically, we sought to determine how such people in these plans differed in terms of:

- prevalence,

- demographic characteristics,

- the types of chronic conditions they have,

- health care utilization and expenditures, and

- their incentives to enroll in indemnity or managed care plans.

Finally, we analyze the usefulness of risk-adjustment systems as methods to evaluate competing health plans and to help plans estimate the costs of treating people who may be high service users.

Study No. 1: Characteristics of People WithPotentially Disabling Chronic Conditions in Indemnity and Managed Care Plans

This study (reported in Chapter 5) provides information on the demographic, employment, case mix, service use, and expenditure characteristics of people with potentially disabling chronic illness in the health plans offered by two large employers. The study does not try to assess causality and does not estimate a managed care impact on service use or expenditures. It simply provides a first look at the data in order to outline the characteristics of a large group of chronically ill people.

Chapter 5 provides information separately for children, adults under the age of 65, and early retirees. We find that rates of potentially disabling chronic illness vary by age group and retiree status and that the major conditions were similar across the two employers. While the results suggest that people with chronic conditions tend to favor the indemnity plans, these plans are not necessarily associated with greater service use.

As a purely descriptive study, Chapter 5 may raise more questions than it answers. This is entirely appropriate, however, since one may not know which questions are important without conducting a detailed first look at the data as illustrated in that chapter. Three of the more important questions raisedby the descriptive study are those addressed in the remaining studies.

Study No. 2: The Impact of Managed Care on Utilization and Expenditures of People with Potentially Disabling Chronic Conditions

Chapter 6 examines whether people with potentially disabling chronic conditions selectively enrolled into more generous forms of health insurance. Specifically, we examine plan switching behavior among people with potentially disabling conditions and determine whether those who switch to more generous plans have higher utilization. This chapter also assesses the impact of membership in managed care versus indemnity-type coverage on service use and payments levels. To isolate the managed care impact, the approach that we used adjusted the overall differences in use and payments across the plans for confounding factors. In particular, variation in patient characteristics that were available in the data (such as age), as well as variation in factors that were unobservable but correlated with the patient's choice of plan (such as the propensity to seek care), were removed from the overall estimates of differences in the levels of utilization and payments.

The descriptive evidence on plan switching suggests that, as a group, switchers to managed care were relatively healthier and generally used fewer services than the individuals that stayed in the indemnity plans. The full analysis shows that enrollment in managed care as opposed to indemnity-type insurance generally reduced service utilization and expenditures. Based on the distribution of patients across the plan types, we found some evidence from one employer that there may be increasing pressure on the indemnity option to raise premiums or reduce services through time. For the other employer, our results suggest that some of the patients who were inherently higher users of health care services may have viewed the indemnity plan as too expensive compared to the managed care plan.

One important finding from this study is that managed care did not have a uniform influence on utilization and expenditures. More research is warranted into why managed care influences some types of health care use and payments but not others. At the least, the findings suggest that a blanket policy of favoring managed care over indemnity coverage is not the best approach for providing health care for people with potentially disabling chronic conditions.

Study No. 3: Risk Adjustment for People with Potentially Disabling Chronic Conditions

Chapter 7 investigates the ability of leading risk-adjustment systems to predict the expenditures of those having selected chronic conditions. Better payment methods can mitigate the incentives faced by patients and health plans to engage in strategic behavior. Risk-adjustment has been proposed as a method to accomplish this objective. Risk-adjustment refers to more precise methods of payment to health plans--methods that account for the above-average cost of treating people who are expected to use unusually high levels of services. Comparisons were made to simple adjustments for age, gender and wage rates, since these are commonly used by insurance plans to predict expenses and by major employers to set payments to insurance plans.

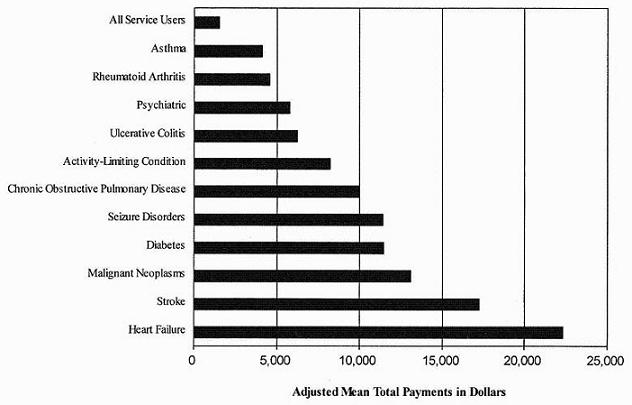

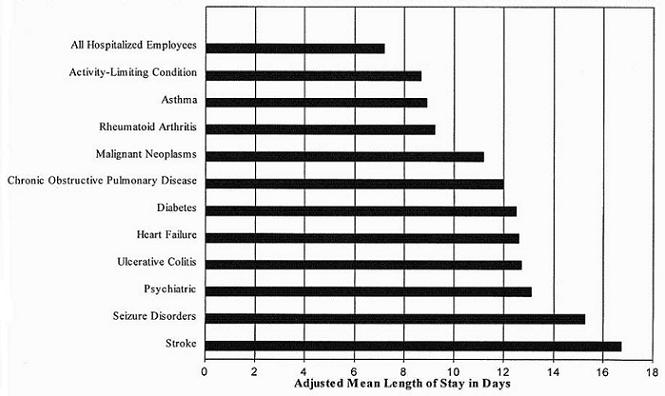

The risk-adjustment systems that we compared were Hierarchical Coexisting Conditions (HCCs), Adjusted Diagnosis Groups (ADGs), and Adjusted Clinical Groups (ACGs). We used these systems to study ten types of potentially disabling chronic conditions: rheumatoid arthritis, asthma, cancer, chronic obstructive pulmonary disease, diabetes, heart failure, psychiatric disorders, seizure disorders, stroke, and ulcerative colitis. The results suggest that health plans and employers should use risk-adjustment methods in addition to traditional age, gender and wage adjustments, especially if they cover services used often by people with potentially disabling chronic conditions. Yet while risk-adjustment would improve payment methods for those with chronic illness, inequities would still remain.

Study No. 4: Risk-Adjustment of Capitation Payments to Behavioral Health Care Carve-Outs: How Well Do Existing Methodologies Account for Psychiatric Disability?

Chapter 8 focuses on risk adjustment for people with psychiatric conditions. It uses 1994 and 1995 data from Employer B to examine the viability of Diagnostic Cost Groups (DCGs--a precursor to HCCs) and ACGs for setting capitation payments to the behavioral health care carve-out plan used by that employer. The carve-out plan was responsible for all of the psychiatric care delivered by the indemnity and PPO plans used by Employer B.

As in Chapter 7, using variants of DCGs or ACGs to risk-adjust expenses resulted in projected payments that were much closer to actual mental health and substance abuse expenditures than were projected payments derived from simpler adjustments. In addition, the study investigated alternative rules for setting risk-adjusted payments. Three alternatives were included:

- full capitation, in which plans receive a set payment for each enrollee, regardless of actual expenses incurred;

- mixed systems, which combine capitation with reimbursement based on actual expenses; and

- soft capitation, in which profits or losses from full capitation are shared by the plan and the employer.

The results showed that full capitation may still lead to substantial profits or losses, even after risk-adjustment. Mixed models and soft capitation performed much better but also diminished some of the incentives for cost containment.

These four studies show that people with potentially disabling chronic conditions use more health care services than the total population, have higher expenditures, and thus are more difficult to insure. The potential for improving their insurability exists with risk-adjustment systems available today and these systems have potential for further improvements. At the same time, while people with potentially disabling chronic conditions are more likely to choose indemnity health insurance, they also enroll in managed care in large numbers. When this differential enrollment is taken into account, the result is that managed care does not necessarily result in less cost and lower utilization. Sometimes it does, sometimes it does not. Purchasers of group health insurance who have substantial populations with disabling conditions would do well to investigate the incentives and results of specific plans to be sure they are getting the best value and highest quality from their health insurers.

V. CHARACTERISTICS OF PEOPLE WITH POTENTIALLY DISABLING CHRONIC CONDITIONS IN INDEMNITY AND MANAGED CARE PLANS

A. Introduction

Chronic illness and associated disability are common among working Americans and their dependents. While researchers have extensively studied the impact of managed care systems on the use and cost of health services in general, they have focused little attention on the impact on chronically ill individuals. These individuals are more likely to use services, and their health care needs may differ from those of the general population due to access difficulties caused by limited physical mobility or mental functioning. Corporate leaders and policymakers need information about the health care experiences of chronically ill people to judge whether current health systems perform adequately for this group. Furthermore, they need simple, straightforward statistics to serve as benchmarks for comparison to their own disabled or chronically ill employees.

This chapter meets these needs by presenting descriptive analyses of the demographics, employment status, case mix and service use of chronically ill people with private insurance. This information serves two purposes. First, it serves as a point of comparison for corporate and public officials assessing the availability and quality of care for the chronically ill in the systems they control. Second, it frames and guides the more advanced statistical analyses presented in later chapters.

Subsequent chapters of this report examine in greater detail the issues raised here. Chapter 6 investigates the impact of health plan type on utilization and expenditures, controlling for differences among those enrolled in different types of plans. Its findings should facilitate discussions of policies designed to enhance access to high-quality health care services for chronically ill individuals.

The second and third studies are natural extensions of the first. Chapter 7 analyzes whether risk-adjustment systems for individuals with diverse chronic health problems will enable employers and health plans to predict expenditures for those with chronic illness. Chapter 8 assesses whether risk-adjustment methods for people with chronic mental illness will allow health plans to predict accurately expenditures for that population. The results of these two studies will assist public and private policymakers to improve access to all types of health plans. The results will also help health plan administrators who want to learn about better methods for assessing the financial risks of enrolling chronically ill people.

In this chapter, we provide some relevant background information on managed care for people with potentially disabling chronic illnesses. Next we describe the methods used to create the descriptive profile. Then, we present results of the descriptive analyses. We conclude by comparing our results to those of other studies and by offering suggestions for additional research.

B. Background

Although estimates vary depending on how disability is defined, roughly 14 percent of adults between the ages of 18 and 65 experience a disability that limits their functional activities (Adler, 1995). Estimates of the percentage American children having special health care needs due to chronic illness or functional limitations vary widely, from 7 percent (Adler, 1995) to nearly 31 percent (Harris-Wehling and Ireys, 1995). Children and adults under the age of 65 constitute about 60 percent of the population of Americans with disabilities (Adler, 1995).

Chronically ill and disabled individuals often require a broad range of health and social services to maximize functional well-being, improve health status and avoid institutionalization. The range of services needed varies depending on the physical or cognitive condition that causes the disability. These specialized needs are often met through multiple programs that have different funding sources and routes to eligibility. As a result, the system from which people with disabilities receive health and social support services is often fragmented.

Managed care health plans cover about 48 percent of disabled people in the U.S. (Fama, Fox, and White, 1994). Policymakers and researchers have argued both that the net effect of managed health care on people with disabilities is positive and that it is negative.

On the positive side, managed care models have been proposed as one way to improve the efficiency and effectiveness of health care services delivered to individuals with disabilities (Batten and Bachman, 1994). They rely on the gatekeeping role of a primary health care professional as the key to regulating costs and ensuring access to coordinated care. Because services delivered through managed care have the potential to be more efficient and of equal or higher quality than traditional fee-for-service medicine, it also holds the potential to improve health services delivery and financing for people with disabilities. Health outcomes for a disabled individual may improve if all services and supports are provided through a single case manager.

On the negative side, the usefulness of managed care models in providing services to people with disabilities has been questioned because these individuals have complex needs for health care and social support--needs that may not be met in a financing and delivery model which has strong financial incentives to reduce costs (Luft, 1991). This concern is particularly important for the increasing number of state Medicaid programs which are turning to managed care in order to control expenditures and increase quality of care for disabled populations.

Private and public payers have implemented many changes in service delivery and financing changes based on a broad range of managed care models. Despite the growing interest of public and private payers in expanding managed care enrollment to include chronically ill people, there are little data available on their needs or experiences in either public or private managed care plans. At a time of rapidly rising enrollment of Medicaid and Medicare enrollees in managed care, federal and state policymakers must learn more about the impact of managed care on chronically ill individuals in order to make informed public policy decisions.

Although about half of disabled individuals are covered by managed care plans in the United States and most of those are employer based, we know of no studies that quantify the impact of managed care on chronically ill people covered by private employer-based insurance. Thus, this chapter is the first to analyze private insurance databases with respect to the chronically disabled population. We address important policy questions including these:

-

Are chronically ill people more likely to enroll in one type of plan or another?

-

Do those in managed care plans and those in indemnity plans have similar types of chronic illnesses and disabilities?

-

How does health care utilization vary by type of managed care plan?

-

Do those in managed care plans have lower health care expenditures than those in indemnity plans?

C. Methods Overview

In this chapter, we address the questions above through a descriptive profile of chronically ill people in the indemnity and managed care plans offered by two large employers. The profiles include:

- disability prevalence estimates for the employee population,

- demographic characteristics of those who used services,

- inpatient case mix,

- outpatient case mix, and

- expenditures of those who used services.

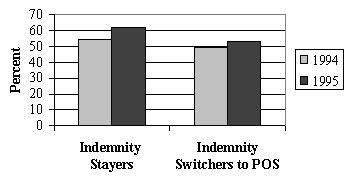

These measures were calculated separately for each plan type to facilitate comparisons between those in indemnity plans and those in managed care plans. We also study individuals in each plan type separately from those who switched plan types from 1994 to 1995 because switching may denote dissatisfaction with premiums, out-of-pocket costs, coverage, perceived access to care, quality of care, or other plan features that cannot be measured directly. Those who remain in the same plan type over time may be less concerned about these issues, or they may be more savvyabout using managed care services to obtain the care they want. In some instances, managed care may involve a tradeoff between access to particular providers versus much lower out-of-pocket costs or better benefits.2 We put all people who switch plans into a single category, not because they are a uniform group but because doing so allows us to define a clean group of stayers--people who stayed with the same plan over both years--versus those who did not. The characteristics and types of plan switchers are discussed in Chapter 6.

We also present data separately for three groups of insured people: children under age 18, active employees, and early retirees. Stratifying by age group is important because, as shown below, the groups have different rates of potentially disabling chronic illness. Moreover, some of these conditions are defined for children only, and the frequency of the remaining conditions varies across age groups.

For these analyses, the data come from two employers. Employer A is a large firm with offices in over 30 cities across the United States. Each location offers an indemnity plan and a POS managed care plan. The benefits offered in these plans are the same across locations, although the POS plan requires lower copayments and deductibles and offers a wider array of preventive services than does the indemnity plan. Employer B is a large state government that offers an indemnity plan, a PPO plan, and seven HMO plans. Like Employer A, its indemnity plan charges higher copayments and deductibles than the managed care plans but makes no restrictions on out-of-network coverage. Chapter 2 describes the features of the plans offered by Employer A and Employer B.

Our statistical analyses used chi-squared tests of independence for comparing variables measured as percentages. We used analysis of variance (ANOVA) to compare means of continuous measures. No other adjustments were made in comparisons, since the purpose of this chapter is to present a global view of descriptive characteristics of those who have potentially disabling chronic conditions. As a result, we do not draw inferences about causality in this chapter. Readers should not assume that differences between those in the indemnity and managed care plans are due to plan design or to treatment practice patterns. Rather, the descriptive statistics constitute a first look at the data, providing an overview of the data and suggesting areas for detailed examination. More sophisticated analyses are presented in Chapter 6, which addresses whether managed care influences health care utilization and expenditure patterns.

D. Results

1. Prevalence Estimates

Employers A and B had 403,700 and 204,724 health plan enrollees in 1995, respectively. The prevalence of potentially disabling chronic conditions varied considerably by employer.The 1995 prevalence rate for Employer A was estimated as 174 per 1,000 covered lives. The prevalence rate for Employer B was higher, 216 per 1,000 covered lives.

Potential Disability AmongService Users. The numerator for the prevalence numbers noted includes service users with potentially disabling chronic conditions. It does not include chronically ill people who used no services in 1995. The denominator includes all plan enrollees, regardless of whether any utilization occurred. The prevalence numbers noted above are based upon all employees and dependents, not just on users of medical care services. In a given year it is natural for many people not to use any health care services (Duanet al., 1983). Non-users pose few difficulties for health plan managers and clinicians. The more difficult group to manage includes those who do use services; this group includes about 75 percent of the enrollees in the health plans offered by Employers A and B.

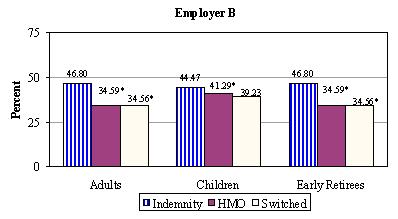

Figure 5-1 limits the denominator to service users in 1995. This figure depicts differences in the percentages of 1995 service users who have potentially disabling chronic conditions, shown separately by plan type and user group (early retirees, active employees, other dependents, and children); all differences shown are statistically significant. We find that people with potentially disabling chronic conditions are more likely to have indemnity coverage than to be enrolled in a managed care plan, with one exception. The exception is that early retirees appear to favor Employer B's PPO plan over its indemnity and HMO plans. In all other cases, however, those with chronic, potentially disabling conditions appear to favor the indemnity plans. Among service users, the prevalence of potentially disabled chronically ill people is substantially higher for early retirees, as one might expect (i.e., many may retire early due to health problems). All of the differences in percentages between indemnity plans and other plans which are shown in the figures are statistically significant, which is not surprising given the large sample sizes overall used in the analysis.

Potentially Disabling Chronic Conditions. While Figure 5-1 considered the entire population of plan service users, Tables 5-1 through 5-4 look only at those with potentially disabling chronic conditions. The tables assess how the enrollee groups (active employees, retirees, dependents) differ in terms of their populations of enrollees with disabling conditions.

Tables 5-1 through 5-3 list the most frequent potentially disabling chronic disease diagnoses for adults (Table 5-1 and Table 5-2) and children (Table 5-3) for both employers. Table 5-4 shows the five most frequent potentially disabling chronic mental health diagnoses for Employer A. (Employer B's mental health data are available upon request.) In general, these tables show that the same types of conditions affect active employees, dependents, and early retirees, but there are some differences in rankings.

| FIGURE 5-1: Percentages of 1995 Service Users Who Have Potentially Disabling Chronic Conditions by Plan Type, Employer, and Employee Group |

|---|

|

|

| NOTE: Values have been rounded to nearest percent. All differences are statistically significant (chi-square test of independence, p<.05). |

Table 5-3, compared to Table 5-1 and Table 5-2, shows that the potentially disabling diseases among children are often different from the diseases observed for adults. For example, children are affected most often by asthma and other illnesses concerning nutrition, metabolism and development, congenital anomalies, and cerebral palsy; adults are more often affected by heart problems, arthritis, and cancer.

All of these tables show a high degree of overlap in the top ten lists of potentially disabling chronic conditions in the two employer populations. The differences in the mission of these two employers do not appear to result in major differences in the nature of their most frequently observed potentially disabling chronic conditions.

| TABLE 5-1. Ten Most Frequent Potentially Disabling Chronic Disease Diagnoses For People Age 18-64, Employer A, 1995 | |||

|---|---|---|---|

| Active Employees | Dependents | Early Retirees | |

| 1 | Chronic Ischemic Heart Disease | Asthma | Chronic Ischemic Heart Disease |

| 2 | Asthma | Chronic Ischemic Heart Disease | Cardiac Dysrhythmias |

| 3 | Cardiac Dysrhythmias | Cardiac Dysrhythmias | Chronic Obstructive Pulmonary Disease |

| 4 | Complications of Heart Disease | Breast Cancer | Complications of Heart Disease |

| 5 | Angina Pectoris | Endocarditis | Angina Pectoris |

| 6 | Chronic Obstructive Pulmonary Disease | Chronic Obstructive Pulmonary Disease | Asthma |