ASPE Report

By: Brigette Courtot, Teresa Coughlin, and Emily Lawton The Urban Institute, Washington, DC

Abstract

This study of Medicaid and CHIP managed care programs in 20 states indicates that capitation rate-setting became more data-driven and transparent during the time period 2001-2010. Benefit packages were fairly consistent with carve outs in every state for a least one acute service. Total spending for Medicaid managed care enrollees varied considerably across states and subgroups, with the lowest for nondisabled children and highest for adults with disabilities.

Disclaimer

This study was conducted by the Urban Institute under contract number HHSP23320095654WC, task order number HHSP2333014T, with the HHS's Office of the Assistant Secretary for Planning and Evaluation. The authors take full responsibility for the accuracy of material presented herein. The views expressed are those of the authors and should not be attributed to ASPE or HHS.

This Report is available on the Internet at:http://aspe.hhs.gov/health/reports/2012/MedicaidandCHIPManagedCarePaymen...

Printer friendly version in PDF format (68 pages)

CONTENTS

Medicaid and CHIP Managed Care Rate Setting Policies.

Medicaid Managed Care Rate Setting Approaches.

The Capitation Rate Development Process.

Medicaid Managed Care Rate Factors and Other Adjustments.

Risk (Health Status) Adjustment.

Maternity-Related and Other Supplemental Payments.

Stop-Loss Coverage and Other Risk-Sharing Arrangements.

Stakeholder Perceptions of the Medicaid Managed Care Rate Setting Process.

CHIP Managed Care Rate Setting Approaches.

CHIP Managed Care Rate Factors and Other Adjustments.

Health Status (Risk) Adjustment.

Stop-Loss Coverage and Other Risk-Sharing Arrangements.

Stakeholder Perceptions of the CHIP Managed Care Rate Setting Process.

Perceptions of Medicaid and CHIP Rate Adequacy.

Services Excluded from Comprehensive Managed Care Benefit Packages.

Positive Aspects of Medicaid Managed Care Carve Outs.

Negative Aspects of Medicaid Managed Care Carve Outs.

Changes in Medicaid Managed Care Carve Outs Over Time.

Carve Outs in CHIP Managed Care Programs.

Monthly Medicaid Managed Care Spending.

APPENDIX A: Detailed Explanation of Data Analysis Methods. A-

APPENDIX B: Carve-Outs in Medicaid Managed Care Programs in Study States, 2001-2010. B-

Background/Overview - Today, the principal way care is delivered to Medicaid and Children’s Health Insurance Program (CHIP) beneficiaries is through managed care organizations, where the state contracts with health plans to provide health care services to enrollees for a capitated, or fixed, rate. The share of Medicaid and CHIP enrollees in managed care has been steadily rising over the past decade and continued growth is expected in the future. Though important policy changes have taken place in Medicaid managed care rate setting over the past decade, scant information is available on how Medicaid managed care programs establish their capitation rates, and even less exists on CHIP managed care rate setting. This report begins to fill that research gap by examining how 20 states establish Medicaid and CHIP managed care capitation rates, and how their approaches to rate setting have changed over the past ten years. It also analyzes how Medicaid managed care spending for four distinct populations (adults and children, with and without disabilities) and capitation rates in CHIP managed care programs vary among states, and how they have changed over time. Findings are based on case study interviews with Medicaid and CHIP stakeholders in the 20 study states and on an analysis of each state’s data from the summary files of the Medicaid Statistical Information System.

Medicaid and CHIP Rate-Setting Processes - Most Medicaid managed care programs in the study states use an administered rate-setting approach, whereby the state offers a specific rate and health plans decide whether or not to participate. Alternative approaches, employed by just a handful of states, include competitive bidding or negotiation with health plans. Per a federal requirement for “actuarial soundness” in Medicaid managed care rates which became effective in 2002, before a final rate is established all states must work with actuaries to develop an actuarially sound rate range. That is, a range for rates that ensures health plans are adequately reimbursed based on the cost of health care expenditures and the populations served. Programs use many different types of data to establish this range, but encounter data—which contain a record for each service delivered to plan enrollees—are perhaps the most critical. States’ access to encounter data has improved considerably, especially in the latter half of the decade, and all study states currently use encounter data to some degree in rate setting. Because encounter data are collected from health plans themselves and reflect actual service use and costs of managed care-enrolled populations, they are more appropriate for rate setting than previous data sources (e.g., fee-for-service data). Indeed, some states have moved to exclusively relying on encounter data for their rate setting purposes.

When developing Medicaid managed care rates, states also account for the various risk factors that influence enrollees’ health care utilization and costs. At the beginning of the study period, most of the states relied only on demographic factors—such as Medicaid eligibility category, age, sex and geography—to adjust their rates. Over time, however, nearly all study states have adopted more sophisticated health status “risk adjustment” models that base rates on diagnoses and historic healthcare utilization data, in an effort to better match payment to risk and to prevent plan risk selection. States now typically use a combination of demographic and health status risk adjustment to establish rates. Another common rate adjustment involves supplemental payments to health plans for maternity-related care provided to enrollees.

Of the nine separate CHIP programs examined for this report, about half have highly-coordinated Medicaid and CHIP rate-setting processes, though Medicaid and CHIP rates themselves are different. In the remaining states, rate-setting processes for Medicaid and CHIP are quite different, in part because CHIP program designers in those states made great efforts to distinguish CHIP from Medicaid and to shape it more like a commercial product. Because CHIP rate setting is not bound by federal regulations for actuarial soundness, the process often does not involve the foundational step of using an actuary to establish a rate range. Moreover, only three of the CHIP study states use encounter data for rate setting. The majority of the CHIP managed care programs examined use competitive bidding to set rates, though a handful of states use an administered rate-setting approach and one state negotiates rates with health plans. Nearly all states use at least one demographic factor in CHIP rate setting, most commonly enrollee age or geography, but only two report using health status risk adjustment for CHIP.

Over the past decade states have made considerable efforts to refine their rate development process. This is especially true for Medicaid managed care programs, but CHIP managed care has also benefited in the states that closely coordinate rate setting processes across the two programs. This evolution of Medicaid managed care rate setting over the past decade has been influenced by several factors. Perhaps most importantly, the 2002 actuarial soundness rules has resulted in increasingly transparent rate-setting processes and has encouraged (at least in part) state Medicaid programs to adopt more sophisticated methods. The actuarial soundness requirement has also affected the extent to which state budget constraints can influence Medicaid managed care rates. Budget-related rate reductions became more common in the study states during the economic recession, but these changes can only be made within an actuarially sound rate range, effectively limiting some negative effects.

Despite findings that the Medicaid rate-setting process has substantially improved over time, there appears to be room for additional improvements, particularly with regard to engaging and educating health plans and other stakeholders about the rate setting process—tasks that become more complex as methods become more sophisticated. There is also room for improvement in state’s CHIP rate-setting processes. Compared to Medicaid, CHIP rate setting processes are still very much in their infancy, in part because there are far fewer federal requirements. At the same time, stakeholders are not overly concerned about CHIP’s more relaxed rules for rate setting, most likely owing to the fact that state CHIP programs are quite small in comparison to Medicaid, and because the program enrolls a comparatively homogenous, low-risk population of primarily children.

Perceptions of Medicaid and CHIP Rate Adequacy - Stakeholders had mixed views of rate adequacy in Medicaid managed care programs. Even in those states where rates were described as generally adequate, plans reported operating on thin margins, making it more difficult for them to expand their provider networks (especially in rural areas and with regard to recruiting specialists), make capital investments, and put innovative care management and quality improvement practices in place. These findings are particularly troubling in light of the planned 2014 Medicaid expansion under federal health reform. State Medicaid programs that hope new plans might enter their Medicaid managed care market in anticipation of the 2014 expansion—for instance because they are concerned about current plan capacity or because they hope to increase competition between plans—must be aware of the critical role of rate setting and adequacy.

There were also mixed views of CHIP rate adequacy, though stakeholders generally thought rates were sufficient to meet plans’ needs. With no guidelines for actuarial soundness, CHIP rates do not have to be adjusted on a regular basis. This distinction may have advantages and disadvantages, from a plan perspective, since the lack of such standards could result in overly generous rates or rates that are inadequate. CHIP managed care rates may also be more heavily influenced by budget constraints in the absence of federal actuarial soundness rules.

Services Excluded from Comprehensive Managed Care Benefit Packages - An important feature of Medicaid and CHIP managed care programs includes the number and scope of “carve outs” or services that are excluded from the comprehensive benefit package and instead provided on a fee-for-service basis or by a limited-benefit managed care plan that receives a separate capitated rate. All of the Medicaid managed care programs examined for this study carve out at least one acute care service, most commonly dental care, mental health care, or prescription drugs. With regard to long-term care services, most states carve out nursing facility services (often under a partial carve-out arrangement) as well as personal care assistance services.

State CHIP officials reported far fewer service carve outs in their managed care programs, which is unsurprising given that many states with separate CHIP programs modeled their benefit package after private health insurance products, which tend to include all covered services (with the exception of dental care) in a single comprehensive benefit package. Dental care was the only service carved out by a majority of CHIP managed care programs, though a handful of programs also carved out mental health care.

On the whole, the contents of Medicaid and CHIP managed care benefit packages have remained relatively consistent across states during the 2001-2010 study period. In a few instances, however, study states made major changes, exemplified by Connecticut Medicaid’s decision to carve out a growing number of services until—in 2012—its risk-based managed care program was effectively dismantled. While individual states have been fairly consistent as to what they include in their managed care benefit package, wide variation exists across the 20 states as to which combination of, and to what extent, services are included and excluded in Medicaid managed care. States continue to consider and implement carve outs, and it is clear that Medicaid programs are still struggling to find the right combination of carve outs given their enrolled population and their unique health care delivery systems and markets.

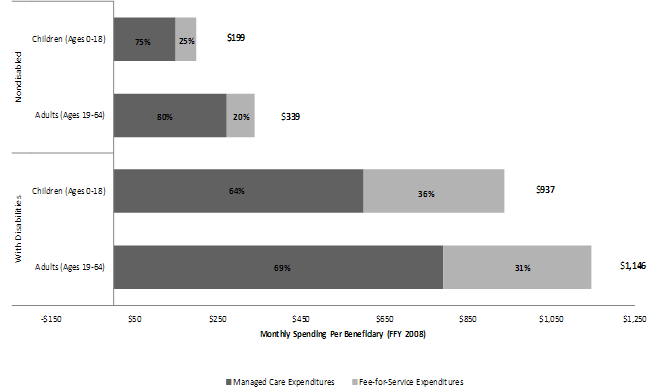

Spending for Medicaid Managed Care Enrollees - Total spending for Medicaid managed care enrollees varies considerably across states and subgroups. As expected, nondisabled children have the lowest level of total spending (an average of $199 per member per month in 2008) and adults with disabilities have the highest level (an average of $1146 per member per month in 2008). While the bulk of total spending for Medicaid managed care enrollees is for payments made to health plans, sizable shares are for services delivered through the traditional Medicaid fee-for-service system. This is particularly true for beneficiaries with disabilities. On average, more than a third of total Medicaid spending on children with disabilities enrolled in managed care was spent on services provided through the fee-for-service system in 2008; for adults with disabilities, this proportion was 30 percent. Though smaller, even for the nondisabled a considerable share of total spending is paid fee-for-service. This reflects the study states’ reliance (in general) on carve-outs to deliver at least some services to Medicaid managed care enrollees.

Summary - In summary, this study indicates that the capitation rate-setting processes employed by Medicaid managed care programs have evolved over the past decade to become more data-driven and transparent. This can largely be attributed to the 2002 federal rule requiring states to demonstrate that managed care rates are actuarially sound—though the rule only applies to Medicaid programs, in several states CHIP programs have also benefited because states often coordinate rate setting across the two programs. Improvements in the availability and use of health plan encounter data have also enhanced the rate-setting process, at least for Medicaid managed care programs. Even with these improvements in rate-setting processes, however, health plans in a number of states were concerned about rate adequacy. They described operating on very thin margins, under rates that are insufficient for maintaining robust provider networks and supporting care management and quality improvement activities. Finding a healthy balance between sound Medicaid managed care rates and a robust Medicaid managed care market is important and will become that much more so as the 2014 Affordable Care Act coverage expansion approaches.

With enrollment of more than 55 million individuals in 2011, the Medicaid program is the nation’s single largest insurer. Today, the principal way care is delivered to Medicaid enrollees is through managed care organizations, where the state contracts with health care plans to provide health care services to enrollees for a capitated, or fixed, rate.1 In 2009, thirty-four states and the District of Columbia had comprehensive risk-based Medicaid managed care programs, and about half of the nation’s Medicaid population received health care services through risk-based managed care (hereafter referred to simply as managed care) (Medicaid and CHIP Payment and Access Commission, 2011) —up from just 15 percent in 1995 (CMS, 1996). With the rise in enrollment, Medicaid managed care spending has also climbed, reaching roughly $90 billion in 2010.2 >While the bulk of Medicaid managed care enrollees are nondisabled adults and children, over the past several years states have increasingly enrolled disabled and aged Medicaid beneficiaries in managed care. One recent study of 20 states reported that between 2001 and 2008, enrollment in risk-based managed care grew by 82 percent (from roughly 300,000 to 550,000) for children with disabilities and by 73 percent (from roughly 800,000 to 1.3 million) for nonelderly adults with disabilities across the states (Howell, Palmer, & Adams, 2012). And, a 2011 survey revealed that 20 states expected to expand their Medicaid managed care programs in the near future (Smith, Gifford, Ellis, Rudowitz, & Snyder, 2010). Moreover, the Medicaid coverage expansion authorized by the Affordable Care Act has the potential to increase the program’s size considerably starting in 2014. A June 2012 Supreme Court ruling made the expansion optional for states; if all states participate in the expansion, an estimated 22.3 million uninsured with incomes below 138 percent of the federal poverty level (FPL) could be eligible for Medicaid (Kenney, Dubay, Zuckerman, & Huntress, 2012). Most of these potential new enrollees would likely be served through managed care organizations.

Paralleling Medicaid, managed care is also the dominant way health care services are delivered to children enrolled in the Children’s Health Insurance Program (CHIP). In 2010, 75 percent of CHIP enrollees, 5.7 million children, were enrolled in managed care (MACPAC, 2011). Enrollment in managed care was higher in states with CHIP programs (81 percent) that are separate from their Medicaid programs than in states with Medicaid-expansion CHIP programs (57 percent) (MACPAC, 2011).

While the share of Medicaid and CHIP enrollees in managed care has been steadily rising and will likely only continue to increase in the coming years, little information is available about how Medicaid managed care operates in today’s environment. Although several studies, primarily analyses of the impact of managed care on program enrollees, were completed in the late 1990s and early 2000s, it has been a decade since a close examination of Medicaid managed care has been conducted, and to date only very limited research has been conducted on CHIP managed care.3

A few recent studies, however, have begun to fill this important information gap: One is the June 2011 Medicaid and Children’s Health Insurance Payment and Access Commission (MACPAC) report, which provides a detailed overview of Medicaid and CHIP managed care. Another is a national Kaiser Commission on Medicaid and the Uninsured survey that profiles state Medicaid managed care programs in 2010 (Gifford, Snipes, & Paradise, 2011). Finally, the Department of Health and Human Services’ Office of the Assistant Secretary of Planning and Evaluation (ASPE) sponsored a recently-completed study, Medicaid and CHIP Risk-Based Managed Care in 20 States, that examines Medicaid managed care over the past decade, detailing the structure of programs in 20 states, including which populations are enrolled, which services are covered, how states administer and monitor the quality of care in their managed care programs, and health plan participation (Howell et al., 2012).

Like other parts of Medicaid managed care, a close look at managed care payment methods and spending across states has not been completed in more than a decade. To the best of our knowledge, the last comprehensive examination of Medicaid managed care rate setting was a 2001 study that focused on managed care payments for nondisabled, poverty-related populations (Holahan & Suzuki, 2003). No comparable study has ever been completed on CHIP managed care payment methods and rates.

This report is a companion to the Medicaid and CHIP Risk-Based Managed Care in 20 States report (mentioned above) and focuses on 20 states’ Medicaid and CHIP managed care payment methods and spending. The study states are: Arizona, California, Connecticut, Delaware, Florida, Maryland, Massachusetts, Michigan, Minnesota, New Jersey, New Mexico, New York, Ohio, Pennsylvania, Rhode Island, Tennessee, Texas, Virginia, Washington, and Wisconsin.

Specifically, the report addresses the following two broad research questions:

- How do 20 states establish capitation rates in their Medicaid and CHIP managed care programs, and how have their approaches to and policies for rate setting changed over the past decade?

- How does monthly Medicaid spending for four distinct managed care enrollee populations (adults and children, with and without disabilities) vary among the 20 states?

Medicaid and CHIP Managed Care Rate Setting Policies

Medicaid Managed Care Rate Setting Policies

Over the past ten years, important policy changes have taken place in Medicaid managed care rate setting. Chief among them is the provision in the Balanced Budget Act (BBA) of 1997 requiring all states to pay health plans participating in Medicaid rates that are “actuarially sound.”4 That is, states are to develop rates in accordance with actuarial principles that are appropriate for the populations and services covered, and which have been certified by an actuary.5 Many of the requirements in the BBA regulations—which were issued in June 2002—focus on the process that states must use when establishing Medicaid managed care payment rates, such as documenting their methods and including an actuarial certification of rates.

Prior to the BBA and the subsequent 2002 regulations, Medicaid managed care rates were regulated using an “upper payment limit” methodology, whereby states could not pay health plans more than they would have paid for the same services on a fee-for-service basis. The upper payment limit provided a hard cap on the maximum amount that states were allowed to pay health plans but, until the BBA, there was no requirement for a minimum payment amount—“a floor”—that states had to pay health plans.

As Medicaid managed care programs expanded during the 1990s, quality fee-for-service data—needed to determine an upper payment limit for rate setting—became increasingly scarce and out-of-date, which posed problems for states in their ability to set sound rates. Also, the absence of any minimum managed care payment rate posed other risks. For example, if rates were set too low, plans may not be able to pay providers enough to maintain an adequate network, which could compromise enrollees’ access to care. Further, if rates were too low, plans may exit the Medicaid market because they could not earn an adequate profit. This too could compromise enrollees’ choice of plans, access and continuity of care. Indeed, in the 1990s, considerable turmoil took place in many states’ Medicaid managed care programs (often stemming from rate-setting methods) and some struggled to maintain plan participation.6

The actuarial soundness provision in the BBA sought to address the twin problems of diminished availability of fee-for-service data for rate-setting purposes and the absence of a minimum rate. BBA regulations also required states to formally document their rate setting methods, such as the data used to construct rates, the adjustments made to smooth data (such as medical trend inflation), and the “rate cells” (or distinct payment amounts) used for each enrolled Medicaid population. Using a detailed checklist, regional office staff from the Centers for Medicare and Medicaid Services (CMS) are responsible for reviewing state Medicaid programs' rate-setting submissions for compliance with the actuarial soundness requirements.

While the intent of actuarial soundness regulations was laudable, problems have ensued. A 2010 Government Accountability Office (GAO) study, for example, found that CMS’s oversight of state compliance with actuarial soundness requirements was lacking (Government Accounting Office, 2010). In a comment letter attached to the GAO report, CMS agreed with the study findings and highlighted steps the agency was taking to improve the process. Continuing issues with Medicaid rate setting could be attributed to the current lack of an actuarial standard of practice (or ASOP) that applies to Medicaid managed care rate setting, a situation that the American Academy of Actuaries is working to rectify (American Academy of Actuaries, 2005).

Apart from requirements for actuarial soundness, there are many other important features of states’ Medicaid managed care programs that have implications for rates. These include:

- Rate setting approaches (e.g., does a state negotiate rates, administer rates, use a competitive bidding process, or employ some combination of these);

- Additional/excluded payments (e.g., supplemental maternity payments);

- Services included in or excluded from the benefit package;

- Risk adjustment methods;

- Risk sharing (e.g., risk corridors and reinsurance) arrangements; and

- Quality incentives (e.g., additional payments or withholds to improve health care quality).

A state’s fiscal situation can also affect state rate setting. Medicaid is often the single largest expenditure item in state budgets, making the program a budget target when savings must be produced. Reducing plan capitation rates or provider reimbursement rates (which ultimately affect plan capitation rates) are important budget savings strategies used by states. Indeed, in a recent 50-state survey of Medicaid programs, 11 states reported reducing plan capitation rates in fiscal year 2011 and 19 states expected to cut rates in fiscal year 2012 (Smith, Gifford, Ellis, Rudowitz, & Snyder, 2011).

CHIP Managed Care Rate Setting Policies

Until recently federal regulation of CHIP managed care programs has been much more limited as compared to Medicaid. It was only in the Children’s Health Insurance Program Reauthorization Act (CHIPRA) of 2009 that several Medicaid managed care provisions were extended to CHIP, including requirements for enrollee plan choice and external quality reviews. CHIPRA, however, did not include provisions requiring states with CHIP programs that are separate from their Medicaid programs (hereafter referred to as separate CHIP programs) to set managed care rates that are actuarially sound. If a state chooses to provide a ’benchmark-equivalent’ benefit package7 to individuals enrolled in separate CHIP programs, it must submit a certification of actuarial equivalence demonstrating that the package it offers is comparable to that of its chosen benchmark (e.g., the HMO with the largest commercial enrollment in the state, coverage offered by the Federal Employees Health Benefits program, or coverage offered to state employees), but this certification is related to plan benefits and not to the adequacy or fairness of plan payment rates (Hearne, 1998).

This study focuses on risk-based Medicaid and CHIP managed programs in the 20 study states taking a retrospective look over a ten-year period, from 2001 a€“ 2010. States were selected primarily on the basis of having either a large number of people covered by risk-based Medicaid managed care programs (again, hereafter referred to simply as managed care), a large proportion of the state’s Medicaid population in managed care, or both. This allowed for the inclusion of some more populous states that cover a relatively smaller proportion of their Medicaid population in managed care (such as Florida and Texas) as well as some less populous states that enroll a relatively large proportion of their Medicaid population in managed care (such as Delaware, New Mexico, and Rhode Island). We also sought regional variation and included at least four states from each of the four major census regions.

In 2010, the 20 study states accounted for about 80 percent of the nation’s Medicaid enrollment in managed care managed care (Table 1). Across the 20 states, 61.9 percent of Medicaid enrollees are in managed care; this is much higher than the non-study states in which only 25.4 percent of the Medicaid population is enrolled in managed care. At the time we selected states (in 2010), there was not yet a source of data on the number of CHIP enrollees in managed care. When those data became available (MACPAC, 2011), it was evident that our study states report a similar proportion of CHIP enrollees in managed care (roughly 60 percent) as for Medicaid (data not shown).

Table 1: Medicaid Enrollment in Managed Care, October 20101

| Region | State | Total Medicaid Managed Care Enrollment (in thousands) | Percent of State Total Medicaid Enrollment | Percent of Total U.S. Medicaid Managed Care Enrollment |

|---|---|---|---|---|

| Northeast | Connecticut | 391 | 58 | 1.5 |

| Delaware | 142 | 74 | 0.5 | |

| Massachusetts | 513 | 39.2 | 1.9 | |

| New Jersey | 974 | 95 | 3.6 | |

| New York | 3,002 | 62.5 | 11.2 | |

| Pennsylvania | 1,222 | 58.5 | 4.6 | |

| Rhode Island | 134 | 75.3 | 0.5 | |

| South | Florida | 1,287 | 45.3 | 4.8 |

| Maryland | 685 | 73.9 | 2.6 | |

| Tennessee | 1,219 | 100 | 4.6 | |

| Texas | 1,698 | 48.9 | 6.4 | |

| Virginia | 527 | 62.1 | 2 | |

| Midwest | Ohio | 1,730 | 85.9 | 6.5 |

| Michigan | 1,251 | 68.1 | 4.7 | |

| Minnesota | 477 | 66.3 | 1.8 | |

| Wisconsin | 624 | 54.2 | 2.3 | |

| West | Arizona | 1,210 | 89.2 | 4.5 |

| California | 4,079 | 55 | 15.3 | |

| New Mexico | 335 | 68 | 1.3 | |

| Washington | 627 | 54.2 | 2.3 | |

| Twenty Study States | 22,127 | 61.9 | 82.7 | |

| All Other States | 4,613 | 25.4 | 17.3 | |

| Total | U.S. | 26,740 | 49.6 | 100 |

Source: Gifford K, Smith VK, Snipes D and J Paradise. A Profile of Managed Care Programs in 2010: Findings from a 50-State Survey. Kaiser Commission on Medicaid and the Uninsured, Washington, DC: September 2011.

To conduct the study we used a mixed methods approach, relying on data from state case study states and analysis of data from the summary files of the Medicaid Statistical Information System.

For the case study, we conducted interviews with state Medicaid officials in person in 11 states and by telephone in nine states between January and November 2011. For states where CHIP managed care programs are administered by an organization or unit of government distinct from that of Medicaid, we interviewed those officials separately. We asked state officials about their current approach to managed care contracting and rate setting, how this approach changed during our study period (2001-2010), best practices in Medicaid/CHIP managed care, and their forecast for federal health reform’s impact on Medicaid/CHIP managed care. Finally, we obtained information on Medicaid and CHIP capitation rates during our study period. Initially, we intended to use these state-supplied capitation rates to construct state- and population-specific managed care payment estimates that could be compared over time. However, the rate information available for many of the states was incomplete, and other states did not supply any rate data at all. Ultimately, we revised our study to include an analysis of Medicaid Statistical Information System (MSIS) summary file data on managed care spending in our 20 study states (as described below).

For each study state, we also conducted telephone interviews with representatives from two health plans that participate in the state’s Medicaid and/or CHIP managed care programs, and from two health care provider organizations. We asked these representatives about the factors that influenced their decision to participate in Medicaid/CHIP managed care, their perceptions of the adequacy of capitation rates (for plans) and provider reimbursement (for providers), provider network requirements, perceptions of beneficiary access and quality of care under Medicaid/CHIP managed care, and the effects of federal health reform.

Thus, there were at least five interviews per state, or over 100 interviews in all. Interviews were conducted using a semi-structured protocol. We also reviewed managed care program documents (including health plan contracts and rate-setting methodology reports) provided by state officials.

Informant interviews were transcribed and the transcripts were coded with NVivo qualitative analysis software,8 using a coding structure that captured the most important interview questions and topics covered; this allowed for a cross-state analysis of common themes across topics.

As part of the case study, we also obtained broad information on Medicaid and CHIP managed care programs, including limited-benefit plans (e.g., plans covering only behavioral health services or dental services) and integrated care plans that include long-term care for those dually enrolled in Medicaid and Medicare. Due to resource and time limitations, however, this report focuses on comprehensive benefit plans for acute care and programs for the non-elderly, non-dual eligible population.

The following is a summary of our data analysis methods; a detailed explanation of these methods is in Appendix A. For the data analysis component of the study, our primary data source was the MSIS summary file. Specifically, we used the summary file of the MSIS for federal fiscal year 2008 (the most recently available year for which there was data on all 20 states) hereafter referred to simply as 2008.

Study Population: We grouped enrollees into four subgroups: nondisabled adults ages 19-64, nondisabled children ages 0-18, adults with disabilities ages 19-64, and children with disabilities ages 0-18. We excluded beneficiaries who had unknown age or eligibility codes; were dually eligible for Medicaid and Medicare; were only eligible for family planning (limited benefit) services; had positive spending for home and community-based services (HCBS) or institutional care services; or were enrolled in CHIP for any part of the year. After applying these restrictions, our final sample of comprehensive Medicaid managed care enrollees across the 20 states in 2008 was 14.2 million.

Estimating Enrollment in Comprehensive Medicaid Managed Care Plans: We estimated enrollment (expressed as person-months) in Medicaid managed care plans for each of the four enrollee subgroups. The MSIS 2008 summary file includes information on monthly enrollment in up to seven different types of managed care plans. We focused on beneficiaries who were enrolled in at least a medical/comprehensive plan; the sample includes those also enrolled in other managed care plans (e.g., dental or behavioral health plans)

Estimating Average Managed Care and Fee-for-Service Spending: MSIS data includes managed care spending variables reflecting annual spending for all managed care plans in which a beneficiary is enrolled, but do not indicate what proportion of managed care spending is attributable to different plan types or to specific months of managed care enrollment. We determined which plan or combination of plans the beneficiary was enrolled in for the seventh month of the fiscal year and allocated the beneficiary’s annual managed care spending total to that plan or combination of plans.

We determined average monthly managed care spending for beneficiaries enrolled in at least a medical/comprehensive plan by dividing the total managed care spending9 for all beneficiaries assigned to that plan or combination of plans by the total person-months enrolled in any managed care plan among those beneficiaries.

We also examined how much Medicaid spent on care provided on a fee-for-service basis to beneficiaries during the months they were enrolled in comprehensive managed care plans. We performed an imputation to exclude fee-for-service spending for any months during which beneficiaries in our sample were not enrolled in managed care; this is only relevant for those beneficiaries who were not continuously enrolled in managed care while Medicaid eligible. The imputation, as well as an explanation of our methods for assigning beneficiaries to a particular plan or combination of plans, is detailed in Appendix A.

Other Adjustments: We performed a series of standard adjustments, including inflation to reflect spending levels reported on CMS-64 forms. These are standard adjustments applied to other Urban Institute analyses of Medicaid spending using MSIS data, and are fully discussed in Appendix A.

Medicaid Managed Care Rate Setting Approaches

Medicaid managed care programs in the 20 study states use varied approaches to establish their capitation rate payments. These rate-setting approaches are broadly classified into three categories—administered, competitive bidding, and negotiated. Table 2 shows each study state’s rate-setting approach as of 2010.

Thirteen study states use an administered rate-setting approach, making this the most common approach. These states select and offer a rate within a range developed by actuaries, and health plans decide whether they are willing to participate in the program under this set rate structure. Typically, states hold one or more meetings with health plans during the process, to discuss both rate-setting factors and methodology. Program officials in most states using administered rate setting emphasized that plans could voice concerns about the rate structure during the meetings, and (though infrequent) Medicaid programs sometimes adjust their rate-setting factors or methodology to reflect these concerns.

Most of the states that use an administered rate setting process did so for the entire data period (2001-2010) though three states (Washington, New Mexico, and New York) initially negotiated rates with health plans. Washington began administering its rates in 2003, New York in 2008 when it implemented health status risk adjustment, and New Mexico in 2009 in response to budget constraints and increasing public scrutiny of health plan management and profits. A fourth state (Michigan) initially used competitive bidding but began administering rates in 2005 in an effort to strengthen its program (described below).

Four study states (Arizona, Connecticut, Delaware, and Tennessee) use a competitive bidding process to set rates in their Medicaid managed care programs. After developing an actuarially-sound rate range, these states provide interested plans with a data book of information needed to develop rate bids. Some program officials in these states noted that they share the rate range with plans before bids are submitted, though others indicated that the range is only used internally. The state selects plans based on their bids and their accompanying technical proposals.

| State | Approach to Establishing Rates - Administered | Approach to Establishing Rates - Negotiated | Approach to Establishing Rates - Competitive Bidding |

|---|---|---|---|

| Arizona | x | ||

| California | x | ||

| Connecticut1 | x | ||

| Delaware | x | ||

| Florida | x | ||

| Maryland | x | ||

| Massachusetts | x | ||

| Michigan | x | ||

| Minnesota2 | x | ||

| New Jersey | x | ||

| New Mexico | x | ||

| New York | x | ||

| Ohio | x | ||

| Pennsylvania | x | ||

| Rhode Island | x | ||

| Tennessee | x | ||

| Texas | x | ||

| Virginia | x | ||

| Washington | x | ||

| Wisconsin3 | x | ||

| TOTAL | 13 | 3 | 4 |

Sources: Interviews with Medicaid and CHIP officials, 2011; managed care program documents.

1Connecticut's program uses competitive bidding followed by some negotation with health plans.

2Minnesota implemented competitive bidding for the Twin Cities (Minneapolis and St. Paul) region in 2012; for the remainder of the state, negotiated rate setting is used (and was used statewide in 2010).

3Wisconsin uses administered rate setting for the Milwaukee region; in the remainder of the state, the medical component of the capitation rate is administered while the adminsitrative component of the rate is set through competitive bidding.

Three states—Arizona, Delaware, and Connecticut—have used competitive bidding throughout the study period. Tennessee initially used an administered rate model, but when it rebuilt its managed care program beginning in 2007 the state adopted a competitive bidding process.10

A fifth state, Minnesota, was implementing competitive bidding for the Twin Cities region at the time of our interviews (2011), and began using this approach in January 2012. According to Minnesota informants, the state adopted competitive bidding as a cost containment measure, and in response to negative political attention and concern about Medicaid managed care plan profits. In 2011, one of the plans participating in Minnesota’s program returned $30 million in excess reserves to the state as legislators faced a huge budget deficit. State officials will consider expanding the competitive bidding model to additional regions in the future.

While Minnesota officials report significant cost-savings ($175 million in state fiscal year 2012) in the first year after implementing competitive bidding, informants in other study states described challenges with this rate approach. For example, Michigan’s Medicaid managed care program used competitive bidding when it began its program in 2000, but in 2005 it switched to an administered rate approach, a primary reason being that some plans were in financial trouble because they had bid rates that were too low and not viable (notably, this was before CMS requirements for actuarially sound rates were in effect). At the other end, Massachusetts used a competitive bidding approach in its 2008 procurement, but program officials determined that rates were too high and not sufficiently competitive, and ultimately returned to an approach where the state sets a rate range and negotiates with plans.

Three states (Minnesota, Massachusetts, and Pennsylvania) use a rate-setting process that involves negotiation with health plans to establish a mutually agreeable rate. In these states, program officials use the actuarially-sound rate range as a foundation for discussions with individual health plans. The state typically enters negotiations with an offer that is on the low end of the range, and plans must make an evidence-based case for a higher rate. Officials in one state emphasized that “bad luck or poor plan management” were not considered justifiable reasons for an increased rate.

Rate negotiation was more common at the start of the study period, but over time several states moved away from this approach. This appears to be related at least in part to state budget constraints (i.e., a state has less flexibility to negotiate payments with plans) and to increasingly sophisticated rate-setting methods that, according to informants, have become more rigid in recent years.

The Capitation Rate Development Process

The three rate-setting approaches described above reflect how the study states conclude their rate setting process and settle on a final rate. Before capitation rates are finalized, however, states undergo a multi-step rate development process. Because of the CMS requirements for actuarial soundness, certain components of this process are similar across all 20 states and their managed care approaches. Every state, for example, works with actuaries to develop an actuarially sound rate range—that is, a range for rates that ensures health plans are adequately reimbursed based on the cost of health care expenditures and the populations served. All but one of the study states contracts with an external actuary to set the rate range—Arizona is the only exception. Early in the study period (2001-2010), Arizona decided to move actuarial responsibilities in-house as a cost-saving measure. Some program officials in other states (for example, Delaware) suggested that, while expensive, having an independent and “neutral” firm be responsible for rate setting is helpful.

Medicaid managed care programs use many different types of data to establish their rate range including national and (less frequently) state health care cost trends, information on health plan provider reimbursement levels, and—perhaps most critical—encounter data collected from the health plans participating in the program. Every study state requires plans to submit encounter data, which contain a record for each service delivered to plan enrollees. The maintenance and use of encounter data has evolved over the past decade to the point where most of the study states are now confident that their encounter data provide useful information for rate-setting purposes. One state official described encounter data as the “lifeblood of the Medicaid managed care program.” 11

Even so, encounter data do not necessarily represent efficient utilization and still have limitations in completeness and accuracy. For example, when plans use “sub-capitation” (paying network providers a capitated rate), there is less incentive for the provider to submit complete data, leading to underreporting of services. In fact, this is one reason that health plans choose to pay providers on a fee-for-service basis rather than through sub-capitation. A health plan representative in New Jersey noted “We prefer fee-for-service because we know we’ll get the encounter data so we’ll have better [quality monitoring] scores and better reporting to the state.” Sub-capitation is particularly prevalent among health plans in California—the only study state where plan representatives said that the majority of providers are reimbursed this way—but is less common in other states. In several states, plan representatives indicated that while medical providers are rarely reimbursed via sub-capitation, they use the arrangement to reimburse for ancillary or non-medical services like durable medical equipment (in Arizona), non-emergency transportation and vision care (in Connecticut) and dental care (in Wisconsin).

Another important factor that influences the quality of plan encounter data is the level of experience health plans have with managing this data. More years of experience with collecting and reporting encounters improves the chances that a plan will have the structures and incentives in place to ensure data quality. States report that they must continually monitor the quality of encounter data and provide feedback to plans, and, moreover, they are becoming more sophisticated in how they do the monitoring.

Each of the study states use encounter data in rate setting, though to varying degrees. Most states began using encounter data to establish rates during the past decade, several in conjunction with implementation of the 2002 CMS requirements for actuarially-sound Medicaid managed care rates. Due to concerns about encounter data reliability in the early years, however, states typically combined encounter data with fee-for-service data to form a basis for capitation rates. As encounter data have become more complete over time, however, state Medicaid managed care programs have come to rely on them more and more. Indeed, some study states (including Massachusetts and Michigan) reported using only encounter data (without relying on supplemental health care cost/use data, such as from Medicaid fee-for-service claims or health plan financial documents) for the first time in their most recent rate cycle, joining states such as Arizona that have used only encounter data for a longer period of time. At the same time, many states continue to use a mix of encounter and other types of health care cost data when setting capitation rates.

Encounter data are also a critical component of health status (risk) adjustment models, which are described below. Officials in several states suggested that adopting risk adjustment in their rate-setting process has improved the quality of encounter data. Since these data are used to determine the health risk of a plan’s enrolled population and capitation rates are adjusted to reflect this risk, plans are invested in making sure that their encounter data are complete and accurate. As one informant noted, “The health plan’s payment is only as good as the data submitted to the Medicaid department.”

In addition to the use of encounter data to set rates, state officials described several other common features in their rate development process. They universally reported accounting for Medicaid program policy changes—including changes to eligibility levels/processes, elimination or addition of benefits, cost-sharing, and the Medicaid provider fee schedule—when establishing rates. Medicaid managed care programs have also increasingly made use of a variety of “managed care efficiencies” in rate setting. In these arrangements, the state sets a specific goal for utilization—such as a reduction in emergency room usage—and adjusts the rates under the assumption that this goal will be met, i.e., the rates assume that plan enrollees will use the emergency room less in the coming rate period than they have in the past. A number of study states—including but not limited to Arizona, Massachusetts, Minnesota, New Jersey, Pennsylvania, and Wisconsin—reported building managed care efficiencies into their rates in 2010. The efficiency adjustments they described involve (among others) emergency room usage, preventable hospital admissions and re-admissions, and pharmacy efficiencies.

A final component that is common across a number of the states is the inclusion of health care quality incentives in rates. For example, twelve study states (Maryland, Massachusetts, Michigan, Minnesota, New Mexico, New York, Ohio, Pennsylvania, Rhode Island, Tennessee, Texas, and Wisconsin) have established at least one “pay-for-performance program” whereby the managed care program provides health plans with financial incentives for improving measures of health care quality (e.g., an increase in the proportion of children who are up-to-date on vaccinations). Usually the incentive is a small portion of the capitation rate (most typically reported to be 1 percent or less, although one state offered up to 5 percent). In most programs, that amount is initially withheld from the capitation rate and awarded retrospectively to those plans that reach a pre-determined threshold.12

Medicaid Managed Care Rate Factors and Other Adjustments

Another area of variation in state rate setting practices involves the combination of factors that shape the rate cells used to pay Medicaid managed care plans. Table 3 shows capitation rate adjustment factors in the study states as of 2010.

Each of the study states uses multiple demographic factors to develop Medicaid rates (Table 3). All states pay distinct managed care rates for enrollees in different eligibility categories (e.g., those who are eligible for Medicaid because of poverty, versus those who are eligible because of their disability status) and all but one (California) adjust rates by enrollee age. Most states also use enrollee sex and geography (county or region of residence) to adjust rates.

For the most part, states’ use of these demographic factors in rate setting has not changed over time. Connecticut initially adjusted rates according to geography but eliminated this factor after determining that there was not enough regional variation in health care costs to merit geographically-adjusted rates in the small state. In 2008, New York replaced its initial structure of ten different age, sex, geography, and eligibility category-adjusted rate cells with three rate cells that account for age and eligibility category (a second step in this state’s revised rate setting process involves applying a regionally-based risk adjustment methodology).

| State | Demographic Factors - Age | Demographic Factors - Sex | Demographic Factors - Geography | Demographic Factors - Eligibility Category | Demographic Factors - Health Status(Name of System/Method)1 | Supplemental Maternity Payment |

|---|---|---|---|---|---|---|

| Arizona | x | x | x | x | x (Ingenix Symmetry) | x |

| California2 | x | x | x (MedicadRx) | x | ||

| Connecticut | x | x | x | |||

| Delaware | x | x | x | x (CDPS) | x | |

| Florida3 | x | x | x | x | x (CDPS) | x |

| Maryland | x | x | x | x | x (ACG) | x |

| Massachusetts | x | x | x | x | x (DxCG) | |

| Michigan | x | x | x | x | x (CDPS) | x |

| Minnesota4 | x | x | x | x | x (CDPS and ACG)5 | |

| New Jersey | x | x | x | x | x (CDPS) | x |

| New Mexico6 | x | x | x | |||

| New York | x | x | x | x (CRG) | x | |

| Ohio7 | x | x | x | x | x (CDPS) | x |

| Pennsylvania8 | x | x | x | x (CDPS plus Rx) | x | |

| Rhode Island | x | x | x | x | ||

| Tennessee9 | x | x | x | x | x (ACG) | |

| Texas | x | x | x | x (CDPS) | x | |

| Virginia | x | x | x | x | x (CDPS) | |

| Washington10 | x | x | x | n/a | x (CDPS) | x |

| Wisconsin | x | x | x | x | x (CDPS) | x |

| TOTAL | 19 | 15 | 17 | 19 | 17 | 14 |

Sources: Interviews with Medicaid and CHIP officials, 2011; managed care program documents.

1The health adjustment systems in use by the study states include the Chronic Payment Disability System or CDPS, Ingenix Symmetry, Medicaid Rx, Adjusted Clinical Groups or ACG, Clinical Pharmaceutical Groups or CRxG, and Diagnostic Cost Groups or DxCG systems.

2California operates three distinct models of Medicaid managed care. The County Organized Health System (COHS) model adjusts rates using enrollee region and eligibility category. The Geographic Managed Care (GMC) and Two-Plan models adjust rates using region, eligibility category, and health status. The GMC and Two-Plan models use a maternity supplemental payment, but the COHS model does not.

3Florida's 5 reform counties, where enrollment in Medicaid managed care is mandatory, use the following factors to adjust rates: geography, eligibility category, health status. Florida's 62 non-reform counties use the following factors to adjust rates: geography, age, sex, and eligibility category. Florida's reform counties use a maternity kick payment but the non-reform counties do not.

4Minnesota also adjusts rates using the following factors: living arrangement, Medicare status, and major program (benefit set).

5Minnesota's managed care program uses CDPS for health status adjustment for rates for beneficaries with disabilities and the ACG system to adjust rates for health status for nondisabled beneficiaries.

6The rate adjustment factors listed for New Mexico are used for the state's Salud! managed care program which covers acute care physical health benefits. The state's separate managed care program that provides long-term care uses geography to adjust capitation rates.

7In Ohio, rates for SSI-related beneficiaries in managed care are adjusted using enrollee region and health status (CDPS). Rates for TANF-related beneficiaries are adjusted uaing region, age, and sex; there is also a maternity kick payment for TANF-related beneficiaries.

8Pennsylvania's mandatory managed care program uses the following factors to adjust rates: age, region, eligibility category, and health status using the CDPS plus pharmacy system. The state's voluntary managed care program uses age, region, and eligibility category to adjust rates, and does not adjust for health status.

9In Tennessee, the long-term services and supports (LTSS) component of the rate is risk-adjusted based on service delivery setting (institutional vs. home/community-based).

10Washington's Health Options managed care program does not adjust rates for eligibility category because its managed care program does not enroll beneficaries with disabilities (i.e., only TANF-related beneficiaries are enrolled). The state operates a managed care program for adults with disabilities in one county; this specialty program--the Washington Medicaid Integrated Partnership or WMIP--was not examined as part of this study.

Risk (Health Status) Adjustment

At the beginning of the study period, most of the states relied only on demographic factors to develop their rates.13 Over time, however, nearly all have adopted more sophisticated methods that base rates on diagnoses and historic healthcare utilization data, in an effort to better match payment to risk and to prevent plan risk selection. As shown in Table 3, seventeen of the study states currently use a “risk adjustment” model to adjust rates for enrollee health status and related risks. These models employ algorithms to assign managed care enrollees into demographic and morbidity or disease categories that each have a specific risk score. The risk score is calculated using historical claims/encounter data—such as diagnosis data from inpatient admissions or pharmacy data—on individuals in the category. States then use the collective risk scores of a health plans’ enrollees to develop a plan-specific capitation rate.

Eleven states use the Chronic Disability Payment System (CDPS) for risk adjustment, the most-commonly used among our study states. Other systems in use include Ingenix Symmetry, Medicaid Rx, Adjusted Clinical Groups (ACG), Clinical Pharmaceutical Groups (CRxG), and Diagnostic Cost Groups (DxCG).14 Among other factors, states considered the type and quality of data available for risk adjustment when deciding which risk adjustment model to adopt. California program officials noted, for instance, that they use a system that relies on Medicaid pharmacy utilization data to assign risk scores, since pharmacy data are more complete and readily available than other forms of encounter data. This is likely related to the prevalence of sub-capitation provider reimbursement models in the California’s Medicaid managed care program; prescription drugs are not part of provider sub-capitation arrangements and are paid on an individual per-prescription basis.

The majority of study states that use risk adjustment models do so to establish rates for all managed care populations. Connecticut and Ohio are the only exceptions to this, and use risk adjustment only for rates for the aged, blind, and disabled population. One state—New Jersey—indicated that it initially used risk-adjustment only for managed care enrollees with disabilities, but began risk-adjusting payments for nondisabled enrollees during the study period.

States typically use a combination of rate adjustments that include both demographic and health status adjustments. Some states have phased in risk adjustment to acclimate health plans and avoid “rate shock”—in California, for example, just 20 percent of the capitation rate is determined using risk adjustment while 80 percent relies on demographic factors. Only one state (Michigan) reported using full risk adjustment, without additional demographic adjustments, to develop rates for people with disabilities.

Maternity-Related and Other Supplemental Payments

More than half of the study states (14, shown in Table 3) make supplemental payments to health plans for maternity-related care provided to enrollees. These are sometimes called maternity “kick” payments because they are paid in addition to the capitation rate. Generally reported in the $5,000 to $10,000 range, maternity kick payments are paid on a per-event (i.e., delivery) basis. Usually the payment supplements the cost of delivery and newborn care, though some states report that their maternity kick payment is also intended to cover the cost of prenatal care. Medicaid program officials described the benefits of these supplemental payments, noting that they protect health plans in the event that a pregnant enrollee changes plans just before or after birth. In that case, only the plan responsible for the delivery costs receives the kick payment. In states without maternity kick payments, program officials noted that other features of their rate setting process account for the additional costs of maternity-related care, primarily the inclusion of age- and sex-specific rate cells for women of childbearing age.

In a few instances, program officials described kick payments for other types of health services, such as newborn care, organ transplants, or care for enrollees with HIV/AIDS. In addition, most states provide a wraparound payment to Federally Qualified Health Centers (FQHCs) in order to assure compliance with the federal cost-based reimbursement requirement for these providers; these payments are generally direct arrangements between the state Medicaid agency and FQHCs, without plan involvement.

Stop-Loss Coverage and Other Risk-Sharing Arrangements

Program officials in roughly half of the study states reported that they provided a risk-sharing arrangement with Medicaid managed care plans. The scope and operation of these arrangements vary considerably. For instance:

- Arizona has a multi-tiered reinsurance program. First, if inpatient care costs for a single enrollee exceed either $25,000 or $35,000 (depending on the plan) in a year, the state begins to share costs, covering 75 percent of any additional inpatient services. If the enrollee’s inpatient costs exceed $650,000 in a year, the state begins to pay for all (100 percent) additional inpatient services. The state also described a “catastrophic reinsurance” plan, whereby the state covers 85 percent of the cost of care provided to enrollees with specific high-cost diagnoses, including Gaucher’s disease, von Willebrand disease, and hemophilia.

- Arizona also uses a reconciliation process to cap plan profits and losses for adult enrollees without dependents—a population experiencing significant recession-related enrollment growth. Since new enrollees in this group were expected to have different health care use patterns than existing (non-recession related) enrollees, the state sought to limit the amount health plans could profit from covering the population. Under the reconciliation process, health plans must remit (in the case of profits) or are reimbursed (in the case of losses) the amount that exceeds the cap.

- New York has a stop-loss program for inpatient care, and caps plan risk at $100,000 of inpatient spending for any single enrollee in a year. The state is responsible for costs exceeding this amount.

- Pennsylvania runs a high-cost risk pool funded by plan premiums. The pool provides additional revenue to a health plan incurring more than $80,000 in costs for any single enrollee in a year.

In a number of the remaining states, Medicaid managed care programs do not provide stop-loss coverage but do require plans to obtain it from a private firm. Minnesota program officials noted that their state had provided stop-loss coverage in the past but, after deciding that it was becoming too much of an administrative burden, began building the cost of this coverage into capitation rates and requiring plans to purchase it privately.

Stakeholder Perceptions of the Medicaid Managed Care Rate Setting Process

Health plans generally described their state’s Medicaid rate setting process as open and transparent. Several expressed satisfaction with the approach, noting that the state engages plans and gives them an opportunity to provide input and raise concerns. A number of plans thought that the rate setting process has evolved and improved over time, becoming more thorough and fair, in part due to states’ adherence to CMS requirements for actuarially sound rates.

At the same time, health plans in a few states expressed dissatisfaction with the rate setting approach. They described it as lacking in transparency, and questioned the soundness of their state’s methodology. In addition, plans in some states were frustrated with Medicaid managed care programs’ use of efficiency adjustments. Generally these involve taking savings realized from plans’ care management practices out of the rates in the next rating period (though in a couple of cases, state program officials described sharing savings with the plan as part of an incentive program). For instance, one plan representative noted, “There is in the Medicaid formula a sort of a disincentive to making improvements. It has to do with the state capturing all savings generated by plans. The state captures 100 percent of savings and there is no incentive to improve the system. That money should go back to plans and fund these initiatives. There would be a sustainable reduction in medical costs.”

Health plans in many states identified ways they thought rate setting could improve; this was true even in states where the process was described positively. Plans’ most common request was for greater transparency, including more granular details about rate methodology. In addition, plans in at least two states thought that the rate setting process did not adequately account for differences in plan provider networks, allowing plans to unfairly select risk by building networks that could discourage enrollees with costlier health care needs (e.g., deliberately excluding certain specialists that treat high-cost conditions). Other plan suggestions included implementing more pay-for-performance initiatives and better long-range planning.

Some state program officials reported that while health plans were initially apprehensive about risk adjustment because it could “take money out from the pockets” of plans with a healthier-than-average enrollee population, over time the plans have become more supportive and appreciative of the practice. Health plan representatives themselves, however, were somewhat more critical of the risk adjustment process, with some expressing a desire for more transparency in this part of the rate setting process in particular. At the same time, plan representatives generally agreed that risk adjustment was a positive development in their state’s rate setting process. They felt that risk adjustment results in plan payments that better reflect the health needs of the population they serve, and also protects plans with large and diverse provider networks from adverse selection.

Most informants reported that their state’s political environment had at least some influence on rate setting, generally through the state budget process. Many of the study states have faced considerable budget deficits in recent years, and this has had a negative effect on plan payment rates. Though state budgets do occasionally prescribe health plan rate reductions, they more often include cuts to Medicaid fee-for-service provider rates, and plan payment rates are reduced accordingly. Health plans can choose to absorb the reductions or they can pass these on to network providers by renegotiating reimbursement rates. Though budget-related rate reductions have become more common in the study states in recent years, most informants emphasized that these changes could only be made within an actuarially sound rate range, effectively limiting how much a state’s budget could influence rates. For instance, one program official noted that, “We know that the rates still have to be actuarially sound, so that’s really the goal and, you know, that’s different from the budgeting... [Rate setting] is very much driven by the underlying data.” Some informants indicated that, prior to the 2002 CMS requirements for actuarially-sound rates, managed care payments were more heavily influenced by their state’s budget; as demonstrated by one program official who said, “The legislature tinkered with rates back in like the late ’90s and early ’00s...it was a little bit more nebulous then. But ever since we really went pure, you know, when [the CMS requirements] came out, we use actuarial-based rates. That’s it.”

CHIP Managed Care Rate Setting Approaches

We focus the analysis of separate CHIP program rate setting on the nine study states that pay health plans capitation rates for CHIP enrollees that are different from Medicaid—that is, California, Connecticut, Delaware, Florida, Michigan, New York, Pennsylvania, Texas and Virginia (Table 4).15 In some of these states (Connecticut, Delaware, Texas, and Virginia) though the capitation rate is different, Medicaid and CHIP rate-setting processes are very similar. In California, Florida, Michigan, New York, and Pennsylvania the rate-setting processes for Medicaid and CHIP are quite different. Indeed, program officials in some of these states noted that when CHIP was established they made great efforts to distinguish the program from Medicaid and to shape it more like a commercial product.

| Approach To Establishing Rates | |||||

|---|---|---|---|---|---|

| State | Administered | Negotiated | Competitive Bidding | Uses Encounter Data to Set Rates | CHIP and Medicaid Rate Setting Are Coordinated |

| California1 | x | ||||

| Connecticut | x | x | x | ||

| Delaware | x | x | x | ||

| Florida | x | ||||

| Michigan | x | ||||

| New York2,3 | x | ||||

| Pennsylvania | x | ||||

| Texas | x | x | x | ||

| Virginia | x | x | x | ||

| TOTAL | 3 | 1 | 5 | 4 | 4 |

Sources: Interviews with Medicaid and CHIP officials, 2011; managed care program documents. Notes:

1 California used competitive bidding for its initial procurement for CHIP plans; since then, rates have been negotiated annually.

2 New York procures health plans through competitive bidding, whereby plans respond to an RFP with a proposed rate. After the initial rate is established, participating health plans are free to request a rate review/increase at any time, though requests must be submitted at least 90 days prior to the requested effective date.

3 New York recently began collecting encounter data from CHIP plans, but had not yet used this data to set capitation rates at the time of our interviews.

Unlike in Medicaid, the CHIP rate-setting process is not bound by federal regulations for actuarial soundness. Though program officials in several states—particularly the four states noted above as having a very similar rate-setting process as Medicaid—indicated that they use Medicaid actuarial soundness principles to guide CHIP rate setting, this was not the case in the other CHIP programs. Consequently, CHIP rate setting does not always involve the step of using an actuary to establish a rate range as a foundation for the rate-setting process. Moreover, only three of the CHIP study states use encounter data for rate setting (Table 4). Other states (New York, Michigan, and Pennsylvania) indicated that they collect CHIP encounter data from health plans, but that it is not yet complete or reliable enough to use for rate setting.

As of 2010, three of the nine study states with CHIP capitation rates that are different from Medicaid use administered rate setting—Michigan, Texas, and Virginia (Table 4). In Texas and Virginia, CHIP rate setting is coordinated with that of Medicaid; in Virginia plans are required to participate in both Medicaid and CHIP, but in Texas this is not the case. Michigan’s CHIP rates are administered separately from Medicaid, and any willing provider can participate if it meets state requirements. CHIP officials in Michigan stated that----in the absence of requirements for an actuarially sound rate-setting process-- administrated rate setting requires less formal data analysis than competitive bidding.

Five of the nine separate CHIP programs we studied use a competitive bidding process (Table 4). In two of these states—Connecticut and Delaware—the process is coordinated with the state’s Medicaid competitive bidding process, and plans are required to submit bids for both Medicaid and CHIP.16 In the other four states with CHIP competitive bidding, the rate setting process is conducted separately—and is quite different—from that of Medicaid, which in those states uses an administered or negotiated process.

One state with competitive bidding for CHIP managed care noted that ensuring a truly competitive process is challenging, because some plans yield considerable market power and the state is compelled to do business with them to ensure access to care for all CHIP enrollees. Program officials noted that this is especially true now that CHIPRA mandates states to provide all CHIP enrollees with a choice of plans (or a Primary Care Case Management (PCCM) or fee-for-service delivery model).

Only one CHIP managed care program (California) uses a negotiated rate setting approach. The state used competitive bidding to procure health plans when CHIP was initially established, but has negotiated rates with plans on an annual basis since then.

CHIP Managed Care Rate Factors and Other Adjustments

In general, CHIP managed care programs are less likely than their Medicaid counterparts to adjust rates using multiple demographic factors, though nearly all of the nine study states with separate CHIP rates use at least one demographic factor in rate setting (Table 5). Most commonly this is enrollee age or geography. Three states adjust CHIP rates for enrollee sex. Michigan is the only state that does not use demographic risk adjustments.

| State | Demographic Factors - Age | Demographic Factors - Sex | Demographic Factors - Region | Demographic Factors - Income | Health Status (Name of System/Method) |

|---|---|---|---|---|---|

| California | x | x | |||

| Connecticut | x | x | |||

| Delaware | x | x | x | x (CDPS) | |

| Florida | x | ||||

| Michigan | |||||

| New York | x | ||||

| Pennsylvania | x | x1 | |||

| Texas | x | x | x2 | x (CDPS) | |

| Virginia | x | x | x | ||

| TOTAL | 5 | 3 | 5 | 3 | 2 |

Sources: Interviews with Medicaid and CHIP officials, 2011; managed care program documents.

1Plans ultimately receive the same capitation amount for children in different income bands, but CHIP enrollees in families with higher incomes pay premiums directly to the plans. Therefore, the state pays plans a lower rate (less the premium) for these enrollees.

2Texas uses income to adjust rates for its CHIP Perinatal program (covering pregnant women and newborns).

In two of the states where CHIP enrollees pay premiums (Pennsylvania and Virginia), the state includes an additional demographic factor in rate setting—income. In Pennsylvania, the state pays a lower capitation rate for CHIP enrollees in higher-income, premium-paying families. The plan is responsible for collecting the premium from families, with the premium making up the lower capitation rate paid by the state for these enrollees. Program officials in Virginia reported a similar arrangement. Other states with CHIP enrollee premiums, such as Florida, noted that they did not adjust their CHIP rates for income because the state collected premiums directly from families.

Health Status (Risk) Adjustment

Just two CHIP programs—in Delaware and Texas—use a risk adjustment model in CHIP rate setting; notably both of these states coordinated their CHIP and Medicaid rate setting processes. In one state that does not use health status risk adjustment for CHIP rates, program officials indicated that there was less need for this step because the CHIP population is comprised of generally healthy (lower risk) children compared to those enrolled in Medicaid.

The Michigan CHIP rate setting process is atypical in that the program does not adjust the capitation rate it pays plans from year to year. Instead, Michigan has paid CHIP plans the same (flat) rate each year since the program began. According to program officials, the rate is typically below what it costs health plans to serve their CHIP enrollees. The state has a cost-settlement arrangement with the largest participating health plan, Blue Cross Blue Shield of Michigan (which has roughly 80 percent of the market) whereby that plan is expected to subsidize CHIP coverage up to $15.5 million each year. If the plan pays out more than $15.5 million above what it receives in CHIP capitation payments, the state begins to pay any additional costs. Michigan officials report that the cost-settlement for the plan was $12.6 million in FY 2010. Program officials noted that they had offered similar cost-settlement arrangements to other participating plans (which have considerably smaller shares of the CHIP market) but that none had taken the option; these plans do, however, continue to participate in the program even under the very low flat rate ($79 per member per month).

Stop-Loss Coverage and Other Risk-Sharing Arrangements

With the exception of Michigan’s cost-settlement process described above, CHIP programs generally do not require or sponsor risk-sharing programs for participating health plans.

Stakeholder Perceptions of the CHIP Managed Care Rate Setting Process

As noted above, in some of the states that pay different rates for enrollees in separate CHIP programs, the rate setting processes for the Medicaid and CHIP are coordinated, and many or all plans serve both programs. These states are Connecticut, Delaware, Texas, and Virginia. Health plan opinions of the coordinated rate setting processes were mixed, with some saying that their state’s processes were open and transparent, and others noting that improvements were needed. Among the remaining states with rate setting processes that are separate from those in Medicaid, health plans expressed generally positive views.

Some informants noted that since CHIP is not bound to the same rules for actuarial soundness that Medicaid is, CHIP rates do not have to be adjusted on a regular basis. This distinction may have advantages and disadvantages, from a plan perspective, since the lack of such standards could result in overly generous rates or rates that are inadequate. Plan perceptions of the adequacy of CHIP rates are examined in greater detail below.

Like Medicaid rates, stakeholders reported that the state’s political environment influenced CHIP rate setting, perhaps to a larger degree than Medicaid given the absence of actuarial soundness requirements for the latter program.

Perceptions of Medicaid and CHIP Rate Adequacy

Informants had mixed views of rate adequacy. Though many described their state’s Medicaid managed care rates as adequate, they frequently qualified this opinion to emphasize that plans, though “surviving,” operate on thin margins and often find it challenging to make a profit. Some informants noted that while rates had been adequate in recent years, they are concerned about the future because their state’s rate-setting process is becoming more rigid. Health plans in a few states reported that rate adequacy fluctuated over time, with more profitable years balancing those that are less profitable.