U.S. Department of Health and Human Services

Does Geographic Location Make a Difference? A Comparative Analysis of the Socio-Demographic and Attitudinal Characteristics of Active Buyers and Non-Buyers of the Federal Long-Term Care Insurance Program

LifePlans, Inc.

September 21, 2004

PDF Version

This policy brief was prepared under contract between the U.S. Department of Health and Human Services (HHS), Office of Disability, Aging and Long-Term Care Policy (DALTCP) and Abt Associates. The brief was written by LifePlans, Inc. For additional information about the study, you may visit the DALTCP home page at http://aspe.hhs.gov/_/office_specific/daltcp.cfm or contact the ASPE Project Officer, Hunter McKay, at HHS/ASPE/DALTCP, Room 424E, H.H. Humphrey Building, 200 Independence Avenue, SW, Washington, DC 20201. His e-mail address is: Hunter.McKay@hhs.gov.

This data brief is one of eight commissioned by the Department of Health and Human Services, Office of the Assistant Secretary for Planning and Evaluation to analyze survey data collected by Long Term Care Partners from members of the federal family regarding the long-term care insurance offering available to them. This brief analyzes how geography is associated with long-term care insurance. The remaining briefs address: a Profile of Buyers; a Profile of Non-Buyers; a Profile of Non-Responders; a Comparison of Active and Retired Buyers, Non-Buyers and Non-Responders; a Comparison of Engagement and Participation among Buyers, Non-Buyers and Non-Responders; a Multivariate Analysis of Buyers and Non-Buyers; and a Comparison of Active Buyers/Non-Buyers in the Federal, Private and Public Sectors. A Literature Review is also available. I. BACKGROUND

One of the more ambitious proposals for encouraging growth in the private insurance market was passage of the Long Term Care Security Act (Public Law 106-265). This Act was passed in the summer of 2000 and was signed into law on September 19th of that year. It authorized the U.S. Office of Personnel Management (OPM) to contract for a long-term care (LTC) insurance program for federal employees. Coverage would be available to active federal employees and annuitants (civilian retirees), as well as active and retired members of the uniformed services. "Qualified relatives" of active workers and military personnel including spouses, adult children, parents, and parents-in-law would also be covered by the program. OPM expected that, like the health and life insurance programs it administers, the Federal Long-Term Care Insurance Program (FLTCIP) would become the largest employer-sponsored LTC insurance program in the nation.

The development of the program was in part meant to send a message to other employers around the country that a "progressive" employer is one that offers LTC insurance to its employees. Naturally it was expected that implementation of the program would spur additional interest and growth in the market. The program began in earnest in July 2002, which constituted the beginning of the open enrollment period. The carriers underwriting the program -- John Hancock and MetLife -- formed a joint venture called Long Term Care Partners, LLC, which is devoted exclusively to administering the program.

Long Term Care Partners conducted one of the largest LTC educational campaigns ever. More than one million people requested enrollment kits. As of August 2004, more than 300,000 applications had been received and more than 210,000 policies issued. About 64% of enrollees were active employees and spouses, 31% annuitants and their spouses, and another 5% surviving spouses, parents/in-laws and adult children. Thus, in relatively short order, the FLTCIP became one of the largest group programs in the United States. In part this was due to the significant marketing and enrollment activities including more than 2,100 educational meetings, briefings to human resources staff and outreach programs to affinity groups.

The large number of enrollments affords a unique opportunity to better understand the attitudes and perspectives of both working and retired individuals regarding LTC concerns, the importance of planning, and the role that insurance may (or may not) play in meeting the needs of disabled individuals. An examination of such attitudes can assist policymakers as well as insurers to better understand marketplace opportunities and barriers, and devise strategies to encourage growth in the market.

II. PURPOSE

This is the eighth in a series of data briefs based on the information collected from active buyers and non-buyers of the federal program. The purpose of this data brief is to determine the extent to which the attitudes, opinions and motivations of individuals who purchased and did not purchase the federal LTC insurance policy are in part a function of geographic location. We are also interested in knowing how geography is associated with their experience with LTC and opinions about LTC insurance. Relevant research questions answered in this brief include (but are not limited to) the following:

- How do the demographic and characteristics of active buyers and non-buyers differ across geographic regions?

- What are the attitudes and opinions about retirement planning among active buyers and non-buyers across geographic regions?

- What are the similarities and/or differences in knowledge of LTC and insurance among individuals in each of the geographic regions?

- Does the extent of exposure to marketing materials and messages vary by geographic region?

III. METHOD AND SAMPLE

Long Term Care Partners used mail surveys to collect information from active buyers and non-buyers. For purposes of this research, the active sample consists of employees who are actively working. A "buyer" is someone who has purchased the insurance plan and paid premiums beyond the free look period. A "non-buyer" is defined as someone who expressed interest in a program but had not purchased the plan at the time that the survey was completed.

Three geographic segments are analyzed: (1) the "DC Area", which comprises the District of Columbia, Maryland, and Virginia; (2) "The East" which comprises all states to the east of Minnesota, Iowa, Missouri, Arkansas and Louisiana; and (3) "The West" which includes all states west of Wisconsin, Illinois, Kentucky, Tennessee and Mississippi. As shown, about 3,300 individuals participated in the various surveys of active and retired buyers and non-buyers. Table 1 below summarizes the sample sizes by market segment and geographic regions.

| Table 1: Distribution of Sample by Market Segment and Geographic Region |

|---|

| | Washington, D.C. | The East | The West |

|---|

| Active Buyers | 196 | 210 | 228 |

|---|

| Active Non-Buyers | 94 | 238 | 223 |

|---|

| Retired Buyers | 226 | 427 | 445 |

|---|

| Retired Non-Buyers | 76 | 257 | 243 |

|---|

| Total | 632 | 1,348 | 1,363 |

|---|

IV. FINDINGS

A. Demographic and Employment Characteristics

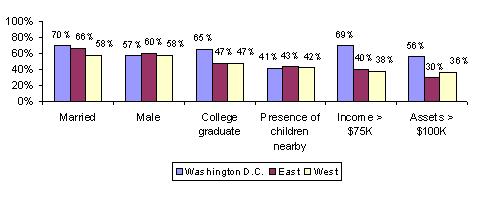

Figure 1 summarizes important demographic characteristics of the aggregate active sample of buyers and Figure 2 shows similar characteristics for active non-buyers. Across each of the regions the majority of buyers are married, male, have children living nearby and are highly educated. The average age of buyers across the regions varies between 52 and 54 years. There are statistically significant differences on three variables: income, assets, and education status. Buyers in Washington, D.C. are more likely to be college graduates and to have higher incomes and assets. In fact, the average income of buyers in the D.C. area is $98,261 compared to $81,710 in other regions of the country. Asset differentials are even greater; the average value of liquid assets of active buyers in D.C. is about $226,000 compared to roughly $186,000 in other areas of the country.

| Figure 1: Demographic Characteristics of Active Buyers by Geographic Region |

|

| Source: Analysis of data from the FLTCIP, 2003. |

As shown in Figure 2, the same pattern of results holds true for non-buyers. Again, the only significant demographic differences across regions are education status and income and asset levels. Non-buyers in Washington, D.C. are more likely to be educated and have significantly higher levels of income and assets -- $92,000 compared to $70,000 (income) and $180,000 compared to $158,000 (assets).

While there are no significant age differences between buyers and non-buyers across the regions, buyers tend to be more educated, wealthier and less likely to be married and have children living nearby. This could suggest that buyers may view having the insurance as compensating for their perceived lack of family support, which is still the largest contributor of long term care services.

| Figure 2: Demographic Characteristics of Active Non-Buyers by Geographic Region |

|

| Source: Analysis of data from the FLTCIP, 2003. |

The patterns observed for the active sample of buyers and non-buyers also holds true for the retired sample. In both cases, retiree buyers and non-buyers in Washington, D.C. have higher incomes and are better educated than those in the East and West. There are, however, no significant differences in asset levels. Again, retired buyers tend to be wealthier and more educated than non-buyers across all of the regions. Finally, in contrast to the sample of actives, there were no significant differences in the marital status of buyers and non-buyers by geographic regions. Retired buyers in the west, however, are the least likely to have children living nearby. (See Appendix for more detailed information on retirees.)

B. Attitudes and Experience with Retirement Planning and Long-Term Care

Previous briefs have established that federal employees tend to be active in planning for their retirement and understand the potential LTC risks associated with later life. Their life experiences with relatives or friends may also influence their decisions regarding the purchase of insurance. We asked a series of questions designed to illuminate key differences between buyers and non-buyers across the three geographic regions.

There are few differences across geographic regions among buyers regarding attitudes and opinions about retirement planning. Most (80%) have at least a general sense for how much to save to live comfortably in retirement, have thought about how to pay for LTC (96%) and believe having the insurance is important to retirement planning (97%). Geographic region is also not associated with non-buyers' attitudes about these issues. However, across all regions non-buyers are less likely to have thought about these issues or believe that insurance is an important part of a retirement plan. By and large, these same patterns hold true for the retired sample.

With few exceptions, geographic region is also unrelated to active employees' experience with LTC and attitudes about risk. Active buyers in Washington, D.C. are, however, somewhat less likely to know someone who has experienced financial hardship as a result of caring for an elderly relative. (Note that this population also is has higher levels of income and assets than buyers elsewhere.) Regarding retirees, buyers in the east are the most likely to have had caregiving experience -- 39% compared to 26% -- to have experienced financial hardship as a result of caring for an elderly relative -- 7% compared to 3% -- and know someone who has experienced financial hardship as a result of caring for an elderly relative -- 42% compared to 35%. There were no significant differences in experience across regions among non-buyers.

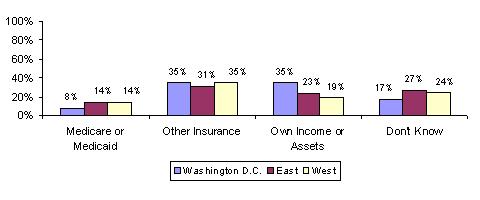

In past research, one factor that has distinguished buyers from non-buyers is their knowledge of potential payment sources for LTC. The insurance industry has invested heavily in educating consumers about LTC financing and there was an extensive educational campaign for the federal program. In order to gauge the effectiveness of that education, we asked buyers and non-buyers who they believe would pay for LTC if they ever needed it. There were no significant differences in responses among buyers. Among active non-buyers, however, there was an important geographic difference regarding knowledge of payment source for LTC services. Figure 3 summarizes results among active non-buyers and shows that those in the Washington, D.C. area are more likely to understand that they will have to use their own income and assets to pay for care if it is needed.

| Figure 3: Active Non-Buyers View of Who Will Pay for Long-Term Care if it is Needed by Geographic Region |

|

| Source: Analysis of data from the FLTCIP, 2003. |

Non-buyers in Washington, D.C. are also most likely to understand that Medicare or Medicaid will not pay for their LTC expenses. Finally, the further away from Washington, D.C. one gets, the more likely is there to be uncertainty about how LTC costs would be paid if services were needed. This finding may suggest that at least with respect to payment source knowledge, the education campaign in the Washington, D.C. area was more effective than in other parts of the country. Alternatively, it may be that given the higher levels of education, this is knowledge that these individuals had even before the marketing campaign began. These trends were not evident among the retiree sample.

Non-buyers of the federal program were also asked whether or not they currently had LTC insurance and whether they bought the insurance after they heard about the federal program. As shown in Figure 4, non-buyers of the federal program in the Washington, D.C. area are twice as likely to purchase LTC insurance as non-buyers in other geographic regions. Moreover, they are the most likely to have bought the insurance after hearing about the federal program. Somewhat surprisingly, of those non-buyers in the East and West who had insurance, a meaningful proportion of them -- between 17% and 25% -- had not heard about the federal program. This finding again suggests that the education and marketing campaign was either heavily targeted or particularly effective in the Washington, D.C. area. It also suggests that other carriers benefited from the wide net cast by the campaign: between one in five and one in ten non-buyers actually purchased a non-federal policy.

| Figure 4: Active Non-Buyers Purchase of Long-Term Care Insurance by Geographic Region |

|

| Source: Analysis of data from the FLTCIP, 2003. |

C. Experience with the Application Process and Exposure to Promotional Materials

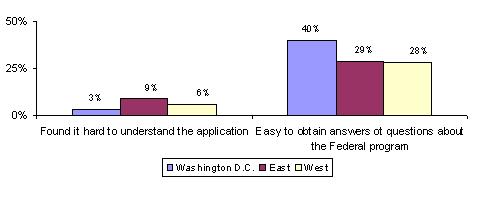

Given some of the major differences in education level and the fact that the program was national in scope, one might have expected differences across geographic region in peoples' experience with the application process. In a prior brief, we demonstrated that non-buyers had a more difficult time understanding the application materials and getting their questions answered than did buyers. This finding holds true across all geographic regions. However, among active buyers, those in the Washington, D.C. area seemed to have an easier time understanding the application and also found it easier to obtain answers to their questions about the program (see Figure 5).

| Figure 5: Active Buyers Experience with Application Process by Geographic Region |

|

| Source: Analysis of data from the FLTCIP, 2003. |

The program sponsors -- Long Term Care Partners -- invested significant resources in the marketing and education campaign. They did so through sponsorship of a variety of promotional activities such as educational meetings, satellite broadcasts, advertisements, articles, brochures, web sites, toll-free numbers, and more. This was done to assure maximum exposure to the program. As outlined in a previous brief, we found that non-buyers were less likely to have actively engaged in activities designed to educate and reinforce the need for insurance protection against the cost of LTC. This is fairly typical across the geographic regions. The extent of non-buyer exposure to educational activities does not vary by geographic region except when it comes to visiting the website and reading articles about the program; non-buyers in Washington, D.C. are far more likely to have visited the website (62%) than are non-buyers elsewhere (34%). They are also more likely to have read newspaper articles about the program than non-buyers elsewhere -- 57% compared to 29%.

The same can be said of buyers: for the most part, exposure does not vary by geographic region. The exception is that compared to buyers in the West and in the D.C. area, those in the East are the least likely to talk to federal colleagues about the program. On the other hand, they are more likely to have read newspaper articles than non-buyers elsewhere. There are few significant variations in exposure by geographic region for the retiree population. Again, retirees living in Washington, D.C. are far more likely to have read newspaper articles about the program than retirees elsewhere.

V. CONCLUSIONS

For the most part, there are few geographic differences in the attitudes and opinions of buyers and non-buyers of the federal program regarding retirement planning and LTC. There are, however, a number of important socio-demographic differences (i.e., those living in the Washington, D.C. area tend to be more highly educated and wealthier), as well as those relating to experience with LTC, especially among retirees. Retirees in the D.C. area have more experience caregiving and are more likely to either know someone who has had, or to have personally experienced, financial hardship as a result of LTC.

Non-buyers in the Washington, D.C. area are also more likely to have purchased a LTC insurance policy not sponsored by the Federal Government than non-buyers in other areas of the country. Moreover, the fact that a meaningful proportion of non-buyers in the East and West who had purchased other policies had not even heard of the federal program, suggests that the marketing campaign may not have been as effective in these areas. This is somewhat supported by the finding that non-buyers outside of Washington, D.C. are also less likely to have been involved in certain promotional activities.

The analysis presented here has focused to a large extent on observed differences between geographic regions on selected variables. It is important to note that on the vast majority of parameters examined, geography is not a particularly important variable.

Notes for Tables

All significance tests are based on 5% level or better. Notations for significance are as follows: If one category out of three contains the symbol (*), then the category starred is statistically different from each of the other two categories, but the non-starred categories are not different from each other. If two categories out of the three contain the symbol (*), then those two categories are statistically different from each other, but each of those categories is not statistically different from the third one. If all three categories contain the symbol (*), then all three are statistically different from each other.

Unless otherwise specified, only the response category that has a notation of significance was tested against all other categories. In some cases, it was determined that a combination of categories would be tested. These are indicated in the footnotes. It also may be the case that if categories were or were not combined, it could change the results of the test of significance.

Unless otherwise indicated, the first response category (i.e., strongly agree, very important, very likely, etc.) or the yes response was tested. Therefore, if there are no notations for significance, the test was not significant at the 5% level.

| TABLE A-1: Socio-Demographic Characteristics of Active Buyers and Non-Buyers by Geographic Location (D.C. vs. East vs. West) |

|---|

| Socio-Demographic Characteristics | Active Buyers DC | Active Buyers East | Active Buyers West | Active Non-Buyers DC | Active Non-Buyers East | Active Non-Buyers West |

|---|

| Average age | 53 | 52 | 54 | 52 | 54 | 54 |

|---|

| Less than 50 | 27 | 31 | 22 | 40 | 30 | 32 |

|---|

| 50 to 54 | 26 | 23 | 26 | 24 | 26 | 23 |

|---|

| 55 to 59 | 27 | 26 | 25 | 18 | 20 | 20 |

|---|

| 60 to 64 | 13 | 15 | 18 | 8 | 9 | 13 |

|---|

| 65 and over | 7 | 5 | 9 | 10 | 15 | 12 |

|---|

| Gender |

|---|

| Male | 46 | 50 | 53 | 57 | 60 | 58 |

|---|

| Female | 54 | 50 | 47 | 43 | 40 | 42 |

|---|

| Marital status |

|---|

| Never Married | 22 | 17 | 13 | 11 | 9 | 9 |

|---|

| Married | 57 | 61 | 59 | 70 | 66 | 73 |

|---|

| Divorced/separated | 15 | 15 | 24 | 16 | 20 | 14 |

|---|

| Widowed | 4 | 5 | 3 | 2 | 4 | 3 |

|---|

| Domestic Partner | 2 | 2 | 1 | 1 | 1 | 1 |

|---|

| Presence of children living within 25 miles |

|---|

| Yes | 41 | 43 | 42 | 53 | 63 | 59 |

|---|

| No | 59 | 57 | 58 | 47 | 37 | 41 |

|---|

| Education level |

|---|

| Less than high graduate | 0 | 0 | 0 | 0 | 1 | 0 |

|---|

| High school graduate | 4 | 9 | 4 | 7 | 17 | 12 |

|---|

| Technical/ trade/ business school | 2 | 4 | 7 | 5 | 7 | 4 |

|---|

| Some college | 15 | 20 | 25 | 23 | 28 | 37 |

|---|

| College graduate1 | 36 |  79* 79* | 34 | 67 | 39 | 64 | 20 | 65* | 29 | 47 | 29 | 47 |

|---|

| Graduate degree | 43 | 33 | 25 | 45 | 18 | 18 |

|---|

| Average income2 | $98,261* | $81,714 | $81,709 | $92,386* | $70,692 | $69,603 |

|---|

| Less than $15,000 | 0 | 0 | 0 | 0 | 1 | 1 |

|---|

| $15,000 to $24,999 | 0 | 1 | 1 | 1 | 1 | 1 |

|---|

| $25,000 to $34,999 | 3 | 3 | 3 | 3 | 4 | 7 |

|---|

| $35,000 to $39,999 | 1 | 2 | 2 | 2 | 7 | 7 |

|---|

| $40,000 to $49,999 | 2 | 11 | 10 | 5 | 15 | 16 |

|---|

| $50,000 to $59,999 | 3 | 12 | 11 | 8 | 15 | 12 |

|---|

| $60,000 to $69,999 | 10 | 10 | 12 | 7 | 10 | 11 |

|---|

| $70,000 to $74,999 | 7 | 8 | 8 | 5 | 7 | 7 |

|---|

| $75,000 to $99,999 | 21 | 23 | 24 | 20 | 22 | 18 |

|---|

| $100,000 to $124,999 | 17 | 15 | 13 | 23 | 10 | 14 |

|---|

| $125,000 or more | 36 | 15 | 16 | 26 | 8 | 6 |

|---|

| Average liquid assets2 | $184,919 | $190,856 | $225,833 | $180,920 | $162,053 | $153,378 |

|---|

| Less than $10,000 | 4 | 9 | 7 | 13 | 18 | 17 |

|---|

| $10,000 to $19,999 | 3 | 3 | 4 | 5 | 10 | 7 |

|---|

| $20,000 to $29,999 | 5 | 6 | 4 | 3 | 8 | 8 |

|---|

| $30,000 to $49,999 | 10 | 8 | 12 | 9 | 13 | 12 |

|---|

| $50,000 to $74,999 | 7 | 12 | 19 | 8 | 14 | 11 |

|---|

| $75,000 to $99,999 | 8 | 10 | 5 | 6 | 7 | 9 |

|---|

| $100,000 to $124,999 | 8 | 9 | 9 | 7 | 7 | 8 |

|---|

| $125,000 to $149,999 | 4 | 7 | 5 | 8 | 4 | 6 |

|---|

| $150,000 to $199,999 | 13 | 6 | 9 | 3 | 5 | 4 |

|---|

| $200,000 to $249,999 | 10 | 10 | 9 | 2 | 3 | 6 |

|---|

| $250,000 and above | 28 | 20 | 17 | 36 | 11 | 12 |

|---|

| Home ownership |

|---|

| Yes | 90 | 91 | 90 | 87 | 83 | 89 |

|---|

| No | 10 | 9 | 10 | 13 | 17 | 11 |

|---|

- Here, having a college degree or better is tested for significance against not having a college degree.

- Averages were calculated by taking the midpoints of the ranges.

|

| TABLE A-2: Socio-Demographic Characteristics of Retired Buyers and Non-Buyers by Geographic Location (D.C. vs. East vs. West) |

|---|

| Socio-Demographic Characteristics | Retired Buyers DC | Retired Buyers East | Retired Buyers West | Retired Non-Buyers DC | Retired Non-Buyers East | Retired Non-Buyers West |

|---|

| Average age | 65* | 66 | 66* | 70 | 71 | 72 |

|---|

| Less than 50 | 3 | 1 | 1 | 3 | 2 | 2 |

|---|

| 50 to 54 | 3 | 4 | 2 | 5 | 3 | 2 |

|---|

| 55 to 59 | 18 | 13 | 12 | 10 | 7 | 7 |

|---|

| 60 to 64 | 23 | 24 | 25 | 8 | 14 | 10 |

|---|

| 65 and over | 53 | 58 | 60 | 74 | 74 | 79 |

|---|

| Gender |

|---|

| Male | 71 | 71 | 69 | 68 | 71 | 79 |

|---|

| Female | 29 | 29 | 31 | 32 | 29 | 21 |

|---|

| Marital status |

|---|

| Never Married | 9 | 9 | 8 | 4 | 5 | 3 |

|---|

| Married | 71 | 67 | 69 | 67 | 69 | 73 |

|---|

| Divorced/separated | 8 | 8 | 11 | 10 | 9 | 7 |

|---|

| Widowed | 10 | 14 | 11 | 19 | 17 | 17 |

|---|

| Domestic Partner | 2 | 2 | 1 | 0 | 0 | 0 |

|---|

| Presence of children living within 25 miles |

|---|

| Yes | 59* | 52 | 48* | 60 | 55 | 54 |

|---|

| No | 42 | 48 | 52 | 40 | 45 | 46 |

|---|

| Education level |

|---|

| Less than high graduate | 0 | 2 | 0 | 0 | 4 | 5 |

|---|

| High school graduate | 11 | 18 | 13 | 12 | 19 | 16 |

|---|

| Technical/ trade/ business school | 4 | 6 | 5 | 7 | 8 | 8 |

|---|

| Some college | 17 | 21 | 24 | 31 | 26 | 32 |

|---|

| College graduate1 | 35* | 28* | 31 | 32 | 24 | 23 |

|---|

| Graduate degree | 33 | 25 | 27 | 18 | 19 | 16 |

|---|

| Average income2 | $79,825* | $62,330 | $59,547 | $63,918* | $49,522 | $47,304 |

|---|

| Less than $15,000 | 1 | 1 | 0 | 2 | 3 | 5 |

|---|

| $15,000 to $24,999 | 1 | 3 | 4 | 6 | 12 | 16 |

|---|

| $25,000 to $34,999 | 2 | 11 | 10 | 9 | 15 | 10 |

|---|

| $35,000 to $39,999 | 4 | 10 | 9 | 12 | 13 | 17 |

|---|

| $40,000 to $49,999 | 12 | 15 | 17 | 12 | 18 | 16 |

|---|

| $50,000 to $59,999 | 13 | 14 | 18 | 9 | 11 | 13 |

|---|

| $60,000 to $69,999 | 10 | 13 | 12 | 7 | 7 | 9 |

|---|

| $70,000 to $74,999 | 6 | 9 | 7 | 12 | 5 | 2 |

|---|

| $75,000 to $99,999 | 19 | 16 | 15 | 19 | 12 | 6 |

|---|

| $100,000 to $124,999 | 17 | 6 | 4 | 3 | 2 | 4 |

|---|

| $125,000 or more | 15 | 4 | 4 | 9 | 2 | 2 |

|---|

| Average liquid assets2 | $126,798 | $204,151 | $212,063 | $181,607 | $170,558 | $162,813 |

|---|

| Less than $10,000 | 4 | 3 | 4 | 3 | 12 | 12 |

|---|

| $10,000 to $19,999 | 1 | 4 | 3 | 7 | 5 | 7 |

|---|

| $20,000 to $29,999 | 2 | 2 | 4 | 6 | 6 | 8 |

|---|

| $30,000 to $49,999 | 6 | 9 | 7 | 10 | 12 | 13 |

|---|

| $50,000 to $74,999 | 9 | 9 | 10 | 7 | 10 | 8 |

|---|

| $75,000 to $99,999 | 7 | 9 | 6 | 7 | 7 | 5 |

|---|

| $100,000 to $124,999 | 9 | 7 | 8 | 10 | 7 | 4 |

|---|

| $125,000 to $149,999 | 4 | 6 | 6 | 4 | 5 | 5 |

|---|

| $150,000 to $199,999 | 6 | 8 | 11 | 9 | 7 | 8 |

|---|

| $200,000 to $249,999 | 8 | 7 | 8 | 4 | 5 | 8 |

|---|

| $250,000 and above | 44 | 36 | 33 | 33 | 24 | 22 |

|---|

| Home ownership |

|---|

| Yes | 94 | 92 | 92 | 90 | 90 | 91 |

|---|

| No | 6 | 8 | 8 | 10 | 10 | 9 |

|---|

- Here, having a college degree or better is tested for significance against not having a college degree.

- Averages were calculated by taking the midpoints of the ranges.

|

| TABLE A-3: Attitudes and Opinions About Retirement Planning and Long-Term Care Among Active Buyers and Non-Buyers by Geographic Location (D.C. vs. East vs. West) |

|---|

| Attitudes and Opinions | Active Buyers DC | Active Buyers East | Active Buyers West | Active Non-Buyers DC | Active Non-Buyers East | Active Non-Buyers West |

|---|

| Determined how much to save to live comfortably in retirement |

|---|

| Yes, a definite sense1 | 25 | 20 | 21 | 14 | 17 | 15 |

|---|

| Yes, a general sense | 56 | 62 | 62 | 61 | 44 | 53 |

|---|

| No | 18 | 17 | 16 | 22 | 36 | 31 |

|---|

| Do not plan to retire | 1 | 1 | 1 | 3 | 3 | 1 |

|---|

| Thought given to paying for LTC expenses |

|---|

| A great deal | 65 | 63 | 59 | 25 | 21 | 21 |

|---|

| Some | 32 | 33 | 37 | 54 | 50 | 49 |

|---|

| Not much thought | 3 | 4 | 4 | 21 | 21 | 26 |

|---|

| No thought at all | 0 | 0 | 0 | 0 | 8 | 4 |

|---|

| How important is LTC insurance to retirement planning |

|---|

| Very important | 61 | 61 | 60 | 24 | 26 | 23 |

|---|

| Somewhat important | 36 | 36 | 38 | 57 | 51 | 56 |

|---|

| Not very important | 3 | 2 | 2 | 13 | 19 | 12 |

|---|

| Not at all important | 0 | 0 | 0 | 1 | 0 | 2 |

|---|

| Have not started planning | 0 | 1 | 0 | 5 | 4 | 7 |

|---|

| LTC insurance programs sold today will cover the cost of LTC services needed in the future |

|---|

| Strongly agree | 10 | 9 | 9 | 1 | 2 | 5 |

|---|

| Agree | 74 | 71 | 72 | 47 | 34 | 38 |

|---|

| Disagree | 13 | 17 | 17 | 42 | 53 | 49 |

|---|

| Strongly disagree | 3 | 3 | 2 | 10 | 11 | 8 |

|---|

| How would LTC costs be paid2 |

|---|

| Medicaid | 1 | 4 | 2 | 3 | 3 | 4 |

|---|

| Medicare | 7 | 10 | 8 | 5 | 11 | 10 |

|---|

| Medigap Supplement Policy | 1 | 2 | 1 | 0 | 1 | 0 |

|---|

| Own health insurance or retiree health care plan | 24 | 23 | 23 | 35 | 30 | 35 |

|---|

| Own income | 39 | 35 | 38 | 35* | 23 | 19* |

|---|

| Children will help pay | 1 | 1 | 1 | 0 | 0 | 1 |

|---|

| Other | 3 | 2 | 3 | 4 | 4 | 2 |

|---|

| LTC insurance | 6 | 7 | 6 | 1 | 1 | 3 |

|---|

| Don't know3 | 18 | 16 | 18 | 17 | 27 | 24 |

|---|

- Here, having a general or a definite sense of how much needs to be saved were combined and tested as a single yes response. Those who did not plan to retire were removed from the analysis.

- Active buyers were asked whether they worried about how to pay for LTC services before they purchased the FLTCIP and how they would pay for LTC in the absence of their LTC policy.

- This response category was tested for significance and it was found not to be significant.

|

| TABLE A-4: Attitudes and Opinions About Retirement Planning and Long-Term Care Among Retired Buyers and Non-Buyers by Geographic Location (D.C. vs. East vs. West) |

|---|

| Attitudes and Opinions | Retired Buyers DC | Retired Buyers East | Retired Buyers West | Retired Non-Buyers DC | Retired Non-Buyers East | Retired Non-Buyers West |

|---|

| Determined how much to save to live comfortably in retirement |

|---|

| Yes, a definite sense1 | 32 | 28 | 25 | 18 | 15 | 19 |

|---|

| Yes, a general sense | 51 | 59 | 61 | 47 | 58 | 50 |

|---|

| No | 17 | 13 | 14 | 35 | 27 | 31 |

|---|

| Thought given to paying for LTC expenses |

|---|

| A great deal | 68 | 68 | 62 | 27 | 25 | 28 |

|---|

| Some | 30 | 30 | 35 | 53 | 59 | 52 |

|---|

| Not much thought | 2 | 2 | 2 | 18 | 12 | 18 |

|---|

| No thought at all | 0 | 0 | 1 | 2 | 4 | 2 |

|---|

| How important is LTC insurance to retirement planning |

|---|

| Very important | 58 | 62 | 55 | 14 | 21 | 21 |

|---|

| Somewhat important | 40 | 37 | 41 | 47 | 42 | 48 |

|---|

| Not very important | 2 | 1 | 4 | 23 | 24 | 19 |

|---|

| Not at all important | 0 | 0 | 0 | 8 | 6 | 3 |

|---|

| Have not started planning | 0 | 0 | 0 | 8 | 7 | 9 |

|---|

| LTC insurance programs sold today will cover the cost of LTC services needed in the future |

|---|

| Strongly agree | 8 | 13* | 8* | 6 | 3 | 3 |

|---|

| Agree | 72 | 67 | 70 | 29 | 32 | 34 |

|---|

| Disagree | 19 | 18 | 19 | 47 | 47 | 47 |

|---|

| Strongly disagree | 1 | 2 | 3 | 18 | 18 | 16 |

|---|

| How would LTC costs be paid2 |

|---|

| Medicaid | 2 | 2 | 1 | 2 | 3 | 1 |

|---|

| Medicare | 6 | 5 | 7 | 13 | 14 | 16 |

|---|

| Medigap Supplement Policy | 0 | 1 | 1 | 2 | 2 | 2 |

|---|

| Own health insurance or retiree health care plan | 14 | 16 | 17 | 30 | 22 | 18 |

|---|

| Own income | 62 | 57 | 54 | 43 | 42 | 42 |

|---|

| Children will help pay | 0 | 0 | 0 | 0 | 1 | 0 |

|---|

| Other | 1 | 2 | 2 | 4 | 2 | 2 |

|---|

| LTC insurance | 8 | 9 | 9 | 0 | 1 | 2 |

|---|

| Don't know3 | 7 | 8 | 9 | 6 | 13 | 17 |

|---|

- Here, having a general or a definite sense of how much needs to be saved were combined and tested as a single yes response. Those who did not plan to retire were removed from the analysis.

- Retired buyers were asked whether they worried about how to pay for LTC services before they purchased the FLTCIP and how they would pay for LTC in the absence of their LTC policy.

- This response category was tested for significance and it was found not to be significant.

|

| TABLE A-5: Experience with Long-Term Care Among Active Buyers and Non-Buyers by Geographic Location (D.C. vs. East vs. West) |

|---|

| Experiences with LTC | Active Buyers DC | Active Buyers East | Active Buyers West | Active Non-Buyers DC | Active Non-Buyers East | Active Non-Buyers West |

|---|

| Parent needed LTC |

|---|

| Yes | 43 | 41 | 43 | 53 | 48 | 41 |

|---|

| No | 57 | 59 | 57 | 47 | 52 | 59 |

|---|

| The repondent has been a caregiver |

|---|

| Yes | 24 | 32 | 24 | 17 | 24 | 28 |

|---|

| No | 76 | 68 | 76 | 83 | 76 | 72 |

|---|

| The respondent knew someone who used most of his/her assets to pay for LTC |

|---|

| Yes | 45* | 58* | 55 | 44 | 47 | 52 |

|---|

| No | 55 | 42 | 46 | 56 | 53 | 48 |

|---|

| The respondent has experienced financial hardship as a result of caring for an elderly relative |

|---|

| Yes | 4 | 10 | 5 | 3 | 11 | 9 |

|---|

| No | 96 | 90 | 95 | 97 | 89 | 91 |

|---|

| The respondent knew someone who has experienced financial hardship as a result of caring for an elderly relative |

|---|

| Yes | 32* | 49 | 48 | 34 | 41 | 44 |

|---|

| No | 68 | 51 | 52 | 66 | 59 | 56 |

|---|

| TABLE A-6: Experience with Long-Term Care Among Retired Buyers and Non-Buyers by Geographic Location (D.C. vs. East vs. West) |

|---|

| Experiences with LTC | Retired Buyers DC | Retired Buyers East | Retired Buyers West | Retired Non-Buyers DC | Retired Non-Buyers East | Retired Non-Buyers West |

|---|

| Parent needed LTC |

|---|

| Yes | 34 | 39 | 43 | 49 | 49 | 52 |

|---|

| No | 66 | 61 | 57 | 51 | 51 | 48 |

|---|

| The repondent has been a caregiver |

|---|

| Yes | 28 | 39* | 24 | 39 | 43 | 32 |

|---|

| No | 72 | 61 | 76 | 61 | 57 | 68 |

|---|

| The respondent knew someone who used most of his/her assets to pay for LTC |

|---|

| Yes | 60 | 59 | 51* | 49 | 52 | 51 |

|---|

| No | 40 | 41 | 49 | 51 | 48 | 49 |

|---|

| The respondent has experienced financial hardship as a result of caring for an elderly relative |

|---|

| Yes | 4 | 7* | 3* | 4 | 12 | 7 |

|---|

| No | 96 | 93 | 97 | 96 | 88 | 93 |

|---|

| The respondent knew someone who has experienced financial hardship as a result of caring for an elderly relative |

|---|

| Yes | 37 | 42* | 33* | 33 | 37 | 38 |

|---|

| No | 63 | 58 | 67 | 67 | 63 | 62 |

|---|

| TABLE A-7: Self-Assessed Risk of Needing LTC Among Active Buyers and Non-Buyers by Geographic Location (D.C. vs. East vs. West) |

|---|

| Type of LTC | Active Buyers DC | Active Buyers East | Active Buyers West | Active Non-Buyers DC | Active Non-Buyers East | Active Non-Buyers West |

|---|

| How likely is it that: |

|---|

| a) the respondent thinks he/she will need help with everyday activities such as bathing and dressing |

|---|

| Very likely | 10 | 12 | 14 | 5 | 12 | 10 |

|---|

| Likely | 19 | 16 | 15 | 9 | 15 | 14 |

|---|

| Somewhat likely | 40 | 45 | 46 | 36 | 35 | 35 |

|---|

| Not very likely | 25 | 23 | 21 | 38 | 30 | 28 |

|---|

| Not at all likely | 6 | 4 | 4 | 12 | 8 | 13 |

|---|

| b) the respondent thinks he/she will need home care services for more than three months |

|---|

| Very likely | 12 | 15 | 13 | 5 | 11 | 9 |

|---|

| Likely | 19 | 16 | 21 | 11 | 15 | 14 |

|---|

| Somewhat likely | 45 | 49 | 41 | 43 | 37 | 38 |

|---|

| Not very likely | 21 | 16 | 22 | 29 | 30 | 28 |

|---|

| Not at all likely | 3 | 4 | 3 | 12 | 7 | 11 |

|---|

| c) the respondent thinks he/she will need nursing home care for more than three months |

|---|

| Very likely | 11 | 13 | 13 | 8 | 11 | 9 |

|---|

| Likely | 17 | 17 | 16 | 9 | 13 | 16 |

|---|

| Somewhat likely | 41 | 43 | 42 | 40 | 32 | 32 |

|---|

| Not very likely | 25 | 20 | 24 | 31 | 34 | 29 |

|---|

| Not at all likely | 6 | 7 | 5 | 12 | 10 | 14 |

|---|

| d) the respondent thinks he/she will need care provided in assisted living facility for more than three months |

|---|

| Very likely | 16 | 17 | 16 | 13 | 12 | 9 |

|---|

| Likely | 21 | 21 | 22 | 16 | 16 | 17 |

|---|

| Somewhat likely | 43 | 41 | 37 | 42 | 34 | 35 |

|---|

| Not very likely | 17 | 16 | 22 | 21 | 29 | 28 |

|---|

| Not at all likely | 3 | 5 | 3 | 8 | 9 | 11 |

|---|

| TABLE A-8: Self-Assessed Risk of Needing LTC Among Retired Buyers and Non-Buyers by Geographic Location (D.C. vs. East vs. West) |

|---|

| Type of LTC | Retired Buyers DC | Retired Buyers East | Retired Buyers West | Retired Non-Buyers DC | Retired Non-Buyers East | Retired Non-Buyers West |

|---|

| How likely is it that: |

|---|

| a) the respondent thinks he/she will need help with everyday activities such as bathing and dressing |

|---|

| Very likely | 4* | 9* | 7 | 6 | 14 | 13 |

|---|

| Likely | 17 | 19 | 15 | 14 | 15 | 21 |

|---|

| Somewhat likely | 47 | 47 | 43 | 32 | 40 | 37 |

|---|

| Not very likely | 24 | 20 | 28 | 33 | 26 | 20 |

|---|

| Not at all likely | 8 | 5 | 7 | 14 | 5 | 9 |

|---|

| b) the respondent thinks he/she will need home care services for more than three months |

|---|

| Very likely | 5 | 7 | 7 | 6 | 12 | 13 |

|---|

| Likely | 20 | 20 | 15 | 15 | 16 | 20 |

|---|

| Somewhat likely | 49 | 47 | 47 | 39 | 40 | 38 |

|---|

| Not very likely | 19 | 21 | 24 | 23 | 26 | 20 |

|---|

| Not at all likely | 7 | 5 | 7 | 17 | 6 | 9 |

|---|

| c) the respondent thinks he/she will need nursing home care for more than three months |

|---|

| Very likely | 4 | 7 | 6 | 6 | 12 | 11 |

|---|

| Likely | 17 | 18 | 14 | 12 | 14 | 14 |

|---|

| Somewhat likely | 43 | 45 | 44 | 43 | 35 | 37 |

|---|

| Not very likely | 28 | 25 | 27 | 14 | 31 | 27 |

|---|

| Not at all likely | 8 | 5 | 9 | 25 | 8 | 11 |

|---|

| d) the respondent thinks he/she will need care provided in assisted living facility for more than three months |

|---|

| Very likely | 7 | 10 | 8 | 4 | 13 | 10 |

|---|

| Likely | 21 | 20 | 20 | 16 | 15 | 13 |

|---|

| Somewhat likely | 47 | 46 | 44 | 35 | 36 | 45 |

|---|

| Not very likely | 18 | 19 | 22 | 27 | 28 | 22 |

|---|

| Not at all likely | 7 | 5 | 6 | 18 | 8 | 10 |

|---|

| TABLE A-9: Opinions about Long-Term Care Insurance Among Active Buyers by Geographic Location (D.C. vs. East vs. West) |

|---|

| Opinions about LTC Insurance | Active Buyers DC | Active Buyers East | Active Buyers West |

|---|

| What % of your expenses do you expect your LTC insurance to pay |

|---|

| 100% | 12 | 17 | 9 |

|---|

| 61%-99% | 67 | 67 | 70 |

|---|

| 40%-60% | 19 | 13 | 17 |

|---|

| 35%-39% | 1 | 2 | 4 |

|---|

| 25% | 1 | 1 | 0 |

|---|

| TABLE A-10: Opinions about Long-Term Care Insurance Among Retired Buyers by Geographic Location (D.C. vs. East vs. West) |

|---|

| Opinions about LTC Insurance | Retired Buyers DC | Retired Buyers East | Retired Buyers West |

|---|

| What % of your expenses do you expect your LTC insurance to pay |

|---|

| 100% | 8 | 10 | 6 |

|---|

| 61%-99% | 65 | 66 | 70 |

|---|

| 40%-60% | 24 | 20 | 19 |

|---|

| 35%-39% | 3 | 3 | 4 |

|---|

| 25% | 0 | 1 | 1 |

|---|

| TABLE A-11: Opinions about Long-Term Care Insurance Among Active Non-Buyers by Geographic Location (D.C. vs. East vs. West) |

|---|

| Opinions about LTC Insurance | Active Non-Buyers DC | Active Non-Buyers East | Active Non-Buyers West |

|---|

| Do you currently have LTC insurance |

|---|

| Yes | 19* | 8* | 10 |

|---|

| No | 81 | 92 | 90 |

|---|

| Did you buy your LTC insurance after you heard about the FLTCIP1 |

|---|

| Yes2 | 72* | 46 | 31* |

|---|

| No | 28 | 37 | 44 |

|---|

| I did not know about the FLTCIP | 0 | 17 | 25 |

|---|

- This question was only asked of those people who stated that they currently had LTC insurance; therefore the percentage of people who said they did not know about the FLTCIP are only of those non-buyers and non-responders who have LTC insurance.

- The distribution for this question is based on the answers of 18 Active Non-Buyers in the D.C. area, 30 Active Non-Buyers in the East and 32 Active Non-Buyers in the West.

|

| TABLE A-12: Opinions about Long-Term Care Insurance Among Retired Non-Buyers by Geographic Location (D.C. vs. East vs. West) |

|---|

| Opinions about LTC Insurance | Retired Non-Buyers DC | Retired Non-Buyers East | Retired Non-Buyers West |

|---|

| Do you currently have LTC insurance |

|---|

| Yes | 30 | 18 | 19 |

|---|

| No | 70 | 82 | 81 |

|---|

| Did you buy your LTC insurance after you heard about the FLTCIP1 |

|---|

| Yes2 | 7 | 15 | 14 |

|---|

| No | 79 | 58 | 55 |

|---|

| I did not know about the FLTCIP | 14 | 27 | 31 |

|---|

- This question was only asked of those people who stated that they currently had LTC insurance; therefore the percentage of people who said they did not know about the FLTCIP are only of those non-buyers and non-responders who have LTC insurance.

- The distribution for this question is based on the answers of 29 Retired Non-Buyers in the D.C. area, 90 Retired Non-Buyers in the East and 100 Retired Non-Buyers in the West.

|

| TABLE A-13: Decision Making Process of Active Buyers by Geographic Location (D.C. vs. East vs. West) |

|---|

| Decision Making Process | Active Buyers DC | Active Buyers East | Active Buyers West |

|---|

| I considered buynig LTC insurance prior to the federal offering |

|---|

| Yes | 57 | 56 | 61 |

|---|

| No | 43 | 44 | 39 |

|---|

| I would have bought LTC insurance if the Federal Government had not offered it |

|---|

| Yes | 34 | 32 | 33 |

|---|

| No | 15 | 17 | 17 |

|---|

| Not sure | 51 | 51 | 50 |

|---|

| TABLE A-14: Decision Making Process of Retired Buyers by Geographic Location (D.C. vs. East vs. West) |

|---|

| Decision Making Process | Active Buyers DC | Active Buyers East | Active Buyers West |

|---|

| I considered buynig LTC insurance prior to the federal offering |

|---|

| Yes | 67 | 75 | 72 |

|---|

| No | 33 | 25 | 28 |

|---|

| I would have bought LTC insurance if the Federal Government had not offered it |

|---|

| Yes | 40 | 44 | 40 |

|---|

| No | 12 | 13 | 14 |

|---|

| Not sure | 48 | 43 | 46 |

|---|

| TABLE A-15: Decision Making Process of Active Non-Buyers by Geographic Location (D.C. vs. East vs. West) |

|---|

| Decision Making Process | Active Non-Buyers DC | Active Non-Buyers East | Active Non-Buyers West |

|---|

| How seriously was buying the FLTCIP considered |

|---|

| Very seriously | 39 | 33 | 33 |

|---|

| Somewhat seriously | 41 | 42 | 40 |

|---|

| Not very seriously | 13 | 16 | 16 |

|---|

| Not seriously at all | 7 | 5 | 6 |

|---|

| Did not consider | 0 | 4 | 5 |

|---|

| How likely did you think it was that you would buy the FLTCIP when you requested the application |

|---|

| Very likely | 18 | 18 | 17 |

|---|

| Likely | 57 | 52 | 50 |

|---|

| Not very likely | 25 | 28 | 30 |

|---|

| Not at all likely | 0 | 2 | 3 |

|---|

| TABLE A-16: Decision Making Process of Retired Non-Buyers by Geographic Location (D.C. vs. East vs. West) |

|---|

| Decision Making Process | Retired Non-Buyers DC | Retired Non-Buyers East | Retired Non-Buyers West |

|---|

| How seriously was buying the FLTCIP considered |

|---|

| Very seriously | 32 | 25 | 24 |

|---|

| Somewhat seriously | 38 | 39 | 36 |

|---|

| Not very seriously | 15 | 20 | 22 |

|---|

| Not seriously at all | 7 | 5 | 7 |

|---|

| Did not consider | 8 | 11 | 11 |

|---|

| How likely did you think it was that you would buy the FLTCIP when you requested the application |

|---|

| Very likely | 13 | 13 | 8 |

|---|

| Likely | 41 | 44 | 43 |

|---|

| Not very likely | 42 | 36 | 44 |

|---|

| Not at all likely | 4 | 7 | 5 |

|---|

| TABLE A-17: Experience with the Application Process Among Active Buyers and Non-Buyers by Geographic Location (D.C. vs. East vs. West) |

|---|

| Experience with the Application Process | Active Buyers DC | Active Buyers East | Active Buyers West | Active Non-Buyers DC | Active Non-Buyers East | Active Non-Buyers West |

|---|

| Was the following easy/difficult for you: |

|---|

| a) getting an application1 |

|---|

| Did not get an application | 0 | 0 | 0 | 14 | 21 | 25 |

|---|

| Did get an application | 100 | 100 | 100 | 86 | 79 | 75 |

|---|

| Easy to get an application | 98 | 99 | 97 | 99 | 94 | 97 |

|---|

| Difficult to get an application | 2 | 1 | 3 | 1 | 6 | 3 |

|---|

| b) understanding the application1 |

|---|

| Did not attempt to understand the application | 0 | 0 | 0 | 27 | 32 | 35 |

|---|

| Did attempt to understand the application | 100 | 100 | 100 | 73 | 68 | 65 |

|---|

| Easy to understand the application | 97* | 91* | 94 | 80 | 70 | 76 |

|---|

| Difficult to understand the application | 3 | 9 | 6 | 20 | 30 | 24 |

|---|

| c) answering health questions1 |

|---|

| Did not answer health questions | 0 | 0 | 0 | 42 | 38 | 44 |

|---|

| Did answer health questions | 100 | 100 | 100 | 58 | 62 | 56 |

|---|

| Easy to answer health questions | 99 | 97 | 98 | 83 | 76 | 81 |

|---|

| Difficult to answer health questions | 1 | 3 | 2 | 17 | 24 | 19 |

|---|

| d) reading the application materials1 |

|---|

| Did not read the application materials | 0 | 0 | 0 | 30 | 31 | 31 |

|---|

| Did read the application materials | 100 | 100 | 100 | 70 | 69 | 69 |

|---|

| Easy to read the application materials | 88 | 84 | 82 | 74 | 67 | 70 |

|---|

| Difficult to read the application materials | 12 | 16 | 18 | 26 | 33 | 30 |

|---|

| Easy/difficult to obtain answers to questions about the federal program |

|---|

| Very easy | 40* | 29 | 28* | 23 | 17 | 22 |

|---|

| Easy | 56 | 65 | 63 | 56 | 52 | 48 |

|---|

| Difficult | 3 | 4 | 8 | 15 | 28 | 24 |

|---|

| Very difficult | 1 | 2 | 1 | 6 | 3 | 6 |

|---|

- The responses for "easy" and "difficult" are calculated on the basis of only those respondents who did the specific activity.

|

| TABLE A-18: Experience with the Application Process Among Retired Buyers and Non-Buyers by Geographic Location (D.C. vs. East vs. West) |

|---|

| Experience with the Application Process | Retired Buyers DC | Retired Buyers East | Retired Buyers West | Retired Non-Buyers DC | Retired Non-Buyers East | Retired Non-Buyers West |

|---|

| Was the following easy/difficult for you: |

|---|

| a) getting an application1 |

|---|

| Did not get an application | 0 | 0 | 0 | 23 | 25 | 34 |

|---|

| Did get an application | 100 | 100 | 100 | 77 | 75 | 66 |

|---|

| Easy to get an application | 100 | 98 | 98 | 96 | 96 | 96 |

|---|

| Difficult to get an application | 0 | 2 | 2 | 4 | 4 | 4 |

|---|

| b) understanding the application1 |

|---|

| Did not attempt to understand the application | 0 | 0 | 0 | 31 | 30 | 39 |

|---|

| Did attempt to understand the application | 100 | 100 | 100 | 69 | 70 | 61 |

|---|

| Easy to understand the application | 93 | 95 | 93 | 80 | 75 | 78 |

|---|

| Difficult to understand the application | 7 | 5 | 7 | 20 | 25 | 22 |

|---|

| c) answering health questions1 |

|---|

| Did not answer health questions | 0 | 0 | 0 | 38 | 39 | 48 |

|---|

| Did answer health questions | 100 | 100 | 100 | 62 | 61 | 52 |

|---|

| Easy to answer health questions | 93 | 92 | 90 | 80 | 76 | 75 |

|---|

| Difficult to answer health questions | 7 | 8 | 10 | 20 | 24 | 25 |

|---|

| d) reading the application materials1 |

|---|

| Did not read the application materials | 0 | 0 | 0 | 31 | 34 | 44 |

|---|

| Did read the application materials | 100 | 100 | 100 | 69 | 66 | 56 |

|---|

| Easy to read the application materials | 84 | 86 | 82 | 73 | 74 | 66 |

|---|

| Difficult to read the application materials | 16 | 14 | 18 | 27 | 26 | 34 |

|---|

| Easy/difficult to obtain answers to questions about the federal program |

|---|

| Very easy | 30 | 40* | 31* | 22 | 15 | 15 |

|---|

| Easy | 65 | 57 | 65 | 56 | 58 | 63 |

|---|

| Difficult | 4 | 3 | 3 | 16 | 24 | 18 |

|---|

| Very difficult | 1 | 0 | 1 | 6 | 3 | 4 |

|---|

- The responses for "easy" and "difficult" are calculated on the basis of only those respondents who did the specific activity.

|

| TABLE A-19: Awareness about the Federal Program Among Retired Non-Responders by Geographic Location (D.C. vs. East vs. West) |

|---|

| Awareness about the Federal Program | Retired Non-Responders DC | Retired Non-Responders East | Retired Non-Responders West |

|---|

| Are you aware that the Federal Government is sponsoring a LTC insurance program |

|---|

| Yes | 46 | 29 | 32 |

|---|

| No | 54 | 71 | 68 |

|---|

| TABLE A-20: Exposure to Promotional Activities Among Active Buyers and Non-Buyers by Geographic Location (DC vs. East vs. West) |

|---|

| Promotional Activities | Active Buyers DC | Active Buyers East | Active Buyers West | Active Non-Buyers DC | Active Non-Buyers East | Active Non-Buyers West |

|---|

| Did you do any of the following: |

|---|

| a) talk to colleagues about the federal program1 |

|---|

| Did not talk to colleagues | 24* | 36* | 33 | 40 | 52 | 48 |

|---|

| Did talk to colleagues | 76 | 64 | 67 | 60 | 48 | 52 |

|---|

| Found it to be helpful | 78* | 73 | 65* | 50 | 59 | 57 |

|---|

| Did not find it to be helpful | 22 | 27 | 35 | 50 | 59 | 57 |

|---|

| b) talk to human resource representative1 |

|---|

| Did not talk to human resource representative | 80 | 87 | 82 | 73 | 83 | 81 |

|---|

| Did talk to human resource representative | 20 | 13 | 18 | 27 | 17 | 19 |

|---|

| Found it to be helpful2 | 84 | 80 | 85 | 64 | 81 | 62 |

|---|

| Did not find it to be helpful | 16 | 20 | 15 | 36 | 19 | 38 |

|---|

| c) attend educational meetings1 |

|---|

| Did not attend educational meetings | 56 | 65 | 58 | 52 | 68 | 69 |

|---|

| Did not know about the educational meetings | 2 | 7 | 6 | 7 | 10 | 15 |

|---|

| Did attend educational meetings | 42 | 28 | 36 | 41 | 22 | 16 |

|---|

| Found them to be helpful | 95 | 91 | 95 | 84* | 80 | 76 |

|---|

| Did not find them to be helpful | 5 | 9 | 5 | 16 | 20 | 24 |

|---|

| d) view satellite broadcasts1 |

|---|

| Did not view satellite broadcasts | 70 | 71 | 72 | 79 | 78 | 73 |

|---|

| Did not know about the satellite broadcasts | 9 | 11 | 10 | 11 | 16 | 17 |

|---|

| Did view satellite broadcasts | 21 | 18 | 18 | 10 | 6 | 10 |

|---|

| Found them to be helpful3 | 93 | 83 | 95 | 56 | 67 | 62 |

|---|

| Did not find them to be helpful | 7 | 17 | 5 | 44 | 33 | 38 |

|---|

| e) read "Get Smart About Your Future"1 |

|---|

| Did not read "Get Smart About Your Future" | 27 | 23 | 32 | 27 | 35 | 35 |

|---|

| Did not know about "Get Smart About Your Future" | 4 | 9 | 8 | 11 | 9 | 12 |

|---|

| Did read "Get Smart About Your Future" | 69 | 68 | 60 | 62 | 56 | 53 |

|---|

| Found it to be helpful | 95 | 94 | 96 | 81 | 86 | 90 |

|---|

| Did not find it to be helpful | 5 | 6 | 4 | 19 | 14 | 10 |

|---|

| f) read advertisements1 |

|---|

| Did not read advertisements | 46 | 40 | 42 | 31 | 41 | 37 |

|---|

| Did not know about the advertisements | 5 | 7 | 10 | 9 | 8 | 14 |

|---|

| Did read advertisements | 49 | 53 | 48 | 60 | 51 | 49 |

|---|

| Found them to be helpful | 86 | 89 | 93 | 66 | 80 | 75 |

|---|

| Did not find them to be helpful | 14 | 11 | 7 | 34 | 20 | 25 |

|---|

| g) visit websites describing the federal program1 |

|---|

| Did not visit websites describing the federal program | 20 | 26 | 29 | 34* | 58 | 51 |

|---|

| Did not know about the websites describing the federal program | 1 | 4 | 4 | 4 | 11 | 13 |

|---|

| Did visit websites describing the federal program | 79 | 70 | 67 | 62 | 31 | 36 |

|---|

| Found them to be helpful | 97 | 98 | 97 | 81 | 83 | 86 |

|---|

| Did not find them to be helpful | 3 | 2 | 3 | 19 | 17 | 14 |

|---|

| h) read banner ads1 |

|---|

| Did not read banner ads | 72 | 68 | 78 | 70 | 73 | 72 |

|---|

| Did not know about the banner ads | 10 | 16 | 11 | 9 | 16 | 17 |

|---|

| Did read banner ads | 18 | 16 | 11 | 21 | 11 | 11 |

|---|

| Found them to be helpful4 | 59 | 61 | 72 | 42 | 60 | 63 |

|---|

| Did not find them to be helpful | 41 | 39 | 28 | 58 | 40 | 37 |

|---|

| i) read newspaper articles1 |

|---|

| Did not read newspaper articles | 48* | 62 | 63 | 38* | 55 | 56 |

|---|

| Did not know about the newspaper articles | 4 | 10 | 9 | 5 | 15 | 16 |

|---|

| Did read newspaper articles | 48 | 28 | 28 | 57 | 30 | 28 |

|---|

| Found them to be helpful | 92 | 86 | 86 | 71 | 68 | 68 |

|---|

| Did not find them to be helpful | 8 | 14 | 14 | 29 | 32 | 32 |

|---|

| j) read general brochures1 |

|---|

| Did not read general brochures | 12 | 13 | 17 | 14 | 20 | 19 |

|---|

| Did not know the general brochures | 1 | 2 | 1 | 1 | 5 | 7 |

|---|

| Did read general brochures | 87 | 85 | 82 | 85 | 75 | 74 |

|---|

| Found them to be helpful | 97 | 95 | 99 | 82 | 83 | 81 |

|---|

| Did not find them to be helpful | 3 | 5 | 1 | 18 | 17 | 19 |

|---|

| k) call toll-free number1 |

|---|

| Did not call a toll-free number | 59 | 59 | 62 | 72 | 76 | 76 |

|---|

| Did not know about the toll-free number | 5 | 5 | 3 | 6 | 10 | 12 |

|---|

| Did call a toll-free number | 36 | 36 | 35 | 22 | 14 | 12 |

|---|

| Found it to be helpful5 | 93 | 96 | 94 | 75 | 75 | 64 |

|---|

| Did not find it to be helpful | 7 | 4 | 6 | 25 | 25 | 36 |

|---|

- The responses for "helpful" and "not helpful" are calculated on the basis of only those respondents who did the specific activity.

- The distribution for this question is based on the answers of 37 Active Buyers in the DC area, 25 Active Buyers in the East and 39 Active Buyers in the West. The distribution for this question is based on the answers of 25 Active Non-Buyers in the DC area, 36 Active Non-Buyers in the East and 37 Active Non-Buyers in the West.

- The distribution for this question is based on the answers of nine Active Non-Buyers in the DC area, 15 Active Non-Buyers in the East and 21 Active Non-Buyers in the West.

- The distribution for this question is based on the answers of 32 Active Buyers in the DC area, 31 Active Buyers in the East and 25 Active Buyers in the West. The distribution for this question is based on the answers of 19 Active Non-Buyers in the DC area, 25 Active Non-Buyers in the East and 24 Active Non-Buyers in the West.

- The distribution for this question is based on the answers of 20 Active Non-Buyers in the DC area, 32 Active Non-Buyers in the East and 25 Active Non-Buyers in the West.

|

| TABLE A-21: Exposure to Promotional Activities Among Retired Buyers and Non-Buyers by Geographic Location (DC vs. East vs. West) |

|---|

| Promotional Activities | Retired Buyers DC | Retired Buyers East | Retired Buyers West | Retired Non-Buyers DC | Retired Non-Buyers East | Retired Non-Buyers West |

|---|

| Did you do any of the following: |

|---|

| a) talk to colleagues about the federal program1 |

|---|

| Did not talk to colleagues | 64* | 74 | 76 | 75 | 80 | 80 |

|---|

| Did talk to colleagues | 36 | 26 | 24 | 25 | 20 | 20 |

|---|

| Found it to be helpful2 | 85 | 79 | 75 | 67 | 69 | 64 |

|---|

| Did not find it to be helpful | 15 | 21 | 25 | 33 | 31 | 36 |

|---|

| b) talk to human resource representative1 |

|---|

| Did not talk to human resource representative | 97 | 97 | 97 | 94 | 97 | 96 |

|---|

| Did talk to human resource representative | 3 | 3 | 3 | 6 | 3 | 4 |

|---|

| Found it to be helpful3 | 83 | 100 | 82 | 50 | 57 | 50 |

|---|

| Did not find it to be helpful | 17 | 0 | 18 | 50 | 43 | 50 |

|---|

| c) read "Get Smart About Your Future"1 |

|---|

| Did not read "Get Smart About Your Future" | 26 | 26 | 30 | 37 | 42 | 39 |

|---|

| Did not know about "Get Smart About Your Future" | 8 | 6 | 6 | 13 | 12 | 12 |

|---|

| Did read "Get Smart About Your Future" | 66 | 68 | 64 | 50 | 46 | 49 |

|---|

| Found it to be helpful | 97 | 96 | 98 | 86 | 84 | 89 |

|---|

| Did not find it to be helpful | 3 | 4 | 2 | 14 | 16 | 11 |

|---|

| d) read advertisements1 |

|---|

| Did not read advertisements | 37 | 36 | 37 | 39 | 44 | 47 |

|---|

| Did not know about the advertisements | 5 | 3 | 5 | 10 | 12 | 10 |

|---|

| Did read advertisements | 58 | 61 | 58 | 51 | 44 | 43 |

|---|

| Found them to be helpful | 92 | 95 | 95 | 75 | 77 | 82 |

|---|

| Did not find them to be helpful | 8 | 5 | 5 | 25 | 23 | 18 |

|---|

| e) visit websites describing the federal program1 |

|---|

| Did not visit websites describing the federal program | 54 | 57 | 51 | 80 | 76 | 76 |

|---|

| Did not know about the websites describing the federal program | 3 | 4 | 4 | 7 | 12 | 11 |

|---|

| Did visit websites describing the federal program | 43 | 39 | 45 | 13 | 12 | 13 |

|---|

| Found them to be helpful4 | 97 | 97 | 96 | 100 | 90 | 86 |

|---|

| Did not find them to be helpful | 3 | 3 | 4 | 0 | 10 | 14 |

|---|

| f) read banner ads1 |

|---|

| Did not read banner ads | 86 | 86 | 84 | 87 | 82 | 81 |

|---|

| Did not know about the banner ads | 7 | 8 | 8 | 10 | 13 | 16 |

|---|

| Did read banner ads | 7 | 6 | 8 | 3 | 5 | 3 |

|---|

| Found them to be helpful5 | 53 | 68 | 82 | 50 | 64 | 57 |

|---|

| Did not find them to be helpful | 47 | 32 | 18 | 50 | 36 | 43 |

|---|

| g) read newspaper articles1 |

|---|

| Did not read newspaper articles | 39* | 64 | 64 | 42* | 52 | 61* |

|---|

| Did not know about the newspaper articles | 5 | 6 | 5 | 1 | 10 | 9 |

|---|

| Did read newspaper articles | 56 | 30 | 31 | 57 | 38 | 30 |

|---|

| Found them to be helpful | 94 | 93 | 90 | 83 | 65 | 76 |

|---|

| Did not find them to be helpful | 6 | 7 | 10 | 17 | 35 | 24 |

|---|

| h) read general brochures1 |

|---|

| Did not read general brochures | 10 | 13 | 13 | 27 | 26 | 25 |

|---|

| Did not know the general brochures | 1 | 1 | 2 | 0 | 7 | 6 |

|---|

| Did read general brochures | 89 | 86 | 85 | 73 | 67 | 69 |

|---|

| Found them to be helpful | 100 | 98 | 98 | 81 | 84 | 87 |

|---|

| Did not find them to be helpful | 0 | 2 | 2 | 19 | 16 | 13 |

|---|

| i) call toll-free number1 |

|---|

| Did not call a toll-free number | 61 | 56 | 53 | 84 | 77 | 80 |

|---|

| Did not know about the toll-free number | 2 | 1 | 3 | 3 | 9 | 7 |

|---|

| Did call a toll-free number | 37 | 43 | 44 | 13 | 14 | 13 |

|---|

| Found it to be helpful6 | 97 | 100* | 96* | 78 | 76 | 76 |

|---|

| Did not find it to be helpful | 3 | 0 | 4 | 22 | 24 | 24 |

|---|

- The responses for "helpful" and "not helpful" are calculated on the basis of only those respondents who did the specific activity.

- The distribution for this question is based on the answers of 18 Retired Non-Buyers in the DC area, 45 Retired Non-Buyers in the East and 44 Retired Non-Buyers in the West.

- The distribution for this question is based on the answers of six Retired Buyers in the DC area, 12 Retired Buyers in the East and 11 Retired Buyers in the West. The distribution for this question is based on the answers of four Retired Non-Buyers in the DC area, seven Retired Non-Buyers in the East and eight Retired Non-Buyers in the West.

- The distribution for this question is based on the answers of nine Retired Non-Buyers in the DC area, 29 Retired Non-Buyers in the East and 29 Retired Non-Buyers in the West.

- The distribution for this question is based on the answers of 17 Retired Buyers in the DC area, 25 Retired Buyers in the East and 34 Retired Buyers in the West. The distribution for this question is based on the answers of two Retired Non-Buyers in the DC area, 11 Retired Non-Buyers in the East and seven Retired Non-Buyers in the West.

- The distribution for this question is based on the answers of nine Retired Non-Buyers in the DC area, 34 Retired Non-Buyers in the East and 29 Retired Non-Buyers in the West.

|

| TABLE A-22: Comparison of FLTCIP to Other Programs Among Active Buyers by Geographic Location (D.C. vs. East vs. West) |

|---|

| Reasons for Buying | Active Buyers DC | Active Buyers East | Active Buyers West |

|---|

| Was the FLTCIP compared to other programs |

|---|

| Yes | 49 | 45 | 46 |

|---|

| No | 51 | 55 | 54 |

|---|

| Why was the FLTCIP purchased instead of a different program |

|---|

| a) lower rates |

|---|

| Yes | 25 | 33 | 35 |

|---|

| No | 75 | 67 | 65 |

|---|

| b) better benefits |

|---|

| Yes | 23 | 26 | 25 |

|---|

| No | 77 | 74 | 75 |

|---|

| c) recommended by others |

|---|

| Yes | 12 | 6 | 8 |

|---|

| No | 88 | 94 | 92 |

|---|

| d) easier to qualify |

|---|

| Yes | 45 | 38 | 39 |

|---|

| No | 55 | 62 | 61 |

|---|

| e) easier to get benefits |

|---|

| Yes | 11 | 17 | 17 |

|---|

| No | 89 | 83 | 83 |

|---|

| f) easier to understand coverage |

|---|

| Yes | 18 | 21 | 25 |

|---|

| No | 82 | 79 | 75 |

|---|

| g) Federal Government sponsorship |

|---|

| Yes | 73 | 69 | 78 |

|---|

| No | 27 | 31 | 22 |

|---|

| h) underwritten by Long Term Care Partners |

|---|

| Yes | 29 | 28 | 27 |

|---|

| No | 71 | 72 | 73 |

|---|

| TABLE A-23: Comparison of FLTCIP to Other Programs Among Retired Buyers by Geographic Location (D.C. vs. East vs. West) |

|---|

| Reasons for Buying | Retired Buyers DC | Retired Buyers East | Retired Buyers West |

|---|

| Was the FLTCIP compared to other programs |

|---|

| Yes | 39* | 29* | 33 |

|---|

| No | 61 | 71 | 67 |

|---|

| Why was the FLTCIP purchased instead of a different program |

|---|

| a) lower rates |

|---|

| Yes | 31* | 48 | 47 |

|---|

| No | 69 | 52 | 53 |

|---|

| b) better benefits |

|---|

| Yes | 26* | 36* | 33 |

|---|

| No | 74 | 64 | 67 |

|---|

| c) recommended by others |

|---|

| Yes | 11* | 6 | 6 |

|---|

| No | 89 | 94 | 94 |

|---|

| d) easier to qualify |

|---|

| Yes | 19 | 22* | 13* |

|---|

| No | 81 | 78 | 87 |

|---|

| e) easier to get benefits |

|---|

| Yes | 7 | 9 | 6 |

|---|

| No | 93 | 91 | 94 |

|---|

| f) easier to understand coverage |

|---|

| Yes | 23 | 24* | 16* |

|---|

| No | 77 | 76 | 84 |

|---|

| g) Federal Government sponsorship |

|---|

| Yes | 87 | 86 | 81 |

|---|

| No | 13 | 14 | 19 |

|---|

| h) underwritten by Long Term Care Partners |

|---|

| Yes | 29* | 39* | 33 |

|---|

| No | 71 | 61 | 67 |

|---|

| TABLE A-24: Reasons for Not Buying the Federal Program: ActiveNon-Buyers by Geographic Location (D.C. vs. East vs. West) |

|---|

| Reasons for Not Buying | Active Non-Buyers DC | Active Non-Buyers East | Active Non-Buyers West |

|---|

| Were the following reasons not to buy the FLTCIP: |

|---|

| a) have other insurance like FEHB |

|---|

| Yes, a reason | 11 | 11 | 17 |

|---|

| No, not a reason | 89 | 89 | 83 |

|---|

| b) will buy the FLTCIP later |

|---|

| Yes, a reason | 47 | 51 | 53 |

|---|

| No, not a reason | 53 | 49 | 47 |

|---|

| c) information about the FLTCIP too confusing |

|---|

| Yes, a reason | 17 | 23 | 23 |

|---|

| No, not a reason | 83 | 77 | 77 |

|---|

| d) not happy with the features of the FLTCIP |

|---|

| Yes | 22 | 18 | 15 |

|---|

| No | 78 | 82 | 85 |

|---|

| TABLE A-25: Reasons for Not Buying the Federal Program: Retired Non-Buyers by Geographic Location (D.C. vs. East vs. West) |

|---|

| Reasons for Not Buying | Retired Non-Buyers DC | Retired Non-Buyers East | Retired Non-Buyers West |

|---|

| Were the following reasons not to buy the FLTCIP: |

|---|

| a) have other insurance like FEHB |

|---|

| Yes, a reason | 24 | 18 | 18 |

|---|

| No, not a reason | 76 | 82 | 82 |

|---|

| b) will buy the FLTCIP later |

|---|

| Yes, a reason | 13 | 24 | 23 |

|---|

| No, not a reason | 87 | 76 | 77 |

|---|

| c) information about the FLTCIP too confusing |

|---|

| Yes, a reason | 13 | 22 | 19 |

|---|

| No, not a reason | 87 | 78 | 81 |

|---|

| d) not happy with the features of the FLTCIP |

|---|

| Yes | 16 | 17 | 15 |

|---|

| No | 84 | 83 | 85 |

|---|

| TABLE A-26: Factors that Would Make Active Non-Buyers More Interested in Buying the Federal Program by Geographic Location (D.C. vs. East vs. West) |

|---|

| Factors | Active Non-Buyers DC | Active Non-Buyers East | Active Non-Buyers West |

|---|

| More interested in buying the FLTCIP if: |

|---|

| a) there were more choices regarding the amount of home care coverage |

|---|

| Agree | 50 | 60 | 59 |

|---|

| Disagree | 50 | 40 | 41 |

|---|

| b) there was a guarantee that premiums will not increase in the future |

|---|

| Agree | 76 | 85 | 84 |

|---|

| Disagree | 24 | 15 | 16 |

|---|

| c) there was a premium discount for couples who purchase the program |

|---|

| Agree | 64 | 67 | 66 |

|---|

| Disagree | 36 | 33 | 34 |

|---|

| d) premiums were tax deductible |

|---|

| Agree | 89 | 87 | 86 |

|---|

| Disagree | 11 | 13 | 14 |

|---|

| Three most important factors that would make a non-buyer more interested in buying |

|---|

| Tax deductible premiums | 32 | 37 | 33 |

|---|

| A guarantee that premiums will not increase in the future | 13 | 21 | 23 |

|---|

| A premium discount for couples who purchase the program | 20 | 19 | 17 |

|---|

| TABLE A-27: Factors that Would Make Retired Non-Buyers More Interested in Buying the Federal Program by Geographic Location (D.C. vs. East vs. West) |

|---|

| Factors | Retired Non-Buyers DC | Retired Non-Buyers East | Retired Non-Buyers West |

|---|

| More interested in buying the FLTCIP if: |

|---|

| a) there were more choices regarding the amount of home care coverage |

|---|

| Agree | 55 | 59 | 60 |

|---|

| Disagree | 45 | 41 | 40 |

|---|

| b) there was a guarantee that premiums will not increase in the future |

|---|

| Agree | 69 | 77 | 78 |

|---|

| Disagree | 31 | 23 | 22 |

|---|

| c) there was a premium discount for couples who purchase the program |

|---|

| Agree | 65 | 61 | 63 |

|---|

| Disagree | 35 | 39 | 37 |

|---|

| d) premiums were tax deductible |

|---|

| Agree | 77 | 77 | 75 |

|---|

| Disagree | 23 | 23 | 25 |

|---|

| Three most important factors that would make a non-buyer more interested in buying |

|---|

| Tax deductible premiums | 25 | 25 | 22 |

|---|

| A guarantee that premiums will not increase in the future | 9 | 19 | 20 |

|---|

| A premium discount for couples who purchase the program | 25 | 16 | 18 |

|---|

This policy brief was prepared under contract between the U.S. Department of Health and Human Services, Office of the Assistant Secretary for Planning and Evaluation, Office of Disability, Aging and Long-Term Care Policy (DALTCP) and Abt Associates. The brief was written by LifePlans, Inc. For additional information on this subject, or to view the other briefs in this series, you can visit the ASPE home page at http://aspe.hhs.gov, the DALTCP home page at http://aspe.hhs.gov/_/office_specific/daltcp.cfm or contact the ASPE Project Officer, Hunter McKay, at HHS/ASPE/DALTCP, Room 424E, H.H. Humphrey Building, 200 Independence Avenue, S.W., Washington, D.C. 20201, Hunter.McKay@hhs.gov. Data Briefs on Federal Long-Term Care Insurance Buyers/Non-Buyers

A total of nine Data Briefs are available from the Office of Disability, Aging and Long-Term Care on this subject: