January 2017

Printer Friendly Version in PDF Format (90 PDF pages)

ABSTRACT

Until relatively recently, insurance coverage for behavioral health has had more restrictions and limitations than coverage for medical/surgical care. Moreover, behavioral health coverage has often been more restricted in individual and small group private plans than in large group employer-sponsored insurance plans. Recently, parity protections were extended to individual and small group plans that offer coverage for behavioral health treatment to have terms of coverage that are no more restrictive than for medical/surgical treatment. For this report, we assessed the degree to which behavioral health coverage and medical/surgical coverage in individual and small group plans changed after federal parity requirements in coverage took effect in 2014. The results focus on changes in scope of coverage (what conditions and services are covered) and level of coverage (quantitative restrictions, such as the co-payment and limits on visits). The findings suggest that parity legislation may have had the intended effect.

DISCLAIMER: The opinions and views expressed in this report are those of the authors. They do not necessarily reflect the views of the Department of Health and Human Services, the contractor or any other funding organization.

TABLE OF CONTENTS

1. INTRODUCTION

2. BACKGROUND

2.1. Overview

2.2. Legislation Affecting Behavioral Health Coverage

2.3. Literature on Behavioral Health Coverage, Network Adequacy, and Workforce Shortage

2.4. Literature on the Impact of Parity

3. METHODS

3.1. Overview

3.2. Identify States, Issuers, and Plans

3.3. Abstract Plan Benefit Data

3.4. Perform Analysis

3.5. Key Informant Discussion: Data and Analysis

4. RESULTS

4.1. Scope of Coverage

4.2. Level of Coverage

4.3. Formulary Coverage and Non-Quantitative Treatment Limitation for Prescription Medication

4.4. Sub-Analyses

4.5. Results from Stakeholder Discussions on Network Adequacy

5. DISCUSSION

APPENDICES

- APPENDIX A: Candidate Measures for Selecting States

- APPENDIX B: Top Four Issuers per State by Market Share

- APPENDIX C: Working Definitions of Behavioral Health Services and Types of Care Used to Abstract Plan Data

- APPENDIX D: Guidance Used to Identify Non-Quantitative Treatment Limitations

- APPENDIX E: T-Tests

LIST OF FIGURES

- FIGURE 3-1: Methods Flow

- FIGURE 3-2: Process of Identifying States and Data Sources

- FIGURE 3-3: Health Insurance Rating Area Selection Process

- FIGURE 3-4: Health Insurance Plan Selection Process

- FIGURE 4-1: Percentage of Plans with Any Explicitly Stated Exclusion for Behavioral Health and for Medical/Surgical Conditions, 2013 and 2014

- FIGURE 4-2: Percentage of Plans in 2013 Explicitly Stating In-Network Coverage for Behavioral Health, by Setting, Behavioral Health Condition, and Type of Marketplace

- FIGURE 4-3: Percentage of Plans in 2014 Explicitly Stating In-Network Coverage for Behavioral Health, by Setting/Network Status, Behavioral Health Condition, and Type of Marketplace

- FIGURE 4-4: Percentage of Plans Explicitly Stating Exclusions for Health Conditions, by Year, Health Condition, and Type of Exchange

- FIGURE 4-5: Percentage of Plans Explicitly Stating Exclusions for Health Conditions, by Year, Health Condition, and Insurance Market

LIST OF TABLES

- TABLE 3-1: Sample States and Selection Criteria Information

- TABLE 3-2: Source of Health Insurance Rate Filings, by State

- TABLE 3-3: Plan Selection Data Sources by Issuer and Year/Exchange

- TABLE 3-4: Source of Health Insurance Benefit Information Policy Documents, by State

- TABLE 4-1: Percentage of Plans with Explicitly Stated Coverage and Exclusions for Select Health Conditions, 2013 and 2014

- TABLE 4-2: Percentage of Plans with Explicitly Stated Coverage and Exclusions, for Setting and Health Condition Category, 2013 and 2014

- TABLE 4-3: Percentage of Plans with Explicitly Stated Coverage and Exclusions for Select Services, by Health Condition Category, 2013 and 2014

- TABLE 4-4: Percentage of Plans with Select NQTLs for Behavioral Health Care, 2013 and 2014

- TABLE 4-5: Percentage of Plans with Co-Payments for the Initial Visit, by Setting and Health Condition Category, 2013 and 2014

- TABLE 4-6: Average Co-Payment Amounts for the Initial Visit, Among Plans with Co-Payments, by Setting and Health Condition Category, 2013 and 2014

- TABLE 4-7: Percentage of Plans with Co-Insurance for the Initial Visit, by Setting and Health Condition Category, 2013 and 2014

- TABLE 4-8: Consumer Co-Insurance Payment for Initial Visit, by Setting and Health Condition, 2013 and 2014

- TABLE 4-9: Average Percentage of Initial Visit Cost Paid for by Consumer, by Setting and Health Condition, 2013 and 2014

- TABLE 4-10: Distribution of Behavioral Health Medications across Formulary Tiers, 2013 and 2014

- TABLE 4-11: Distribution of Medical/Surgical Medications across Formulary Tiers, 2013 and 2014

- TABLE 4-12: Percentage of Behavioral Health Medications with Selected Types of Limitations, 2013 and 2014

- TABLE 4-13: Percentage of Medical/Surgical Medications with Selected Types of Limitations, 2013 and 2014

- TABLE 4-14: Percentage of Plans with Select NQTLs for Prescription Medication, by Health Condition, 2013 and 2014

- TABLE 4-15: Percentage of Plans with Explicitly Stated Coverage and Exclusions, by Setting/Network Status and Health Condition, 2013 and 2014

- TABLE 4-16: Percentage of Plans with Select NQTLs for Behavioral Health Care in the Inpatient Setting, by Network Status, 2013 and 2014

- TABLE 4-17: Percentage of Plans with Select NQTLs for Behavioral Health Care in Ambulatory Settings, by Network Status, 2013 and 2014

- TABLE 4-18: Percentage of Plans with Co-Insurance for the Initial Visit, by Setting/Network Status, Health Condition, 2013 and 2014

- TABLE 4-19: Consumer Co-Insurance Payment for Initial Visit, by Setting/Network Status and Health Condition, 2013 and 2014

- TABLE 4-20: Percentage of Plans with Select NQTLs for Prescription Medication for Behavioral Health Conditions, by Network Status, 2013 and 2014

- TABLE A-1: Candidate Measures by State and Region

- TABLE B-1: Top 4 Issuers per State by Market Share

- TABLE C-1: Data Abstraction Template Keywords for Select Services

- TABLE E-1: Percentage of Plans with any Explicitly Stated Exclusion for Behavioral Health and for Medical/Surgical Conditions: T-test across 2013 and 2014

- TABLE E-2: Percentage of Plans with any Explicitly Stated Exclusion for Behavioral Health and for Medical/Surgical Conditions: T-test across Health Conditions

- TABLE E-3: Percentage of Plans with Explicitly Stated Coverage and Exclusions for Select Health Conditions: T-test across 2013 and 2014

- TABLE E-4: Percentage of Plans with Explicitly Stated Coverage and Exclusions, by Setting and Health Condition: T-test across 2013 and 2014

- TABLE E-5: Percentage of Plans with Explicitly Stated Coverage and Exclusions, by Setting and Health Condition: T-test across Health Condition Categories

- TABLE E-6: Percentage of Plans with Explicitly Stated Coverage and Exclusions for Selected Services, by Health Condition: T-test across 2013 and 2014

- TABLE E-7: Percentage of Plans with Explicitly Stated Coverage and Exclusion for Selected Services, by 2013 and 2014: T-test across Health Conditions

- TABLE E-8: Percentage of Plans with Select NQTLs for Behavioral Health Care, 2013 and 2014: T-test across Year

- TABLE E-9: Percentage of Plans with Co-Payments for the Initial Visit, by Setting and Health Condition: T-test across 2013 and 2014

- TABLE E-10: Percentage of Plans with Co-Payments for the Initial Visit, by Setting, 2013 and 2014: T-test across Health Conditions

- TABLE E-11: Average Co-Payment Amounts for the Initial Visit, Among Plans with Co-Payments, by Setting and Health Condition: T-test across 2013 and 2014

- TABLE E-12: Average Co-Payment Amounts for the Initial Visit, Among Plans with Co-Payments, by Setting, 2013 and 2014: T-test across Health Conditions

- TABLE E-13: Percentage of Plans with Co-Insurance for the Initial Visit, by Setting and Health Condition: T-test across 2013 and 2014

- TABLE E-14: Percentage of Plans with Co-Insurance for the Initial Visit, by Setting, 2013 and 2014: T-test across Health Conditions

- TABLE E-15: Consumer Co-Insurance Payment for Initial Visit, by Setting and Health Condition: T-test across 2013 and 2014

- TABLE E-16: Consumer Co-Insurance Payment for Initial Visit, by Setting, 2013 and 2014: T-test across Health Conditions

- TABLE E-17: Average Percentage of Initial Visit Cost Paid for by Consumer, by Setting and Health Condition: T-test across 2013 and 2014

- TABLE E-18: Average Percentage of Initial Visit Cost Paid for by Consumer, by Setting, 2013 and 2014: T-test across Health Conditions

- TABLE E-19: Percentage of Plans with Select NQTLs for Prescription Medication, by Health Condition: T-test across 2013 and 2014

- TABLE E-20: Percentage of Plans with Explicitly Stated Coverage and Exclusions, by Setting/Network Status and Health Condition: T-test across 2013 and 2014

- TABLE E-21: Percentage of Plans with Explicitly Stated Coverage and Exclusions, by Setting/Network Status and Health Condition: T-test across Health Condition Categories

- TABLE E-22: Percentage of Plans with Explicitly Stated Coverage and Exclusions, by Setting/Network Status and Health Condition: T-test across Network

- TABLE E-23: Percentage of Plans with Select NQTLs for Behavioral Health Care in the Inpatient Setting, 2013 and 2014: T-test across Network

- TABLE E-24: Percentage of Plans with Select NQTLs for Behavioral Health Care in Ambulatory Settings, 2013 and 2014: T-test across Network

- TABLE E-25: Average Co-Insurance Rate for Initial Visit, by Setting/Network Status and Health Condition: T-test across 2013 and 2014

- TABLE E-26: Average Co-Insurance Rate for Initial Visit, by Setting/Network Status, 2013 and 2014: T-test across Health Conditions

- TABLE E-27: Average Co-Insurance Rate for Initial Visit, by Setting and Health Condition, 2013 and 2014: T-test across Network

- TABLE E-28: Percentage of Plans in 2013 Explicitly Stating In-Network Coverage for Behavioral Health, by Setting, Behavioral Health Condition, and Type of Exchange: T-test across Marketplace Facilitation

- TABLE E-29: Percentage of Plans in 2014 Explicitly In-Network Stating Coverage for Behavioral Health, by Setting/Network Status, Behavioral Health Condition, and Type of Exchange: T-test across Marketplace Facilitation

- TABLE E-30: Percentage of Plans Explicitly Stating Exclusions for Health Conditions, by Year, Health Condition, and Type of Exchange: T-test across Marketplace Facilitation

- TABLE E-31: Percentage of Plans Explicitly Stating Exclusions for Health Conditions, by Year, Health Condition, and Insurance Market: T-test across Insurance Market Types

ACKNOWLEDGMENTS

RTI International prepared this report under contract to the Office of the Assistant Secretary for Planning and Evaluation (ASPE), U.S. Department of Health and Human Services (HHS) (contract number HHSP23320095651WC, task order number HHSP23337044T). The authors appreciate the guidance of Emily Jones, Kirsten Beronio, and D.E.B. Potter (ASPE) and staff of the Center for Consumer Information and Insurance Oversight. The authors would also like to thank the individuals who participated in the key stakeholder discussions and the individuals from state departments of insurance who provided and helped interpret insurance plan documents.

The views and opinions expressed here are those of the authors and do not necessarily reflect the views, opinions, or policies of ASPE or HHS. The authors are solely responsible for any errors.

ABSTRACT

Summary: In 2014, parity protections were extended to individual and small group plans that offer coverage for behavioral health treatment to have terms of coverage that are no more restrictive than for medical/surgical treatment. For this report, we assessed the degree to which behavioral health coverage and medical/surgical coverage in individual and small group plans changed after federal parity requirements in coverage took effect in 2014. The results focus on changes in scope of coverage (what conditions and services are covered) and level of coverage (quantitative restrictions, such as the co-payment and limits on visits). The findings suggest that parity legislation may have had the intended effect.

Major Findings: The current study suggestions that, on the whole, there was little evidence of differential quantitative restrictions in the 2014 plans. The findings show that there were some differences in scope and level of coverage between behavioral health and medical/surgical coverage in 2013, but these were not apparent in 2014. For example, in 2013, 86 percent of plans covered office visits for behavioral health reasons, but 88 percent covered office visits for medical/surgical reasons. In 2014, the two proportions were equal: 86 percent of plans covered office visits for behavioral health, and the same proportion covered office visits for medical/surgical care. Our findings suggest at least two areas where further understanding is needed on parity in the individual and small group market. First, the results suggest focusing on aspects of coverage other than quantitative restrictions, such as non-quantitative treatment limitations (NQTLs). A second area requiring further scrutiny is whether plans' provider networks sufficiently ensure consumer access to services.

Purpose: The findings in the current study should contribute to the current policy discussions regarding parity in behavioral health care in practice, both in terms of quantitative restrictions and NQTLs.

Method: We created a purposive sample of states and then a sample of individual and small group plans within those states. We obtained documents for 166 plans and then used those documents to compare changes in coverage from 2013 (before the parity requirements took effect) to 2014 (after they took effect). We also convened discussions with key informants to provide context and insight into aspects of coverage -- such as network adequacy -- that were not captured by reviewing plan data.

ACRONYMS

The following acronyms are mentioned in this report and/or appendices.

| ADHD | Attention Deficit/Hyperactivity Disorder |

|---|---|

| AHRQ | HHS Agency for Healthcare Research and Quality |

| AIDS | Acquired Immune Deficiency Syndrome |

| ASPE | HHS Office of the Assistant Secretary for Planning and Evaluation |

| BCBS | Blue Cross Blue Shield |

| CCIIO | Center for Consumer Information and Insurance Oversight |

| CFR | Code of Federal Regulations |

| CMS | HHS Centers for Medicare & Medicaid Services |

| EHB | Essential Health Benefits |

| FFM | Federally Facilitated Marketplace |

| HCl | Hydrochloride |

| HIV | Human Immunodeficiency Virus |

| HHS | U.S. Department of Health and Human Services |

| HPSA | Health Professional Shortage Area |

| HRSA | HHS Health Resources and Services Administration |

| IOT | Intensive Outpatient Treatment |

| MAT | Medication Assisted Treatment |

| MHPAEA | Mental Health Parity and Addiction Equity Act |

| MLR | Medical Loss Ratio |

| NAIC | National Association of Insurance Commissioners |

| NAMHC | National Advisory Mental Health Council |

| NQTL | Non-Quantitative Treatment Limitation |

| PUF | Public Use File |

| QHP | Qualified Health Plan |

| RBIS | CCIIO Rate and Benefit Information System |

| RF | Rate Filings |

| RTI | Research Triangle Institute |

| SAMHSA | HHS Substance Abuse and Mental Health Services Administration |

| SERFF | System for Electronic Rate and Form Filing |

| SHOP | Small Business Health Options Program |

EXECUTIVE SUMMARY

Historically, behavioral health coverage has often been more restricted in individual and small group private plans than in large employer plans. In 2014, parity protections were extended to individual and small group plans, requiring plans that cover behavioral health treatments to have terms of coverage that are no more restrictive than coverage for medical/surgical services. These requirements represent an expansion of parity protections established in prior federal legislation in 2008 and 1996, as well as numerous state legislative actions over at least three decades.

For this report, we assessed the degree to which behavioral health coverage and medical/surgical coverage in individual and small group plans changed after federal parity requirements in coverage took effect. The results focus on changes in scope of coverage (what conditions and services are covered) and level of coverage (quantitative restrictions, such as the co-payment and limits on visits).

We created a purposive sample of states and then a sample of individual and small group plans within those states. We obtained documents for 166 of the 217 plans included in the sample and then used those documents to compare changes in coverage from 2013 (before the parity requirements took effect) to 2014 (after they took effect). We also convened discussions with key informants to provide context and insight into aspects of coverage -- such as network adequacy -- that were not captured by reviewing plan data.

The current study suggestions that, on the whole, there was little evidence of differential quantitative restrictions in the 2014 plans. However, findings suggest that parity legislation may have had some effect. The purpose of parity legislation was to remove differences between behavioral health and medical/surgical coverage in terms of quantitative restrictions. The findings show that there were some differences in scope and level of coverage between behavioral health and medical/surgical coverage in 2013, but these were not apparent in 2014. For example, in 2013, 86 percent of plans covered office visits for behavioral health reasons, but 88 percent covered office visits for medical/surgical reasons. In 2014, the two proportions were equal: 86 percent of plans covered office visits for behavioral health, and the same proportion covered office visits for medical/surgical care. The findings also indicated similar convergence in the level of coverage -- such as co-insurance -- from 2013 to 2014.

Our findings suggest at least two areas where further understanding is needed, and thus where further investigation on parity may be most productively focused. First, the results support the developing guidance for enforcing parity requirements in the individual and small group market toward aspects of coverage other than quantitative restrictions, such as non-quantitative treatment limitations (NQTLs). NQTLs are used by insurers to manage utilization, such as through prior authorization, which typically requires plan administrators or qualified providers to approve reimbursement for a service for a specific patient before it is provided. The data in the current study allowed only a limited assessment of parity in NQTLs between behavioral health and medical/surgical coverage. Thus, although the current study did not find differences in NQTLs with regard to behavioral health and medical/surgical coverage, further study is warranted.

A second area requiring further scrutiny is whether plans' provider networks sufficiently ensure consumer access to services. The data clearly show that, relative to 2013, plans in 2014 had increased incentives for consumers to use care from providers in the plan network. In 2014, for example, only half of the plans covered out-of-network outpatient care. For in-network coverage to help ensure access to services, the provider network must be adequate and the appropriate services must be available in a timely fashion. Even though the current study does not show coverage differences between behavioral health and medical/surgical services, research is needed on the adequacy of networks and the impact of ongoing shortages in specialty behavioral health care providers.

Until the current study, no study to our knowledge used a wide selection of plan data from the individual and small group markets to determine how behavioral health coverage may have improved over time. The findings in the current study should contribute to the current policy discussions regarding behavioral health coverage, both in terms of quantitative restrictions and NQTLs. The results presented here will inform future directions for improving parity in behavioral health coverage specifically and further research on policies to help people with behavioral health needs access treatment and services.

1. INTRODUCTION

In 2014, parity protections were extended to individual and small group plans, requiring plans that cover behavioral health treatments to have terms of coverage that are no more restrictive than coverage for medical/surgical services. These changes represented an expansion of parity protections established in prior federal legislation in 2008 and 1996, as well as numerous state legislative actions over at least three decades.

In 2014, the Office of the Assistant Secretary for Planning and Evaluation (ASPE), U.S. Department of Health and Human Services (HHS) awarded a Task Order contract to RTI International and its subcontractor, the National Academy for State Health Policy, to assess the degree to which the extension of parity requirements to the individual and small group markets were associated with changes in behavioral health coverage and medical/surgical coverage in small group and individual plans. Relevant coverage dimensions are scope (what conditions and services are covered), level (quantitative restrictions), and network adequacy (whether a sufficient number of care providers was available to patients under the plan).

This report documents findings under four research questions:

-

Research Question 1: What was the scope of coverage for mental health and substance use disorder benefits in individual and small group plans in 2013 and 2014, and how does this differ from the scope of coverage for medical/surgical benefits?

-

Research Question 2: What was the level of coverage for mental health and substance use disorder benefits in individual and small group plans in 2013 and 2014, and how does this differ from the level of coverage for medical/surgical benefits?

-

Research Question 3: To what degree are the findings from the research questions attributable to characteristics such as whether that state had a state or federally facilitated exchange?

-

Research Question 4: To what degree were there changes in network adequacy for mental health and substance use disorder treatment through individual and small group plans from 2013 to 2014, compared with medical/surgical treatment?

Under the guidance of ASPE, we created a purposive sample of states and individual and small group plans, obtained plan documents, used those documents to compare changes in coverage from 2013 (before implementing the parity requirements in these markets) to 2014 (after implementing the requirements), and then compared the change over time for behavioral health coverage with the change over time for medical/surgical coverage. We also convened discussions with key informants to provide context and insight into aspects of coverage that were not captured by reviewing plan data.

This report is structured as follows:

-

Section 2 (Background) provides some background to the current policy landscape. The background is important because over the past three decades, several legislative approaches at the federal and state levels have attempted to address the difference between behavioral health coverage and medical/surgical coverage in a piecemeal manner. Understanding the gaps that remain from those legislative actions is key to understanding the potential impact of the application of parity to the individual and small group markets. The summary of the literature to date motivates the research questions that are central to the current study, and these research questions focus on each of the relevant coverage dimensions.

-

Section 3 (Methods) describes the data sources used to create the samples of states and plans within states, and the plan data used for the main analyses; we also describe the key informant discussions in this section.

-

Section 4 (Results) presents quantitative findings from the plan data, and these are supplemented by the key informant discussion findings.

-

Section 5 (Discussion) focuses on implications for policy and recommendations for future work.

2. BACKGROUND

2.1. Overview

Prior to 2008, parity laws between behavioral health coverage and medical/surgical coverage consisted of a patchwork of policies at the state level overlaid with the federal Mental Health Parity Act of 1996. The Mental Health Parity and Addiction Equity Act (MHPAEA) of 2008 helped standardize what parity meant across states and addressed significant gaps in the Mental Health Parity Act. MHPAEA was also particularly significant for the current study, because MHPAEA parity requirements were extended to individual and small group plans, beginning in 2014.[1] Also in that year, health insurance marketplaces were created at the state level for individual and small group plans. Parity legislation affected plans offered both within and outside of those marketplaces.

There is a growing literature on the association between the recent federal health care reforms of 2010 through 2014 and behavioral health care access and use (Berry et al., 2015; Busch et al., 2014; Grazier et al., 2016; Horgan et al., 2016; McGinty et al., 2015). However, gaps and lags in data mean that there is relatively little evidence on the impact of key aspects of legislation, which include parity requirements on individual and small group plans (Barry et al., 2016; French et al., 2016). Moreover, to our knowledge, few studies have used plan coverage documents as data to assess changes in coverage over time and compare behavioral health coverage and medical/surgical coverage.

2.2. Legislation Affecting Behavioral Health Coverage

2.2.1. Legislation Before 2008

The discrepancy in coverage between behavioral and medical/surgical health insurance benefits has been a key health policy concern in the United States for at least the past two decades. In 1996, the Mental Health Parity Act was passed and signed into law (NAMHC, 2000). Before this legislation, insurance coverage for mental health care was notably different from all other medical care in terms of hospital stays, annual or lifetime dollar limits, and the extent of cost-sharing through co-payments and deductibles. The Mental Health Parity Act stated that if a health insurance plan included mental health benefits, the annual and lifetime limits of mental health care and medical care must be the same. However, the Mental Health Parity Act did not require health insurance plans to offer mental health services, require parity in cost-sharing provisions, or specify which, if any, behavioral health services were to be covered. Additionally, the law exempted small employers (defined as a firm having fewer than 50 employees) and employers that could prove that medical costs would increase by 1 percent or more as a result of complying with the Mental Health Parity Act.

Partly as a response to the gaps in this federal legislation, many states proposed more ambitious laws to address behavioral health coverage. In the 1990s and early 2000s, a number of states passed their own parity laws that varied greatly in strength and enforcement. By 2008, parity legislation had been enacted in 45 states (Lang, 2013).

2.2.2. The Mental Health Parity and Addiction Equity Act of 2008

In 2008, the nationwide variation in coverage for behavioral health benefits was addressed by the passage of the federal MHPAEA, which extended full parity in coverage and treatment limitations to large group plans (Beronio et al., 2014). MHPAEA specified six benefit classifications for care in which parity was required: inpatient in-network, inpatient out-of-network, outpatient in-network, outpatient out-of-network, emergency care, and prescription drugs. The law applies to employers and group health insurance plans with more than 50 employees that offer coverage for mental illness and substance use disorders and requires that coverage be no more restrictive than that for other medical and surgical procedures covered by the plan. MHPAEA does not require group health plans to cover behavioral health care, but when they do, that coverage must be comparable to coverage for medical/surgical care.

Parity under MHPAEA is operationalized as mental health and substance use -- or behavioral health -- disorder coverage being no more restrictive than medical/surgical coverage with regard to predominant financial requirements and treatment limits. Generally, behavioral health benefits may not be applied more stringently than the processes, strategies, evidentiary standards, or other factors used in applying limitations to medical/surgical benefits. The only exception to this was where there are differences in recognized clinically appropriate standards of care. Even though behavioral health benefits can be carved out for administration by a separate insurer, plan offerings must have parity in behavioral health benefits. The law also required that plans make available information on medical necessity criteria and reasons for any denials for services.

2.2.3. Expansion of Parity Requirements to the Individual and Small Group Markets

In 2010, the parity requirements in MHPAEA were applied to new individual and small group plans issued in each state to cover behavioral health services at parity (Sarata, 2011). An ASPE analysis projected that this extension of the MHPAEA would lead to an estimated 7.1 million Americans in the individual market and 23.3 million Americans in the small group market seeing their existing behavioral health benefits covered at parity with medical/surgical benefits (Beronio et al., 2013).

In addition to improving parity in coverage for behavioral health benefits whenever such benefits are offered, the 2010 legislation also helped ensure certain types of plans actually offered behavioral health benefits. In 2014 the legislation established private insurance exchanges in each state and these exchanges could be state-run or federally-run. All health plans sold on the exchange must offer coverage in ten "Essential Health Benefit (EHB)" categories, including behavioral health services. Each state selected a benchmark plan that complied with the MHPAEA parity requirement, and that plan was used to define the EHB package for all insurance plans offered through the exchanges (Sarata, 2011).

An ASPE study of EHB's offered by small group plans in 2011 found that 95 percent offered coverage for behavioral health inpatient and outpatient services (Skopec et al., 2011), but the scope and level of coverage for these services in individual plans was unclear. The EHB requirement in 2014 was expected to provide access to behavioral health benefits for almost 4 million people in the individual market and 1.2 million people in the small group market whose plans did not offer such benefits previously (Beronio et al., 2013).

The 2010 legislation also created the Small Business Health Options Program (SHOP) to help small employers provide access to affordable insurance for their employees (Healthcare.gov, 2016a). The program streamlined the payment process for offering a variety of plans to full-time employees through the state marketplaces. Evidence suggests that uptake of SHOP was slow at the outset, with less than 1 percent of people in the small group market using the program as of February 2015 (Curran et al., 2016). Nevertheless, employees whose employers use SHOP to provide insurance are also subject to the EHB requirements and thus will be ensured coverage for behavioral health benefits as well.

In addition to other requirements, exchange plans must meet network adequacy standards, which should have an impact on access to behavioral health services. This requirement is intended for people to receive care without unreasonable delay.[2] Issuers must also submit provider directories to the exchange for publication. States are left to determine how to enforce the rules and may impose stricter requirements than the federal standards. Network adequacy is particularly important for behavioral health care because of well-documented shortages in providers, particularly in rural areas (e.g., SAMHSA, 2013a).

Overall, parity requirements should usher in improvements in parity, provision of benefits, and improved access for behavioral health care. Estimates suggest that the recent legislative changes in behavioral health insurance coverage will have allowed at least 35 million individuals in individual or small group plans to access behavioral health services at full parity (Beronio et al., 2013).

2.3. Literature on Behavioral Health Coverage, Network Adequacy, and Workforce Shortage

Improved and expanded coverage for behavioral health care will only result in increases in access if there is a sufficient supply of providers and if plans' provider networks are adequate. Data lag behind policy events by 1-3 years. Thus, evidence on the degree to which these issues have been addressed since the systemic changes coming in 2014 will likely be available soon after the publication of this report.

The literature has documented behavioral health care workforce shortages for decades (Cummings et al., 2014; SAMHSA, 2013; Thomas et al., 2009). There are few psychiatrists, for example, in rural areas. The potential for variation in specific services covered in benchmark plans across states also suggests that the scope of coverage for behavioral health services may not be despite recent legislation. For example, studies document variation in the coverage of specific services, such as behavioral therapies for autism, among small group plans (Skopec et al., 2011). This variation may be associated with the availability of providers in the health care system. The role that provider capacity will play in realizing the benefits of coverage expansion for behavioral health services across states is not yet known and will require in-depth review as the insurance plans offered on the health exchanges go into effect.

Despite a burgeoning literature on network adequacy (Haeder et al., 2015, 2016; Polsky & Weiner, 2015), few published studies exist on network adequacy specifically for behavioral health provision. Studies have anticipated the potential impact of network adequacy requirements (e.g., Corlette et al., 2014), and yet other studies have addressed how standards should be considered for mental health more specifically (Miller et al., 2014). However, limited evidence on this topic is available using data more recent than 2013.

2.4. Literature on the Impact of Parity

Recent literature on the impact of federal efforts to expand behavioral health coverage focuses on the Federal Employees Health Benefits Program and MHPAEA. Studies on the parity requirements of 2010 are still coming to light at the time of this report. Importantly, the existing studies use utilization of and access to care as outcomes, but few studies examine changes in the availability of benefits from insurance plans.

Findings on parity implementation among plans offered by the FEBHP are encouraging. Goldman et al. (2006) and Northrup Grumman Information Technology, Inc. (2004) found that plans complied with parity by 2011, no plans reported major problems expanding behavioral health coverage to meet the MHPAEA requirements, and no plans stopped offering FEBHP plans to avoid complying with the MHPAEA. Most of these plans chose to carve out behavioral health benefits, and there was no evidence of increased use of non-quantitative treatment limitations (NQTLs) for behavioral health treatment. The expansion of benefits was associated with a significant decrease in out-of-pocket spending on behavioral health for beneficiaries (Azrin et al., 2007). Evidence on changes in utilization was unclear and likely minimal (Azrin et al., 2007). The finding that the legislation was not associated with a significant change in utilization is similar to the finding from analyses on the impact of state mental health parity laws on utilization among children and adolescents (Busch et al., 2013).

A study of several samples of large employer-sponsored health insurance plans following implementation of the MHPAEA showed that health plans had made substantial changes to plan designs to meet the standards in the MHPAEA (Goplerud, 2013). That study suggests inpatient, prescription medication, and emergency department benefits conformed to many MHPAEA standards in 2011. For inpatient benefits, this finding was perhaps particularly significant because consumer cost-sharing had been higher for mental health services than medical/surgical services in 2009. Meeting the standards did not appear to come at the cost of increasing financial requirements for medical/surgical care.

The study of large employer-sponsored plans also raised at least four considerations that are potentially relevant to individual and small group plans in the current study. First, in-network outpatient behavioral health benefits were more likely to be inconsistent with requirements than out-of-network outpatient benefits. Second, approximately one-fifth of the plans used outpatient in-network co-pays that failed to meet MHPAEA standards. Third, plans frequently employ NQTLs -- such as precertification requirements -- for behavioral health conditions that are more restrictive than those used for medical/surgical conditions.

Fourth, by the time the 2014 deadline came into effect, individual and small group markets may have already adjusted to accommodate parity requirements. Evidence in the large group market from a sample of plan designs in 2010 -- 1 year before the MHPAEA took effect for large group plans -- found that most plans that were offered to employees of large businesses provided prescription coverage that met MHPAEA standards for cost-sharing.

One study to date assesses coverage for substance use disorders in EHB benchmark plans used by states (National Center on Addiction and Substance Abuse, 2016); EHBs are the ten benefit categories that most individual and small group market plans must include. The results indicate up to 31 percent of plans were identified as potentially having a parity violation for substance use disorder service coverage. Residential treatment programs and methadone maintenance therapy were particularly unlikely to be covered by EHB plans, while 88 percent of plans lacked the necessary data to evaluate compliance with EHB mandates fully.

3. METHODS

3.1. Overview

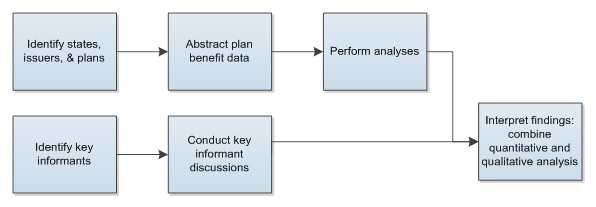

This section describes the methods used to address the research questions. Because no single data source is readily available to answer the research questions directly, we relied on several sources to obtain quantitative and qualitative data. We first identified the states, issuers, and plans to include in the analysis (Figure 3-1). We selected 217 plans, of which 166 had usable data. The sample was based on a number of criteria, including practical considerations, such as data quality and project resources.

After identifying plans and obtaining pertinent documents for each plan -- typically, the contract and summary of benefits and coverage -- we abstracted plan benefit data from plan documents using a standardized template. The template includes the conditions and services covered or excluded, disaggregated by setting (e.g., outpatient) and network status (in-network vs. out-of-network). We also conducted key informant discussions as a separate data source and to contextualize the findings from the quantitative analysis. We then analyzed the quantitative data and reviewed the synthesis of the findings from the key informant discussions.

Quantitative analyses focused on the plan benefit data that we abstracted and were used primarily in three research questions: scope (RQ1), level (RQ2), and these two stratified by type of exchange plan (RQ3). Qualitative analyses focused on the informant discussions.

| FIGURE 3-1. Methods Flow |

|---|

|

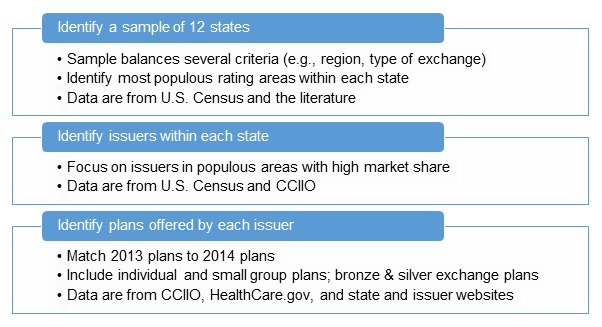

3.2. Identify States, Issuers, and Plans

To identify the plans to include in the study, we first identified a representative sample of 12 states and then determined the most populous health insurance rating areas within those states (Figure 3-2). We chose issuers based on market share and data availability. We then applied standardized selection criteria to identify plans from those issuers. Our final list of plans consisted of on-exchange and off-exchange, individual and small group, and bronze and silver metal tiers.

| FIGURE 3-2. Process of Identifying States and Data Sources |

|---|

|

3.2.1. Identify a Sample of States and Rating Areas within States

Data Sources

To construct a sample of states, we used information on state characteristics from the Census Bureau, public sources on exchange characteristics, and the Center for Consumer Information and Insurance Oversight (CCIIO). To select the most populous rating areas within each state in 2014, we used CCIIO's Rate and Benefit Information System (RBIS) data and the CCIIO Individual and Small Group Market Geographic Rating Areas by State (CCIIO, 2014). Under the Market Rules and Rate Review Final Rule (45 CFR Part 147), each state has a set number of geographic rating areas that all issuers in the state must uniformly use as part of their rate setting.

Process of Creating a State Sample

We constructed the sample of states using four primary criteria (Table 3-1), which ensured that at least one state was represented within each of the following categories: the four census regions of the country (Northeast, Midwest, South, and West) (Census Bureau, 2015b); three types of exchanges (federal, state, and partnership); whether the Federal Government directly enforces exchange regulation compliance, including rate filing (CCIIO, n.d.); and proportion of population living in a rural area rather than an urban area (Census Bureau, 2010). After ensuring that each of these four primary criteria were met, we applied secondary selection criteria, which gave preference to states with a large population (Census Bureau, 2013) and for which sufficient data were available.

| TABLE 3-1. Sample States and Selection Criteria Information | |||||

|---|---|---|---|---|---|

| State | Census Region | Type of Exchange | Proportion Urban Population (%) |

Direct Federal Enforcement of Requirements |

State Population (millions) |

| California | West | State | 95 | No | 38.3 |

| Connecticut | Northeast | State | 88 | No | 3.6 |

| Florida | South | Federal | 91 | No | 19.6 |

| Idaho | West | State | 71 | No | 1.6 |

| Michigan | Midwest | Partnership | 75 | No | 9.9 |

| Minnesota | Midwest | State | 73 | No | 5.4 |

| New Hampshire | Northeast | Partnership | 60 | No | 1.3 |

| New Jersey | Northeast | Federal | 95 | No | 8.9 |

| New York | Northeast | State | 88 | No | 19.7 |

| Ohio | Midwest | Federal | 78 | No | 11.6 |

| Oklahoma | South | Federal | 66 | Yes | 3.9 |

| Pennsylvania | Northeast | Federal | 79 | No | 12.8 |

| SOURCES: HRSA, 2014; Kaiser Family Foundation, 2016; SAMHSA, 2013; Census Bureau, 2010, 2013, 2014, and 2015b; HHS, 2016. | |||||

The sample excludes five states that implemented major statewide reforms of commercial insurance coverage before 2013: Hawaii, Maryland, Massachusetts, Oregon, Vermont, and Washington. The exclusion helps ensure that the final sample of plans more closely represents typical plan offerings in the individual and small group market across the United States. An initial review of state characteristics considered other factors, such as whether the state had a strong or weak parity law (Lang, 2013). Appendix A documents the initial review of all 50 states across a larger set of criteria.

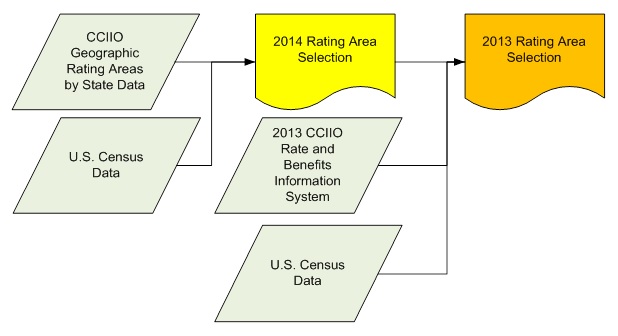

Process of Identifying Most Populous Rating Areas within Each State

Figure 3-3 describes how we combined three data sources to identify the most populous rating areas in each of the sample states. We first selected 2014 rating areas with the highest population according to 2010 census data. We then identified the most populous zip code in those selected 2014 rating areas and selected the 2013 rating areas that contained those most populous 2014 zip codes (Census Bureau, 2015a, 2016). We used Stata 14 and Microsoft Excel 2013 to extract and rank rating areas.

| FIGURE 3-3. Health Insurance Rating Area Selection Process |

|---|

|

3.2.2. Issuer Selection

Data Sources for Selecting Issuers

We used the CCIIO Medical Loss Ratio (MLR) database to rank issuers by market share in each state and select issuers for the analysis. Insurers are required to submit a report to HHS by June of each year showing how they spent revenues in the past year. Medical loss refers to the amount of the premium spent on medical care and quality improvement; the law requires that 80 percent of insurance premium dollars in the small group insurance plans be spent on medical care or quality improvement and that rebates be provided to customers if the insurer fails to meet this standard. Each insurer's MLR information is provided by state and market (individual, small group, or large group). We decided to focus on determining market share by comparing the issuers with the largest market shares in each state based on: (1) number of covered lives; and (2) total number of policies issued.

Process to Select Issuers

To select issuers within each of the sample states, we first identified the top four issuers with the largest market share for individual and small group markets combined within each state using available information from the MLR database. Market share was defined by: (1) number of covered lives; and (2) total number of policies issued. Of the four identified issuers per state, we then selected at least two issuers based on the availability and completeness of rate and benefit data for those issuers. If the issuer with the highest market share had limited availability of rate and benefit data, the issuer with the next highest market share was selected. Appendix B lists the top four issuers by market share in the sample.

Because we were able to obtain policy documents from only one issuer in California, Blue Cross of California, we deviated from the principle of selecting issuers by largest market share. To identify additional plans due to the lack of data availability in California, we selected two issuers in Oklahoma and Florida that had high market share but were not among the top four issuers already selected. We chose these states and issuers on the basis of available data on insurance plan rate and benefits.

3.2.3. Plan Selection

Data Sources to Select Plans

To identify plans, we used four distinct data sources:

-

CCIIO Health Insurance Marketplace Public Use Files (PUF),

-

CCIIO RBIS data,

-

HealthCare.gov Federal Facilitated Marketplace (FFM) Qualified Health Plan (QHP) Landscape Files, and

-

health insurance rate filings.

The CCIIO Health Insurance Marketplace PUF provided a large portion of 2014 health insurance plan rate data (CCIIO, 2016a). The Marketplace PUF includes plan-level and issuer-level information for certified QHPs and stand-alone dental plans offered to individuals and small businesses through the Health Insurance Marketplace. The Marketplace PUF includes data from states participating in the FFM, which include State Partnership Marketplaces, and states whose state-based Marketplaces rely on the federal information technology platform for QHP eligibility and enrollment functionality.

The CCIIO RBIS data provided the majority of 2013 rate information, because they contain data for the HealthCare.gov inventory of insurance plans, by quarter beginning in 2012 (CCIIO, 2016b). Although RBIS data provide rate information for plans, they have two limitations. First, select issuers in states have redacted rate information from the publicly available data. Therefore, the team requested and received from CCIIO the unredacted 2013 and 2014 rate data to complete this analysis. Second, the 2013 RBIS small group data does not provide rate information for specific small group plans, but rather provides a range of rates for groupings of plans known as products. Therefore, we were unable to use the 2013 RBIS small group data for plan selection.

FFM QHP landscape files provide a succinct and limited set of data available from the Marketplace PUF (HealthCare.gov, 2016b). The FFM QHP landscape files also include plan names, which are not available in the Marketplace PUF. We used this source to link plan names with the plans identified in the Marketplace PUF.

We used health insurance rate filing documents to identify rate information when other previously mentioned data sources did not provide sufficient information. These documents were sourced from required rate filings on state websites, the National Association of Insurance Commissioners' (NAIC's) System for Electronic Rate and Form Filing (SERFF), and by direct request to the states by e-mail and telephone communication. Table 3-2 summarizes the relevant regulatory agencies and the rate filing sources we used, by state.

| TABLE 3-2. Source of Health Insurance Rate Filings, by State | ||||||

|---|---|---|---|---|---|---|

| State | State Regulatory Agency | Federal Marketplace | RBIS | SERFF | State Website | Direct State Contact |

| California | Department of Managed Health Care, California Department of Insurance | X | X | |||

| Connecticut | Connecticut Insurance Department | X | X | X | ||

| Florida | Florida Office of Insurance Regulation | X | X | X | ||

| Idaho | Idaho Department of Insurance | X | X | X | ||

| Michigan | Michigan Department of Insurance and Financial Services | X | X | X | ||

| Minnesota | Minnesota Department of Commerce | X | X | X | ||

| New Hampshire | New Hampshire Insurance Department | X | X | X | ||

| New Jersey | Department of Banking and Insurance | X | ||||

| New York | Department of Financial Services | X | X | |||

| Ohio | Ohio Department of Insurance | X | X | X | ||

| Oklahoma | Oklahoma Insurance Department | X | X | |||

| Pennsylvania | Pennsylvania Insurance Department | X | X | X | ||

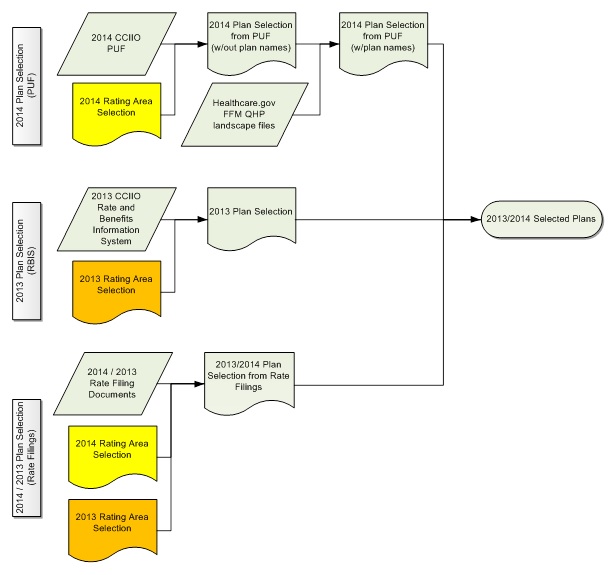

Process to Select Plans

To select plans, we followed the process shown in Figure 3-4. We used CCIIO PUF data to select 2014 plans in the selected rating areas, and we used the HealthCare.gov FFM QHP landscape files to identify plan names. We then used CCIIO RBIS data to select 2013 plans in the selected rating areas. For issuers that did not provide plan information in the PUF or RBIS, we completed the process of selecting plans using rate filing documents in the selected rating areas. We completed plan selection using Stata 14, SAS 9.4, and Microsoft Excel 2013.

| FIGURE 3-4. Health Insurance Plan Selection Process |

|---|

|

For each issuer, we selected 2014 health insurance plans using the following criteria:

-

Within the most populous 2014 rating area for each state, or the next most populous rating area when plans for the selected issuers are not available in the most populous rating area;

-

45 years old;

-

Male;

-

Non-smoker;

-

Coverage for one person only (not a family, no dependents);

-

Not a dental-only plan;

-

Not a grandfathered plan;[3]

-

With an effective date closest to but not before January 1, 2014.

We then selected the lowest priced bronze plan and second highest silver plan per issuer for the individual market and for the small group market, for both on-exchange and off-exchange plans. In cases where only one silver plan was offered, we selected that plan. A maximum of eight plans per issuer could be selected through this process, depending on whether all data were available and the issuer offered both on-exchange and off-exchange plans.

We selected 2013 plans with plan premiums most similar to the premiums of selected 2014 plans. This approach helped reduce confounds when comparing 2013 and 2014 plans. We adjusted 2013 plan premiums for inflation using the Consumer Price Index. Although the annual inflation rate has been low -- at just over 1.5 percent -- we made this adjustment so that for any given 2014 plan we would be able to choose among alternative 2013 comparison plans. Note that it was not possible to use metal category rather than premium to match plans because exchanges were newly created in 2014.

| TABLE 3-3. Plan Selection Data Sources by Issuer and Year/Exchange | |||||||

|---|---|---|---|---|---|---|---|

| State | Issuer | 2014 | 2013 | ||||

| On-Exchange | Off-Exchange | ||||||

| Sourcea | N | Sourcea | N | Sourcea | N | ||

| CA | Blue Cross of California | RF | 2 | RF | 2 | RBIS | 4 |

| CT | Anthem Health Plans | RF | 4 | RF | 4 | RBIS | 7 |

| FL | Aetna Life Insurance Company | PUF | 2 | N/A | N/A | ||

| BCBS of Florida | PUF | 3 | RF | 3 | RBIS | 7 | |

| Coventry Health Care of Florida | PUF | 2 | N/A | RBIS | 2 | ||

| ID | Blue Cross of Idaho | PUF | 2 | RF | 2 | RBIS | 2 |

| PacificSource Health Plans | PUF | 2 | N/A | RBIS | 1 | ||

| SelectHealth | PUF | 2 | N/A | N/A | |||

| MI | BCBS of Michigan | PUF | 2 | N/A | RBIS | 3 | |

| Priority Health | PUF | 2 | N/A | N/A | |||

| MN | BCBS | RF | 4 | RF | 4 | RF | 6 |

| HealthPartners | RF | 2 | RF | 2 | RBIS | 5 | |

| Medica | N/A | 2 | N/A | RBIS | 2 | ||

| NH | Matthew Thornton Health Plan (Anthem BCBS) | PUF | 4 | RF | 4 | RBIS | 6 |

| NJ | AmeriHealth | RF | 2 | RF | 2 | RF | 2 |

| Horizon BCBS | RF | 2 | RF | 2 | RF | 1 | |

| NY | Empire | RF | 2 | N/A | N/A | ||

| Oxford Health Plans | N/A | RF | 2 | N/A | |||

| OH | Community Insurance Company (Anthem BCBS) | PUF | 2 | RF | 2 | RBIS | 4 |

| Humana Health Plan of Ohio | PUF | 1 | N/A | N/A | |||

| OK | BCBS of Oklahoma | PUF | 2 | N/A | RBIS | 1 | |

| CommunityCare | PUF | 2 | N/A | RBIS | 1 | ||

| Coventry Health Care of Kansas | PUF | 2 | N/A | RBIS | 2 | ||

| PA | Aetna | PUF | 2 | N/A | RBIS | 2 | |

| Highmark | PUF | 2 | RF | 2 | RBIS | 2 | |

| Total number of plans | 54 | 31 | 60 | ||||

|

|||||||

To complete 2013 plan selection, we restricted rates for 2013 health insurance plans to the same conditions as those for 2014 plans, with two exceptions. First, we identified the most populous zip code within the most populous 2014 rating area and then selected 2013 plans offered in that zip code. Second, we selected plans with an effective date closest to but not before January 1, 2013. Then, for each selected 2014 plan, we selected a matching 2013 plan from the same state, issuer, and market type by choosing the 2013 plan with the smallest absolute difference in premium from the 2014 plan. We normalized prices using the Consumer Price Index. Because we were interested in obtaining the best match based on premium, some selected 2014 plans with equal or similar premiums from the same state, issuer, and market were matched to identical 2013 plans.

In some cases, selected plans from either year did not have sufficient benefit information to complete benefit abstraction. We therefore removed such plans from the analysis and selected the next most applicable plan.

The original design of the study was to select 2014 plans and then case match to them comparison plans from 2013, potentially with duplication. For the 85 2014 plans we were able to identify 81 2013 group plans as case-matched comparison plans (166 plans in total). These 81 case-matched comparison plans included 16 duplicate plans. Excluding these duplicates, we thus had documents for 145 unique plans, with 85 2014 plans and 60 2013 unique plans. Of the 2014 plans, 66 were individual market plans and 19 were small group, and of the 2013 plans, 47 were individual market and 13 were small group. Table 3-3 lists each of the selected states and issuers, the data sources used to complete plan selection for each, and the number of plans selected for each issuer, by year and exchange type.

3.3. Abstract Plan Benefit Data

After identifying plans, we located and manually reviewed each plan's benefit data. We then systematically abstracted the benefit information using two templates, one for the plan benefit data on scope and coverage and the other for information on prescription drug coverage and formulary design.

3.3.1. Data Sources

We obtained plan benefit data and issuer pharmacy data from health insurance policy documents, including plan policy contracts, certificates of coverage, summaries of benefits and coverage, and other documents that detailed either scope of benefits covered or cost-sharing level (e.g., HealthCare.gov, 2016c). These documents were sourced from required form filings on state websites, NAIC's SERFF, or publicly accessible insurer or insurance broker websites (Table 3-4). If the data were not available online, we requested policy documents directly from states.

| TABLE 3-4. Source of Health Insurance Benefit Information Policy Documents, by State | |||||

|---|---|---|---|---|---|

| State | State Regulatory Agency | SERFF | State Website | Other Website | Direct State Contact |

| California | Department of Managed Health Care, California Department of Insurance | X | |||

| Connecticut | Connecticut Insurance Department | X | X | ||

| Florida | Florida Office of Insurance Regulation | X | X | ||

| Idaho | Idaho Department of Insurance | X | |||

| Michigan | Michigan Department of Insurance and Financial Services | X | X | ||

| Minnesota | Minnesota Department of Commerce | X | X | X | |

| New Hampshire | New Hampshire Insurance Department | X | X | ||

| New Jersey | Department of Banking and Insurance | X | X | ||

| New York | Department of Financial Services | X | |||

| Ohio | Ohio Department of Insurance | X | |||

| Oklahoma | Oklahoma Insurance Department | X | |||

| Pennsylvania | Pennsylvania Insurance Department | X | X | ||

| NOTE: Other Website = insurer, broker, or consumer website. | |||||

3.3.2. Plan Data Abstraction

We developed a data entry template in Microsoft Excel to systematically abstract and store data from plan documents. The template details scope and level information for behavioral health and medical/surgical conditions on parallel benefit classes (e.g., inpatient, outpatient, office visits) and for unique and policy-relevant specific conditions and services (e.g., coverage for autism). Combined across scope and level and across types of conditions, the template included 241 data fields.

Analysts reviewed all documents for each plan for text on each data field and entered the findings into the template. To ensure that the data supported quantitative analysis, we standardized the entry of freeform text by defining keywords and, where applicable, defining common synonyms for keywords. We created a separate reference document that details and distinguishes between the following categories of services in particular: intermediate care, intensive behavioral therapy, intensive outpatient treatment (or therapy), and post-acute or rehabilitative care. Because these services share similar characteristics, it was particularly important to distinguish among the services. Appendix C presents the keywords and discusses guidance on abstracting data on these services.

Many data fields on scope recorded whether coverage for a specific condition or service was evident; the data from the plan text for these fields were entered into four categories:

-

explicitly provides coverage;

-

explicitly excludes coverage;

-

neither explicitly provides nor excludes coverage; and

-

mentions the item, but coverage is unclear.

We reviewed and reconciled instances where data fields had an "unclear" data entry.

3.3.3. Pharmacy Data Abstraction

The main data source for pharmacy data was plan formularies. A formulary lists covered medications by class and sub-class of condition and contains rudimentary information on which cost-sharing tier of coverage the medication falls into and coverage limitations within that tier, such as quantity limits. The tier determines the consumer burden, with the first tier typically covering many generic medications with the lowest level of consumer burden. The number and meaning of tiers varies across formularies.

Importantly, we found that for all the plans we assessed, the formulary was set at the issuer-level and did not vary across plans. We could not find formulary data for all plans or always reliably attribute a formulary to a specific plan that was consistent over time. For these reasons, we sampled five issuer formularies for both 2013 and 2014.

Because the number of all available medications would be unwieldy analytically, we narrowed the formulary analysis to therapy for behavioral health and four classes of chronic medical conditions: asthma, cardiovascular disease, diabetes, and HIV/AIDS. Although the number of medications that this process then included varied by formulary and year, the final data included approximately 270 medications for each formulary.

To develop a template for pharmacy data, we developed a list of medications for behavioral health and medical/surgical conditions using medication guidance from government agencies (e.g., U.S. National Library of Medicine), non-profit interest groups (e.g., American Heart Association), and the appropriate academies (e.g., American Academy of Allergy, Asthma and Immunology). We abstracted for each medication whether the medication was explicitly covered, the tier for medication, and the type of any limitations.

3.4. Perform Analysis

We merged and analyzed abstracted plan benefit and pharmacy benefit data using Stata 14. We converted data on scope of coverage to dichotomous variables in the case of "yes" or "no" responses and to categorical variables in the case of "explicitly covered," "explicitly excluded," or "neither" responses. "Unclear" responses were converted to missing. We used the converted data to create frequency counts and percentages of the various response types by year and exchange type.

We converted data on level of coverage, including deductibles, out-of-pocket limits, co-insurance, and co-pay, to numeric variables. Non-numeric responses (e.g., "n/a," "none," or "not stated") were converted to missing. For plan benefit characteristics that were tiered (e.g., pharmacy cost-sharing), we used only the data for the first tier in the analysis. We treated co-insurance for plans with a 0 percent co-insurance and positive co-payment as having no co-insurance; we treated plans with a zero co-payment and positive co-insurance as having no co-payment. We did not adjust monetized benefit features, such as co-payments, for inflation. We created new dichotomous variables indicating whether plans applied the specified type of cost-sharing (for example, whether a co-insurance rate is applied). We then used the converted data and new variables to create summary statistics by year and exchange type.

For each prescription drug, we assessed its tier (i.e., 1, 2, 3, or missing) and any exceptions noted in the formulary (e.g., step therapy, prior authorization) as categorical variables. We grouped prescription medications by condition type (e.g., attention deficit/hyperactivity disorder [ADHD], anti-anxiety, asthma) and then tabulated frequency distributions for the count of drugs by condition type within each tier and exception type by year. In some instances, matched formularies would list prescription medication information in one year's formulary but not the other. Because of the small sample size, these partially missing data could bias the results. We therefore included medication data only if they were available in matched formularies for both years.

We used t-tests to assess statistically significant differences in scope, level, and prescription drug coverage across years. To the extent possible, we also used t-tests to compare differences in scope and level between behavioral health and medical surgical, and in-network and out-of-network. Finally, we ran t-tests in sub-analyses to compare differences in scope and level between on-exchange and off-exchange plans, plans in Medicaid and non-Medicaid expanded states, and plans in state and federally facilitated marketplaces.

We searched data on measures of NQTLs by reviewing text that had not been systematically captured when applying the pre-designed template. We searched for keywords (e.g., prior authorization) and then thematically categorized and aggregated the results. We followed the guidance for terminology in Appendix D.

A review of plan data confirmed that the plan documents that we reviewed do not contain sufficient information about network size. Research questions on this topic relies on synthesizing the discussion from the key informant discussions.

3.5. Key Informant Discussions: Data and Analysis

3.5.1. Overview

We held discussions with nine key informants representing eight different organizations to get their impressions on the behavioral health benefit coverage changes after the implementation of parity requirements. Information from the key informant discussions addressed the first four research questions. Key informants for this project included representatives from issuers, state health insurance officials, nationally recognized experts who study state health insurance plans more broadly, and benefits consultants with experience in benefit and plan design. In addition to the key informants below, the National Academy for State Health Policy was a partner on this project and also provided their knowledge and expertise.

3.5.2. Key Informant Discussions: Data

The discussions were 1-hour, open-ended, semistructured meetings conducted by telephone. We developed and used a discussion guide for all conversations (Appendix D) that covered the four core areas of the research questions: scope of coverage, level of coverage, network adequacy, and the use of Managed Behavioral Health Organizations. We tailored each guide to fit the background of the informant. For example, for informants with state-specific expertise, the guide included probes on how the state defines and applies network adequacy requirements.

At least two study team members participated in each discussion: a lead, who conducted the conversation, and a note taker. We audio-recorded the conversation with informants' approval. The recording was used to prepare detailed and accurate notes. After summarizing the discussion findings in a report, we deleted the recordings.

3.5.3. Key Informant Discussions: Analysis

We reviewed the notes for each discussion and created thematic statements for each topic that was discussed, including topics that were raised but were not included in the discussion guide. We then created thematic statements by combining topical statements across discussions. This approach to analysis deliberately treated the data from the discussions as qualitative data from a limited set of discussions. Thus, the data did not support quantification -- which was a key step in the plan benefit data, above -- and significant gains were not likely from applying qualitative data analysis tools, such as ATLAS.ti.

We reviewed the qualitative data to identify themes regarding coverage and relevant changes between 2013 and 2014. For example, with regard to network adequacy, we assessed the responses for themes on the types of behavioral health services provided in networks, the extent to which difficulties with accessing behavioral health services are related to geographic dispersion, and whether there was a trend among behavioral health providers in accepting new patients following the coverage expansion. We then compared these themes with those for medical/surgical benefits.

4. RESULTS

4.1. Scope of Coverage

4.1.1. Overview

To assess scope of coverage, analyses focus on coverage exclusions and inclusions, broken out by conditions and treatment services. To ensure that the results are easily interpretable, all main analyses focused on in-network coverage, wherever network status is specified in plan documents. Out-of-network coverage is described in a separate sub-analysis. Also, this section addresses the proportion of plans covering prescription medications; Section 4.3 describes more detailed analyses of formularies and NQTLs for prescription medication.

The tables and figures in this section report the number of observations and estimates of the relevant percentages and counts. For the sake of clarity of presentation, these tables and figures do not present t-values and p-values. The appendix tables (Appendix E) present the estimates of t-values and p-values. The title of each appendix table provides the corresponding table number from the main report. Because we used the estimates from one table or figure to make multiple comparisons (e.g., by year and by setting), a given table in the main body of the text may map to more than one appendix table.

4.1.2. Scope of Coverage by Medical or Behavioral Health Condition

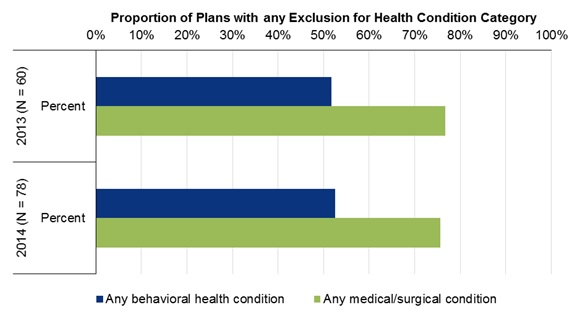

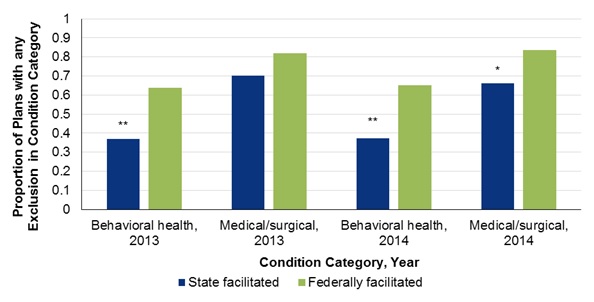

Figure 4-1 shows little change in the proportion of plans with an explicit exclusion for any behavioral health condition between 2013 and 2014 (52 percent and 53 percent), and little change in this proportion for any medical/surgical condition (77 percent and 76 percent). Explicit exclusions were less common for behavioral health than medical/surgical conditions (p = 0.00 in both years).

| FIGURE 4-1. Percentage of Plans with Any Explicitly Stated Exclusion for Behavioral Health and for Medical/Surgical Conditions, 2013 and 2014 |

|---|

|

Table 4-1 disaggregates the estimates by three specific, policy-relevant conditions. The proportion of plans explicitly covering autism more than doubled from 2013 to 2014, with an increase from 20 percent to 53 percent. The proportions explicitly excluding and omitting the condition from the plan document altogether fell by more than 50 percent over this same period. The estimates of change over time for autism were statistically significant at conventional levels (p < 0.05). The proportion of plans with missing data (approximately 11 percent) regarding autism -- because the document with relevant coverage information was missing -- changed little over time.

The estimates in Table 4-1 also vary considerably across the three conditions. Organic brain disorders and tobacco use were typically not mentioned in plan documents. However, whereas the proportion of plans explicitly covering organic brain disorders did not change over time, the proportion covering tobacco use doubled. The relatively large increase in the proportion of plans covering tobacco use -- from 12 percent to 21 percent -- was not statistically significant. For the purposes of the current study, the plan documents frequently did not sufficiently describe coverage for any of the three conditions. Autism coverage in 2014 was insufficiently described in nearly 25 percent of the plans, for example.

| TABLE 4-1. Percentage of Plans with Explicitly Stated Coverage and Exclusions for Select Health Conditions, 2013 and 2014 | ||||||||

|---|---|---|---|---|---|---|---|---|

| Health Condition | 2013 (N=60) | 2014 (N = 78) | ||||||

| Covered | Excluded | Uncleara | Missingb | Covered | Excluded | Uncleara | Missingb | |

| Autism | 20% | 23% | 45% | 12% | 53% | 9% | 24% | 14% |

| Organic brain disorders | 7% | 0% | 82% | 12% | 8% | 0% | 76% | 17% |

| Tobacco use | 12% | 0% | 77% | 12% | 21% | 0% | 63% | 17% |

|

||||||||

4.1.3. Scope of Coverage by Care Setting

Table 4-2 presents estimates for the five categories of care that map to those specified in parity legislation. For the sake of brevity, the discussion focuses on the proportion of plans explicitly stating coverage. We found that plan documents almost always mentioned setting.

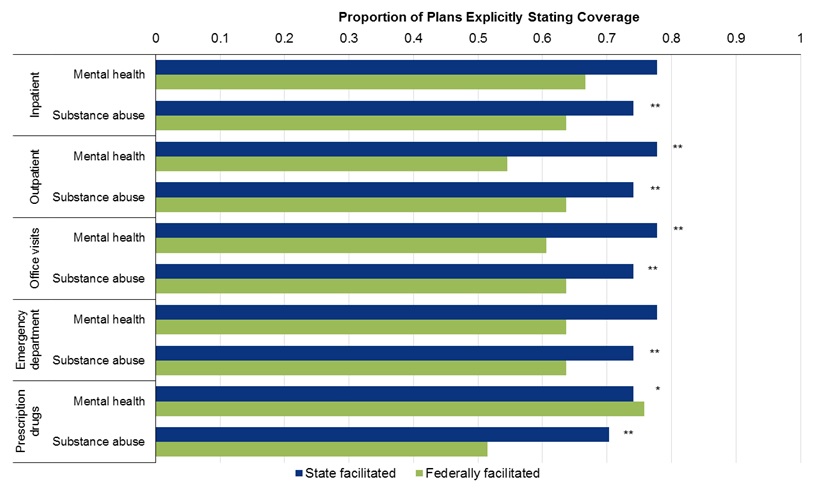

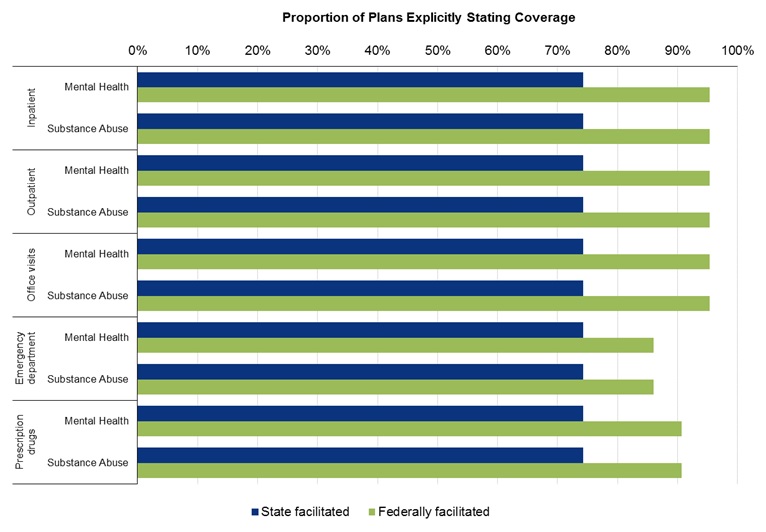

From 2013 to 2014, coverage in the five settings for behavioral health conditions converged with coverage for medical/surgical conditions. Consider, for example, outpatient coverage. In 2013, a lower proportion of plans explicitly covered either mental health (65 percent) or substance use (68 percent) conditions than medical/surgical conditions (88 percent) (p = 0.00 for comparisons to medical/surgical coverage). By 2014, the proportion of plans covering the two sets of behavioral health conditions had increased to equal the proportion covering medical/surgical conditions (approximately 86 percent).

In Table 4-2, we separately assess plan document coverage for mental health care and for substance use disorder care. In both years, we found these two proportions to be similar across all five service settings.

| TABLE 4-2. Percentage of Plans with Explicitly Stated Coverage and Exclusions, for Setting and Health Condition Category, 2013 and 2014 | ||||||||

|---|---|---|---|---|---|---|---|---|

| Setting/Health Condition | 2013 (N=60) | 2014 (N = 78) | ||||||

| Covered | Excluded | Uncleara | Missingb | Covered | Excluded | Uncleara | Missingb | |

| Inpatient | ||||||||

| Mental health | 72% | 17% | 0% | 12% | 86% | 0% | 0% | 14% |

| Substance abuse | 68% | 20% | 0% | 12% | 86% | 0% | 0% | 14% |

| Medical/surgical | 88% | 0% | 0% | 12% | 86% | 0% | 0% | 14% |

| Outpatient (including urgent care) | ||||||||

| Mental health | 65% | 23% | 0% | 12% | 86% | 0% | 0% | 14% |

| Substance abuse | 68% | 20% | 0% | 12% | 86% | 0% | 0% | 14% |

| Medical/surgical | 88% | 0% | 0% | 12% | 86% | 0% | 0% | 14% |

| Office visits | ||||||||

| Mental health | 68% | 20% | 0% | 12% | 86% | 0% | 0% | 14% |

| Substance abuse | 68% | 20% | 0% | 12% | 86% | 0% | 0% | 14% |

| Medical/surgical | 88% | 0% | 0% | 12% | 86% | 0% | 0% | 14% |

| Emergency | ||||||||

| Mental health | 70% | 18% | 0% | 12% | 81% | 0% | 5% | 14% |

| Substance abuse | 68% | 18% | 2% | 12% | 81% | 0% | 5% | 14% |

| Medical/surgical | 88% | 0% | 0% | 12% | 86% | 0% | 0% | 14% |

| Prescription drugs | ||||||||

| Mental health | 75% | 13% | 0% | 12% | 83% | 0% | 3% | 14% |

| Substance abuse | 60% | 22% | 7% | 12% | 83% | 0% | 3% | 14% |

| Medical/surgical | 88% | 0% | 0% | 12% | 86% | 0% | 0% | 14% |

|

||||||||

4.1.4. Scope of Coverage by Service

Table 4-3 describes plan coverage for four types of services that are important for behavioral health care; are resource-intensive yet community-based; and that may have a medical/surgical equivalent: intensive behavioral therapy, intensive outpatient treatment (IOT), intermediate care, and post-acute or rehabilitative treatment. Intensive behavioral therapy is typically used for autism spectrum disorder and requires significant provider time; therapies for dialysis or diabetes management may require similar levels of care. IOT occurs in an outpatient setting but is a higher level of care than outpatient care. Intermediate care is as much defined by its setting as being a specific type of care; it often takes place in the community and often includes care in the home. Post-acute care may include some of the other three forms of therapy in the table and refers to services following an acute event, as opposed to, say, chronic care management (Appendix C further describes the services).

There were four major findings. The first and perhaps most important finding was that the proportion of plans explicitly covering each service for behavioral health conditions increased over time. The increase was statistically significant for each service (p < 0.05). For example, the proportion covering post-acute care or rehabilitative treatment for behavioral health conditions increased from 33 percent to 54 percent (p = 0.00).

A second finding is the proportion of plans with explicit coverage for these services when applied to medical/surgical conditions did not generally change over time. The exception was intensive behavioral therapy, which increased over the 2 years, from 3 percent to 18 percent (p = 0.01). For the other three services, the proportion explicitly stating coverage was relatively high and did not change over time. For example, the proportion of plans explicitly covering post-acute or rehabilitative treatment for medical/surgical conditions was 87 percent in 2013 and 83 percent in 2014.

| TABLE 4-3. Percentage of Plans with Explicitly Stated Coverage and Exclusions for Select Services, by Health Condition Category, 2013 and 2014 | ||||||||

|---|---|---|---|---|---|---|---|---|

| Health Condition | 2013 (N=60) | 2014 (N = 78) | ||||||

| Covered | Excluded | Uncleara | Missingb | Covered | Excluded | Uncleara | Missingb | |

| Intensive behavioral therapy | ||||||||

| Behavioral health | 12% | 30% | 47% | 12% | 32% | 29% | 22% | 17% |

| Medical/surgical | 3% | 18% | 67% | 12% | 18% | 13% | 53% | 17% |

| IOT | ||||||||

| Behavioral health | 38% | 18% | 32% | 12% | 74% | 0% | 9% | 17% |

| Medical/surgical | 78% | 0% | 10% | 12% | 77% | 0% | 6% | 17% |

| Intermediate care settings | ||||||||

| Behavioral health | 15% | 27% | 47% | 12% | 38% | 0% | 45% | 17% |

| Medical/surgical | 60% | 8% | 20% | 12% | 67% | 0% | 17% | 17% |

| Post-acute or rehabilitative treatment | ||||||||

| Behavioral health | 33% | 18% | 37% | 12% | 54% | 0% | 29% | 17% |

| Medical/surgical | 87% | 0% | 2% | 12% | 83% | 0% | 0% | 17% |

|

||||||||