U.S. Department of Health and Human Services

Market Changes in the Supply and Use of Home Health Services: 1996-1999

Frank Porell, Ph.D., University of Massachusetts, Boston

Korbin Liu, Ph.D., The Urban Institute

Douglas Wissoker, Ph.D., The Urban Institute

David P. Brungo, M.B.A., Ph.D., Candidate University of Massachusetts, Boston

January 2004

PDF Version (87 PDF pages)

This report was prepared under contract #HHS-100-97-0010 between the U.S. Department of Health and Human Services (HHS), Office of Disability, Aging and Long-Term Care Policy (DALTCP) and the Urban Institute. For additional information about this subject, you can visit the DALTCP home page at http://aspe.hhs.gov/_/office_specific/daltcp.cfm or contact the ASPE Project Officers, William Marton and Hakan Aykan, at HHS/ASPE/DALTCP, Room 424E, H.H. Humphrey Building, 200 Independence Avenue, S.W., Washington, D.C. 20201. Their e-mail addresses are: William.Marton@hhs.gov and Hakan.Aykan@hhs.gov.

The opinions and views expressed in this report are those of the authors. They do not necessarily reflect the views of the Department of Health and Human Services, the contractor or any other funding organization.

TABLE OF CONTENTS

- 1. BACKGROUND AND OUTLINE OF THE REPORT

- 1.1. Introduction

- 1.2. Background

- 1.3. Outline of the Report

- 2. HHA CLOSURE RATES AMONG GEOGRAPHIC MARKET AREAS: 1996-1999

- 2.1. Introduction

- 2.2. Data and Methodology

- 2.3. Empirical Results

- 2.4. Discussion

- 3. CHANGES IN MEDICARE HOME HEALTH AGENCY SUPPLY: 1996-1999

- 3.1. Introduction

- 3.2. Background

- 3.3. Data and Methodology

- 3.4. Empirical Results

- 3.5. Discussion

- Appendix 3.A. Methodology for Classifying HHA Service Area Changes

- 4. CHANGES IN MEDICARE UTILIZATION

- 4.1. Introduction

- 4.2. Approach and Data Sources

- 4.3. Empirical Results

- 4.4. Discussion

- Appendix 4.A. States by Census Region

- 5. GEOGRAPHIC PATTERNS OF MEDICARE HHA SUPPLY CHANGES: 1996-1999

- 5.1. Introduction

- 5.2. Data and Methodology

- 5.3. Empirical Results

- 5.4. Discussion

- Appendix 5.A. Supply Expansion and Contraction Measures

- 6. DISCUSSION

- LIST OF FIGURES

- FIGURE 2.1: Prevalence Rates of HHA Closures among HSMAs

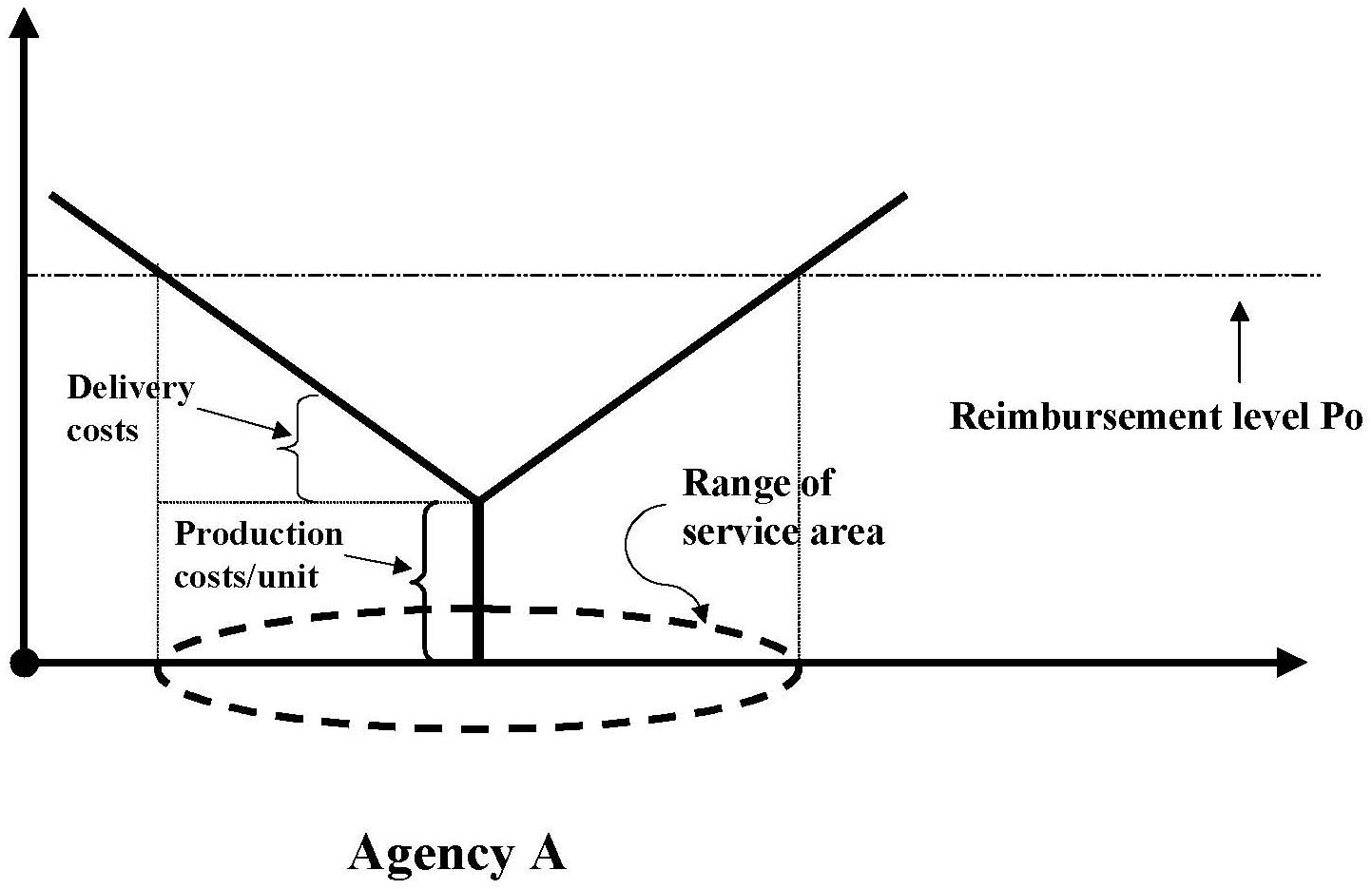

- FIGURE 5.1: The Range of Agency As Geographic Service Area with Reimbursement Level P0

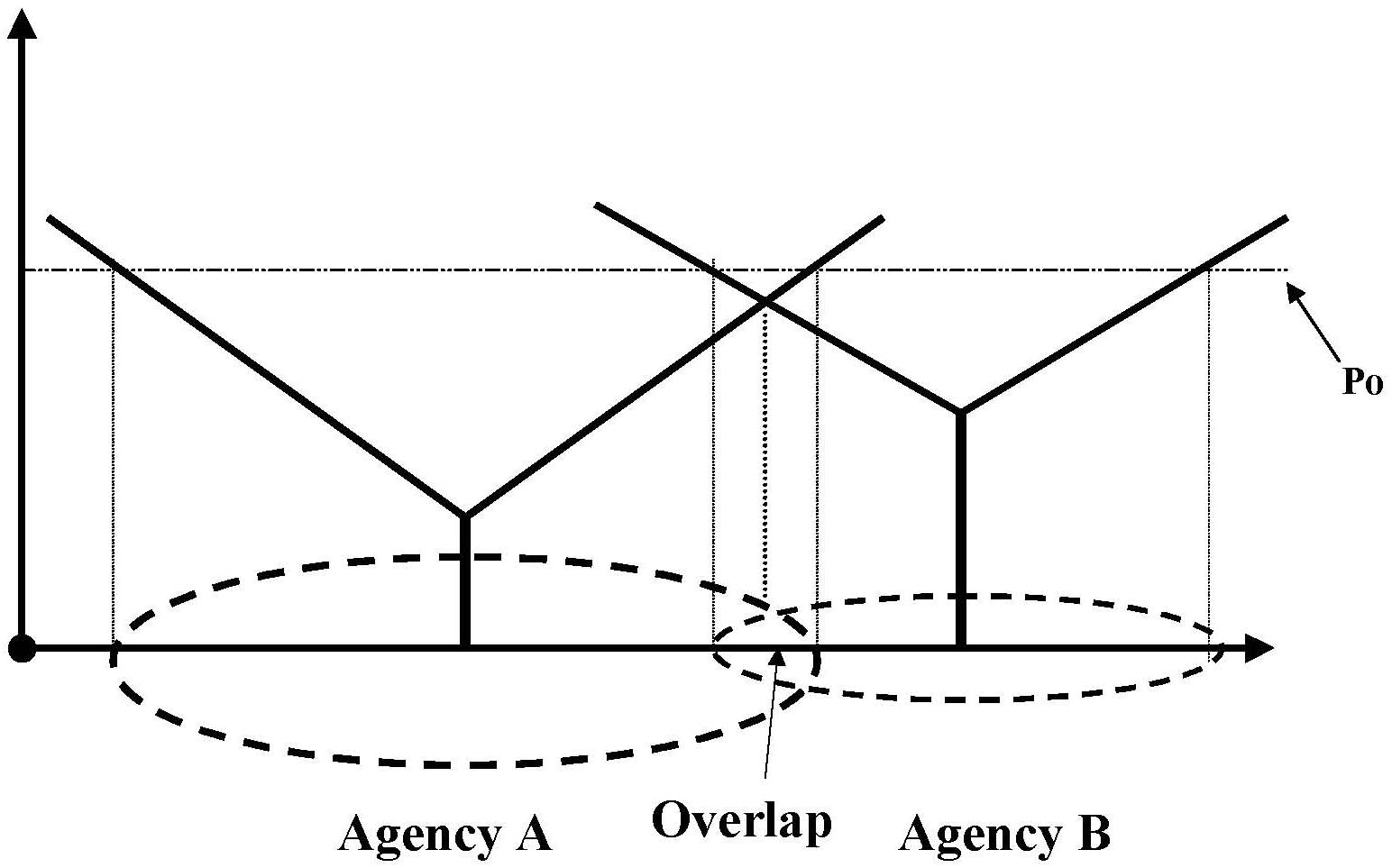

- FIGURE 5.2: Service Areas for Agencies A & B with Reimbursement Level P0

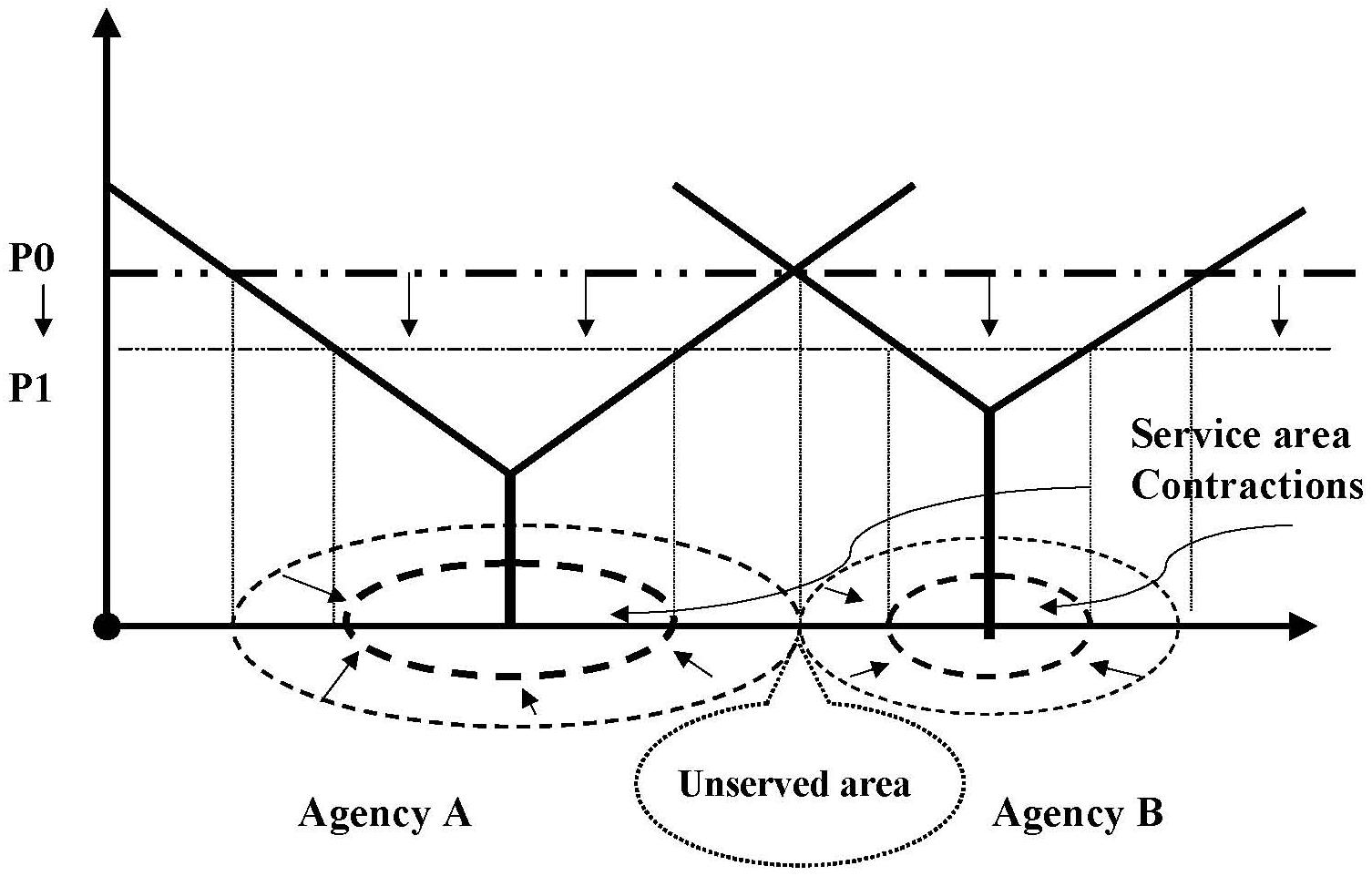

- FIGURE 5.3: Changed Service Areas for Agencies A & B After Lower Reimbursement Rate P1

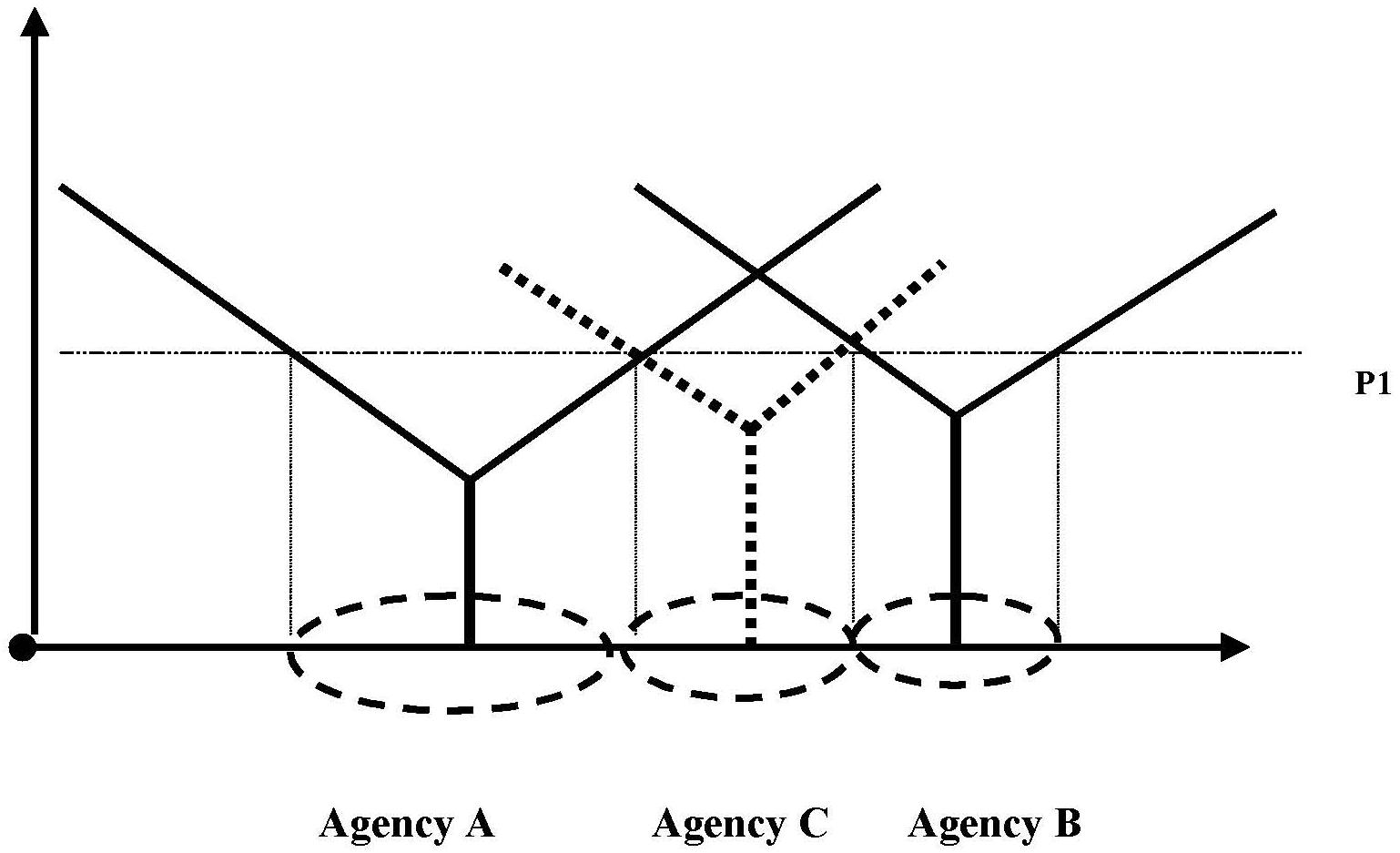

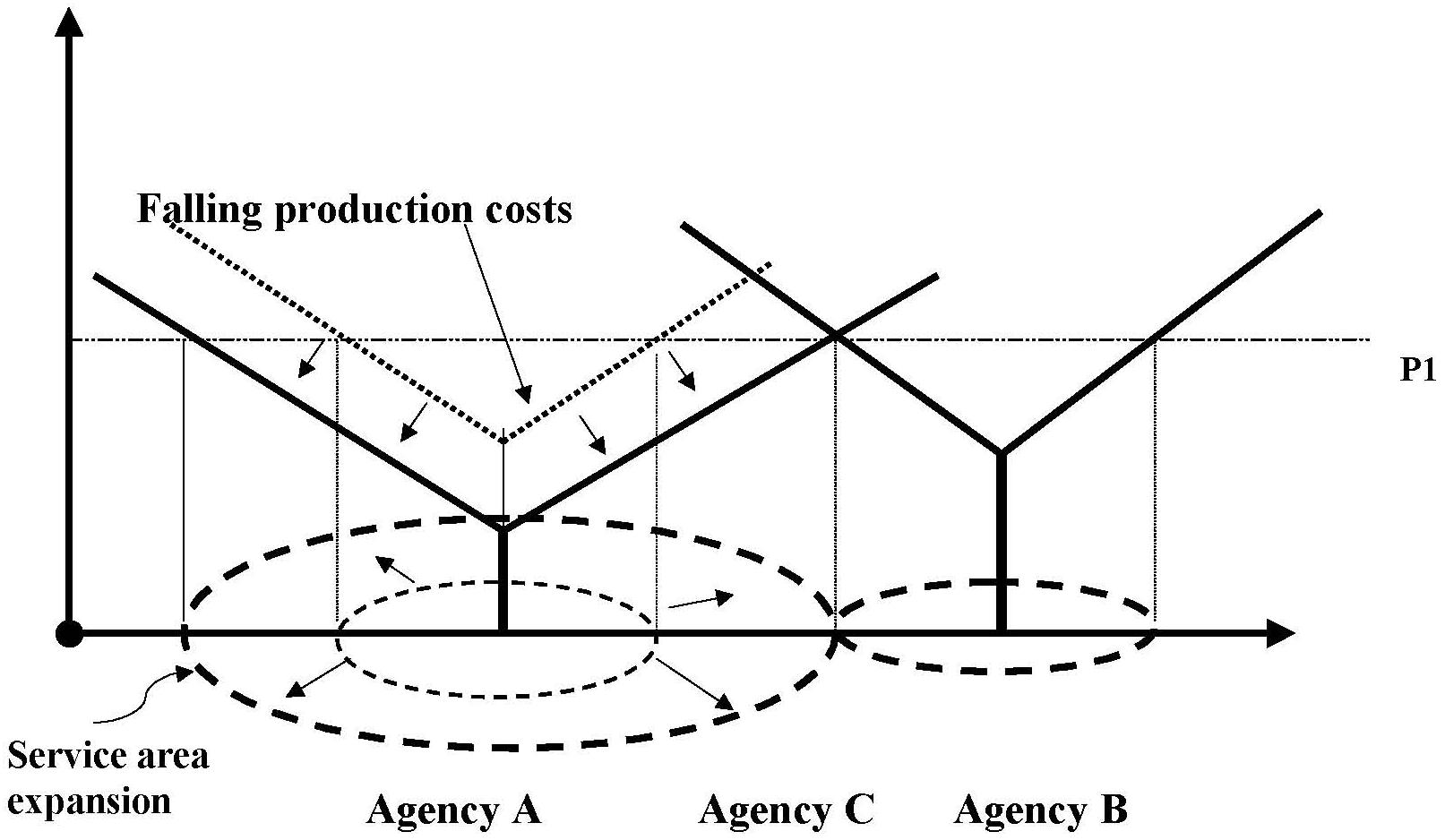

- FIGURE 5.4: New Market Entry by Agency C After Service Area Contractions by Agencies A & B

- FIGURE 5.5: Service Area Expansion by Agency A Following the Service Area Contraction by Agency B

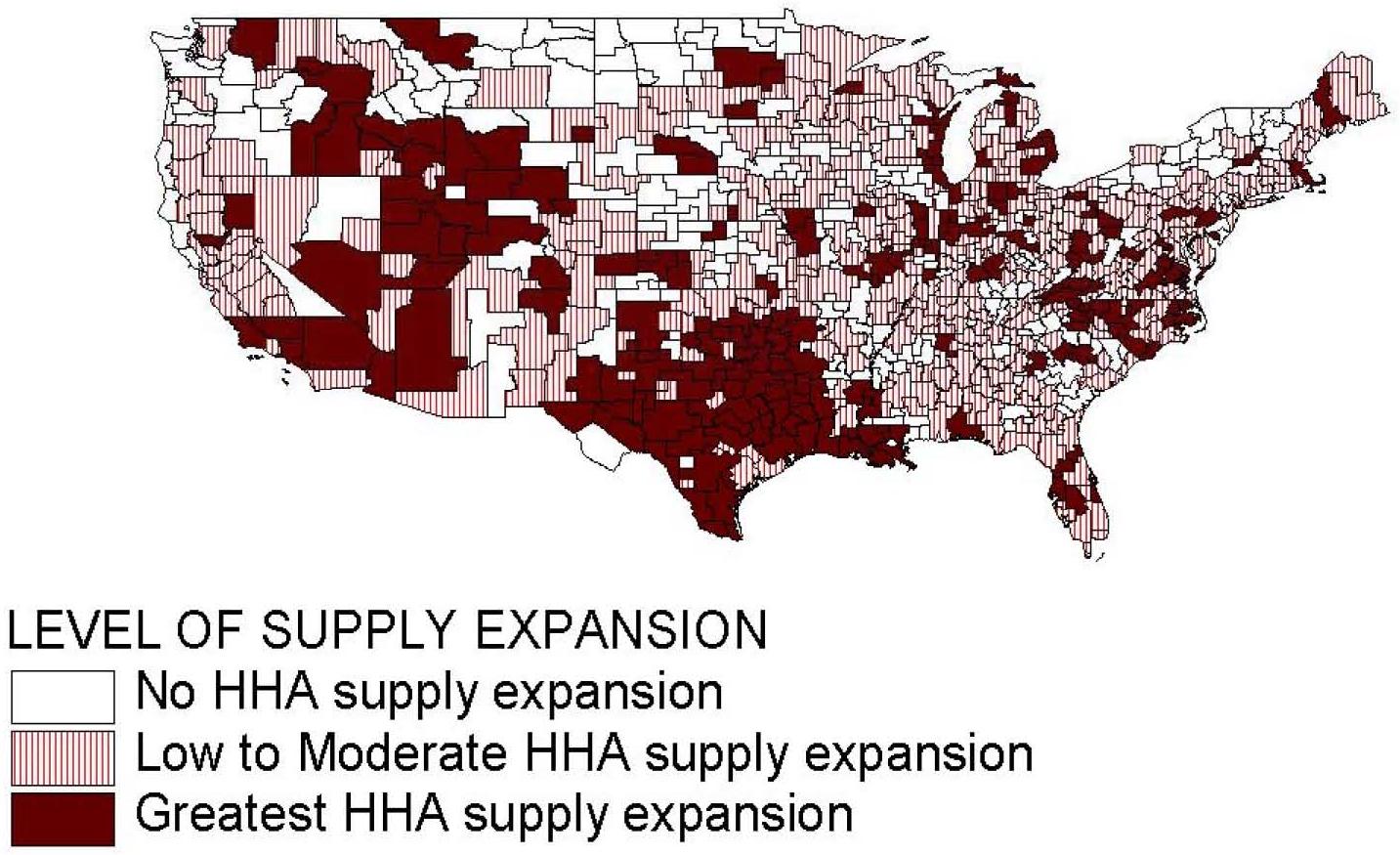

- FIGURE 5.6: Geographic Distribution of HSMAs by Level of Medicare HHA Supply Contraction

- FIGURE 5.7: Geographic Distribution of HSMAs by Level of Medicare HHA Supply Expansion

- LIST OF TABLES

- TABLE 2.1: Self-Containment of HSMAs and Counties in the Delivery of Medicare HHC Visits in 1996

- TABLE 2.2: HSMA Geographic Attributes by Category of HHA Closure Rate

- TABLE 2.3: HSMA Market Area Attributes by Category of HHA Closure Rates

- TABLE 3.1: Categories of Change in Medicare HHA Supply 1996-1999 with Selected Agency Attributes

- TABLE 3.2: Variable Definitions and Descriptive Statistics

- TABLE 3.3: Components of Change in Medicare Beneficiaries Served 1996-1999

- TABLE 3.4: Multinomial Logit Model Results for HHA Supply Decisions 1996-1999

- TABLE 4.1: Number of HHA Users per 1000 Enrollees in HSMAs, by Age and Gender, 1996-1999

- TABLE 4.2: Patterns of Medicare HHA Supply, 1996-1999

- TABLE 4.3: Comparisons of Percent of HHAs that Closed in 1996-1999 and the Corresponding Percent of Total Users They Served in 1996

- TABLE 4.4: OLS Estimates of the Effect of Closures on Change in Use Rate Between 1996 and 1999

- TABLE 4.5: Two-Stage Least Squares Estimates of the Effect of Closures on Change in Use Rate Between 1996 and 1999

- TABLE 5.1: Variable Definitions and Descriptive Statistics

- TABLE 5.2: HSMAs Cross-Classified by Levels of HHA Supply Contraction and Expansion

- TABLE 5.3: Multinomial Logit Model Empirical Results

ACKNOWLEDGEMENTS

This research report was supported by the U.S. Department of Health and Human Services, Office of the Assistant Secretary for Planning and Evaluation, under Contract No. 100-97-0010-24. The views in this report are solely those of the authors and do not necessarily represent the views of the Urban Institute, University of Massachusetts, or the U.S. Department of Health and Human Services. The authors are grateful to Kamal Hijjazi, Cille Kennedy, and Hakan Aykan who served as project officers at times during this study. Hakan Aykan provided very thoughtful and extensive comments on earlier drafts of this report. We are particularly grateful to Kamal Hijjazi for his guidance and technical assistance in the early development phases of this study.

A number of individuals contributed valuable technical assistance at various stages of the study. We thank Thy Dao for constructing the 1996-1999 files containing linked information on Medicare claims, provider characteristics, and geographic locations. Laura MacDougall and Dongsoo Lee provided technical assistance in analytic file construction and preparation of tables and figures for several of the chapters. We also thank Brian Overington for his help in preparing several chapters of this report, and Josephine Sturgis who provided clerical assistance in the preparation of the report. Any remaining errors are the responsibility of the authors.

EXECUTIVE SUMMARY

Two of the most prominent changes that took place in the home health care (HHC) delivery system over the three years following the Balanced Budget Act (BBA) of 1997 were a nearly 50% decrease in Medicares HHC expenditures and the market exit of a substantial number of home health agencies (HHAs). These changes prompted concerns from advocates and the home health industry about the potential impact of agency closures on access to home health services by Medicare beneficiaries, especially among the sickest beneficiaries and those living in rural areas.

Studies by official agencies, such as the U.S. General Accounting Office (GAO) and the U.S. Department of Health and Human Services, Office of Inspector General, examined the impact of the BBA policies on beneficiaries and providers. While documenting changes in the supply of HHAs, these studies concluded that agency closings did not cause a shortage of Medicare home health providers and that beneficiaries access to services were not generally affected. Our research builds on these prior studies, and examines, in greater detail, dynamic responses of HHAs within delineated health services market areas (HSMAs). We analyze changes between 1996 and 1999 in market entry and exit of HHAs, as well as changes in the expansion or contraction of service areas by ongoing agencies. We then relate home health utilization changes to such supply changes within HSMAs. Our aim was to address three substantive issues:

- To document changes in the structure and composition of Medicare HHC markets associated with the interim payment system (IPS);

- To develop a fuller understanding of the supply behavior (exit, entry, contraction, expansion) following the IPS;

- To identify changes in beneficiary home health utilization associated with supply changes of HHAs.

Our market area analyses of changes between 1996 and 1999 indicated that those geographic locations where agency closures were the greatest were the same ones where new agency entry or service area expansion of existing agencies was the greatest. Hence, while reports of significant agency closures portended serious HHA supply problems, potential gaps in service area coverage left by those exiting agencies were largely filled by others. Our findings that beneficiary utilization rate changes were only slightly affected by agency closures are consistent with the findings that supply of agencies was not depleted because of the closings. They are also consistent with GAOs conclusion that beneficiary access to Medicare home health services was not compromised by agency closures.

We found that certain groups of HHAs were more predisposed to exit or contract their service areas than others. Notably, higher rates of closure were associated with for-profit, freestanding, and recently certified agencies. In addition, rates of closure were considerably higher in certain regions of the country. Similar findings emerged in prior studies on the subject, but we also found that the agencies that were likely to enter market areas or expand service areas had about the same characteristics. Recently certified agencies, for example, were among the most dynamic providers. We infer from these results that such agencies were very flexible in their response to Medicare payment policies and market conditions.

Although Medicare home health use declined dramatically after the IPS, its major effect appears to be a reduction of number of visits per user, rather than reductions in the number of users per Medicare enrollee. Hence, access to Medicare HHC did not seem to be a major problem. We also found that agency closures, per se, did not greatly increase the likelihood of not obtaining any Medicare home health services. It was beyond the scope of our study, as well as prior ones, to determine if the generalized reductions in utilization following IPS resulted in negative health outcomes for Medicare enrollees. We are pretty confident, however, that agency closures were not a big part of the issue. Overall utilization reductions appeared to be due primarily to changes in payment policies, per se, and not to the intermediate factor of agency closings.

Given the dynamic behavior of the Medicare HHA industry found in this study, future research would also benefit from examining the service area expansion and contraction, as well as actual closures and openings of HHAs. Measurement of these types of activities helps to provide, for example, a fuller explanation of supply-related effects on beneficiary utilization and access to services. A natural application of this framework may be an examination of the impact of changes after Medicare started paying for home health services under a prospective payment system in 2000.

1. BACKGROUND AND OUTLINE OF THE REPORT

1.1. Introduction

During the three years following the Balanced Budget Act (BBA) of 1997, significant changes took place in the home health care (HHC) delivery system. Two of the most prominent changes were the drop in Medicares HHC expenditures by nearly 50% and the market exit of a substantial number of home health agencies (HHAs). These changes prompted concerns from advocates and the home health industry about the potential impact of agency closures on access to home health services by Medicare beneficiaries, especially among the sickest beneficiaries and those living in rural areas.

Studies by official agencies, such as the U.S. General Accounting Office (GAO) and the U.S. Department of Health and Human Services (HHS), Office of Inspector General (OIG), examined the impact of the BBA policies on beneficiaries and providers. While documenting changes in the supply of HHAs, these studies concluded that agency closings did not cause a shortage of Medicare home health providers and that beneficiaries access to services were not generally affected.

Because of the policy urgency of the perceived effects of the HHA closures, nearly all of the studies were short-term, had limited scopes of work, or covered few geographic entities. Our research builds on these prior studies, and examines, in greater detail, dynamic responses of HHAs within delineated health services market areas (HSMAs).1 We analyze changes between 1996 and 1999 in market entry and exit of HHAs, as well as changes in the expansion or contraction of service areas by ongoing agencies. We then relate home health utilization changes to such supply changes within HSMAs. Our aim was to address three substantive issues:

- To document changes in the structure and composition of Medicare HHC markets associated with the interim payment system (IPS);

- To develop a fuller understanding of the supply behavior (exit, entry, contraction, expansion) following the IPS;

- To identify changes in beneficiary home health utilization associated with supply changes of HHAs.

The next section of this chapter presents background information on the Medicare home health benefit, trends in spending and use leading up to the 1997 BBA, home health policies in the BBA, and impact of those policies on providers and utilization rates. In subsequent chapters of this report, we deal more deeply with patterns of HHA closures, market expansion and contraction, as well as provide a unique and thorough analysis of market supply responses--and potential changes in utilization that resulted--using HSMAs as the units of observation. We wrap things up by discussing the potential implications of our findings for policy and research.

1.2. Background

A. Medicare Home Health Benefit

Medicare finances home health services for enrollees who require intermittent or part-time skilled nursing care and therapy services, and who are homebound. These services must be prescribed, (and re-certified every 62 days), by a physician. There is no prior hospitalization requirement or limit on the number of visits a person may receive. Nor is there a co-payment for Medicare home health visits under Medicares Part A hospital insurance program. Although the Medicare home health benefit was originally conceived to be a post-hospital extended care service, it evolved during the 1980s into more general home-based care for individuals requiring nursing or rehabilitative care. Despite the broadening of the benefits intent, Medicare spending for home health grew only modestly during this period, in large part because of relatively strict, and inconsistent, interpretation by Medicare fiscal intermediaries of coverage and eligibility rules. In 1988, however, a class-action lawsuit against HHS (Duggan v. Bowen 1988), which administers the Medicare program, resulted in a liberalization of coverage and eligibility standards. New guidelines provided more explicit definitions of when patients' conditions constituted need for intermittent skilled nursing care. In addition, they provided that need for skilled management and evaluation (not necessarily along with skilled nursing care) would qualify an individual for the benefit, and that care needs could be chronic rather than progressively improving. These revisions expanded the number of beneficiaries eligible for home health services.

B. Rapid Growth in Medicare Home Health Spending

After the Duggan v. Bowen case, spending on Medicares home health benefit grew rapidly. Between 1988 and 1997, spending increased an average of 28.2% annually, from $1.9 billion to $17.8 billion (GAO 1999; Health Care Financing Administration (HCFA) 1998). This growth has been attributed primarily to application of the new guidelines (Bishop, Kerwin & Wollack 1999; McCall, Komisar, Petersons & Moore 2001; GAO 1998), including some states Medicare maximization policies that fostered coverage of some of the long-term care (LTC) costs of beneficiaries eligible for both Medicare and Medicaid (GAO 1998).

Growth in spending during this period reflected dramatic increases in utilization, both in terms of the number of beneficiaries receiving services and the amount of care they received. Between 1988 and 1997, the number of beneficiaries receiving Medicare HHC increased by 225% (from 1.6 million to 3.6 million), while visits per user increased by 343% (from 23 to 79 visits per user).

C. 1997 Balanced Budget Act HHA Provisions

Concerned about the rapid growth in home health expenditures, Congress mandated in the BBA of 1997 that Medicare HHAs be paid through a prospective payment system (PPS; implemented eventually in October 2000). Recognizing that the development of a PPS for HHAs would take considerable time, Congress also mandated that an IPS be imposed immediately to slow expenditure growth. Centers for Medicare and Medicaid Services (CMS) began phasing in the IPS as early as October 1997 depending on an HHAs cost reporting year. The BBA also tightened eligibility rules for the home health benefit by clarifying the definition of intermittent skilled nursing care and excluded venipuncture (blood drawing) as a sole qualification for home health services.

The IPS established lower per-visit payment limits, as well as a per-beneficiary limit on HHAs. The per-visit limits were reduced from 112% of the national mean cost per-visit to 105% of the national median cost per-visit. The per-beneficiary payment limit was calculated by summing 75% of an agencys costs per beneficiary and 25% of the average cost per beneficiary for agencies in its census region. The per-beneficiary limit is calculated differently for agencies participating in Medicare for at least a full year by October 1, 1994 and for newer agencies (GAO 1998). Of the various provisions of the IPS, the per-beneficiary limit was expected to reduce payments the most severely.

Revisions to the IPS by Congress in October 1998 increased payments to HHAs by upping the per-visit limit to 106% of median per-visit costs, and changing the per-beneficiary limits for HHAs depending on their cost reporting year. In general, HHAs established prior to 1994 that had annual costs lower than the national median received an incremental payment, HHAs entering the program between 1994 and 1998 were limited to 100% of national costs, and new HHAs (i.e., those entering the market in 1999 or after) were subject to per-beneficiary limits set at 75% of national costs. These revisions were designed, in part, to prevent new HHAs from being able to gain reimbursement advantages over existing HHAs (National Health Policy Forum 1999).

D. Impact of the IPS on Spending, Provider Supply, and Utilization

After the IPS was implemented, total Medicare home health spending decreased by over 50% (from around $16.4 billion to around $7.8 billion), and per-user spending decreased by 37%. As a result of the dramatic decline in spending, the Congressional Budget Office (CBO) in March 1999 revised its pre-BBA projections of home health savings by a factor of four, projecting that the BBA would reduce Medicare home health outlays by $64 billion through 2002 (CBO 1999 as cited in Bishop, Kerwin & Wallack 1999).

Changes in HHA Supply After the IPS. Coincident with the dramatic reduction in Medicare expenditures following the IPS, a large number of HHAs exited the Medicare program, likely because the new payments were insufficient to meet their costs or, perhaps, profit expectations. Nationally, 26% of the HHAs, participating in Medicare in 1996, were no longer participating in the program by 1999. The net decline in participating Medicare HHAs between 1996 and 1999 was only 15%, however, because other agencies started providing Medicare home health services after 1996.

Changes in the supply of HHAs after the IPS varied widely with respect to agency characteristics and geographic location. For example, between 1996 and 1999, proprietary HHAs had the greatest net decline (-21%), while both non-profit and government agencies had much smaller declines (about 7% each). HHAs in the largest metropolitan areas were also more likely to exit the Medicare program; 30% of such HHAs dropped out between 1996 and 1999. Because metropolitan areas, relative to less populated areas, may have had an abundant supply of HHAs, beneficiaries needs resulting from the closure of some agencies could be met by ongoing ones. In contrast, where relatively few agencies were available, for example in rural areas, community needs could have made it more difficult for HHAs to close.

The closures of so many HHAs after the IPS prompted short-term policy studies by GAO (1998, 1999) and HHS/OIG (2000). GAO found that, despite the high HHA closure rate, the number of Medicare participating agencies in 1999 was still substantial due to the rapid growth of agencies between 1990 and 1997 (GAO 1999). GAO also found that agencies that stopped participating in Medicare were distinctive in their regional and provider characteristics. Approximately 40% of the agencies that closed were located in three states (i.e., Louisiana, Oklahoma, and Texas), which were among those with the highest recent growth in number of agencies. Consistent with this trend, many agencies that closed were among those with fewer than five years of participation in Medicare. Relative to agencies that continued to participate in Medicare after the IPS, agencies that closed were also more likely to have been of proprietary ownership, located in urban areas, freestanding, and served lower than average numbers of patients.

In its study, GAO (1998) also made the important distinction between agency closures and agency branch closures. Under Medicare rules, HHA branches are not considered independent providers. Rather, they are integral parts of the parent agency. As such, branches are not individually surveyed or certified for Medicare compliance, and are not required to file a unique Medicare cost report. In general, it was often financially advantageous for an HHA to have the parent unit based in an urban locale (with higher wage index and reimbursement), while branches provided services in areas with lower wage indices. The distinction between agency and branch closures was reiterated after the home health industry reported numbers of agency closures that were substantially higher than those calculated by GAO.

E. Changes in Medicare Home Health Use After the IPS

Consistent with spending decline after the IPS, Medicare home health services utilization declined between 1996 and 1999. County-level Medicare home health use rates declined by 29%, on average, between 1996 and 1999 (Liu, Wissoker, Porell & Overington 2003). This change reflects a substantial drop in the use rate from 104 per 1000 enrollees in 1996 to 72 per 1000 enrollees in 1999.

Changes in the use rates between 1996 and 1999 were about the same for various demographic groups by age, gender and race. While changes in use rates varied only slightly by urban and rural location, regional differences in beneficiary utilization rate changes were considerable. For example, where use rates declined by about 20% in the Mid-Atlantic and Pacific regions, the decline was 37% in the West South Central region and 32% in the East South Central region, two regions that had the highest use rates in 1996.

Although users per agency declined only modestly, the number of visits per user declined dramatically from 79 visits per user in 1996 to 38 visits per user in 1999. Visits per user declined more among proprietary HHAs (54%) than among voluntary and government agencies, both of which averaged declines of about 42%. Virtually no difference in average visits per users was found by urban/rural status. By region, the smallest decline in visits per user was 32% in the Mid-Atlantic region (e.g., New York, Pennsylvania), while the largest percent decline was found in the West South Central region (e.g., Texas, Oklahoma). In general, the greater the number of average visits provided by agencies in a region before the BBA, the greater was the decline in number of visits after the BBA. This type of response would be expected in light of the per-beneficiary cost limit imposed by the IPS.

F. IPS Effects on Sub-groups of Beneficiaries

The dramatic decrease in utilization after IPS raised the question of whether access for sub-groups of beneficiaries would be affected. Special concerns were expressed for rural communities, which may have fewer alternatives, and for beneficiaries with chronic illness that often incur costs higher than the caps that were imposed under IPS (Smith & Rosenbaum 1998; Komisar & Feder 1998).

McCall, Petersons, Moore & Korb (2003) compared the characteristics of home health users and non-users, as well as the utilization of home health services, between 1997 and 1999. They found that home health users were very similar for both years and only small significant differences existed with respect to demographics, geographic region and supply of county-level acute and post-acute resources. A notable difference was that post-BBA users were more likely to be disabled and have prior hospital care. They also found slightly greater reductions in use among beneficiaries age 85 and over, living in states with high historical Medicare home health use, and in states with Medicaid buy-in.

McCall et al., (2003) also found different patterns of service provision across the six home health service disciplines. Specifically, home health aide visits decreased by 54%, medical social worker visits decreased by 38%, skilled nursing visits decreased by 29%, occupational therapy visits decreased by 20%, and physical therapy visits decreased by 7%. In contrast, only speech-language pathologist visits increased by 6%.

G. HHA Closures and Beneficiary Access

A key focus of GAOs (1998, 1999) studies was the relationship between HHA closures and beneficiary access. For those studies, the GAO examined HHA certification status and beneficiary utilization information from Medicare administrative records, and conducted interviews with stakeholders, including hospital discharge planners, consumer advocates, state agency officials, and HHA representatives.

Although GAO found a high (14%) closure rate of Medicare participating HHAs after implementation of the IPS in October 1997, it did not conclude that the reduced capacity would be a threat to beneficiary access to the benefit, largely because of the very rapid growth in the number of agencies leading up to 1997.2 GAO found large declines in both rates of beneficiary use and number of visits among users after IPS was implemented. In addition, while the IPS narrowed variations in use among counties, substantial variation continued to exist. Despite the utilization changes, interviews with hundreds of stakeholders indicated that, in general, Medicare beneficiary access to home health services was not greatly affected by the agency closures. Some providers indicated, however, that individuals with greater needs (e.g., diabetics, wound care patients, individuals with Alzheimers disease) required a greater effort to be placed. Similarly, Smith, Maloy & Hawkins (1999, 2000) found that the sickest home health beneficiaries were more likely to experience more limited access.

OIG (2000) also found suggestions that some hospital discharge planners were experiencing placement difficulties for potential home health beneficiaries on occasion as a result of process oriented changes in HHAs since the implementation of the IPS, including stricter Medicare home care eligibility criteria and enforcement, an apparent closer preadmission scrutiny of potential patients medical conditions, fewer HHAs in certain geographic areas, and HHA staffing shortages. In sum, these studies on beneficiary access suggested that closure of HHAs after the IPS was implemented did not generally affect access to the Medicare home health benefit.

1.3. Outline of the Report

In this chapter we have provided background information on the Medicare home health benefit, home health policies in the BBA, and a summary of the findings of past research regarding the impact of those policies on providers and utilization rates. The outline of the remainder of the report is as follows. Chapter 2 contains a descriptive analysis of geographic patterns of HHA closures between 1996 and 1999. Unlike prior studies, we created and analyzed HSMAs as the geographic units of observation. In Chapter 3 we consider two other forms of HHA supply response to the Medicare IPS aside from agency closure, namely, the contraction or expansion of an agencys geographic service area. We estimate the magnitude of HHA supply response with changes in HHAs geographic service areas, and report the findings of an empirical analysis of agency and market area factors influencing the various supply decisions of individual agencies. In Chapter 4 we examine potential utilization impacts associated with changes in the supply of HHAs. We report the findings of an empirical analysis of Medicare HHC utilization rate changes associated with changes in the supply of HHAs between 1996 and 1999. This is followed in Chapter 5 by an empirical investigation whether those market areas where substantial reductions in HHA supply occurred as a consequence of agency closures and geographic service area contractions also experienced substantial HHA supply expansion as a consequence of market entry and service area expansion by other agencies. In the final section, we discuss the implications of our findings for policy and research.

2. HHA CLOSURE RATES AMONG GEOGRAPHIC MARKET AREAS: 1996-1999

2.1. Introduction

This chapter describes the geographic pattern of Medicare HHA closures that followed implementation of the Medicare IPS and examines characteristics that distinguish market areas with higher versus lower rates of agency closures between 1996 and 1999. Its purpose is to provide an empirical context for the three empirical analysis chapters that follow. Since changes in Medicare HHA supply that occurred after IPS implementation are the main focus of this study geographic market areas should be properly delineated to approximate the concept of an economic market. As one researcher investigating patients hospital admission choices asserted, "If we want to be sure we capture the full extent of consumer behavior within local markets, we must address the issue of what constitutes a market" (Dranove, White & Wu1993). This point is probably equally, if not more important for the study of the supply behavior of HHAs the impacts of this supply behavior upon beneficiary access to the Medicare HHC benefit.

GAOs (1999) study of the geographic distribution of HHA closures that followed implementation of the IPS employed counties as geographic units. There are extreme variations in the land area and population sizes of counties (Porell, Tompkins & Turner 1990). San Bernadino County, California with a land area of 20,064 square miles is larger than the area of seven of the states in the United States. In contrast, the independent city of Emporia, Virginia is a county spanning little more than two square miles, with a population of less than 5,000 in 1990. Whereas the entire Metropolitan Statistical Area (MSA) of Los Angeles is comprised of a single county with a population exceeding seven million persons, 18 different counties, with a combined population about 1/3 of Los Angeles county, comprise the MSA of Atlanta, Georgia. Given the political origins of counties as jurisdictional units, there is little reason to expect that county geographic boundaries will coincide with what one might think of as a health care market area. Accordingly, we address the concept of geographic market area and the geographic units employed as markets before examining geographic patterns and market characteristics associated with HHA closures between 1996 and 1999.

2.2. Data and Methodology

A. Data Sources

The major sources of data used in this study are Medicare administrative records maintained by CMS. They include 1996 and 1999 Medicare HHA claims, Medicare's enrollment files, and data from the Online Survey, Certification and Reporting (OSCAR) system. We also use variables from the 2000 Area Resource File (ARF).

Medicare HHA claims data include information on number of visits, by specialty, age and gender, and diagnoses of users. The year 1996 is the latest full calendar year preceding implementation of the IPS on October 1, 1997. The year 1999 was the most recent full calendar year of claims data available at the start of the study. It precedes the implementation of the Medicare HHC PPS that occurred in October 2000. Medicare enrollment data provided denominator information for the construction of utilization rates.

The OSCAR system provides information from the state survey and certification process to identify and characterize providers that participate in Medicare and Medicaid. Medicare Provider of Service (POS) files derived from the OSCAR system provide information on ownership, geographic location, certification dates of Medicare providers, the number of employees of various types (for example, inhalation therapists, occupational therapists, and physical therapists) and the number of different types of beds and care units, and other attributes of HHAs participating in Medicare.

We derived a number of variables characterizing the HHAs and the market areas they are located. With data from the OSCAR, we derived source variables on control of ownership (e.g., proprietary, non-profit), hospital-based affiliation, dates of participation in Medicare, and geographic location. OSCAR data on staffing enabled us to construct various measures of staffing, by type of staff (e.g., nurses, physical therapists). The ARF files provided information on geographic characteristics of the HHAs, such as whether they were located in metropolitan areas, non-metropolitan urban areas, or rural areas. ARF also provided information on other providers in the area such as hospitals. We used Medicare claims and enrollment data to measure utilization rates and amounts of HHA visits recorded in 1996 and 1999.

B. Geographic Market Areas

Geographic supply analyses should employ geographic units that approximate the economic concept of a geographic market area. Distinct geographic market areas have long been defined to exist when supply and demand forces outside the geographic area are small relative to those within (i.e., when the geographic market is self-contained). Using their shipments approach, Elzinga and Hogarty (1973) describe a geographic market area as being selfcontained when producers within that market area export few goods out of the area (i.e., little outside from inside), and consumers within that market area import few goods into the area (i.e., little inside from outside).

The greater is the prevalence of border-crossing among counties in the delivery of HHC visits, the more difficult it is not only to reliably identify the beneficiary population potentially affected by HHA closures, but also to assess potential mediating effects of supply response behavior of agencies that did not close. Based on the concept of an economic market area, our study draws upon the work of Makuc, Haglund, Ingram, Kleinman & Feldman (1991) in which the authors measured shipments with 1988 county-to-county patient origin hospital data for Medicare beneficiaries. The authors define a population import of hospital services to be a hospital admission of a local resident to a hospital located outside of that residents geographic market area, and a supplier export of services as a hospital admission of a non-resident a hospital based inside the market area. Employing an explicit objective of minimizing imports and exports of hospital services, statistical cluster analysis techniques were used to identify some 800 HSMAs in the United States as clusters containing at least one county.

This study uses HSMAs as the geographic unit of analysis to assess Medicare HHA supply change associated with agency closures from 1996 through 1999. Although the HSMAs of Makuc et al. (1991) were delineated using data on Medicare inpatient hospital admissions rather HHC visits, patient origin Medicare HHC visit data for 1996 suggest that HSMAs are also much more self-contained for counties for HHA visits. The top portion of Table 2.1 displays the respective distributions of county and HSMAs among categories defined by the percentage of total 1996 visits to resident Medicare HHC users made by HHAs based in the same market area. In nearly 85% of HSMAs, local HHAs delivered 75% or more of the total volume of Medicare HHC visits received by beneficiary residents in 1996. In contrast, in 1996 local agencies delivered at least 75% of total Medicare HHC visits received by beneficiary residents for only 22% of counties. When geographic areas are weighted to reflect differences in the relative volume of visits among geographic market areas, HSMA-county differences are even more striking. The bottom portion of Table 2.1 contains data about the degree to which HHAs based in a market area serve local resident beneficiaries. When HSMAs rather than counties are used to delineate market areas, a much higher percentage of total visits delivered by HHAs based in a market area are delivered to local residents of that same market area. In nearly 73% of HSMAs local beneficiary residents received 75% or more of total visits delivered in 1996 by HHAs based in the HSMA. In contrast, in only 56% of counties did local beneficiaries accounted for three-quarters of the visits by HHAs based in the county. When differences in HHA visit volumes are accounted for with relative weights, again the HSMA-county differences are accentuated. Finally, we consider the prevalence of geographic market areas served entirely by HHAs based in other market areas. In 1996 there were more than 700 counties in the United States with resident Medicare beneficiaries (of a total of about 3,080 counties) with no HHAs based within their boundaries. Whereas nearly a quarter of counties (i.e., 23%) had no HHAs in 1996, there were no HHAs based in only about 2% of HSMAs (i.e., 13 out of 803).

The HSMAs developed by Makuc et al. (1991) were developed to represent economic health care markets due to their explicit objective of minimizing border-crossing by beneficiaries for hospital care. Given the high prevalence of HHC episodes initiated by hospital stays, market areas derived from Medicare hospital patient origin data are likely to correspond well with Medicare HHC delivery patterns. This assertion is supported by a comparison of county and HSMA market areas with respect to agency border-crossing in the delivery of Medicare HHC visits. This comparison showed that HSMAs are much more self-contained than counties for Medicare HHC services. In other words, the local nature of the supply of and demand for Medicares home health benefit is more profound when assessed for market areas defined as HSMAs than for counties. As such, HSMAs represent an attractive alternative to counties for analysis of Medicare HHA supply changes.

C. Definition of HHA Closure

In order to identify Medicare HHAs that closed between 1996 and 1999 it was first necessary to adopt a definition of what constitutes an active HHA. To estimate the number of HHAs that were "active" in the Medicare program in 1996 and 1999, we examined information from the OSCAR and the claims. While the OSCAR provides information on "termination dates" we discovered some inconsistencies between whether an agency was considered active by OSCAR, and whether we located Medicare claims for the year. Hence, for the purpose of identifying HHA closures, we decided to designate agencies as active in 1996 and in 1999 based on whether Medicare claims were recorded for each of the given years.

In the descriptive analysis of HHA closures that follows in this chapter, agency closures are defined simply in terms of the presence of Medicare claims for an agency in 1996 and or 1999.3 That is, HHAs with Medicare claims in 1996 but not in 1999 are defined as agencies that closed.

D. Market Area HHA Closure Rates

To assess geographic concentration of HHA closures between 1996 and 1999, we computed unweighted HHA closures rates for HSMAs. Each active HHA was based in an HSMA in 1996 using the agencys five-digit zip code recorded in the Medicare POS file. The unweighted HHA closure rate is simply the number of HHAs that were active in 1996 but not in 1999 in an HSMA as a percentage of the total number of active HHAs based in the HSMA in 1996.4 Using this convention, we then defined four categories of HHA closure rates based on the quartiles of the distribution of HHA closure rates among the 790 HSMAs with at least one HHA in 1996. Since the 330 HSMAs with no HHA closures between 1996 and 1999 account for more than 25% of HSMAs, all of these HSMAs were assigned to the lowest quartile category of No Closures. The remaining three categories are based on the remaining quartile values of the HSMA distribution and are described as: Lower Closure Rate (i.e., HSMAs with a positive HHA closure rate less than or equal to 14.3%); Moderate Closure Rate (i.e., HSMAs with an HHA closure rate greater than 14.3% but less than or equal to 30%), and Higher Closure Rate (i.e., HSAs with an HHA closure rate greater than 30%).

2.3. Empirical Results

A. Geographic Patterns of HHA Closure Rates

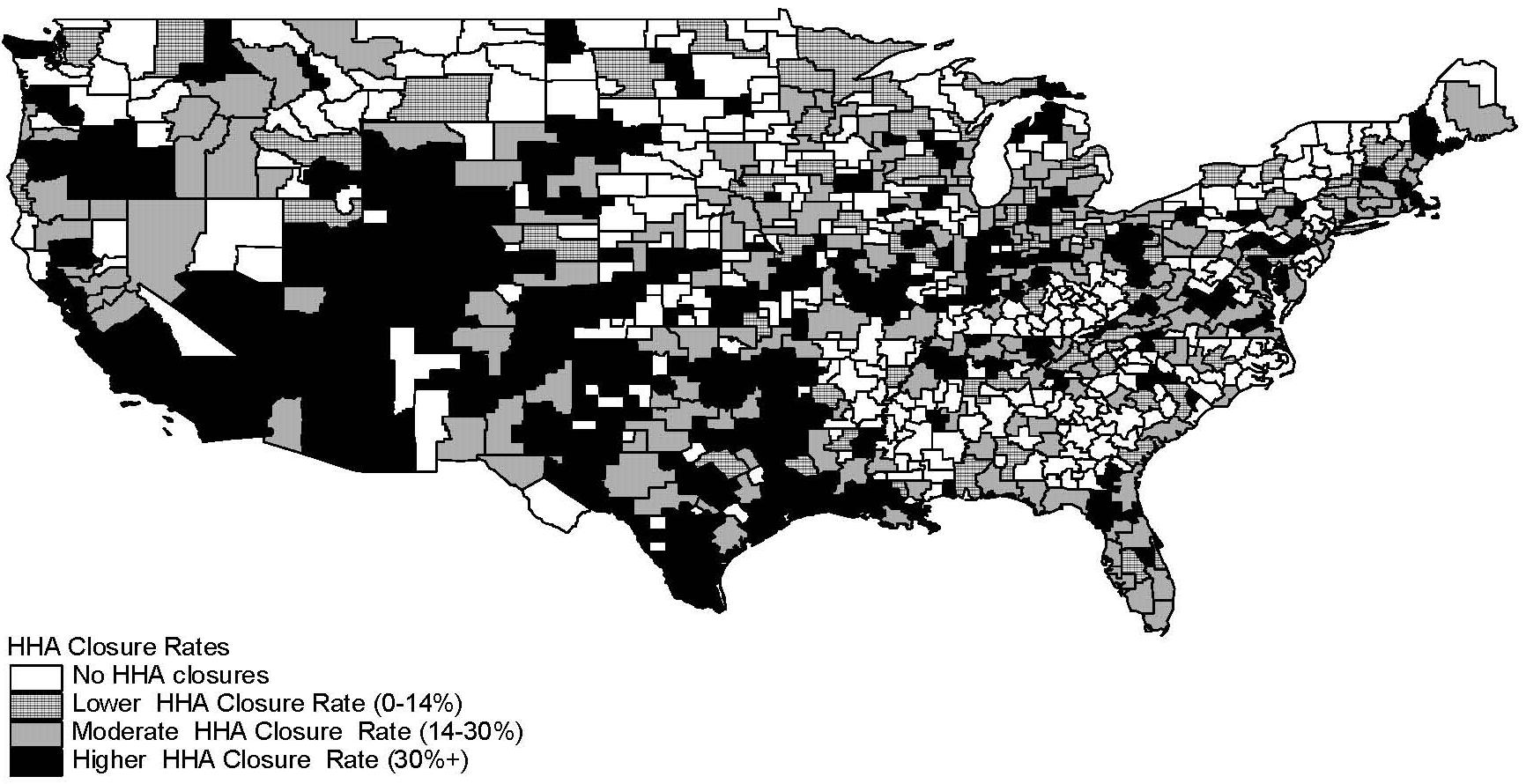

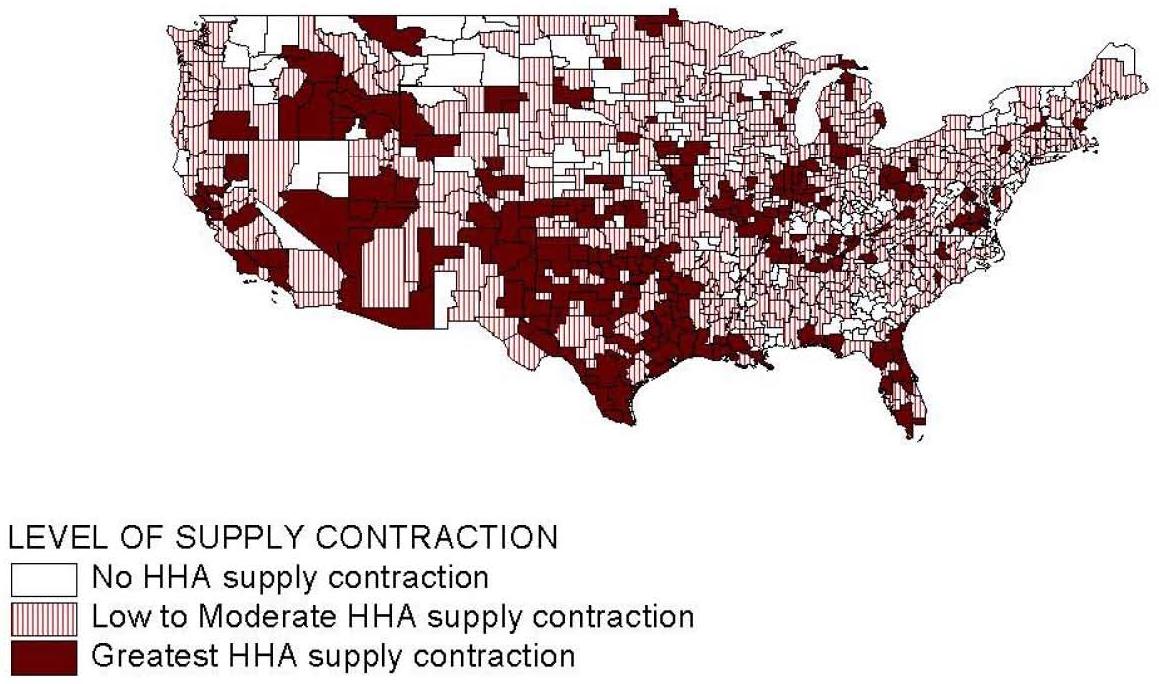

Figure 2.1 contains a map displaying the geographic distribution of HSMAs with different HHA closure rates. HSMAs with moderate or higher closure rates seem to be much more prevalent in the south central, mountain, and western areas of the United States HSMAs with none or lower agency closure rates appear to be a little more concentrated in the northeast and north central areas of the country.

Geographic variables describing system patterns in agency closure rates among HSMAs are reported in Table 2.2. The geographic patterns indicated on the map in Figure 2.1 are reflected in differing distributions of HSMAs among Census divisions when HSMAs are stratified by closure rate category. Relative to other closure categories, HSMAs with the highest agency closure rates are clearly over-represented in the West South Central, Mountain and West Census divisions.

Interestingly, other data reported in Table 2.2 suggests that HSMAs where no closures occurred are very different from all other HSMAs with respect to population size and metropolitanization. HSMAs with no closures, on average, had a markedly smaller 1996 populations (145,077) than all other HSMAs. The average population size of HSMAs where relatively few closures occurred (500,788) modestly exceeded that of HSMAs with the highest closure rates (458,938). With the exception of HSMAs with no closures, HSMA agency closure rates tend to vary inversely with the percentage of HSMA population living in a metropolitan area. This pattern lies in stark contrast to nonmetropolitan character of HSMAs with no closures, where only around 21% of total population was living in a metropolitan county in 1996.

B. Characteristics of HSMAs Associated with HHA Closure Rates

Aside from their geographic concentration in the Southwestern United States and population differences, HSMAs with high prevalence rate of agency closures are likely to differ from HSMAs with lower or no agency closures in ways that provide some insights into factors contributing to HHA market exits. Table 2.3 contains sample means for a series of variables describing agency composition, market area, Medicare HHA service use, and HHA supply attributes for HSMAs comprising each of the four closure rate groups defined above.

Agency Composition. Table 2.3 shows HHA closure rates among HSMAs vary with HSMA agency composition with respect to tenure of Medicare program participation. For example, the average number of years of HHA Medicare participation in all HSMAs in 1996 was around 11.4 years. However, successively higher closure rates are found in HSMAs served by agencies with fewer average years of Medicare participation. HSMAs with no closures were served by HHAs with an average of about 14 years of Medicare tenure in 1996. HSMAs with lower and moderate closure rates were served by HHAs with an average of 12 years and ten years tenure in 1996, respectively. Finally, HSAs with higher closure rates were served by HHAs with an average of only eight years of Medicare tenure. In particular, HHAs with less than five years of Medicare participation tenure appear to be at higher risk of closure. A greater percentage of the HHAs based in HSMAs with higher closure rates had less than five years of Medicare program tenure than in HSMAs with lower closure rates or no closures.

When considering an HHAs proprietary status with respect to closures, the data in Table 2.3 suggest that for-profit HHAs were at greater risk of closure than other forms of ownership. For example, for-profit HHAs comprised greater than 50% of agencies based in HSMAs with the highest closure rates. In stark contrast, on average less than 20% of HHAs in HSMAs with no closures were for-profit agencies. For-profit agencies clearly comprise a successively increasing percentage of HHAs that were based in HSMAs in the low, moderate and higher closure rate categories.

An HHAs organizational setting seemed to have a less consistent association with closures. Table 2.3 breaks out the composition of hospital-based vs. freestanding agencies in HSMAs with different closure rates. Overall, HSMAs with a greater percentage of freestanding HHAs appear to have higher closure rates, but this association did not appear to trend as clearly or consistently as with proprietary status. Among HSMAs where there were no closures, hospital-based and freestanding HHAs were roughly equally represented, each comprising nearly 50% of all HHAs on average. However, in HSMAs for all other closure categories freestanding HHAs outnumbered hospital-based HHAs ranging from about 62% of HHAs in the moderate closure rate sub-group to a high of nearly 70% of HHAs among HSMAs with the highest closure rates.

Market Competition Attributes. In what might be considered a reflection of the degree of HHA market saturation in an HSMA, the data in Table 2.3 suggest that HSMAs with greater numbers of HHAs experienced successively higher rates of agency closures. For example, on average, it appears that HSMAs with the highest closure rates were served by over five times as many HHAs as HSMAs where no closures occurred (22.5% vs. 4.2 %, respectively). Table 2.3 also shows how HSMA markets broke out according to their market concentration, which was measured via a Herfindel index. This index represents the extent to which the supply of the Medicare home health benefit in 1996 was controlled by a relatively small number of HHAs based in the HSMA. As might be expected, there were no HHA closures in HSMAs where the supply of the Medicare home health benefit was dominated by relatively few HHAs, as evidenced by a higher average Herfindel index (0.51). However, and perhaps contrary to what might be expected, an inverse relationship was observed between the average Herfindel indices among HSMAs in the other closure rate categories. Note that HSMAs experiencing the highest rate of closures scored a higher average Herfindel index compared to HSMAs in both the moderate and low closure rate categories (0.28, 0.23 and 0.21, respectively).

Medicare HHA Service Use. Overall, HHAs provided an average of around 28,200 visits to Medicare annually in 1996. Average annual visits per HHA in 1996 were higher in HSMAs experiencing successively lower closure rates, ranging from around 20,200 visits per year in HSMAs in higher closure rate category to around 32,800 visits per year in HSMAs where no closures occurred. HHAs based in HSMAs with higher closure rates appear to exhibit more visit-intensive practice styles than HHAs based in other market areas. Agencies based in HSMAs with the highest closure rates provided 77 visits per beneficiary served, on average, in 1996 compared to the lower visit rates per beneficiary (ranging from 66 to 60 annual visits per beneficiary) of HHAs in HSMAs with lower closure rates.

Medicare HHA and Nursing Home Bed Supply. The data in Table 2.3 suggest that HSMAs with the highest closure rates had nearly double the supply of HHAs per beneficiary (6.3 HHAs/10,000 beneficiaries) compared all other HSMAs (3.6, 2.8, and 3.5 HHAs/10,000 beneficiaries for HHAs in the moderate closure rate, lower closure rate, and no closure categories, respectively). A similar pattern is evident in the HHA staffing level data. HSMAs with the highest closure rates also had more full-time registered nurses (RNs) and nurse aides on average per resident Medicare beneficiary in 1996 than HSMAs with lower closure rates or no closures. Since these HSMAs also had a greater supply of Medicare-certified nursing home beds (56.7) per older Medicare beneficiary (i.e., 75 years old and over) compared to all other closure rate groups in 1996, these data suggest that LTC and post-acute care (PAC) supply was relatively abundent in the HSMAs with the highest HHA closure rates.

2.4. Discussion

This descriptive analysis of differences among HSMAs with varying agency closure rates between 1996 and 1999 suggest that HSMAs with the highest closure rates exhibit some very distinctive characteristics. Foremost these HSMAs were highly concentrated in the South Central, Mountain, and Western Census divisions of the United States. These HSMAs tended to be less populated and had greater shares of non-metropolitan population than all other HSMAs except those where no agency closures occurred. HSMAs where no closures occurred were generally comprised of the least populated non-metropolitan counties.

HSMAs with higher agency closure rates differed rather markedly from other HSMAs with respect to the composition of agencies serving the HSMA in 1996. For-profit agencies, freestanding agencies, and agencies that only recently obtained Medicare certification all comprised a much greater share of the agencies based in HSMAs with the highest closure rates. Furthermore, HHA provider supply in HSMAs with the highest closure rates was considerably greater, as reflected by the number of agencies, RN staff, and HHA staff per resident Medicare beneficiary than in other HSMAs. Finally, agencies based in HSMAs with the greatest closure rates also appear to exhibit more visit-intensive practice styles, as reflected by higher rates of visits per beneficiary served than agencies based elsewhere.

Overall, HSMAs with the highest agency closure rates between 1996 and 1999 appear to be market areas where Medicare HHA supply was likely saturated by recent market entries of smaller, for-profit agencies exhibiting more visit-intensive practice styles. While these characteristics are suggestive of excess supply in these HSMAs, such a conclusion is premature without additional corroborating empirical evidence indicating that access to Medicare HHC services has not been impaired in these market areas. Furthermore, it is not immediately evident that agency closures tell the entire story of HHA supply response after IPS implementation. These descriptive analyses have not considered other ways that agencies may have reduced Medicare HHA supply. Agency closures may understate the agency supply contraction that followed IPS implementation if substantial numbers of agencies that remained open discontinued serving Medicare beneficiaries in portions of their geographic service areas. Some agencies may have also expanded Medicare HHA supply through new market entry, while others may have initiated service delivery in areas, thus expanding their geographic service areas. In the next chapter, we investigate the magnitude of these other forms of Medicare HHA supply response after the IPS, as well as agency and market area attributes associated with the supply responses of individual agencies.

| FIGURE 2.1: Prevalence Rates of HHA Closures among HSMAs |

|

| TABLE 2.1: Self-Containment of HSMAs and Counties in the Delivery of Medicare HHC Visits in 1996 | ||||

| % Visits from Local HHAs | Unweighted Geographic Units | Geographic Units Weighted by 1996 HHA Visits | ||

| % of Counties | % of HSMAs | % of Weighted Counties | % of Weighted HSMAs | |

| A. Distributions of the Percentage of Visits to Resident Beneficiaries Made by HHAs Based in the Same County or HSMA | ||||

| 0% - 9.99% | 27.08 | 3.05 | 4.01 | 0.19 |

| 10.0% - 24.99% | 5.81 | 2.28 | 2.46 | 0.29 |

| 25.0% - 49.99% | 16.99 | 10.28 | 7.77 | 2.61 |

| 50.0% - 74.99% | 21.55 | 26.78 | 63.41 | 12.25 |

| 75.0% - 89.99% | 16.74 | 36.80 | 13.03 | 72.73 |

| 90.0% - 100.0% | 11.82 | 20.81 | 9.32 | 11.92 |

| TOTAL | 100 | 100 | 100 | 100 |

| B. Distributions of the Percentage of Visits by HHAs Based in a County or HSMA Made to Resident Beneficiaries | ||||

| 0% - 9.99% | 0.76 | 2.84 | 0.20 | 0.06 |

| 10.0% - 24.99% | 3.50 | 0.39 | 3.02 | 0.06 |

| 25.0% - 49.99% | 14.86 | 5.54 | 10.71 | 2.52 |

| 50.0% - 74.99% | 25.07 | 18.68 | 67.06 | 12.47 |

| 75.0% - 89.99% | 28.92 | 34.15 | 13.65 | 69.77 |

| 90.0% - 100.0% | 26.89 | 38.40 | 5.36 | 15.12 |

| TOTAL | 100 | 100 | 100 | 100 |

| TABLE 2.2: HSMA Geographic Attributes by Category of HHA Closure Rate (1996-1999) | |||||

| HSMA Attributes | None | Lower HHA Closure Rate | Moderate Closure Rate | Higher Closure Rate | All HSMAs |

| No HHA Closures 1996-99 n=330 | HHA Closures as % of HHAs in 1996 (1-14.3%) n=73 | HHA Closures as % of HHAs in 1996 (14.3-30%) n=183 | HHA Closures as % of HHAs in 1996 (30+%) n=204 | n=790 | |

| Geographic Location Attributes | |||||

| Total population 1996 | 145,077 | 500,788 | 474,911 | 458,938 | 335,399 |

| Metropolitan Area Population as % of Total | |||||

| HSMA population | 21.3% | 62.7% | 55.3% | 43.7% | 38.8% |

| Census Division (% of HSMAs) | |||||

| New England | 2.4% | 2.7% | 4.9% | 2.5% | 3.0% |

| Middle Atlantic | 8.4% | 12.3% | 3.8% | 2.9% | 6.3% |

| East North Central | 9.0% | 26.0% | 20.2% | 13.2% | 14.3% |

| West North Central | 24.7% | 12.3% | 14.8% | 15.7% | 18.9% |

| South Atlantic | 17.5% | 16.4% | 17.5% | 9.3% | 15.3% |

| East South Central | 16.3% | 11.0% | 8.7%% | 5.9% | 11.4% |

| West South Central | 9.9% | 9.6% | 13.7% | 25.5% | 14.8% |

| Mountain | 7.2% | 5.5% | 9.3% | 14.7% | 9.5% |

| Pacific | 4.5% | 4.1% | 7.1% | 10.3% | 6.6% |

| TABLE 2.3: HSMA Market Area Attributes by Category of HHA Closure Rates (1996-1999) | |||||

| HSMA Attributes | No Closures | Lower Closure Rate | Moderate Closure Rate | Higher Closure Rate | All HSMAs |

| No HHA Closures 1996-99 n=330 | HHA Closures as % of HHAs in 1996 (1-14.3%) n=73 | HHA Closures as % of HHAs in 1996 (14.3-30%) n=183 | HHA Closures as % of HHAs in 1996 (30+%) n=204 | n=790 | |

| Medicare Program Participation | |||||

| Mean years of Medicare participation | 14.1 | 12.2 | 10.2 | 8.0 | 11.4 |

| HHAs less than 1 year | 6.7% | 10.8% | 17.4% | 21.5% | 13.4% |

| HHAs between 1-5 years | 14.0% | 21.4% | 22.8% | 30.5% | 21.0% |

| HHAs between 5-10 years | 13.0% | 13.9% | 11.1% | 10.7% | 12.0% |

| HHAs 10 years or more | 66.3% | 54.0% | 48.7% | 37.3% | 53.6% |

| Proprietary Status | |||||

| For-profit HHAs | 19.2% | 36.3% | 44.0% | 51.9% | 35.0% |

| Voluntary non-profit HHAs | 44.4% | 40.9% | 35.2% | 28.2% | 37.8% |

| Government HHAs | 36.5% | 22.8% | 20.9% | 19.9% | 27.3% |

| Organization Type | |||||

| Hospital-based HHAs | 49.8% | 32.8% | 35.8% | 29.7% | 39.8% |

| Freestanding HHAs | 48.6% | 64.2% | 61.8% | 68.3% | 58.2% |

| HSMA Market Characteristics | |||||

| Number of HHAs | 4.2 | 12.9 | 15.6 | 22.5 | 12.4 |

| Herfindal Index of Market Concentration | 0.51 | 0.21 | 0.23 | 0.28 | 0.36 |

| Medicare HHA Service Use | |||||

| Average annual Medicare users per HHA | 2,107 | 7,125 | 7,702 | 6,224 | 4,930 |

| Average annual visits per Medicare user | 60.2 | 62.2 | 65.5 | 77.0 | 65.9 |

| Annual HHA visits per resident beneficiary | 8.8 | 7.0 | 7.6 | 10.1 | 8.7 |

| LTC Supply Indicators | |||||

| HHAs per 10,000 resident beneficiaries | 3.5 | 2.8 | 3.6 | 6.3 | 4.2 |

| HHA RN FTEs per 1,000 resident beneficiaries | 3.53 | 3.14 | 3.44 | 4.10 | 3.62 |

| HHA aid FTEs per 1,000 resident beneficiaries | 3.96 | 3.43 | 3.60 | 5.18 | 4.15 |

| Medicare-certified nursing home beds per 1,000 beneficiaries 75+ years | 43.43 | 32.37 | 38.74 | 56.72 | 44.75 |

3. CHANGES IN MEDICARE HOME HEALTH AGENCY SUPPLY: 1996-1999

3.1. Introduction

Closure of many Medicare HHAs following implementation of the IPS mandated by the BBA of 1997 was a concern of policy makers, stakeholders, and advocacy groups. GAO (1999) found that over the 18 months that followed implementation of the IPS in October 1997, 760 HHAs closed, either voluntarily or involuntarily, and only 45 HHAs entered the market nationwide. OIG (2000) reported that the number of Medicare-certified HHAs decreased by 25% overall from 1997 to 1999.

Past studies of changes in the supply of Medicare HHAs after IPS implementation have employed data from the Medicare OSCAR system to analyze (GAO 1999; OIG 2000). OSCAR system data are helpful in identifying agencies that either no longer participate at all in the Medicare program or which have merged with another Medicare-certified HHA. However, they do not contain information on a less obvious way that HHA supply can be reduced, namely, by active HHAs shrinking their geographic service areas. That is, rather than discontinuing all service to Medicare beneficiaries, an agency may opt to only discontinue service in a portion of its geographic service area, for example, by the closure of one or more of its branches or subunits. In addition, because the provider surveys entered into OSCAR are conducted in up to18 month intervals, counts of certified agencies for any particular year may be inaccurate because of lags in reporting.

This chapter expands upon previous research addressing the question of how supply of Medicare HHAs changed after implementation of the IPS in two important ways. First, Medicare HHA claims activity is used together with Medicare certification status from the OSCAR system to determine the Medicare service activity status of HHAs. Second, changes in the supply of Medicare HHC is more broadly defined by considering not only agency closings, but also agencies that changed their geographic service areas following implementation of the IPS. Descriptive analyses provide some new insight about the magnitude of both of these sources of Medicare HHC supply change following implementation of the IPS. Multivariate analyses provide a deeper understanding of how HHAs responses to the IPS varied with respect to characteristics of agencies and the geographic markets they served.

3.2. Background

Beginning in the late 1980s, spending on Medicares home health benefit grew rapidly. Between 1988 and 1997, spending increased an average of 28.2% annually, from $1.9 billion to $17.8 billion (GAO 1999; HCFA 1998). This growth has been attributed primarily to a loosening of eligibility and coverage criteria in 1989 in response to a class action suit involving inconsistent interpretations of these criteria by Medicare fiscal intermediaries (Bishop, Kerwin & Wollack 1999; McCall, Komisar, Petersons & Moore 2001; GAO 1998), as well as some states Medicare maximization policies that took advantage of more liberal Medicare guidelines to cover some of the costs associated with LTC for beneficiaries eligible for both Medicare and Medicaid (GAO 1998). The BBA of 1997 required the HCFA (now CMS) to replace its cost-based reimbursement systems to PPS in many settings, including hospital outpatient departments, skilled nursing facilities, HHAs, inpatient rehabilitation facilities and LTC hospitals (Medicare Payment Advisory Commission 2000). The reimbursement changes of the BBA were intended to slow spending growth and provide incentives to providers in these settings to deliver care more efficiently. For HHAs, the BBA sought to impose limits on spending per beneficiary and per visit (National Health Policy Forum 1999).

Recognizing that the development of a PPS for HHAs would take considerable time, CMS created an IPS to affect a more immediate slowing of expenditure growth. CMS began phasing in the IPS as early as October 1997 depending upon an HHAs cost reporting year, with original expectations that the PPS would be fully implemented by October 1999 (later delayed until October 1, 2000). Under the IPS, HHAs continued to be reimbursed according to their costs, but these costs were subject to two cost limits in the aggregate: an area-specific per-visit ceiling that was more stringent than pre-IPS reimbursement, and an annual maximum HHA payment limit that considered the total number of beneficiaries served using an annual maximum per-beneficiary amount.

A dramatic contraction in Medicare home health expenditures was observed following implementation of the IPS. Whereas Medicare expenditures per home health fee-for-service user increased by an average annual rate of about 22% from 1992-1997, they decreased by an average annual rate of about -27% between fiscal years 1997 and 1999 (MedPAC 2000). According to McCall, Kosimar, Petersons & Moore (2001), total spending decreased over 50% (from around $16.4 billion to around $7.8 billion), total per-beneficiary spending decreased 50% (from around $500 to around $248), and annual per-user spending decreased 37% (from around $4,969 to around $3,110). Likewise, the total number of visits per-user decreased around 41%. Payments per-visit increased over this period by 7% (from around $63.00 to around $67.40).

In their 1998 report, the GAO described the impact of the IPS in terms of agency closures. In sum, GAO (1998) indicated that there were more HHAs in August 1998 than there were in October 1996, and that recent closures were dwarfed by longer-run industry growth. Since the implementation of the IPS in October 1997 through June 1998, 554 HHAs closed voluntarily nationwide, with an additional 206 closing involuntarily due primarily to a failure to meet minimum quality or financial standards. During the same period, only 45 HHAs entered the market nationwide. An OIG (2000) report indicated that the number of HHAs decreased by 25% overall from 1997 to 1999.

For the three years prior to the implementation of the IPS, an annual average of 285 HHAs closed voluntarily and 62 closed involuntarily (during the same three-year period, an average of 1,227 HHAs opened each year). Half of these closures were concentrated in four states; California, Louisiana, Oklahoma and Texas. Moreover, HHAs that closed voluntarily were more likely to be smaller (treating an average of 166 beneficiaries compared with 385 beneficiaries for HHAs that remained open) and provided more treatments per beneficiary (averaging over 90 visits per beneficiary compared to about 65 for HHAs that remained open). These factors may suggest that less efficient HHAs were less able to accommodate the changes to their reimbursement (GAO 1998), but much in the literature suggests that providers that focus on meeting the needs of more complex, higher cost beneficiaries are more likely to be negatively impacted by the reimbursement limits and blended rates of the IPS (GAO 1998; National Health Policy Forum 1999; Bishop, Kerwin & Wallack 1999).

An important distinction between agency closures and agency branch closures is made in the GAO (1998) report. Under Medicare rules, HHA branches are not considered independent providers. Rather, they are part and parcel of the parent agency. As such, branches do not receive unique provider certification, are not individually surveyed or certified for Medicare compliance, and are not required to file a unique Medicare cost report. In general, it was often financially advantageous for a branch to operate under a parent agency that had more attractive reimbursement as a result of their urban locale and higher wage index, while the branch provided services in an area with a lower wage index. This distinction was reiterated after reports from the home health industry about agency closures were substantially higher than those calculated by GAO.

3.3. Data and Methodology

A. Data Sources

Multiple data sources were employed in the study. Medicare HHC claims data for the calendar years 1996 and 1999 were used to determine the activity status of HHAs and to delineate their geographic service areas. The year 1996 is the latest full calendar year preceding implementation of the IPS on October 1, 1997. The year 1999 was the most recent full calendar year of claims data available at the start of the study. It precedes the implementation of the Medicare HHC PPS that occurred in October 2000. The Medicare POS files for 1996 and 1999, derived from the OSCAR system, contained information on Medicare certification status and several organizational attributes of agencies. Medicare Denominator File (MDF) data from 1996 were aggregated to produce measures of the total Medicare beneficiary population residing in geographic health service market areas.

Finally, county-level data from the 2000 ARF on hospitals and nursing homes were used to specify various indicators reflecting the supply of LTC services for the multivariate analysis.

B. Components of Medicare HHA Supply Changes

Although complete market exit and market entry by HHAs via changes in Medicare certification status clearly represent changes in Medicare HHA provider supply, these are not the only ways in which Medicare HHA supply changes can occur. While still retaining their Medicare certification, some HHAs may decrease Medicare HHA supply by contracting their geographic service area and visit volume, perhaps through the closure of branches or subunits. Other certified HHAs may increase Medicare HHA supply by adding staff to serve additional beneficiaries in an expanded geographic service area.

Medicare HHA supply changes, as reflected by increased or decreased visit capacity, can also occur in the absence of agency closures or any changes in HHAs' geographic service areas. However, there is an important fundamental geographic basis underlying policy concerns about the many HHA closures that followed implementation of the IPS. When Medicare HHA supply reductions occur via agency closure (or geographic service area contraction), the potential adverse impacts on beneficiary access are spatially concentrated in geographic areas where service is discontinued. Given the geographic basis of HHC service delivery, travel costs naturally limit the geographic extent of HHA service areas, which in turn, may limit the number of agencies able to expand service to affected areas. Potential access problems may be of particular concern in places where Medicare beneficiaries are served by a handful of HHAs. If the Medicare HHA supply reductions that followed the IPS resulted from proportional reductions in staffing and service capacity among all Medicare-certified HHAs, it is doubtful that there would be a similar level of policy concern about potential access problems.

In this study Medicare HHA supply changes are broadly defined to encompass not only market exits and entries, but also significant changes in agencies geographic service areas. When an HHA fully exits the Medicare home health market, the agency discontinues service to all Medicare beneficiaries in the service area it previously served. Similarly, when an HHA is a new market entrant, service is initiated to all Medicare beneficiaries in the new geographic service area where the agency willingly provides visits. Under this line of reasoning, HHAs which exhibit significant contractions or expansions of their geographic service areas can be viewed as partial market exits or partial market entries in the sense that service is discontinued to or added for some, but not all beneficiaries.

C. Requirements for Active Medicare Service

Measuring HHA supply changes in ways other than Medicare certification status requires consideration of what level of service to Medicare beneficiaries is necessary for an HHA to be actively serving Medicare beneficiaries. Although a reliable measure of Medicare certification would certainly seem to be a necessary condition for active Medicare service, it may not be sufficient for practical measurement of HHA supply changes. National Medicare HHA claims data for 1996 and 1999 reveal that a small but significant number of Medicare-certified HHAs actually serve very few Medicare beneficiaries annually. For example, 559 HHAs, amounting to 5.7% of the 9,806 HHAs with at least one Medicare visit claim in 1996, served ten or fewer different beneficiaries in 1996. The market behavior of HHAs serving so few patients is unlikely to have much practical significance for measuring HHA supply change. As part of the changes in Medicare participation rules made in 1997 designed to screen out problem providers, agencies were required to serve at least ten patients before seeking Medicare certification (GAO 1999). While these rules could be used as a basis for defining active Medicare service, there are practical difficulties in measuring geographic service area changes for HHAs serving so few users. As any assumed minimum beneficiary threshold will be arbitrary, active service to Medicare beneficiaries is conservatively defined in this study to be the provision of visits to more than 20 different beneficiaries annually. There were 958 HHAs, which accounted for 0.22% of total Medicare HHA visits in 1996, considered to be inactive in 1996 under this definition. Among these 958 HHAs, 208 of them were certified but also inactive in 1999, and 434 of them were no longer Medicare-certified in 1999. There were also 211 HHAs that obtained Medicare certification after 1996 but did not meet the minimum beneficiary service threshold in 1999. These latter 853 HHAs that did not actively serve Medicare beneficiaries in either 1996 and/or 1999 under the assumed threshold were excluded from the study, leaving 10,034 HHAs that met the active Medicare service requirement in 1996 and/or 1999.

D. Classification of Medicare HHA Supply Changes

A methodology was developed to classify HHAs that actively served Medicare beneficiaries in at least one of the years 1996 or 1999 into one of six mutually exclusive categories:

- HHA market exit: This category includes HHAs that actively served beneficiaries in 1996 with no Medicare claims in 1999.

- HHA service area contraction: This category includes: (1) HHAs that actively served beneficiaries in both 1996 and 1999 and contracted their geographic service area between 1996 and 1999, and (2) HHAs with Medicare claims in both 1996 and 1999 that actively served beneficiaries only in 1996.

- HHA service area expansion: This category includes: (1) HHAs that actively served beneficiaries in both 1996 and 1999 and expanded their geographic service area between 1996 and 1999, and (2) HHAs with Medicare claims in both 1996 and 1999 that actively served beneficiaries only in 1999.

- HHA service area change: This category includes HHAs that actively served beneficiaries in both 1996 and 1999 whose geographic service area changed between 1996 and 1996 due to both discontinued service in some areas and expansion of service to others.

- HHA service area stable: This category includes HHAs that actively served beneficiaries in both 1996 and 1999 whose geographic service area was relatively stable between 1996 and 1999.

- HHA new market entrant: This category includes HHAs that actively served beneficiaries in 1999 with no Medicare claims in 1996.

A summary of the methodology employed to classify HHA geographic service area changes as expanding, contracting, stable, or changed, is contained in the Appendix 3.A.

Table 3.1 contains information about the distribution of 10,034 HHAs that actively served Medicare beneficiaries in either 1996 or 1999 or both years among the six Medicare HHA supply change categories defined above. The relatively conservative criteria used to classify HHAs as expanding or contracting their service areas have produced a set of HHA classifications exhibiting a high degree of face validity. Among HHAs classified as contracting their service areas, about 36.3% of total beneficiaries served in 1996 lived in zip codes that were subsequently dropped from these HHAs geographic service areas. Only 3.2% of beneficiaries served in 1999 by HHAs in this group lived in zip codes that were newly served in 1999. A reciprocal pattern to this one is found for HHAs classified as expanding their geographic service areas. Whereas only 2.5% of beneficiaries served by these HHAs in 1996 lived in zip codes that were later dropped from an HHAs service area, 39.2% of beneficiaries served in 1999 lived in zip codes that were not previously served by these HHAs in 1996. Among HHAs classified as having stable geographic service areas, only 3.2% of beneficiaries served in 1996 and 4.1% of beneficiaries served in 1999 lived in zip codes that were dropped and added to these HHAs service areas between 1996 and 1999, respectively. A relatively small number of HHAs, accounting for only 3.7% of active HHAs in 1996, could not be classified as either expanding or contracting their service areas under the classification criteria employed. As expected, a relatively high percentage of beneficiaries served by these HHAs in 1996 and 1999, respectively, lived in zip codes that were dropped (18.5%) or added between 1996 and 1999.

Table 3.1 also contains information about distance traveled to beneficiaries served by HHAs in 1996 and 1999. Mean distance traveled to beneficiaries in their service areas among HHAs that contracted their service areas declined by about three miles between 1996 and 1999, presumably as a consequence of a tendency to discontinue service in more distant than closer zip codes.5 On the other hand, the mean distance traveled to beneficiaries in their service areas among HHAs that expanded their service areas increased by about 4.3 miles, presumably as a consequence of a tendency to add service in more distant than closer zip codes. In stark contrast to these two groups of HHAs, there was very little if any change in mean travel distance to beneficiaries in the service areas of HHAs with stable geographic service areas.

Table 3.1 shows similar differences among categories in the data on changes in staffing levels for RNs and certified nurse aides (CNAs). The decrease in mean RN and CNA staffing among HHAs with stable service areas reflects broader overall trends of supply contraction in the HHA industry following the IPS. Nevertheless, the data suggest that on average HHAs that were classified as contracting their service areas exhibited larger percentage decreases in staffing, particularly for RNs. The mean staffing level changes among HHAs classified as expanding their geographic service areas are sharply different from all other categories of HHAs. On average HHAs that expanded their service areas exhibited RN and CNA staffing levels in 1999 that were 83% and 23% higher than those in 1996, respectively. Overall these supporting data also suggest of a high degree of construct validity in the HHA response classifications.

E. Variable Specification

Multivariate analyses were performed to identify agency and market area attributes associated with the categorization of HHA supply changes described above. Table 3.2 contains a summary of definitions for all specified independent variables. Here we discuss the rationale for specification of these variables and their expected relationships with the outcome variable, or the likelihood that HHAs responded to the IPS through market exit, service area expansion, service area contraction, or a changed service area, relative to maintaining a stable geographic service area. Given our premise that the motivations for service area contraction and expansion are similar to the more extreme respective responses of market exit and entry, generally it is expected that most independent variables should have the same directional influence on these two outcomes. Weaker relationships are expected for service area contraction outcome relative to market exit, however. Expectations about the signs of variables with respect to the outcome of changed service areas are uncertain given the mixed nature of this form of supply response.

Agency Attributes. Dummy variables were specified for variables measuring the ownership status, organizational setting, and organizational structure of HHAs. GAO (1999) found that for-profit HHAs were disproportionately over-represented among market exits relative to government and voluntary non-profit agencies. In addition to a dummy variable distinguishing proprietary HHAs a separate dummy variable was specified for HHAs with government control. Voluntary non-profit control served as the reference class. Given the broader service missions that are likely to influence the behavior of non-profit agencies, for-profit HHAs are expected to be more likely than their voluntary non-profit counterparts to exit and to contract their service areas, and less likely to expand their service areas. As government HHAs may be less dependent on Medicare revenue than are voluntary non-profit agencies, government HHAs are expected to be less likely to exit and contract their service areas than non-profit HHAs.

Expectations about differences service area expansion among HHAs with different control status are uncertain. To the extent that many service area expansions reflect an agency responding to service demands of beneficiaries in places affected by closures and/or service area contractions, government HHAs may be less likely than voluntary non-profit agencies to fill those needs given their service missions. A dummy variable was specified to distinguish HHAs based in hospitals or nursing facilities from freestanding agencies. Such facility-based agencies should be less dependent on Medicare HHC revenues than freestanding agencies since they also receive patient revenue for institutional care. More modest market responses are expected for facility-based agencies (i.e., less likely to contract or expand their service areas, and to exit) than freestanding agencies.