The Affordable Care Act (ACA) provides two main avenues for expanding health coverage: the Health Insurance Marketplaces (“Marketplaces”) and the law’s federal support for states that wish to expand their Medicaid programs. This brief estimates how many individuals nationwide might have Marketplace coverage after the upcoming Open Enrollment period (November 1, 2015–January 31, 2016) through the end of 2016.[1]

Looking ahead to the third Open Enrollment period (OE3), analysts have produced a wide range of estimates of the number of people who will enroll in coverage through the Marketplaces that vary due to differing underlying assumptions and analytical methods. Last year, the Secretary of Health and Human Services projected that 9.1 million consumers would be enrolled through the Marketplaces for individual coverage at the end of 2015. We expect that figure to be the starting point for the third open enrollment period.

In preparation for OE3, the Department of Health and Human Services Office of the Assistant Secretary for Planning and Evaluation (ASPE) developed a projection for potential 2016 enrollment through the Marketplaces, taking into account both short-run and long-run factors that affect the level of enrollment. Given the range of factors that may affect enrollment, we provide ranges for enrollment and cross-validate our results using additional methods. The ASPE projection is the product of collaboration among individuals involved in research, operations, and consumer outreach for the Marketplaces. ASPE also gathered feedback on the projection models and results from a variety of outside experts.

ASPE’s Estimates of Marketplace Enrollment

ASPE’s projection uses a “bottom up” approach that builds a national estimate up from state-level information on previous enrollment periods and analysis of the broader insurance market. This method yielded an estimated range of 9.4 to 11.4 million effectuated enrollees in the Marketplace at the end of 2016. The range is based on assumptions about the effectuated enrollment at the end of 2015, the starting point for OE3, rates of re-enrollment, take-up by new enrollees, and attrition of those who initially select a plan but do not maintain coverage for the entire year.

Bottom Up Approach: Projection of Marketplace Enrollment in 2016

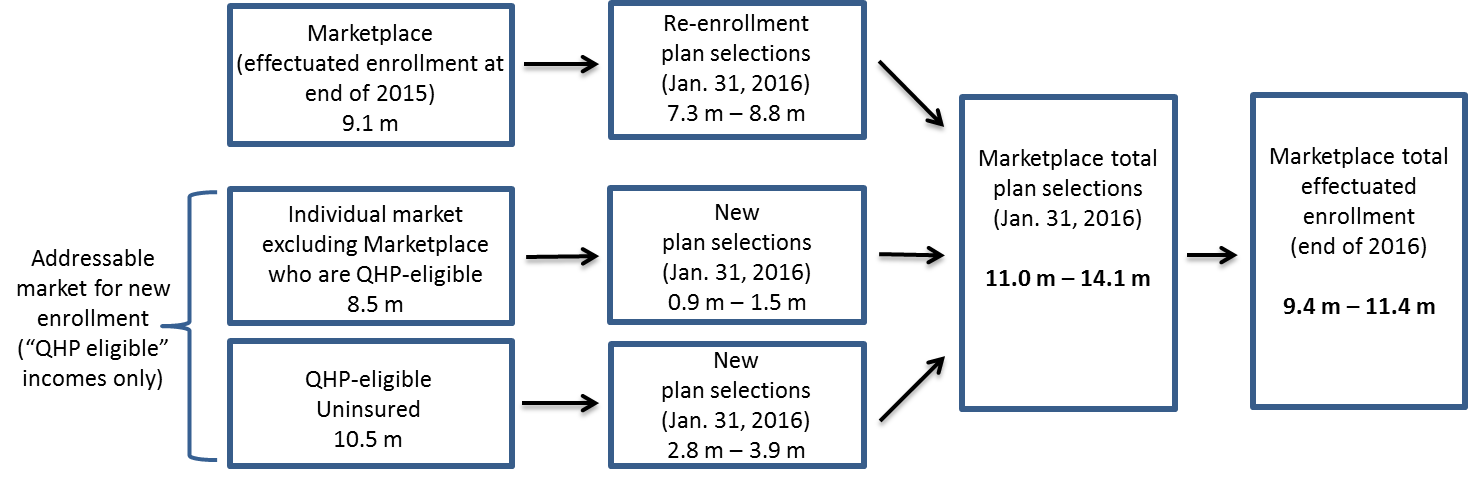

In generating its bottom up estimate for 2016 enrollment, ASPE analyzed the potential for re-enrollment and new enrollment in coverage through the Marketplaces. ASPE modeled 2016 enrollment as coming via three channels (FIGURE 1):

- Continued enrollment by 2015 Marketplace enrollees: The number of Marketplace policyholders with plan year 2015 coverage and the rate at which they will re-enroll;

- Shifts from off-Marketplace individual coverage into coverage through the Marketplaces: The number of individuals who currently hold “off-Marketplace” individual policies and who will have plan selections through the Marketplaces at the end of OE3; and

- Enrollment of the uninsured through the Marketplaces: The number of QHP-eligible uninsured who will have plan selections through the Marketplaces at the end of OE3.[2]

FIGURE 1

For the first element, continued enrollment by 2015 Marketplace enrollees, ASPE used data from the Centers for Medicare & Medicaid Services (CMS) on individuals currently enrolled in coverage through the Marketplaces and an analysis of re-enrollment rates from OE2 to project a range for OE3. As discussed above, we expect that 9.1 million individuals will be enrolled through Marketplaces for individual coverage at the end of 2015, but we also consider a range of starting points on which to base projections given uncertainty.

The latter two elements, shifts from off-Marketplace individual coverage and enrollment of the uninsured into coverage through the Marketplaces, comprise the inflows from the “addressable market” for new enrollment. The “addressable market” was defined as all individuals who are uninsured or have coverage through the individual market and who have family incomes at or above the level for eligibility for Marketplace insurance affordability programs (generally greater than 100% or 138% of the federal poverty level, depending on state Medicaid expansion status). To estimate the size of the uninsured portion of the addressable market, ASPE used data from the American Community Survey (ACS) and the Gallup-Healthways Well-Being Index, a daily poll of American adults. Information from the Kaiser Family Foundation and the National Health Interview Survey was used to estimate the size of the individual market.

We estimate that there are currently about 19 million people in the addressable market for new enrollment, consisting of 8.5 million people with off-Marketplace non-group coverage and 10.5 million who are uninsured. Based on the 2013 ACS, we calculated the number of QHP-eligible uninsured individuals prior to the first open enrollment period. Adjusting that estimate to reflect the reduction in uninsured rates between 2013 and Q2 2015 according to the Gallup-Healthways Well-Being Index suggests there are currently 10.5 million QHP-eligible uninsured. This number of eligible uninsured is smaller than in previous years, reflecting take-up of Marketplace coverage by eligible uninsured during the first two years of the Marketplaces’ operations, and, to a less extent an improving economy where more people have access to employer-sponsored insurance (ESI) through a job, as well as increased access to health coverage as states expand Medicaid and introduce new plan options such as the Basic Health Program in New York and Minnesota.

The projection for new enrollment depends on the likelihood that potential consumers from the addressable market will enroll in Marketplace coverage or the “take-up rate.” To predict take-up in the addressable market, ASPE stratified that population by family income into groups that were likely eligible for subsidies (financial assistance in the form of advance premium tax credits and cost sharing reductions) or had incomes too high to be eligible for financial assistance. State-level OE3 take-up rates are based on observed rates by these income groups in OE2, adjusted to account for increasing awareness of the Marketplaces, the increase in the individual shared responsibility penalty amount (and increasing awareness of the penalty), and the fact that some states have already achieved such large reductions in the uninsured population that any remaining uninsured people would likely be particularly difficult to reach. We vary these rates to account for uncertainty, which generates a range of estimates for plan selections through the Marketplaces in 2016. Our analyses suggest that between 0.9 and 1.5 million individuals with non-group coverage outside the Marketplaces and between 2.8 and 3.9 million eligible uninsured individuals will select plans through the Marketplaces.[3]

ASPE combined these population estimates and take-up rates for re-enrollment and new enrollment to estimate total Marketplace plan selections at the end of OE3. By the end of OE3, we expect 11.0 to 14.1 million individuals will have selected plans for 2016 coverage through the Marketplaces.

Effectuated (active) enrollment at the end of 2016 is expected to be lower than the number of OE3 plan selections. Based on the Marketplaces’ first two years, we expect a net decrease in Marketplace enrollment relative to the level at the end of open enrollment. The number of individuals joining through Special Enrollment Periods (SEP) throughout the year does not fully offset those who leave for other forms of coverage or due to factors such as non-payment or termination from coverage as a result of a data matching issue. We project that in 2016 the year-end effectuated enrollment will be 9.4 to 11.4 million.[4] ASPE’s analysis implies that most of the new Marketplace enrollment for 2016 is likely to come from the ranks of the uninsured, with more than three previously uninsured new enrollees for each one new enrollee who previously had off-Marketplace individual coverage.

Uncertainty

As a check on the “bottom up” approach, we used a “top down” approach of modifying existing forecasts based on data from the first two years of Marketplace experience to put our estimates into the context of other models used to forecast enrollment. Specifically, the top down approach builds off 2015 projections from the Congressional Budget Office (CBO) that the Marketplaces will enroll a total of 20 million people in 2016 and level off at 23 million starting in 2017.[5] We adjusted the CBO projections according to lessons learned over the past two years about enrollment through the Marketplaces and the most recent information available about trends in ESI coverage and in the individual market outside the Marketplaces. Specifically, we adjust CBO estimates downward based on employer surveys from Mercer and other industry sources, which suggest that shifts from ESI coverage and the off-Marketplace individual market into coverage through the Marketplaces will be smaller than CBO expected and that the remaining uninsured may be harder to reach than in previous years. When these adjustments are accounted for, projections of 2016 enrollment using the top-down method are consistent with ASPE’s bottom-up projections.

There is a high degree of uncertainty about any projection, especially in the early years of a program. The Marketplaces have been in place for only two years, and thus we have limited experience upon which to base projections. There are numerous factors that affect consumers’ insurance enrollment, including attitudes of consumers and employers, the effect of payments under the individual responsibility fee, the size of premiums and premium tax credits, the ease of the enrollment process, communication and outreach efforts, and whether and how insurance products change over time. As Marketplace coverage becomes more widespread and the size of the uninsured population eligible for enrollment in coverage through the Marketplaces shrinks, the remaining uninsured may be harder to reach, slowing enrollment growth. Beyond these factors, there are macroeconomic forces such as changes in population and economic conditions, which are difficult to predict but likely to affect enrollment. Thus, actual enrollment could vary significantly from projected levels.

The Bottom Line

Our bottom-up approach results in an estimated range of 9.4 to 11.4 million effectuated enrollees at the end of 2016. This range reflects the considerable degree of uncertainty in making such projections. The top of the estimated range is based on the combination of a higher take-up rate, higher reenrollment, and less attrition, while the bottom of the range reflects the combination of a lower take-up rate, less reenrollment, and more attrition. Marketplace enrollment is an essential component to achieving ACA’s mission to reduce the number of uninsured individuals in the U.S. Through Marketplace retention and new enrollment and increased Medicaid coverage, we will continue to work to provide every American with access to high-quality, affordable insurance.

[1] This brief considers only individual market Qualified Health Plan (QHP) enrollment through the Marketplaces and not enrollment through the Small Business Health Options Program (SHOP).

[2] Office of the Assistant Secretary for Planning and Evaluation. “Health Insurance Marketplace: Uninsured Populations Eligible to Enroll for 2016.” October 2015. Available at: http://aspe.hhs.gov/pdf-report/health-insurance-marketplace-uninsured-populations-eligible-enroll-2016.

[3] Going forward, it will be important to track take-up rates among eligible uninsured people. Take-up rates will change with time, as will the base population of remaining uninsured as more individuals enroll in Marketplace plans, and thus rates of overall growth in enrollment will necessarily decline.

[4] This range for year-end enrollment equates to 9.8 to 12 million for average monthly effectuated enrollment during 2016; our year-end estimate incorporates expectations about attrition over the year.

[5] Budgetary and Economic Effects of Repealing the Affordable Care Act. Accessed at: https://www.cbo.gov/publication/50252